The average UK house price has surged by 74% or more than GBP150,000 over the past 20 years, according to the property website Zoopla. Across the past two decades, the typical property value has risen from GBP113,900 to GBP268,200, Zoopla said. London has seen average house prices more than double over the past 20 years. The south-east and eastern England have also seen a particularly big jump in house prices, with average property values rising by 87% in both regions over the past 20 years. By contrast, house prices in the north-east of England have risen by 39% during the period.

Pictet strategists reveal the adverse trends in equity markets that investors will face over the next half a decade.

09 June 2025

Pictet strategists reveal the adverse trends in equity markets that investors will face over the next half a decade.

By Matteo Anelli

Deputy editor, Trustnet

Equity investors should expect to make half the returns they have become accustomed to over the past decade and a half, as markets will be challenged on several different fronts in the years to come, according to Pictet Asset Management senior multi-asset strategist Arun Sai.

“Both on earnings and on multiples, the primary drivers of growth tell us that returns are going to be much weaker for equities. It’s going to be as much as half of the past five to 10 years,” he said.

“Returns over the next five years for global equities will be around 5% rather than the 10% we have got used to.”

This all comes down to Sai’s view that the key driver of equity returns over the past 20 years has been a “bizarre” structural uptrend in profit margins – a consequence of globalisation.

Although globalisation is “not going to reverse”, it will be “more nuanced”, he said, continuing for services, plateauing on goods and reversing on capital – all of which will lead to lower margins.

His way to tackle that is to “allocate deliberately to non-US champions, mid-cap stocks and European assets”.

Challenged US leaders

The US will be particularly affected. US tariffs, tax increases and weaker consumer demand will push global equities into a profit downturn, just as investors will grow more wary of inflation volatility and less inclined to pay a premium for stocks from a country that is losing momentum and soft power amid divisive policies.

There will be no US exceptionalism to come to the rescue, said Sai, not even its superiority in tech.

“There is no question that the US is the leader in tech across several dimensions, but are the moats around tech companies as deep as we thought they were a year ago? Perhaps not,” he said.

Sai used the example of Chinese artificial intelligence (AI) firm DeepSeek, which challenged Open AI’s ChatGPT at the start of the year. But this isn’t the only champion whose leadership is “not quite eroding, but at least being challenged”.

The US does not have a monopoly on innovation, Sai stressed.

“There are champions everywhere that benefit from the same kind of winner-takes-all trend, but trade on much lower multiples,” he said. “While retaining your investments in the winners, some amount of exposure to these other companies makes sense and diversifies you away from very crowded positions.”

