Even the global financial crisis couldn’t tarnish this trust’s premium.

This debt-seeking vehicle treads where others dare not James Carthew

Questor is The Telegraph’s stockpicking column, helping you decode the markets and offering insights on where to invest.

Debt is huge across investment companies right now – in a good way. Trusts offering access to this sector come with the obvious attraction of rising dividends, which have been buoyed thanks to higher interest rates. Better still, the dividend yields on these trusts are well ahead of those that an investor would receive from a government bond, but achieving this requires taking on additional risk in some form.

While many managers rely on leverage to achieve the desired result, CQS New City High Yield Fund looks for debt issues that would normally be considered too small for most debt investors and those that have not been assessed by a credit rating agency. These relatively overlooked issues tend to trade on higher yields, but require the manager to run its own credit assessments to ensure the yields on offer are not too good to be true.

The trust pays a quarterly dividend and can boast a track record of increasing dividends every year since its inception more than two decades ago. The trust’s financial year runs to June 30, and at the interim stage the board said that it thought this year’s dividend would be covered by earnings.

In addition to providing a high yield, preservation of capital is an important part of the investment objective and to that end the manager’s approach is conservative.

The team is headed up by Ian Francis, who brings more than three decades of experience and can draw on the substantial resources of Manulife CQS Investment Management’s credit analysis team. The portfolio is fairly diversified, with exposures to more than 100 different issuers, but thanks to the detailed research of his team Mr Francis is comfortable with a high concentration of roughly 40pc of assets in the 10 largest positions.

Some of the names in that list will be familiar: Co-op Bank, Virgin Money and Barclays. Some of the more unusual ones are subsidiaries of more well-known brands. For example, other top 10 positions are TVL Finance, which issues debt on behalf of Travelodge, and Galaxy Bidco, a financing arm for Domestic & General Insurance and a longstanding position in the portfolio.

The overall bias is to sterling-denominated issues, which comprise more than 70pc of the portfolio. Some readers may be comforted that just 16pc of the portfolio was exposed to US dollars at the end of December 2024, given President Trump’s ambition to weaken the currency.

The portfolio also includes some exposure to preference shares, convertibles and high-yielding equities (about 13pc of the trust at end January 2025). At the end of 2024, there was a position in NextEnergy Solar Fund, which is trading on a yield of 12.4pc, for example.

CQS New City High Yield has peers with higher returns, but these tend to come with higher Nav volatility. It has built up a loyal fanbase and, if you are already a shareholder in the trust, you are probably happy to hang on. However, new investors will have to stomach the premium that the shares trade on.

CQS New City High Yield Fund’s shares have traded at a premium to net asset value for almost all of the trust’s life, even during 2008’s financial crisis, reflecting the impressive work of the manager. Notable exceptions were the Covid panic five years ago, when the discount briefly breached 18pc but returned to a premium a few days later, and the early part of 2021. It is worth remembering that five-year performance figures are currently misleading, thanks to the Covid anniversary.

The 2021 event was significant because this was the point when some investors began to suspect that we were headed for higher inflation, which began to show up in the figures in April of that year – higher inflation meant higher interest rates were on the way. In the long run, that would be good for trusts like CQS New City High Yield as it fed through into the revenue account, but in the short term it meant higher yields and lower prices for the debt in the portfolio.

To mitigate against the risk of this the manager keeps the duration of the portfolio (a measure of time-weighted cashflows) relatively low. Issues with long maturities tend to be more volatile.

Mr Francis feels there is a risk that the UK economy enters a period of stagflation this year, and believes further UK rate cuts are possible. However, with the increasing likelihood that interest rates will stay higher for longer (or, perhaps more accurately, a return to conditions that prevailed over the decade before the financial crisis), Questor feels that CQS New City High Yield Fund will continue to offer attractive long-term returns.

London-based developer and manager of retail infrastructure – Swings to pretax profit of GBP8.2 million in half-year to September 30, from GBP2.6 million loss year-on-year. Net tangible assets per share fell to 106 pence at September 30, down 8% from 115p at March 31. NewRiver is cuts half-year dividend to 3.0p per share, versus 3.4p the year prior. Half-year revenue has drops to GBP31.8 million from GBP33.2 million last year.

BioPharma Credit PLC ex-dividend date Chelverton UK Dividend Trust PLC ex-dividend date CT UK High Income Trust PLC ex-dividend date CT UK High Income Trust PLC B ex-dividend date European Assets Trust PLC ex-dividend date European Smaller Cos Trust PLC ex-dividend date Finsbury Growth & Income Trust PLC ex-dividend date Henderson High Income Trust PLC ex-dividend date Lowland Investment Co PLC ex-dividend date Murray International Trust PLC ex-dividend date New Star Investment Trust PLC ex-dividend date Pollen Street Group Ltd ex-dividend date Real Estate Investors PLC ex-dividend date RIT Capital Partners PLC ex-dividend date Schroder Income Growth Fund PLC ex-dividend date Shires Income PLC ex-dividend date Smithson Investment Trust PLC ex-dividend date STS Global Income & Growth Trust PLC ex-dividend date VinaCapital Vietnam Opportunity Fund Ltd ex-dividend date

The company said a dividend of 1.5 pence per share was approved, in line with its 6.0p per share target for financial year 2025, up 3.4% from 5.8p a year prior.

