2 dividend shares to consider in July to target a £1,200 passive income The dividend yields on these UK shares are among the largest to be found on either the FTSE 100 index or the FTSE 250 right now.

Posted by Royston Wild Published 29 June

SUPR UKW

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

Though the FTSE 100 and FTSE 250 remain on prolonged bull runs, many top UK shares continue to offer great value. The environment is especially attractive for investors seeking high-yield dividend shares to buy.

Here are just two great dividend stocks with sky-high dividend yields to consider:

Supermarket Income REIT (LSE:SUPR) 7.3% Greencoat UK Wind (LSE:UKW) 8.6%

Of course dividends are never guaranteed. But if broker forecasts prove accurate, a £15,000 lump sum spread equally across these companies will provide a near-£2k second income over the next 12 months alone (£1,193 to be exact).

I’m confident too that each of these dividend shares will steadily grow the passive income they deliver over time. Here’s why.

Supermarket Income REIT As a real estate investment trust (REIT), this business is set up to deliver a consistent stream of dividends to shareholders. At least nine-tenths of profits from their rental earnings must be paid out each year under sector rules.

Supermarket Income owns and lets 81 stores to the stable grocery industry’s big beasts like Tesco and Sainsbury. This ensures a steady flow of income that’s not vulnerable to changes in the economic cycle.

As you may expect, the business is mindful of the growth of online retail and the threat this poses to future property demand. According to Statista, online penetration rates for food and other groceries in the UK have more than doubled since 2016.

Consequently, the company’s investment strategy is focused on so-called omnichannel stores that “provide in-store shopping, but also operate as last mile, online grocery fulfilment centres for both home delivery and click and collect“. This helps to greatly reduce (if not totally eliminate) the threat of click-based shopping.

I’m more concerned about the impact of future inflation on the business. A subsequent pickup in interest rates could dent earnings and pull its share price sharply lower again. But I feel the potential rewards of owning the REIT’s shares outweigh this danger. Annual dividends have risen each year since it listed on the London stock market in 2017.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Greencoat UK Wind Renewable energy providers like Greencoat UK Wind, on the other hand, have a rapidly growing market to capitalise on. The climate’s especially favourable in the UK, with the current government putting Net Zero among its policy priorities.

For dividend investors, this fellow FTSE 250 REIT has other attractive qualities. Due to the stable nature of electricity demand, cash generation isn’t impacted by broader economic conditions like many other UK shares. What’s more, its revenues are essentially guaranteed by long-term contracts with energy suppliers.

This has resulted in annual dividend growth that, except for last year when payouts were frozen, goes back to when the company joined the London Stock Exchange in 2013.

That’s not to say Greencoat UK Wind isn’t without risk, of course. Like that other REIT I’ve described, profits are sensitive to interest rate changes. With just 49 wind farms on its books too, it doesn’t enjoy technological diversification that can protect earnings when the wind doesn’t blow.

That said, on balance, I think its other safe-haven qualities — allied with that 8%+ dividend yield — make it worth serious consideration today.

Remember, your portfolio should be different to the above, to reflect you risk profile and how many years you have to retirement. If your retirement date is in the distant future, you maybe willing take on more risk as you have time to repair any damage if you buy a clunker. GL

CC Japan Income & Growth Trust PLC ex-dividend date CT Private Equity Trust PLC ex-dividend date European Assets Trust PLC ex-dividend date F&C Investment Trust PLC ex-dividend date Franklin Global Trust PLC ex-dividend date ICG Enterprise Trust PLC ex-dividend date JPMorgan European Discovery Trust PLC ex-dividend date Murray International Trust PLC ex-dividend date Premier Miton Group PLC ex-dividend date Real Estate Credit Investments Ltd ex-dividend date Schroder Japan Trust PLC ex-dividend date Shires Income PLC ex-dividend date Warehouse REIT PLC ex-dividend date Workspace Group PLC ex-dividend date

12 popular dividend disasters you need to dump right now.

How you could bank tens of thousands of dollars in yearly dividend cash for every $500,000 invested, and …

3 incredible monthly payers dishing out dividends up to 10%.

Dear Reader,

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income today if you limit yourself to popular mainstream investments.

The 10-year Treasury pays around 4.3% as I write this. That’s not bad, historically speaking, but put your $500K in them and you’re only looking at $21,500, right around the poverty level for a two-person household. Yikes.

And dividend-paying stocks don’t yield nearly enough. For example, Vanguard’s popular Dividend Appreciation ETF (VIG) pays around 1.7%. Sad.

When investment income falls short, retirees are often forced to sell their investments to supplement their income.

Of course, the problem here is that when capital is sold, the payout stream takes an immediate hit – so that more capital must be sold next time, and so on.

Avoid the Share Selling “Death Spiral”

Some financial advisors (who are not retired themselves, by the way) say that you can safely withdraw and spend, say, 4% of your retirement portfolio every year. Or whatever percentage they manipulate their spreadsheet to say.

Problem is, in reality, every few years you’re faced with a chart that looks like this.

Apple’s Dividend Was Fine – Its Stock Wasn’t

As you can see, the dividend (orange line above) is fine — growing, even — but you’re selling at a 25% loss!

In other words, you’re forced to sell more shares to supplement your income when they’re depressed.

Remember the benefits of dollar-cost averaging that built your portfolio? You bought regularly, and were able to buy more shares when prices were low?

In this case, you’re forced to sell more shares when prices are low.

When shares rebound, you need an even bigger gain just to get back to your original value.

The Only Reliable Retirement Solution

Instead of ever selling your stocks, you should instead make sure you live on dividends alone so that you never have to touch your capital.

This is easier said than done, and obviously the more money you have, the better off you are. But with yields still pretty low, even rich folks are having a tough time living off of interest today.

And you can actually live better than they can off of a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield.

I’m talking about annual income of 8%, 9% or even 10%+ so that you’re banking $50,000 (and potentially more) each year for every $500,000 you invest.

You and I both know an income stream like that is a very nice head start to a well-funded retirement.

And it’s totally scalable: Got more? Great!

We’ll keep building up your income stream, right along with your additional capital.

And you’ll never have to touch your nest egg capital – which means you won’t have to worry about or running out of money in retirement, or even the day-to-day ups and downs of the stock market.

The only thing you need to concern yourself with is the security of your dividends.

As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement.

Problem is, they don’t know how to find 8%, and 10% yields to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cash flow to pay the dividends into the future?

And how sensitive are these payouts to the latest headline, Fed policy changes or unrest on the other side of the globe?

We’ll talk specific stocks, funds and yields in a moment.

But first, a bit about myself.

I graduated cum laude with an industrial engineering degree — which is actually pretty popular with Wall Street recruiters.

But I couldn’t stand the thought of grinding it out in a cubicle for 80 hours a week. So I moved to San Francisco and got into the tech scene.

A buddy and I started up two software companies that serve more than 26,000 business users.

The result was a nice chunk of change coming in … and I had to decide what to do with my money.

I had seen plenty of young “techies” come into sudden cash and burn through their windfall in a year, ending up right back where they started.

That was NOT going to be me. I already had dreams of living off my wealth one day, decades before I retired.

I got plenty of cold calls from brokers wanting to “help” me. But I knew that nobody would care as much about my money as me.

So I went out on my own and invested my startup profits in dividend-paying stocks.

I’ve been hunting down safe, stable and generous yields ever since, growing my wealth with vehicles paying me 8%, 9%, even 10%+ dividends.

Over the past 10+ years, I’ve been writing about the methods I use to generate these high levels of income.

Today I serve as chief investment strategist for Contrarian Income Report — a publication that uncovers secure, high-yielding investments for thousands of investors.

Since inception, my subscribers have enjoyed dividends 5 times (and much more!) the S&P 500 average, plus big annualized gains!

And that brings me to a crucial piece of advice…

The ONE Thing You Must Remember

If I could leave you with just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are.

Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $87,560 by 2023, or 87x your money.

But the same $1,000 in the non-dividend payers would have grown to just $8,430 — 90% less.

That’s why I’m a dividend fan.

The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up!

There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives us dividend investors such an edge.

When you lock in an 8%+ yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

So let’s wipe the false promises of mainstream finance from our minds and start thinking the “No Withdrawal” way…

Step 1: Forget “Buy and Hope” Investing

Most half-million-dollar stashes are piled into “America’s ticker” SPY.

The SPDR S&P 500 ETF (SPY) is the most popular symbol in the land. For many 401(K)’s, this is all there is.

And that’s sad for two reasons.

First, SPY yields just 1.2%. That’s $6,000 per year on $500K invested… poverty level stuff.

Second, consider 2022 for a moment (and only a moment, I promise!).

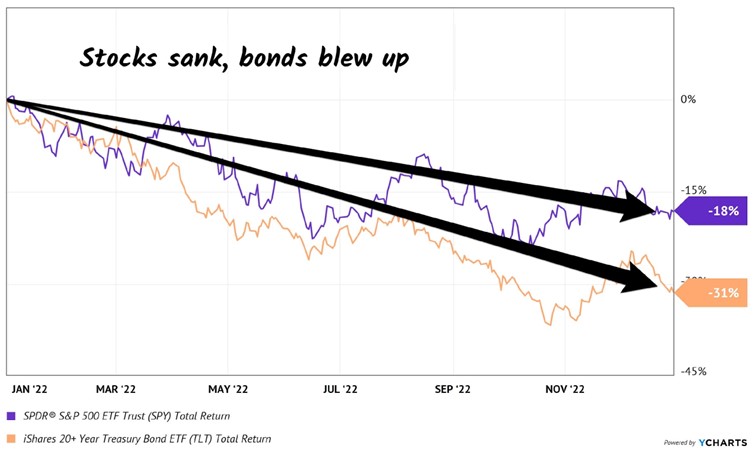

SPY was down nearly 20% that year. That is no bueno, because that $500K would have been reduced to $400K.