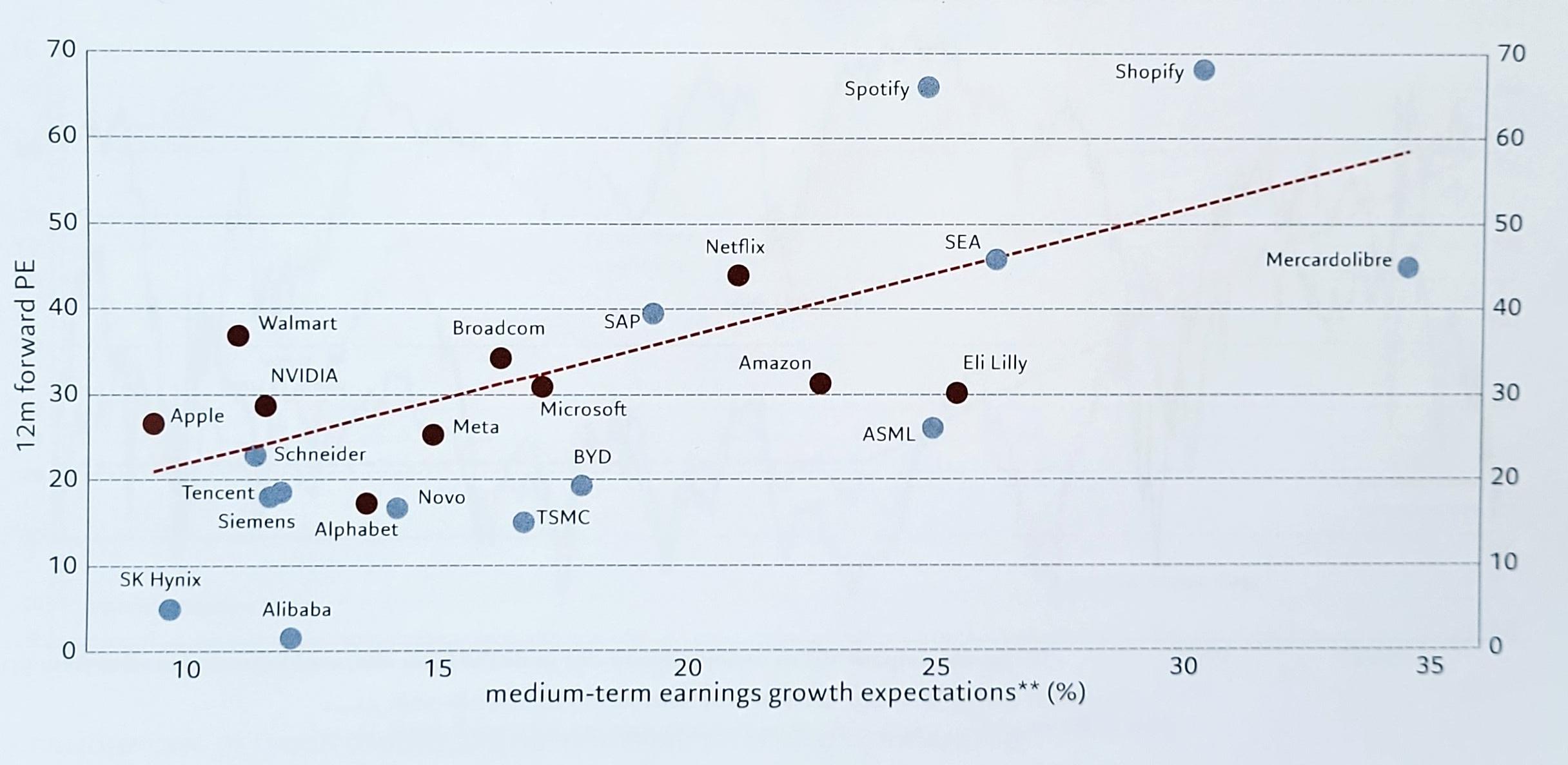

Below is a chart of such companies, showing the price-versus-growth expectations of US champions (in brown) and non-US champions (in blue).

US versus non-US leader by 12 months forward P/E ratio Source: Refinitiv, Pictet Asset Management. As of 30 May 2025.

“The blue dots are either as critical to some of these secular growth stories, or as good as some of the US winners,” Sai said. For example, he argued that the growth potential of Brazilian e-commerce company MercadoLibre is comparable to that of Amazon.

“There are a number of these players that have been left behind in the whole US exceptionalism narrative.”

To illustrate the transformation driving this winner-takes-all dynamic, Sai pointed to John Deere – a 200-year-old US tractor manufacturer that has reinvented itself as a high-tech solutions provider.

“We’re not abandoning that dynamic,” he said, “but on the margin we’re shifting toward non-US champions that are tapping into similar forces but trade at more reasonable valuations.”

Mid-caps on the rise

Not only did Sai suggest moving away from US leaders, he also argued that the large-cap space overall is getting overcrowded.

“If you had the luxury of taking a 30-year investment horizon, then all you would do is bet on the median stock, not on the winners,” he said. “That is because, over time, the median stock catches up to the winners. You always sell the winners and buy the median stock.”

Unfortunately, no investors can think that far ahead, so Sai suggested to hedge your bets: staying with the winners and allocating deliberately to what he called the “feed” stock.

“We think of this as mid-cap stocks. Investors should take an equal-weighted exposure to markets, rather than just focus on the mega-caps,” he said. “This gives them exposure to some of the next generation of winners, which will begin to play out in the next five years or so.”

The European advantage

Pictet chief strategist Luca Paolini mentioned another trend: there will be a “very minimal difference” between US and European GDP growth in a scenario where growth will normalise across developed countries.

“The US will always be a much more dynamic place to do business than in Europe. We are not saying sell everything in the US and come to the European heaven,” he said.

“Europe is not going to move significantly, but it is going to improve from a period of stagnation that has lasted for the past decade.”

Investors, especially if they are based in Europe, should also “think twice” about having a permanent, structural overweight to the US and would be better off putting their money to work at home.

“What we tend to forget is that, for Britons and Europeans investing abroad in equities, roughly 30% or 40% of total returns come from currency movements,” he said.

“The currency risk is not that relevant normally, but if you have low returns and low dispersion, like we will, one of the critical factors in achieving your expected returns is to get the currency right.”

DIY Investor Diary: this rule takes the emotion out of investment decisions

In the next instalment of our DIY Investor Diary series, Kyle Caldwell speaks to an investor who has a strict discipline of taking profits and cutting losses.

20th February 2024

by Kyle Caldwell from interactive investor

One investment pitfall is becoming too emotionally attached to a share, fund or investment trust whether it is a winner or a loser.

For the winners, investors risk becoming complacent having potentially “fallen in love” with the returns made in the past. However, there is no guarantee a top-performing company or fund will continue making hay in future years.

It’s important to take a step back and assess why an investment winner has been performing well. A fund, for example, could have been boosted by the region, area of the market, or investment style being in favour, which may not persist indefinitely.

In a similar vein, many investors find it hard to cut losses when an investment is underperforming. Some of this is rooted in behavioural finance biases, which cause investors to make irrational decisions based on emotion. Inertia, a tendency to maintain the status quo, is one example of a behavioural bias that can affect investment decisions. Inertia is part of the “endowment effect”, where an investor puts a higher value on something they own, so they are more reluctant to sell.

The latest interactive investor customer to feature in our DIY Investor Diary series seeks to take the emotion out of investing by enforcing a strict discipline of applying a “stop loss” of 15%.

The investor, who prior to retirement was a financial adviser, explains: “If, for example, I buy something at £1, I will sell it if it drops to 85p. Conversely, if it hits £1.50 and drops 15% from its all-time high, then I will also sell it if it falls to £1.27.”