Five ways to generate an income from your investments

Dan Coatsworth

Invest with AJ Bell

One of the key attractions of investments is the potential to earn a regular income, and for many people it’s the number one priority.

There isn’t a one-size-fits-all approach for income investing and product innovation in the asset management industry has increased the choices available to investors.

It’s important to understand the various strategies, how they work, and to whom they might appeal. Here are five of the most popular ones used today.

1. High yield

For decades, investors have looked to investment markets to see if they can find something that offers a better yield than available on cash in the bank. The current benchmark to beat is 5%, being the best-buy savings account rate. That might seem a high bar to clear, yet qualifying opportunities are widespread across stocks, bonds, funds and investment trusts.

The UK stock market is a treasure trove of high yielding stocks thanks to the plethora of low growth, yet highly cash-generative industries. Life insurance, tobacco and property feature heavily, with approximately one fifth of the FTSE 100 offering a prospective yield above 5%.

Investment trusts are also a popular hunting ground, with big yields from companies across the property, renewable energy and debt sectors.

While it is tempting to sit back and let the cash roll in, the income stream only forms part of the returns from an investment. It is important to also look at capital gains or losses.

There’s no point owning a share, trust or fund if you’re consistently losing more money than you make from dividends. Total return is a term that looks at both capital gains/losses and income, and the goal is for that figure to be positive on a long-term basis.

Yields can look high as a result of big share price declines. A falling share price reflects market concerns about something — such as tougher trading conditions or a lack of faith in earnings forecasts. If a company struggles for a long time, it might cut or cancel the dividend.

Just because an investment offers a high yield doesn’t mean that dividend is sustainable — in fact, the high yield could be a red flag. It’s as important to weigh up what could go wrong with an investment as what could go right.

2. Monthly dividend payers

People receive their salary like clockwork throughout their working life. While it’s reassuring to know that money is coming in on a regular basis to cover monthly bills, it can be a shock when someone retires and they no longer have that money topping up their bank account. Investments play a role in replacing that income — either selling small chunks to generate capital or, ideally, using dividends to pay the bills.

Individual stocks typically pay dividends twice a year but that frequency might not suit someone who has monthly bills to settle. An investor could create a portfolio with dividends trickling in across different months. Alternatively, there is a growing number of funds and investment trusts paying dividends monthly to investors.

3. Dividend Aristocrats

While income hunters may judge an investment on its dividend yield, it’s also worth considering dividend growth.

The cost of living typically goes up each year so it’s important that dividends grow at least in line with inflation to ensure you maintain spending power. The ability of a company to grow dividends each year can also be a sign it’s a high-quality business.

There are two ways to quickly identify investments with dividend growth. One is to look at investment trusts classified as ‘Dividend Heroes’ which are names that have consistently raised their dividends for at least 20 years in a row, including F&C Investment Trust and City of London Investment Trust.

The other is to look at tracker funds labelled as ‘Dividend Aristocrats’. This is a term to describe companies with a long record of raising their dividend each year, often by 25 years or more. The term will appear in the fund name, or sometimes you might see a variation such as ‘Dividend Leaders’.

There are us ETFs which track a basket of companies classified as Dividend Aristocrats in Europe and the US.

Not all investors need to take the income from their investments and they might choose to reinvest any dividends to enjoy compounding benefits. The prospect of owning an investment that aims to deliver consistent dividends or even dividend growth — such as Dividend Aristocrats – might appeal to them.

4. Enhanced income

Income-hungry investors are often happy to receive the bulk of their returns from dividends rather than capital gains. There is a specific type of fund that might appeal to this type of person.

Enhanced income funds (also known as ‘income maximiser’ funds) have a clever trick up their sleeve to boost their dividend power. They might generate a 4% or 5% yield from their underlying portfolio but have a neat way to pay even more to investors.

They sell call options on stocks held in the portfolio to generate additional income. These options are contracts that give the buyer the right, but not the obligation, to buy the underlying asset at a specific price on or before a certain date.

For example, an investment bank buys an option on Company X from an enhanced income fund for a fee. This entitles the investment bank to any rise in the price of the underlying share above a certain level over a set period, typically three months. The enhanced income fund uses the option fee to top up its dividends, but in doing so it sacrifices part of the capital growth from the stock holding.

Enhanced income funds might underperform traditional equity income funds when markets are rising but potentially outperform in a falling market.

Call options can be difficult to understand and charges on enhanced income funds are often much higher than a traditional equity income fund. That means these types of funds won’t suit everyone.

5. Blending income and growth

The blended approach of income and growth is increasingly popular with investors who want a happy medium of dividends and capital gains.

Someone in retirement looking to make their pension last longer might use this approach. So might an individual who wants their investments to grow and use cash from dividends to fund additional investments down the line.