The last thing we want to do is lose the money we’re getting in dividends (or more) to losses in the share price. Which is why we must protect our capital at all costs.

Step 2: Ditch 60/40, Too

The 60/40 portfolio has been exposed as senseless.

Retirees were sold a bill of goods when promised that a 60% slice of stocks and 40% of bonds would somehow be a “safe mix” that would not drop together.

Oops.

Inflation — plus an aggressive Federal Reserve, plus a (thus far) persistently steady economy — drop-kicked equities and fixed income before they went on a serious bull run in 2023 and 2024.

It just goes to show that bonds are not the haven guaranteed by the 60/40 high priests. They could easily plunge just as hard (or harder) than stocks in the next economic crisis.

Just like they did in 2022 (sorry, we’re only going to spend one more second on that disaster of a year). US Treasuries plunged, which resulted in the iShares 20+ Year Treasury Bond ETF (TLT) getting tagged.

Sure, it still paid its dividend. But even including payouts, the fund was down 31% — worse than the S&P 500. Ouch!

When stocks and bonds are dicey, where do we turn? To a better bet.

A strategy to retire on dividends alone that leaves that beautiful pile of cash untouched.

Step 3: Create a “No Withdrawal” Portfolio

My colleague Tom Jacobs and I literally wrote the book on a dividend-powered retirement.

In How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact, we outline our “no withdrawal” approach to retirement:

Save a bunch of money. (“Check.”)

Buy safe dividend stocks with big yields

Enjoy the income while keeping the original principal intact.

To make that nest egg last, and our working life worthwhile, we really need yields in the 7% to 10% range. We typically don’t see these stocks touted on Bloomberg or CNBC, but they are around.

Of course, there are plenty of landmines in the high-yield space. Some of these stocks are cheap for a reason. Which is why we need to be contrarian when looking for income.

We must identify why a yield is incorrectly allowed to be so high. (In other words, we need to figure out why the stock is priced so cheaply!)

As I write, the top 10 payers in my Contrarian Income Report portfolio yield about 10.6% on average.

On every million dollars invested, this dividend collection is spinning off an incredible $106,000 every single year!

And you don’t have to be a millionaire to take advantage of this strategy.

A $750k nest egg will generate $79,500 annually…

$500K could hand you $53,000…

You get the idea.

The important thing is that these yields are safe, which creates stability for the stock (and fund) prices attached to them.

We want our income, with our principal intact.

It’s really the only way to retire comfortably, without having to stare at stock tickers all day, every day.

Now, many blue-chip yields are safe. They just need to hit the gym and bulk up a bit. Here’s how we take perfectly good, yet modest, dividends and make them into braggarts.

Step 4: Supersize Those Yields

Mastercard (MA) is a near-perfect dividend stock. Its payout is always climbing, having nearly doubled over the last five years. (MA shareholders, you can thank every business that accepts Mastercard for your “pennies on every dollar” rake.)

Tap, tap, tap. Remember cash? Me neither. Another 2020 casualty, with Mastercard making a few dimes or dollars on every plastic transaction.

The cashless trend has been in motion for years. But international growth prospects remain huge. Just a few years ago, 80%+ of transactions in Spain, Italy and even tech-savvy Japan were in cash.

We expect more dividend hikes as more cash turns to plastic. Or skips plastic entirely and goes straight to e-transfers. Mastercard and close cousin Visa (V) nab a nice piece of that action, too.

The only chink in MA’s armor? Everyone knows it is a dynamic dividend stock. So it only yields 0.5%. Investors keep bidding it higher, knowing that the next dividend raise is just around the corner.

So, the compounding of those hikes makes MA a great stock for our kids and grandkids. You and I, however, don’t have the time to wait for 0.5% to grow. And $2,500 on a $500K investment simply won’t get it done.

Let’s instead consider top-notch closed-end fund (CEF) Gabelli Dividend & Income Trust (GDV), managed by legendary value investor Mario Gabelli.

Mastercard is one of Gabelli’s largest holdings. But we income investors would prefer GDV because it boasts a healthy dividend right around 6.8%, paid monthly, nearly 14 times what Mastercard pays (and this is low in CEF-land; other funds, like the next one we’ll talk about, pay nearly double that).

And today, thanks to the conservative folks who buy CEFs, we have a rare opportunity to buy Mario’s portfolio for just 87 cents on the dollar.

Yup, GDV trades at a 13% discount to its net asset value, or NAV. It’s a way to boost MA’s payout and snag a discount, too.

Where does this discount come from?

CEFs are like their mutual fund cousins, with one exception: they have fixed pools of shares, so they can (and do) trade higher and lower than their NAVs, or “fair” values (the value of their holdings minus any debt).

As contrarians, we can step in when they are temporarily out of favor, like after a pullback, when liquidity is low, and buy them at generous discounts.

GDV holds more blue-chip dividend payers alongside MA, such as American Express (AXP), Microsoft (MSFT) and JPMorgan Chase & Co. (JPM). And with GDV, we have an opportunity to purchase them at a 13% discount.

These high-quality stocks wouldn’t normally qualify for our “retire on $500K” portfolio because everyone in the world knows they are strong long-term investments.

Even though these companies are constantly raising their dividends, constant demand for their shares keeps their prices high (and current yields low). So they never meet our current-yield requirement.

GDV does. The fund pays a monthly dividend that adds up to a nice 6.8% annual yield.

Let me give you one more idea (and this is where that much larger payout comes in): the Eaton Vance Tax-Managed Global Diversified Equity (EXG) is another CEF with a similar blue-chip dividend portfolio.

But EXG generates even more income than GDV by selling covered calls on the shares it owns.

More cash flow means a bigger dividend — and EXG pays an already terrific 9.4%!

So we buy and hold EXG and GDV forever, collecting their monthly dividends merrily along the way? Not quite.

In bull markets, these funds are great. But in bear markets, they’ll chew you up.

Step 5: Protect That Principal!

My CIR readers will fondly recall the 15 months we held GDV and EXG together, collecting monthly dividends plus price gains that added up to 43% total returns.

What was happening in that period, from October 2020 until February 2022? The Federal Reserve was printing money like crazy. Not only did the Fed stoke inflation, but we also enjoyed an asset-price lift.

Starting in 2022, we had the opposite situation. The stock market was topping, and we didn’t want to fight the Fed. We sold high, and by late 2022, both funds were down sharply:

We Sold EXG and GDV Just Before They Plunged

For whatever reason, “market timing” is a taboo phrase among long-term investors. That’s a shame because it is quite important.

By aligning our dividends with the market backdrop, we can protect our principal from bear markets.

Step 6: Start Here to Retire on $500K

So if the “tried and true” money advice — like the 60/40 portfolio and the 4% rule — has been properly exposed as broken…

Where do we go from here?

Well, imagine your portfolio in just a few days or weeks from now spinning off 8%, 9% and even double-digit dividends with the reliability of a Swiss watch… with many of my recommendations paying every single month no less!

No more worrying how much is coming in next month.

No more worrying about the Fed’s next move.

No more worrying about outliving your nest egg.

Let me tell you more about my solution — what I call the 10% “No-Withdrawal Portfolio.”

Better yet, I want to give you the names of my favorite stocks and funds to buy right now…

Yields Up to 10%, With Upside

To make it easy to transition into this new way of investing… where you are buying “bird in the hand” cash flows… instead of stocks that you just hope will go up… I’ve prepared two in-depth guides that hone in on the strategies I mentioned above…

Special Report #1:

Monthly Dividend Superstars: Yields Up to 10%, With Double-Digit Upside

This is where you’ll find the bargains that investors are leaving on the table in their misplaced fear of the Fed.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs:

A well-hedged 10% payer in one of the most in-demand sectors right now,

The brainchild of one of the top fund managers on the planet, throwing off an amazing 8.6% yield,

And a rock-steady 7.1% dividend whose managers have guided it to an astonishing 1,700% total return since inception.

Special Report #2:

The Perfect Income Portfolio

In this guide, you’ll get all the details of what I call the “Perfect Income Portfolio.”

Step-by-step, I’ll show you exactly how to set up your portfolio for maximum income without taking on additional unnecessary risk.

And, if you follow the simple steps laid out, I’m confident you’ll be able to enjoy an income stream that far exceeds what most folks who buy the typical S&P 500 stock earn.

This report includes investments that have passed my strict due-diligence process—including one of the best ways I’ve ever seen to invest in utilities (which I’ve picked for strong gains as interest rates move lower starting later in 2025).

This fund pays a whopping 7.6% today, holds some of the strongest electrical utilities in the country and trades at a bargain valuation. Its bargain status won’t last as lower rates pull more investors toward its rich payout!

I’ll walk you through each recommendation, giving you a clear, concise and easy-to-understand breakdown of exactly why I see these as “perfect” income plays.