To keep track of how his investments are faring, the investor has created a spreadsheet. He says: “I record the date of purchase, the epic (a shortcut for the name of the investment) buy price, current price, highest price ever achieved, present percentage gain or loss, the highest percentage gain, and finally the date it happened.”

He is a very active trader and a follower of the momentum style of investing.

Momentum investing is a strategy that taps into investors’ psychology. Some investors will refuse to buy a particular share or fund until they see an uptick in performance, as they want their inclination to buy to be validated by the market as a whole. Then, if that company or fund starts to rise decisively, investors who initially sat on the sidelines start to fear missing out on an opportunity to make money. They then buy, leading to momentum being retained.

However, this approach is only for those with the time and dedication to keep on top of their investments on a daily basis. Moreover, trading frequently can eat into overall returns.

The investor says: “I am a believer in momentum. I am trying to catch a wave and find investments that are starting to have a good run of performance. I study performance figures over one, three and six months, look at which shares, funds and investment trusts are starting to move, and consider the reasons why they are going up.”

He has both a self-invested personal pension (SIPP) and a stocks and shares ISA. The SIPP holds a mixture of shares, funds and investment trusts, while the ISA contains AIM shares that typically qualify for Business Property Relief. Such shares are exempt from inheritance tax (IHT) if they’ve been held for more than two years. The plan is for both the pension and the AIM ISA to be gifted to his four children.

In the SIPP, the six funds held are Comgest Growth America, L&G Global Technology Index, TM Natixis Loomis Sayles US Equity Leaders, Nomura Funds Japan Strategic Value, Pictet Robotics and GAM Disruptive Growth. The latter two are new holdings, introduced at the start of 2024.

Three investment trusts are held at present.

3i Group Ord

Ashoka India Equity Investment Ord

and India Capital Growth Ord IGC1.14%.

Despite currently holding fewer trusts than funds, the investor says he favours investment trusts due to their structural differences.

He says: “Investment trusts have a board of directors who can, and have, taken the investment mandate from an investment company and awarded it to another if they feel that there is underperformance or poor management.

“As regards dividends, they can withhold income and carry it forward to the next year, something that their collective cousins can’t do. Often it is possible to buy the investment trust at a discount to its net asset value. Again, this is something denied to funds.

“[Trusts] can gear (borrow) to magnify returns, but this can work against them in falling markets.

“Finally, you can deal instantly, whereas prices change only once a day with funds. If the market is either falling or rising rapidly, you have to wait until the following day to deal in funds, by which time prices may have moved badly against you.”

In addition, some exchange-traded funds (ETFs) are owned, including

Amundi IS Nasdaq-100 ETF-C USD GBP

Amundi Russell 1000 Growth ETF,

Invesco EQQQ NASDAQ-100 ETF GBP

Invesco Technology S&P US Sel Sec ETF GBP

iShares S&P 500 Info Tech Sect ETF$Acc GBP

IITU0 and ETC Group Global Metaverse ETF.

Given the yearly fund charge for passive funds is much lower than active funds, our DIY Investor says he’s drawn to passive strategies in areas that are heavily researched, meaning it is harder for active fund managers to gain an edge.

He says: “It has to be a special actively managed fund to get my attention.”

Key lessons learnt over the years include being both patient and humble. He notes: “One of my mottos is that success or failure in life is never final. It’s very chastening because it stops you from becoming complacent if things are going well, and it’s uplifting that even if things are bad, [things] can and will change.

“When applied to investment, don’t get cocky just because your investments seem to be flourishing, and don’t despair if they are suffering. Nothing lasts forever. Most investments enjoy a hot spell, but they can also endure lean times.

“Just to emphasise the point, when practising as an Independent Financial Adviser I had several “bankers” such as Lindsell Train Ord Worldwide Healthcare Ord and TR Property Ord TRY but in the six years since I retired they have gone nowhere.

“Investments are only a vehicle or means to an end, so don’t get emotionally attached to them. Some people can’t sell even when something is floundering because it would confirm that their judgement might have been wrong. I have often sold a holding and bought back in again at a future date.”

9% plus yields: how to navigate this investment trust sector.

Falling interest rates could provide a good entry point into renewable energy infrastructure trusts with their near double-digit yields, says Jennifer Hill.

9th June 2025

by Jennifer Hill from interactive investor

In the investment world, few sectors have experienced as sharp a reversal as renewable energy infrastructure trusts. Once buoyed by strong investor demand, these vehicles – powered by sun, wind, and waves – offered the appeal of clean energy alongside reliable, high-yield income.

But as interest rates climbed and sentiment turned cautious, the sector’s once-steady premiums to net asset value (NAV) gave way to steep discounts – from an average 7.2% premium at the end of 2021 to a 34.1% discount at the end of April this year.

“The renewable infrastructure sector has certainly been through the mill – wind or otherwise,” says David Liddell, a director at IpsoFacto Investor. “It’s important to note that the disastrous share price performance of many of these trusts has mainly been the result of this de-rating, rather than necessarily a fundamental loss in underlying value.”

With interest rates cut again last month to 4.25%, is now the time for investors to reconsider the sector and its weighted average yield of 9.4%?

Headwinds

A perfect storm of challenges triggered the sector’s sharp de-rating. Chief among them were rising interest rates – making cash and bonds more appealing – and waning investor enthusiasm for renewables. These were compounded by a flood of new investment trust launches, government intervention, surging construction costs, and growing doubts over long-term viability.