Jonathan Maxwell, CEO of the Investment Manager, SDCL, said:

“SEEIT’s active management of the assets in its portfolio has delivered substantial income to the Company, in line with previous years. This stable performance ensures that we can cover the target dividend of 6.32p which represents a double-digit yield for investors at the current share price.

“We are confident that the portfolio is well positioned to maintain its performance and secure opportunities that are accretive to NAV. As the market challenges faced by SEEIT and its peers continue, our priority remains reducing the current discount to NAV. We are highly focused on preserving value and upside for shareholders, while at the same time considering ways to cut costs and find capital efficiencies at project and company level.”

Brett Owens, Chief Investment Strategist Updated: March 28, 2025

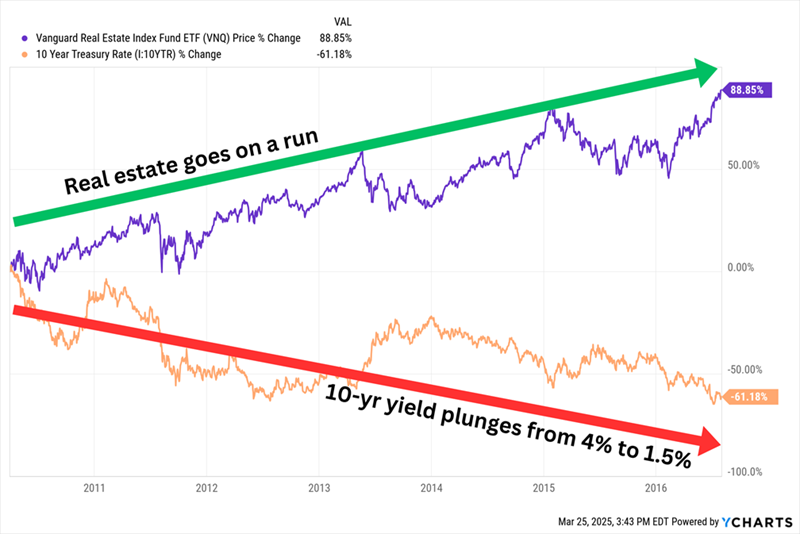

Interest rates are trending lower, which means real estate investment trusts (REITs) are rallying. These “bond proxies” tend to move alongside bonds and opposite rates.

If you believe the economy is likely to continue slowing, then select REITs are intriguing income plays here. Especially those yielding between 7.2% and 13.2%, which we’ll discuss shortly.

As I’ve been saying for a few weeks, the real story is in longer rates, namely the 10-year Treasury.

To recap, Treasury Secretary Scott Bessent has been upfront that he and President Trump are focused on the 10-year Treasury rate (the “long” end of the yield curve), and not the Fed benchmark (the “short” end).

That’s generally a boon for bonds and bond proxies (like preferred stocks, as well as certain equity sectors such as utilities). Naturally, lower 10-year yields will make REITs’ generous yields even more attractive, too, but in general, REITs have thrived much more often than not during periods of falling Treasury rates.

For example, let’s consider the 2010 to 2016 period in which the 10-year Treasury eased lower and lower:

REITs Rallied From 2010 to 2016

Of course we’re not looking to buy a pedestrian ETF. We are here for the dividends, the bigger the better! Our mandate is income so let’s review five REITs paying up to 13.2%.

Rayonier (RYN) Dividend Yield: 10.6%

This first name rarely shows up on lists of high-yield REITs, and for good reason! Its yield is artificially inflated right now.

Florida-based Rayonier (RYN) is a specialty REIT that boasts a little more than 2.5 million acres of timber-growing land across the U.S. South, U.S. Pacific Northwest and New Zealand. That land is used in forestry products such as paper, sure, but also a lot more: hunting, recreation, beekeeping, mineral exploration, and in some cases, even community development.

Some of those acres are going away. The company in March announced it would sell its entire 77% interest in a New Zealand joint venture for $710 million. That JV accounts for 70% of its total NZ acreage and all of its productive acreage.

This is just the latest sale in a massive “right-sizing” at Rayonier, started in 2023, meant to streamline operations and financial reporting, improve resource allocation and, in the case of the NZ disposition, reduce exposure to log export markets and focus on its lucrative U.S. acreage. Rayonier originally targeted $1 billion in asset sales, but once the NZ transaction closes, its total dispositions will be closer to $1.5 billion.

Why am I focusing on all this M&A? Well, for one, RYN is making itself more attractive operationally while also raising funds to reduce its leverage.

But it also speaks to Rayonier’s payout potential.

Rayonier pays a merely so-so regular dividend that yields 4%. But in January 2025, the company paid out a massive special dividend of $1.80 per share (+6.6% in additional yield)—after making $495 million in dispositions during the fourth quarter. That follows a smaller 20-cent special dividend in January 2024 in the wake of a smaller timberland sale.

In other words, it’s possible that another big windfall might be on the way for shareholders after its $710 million New Zealand asset dump.

Longer-term, a healthier operational base and a healthier balance sheet could free Rayonier up to improve its regular distribution. The chart shows that the regular dividend is declining by 5% for the March payment, but it’s not really a cut—RYN paid out 25% of its special dividend in cash, and 75% in new shares, so the lower payment is just an adjustment to account for 7 million-plus new shares issued.