How to Get Both Reports Absolutely Free

To access both reports, Monthly Dividend Superstars and The Perfect Income Portfolio, at no cost whatsoever, I simply ask that you take a risk-free trial of my research service, Contrarian Income Report.

I created Contrarian Income Report to help investors uncover overlooked and underappreciated income plays before Wall Street and the mainstream herd bid them up.

People often ask me, “I get the income part, but where does ‘contrarian’ fit in?”

My answer is simple: You’ll never beat the market by following the herd.

If you buy the same investments as everyone else, you’re going to have the same results as other people — which are always mediocre. This is why my advisory is defiantly contrarian.

It all boils down to one simple principle: If you want to make money, really big money, do what nobody else is doing.

Contrarian investing is probably the simplest, sanest, most powerful and reliable money-making technique ever devised to buy low and sell high. It works in any market, from stocks and bonds to gold and real estate — because human nature is the same everywhere.

You don’t need special training. All you need is an independent mind, a bit of patience and an ounce of courage.

If you want to buy low and sell high, you must force yourself to buy when everybody, including yourself, is feeling discouraged — when the news is bad. That’s likely to be the bottom. And you should sell when everybody is excited and the news is good, because that’s likely to be the top.

Right now, we’re holding a diverse collection of these high-yielding stocks and funds, and you’ll get instant access to each one the moment your no-risk trial starts.

And every new investment you get in Contrarian Income Report comes with a simple goal: it will pay a reliable 5% dividend — or better.

In fact, some holdings in our portfolio go way further than that, delivering 12%+ income right now.

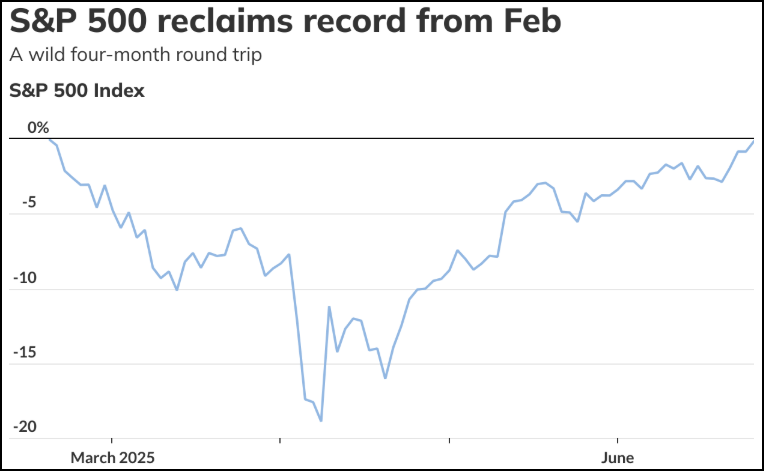

The S&P 500 has staged a remarkable rebound from near bear market lows in April to a new record Friday.

Two Fed governors have called for an early rate cut due to encouraging inflation data. Fed Chair Jerome Powell has advocated for a wait-and-see approach.

The current market enthusiasm faces multiple risks, including upcoming tariff deadlines and Q2 earnings, which may reveal tariff impacts that could reignite market turbulence.

Given the potential for renewed volatility, investors should consider a barbell approach, pairing growth assets with stable dividend-paying stocks.

Using the Seeking Alpha Stock Screener, I’ve identified five “Strong Buy” stocks with solid Quant factor and dividend grades, averaging a FWD yield greater than 4%.

Phimprapha Kitaiamphaisan

A New High for the S&P 500

Market activity in early summer has been a tug of war between optimism and uncertainty. In May 2025, markets staged an impressive comeback following the April sell-off. The S&P 500 posted its strongest monthly gain since late 2023, driven by strong tech earnings, easing trade tensions, and improving inflation data. However, volatility soon followed.

The S&P 500 experienced consecutive losses (June 18 and 20) as escalating conflict between Israel and Iran drove oil prices to their highest point since January. The market has since recovered in the wake of a ceasefire, and the S&P 500 reached a new high after being on the cusp of a bear market just two months ago.

MarketWatch

Key factors driving the rebound include President Donald Trump reaching a trade truce with China and resilient economic data. However, the rapid turnaround has also perplexed many investors, given the number of catalysts for volatility on the horizon.

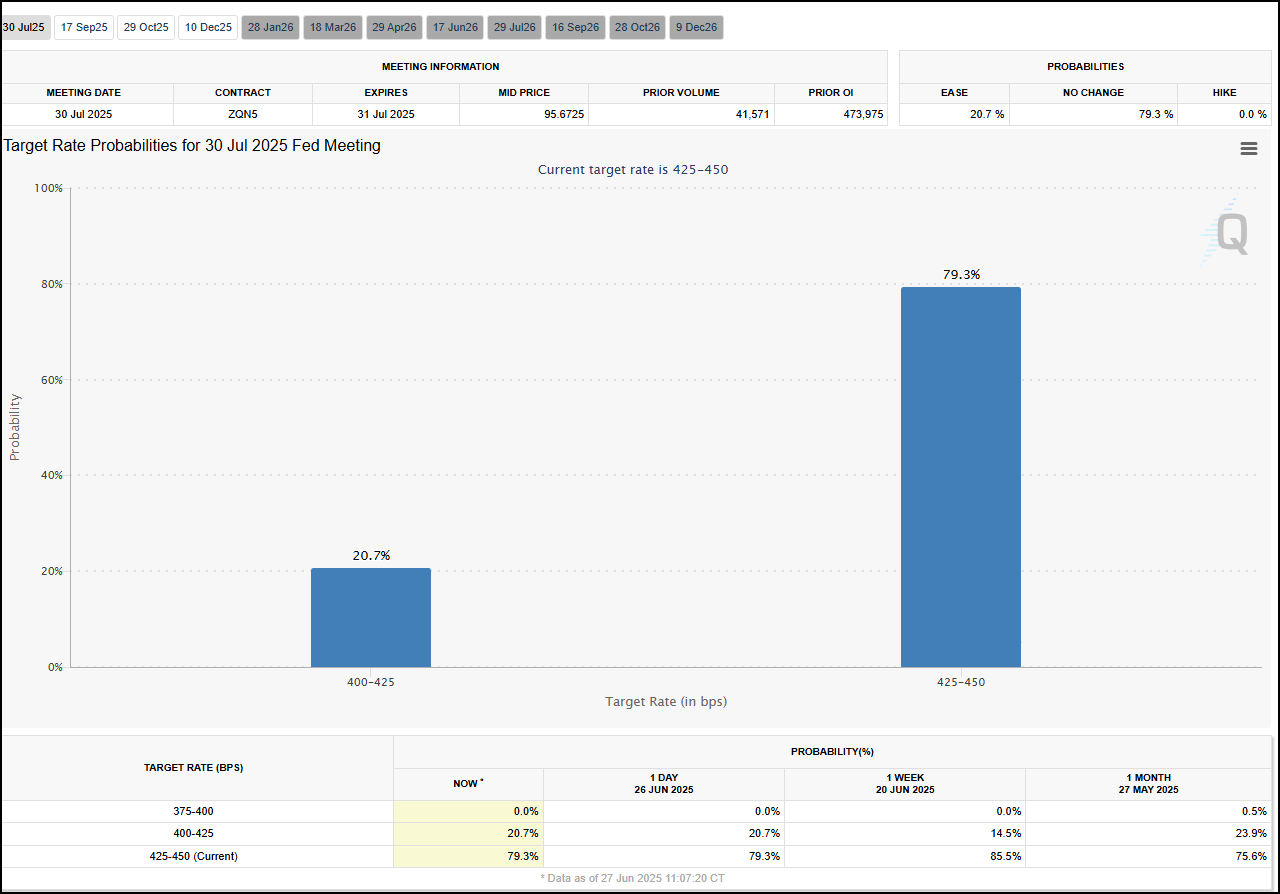

Rate Cut Speculation

Another push-pull factor for equity markets has been chatter around rate cut expectations. Both Federal Reserve Governors Michelle Bowman and Christopher Waller suggested that the Fed could consider cutting rates as soon as July. Bowman and Waller cited encouraging inflation data, the minimal impact of tariffs, and growing concerns about potential weakness in the labor market as justification for the cut. However, earlier this week, Fed Chair Jerome Powell countered that the central bank still needs more time to assess the impact of new tariffs on inflation before considering any rate reductions.

At the start of the year, the Fed was expected to deliver two 25 bps cuts in 2025, with a potential third cut based on economic conditions. Yet, no rate cuts have taken place year-to-date. The July FOMC decision will likely depend heavily on labor market data, which could trigger volatility in the interim if it surprises to the negative.

Mortgage Rates Fall on Fed Debate

Mortgage rates in the U.S. have recently experienced a slight decline, with the average 30-year fixed-rate mortgage now hovering around 6.8%. All eyes will be focused on the Fed at the end of July to see where the trend is heading. Lower mortgage rates could be a welcome reprieve for the softening real estate market, which has seen inventories rise to a three-year-high.

… And What about Tariffs?

Tariffs and their impact on corporate earnings remain a huge question mark in the second half 2025. Reciprocal tariffs, the same levies that caused the market to plunge more than 10% in two days in early April, are scheduled to be revisited on July 8 when the 90-day pause is set to expire. Unless further modified, higher rates for countries identified in the original announcement will automatically resume, which will likely have ramifications for the market. This will also coincide with the start of Q2 earnings season, where the impacts of existing tariffs will likely show up in earnings announcements. Both of these factors will be huge determinants of whether the market recovery can sustain itself.