William Heathcoat Amory, managing partner at Kepler Partners, cites Ørsted’s early May decision to cancel Hornsea 4 – a major UK offshore wind project – as a telling signal.

“The Hornsea 4 cancellation is illustrative of higher build costs and lack of transaction data, which has meant developers are less confident on returns,” he says.

An exodus of wealth managers hasn’t helped either. An obscure regulatory ruling on how costs are attributed has eroded the appeal of these trusts among fund-of-funds managers.

Ongoing consolidation within the wealth management industry has only added to the pressure. Nowadays for a wealth manager to consider an investment trust, the assets need to be around 300 million for it to have a sufficient amount of liquidity.

“A focus on liquidity, in part driven by the consolidation of wealth managers and the increasing use of model portfolios, means that many infrastructure investment companies that failed to reach scale are now off the radar for potential new investors,” says Numis analyst Colette Ord.

“At the end of 2024, we decided to exit most of the holdings,” says Jack Turner, head of ESG portfolio management. “The decision was based on doubts on when discounts would close but also the uncertainty on the success of underlying infrastructure projects, especially those linked to renewable technologies.”

Tailwinds

Others see green shoots – and an opportunity to buy at the bottom. For Ord, current pessimism is “excessive”, while Liddell and James Carthew, head of investment companies at QuotedData, describe the sector as “just too cheap” and “irrationally cheap”, respectively.

Ord highlights the disconnect between weak sentiment in listed markets and robust demand for infrastructure exposure in private equity and debt. “Banks continue to view the sector as a high-quality covenant, evidenced by the number of successful financings at both project and company level,” she adds.

Demand could be fuelled by as much as £50 billion in fresh investment under the government’s Plan for Change – an initiative involving the UK’s largest pension funds and aimed at boosting business and infrastructure.

Signatories to the agreement will commit 10% of their workplace pension portfolios to assets supporting economic growth, such as infrastructure, real estate and private equity, by 2030.

“At least half that will be directed specifically to UK-based investments, expected to generate £25 billion for the domestic economy by the end of the decade,” says Darius McDermott, managing director at FundCalibre, the fund research firm.

“And with the current level of global uncertainty, the UK looks an increasingly stable haven. We’re already beginning to see asset managers return to undervalued UK assets – particularly lower down the cap scale – which could mean falling discounts and rising capital returns for trust investors.”

There may be other longer-term political and economic forces at play, with Kepler’s Heathcoat Amory perceiving strong public support for renewable energy.

“I think the UK populace other than Reform voters are in favour of a significant expansion in renewable power, so Hornsea 4 may in time be met by further political or financial support to get built out, which may help turn sentiment.”

In the short term, he adds, a slowdown in wind turbine development could benefit existing assets. “Less development buildout will reduce the pressure on long-term power prices, one of the inputs into valuations, which will be a tailwind at the margin.”

Short-term opportunity?

Fairview Investing director Ben Yearsley points to a “fascinating area with what could turn out to be a short-term opportunity”.

in a £1 billion deal that represents a premium to NAV, while in battery storage Harmony Energy Income Trust Ord is being acquired at a 5% discount to NAV and 35% premium to where shares had been trading.

Ord at Numis says it “sends strong signals on valuation”. She expects consolidation to continue while share prices trade at such wide discounts.

Given the amount of takeover activity, “will there be any interesting ones left in a year’s time or will it be only the dross left?” asks Yearsley.

The sector spans a diverse range of strategies – solar, wind, hydrogen, energy efficiency and energy storage. Some trusts focus on one area, while others combine multiple technologies to balance seasonal generation and market cycles.

Single-asset-class trusts are more likely to become takeover targets, says Carthew – a prospect that could help crystallise value for shareholders. But trusts with broader diversification may offer greater resilience against shifting weather patterns and regulatory pressure.

“Geographic and technology diversification has benefits,” says Ashley Thomas, an analyst at Winterflood Securities. “This is currently demonstrated by the weak wind speeds experienced year-to-date across Europe, which has impacted wind generation. In contrast, solar generation in the UK has been strong in March and April, but relatively weak in Spain and Australia.”

As renewable capacity expands, Thomas expects to see more pronounced intra-day price volatility, with solar pushing down prices during bright summer days and wind doing the same on breezy winter nights.

The potential of locational pricing being introduced into the UK, as well as general regulatory or political risk in certain geographies, also supports the case for diversification, he adds.

Best buys

For investors sitting on the sidelines, there is one overriding reason to consider infrastructure trusts.

“Yield is the obvious and relevant answer,” says Mike Neumann, bespoke investment management director at EQ Investors.

This, he adds, applies both to income seekers and growth-focused investors. Investors can increase the value of their shareholding by reinvesting dividends and achieve capital growth over time without any additional cash outlay.

Yearsley agrees: “While there’s a short-term opportunity for discount narrowing and capital gains, it’s a long-term income-producing story you’re really investing for.”