Could We See 3 Special Dividends in 2 Years?

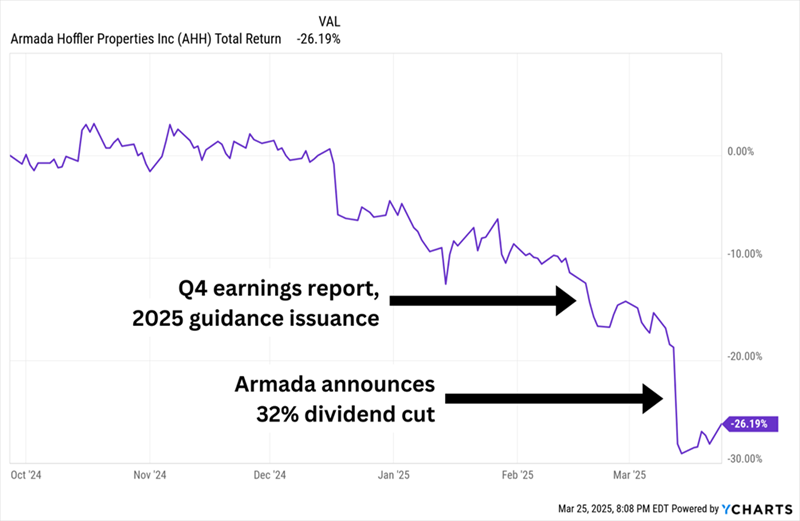

Armada Hoffler Properties (AHH) Dividend Yield: 7.2%

Armada Hoffler Properties (AHH) is a diversified REIT with 71 buildings. It gets the majority of its annualized base rent (ABR) from mixed-use office buildings (57%), with another quarter coming from mixed-use multifamily and the rest from mixed-use retail.

The last time I looked at Armada, in September 2024, it was yielding just a hair under 7%. Since then, the yield has ticked up to 7.2%. Unfortunately this is a case of a double dividend raise the “wrong way”—via a falling share price that sniffed out a payout cut!

Falling Price Sniffs Out Lower Payout

Armada looked like one of many real estate COVID bounceback stories. Occupancy was in the mid-90s. Same-store cash net operating income (NOI) was improving. It had recouped its dividend to near pre-COVID levels. Dividend coverage from adjusted funds from operations (AFFO) was a little tight but not sending out warning flares yet.

Still, I said AHH wasn’t yet an ideal situation.

In February, Armada delivered lousy guidance for 2025, expecting normalized FFO to decline anywhere between 15% and 22%. And in March, the company hacked its quarterly dividend by 32%, to 14 cents per share.

Armada had been working to improve its balance sheet, including reducing its exposure to variable-rate debt, and its guidance implied double-digit savings on general and administrative expenses. But tight coverage clearly was going to become undercoverage, so Armada pulled the trigger, with management noting the dividend would now be fully covered by “property income without any consideration of fee income.”

It’s possible AHH represents a healthier 7% yield today than it was last year, and because shares have fallen off a cliff, they trade at a cheaper 10 times starkly reduced AFFO estimates. But it’s a nonstarter without seeing more operational improvement first.

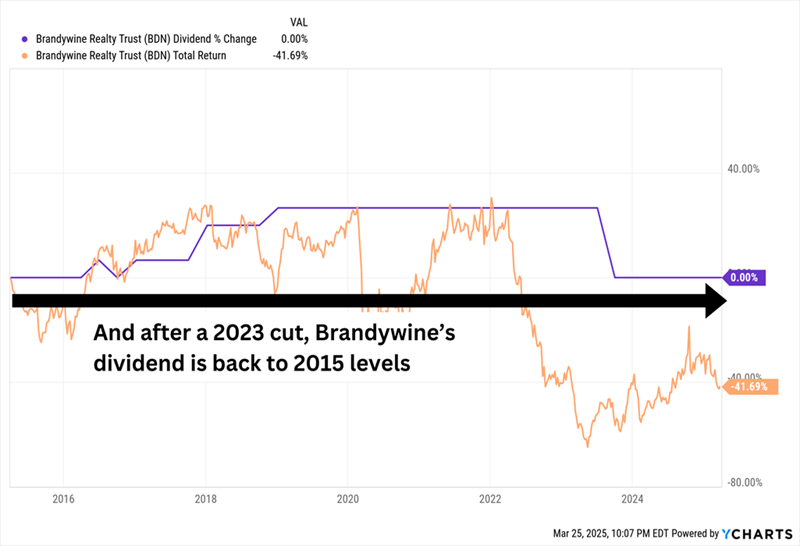

Brandywine Realty Trust (BDN) is another hybrid REIT with a heavy office bent, but large (and increasing) focus on residential and life sciences buildings. It’s also very acutely focused, with its 64 properties located in either greater Philadelphia or Austin, Texas.

I looked at it just a few months ago, it was trading at just 6 times FFO estimates. It’s trading at 7x now—but not because shares have improved. The company delivered a shoddy fourth-quarter report and disappointing guidance for 2025, and that has sent the stock back to the mat in 2025.

Brandywine’s wholly owned portfolio is performing decently. The problem is with its joint ventures. BDN is experiencing a heavy drag from its development projects. Some of its construction has been funded by expensive capital, and its arrangements with partners require Brandywine to recognize full interest and other costs until the projects become profitable. Estimates for JV FFO are tumbling as a result, and investors are responding by unloading shares.

Despite a massive 13% yield, we don’t want what they’re selling.

BDN’s Dividend Hasn’t Gone Anywhere. Its Stock Price Is Jealous.

Easterly Government Properties (DEA) Dividend Yield: 10.1%

Federal government housing, anyone?

Didn’t think so.

Easterly Government Properties (DEA) is an office REIT on the exact wrong side of DOGE. This REIT owns 100 properties that it leases out to U.S. government agencies such as Veterans Affairs, the FBI, and the Drug Enforcement Administration, among others. And its buildings go beyond offices, spanning outpatient facilities, warehouses, courthouses, labs, even built-to-purpose properties.

DOGE, however—which wants to boot federal employees by the tens of thousands and reduce real estate footprint—is problematic for DEA. Alas, there are a couple of hopeful points for longs.

For one, Easterly has offices in more than two dozen states, but it doesn’t own any property in Washington, D.C., where Elon Musk appears to be concentrating his focus for now.

But more importantly (and more of a complication): Much as it might want to, DOGE can’t just rip up real estate contracts. Instead, many real estate contracts the government does want to get rid of will likely just have to run their course—and in some cases, they might have a change of heart by then.

“Every year we give ideas to the U.S. government on how to improve a facility,” CEO Darrell Cratetold Institutional Investor. “With DOGE, people all of a sudden are receptive to ideas.”

While Easterly might defy the odds and not die by DOGE’s sword, this is a company that already had a longstanding problem consistently growing FFO. Hard pass on this double-digit divvie.

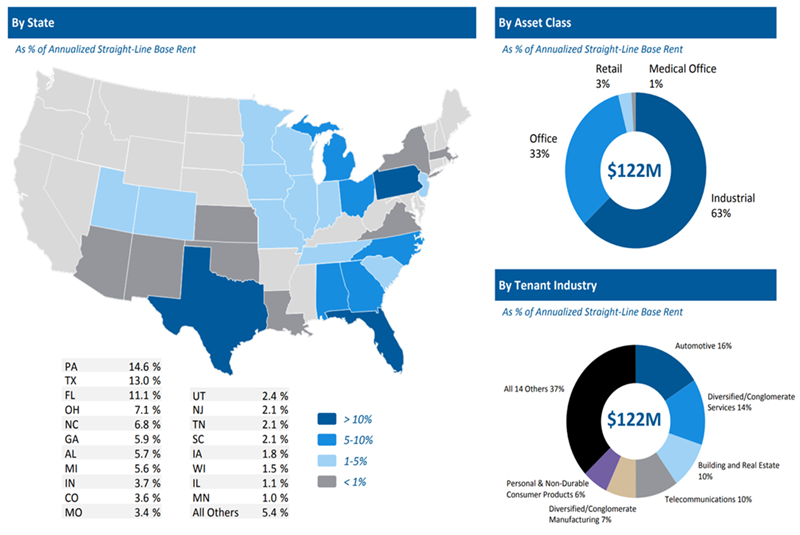

Gladstone Commercial (GOOD) Dividend Yield: 8.1%

Gladstone Commercial (GOOD) isn’t a spectacular prospect right this second. Acquisitions are few and far between, and growth has flatlined, with few immediate catalysts on deck.

But it might just be building itself into a potential long-term winner.

If “Gladstone” sounds familiar, that’s because GOOD is part of the Gladstone family of REITs and business development companies (BDCs), which also Gladstone Land (LAND) and Gladstone Investment (GAIN) and Gladstone Capital (GLAD).

Gladstone Commercial owns 135 single-tenant and anchored multi-tenant net-leased properties, leased out to 106 tenants across 27 states.

The biggest strike against Gladstone has long been its office properties. Weakness in offices forced GOOD to reduce its payout by 20% in 2023, and even today, office occupancy of 94.3% pales compared to its industrial occupancy of 99.4%.

Fortunately, Gladstone has been reducing that office exposure, which is now down to 33% of annualized straight-line base rent. Most of the rest is industrial, though it does own a little bit of retail and medical office real estate. I’d like to see it pare down even more of its office portfolio, but GOOD is being constrained by a weak market for sellers.

An Increasingly Diversified Portfolio: That’s GOOD!

In the meantime, Gladstone has been reducing leverage and producing results that have largely been in line with expectations.

Which, whilst it’s always a good time to be a dividend hunter, some times are better than other times.

The ‘unpleasant conclusion’ given by five key indicators

27 March 2025

AJ Bell’s Russ Mould explains what the outlook for the global economy is, after reviewing several important measures.

By Gary Jackson,

Head of editorial, FE fundinfo

Investors should keep a close eye on indicators such as transport stocks, small-caps and copper in order to gauge the possible direction of the economy and financial markets, according to AJ Bell.

The second presidency of Donald Trump in the US, coming after more than a decade of unorthodox monetary policy, failed attempts at austerity, ballooned government debt and the fallout of the Covid pandemic, means investors are split on whether the globe is headed into inflation, deflation or stagflation.

Russ Mould, investment director at AJ Bell, said: “All three of those potential endgames would require a different portfolio allocation, at least if history is any guide, with inflation perhaps leaning toward select equities and ‘real’ assets such as commodities, deflation favouring cash and bonds and stagflation, the worst of all worlds, putting gold and commodities (again) in the driving seat.”

To help investors guess what might be coming, AJ Bell offers up five indicators that can give a steer on what is happening in the global economy.

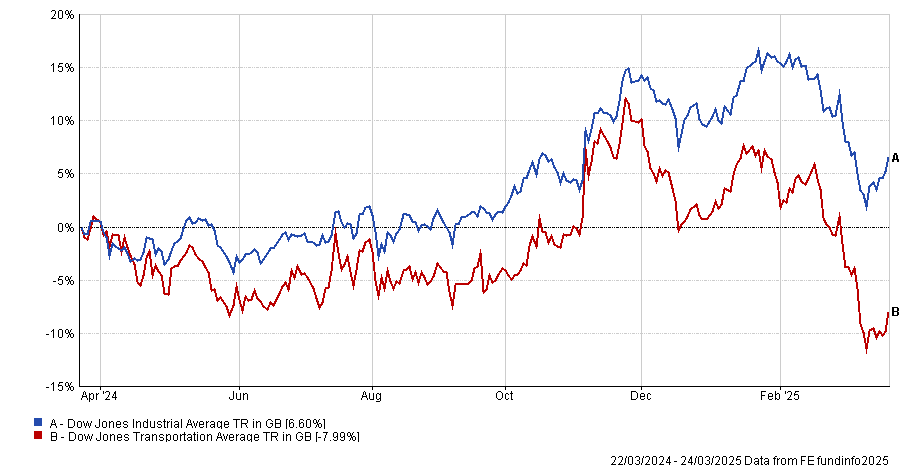

Transport stocks

Proponents of Dow Theory – which is a form of technical analysis derived from Wall Street Journal editorials of Charles H. Dow – watch transportation stocks as a bellwether of the wider economy.

Because a strong economy means there’s strong demand for goods, products need to be shipped from manufacturers to retailers and wholesalers to replenish shelves. Therefore, strong performance from freight, truck, airline and shipping companies suggests the economy is doing well.

Of course, the opposite also stands. If transportation companies are struggling, then it suggests diminishing economic activity.

Performance of Dow Jones Industrials and Dow Jones Transportation indices over 1yr

Source: FE Analytics

“It will therefore be of some concern to bulls of US stocks to see the Dow Jones Transport index slide by 18% from last November’s high, to leave it on the fringes of bear market territory,” Mould said.

This could indicate that the US is moving towards slowdown or recession.

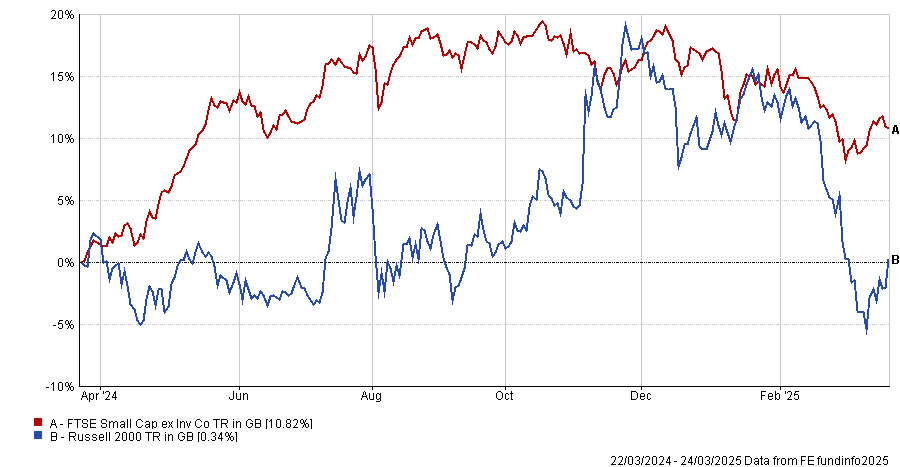

Small-caps

The small-cap Russell 2000 index initially rallied after Trump won the 2024 election but, like the transportation index, is currently pointing to a slowdown or recession.

UK small-caps paint a similar picture.

Performance of US and UK small-caps over 1yr

Source: FE Analytics

“Small-cap companies tend to be less well-resourced than their multi-national, mega-cap peers, and are often more dependent upon their domestic economy as a result,” Mould said.

“As such, they can be seen as a guide to trends in local output, so the slide in market minnows on both sides of the Atlantic could be seen as a harbinger of an economic slowdown.”

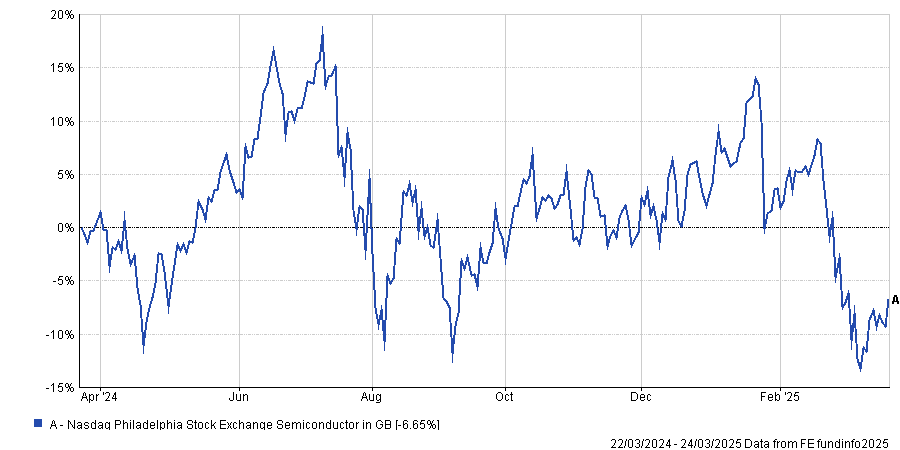

Semiconductor stocks

The AJ Bell investment director also argued that silicon chip and semiconductor production equipment (SPE) manufacturers can also be a useful economic indicator. Silicon chips are widely used in electronic devices ranging from smartphones to cars to servers, meaning they are in demand from every part of the economy.

Although the industry’s annual sales are expected to reach a new all-time high of almost $700bn this year, it’s worth remembering that it is cyclical. Semiconductor stocks often experience booms driven by spikes in demand from new applications followed by busts, as output slows because of a wider economic slowdown.

Performance of Philadelphia Semiconductor index over 1yr

Source: FE Analytics

“The Philadelphia Semiconductor index, known as the SOX, consists of 30 major silicon chip and SPE specialists,” Mould said.

“It may be a source of discomfort to bulls to see the benchmark sit below where it lay a year ago, for all of the hoopla surrounding AI and the SOX has dropped to more than a fifth below last summer’s peak – bear market territory.”

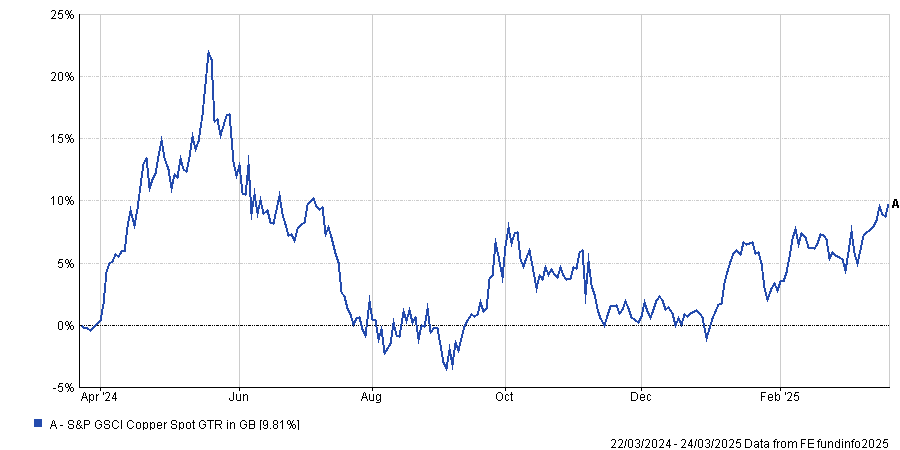

Copper

Copper is used in many parts of the economy, from white goods to cars to construction. Because of this, it is often seen as a good guide to global economic health – so much so that its nickname is ‘Doctor Copper’.

Copper prices fell in 2024 on the back of China’s real estate bust but have bounced back this year. AJ Bell said the rally could be bolstered by more monetary and fiscal stimulus from Beijing as well as Germany’s proposals for debt-funded growth.

Copper over 1yr

Source: FE Analytics

However, part of the rise in demand could be copper traders buying up supplies in case the metal is subject to US tariffs. It could also be investors buying up real assets to protect against inflation or stagflation.

As such, Mould thinks the copper price could be indicating growth or higher inflation from here.

Government bonds

Interest rates have been trending downwards across the globe, with 193 rate cuts from central banks in 2024 and another 31 so far this year. However, 10-year government bond yields have not moved lower in anticipation of more to come, as might be expected.

This dynamic could be explained by worries over increased supply of government debt and concerns over the potentially inflationary impact of the US’s tariffs, according to Mould.

AJ Bell said bond yields seem to be pointing to inflation or stagflation.

10yr government bond yields

Source: LSEG Refinitiv data

Mould finished: “The unpleasant conclusion from these five trends is that the global outlook is deviating from the one which markets priced in so enthusiastically in 2024, namely a return to the low growth, low inflation, low interest rate world that had worked so well for bonds and long-duration assets such as technology stocks during the 2010s and early 2020s.”

He offered one final indicator that investors might want to keep an eye on: “If the environment really has changed – and we are now in an era of inflation or stagflation and not the low-growth, low-rate, low-inflation murk that dominated in the wake of the financial crisis – then it could just show up in how the CRB Commodities benchmark does relative to the S&P 500. Such a dramatic change may just favour commodities, at least if the experiences of the 1970s are any guide.”

A case study of Trusts added to the Watch List, starting with Property shares as that is where the market’s interest is at the moment. Not a recommendation to buy just posted in alphabetical order for you to DYOR.

As always timing and then time in if you want to GRS.

AEW UK REIT plc

NAV Update and Dividend Declaration

AEW UK REIT plc (LSE: AEWU) (“AEWU” or the “Company”), which directly owns a value-focused, diversified portfolio of 32 UK commercial property assets, announces its unaudited Net Asset Value (“NAV”) at 31 December 2024 and interim dividend for the three-month period ending 31 December 2024.

Highlights

· NAV of £174.30 million or 110.02 pence per share at 31 December 2024 (30 September 2024: £172.76 million or 109.05 pence per share).

· NAV total return of 2.73% for the quarter (30 September 2024 quarter: 4.85%).

· 1.22% like-for-like valuation increase for the quarter (30 September 2024 quarter: 2.94% increase).

· EPRA earnings per share (“EPRA EPS”) for the quarter of 2.35 pence (30 September 2024 quarter: 2.68 pence).

· Interim dividend of 2.00 pence per share for the three months ended 31 December 2024, paid for 37 consecutive quarters and in line with the targeted annual dividend of 8.00 pence per share, representing a dividend yield of 7.9%.

· Loan to GAV ratio at the quarter end was 25.03% (30 September 2024: 25.04%). Significant headroom on all loan covenants.

· Company continues to benefit from a low fixed cost of debt of 2.959% until May 2027.

· Disposal of Units 1-11 of Central Six Retail Park, Coventry, for £26,250,000, reflecting a net initial yield of 7.49% and a capital value of £213 per sq. ft, representing a 60% premium to the purchase price.

Henry Butt, Assistant Portfolio Manager, AEW UK REIT, commented:

“We are pleased with the growth in NAV per share and the dividend being covered by EPRA earnings for a third consecutive quarter, which continues to evidence the earnings accretion produced by the Company’s programme of ongoing asset management initiatives through income generation and void cost mitigation. Rental income has been buoyed by the billing of annual turnover rent for Next in Bromley, and Poundland in Coventry, while the Company’s ‘bottom line’ continues to benefit from a stabilised portfolio and tenant base.

The part sale of Central Six Retail Park, Coventry, at a very healthy premium of 60% to the purchase price, means the Company has capital to deploy on a pipeline of attractive investment opportunities, a significant amount of which is already under offer.

The Company has committed to pay its quarterly dividend of 2.00 pence per share, which has now been paid for 37 consecutive quarters.”

20/01/25

AEW UK REIT plc

Acquisition of high-yielding asset in affluent town

AEW UK REIT plc (LSE: AEWU) (“AEWU” or the “Company”) is pleased to announce that it has completed the purchase of a freehold, high-street retail asset at 13/13A, 114-119, 121-123 Bancroft and 3-4 Portmill Lane (the “Property”) in the affluent commuter town of Hitchin for £10,000,000. The purchase price reflects an attractive net initial yield of 8.31% and a capital value of £213 per sq. ft.

The Property, located in the centre of Hitchin’s high-street retail pitch, provides 46,905 sq. ft. of space across 12 retail units and a standalone office building, as well as car parking and service yards. The retail elements of the Property are fully let to a strong line up of 12 tenants, with recent leasing activity evidencing the strength of the location. Major tenants include Marks & Spencer plc, Next Holdings Ltd, Vodafone Ltd, The White Company and Holland & Barrett. The vacant office element to the rear provides various asset management options in the short-to-medium term, including new lettings or residential conversion.

Hitchin is a busy market town located in Hertfordshire with an affluent catchment. The town is served by rail connections to both London and Cambridge, underpinning its attractiveness as a commuter location.

The acquisition demonstrates the Company’s swift and ongoing redeployment of sale proceeds from the recent disposal of Central Six Retail Park in Coventry, with a significant amount of the remaining proceeds also under exclusive negotiation. In considering the re-deployment of the proceeds from Central Six, the Company has identified an attractive pipeline of investments available for purchase in the current market and is considering available growth opportunities for further earnings accretive acquisitions.”

Commenting on the purchase, Laura Elkin, Portfolio Manager of AEW UK REIT said: “We are delighted to have purchased this well-located asset at a day one yield that will enhance the Company’s earnings. Completing this acquisition marks a significant milestone in our strategy to reinvest capital generated from the recent successful sale of our retail park in Coventry into higher-yielding and value-add assets. We continue to actively monitor a pipeline of attractive potential investments, and believe the Company is well positioned to focus on the growth of the portfolio should the right earnings accretive opportunities arise.”