Time to Stack your Barbell

What do all these disparate market narratives mean for investors? While the market is displaying relative optimism, several events on the horizon could reignite the market volatility, and investors need to be prepared. I started advocating for the barbell approach when market turbulence first surfaced back in February. Investors can get ahead of potential volatility by complementing their growth assets with lower-risk, income-generating assets. High-quality dividend stocks offer reliable income and portfolio stability when uncertainty persists. Dividend stocks can provide the potential for capital appreciation and hedging against inflation through their payouts.

Top 5 Dividend Powerhouses with Yields Over 4%

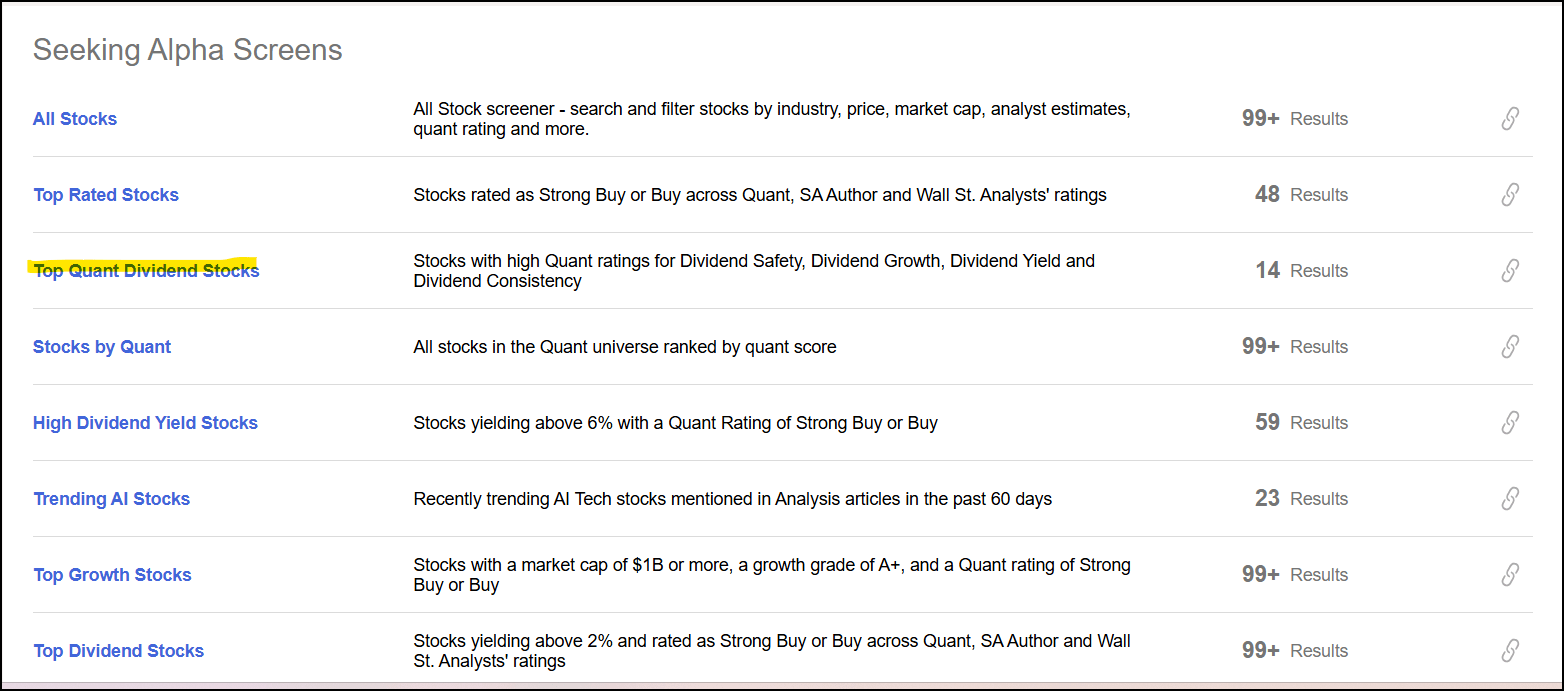

SA Quant has explored its universe of top dividend stocks and selected five options for investors based on their exceptional Quant factor and dividend grades. Typically, yields are less of a consideration for me as I prioritize dividend safety and growth. However, leveraging Seeking Alpha’s stock screener, I realized I could achieve a nice balance of solid dividend and factor grades with a minimum FWD yield of 4%.

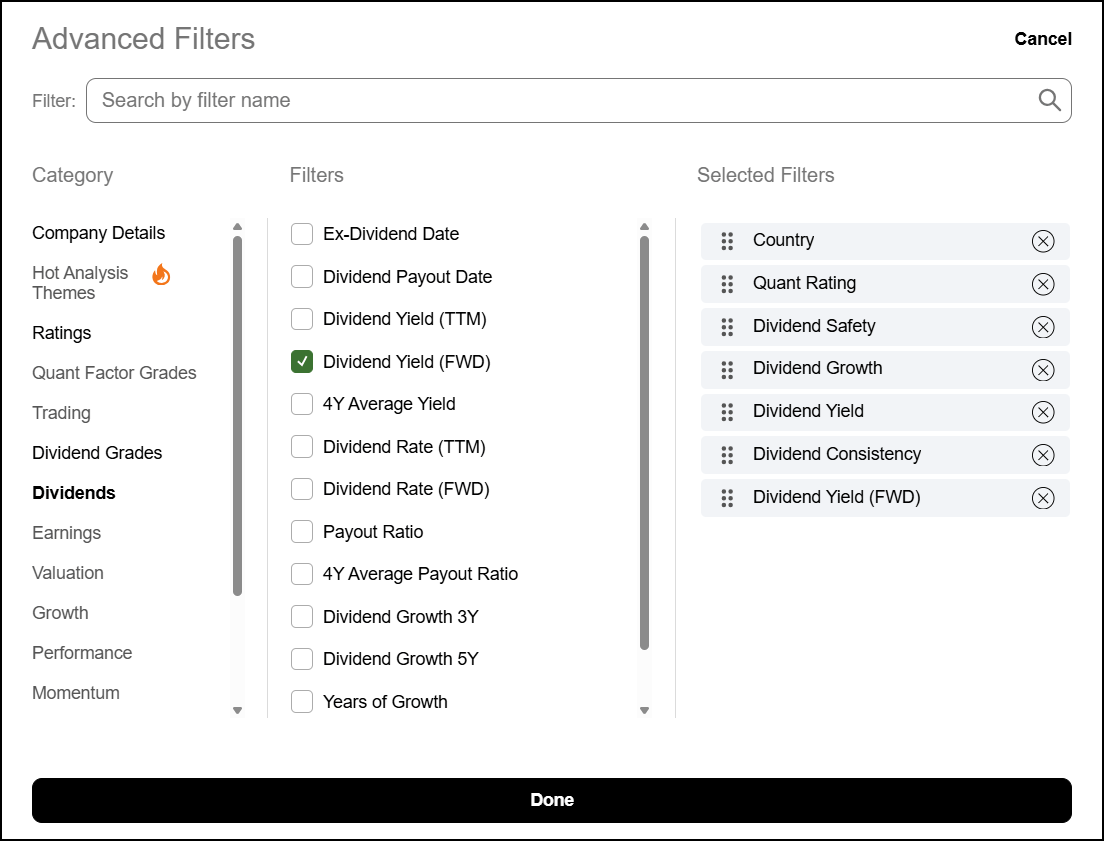

To find these securities, I selected “Top Quant Dividend Stocks” from the pre-existing Seeking Alpha Screens.

SA Premium

This initially yielded 14 stocks—Quant Strong Buys with excellent dividend grades. To broaden my scope and ensure sector diversification, I adjusted the dividend grades to allow for stocks with lower dividend consistency grades. Dividend consistency grades can sometimes penalize a company that has not been paying dividends for a long time, which I wanted to exclude for this article.

SA Premium

Finally, I added ‘FWD Yield’ as a field from the ‘Advanced Filters’ button. This allows me to screen for specific yield thresholds. For this article, I chose a minimum of 4%.