He says the “good opportunities” lie in trusts able to secure long-term power purchase agreements – which tends towards solar, wind and hydro – and those with dividends covered by cash flow. His top picks are Greencoat UK Wind and Downing Renewables & Infrastructure Ord

EQ is also a fan of Greencoat UK Wind, with its market capitalisation of £2.5 billion, -21.9% discount and yield of 8.9%. “It yields about twice that of a long-dated gilt and generates a significant level of cash even when wind resource is low,” says Neumann.

Carthew finds it harder to choose just one name. “It’s hard to pick – I own a few – but I love Downing Renewables mainly because of the hydro and battery storage potential, and to me, this feels like a relatively lower-risk investment,” he says.

The top pick for both Ollie Clark, deputy head of research at WH Ireland, and Liddell at IpsoFacto Investor is the Renewables Infrastructure Group, which is predominantly exposed to wind, with additional exposure to solar and a growing interest in energy storage through its acquisition of Fig Power.

Clark rates the trust’s “risk dynamics”, while its near £1.9 billion size and fully operational, “quality” portfolio should help it to capture inflows from liquidity-conscious investors. “Despite the near 10% yield and these attractive characteristics, TRIG still trades on a discount of -28.2%,” he says.

Liddell, meanwhile, appreciates TRIG’s long experience in the sector (since its launch in 2013) and its size, which allows it to sell assets to other institutional investors without compromising its own viability.

“TRIG has shown the way in raising cash through divestments, which have been at an average premium to valuations of 11%, giving some justification to the level of NAV,’ he adds.

focuses on reducing energy use through on-site generation and efficiency projects.

“Its holdings are diversified across sectors and geographies, with assets located in the UK, Europe, and North America,” says McDermott. The £480 million trust is trading on a -51.4% discount and yields 14.2%.

How the pros spot value-trap shares with dividends ‘in danger’

Kyle Caldwell runs through the main warning signs the professionals look out for that point to a dividend in danger.

13th September 2023

by Kyle Caldwell from interactive investor

Income-seeking investors are spoilt for choice, with dividend-paying shares no longer the only game in town.

Prior to interest rates rising from the end of 2021 onwards, investors had no choice but to size up equities to procure a decent level of income. However, now that bonds have re-priced in response to rate rises, yields of 4% to 5% are obtainable on debt that’s deemed relatively low risk. For those who are prepared to stomach greater levels of risk, yields of 5% and 6% can be found on both corporate and government debt.

In addition, savings rates and cash-like investments (money market funds) have seen their income returns increase on the back of interest rate rises. The Bank of England base rate has moved from 0.25% to 5.25% over the course of nearly two years.

However, while bonds are certainly attractive again for income seekers, investors who buying individual bonds today, today, and looking to hold them to maturity, are currently accepting a below-inflation income return. In contrast, while there’s no guarantee, dividend-paying equities offer the prospect of inflation-beating returns through a combination of capital growth and dividend returns.

investment trust, one of our Super 60 investment ideas, observes that as companies grow their profits and their dividends, this provides dividend growth over the long term. However, with bonds “the interest is fixed”.

Speaking to interactive investor, Curtis said: “I think this is particularly important in a period when you’ve got inflation. In real terms, if you’ve got a fixed-rate deposit or bond, and inflation is around 8%, within a year your money has lost 8% of its purchasing power.

“While in an equity fund, you’ve at least got the growth in income, which can alleviate that inflationary effect.”

Drilling down into the dividend

However, a trade-off is that equities are riskier than bonds. The same is true for income-seeking investors, as company dividends can be cut, suspended or cancelled without notice. But with bonds, the income on offer will keep on flowing unless the company falls into financial difficulties.

It is therefore important to drill down into the dividend to assess whether it is sustainable.

Below are some of the main warning signs the professionals look out for that point to a dividend in danger.

A high dividend yield

A high dividend yield looks attractive on paper, but it should be treated with a healthy dose of scepticism.

As share prices and yields have an inverse relationship, a high yield is often a sign that a stock, for whatever reason, is out of favour.

It is therefore crucial to do some digging to check whether the yield on offer is sustainable to avoid so-called value traps.

George Cooke, manager of Montanaro European Income fund, one of interactive investor’s ACE 40 investment ideas, says: “We view high dividend yields as a warning sign more often than not. If you have a dividend yield of 10% or 15%, it’s usually just the market telling you that you’re about to get a dividend cut rather than this is a stunningly great opportunity.”

For Simon Gergel, fund manager of Merchants Trust Ord an attractive yield is important, but does not drive the investment decision.

Gergel said: “We always buy companies where we think we can make a good total return. So, we fish in the pond of high-yielding companies. But once we own them, we’re not concerned whether that dividend is growing fast or not growing much at all.

“We want to buy companies where we think we can make good money, and if we can make good money on the underlying company. Ultimately, we can either get dividend growth from that company, or we can reinvest the proceeds to get dividend growth elsewhere.”

Another thing to bear in mind is that high yields do not mean market-beating returns from a total return perspective – when both capital and income are combined. In addition, dividend growth may be higher for dividend-paying shares with lower yields.

Check the track record for paying dividends

A company’s track record for paying dividends is worth considering. Although a stock that has historically been a generous payer should not be considered a sure bet for dividends continuing to roll in, those businesses which have patchy records should set alarm bells ringing.

However, bear in mind that a dividend track record does not show the fundamentals of a business, such as balance sheet strength and return on capital.

