The recent addition to the Snowball was bought for the near dividend and to try and emulate the above chart, whilst history doesn’t always repeat it often rhymes. It’s possible the share price could fall from here before finding a floor.

MRCH offers a lower yield but a secure dividend to balance the higher risk yields in NESF, SEIT and FGEN a blended yield of 7%. Unless the price of MRCH falls out of bed, future dividends will be used to buy more shares in the higher yielders.

I bought for the Snowball 1798 shares in MRCH for 9k.

Buying yield 5.8%

Income

Income from Merchants’ investment portfolio saw a modest year-on-year decline from the record year in 2024, with revenue earnings per ordinary share at 29.4p (2024: 30.5p), representing a 3.6% reduction.

Despite this, earnings fully covered the total proposed and declared dividends for the year, allowing for a small addition to revenue reserves, which stood at 18.8p per ordinary share at year-end.

Shareholders will appreciate that one of the key advantages of the investment trust structure is its ability to smooth income distributions-drawing on reserves during challenging market conditions and replenishing them in stronger periods. It is encouraging to see that, following the Board’s strategic use of reserves to sustain dividends through the COVID-19 period, we have now been able to rebuild reserves over recent years.

43 years of dividend growth

The Board proposes a final dividend of 7.3p per share for shareholder approval at Merchants’ upcoming AGM on 20 May 2025. If approved, the dividend will be paid on 29 May 2025 to shareholders on the register at the close of business on 22 April 2025, with an ex-dividend date of 17 April 2025. A Dividend Reinvestment Plan (DRIP) is available, with an election deadline of 7 May 2025.

This brings the total proposed dividend for the year to 29.1p (2024: 28.4p), representing a 2.5% increase over the previous year. Notably, this marks Merchants’ 43rd consecutive year of dividend growth, reinforcing our position as an Association of Investment Companies’ (AIC) Dividend Hero.

£££££££££££££££££

With the two recent trades the current income has been reduced slightly but added a safety net of ‘secure’ dividends.

The Snowball allows costs of five pounds for buys and ten pounds for sales.

The current charges for both are five pounds but some purchases have stamp duty charged, so along with no interest is added the account for cash not invested the figures roughly balance.

The year end dividend is dependent on any surplus cash being paid as a dividend around October.

13 March 2025

TwentyFour Select Monthly Income Fund Limited

Re: Dividend Announcement

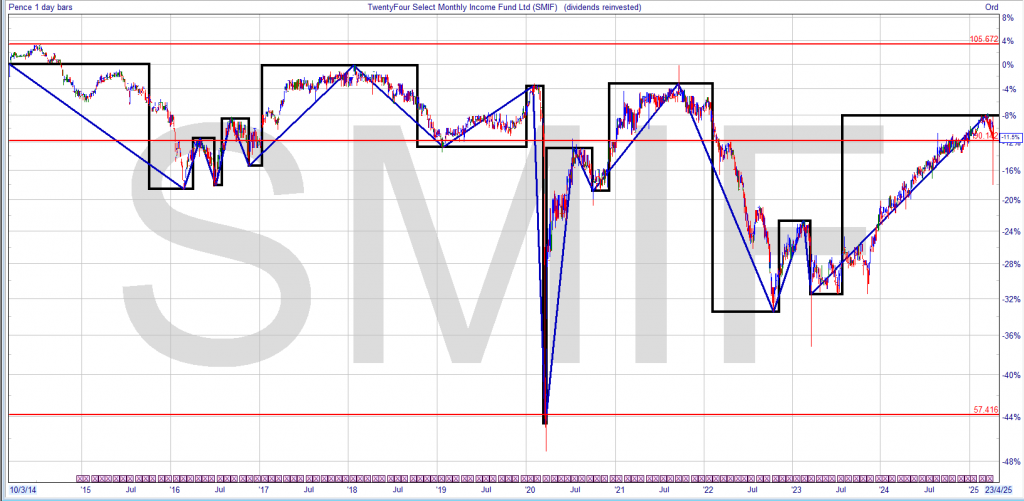

The Directors of TwentyFour Select Monthly Income Fund Limited (“SMIF“), the listed, closed-ended investment company that invests in a diversified portfolio of credit securities, have declared that a dividend of 0.5 pence per share will be paid, in line with the Prospectus, representing the regular monthly targeted dividend for the financial period ended 28 February 2025 as follows:

Can you imagine living by the “4% rule” right now?

Selling 4% of our stocks every year, hoping we don’t run out of money…

Meanwhile the S&P 500 is dropping 4% every day as Wall Street battens down the hatches for a global recession.

No, thank you. That’s a recipe for disaster!

As Chief Strategist Brett Owens wrote to us this morning, serious income investors have it better than most hopeful and current retirees.

We don’t need to rely on stock prices for income. Our carefully curated dividend portfolio provides us with the cash flow we need to pay the bills and fund our lifestyle.

Take Brett’s newest recommendation: it throws off a whopping 13.4% dividend and is built to withstand market volatility. It even has upside potential when sentiment turns.