SA Premium

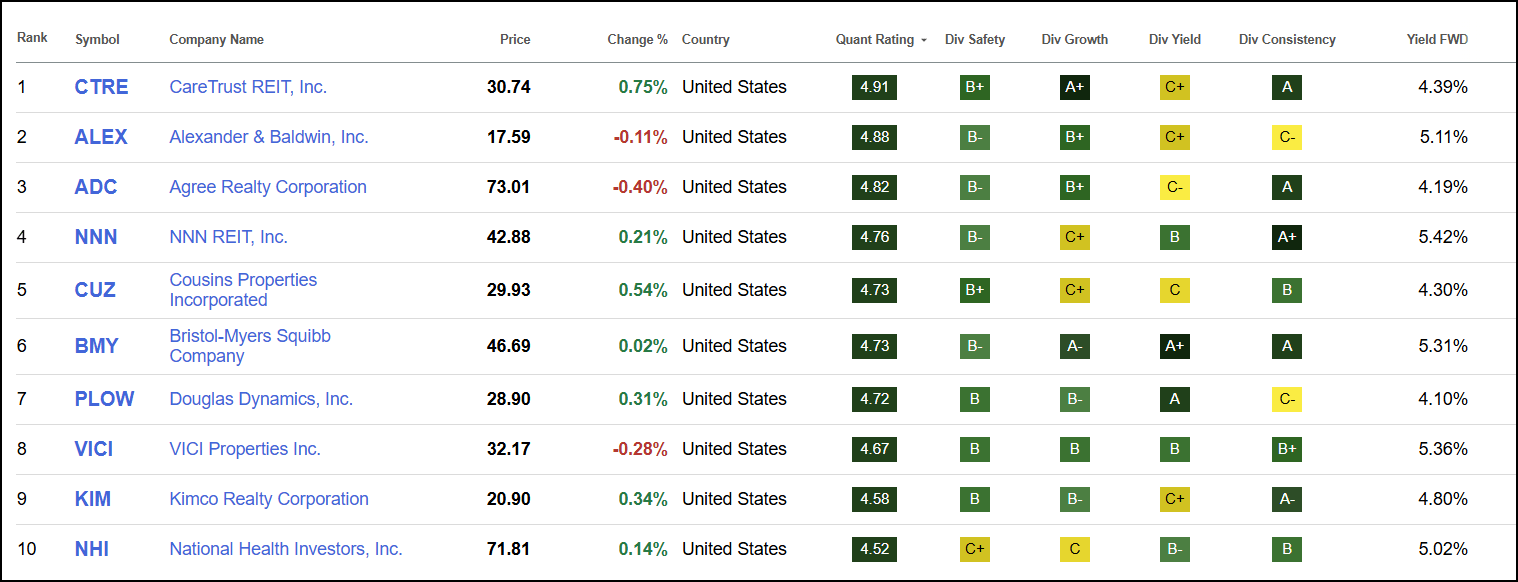

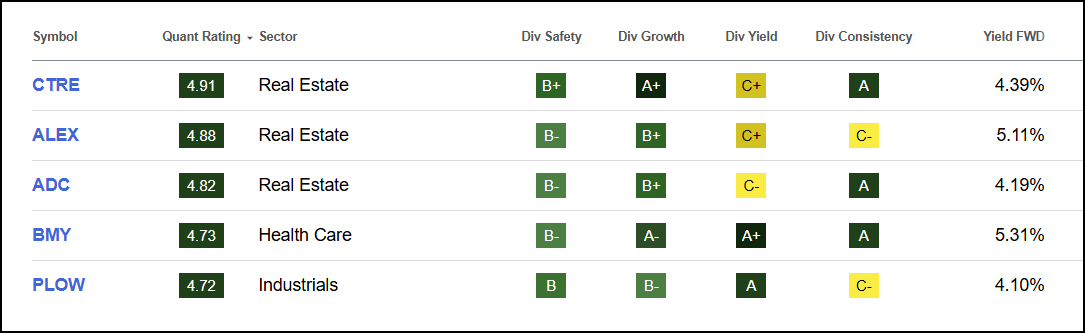

This yielded a selection of 10 stocks. I chose the first three as well as six and seven to diversify beyond the REIT sector.

SA Premium

This basket of five stocks has an average dividend yield of 4.62%, well above the 1.16% for the S&P 500 and 1.85% for Vanguard Dividend Appreciation Index Fund ETF Shares (VIG).

Top 5 Dividend Stocks Have an Average FWD Yield of 4.62% vs. the S&P 500’s 1.16%

SA Premium

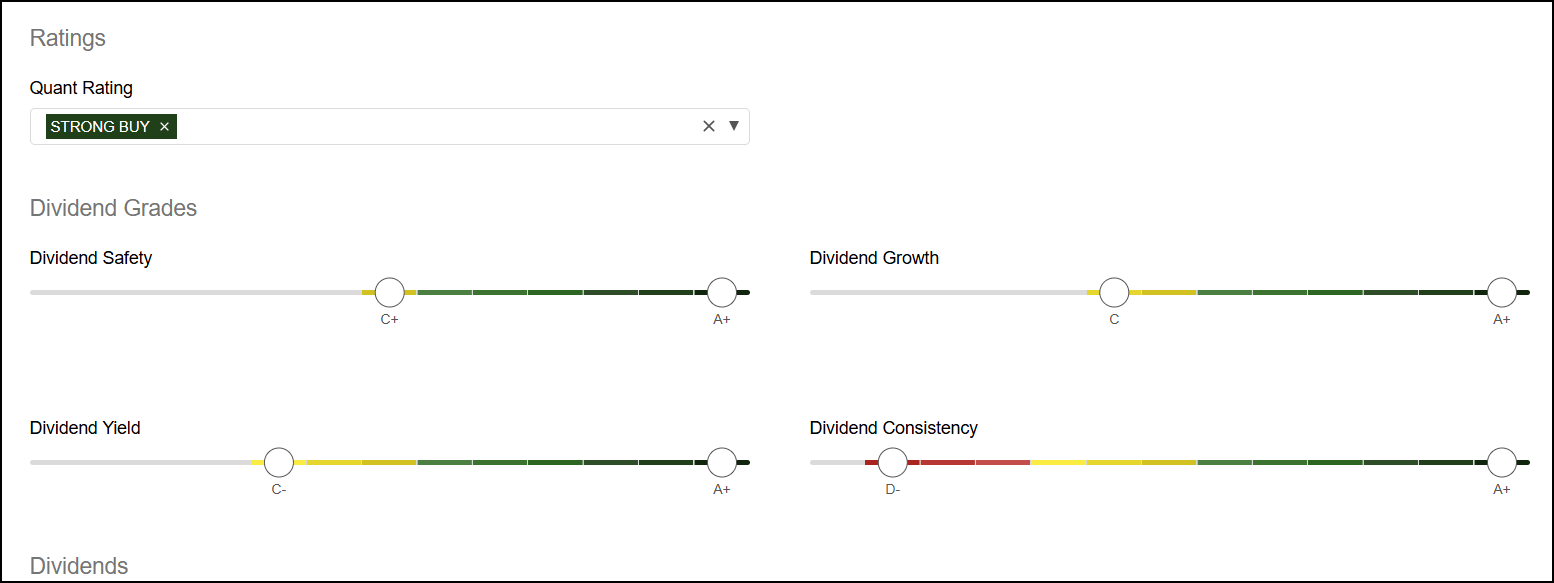

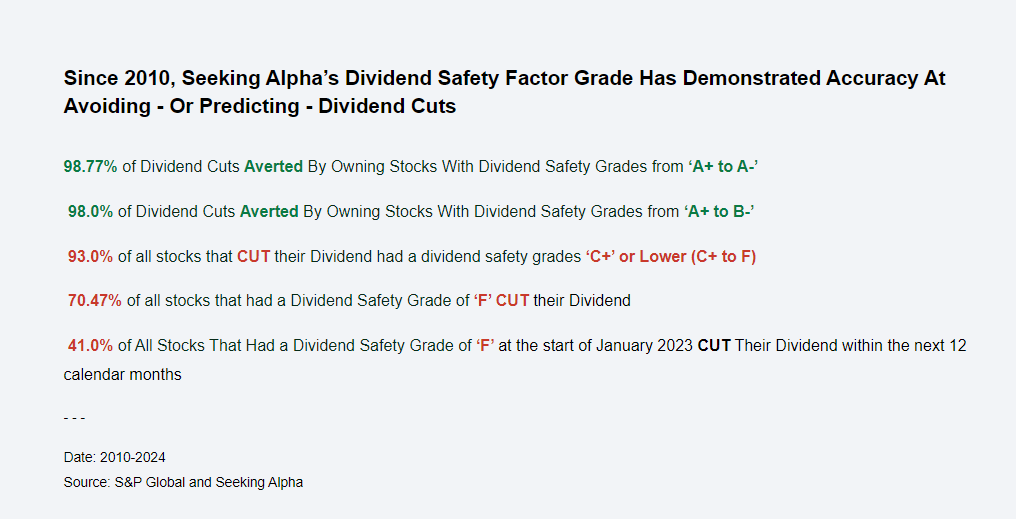

As I mentioned, these stocks were evaluated along multiple dividend grades, including safety and growth. The dividend safety grade leverages a sophisticated data-driven approach to offer a reliable assessment of a company’s ability to keep paying its dividends and avoid dividend cuts.