Moreover, to keep the dividend track record going, there’s the risk that some companies will keep on paying dividends for longer than is sustainable, such as through increasing their debt levels to fund income payments.

says that the most important things to check are “balance sheet, cash flow, the barriers to entry and how much the underlying company is growing”.

Cooke adds: “First and foremost the companies have to be high-quality and growing. And we think doing it that way round prevents us and helps to stop us from being seduced by an optically high dividend yield, which then turns out to be high for a reason, which is that the company is declining.”

The The SPDR S&P UK Dividend Aristocrats ETF UKDV is one way to gain exposure to stocks with long dividend track records. It tracks the 40 highest-yielding UK companies that have increased or maintained dividend payments for at least seven consecutive years. Its top five holdings are

British American Tobacco IG Group Holdings Intermediate Capital Primary Health Properties and Legal & General Group

Payout pledges can be broken

A commitment from the management of a company to maintain a future dividend payment should, in theory, be seen as a positive. However, the reality is that there have been far too many broken promises over the years for investors to bank on such pledges.

During the Covid-19 pandemic, oil major Shell ended its remarkable dividend run by cutting its income payout for the first time since the Second World War.

Direct LineThe firm unexpectedly cut the dividend at the start of 2023, just months after former chief executive Penny James had said it was safe. Following the dividend cut, James stepped down.

In response, Curtis sold down Direct Line, but retained a holding. He explained: “Sometimes when a dividend cut happens, it can be after a period of share price underperformance. And if you sold out of the stock, you’d be throwing out the baby with the bathwater so to speak and doing it at the worst possible moment.

“But, in the case of Direct Line, we’ve reduced the holding quite substantially and so sold more than half our holding because there are other companies in insurance and financials generally which have carried on paying and growing their dividends, so are, in the short term, more help to us.

“But Direct Line has got very good recovery prospects in my opinion. It is a kind of leading insurer in motor and property insurance in the UK and it’s been a very strong brand, so I didn’t really want to sell out of it entirely, so we’ve kept a smaller holding.”

Dividend cover

This is considered a key metric to assess whether a company is in a healthy position to distribute dividends. It is calculated by dividing earnings per share (EPS) by the dividend per share (DPS).

As a rule of thumb, a low dividend cover ratio – around one times or lower – suggests dividends are vulnerable, as a company is using most, if not all, its profits to fund the dividend. A figure of two or more is seen as comfortable because it’s a sign a business is not over-distributing.

Those firms that do hand back more cash than they can afford risk damaging their longer-term growth prospects through lack of investment in the business.

Curtis points out: “It’s very important that companies are also investing in themselves enough for the future, making enough capital expenditure on plants and equipment or their brands because, unless they are investing enough for the future, you won’t get the future growth.

“I should also say that I prefer companies with strong balance sheets. Those companies are much more resilient when times are tough and the economy’s turning down. In that type of situation, companies that are highly indebted are going to be more at risk. They might well be under pressure to cut their dividends.”

Dividend payout ratios

Another thing to be aware of is that some companies have strict dividend payout ratios, which is the percentage of earnings paid to shareholders via dividends.

Some mining companies fall into this camp. As a result, if they make less money, dividends are cut. The sector is not a reliable dividend payer, as dividends fluctuate depending on the performance of the iron ore price.

Debt levels on the rise

When the dividend is being funded out of debt, it is a potential red flag. One way for private investors to work this out is by looking at the free cash flow measure. This takes into account how much money a company has left over once all business expenses have been made, including interest on borrowings.

Those businesses that pay their dividends without resorting to borrowing will have a positive free cash flow figure.

But bear in mind that a negative score does not always mean the dividend is under threat. If money is borrowed cleverly and efficiently, the business will ultimately become more profitable.

Henry Dixon, fund manager of Man GLG Income, one of interactive investor’s Super 60 investment ideas, says that financial leverage is certainly a warning sign that a dividend may not be sustainable.

He says: “Value traps are just such a painful part of the job, and you do everything you can to insulate yourself from that.

“And you try and work out a common theme of value traps and what happens. I definitely would observe that financial leverage can certainly get in the way of realising the value that might be on offer.”

DIY Investor Diary: how my ISA and SIPP are invested differently

The latest ii customer to feature in our series explains how and why he is taking more risk with his SIPP compared to his stocks and shares ISA.

14th November 2023

by Kyle Caldwell from interactive investor

21

0

Share on

Related Investments

Buying shares involves more work and effort than outsourcing the investment decision-making process to a fund manager, or following the up and down fortunes of a passively managed index fund or exchange-traded fund (ETF).

Of course, not everyone who buys shares in individual companies is a forensic accountant. In addition, many investors do not fully understand accounting jargon or every industry valuation measure.

However, this doesn’t mean that you shouldn’t buy shares. People choose to do so for many reasons. You might enjoy the intellectual stimulation, or you could be interested in smaller, more speculative companies that aren’t available in funds or investment trusts.

In return for the higher risk that comes with buying individual shares, the potential reward can be higher too. This is a major part of the appeal.

The latest investor to be profiled in our DIY Investor Diary series mainly picks his own shares. He holds around 20 stocks, alongside a couple of ETFs and one active fund, Fundsmith Equity.

This investor, who is in his early 30s and works in the financial services industry, decided to be more active with his savings and investments about two years ago.

He explains: “Beforehand, I simply used my company pension and savings accounts, as I wanted to be sure I could commit sufficient time to properly managing my own portfolio before investing more actively.”

While he had built up knowledge in his line of work, the DIY investor also swotted up further before taking the plunge into the stock market. As well as wanting to take control of his own finances to grow wealth over the long term, he also views investing as a bit of a hobby.

He holds an ISA, SIPP and general investment account with interactive investor. He contributes to his SIPP monthly alongside his employer, and adds lump sums to the ISA and general investment account.

For both ISAs and SIPPs, all income and capital gains on investments grow free of tax. Both offer a wide variety of investment options – shares, funds, investment trusts and ETFs.

However, as ISAs offer much more flexibility, since you can withdraw from them whenever you like, this tax wrapper can be utilised to save towards a specific goal. In contrast, a SIPP is a retirement pot, as money cannot be withdrawn before the age of 55, rising to 57 from 2028.

Due to the difference in when money can be accessed, the DIY investor manages his ISA and SIPP in different ways.

His ISA is more conservative, reflected in the holding of a couple of ETFs and Fundsmith Equity. In contrast, the SIPP is more aggressive, with around 20 positions.

“Given the longer-term goals of the SIPP, I take on considerably more risk, investing in single stocks and keeping quite a concentrated portfolio.

“With my ISA, I don’t want to see a lot of volatility. My ISA strategy is to build up sufficient savings to go towards deposits for a house, car or other potential shorter-term goals. As such, I look to preserve capital via diversification by holding funds which contain many stocks. This makes it simpler and more cost effective for when I need to sell the positions in the ISA for these goals.”

To narrow down the universe of thousands of companies that he could potentially invest in, our DIY investor has a couple of stock screeners in place in an attempt to find good value companies with strong margins and strong profit levels. He also looks for potential catalysts to drive share prices higher. As well as looking for certain attributes, he picks up ideas from reading articles and research pieces.

“When I look for new stocks, I generally look to add positions that are different to what is in the portfolio already, so as to keep up diversification. Valuation is key, I want to get value for money.”

“When I started investing, it was scattergun approach, with a number of familiar UK names. I didn’t carry out too much due diligence on each stock. This was not a good strategy, and could have been replicated much easier and more cost effectively by holding a UK-focused fund or ETF.

“I wasn’t sufficiently diversified, and to change that I have been moving to having more of an international portfolio.”

Typically, one or two trades are made each month, with around 30 shares on a watchlist.

His top tip for fellow investors is “not to become too emotionally tied to a holding”.

He adds: “It is important to continually reassess your thoughts, thesis and approach. It is always worth challenging your own perspective. And when things change, don’t be afraid to cut losses.”

Basing investment decisions on emotion and falling in love with stocks are major pitfalls that can prove detrimental to returns. Instead, as he wisely remarks, it is important to “be clear in your investment goals and build your portfolio accordingly”.

He adds: “Large institutional investors and funds have to manage their liquidity risk, making sure the liquidity of the assets they invest in matches the liabilities of their fund.

“Although it’s a bit different when it comes to individual investors, as they are unlikely to hold large enough holdings in a single stock or fund that could be a liquidity issue, it is still important to understand the liabilities (retirement income, saving for a deposit, etc) and having a portfolio of assets which matches those specific goals in a cost-effective manner.”

His views on active versus passive investing is that there’s a place for both. However, overall he prefers to pick his own stocks.

He likes the investment style of Terry Smith of Fundsmith Equity, which is why it is the only active fund he owns.

He describes ETFs as “great tools for investors” that offer a “much easier and much more cost-efficient way to run a diversified portfolio than holding 50-100 single stocks”.

“Additionally, you can get exposure to other asset classes, such as corporate bonds or derivative strategies, which can be interesting portfolio diversifiers,” he points out.

When buying individual shares, putting in the time and being dedicated are key. Questions to ask yourself and things to bear in mind when buying shares include:

How does the business make money ? What is the business model ?

What is its financial position? You will need to read the balance sheet and analyse cash flow

Analyse the risks the firm faces to understand if it might be more or less profitable in the future

Is now a good time to buy? You need to take into account the various valuation metrics that indicate whether a share is overvalued or undervalued

Are you investing for growth, income or both? If you want a certain level of income, you will need to consider whether the company pays dividends, and whether those dividends are sustainable going forwards. This article has plenty of pointers on how to delve into a dividend.

3i Infrastructure PLC ex-dividend date BlackRock Energy & Resources Income Trust PLC ex-dividend date CT UK Capital & Income Investment Trust PLC ex-dividend date Empiric Student Property PLC ex-dividend date Henderson High Income Trust PLC ex-dividend date JPMorgan US Smaller Cos Investment Trust PLC ex-dividend date Land Securities Group PLC ex-dividend date Pacific Assets Trust PLC ex-dividend date Palace Capital PLC ex-dividend date Scottish Mortgage Investment Trust PLC ex-dividend date US Solar Fund PLC ex-dividend date VPC Specialty Lending Investments PLC dividend payment date Worldwide Healthcare Trust PLC ex-dividend date

Do you ever feel “the curse” of investing at exactly the wrong point? Like your investing is too late, at the wrong time, or maybe that you’re just unlucky?

Well meet Bob – the World’s Worst Market Timer. Bob began his working career in 1970 at age 22 and was a diligent saver and planner.

His plan was to save $2,000 a year during the 1970’s, then increase his savings by $2,000 each decade. In other words $2,000/year in the 70’s, $4,000/yr in the 80’s, $6,000/year in the 90’s… you get the picture.

Bob started in 1970 with $2,000, added $2,000 in ’71 and ’72, then decided to take the plunge and invest in the S&P 500 at the end of 1972. (Time out: there were no index funds in 1972, but come along with me for illustration purposes).

Now in 1973 – 74, the S&P dropped by nearly 50%. Bob had invested his life savings at the peak, just before it fell in half! Bob was bummed, but Bob had a plan and he was sticking to it. You see Bob never sold his shares. He didn’t want to be wrong twice by investing at the peak and then selling when prices were low. Smart move Bob!

So Bob kept saving $2k/year in the 70’s and then $4k/yr in the 80’s. But he was feeling the sting of his last investment and did not feel comfortable adding to his fund until he had seen the markets rise a fair amount. In August of 1987 Bob decided to put 15 years of his savings to work. Seriously Bob?

This time the market fell more than 30% right after Bob invested. Bob, amazed at his investing prowess, did not sell.

After the 1987 crash, Bob was really planning to wait it out. In the late 1990s everything was on fire. The internet was unbelievable new technology and stocks were flying high. By 1999 Bob had accumulated $68,000 from saving each year. A firm believer that the Y2K bug was boloney, Bob invested his cash in December 1999 just before a 50% decline that lasted until 2002.

The next buy decision in October 2007 would be one more big investment before he would retire. He had saved up $64,000 since 2000, deciding to invest this right before the financial crisis that saw Bob experience another 50% decline. Monkey’s throwing darts were probably better at investing than Bob.

Distraught and disheartened, Bob continued to save each year and accumulated another $40k. He kept his investments in the market until he retired at the end of 2013.

So let’s recap: Bob is definitely has “bad timing”, only investing at market peaks just before severe market declines. Here are the purchase dates, subsequent declines and the amounts Bob invested:

Fortunately Bob was a good saver, and actually a good investor. You see once he made his investment he considered it to be a long-term commitment and never sold his shares. Even the Bear Market of the 70’s, Black Monday in 1987, the Tech Bubble or the Financial Crisis did not cause him to sell or “get out” of the market.

He never sold a single share. So how did he do?

Bob almost fell out of his chair when his advisor told him he was a millionaire! Even though Bob made every single investment at the peak, he still ended up with $1.1M! How you might ask? Bob actually had what we would call “Good Investor Behavior”.

First, Bob was a diligent and consistent saver. He never waivered from his savings plan (recall $2k/year in the 70’s, $4k in the 80’s, $6k in the 90’s, $8k in the 2000’s, $10k in the 2010’s until his retirement in 2013 at age 65).

Second, Bob allowed his investments to compound through the decades, never selling out of the market over his +40 years of investing – his working career.

During that time Bob endured tremendous psychological toil from seeing huge losses accumulate right after he made each investment. But Bob had a long-term perspective and was willing to stick with his savings and investment plan – even if his timing was “a bit off”. He saved and kept his head down.

Certainly you realize Bob is an illustration. We would never advise only investing in a single strategy, let alone a single investment like an index fund. If Bob had invested systematically, the same amount each month, increasing his savings like he did he would have ended up with even more money, (over $2.3M) – but that would not have been Bob, the Worlds Worst Market Timer.

So what are the lessons?

If you are going to invest, invest with an optimistic outlook. Long-Term thinking often rewards the optimist. Unless you think the world is coming to an end, optimists are typically rewarded.

Temporary, short-term losses are part of the deal when you invest. How you react to those losses will be one of the biggest determinants of your investment performance.

The biggest factor in investment success is savings. How much you save, and how methodically you save has a much bigger impact than investment return. Get these three things right along with a disciplined investment strategy and you should do well. Even Bob did well. Nice work Bob.

Buy a tracker, add funds when you can, when nearing retirement have a cash fund in case the market crashes before you start to spend your hard earned.

This article provides a detailed perspective on planning for a comfortable retirement through passive income. It’s interesting how the author emphasizes the importance of tailoring retirement goals based on individual circumstances. The breakdown of income requirements for single and two-person households is quite eye-opening, especially the £43,900 figure for a single person. I wonder, though, how realistic it is for the average person to achieve such a high passive income through investments alone. The author’s strategy of investing in global stocks and maintaining a cash reserve seems balanced, but what about those who may not have the knowledge or confidence to invest in shares? Could there be simpler, less risky alternatives for people who are not as financially savvy? Also, how much of this plan relies on market stability, and what happens if the returns don’t meet expectations? It’s a thought-provoking read, but I’d love to hear more about how to mitigate risks for those who are just starting their retirement planning journey. What would you suggest for someone who’s hesitant to dive into the stock market?

If you buy a world tracker fund, as long as you can choose when to sell you will not lose money, it could be several years though, so if you are saving for a specific reason, like a deposit for a car or a house etc., compound your interest where cash is king.