And it’s just one part of Brett’s ” 8%+ Monthly Payer Portfolio.” This handpicked collection of stocks and funds is designed to turn your portfolio into a monthly income machine – with safe, steady payouts you can actually live on.

We’ve been living through a record-setting market – but not the good kind of records…

Stocks just suffered their worst first quarter of the year since 2022. March was also the worst month for stocks since December 2022.

Last week, we saw the market’s worst week of losses in almost five years, going back to the early months of COVID-19.

And according to Bloomberg, the stock market just experienced its worst 10 weeks to start any presidency since 2001.

But unlike in 2001, the recent crash isn’t due to a bubble bursting. It’s the result of a deliberate economic shock…

After markets closed on Wednesday, President Donald Trump revealed his much-discussed tariff package.

The plan included a flat tariff of 10% on all foreign imports, plus higher duties for America’s biggest trade partners. The tariff package shocked Wall Street… and provoked Thursday’s hasty sell-off.

So far, this administration has been painful for stock investors. And the new tariffs look certain to ring in more volatility from here.

But there’s a simple way to protect your portfolio from future shocks. You just need to be strategic about asset allocation.

Let me explain…

The Downside to Passive Index Investing

One of the most common market approaches is “passive index investing“…

If you’re a passive index investor, you’re paying a percentage of your wages into a broad market index like the S&P 500. This approach gives investors easy exposure to the whole scope of American industry. But this strategy has a catch…

Stock indexes are weighted by market capitalization. That means the bigger a company is, the more space it takes up in its index and this weighting can burn passive investors worse than they realize.

For example, the top seven tech companies in the S&P 500 make up about 28% of the index today. That means passive investors are putting a lot of eggs in the Big Tech basket.

But supply chains for Big Tech are complex… And just about all of them run through China. That leaves stocks like the so-called “Magnificent Seven” extra exposed to the new tariffs. That’s part of why the S&P 500 fell so much last week.

Investors who pour their money into a market-cap-weighted index fund risk taking greater losses whenever Big Tech names hit a stumbling block.

A top-heavy market can be dangerous. But investors can protect themselves by simply buying other assets…

Since November, I’ve highlighted the importance of diversification in a high-tariff regime. I’ve recommended a blend of stocks, bonds, and precious metals like gold to prepare for the new “Trump Trade.”

Now that there’s some data in the books, we can look at how diversification has performed since Trump took office.

We’ll use the iShares 20+ Year Treasury Bond Fund (TLT) as a stand-in for bonds. This fund tracks the performance of long-dated U.S. Treasurys.

And we’ll use SPDR Gold Shares (GLD) for gold. This fund holds gold bullion in trust and allows investors to get easy exposure to the metal.

Below is a chart of how stocks, bonds, and gold have fared since Inauguration Day on January 20. Take a look…

Since Trump took office, stocks have tanked by about 16%. But in the same period, bonds and gold have soared – rising 6% and 11%, respectively.

In other words, a blended approach was a strong defense compared with an all-stock strategy.

You can see just how much of a difference asset allocation makes in a few different portfolio mixes below..

Again, an all-stock portfolio has fallen 16% since Inauguration Day. But by placing a third of that allocation into a 50-50 blend of bonds and gold, the drawdown shrinks to just 8%.

Allocating half of the portfolio to the bond-gold blend would have resulted in a 4% drawdown since Inauguration Day.

And a portfolio split evenly between all three assets would be about flat.

Passive investors have been eating losses all year. But you can break that cycle now, simply by adding variety to your investments.

Amedeo Air Four Plus Ltd ex-dividend date Athelney Trust PLC ex-dividend date BlackRock American Income Trust PLC ex-dividend date BlackRock Latin American Investment Trust PLC ex-dividend date CT Private Equity Trust PLC ex-dividend date F&C Investment Trust PLC ex-dividend date International Personal Finance PLC ex-dividend date Invesco Asia Dragon Trust PLC ex-dividend date JPMorgan Asia Growth & Income PLC ex-dividend date Manchester & London Investment Trust PLC ex-dividend date Petershill Partners PLC ex-dividend date Schroder Asian Total Return Investment Co PLC ex-dividend date Schroder European Real Estate Investment Trust PLC ex-dividend date

I’ll finish with one last leftfield note. It involves what I think is a companion piece to the UBS report, namely a fab little paper by Lindsell Train portfolio manager James Bullock – whose work contributes to the Lindsell Train (LTI) investment trust – called A Very Long Hill.

Bullock makes what I believe is a crucial point that complements the conclusions reached in the UBS report: that time in the market is essential, as is adhering to long-term compounding returns. Bullock observes: ‘Most savers don’t (or can’t) stay fully invested, resulting in “time out of the market” and behavioural traps for those who “time the market”.’ The “gap” might not sound like much, but it costs the compounder greatly.’

As Brad Barber & Terrance Odean noted in an influential Journal of Finance paper on this topic: ‘Individual investors who hold common stocks directly pay a tremendous performance penalty for active trading… Our central message is that trading can be hazardous to your wealth.’

Or, to put it simply, that massive compounding engine for equity returns suggested by the UBS report only really works if left uninterrupted.