Dividend Cuts Can Be Avoided With Strong Dividend Safety Grades

SA Premium

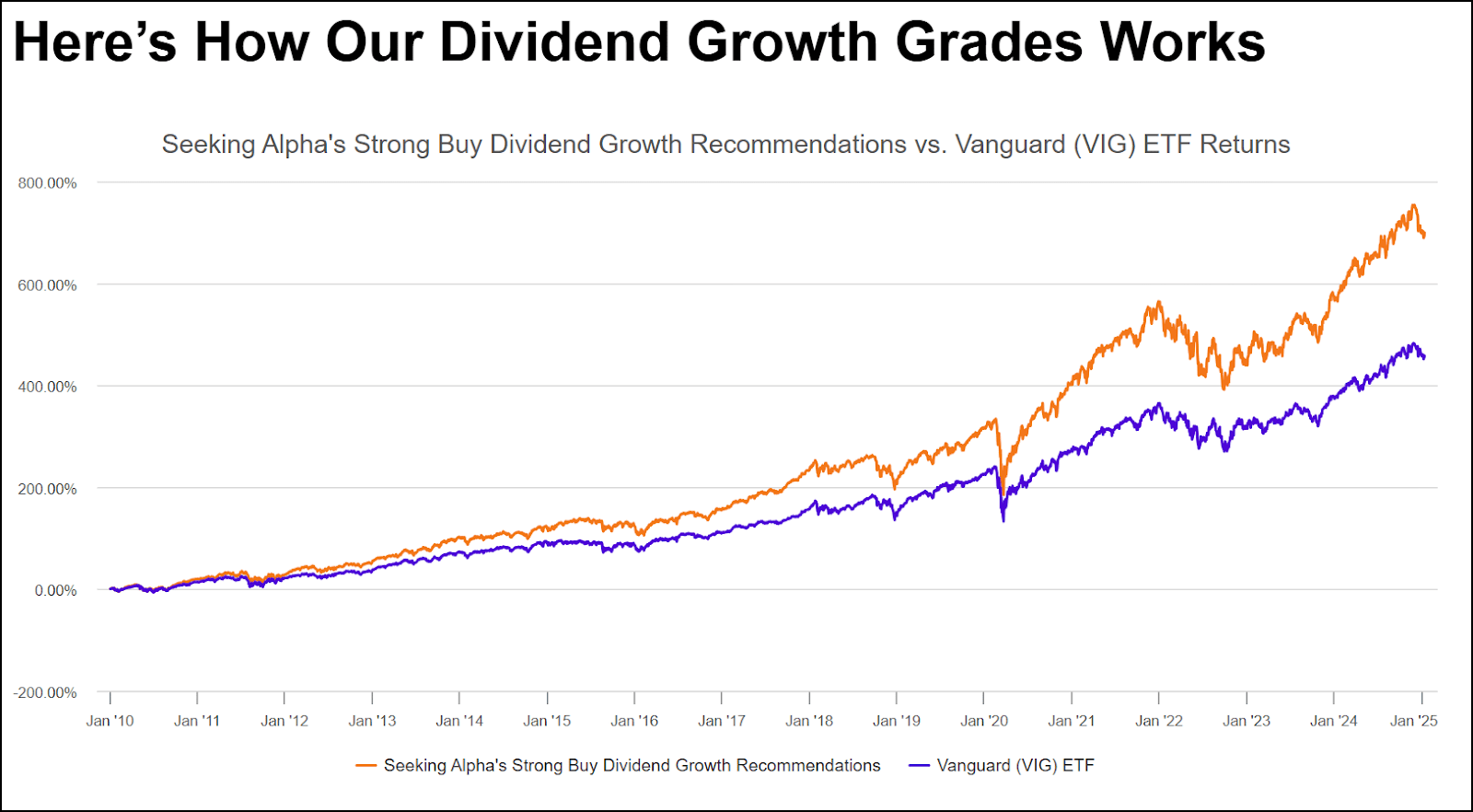

Similarly, the dividend growth grade provides an instant characterization of a company’s ability to grow its dividends based on data-driven analysis. This tool is valuable for income-focused investors who want to pinpoint companies with better dividend growth potential.

SA Premium

Note that because these stocks were holistically evaluated across factor and dividend grades, they do not represent the highest-yielding dividend stocks. Instead, they’re a combination of dividend yield, safety, and growth, in addition to high factor grades and a Quant “Strong Buy” recommendation.

Quant Sector Ranking (as of 6/27/25): 3 out of 175

Quant Industry Ranking (as of 6/27/25): 1 out of 17

Quant Rating: Strong Buy

FWD Yield: 4.38%

CTRE continues to rank as the No. 1 Quant-ranked Healthcare REIT and has climbed to the No. 3 REIT overall since I published my Stay In May: Top 5 Dividend Stocks article. Since I last covered CTRE, the company closed on its $817M acquisition of Care REIT in the United Kingdom, which is slated to boost its growth and add geographic diversification benefits. Management is so optimistic about the acquisition’s potential that CTRE raised its guidance to a normalized FFO per share of $1.75-$1.78 from $1.68-$1.72.

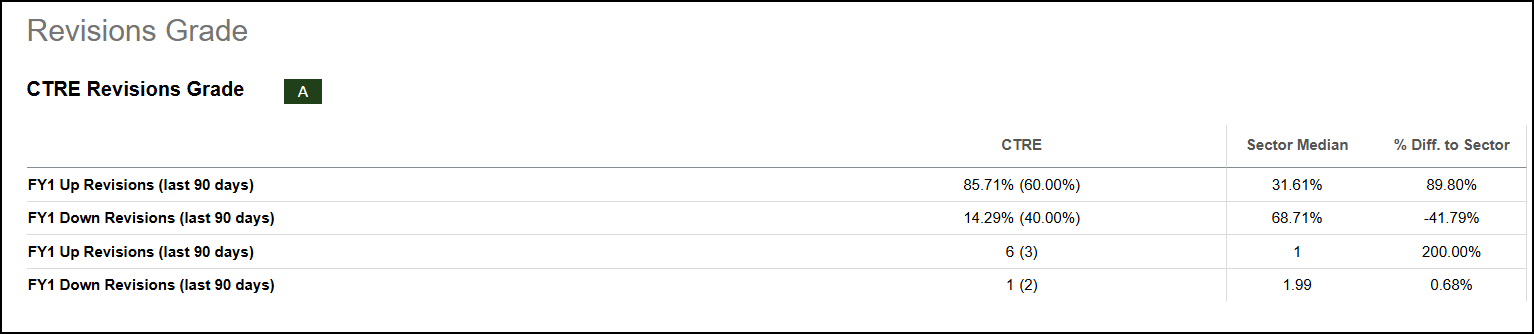

In addition to management, analysts are also optimistic about the company’s earnings. CTRE’s EPS revision grade has improved from ‘B+’ to an ‘A’ with six FY1 up revisions versus one downward revision.

CTRE Revisions Grade

SA Premium

The company shows excellent growth and dividend growth prospects, notching ‘A+’ grades for both categories. Key highlights include a forward FFO growth rate that is 395% above the REIT sector and a Dividend Growth Rate 10Y (CAGR) of nearly 16%. CTRE’s impressive growth figures, coupled with solid profitability and dividend safety, present investors with an attractive balance of stability and potential.

Quant Sector Ranking (as of 6/27/25): 4 out of 175

Quant Industry Ranking (as of 6/27/25): 1 out of 13

Quant Rating: Strong Buy

FWD Yield: 5.04%

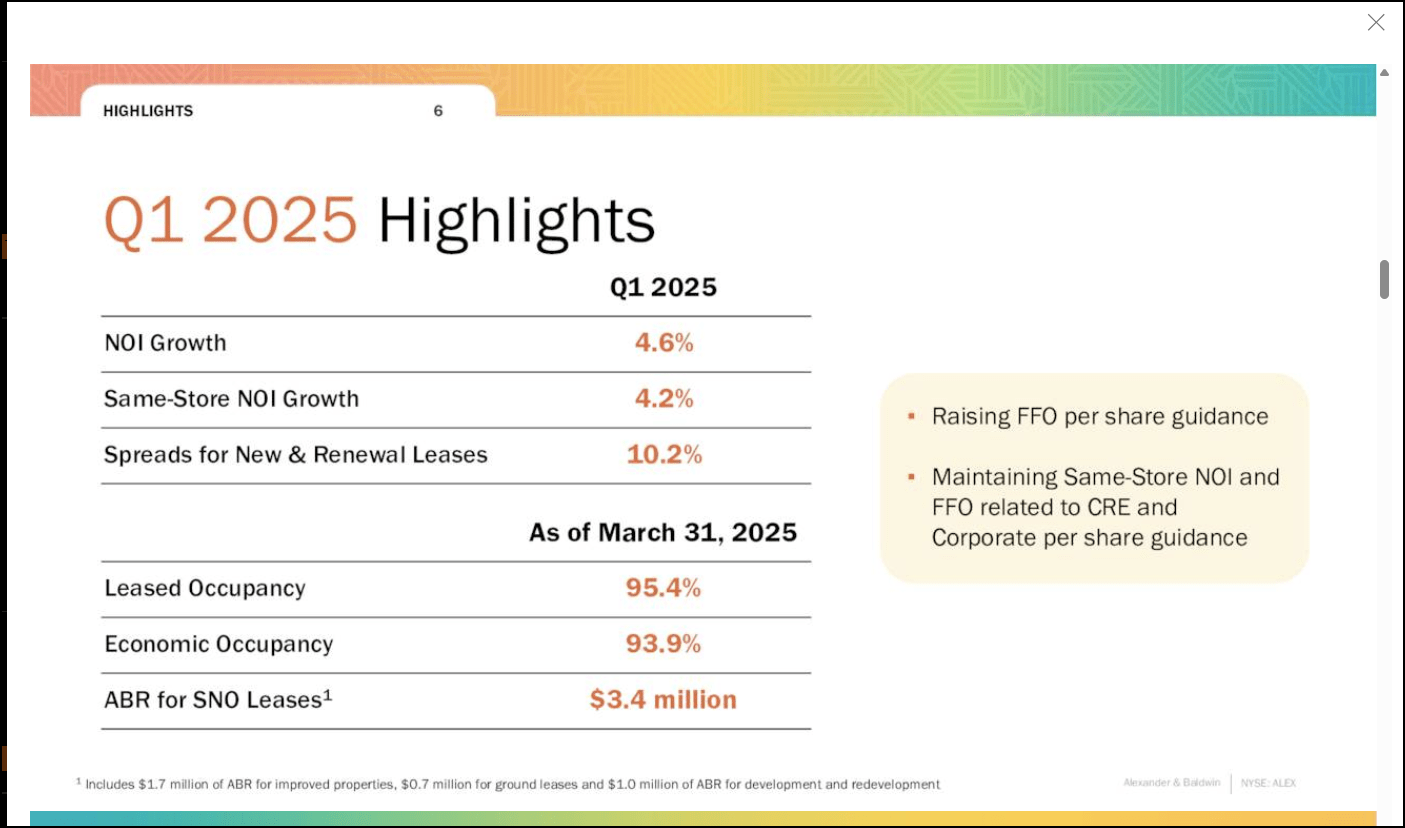

Operating over four million square feet of commercial space, Alexander & Baldwin, Inc. is the No. 1 Quant-ranked Diversified REIT. ALEX is focused on developing and managing commercial, retail, industrial, and office properties in Hawaii. ALEX employs a capital efficient strategy centered on maximizing value from existing land assets through redevelopment projects, expansion of Komohana Industrial Park. In Q1 2025, the company delivered robust results, reporting same-store net operating income up 4.2% while maintaining lease occupancy above 9.

ALEX sports an overall ‘B’ growth grade, a FWD AFFO growth of 276% above the REIT sector. The company also delivers solid profitability, highlighted by its FFO interest coverage ratio of 4.8x. ALEX’s dividend profile is excellent, yielding over 5% with a track record of growing its dividend over the last three years. Investors looking for a unique exposure to the Hawaiian real estate market, with a safe and impressive dividend, should consider ALEX.

Quant Sector Ranking (as of 6/27/25): 6 out of 175

Quant Industry Ranking (as of 6/27/25): 1 out of 23

Quant Rating: Strong Buy

FWD Yield: 4.21%

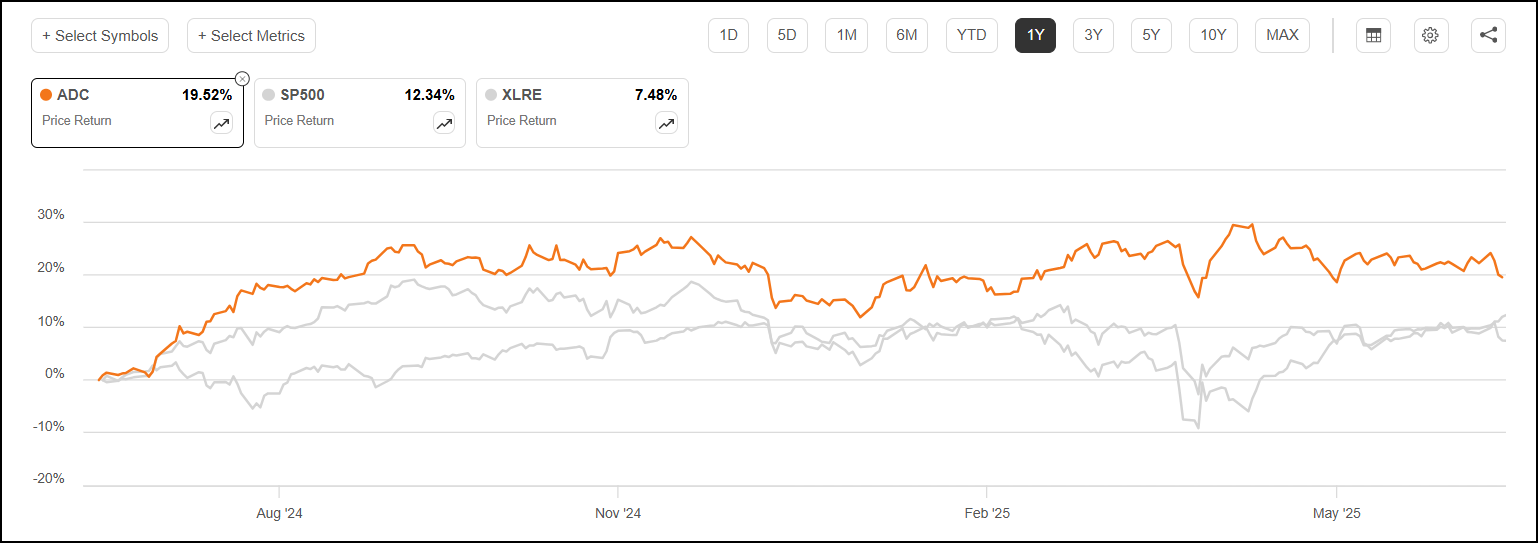

ADC is the top Quant-ranked retail REIT, specializing in essential retail, with a portfolio of tenants including grocery stores, discount retailers, auto parts suppliers, and convenience stores. Operating in 50 states and across 2,400 properties, ADC has strongly outperformed the real estate sector over the past year, returning nearly 20% vs. The Real Estate Select Sector SPDR Fund ETF’s (XLRE) 7.48%.

ADC vs. XLRE Trailing 1Y Return

Seeking Alpha

Despite a volatile macro environment, the company achieved its largest investment volume in Q1 since 2023, with more than $375M invested across 69 platforms with a strategic focus on recession-resistant retailers.

“We launched the acquisition platform in 2010 with a focus on recession-resistant retailers that have adapted to a comprehensive omni-channel strategy. Although we have yet to experience a traditional recession since its inception, our portfolio has proven to be pandemic-proof and we remain confident it will be tariff-resistant,” said Joey Agree, President and CEO of ADC

ADC offers impressive growth, with highlights including an AFFO growth (5Y Hist. CAGR) of more than 168% above the REIT sector, which is supported by exceptional profitability. ADC sports a TTM AFFO margin that’s 92% above the REITs sector, while offering an interest coverage ratio of 2.7x. The REIT’s lower leverage earned it a spot on SA analyst David Johnson‘s list of best REIT stocks earlier in June. This strong profitability contributes to ADC’s attractive dividend safety grade that complements the company’s 4.21% FWD yield. The company also boasts a ‘B+’ dividend growth grade in addition to its rock-solid yield. ADC’s strong profitability and specialty in recession-resistant retailers make it a strong pick in a shifting macro environment.

Quant Sector Ranking (as of 6/27/25): 18 out of 988

Quant Industry Ranking (as of 6/27/25): 7 out of 176

Quant Rating: Strong Buy

FWD Yield: 5.32%

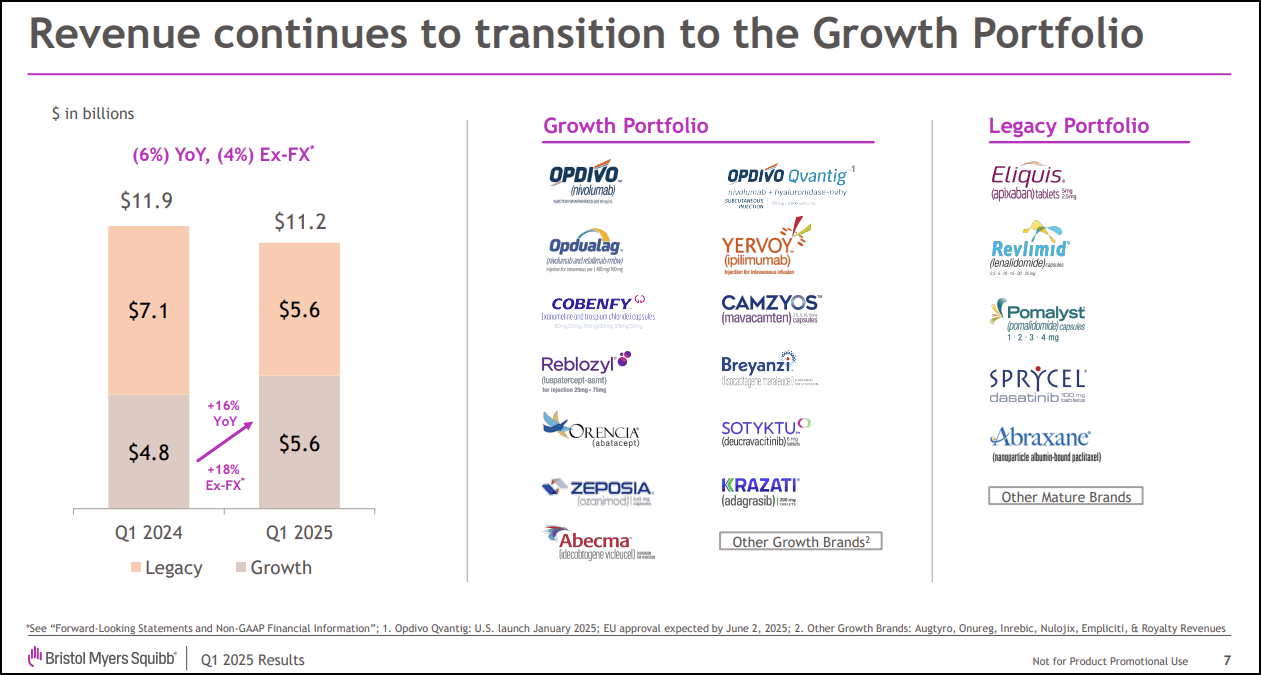

Bristol-Myers Squibb is a global biopharmaceutical company specializing in oncology, immunology treatments, operating through both innovative growth products and established legacy drugs. The company delivered exceptional Q1 2025 performance with $11.2 billion in revenue, driven primarily by 18% growth in its newer drug portfolio.

BMY raised its full-year revenue guidance to $45.8-46.8 billion and increased EPS projections, reflecting the company’s successful transition toward a diversified portfolio of innovative treatments. BMY’s growth trajectory is evident in its ‘A+’ growth grade, particularly in its impressive 60% EPS FWD Long-Term Growth (3-5Y CAGR), which is more than 450% above the health care sector.

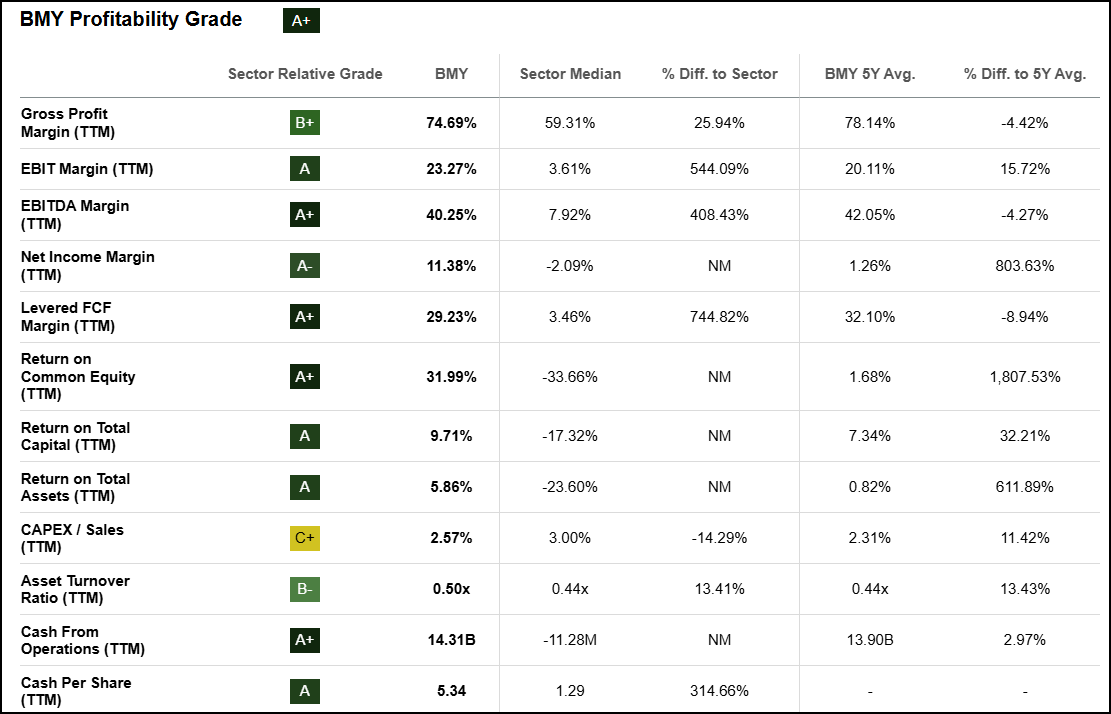

BMY also impresses in terms of profitability. The company boasts a 40% EBITDA margin vs. the sector’s 8%, offering $14B in cash from operations.

BMY Profitability Grade

SA Premium

Bristol rounds out its impeccable fundamental grades with an ‘A+’ valuation grade. The company is trading at a steep discount across key metrics like its FWD PEG, which is more than 90% reduced compared to the healthcare sector. The company’s fundamental strength is dovetailed by its eye-popping 5.32% FWD yield and ‘A-’ dividend growth suggest both BMY’s share price and dividend have further room to run.

Industry: Construction Machinery & Heavy Transportation Equipment

Quant Sector Ranking (as of 6/27/25): 33 out of 614

Quant Industry Ranking (as of6/27/25): 2 out of 31

Quant Rating: Strong Buy

FWD Yield: 4.03%

Douglas Dynamics leads North America in manufacturing and installing commercial work truck attachments and equipment, with a specialty focus on snow and ice control systems for trucks and municipal fleets. PLOW serves dealers, fleets, and municipalities across its Work Truck Attachment and Work Truck Solutions segments.

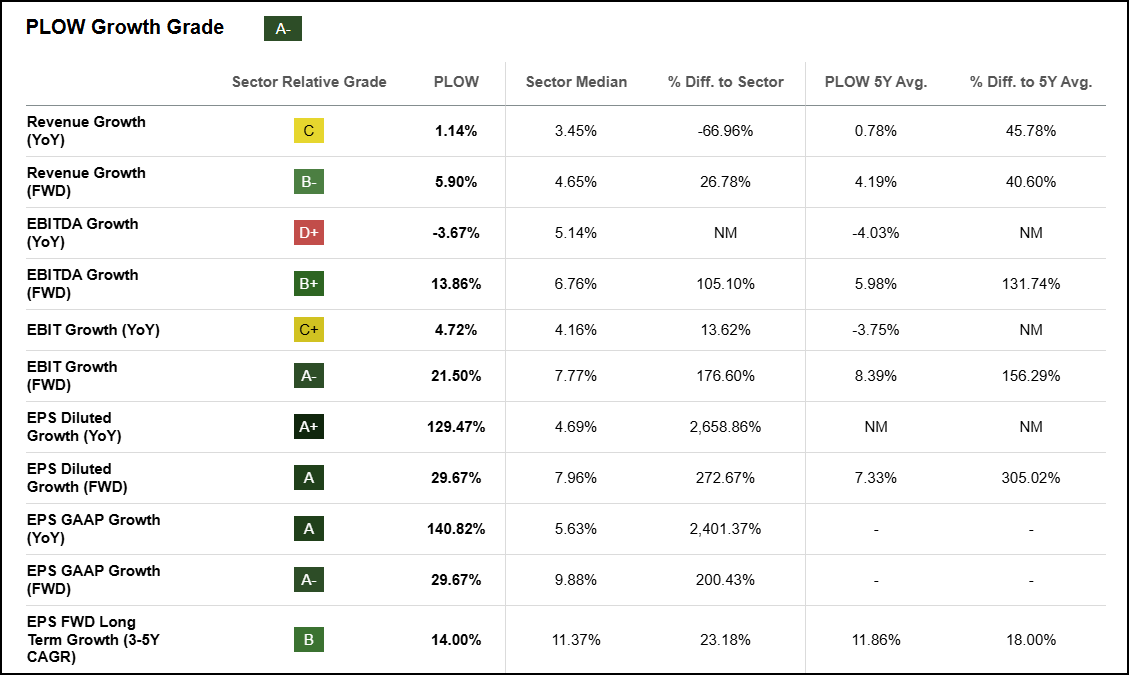

Net sales climbed over 20% in Q1 2025, with gross margins expanding to 24.5%. Strong winter weather drove a 50% increase in the Work Truck solutions segment. This impressive quarter is reflected in the company’s solid growth grade, with a FWD EBITDA growth over 100% above the sector median.

PLOW Growth Grade

SA Premium

The company also displays strong profitability, with a 27% ROE vs. 12% for the sector and a net income margin of 11%. Its earnings track record is strong, beating consensus estimates for the past five consecutive quarters. Analysts have shown unanimous confidence in the company’s earnings potential, with three FY1 up revisions vs. zero downward revisions. PLOW’s current 4.03% FWD yield is head and shoulders above the industrials sector’s median, and is supported by compelling dividend safety metrics, including a dividend yield to dividend payout ratio that’s 24% above the sector median. Investors looking for a high-yielding industrial with excellent fundamentals should consider PLOW.

Conclusion

The S&P 500 has staged a remarkable comeback from near bear market territory in April to hover just below record highs, driven by strong tech earnings, easing trade tensions, and improving inflation data. However, multiple risks loom with reciprocal tariffs slated to resume and the start of Q2 earnings season, where tariff impacts may become visible in corporate results. A barbell investment approach, which combines growth assets with high-quality dividend stocks for income and stability, is one way for investors to prepare for possible turbulence. SA’s Quant Team used its Dividend Grading System to identify five dividend stocks with yields above 4%, strong quant ratings, and excellent dividend growth and safety grades.

The stocks featured here can help complement a diverse portfolio. Alternatively, consider exploring Alpha Picks if you’re seeking a limited number of Seeking Alpha Quant’s best monthly ideas from the hundreds of top quant Strong Buy-rated stocks. If you prefer to rely on investment professionals for stock recommendations, Alpha Picks is a service that identifies high-quality opportunities using a systematic, data-driven approach. It targets stocks with strong financials, attractive valuations, and long-term growth potential, offering research-backed selections designed to help long-term investors outperform the market.

For more active investors with a fixed amount of capital, the PRO Quant Portfolio (PQP) delivers a disciplined, data-driven, systematic model portfolio. Powered by Seeking Alpha’s proprietary Quant system, PQP draws from nearly 5,000 U.S.-listed stocks and ADRs worldwide, selecting top opportunities based on rigorous multi-factor selection. The portfolio holds 30 equal-weighted positions, rebalanced weekly to reflect updated ratings and market conditions. Subscribers receive weekly alerts on all trades and detailed analysis from the Quant Team, making it easy to follow or use as an idea generator.

I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs:

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs: