Dividend Wealth Journal: REITs and Interest Rate Cuts, A Double Dipping Opportunity

Hey folks, over the weekend I mentioned how dividends can be great for “Double Dipping” when you play them right.

In other words, buying a stock that gains value in your portfolio and collecting passive income along the way.

I want to follow up with a specific opportunity that could be primed over the next few months for a double dip.

With the recent talks and actions around interest rate cuts, the spotlight is once again turning towards Real Estate Investment Trusts (REITs).

Lower interest rates often breathe life into the real estate market, making REITs increasingly attractive (and potentially more profitable once again) for investors.

Why do lower interest rates matter for REITs?

Interest rate cuts have a direct impact on the real estate sector. Lower borrowing costs can lead to an uptick in purchasing and development activities, directly benefiting REITs that hold or manage these properties.

As financing becomes cheaper, properties in the portfolios of REITs may increase in value, and their income potential can improve due to higher occupancy rates and rising rents.

The infusion of lower rates can turn the REIT market bullish in several ways:

Enhanced Property Values: As more investors and businesses find it affordable to finance real estate purchases or expansions, the demand drives property values up.

Increased Occupancy and Rent: Lower interest rates generally boost economic activity… This leads to higher demand for both commercial and residential real estate. This increases occupancy rates, allows for rent hikes, and boosts REITs profits.

Double Dipping Opportunity With those tailwinds giving REITs an opportunity to gain in underlying value, the next cycle of rate cuts present a unique “double dip” opportunity. But how? •Dividends: REITs are required by law to distribute at least 90% of their taxable income to shareholders in the form of dividends, offering investors a steady income stream. •Capital Appreciation: As the underlying properties appreciate in value due to increased demand and higher rental incomes, the value of the REITs themselves soar. This scenario allows investors not only to enjoy solid dividends but also to benefit from the appreciation of the stock itself.

For dividend investors looking to leverage these benefits, considering REITs in sectors that are most sensitive to interest rate changes, like residential and retail, or those focused on regions with growing economies, might be particularly lucrative for this double dipping strategy.

But, as always, the key to capitalizing on these opportunities lies in choosing solid dividends, specifically ones with strong fundamentals, strategic property holdings, and a solid leadership team.

As interest rates decrease over the next year and a half, the relationship between interest rates and the real estate markets will grow increasingly important.

We haven’t seen a great opportunity for real estate to gain inflows since 2020 when it took off, so now could be another double dip run.

pttogel Thanks , I’ve recently been looking for information about this subject for ages and yours is the best I’ve came upon till now. But, what in regards to the bottom line? Are you positive concerning the supply ?

£££££££££££££££

Yes, there are currently 35 Investment Trusts paying a ‘secure’ yield above 7%, remembering that nothing is ever 100% secure.

7% re-investment is important as it doubles your income in ten years.

There is normally Trusts that the market have sold, for various reasons and u only need one to re-invest in.

The Snowball is currently not buying any new positions but re-investing in the portfolio to increase the income.

If there are no Trusts to buy at 7% or above, the current portfolio shares are trading at a blended discount of 30%, u would have funds to re-invest as well as your income. The income target is secure although u would have to extend the time line.

As the price rises the yield falls and vice versa.

The rules for any new readers, there are only three.

Buy Investment Trust that pay a ‘secure’ dividend to buy more Investment Trust that pay a ‘secure’ dividend.

Any Investment Trust that drastically changes its dividend policy must be sold even at a loss.

Remember the rules.

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors.

As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

The emotional benefits of dividend re-investment. In fact, with this investment strategy you can actually welcome falling share prices.

There seems to be some perverse human characteristic that likes to make easy things difficult. Warren Buffett

Vanguard economic and market update: Fed rate cut signals confidence

Vanguard’s latest economic and market update, including our outlook for growth, inflation and interest rates.

Shaan Raithatha Senior Economist

Key points

The US Federal Reserve has cut its policy interest rate for the first time in four years, by 50 basis points.

The euro area, already in the midst of a policy easing cycle, is seeing growth after stagnation in 2023.

In the UK, an uptick in services inflation meant the Bank of England did not cut rates at its September meeting.

The US Federal Reserve (Fed) has cut its federal funds rate for the first time in four years. The move signals the Fed’s confidence that US inflation is slowing, as well as a shift in focus to shore up the weakening US labour market. In kicking off its easing cycle, the US now joins the euro area and UK, where central banks had already begun cutting policy rates.

While the US, euro area and UK are seeing varying degrees of economic health, China may struggle to meet its growth target given lacklustre domestic demand. A strong, timely policy response will be required.

United States

The Fed cut its policy interest rate by 50 basis points (bps)1 but did so in the context of economic resilience rather than concerns about a material slowdown.

The Fed’s decision, announced on 18 September, marked a strong start to its easing cycle. The 50-bps reduction in the federal funds rate indicates a target range of 4.75%-5%. The Fed had resisted cuts at previous meetings, which allowed monetary policymakers to see more evidence of slowing inflation and gave them the confidence to cut by 50 bps rather than 25 bps.

At the midpoint of the year, GDP growth was tracking largely in line with Vanguard’s 2% outlook for 2024. The US economy grew more in the second quarter than previously thought, with real GDP rising by an annualised 3%. Strong consumer spending contributed to the growth.

The pace of headline inflation, as measured by the consumer price index (CPI), slowed again in the year to August to 2.5% compared with 2.9% in the year to July. Core CPI, which excludes volatile food and energy prices, rose by 3.2% in the year to August, little changed from July.

Recent data suggest softening in the labour market. There was a second consecutive month of below-consensus job growth, coupled with a recent pattern of downward revisions to already-announced totals. We expect job growth continuing to slow amid moderating economic activity, with the unemployment rate ending the year marginally above current levels (4.2% in August).

Euro area

The euro area is growing after stagnation in 2023. We expect steady—but not spectacular—growth in 2024 as restrictive monetary and fiscal policy constrain activity.

The European Central Bank (ECB) announced a 25-bps cut to its policy rate on 12 September. The decrease in the deposit facility rate, to 3.5%, was the second cut of a cycle that began in June with a similar 25-bps cut. Vanguard does not expect a further cut at the ECB’s October meeting, although we anticipate the easing cycle will resume with a 25-bps cut in December, followed by a quarterly cadence of 25-bps reductions in 2025.

The euro area economy grew again in the second quarter, with real GDP rising by 0.2% compared with the first quarter. This was despite an unexpected drag from Germany, where a rebound in the manufacturing sector remains elusive.

The pace of headline inflation slowed in August, driven by a drop in energy prices. Headline inflation slowed to 2.2% in the year to August—the slowest in three years—compared with 2.6% in the year to July. Core inflation, which excludes volatile food, energy, alcohol and tobacco prices, slowed marginally in August; however, services inflation remained sticky.

The unemployment rate returned to a record low of 6.4% on a seasonally adjusted basis in July, falling from 6.5% in June. We foresee little change to the unemployment rate into year-end.

United Kingdom

In the UK, the Bank of England (BoE) held rates steady at 5% in September after initially cutting in August. We expect rate cuts to resume in the fourth quarter and believe rates will end the year at 4.75%.

The BoE’s decision to keep rates unchanged reflects that risks to resurgent inflation remain, although services inflation, pay growth and GDP data have all undershot expectations since the bank’s last meeting.

GDP growth increased by 0.6% in the second quarter compared with the first. We expect the UK economy to moderate in the second half the year, growing by 1.2% for all of 2024.

The pace of headline inflation held steady at 2.2% in the year to August. Meanwhile, core CPI, which excludes volatile food, energy, alcohol and tobacco prices, jumped to 3.6% in the year to August, compared with 3.3% in the year to July. Vanguard expects core inflation to end 2024 around 2.8% and to hit the BoE’s 2% target by the second half of 2025.

Wage growth cooled to its slowest pace in more than two years in the May-July period, even as the unemployment rate fell to 4.1% and job vacancies decreased for a 26th consecutive reading during that period. We foresee the unemployment rate ending 2024 in the 4%-4.5% range.

China

Sluggish domestic demand has put China’s 2024 growth target of 5% at risk. Fiscal policy in the form of increased government loan issuance in August provides hope, but more of the same will likely be required in the months ahead.

Government loan issuance totalled 900 billion yuan in August, a significant ramp up compared with the 260 billion yuan issued in July. In order for the government to hit its 5% growth target for 2024, this is the type of timely policy response that will be required. On the monetary policy side, we expect the start of the Fed’s rate-cutting cycle could give the People’s Bank of China (PBoC) room to cut as well.

GDP grew by only 0.7% in the second quarter compared with the first and by 4.7% compared with the second quarter last year. Weaker-than-expected retail sales and industrial production figures suggest that China’s growth momentum slowed in August.

The pace of inflation, as measured by consumer prices, rose 0.6% in the year to August, below expectations and well below the 3% inflation target set by the PBoC. We expect inflation in 2024 to be mild, with headline inflation of 0.8% and core inflation, which excludes volatile food and energy prices, of just 1.0%.

The unemployment rate rose to 5.3% in August from 5.2% in July. Vanguard expects that rate to remain around current levels for the rest of the year.

The points above represent the house view of the Vanguard Investment Strategy Group’s (ISG’s) global economics and markets team as at 19 September 2024.

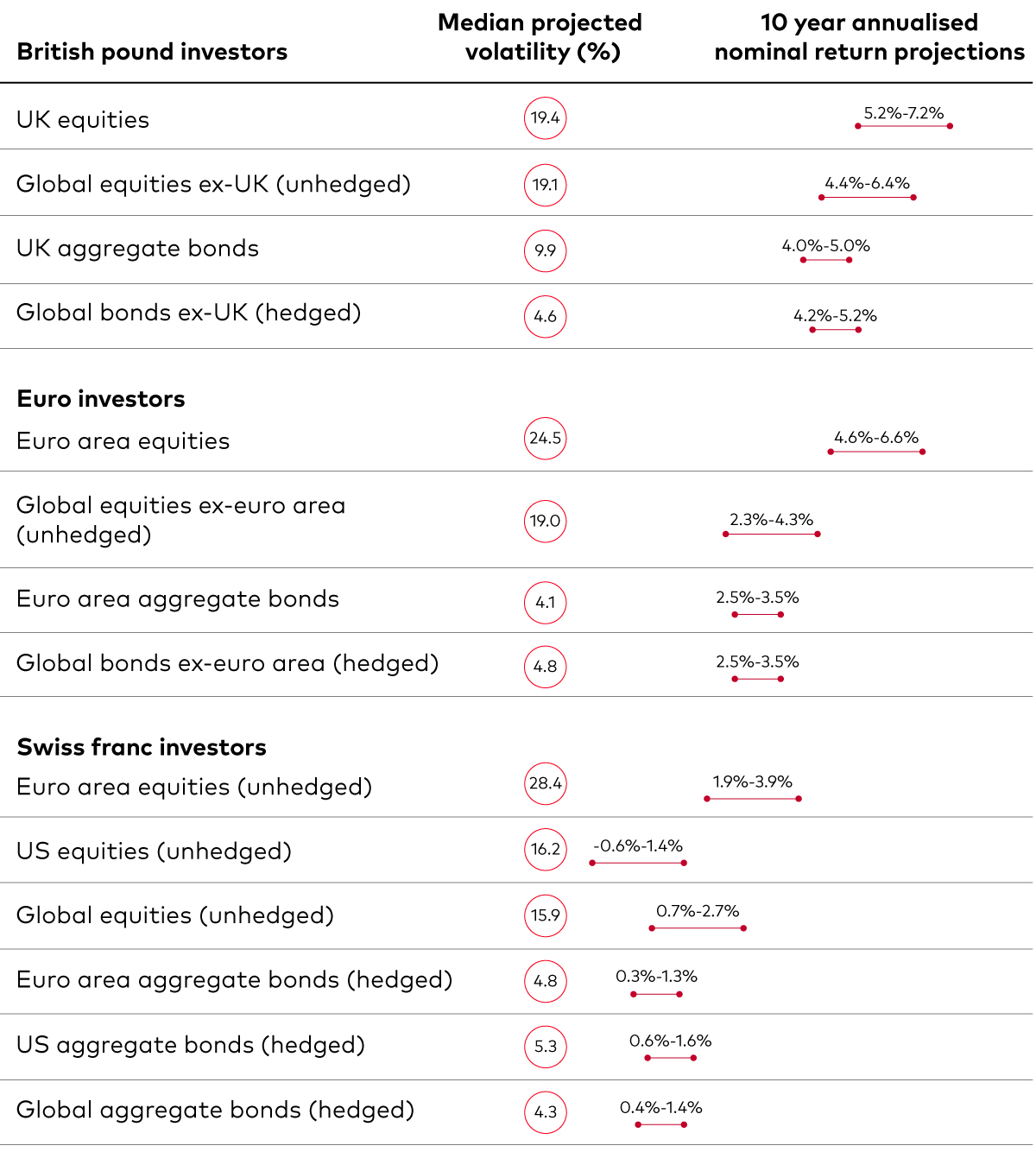

Asset-class return outlook

Vanguard has updated its 10-year annualised outlooks for broad asset class returns through the most recent running of the Vanguard Capital Markets Model® (VCMM), based on data as at 30 June 2024.

Our 10-year annualised nominal return projections, expressed for local investors in local currencies, are as follows2.

It’s likely they will continue to pay a gently increasing dividend but could be taken over but as the discount to NAV is 17%. U would then have to buy another IT with the profits but u can only control what u can control.

If the price rises the yield falls, so u may decide to re-invest the dividends elsewhere or even better spend them in your local Supermarket.

In twelve years time, most probably less, u have received all your cash back and now have a share yielding income at zero cost.

The holy grail of investing, not dependent on a rising market. If markets fall u could re-invest the dividends back into SUPR to earn even more income.

Other Trusts are available so not a recommendation to buy but as always best to DYOR.

Understanding when to retire, and how much money to take out of your pension to give you a reliable stream of income, is crucial.

Moneyweek

That is especially important as the cost of retirement is rising.

The latest research from the Pensions and Lifetime Savings Association, a trade body, suggests retirees need an income of £43,100 per year for a “comfortable retirement”.

Can applying the 4% pension rule help? We explain what it is and how it works.

What is the 4% pension rule? A popular rule for pension savers is to take 4% of their fund in the first year of withdrawals and increase that by the rate of inflation each year. This is supposed to last a typical retiree 30 years.

Academics at the American Association of Individual Investors devised the 4% rule in 1998 after researching a sustainable withdrawal rate for a retirement pot that wouldn’t deplete the savings.

It looked at data from 1926 to 1995 and found that a rate of 3-4% is “extremely unlikely to exhaust any portfolio of stocks and bonds”.

Can I rely solely on the 4% rule? Like all rules of thumb, says John Corbyn, pensions specialist at the wealth manager Quilter, the 4% concept is based on certain assumptions.

“It needs to be overlaid with someone’s state of health and propensity to spend, which is likely to be higher for younger clients and lower for older clients,” he says.

“Care needs to be taken to ensure the attitude to risk and propensity for loss is also built into these assumptions.

“Depending on your risk tolerance, investment strategy, and the actual returns you get, you might consider a slightly more conservative withdrawal rate.”

Corbyn says it is crucial to continuously review and adjust your strategy based on your actual investment returns, spending needs, and the broader economic landscape.

“Ultimately, pensions are a long-term savings vehicle and potentially may need to pay for someone’s income for up to 30-40 years, and care needs to be taken if the fund is accessed early, as short-term gain may lead to long-term pain so getting advice is key,” he adds.

Joshua Gerstler, chartered financial planner for The Orchard Practice, says that while the 4% rule is a good guide, in reality our spending patterns are not linear.

“We might want to spend more in the early years of retirement, for example, to travel around the world,” he says.

“Our spending may slow down as we get older and are less able to get out and about. Albeit this could be offset by an increase in care fees. If you have a financial plan then you will have a good idea of how much you can access without ever running out of money.”

It’s important to note that this strategy may not work for everyone and is just one of many factors to consider when retiring.

Make a retirement plan What you plan to do with your retirement will also have a huge impact on when you should start accessing your pension pot, so it’s a good idea to know what you want to do and the costs of doing it.

“If you have dreams of travelling the world then you might need much more retirement income than if you are content with a quiet life at home,” says Corbyn.

“It’s essential to have a realistic projection of your monthly and yearly expenses, including contingencies for unexpected costs.

“Financial planners can help produce cashflow models that look at your holistic finances and show you how much you can expect to have and what kind of retirement lifestyle that will buy you.”

The importance of timing when retiring You can’t help when you were born but it is worth thinking about when you start accessing your pension pot as market returns will have an influence on the success of the 4% rule.

Investment firm Fidelity recently attempted to see if the 4% rule had stood the test of time.

One major factor was timing.

It looked at the value of two £100,000 funds after 15 years – one starting in 2000 and one in 2003.

Despite there being just three years between their start points, the pot beginning in 2003 grew to be more than two-and-a-half times bigger than the pot beginning in 2000.

This is because the pot being accessed in 2000 was hit by the dotcom boom, so there wasn’t an opportunity to make up for these losses, while the 2003 pot benefited from the post-crash recovery.

Ed Monk of Fidelity suggests building flexibility into the strategy so you can avoid the worst time to sell your investments.

“Another tactic is to tweak your withdrawals in periods of falling markets so that you take just the income that is produced naturally from investments,” he says.

“This might include the dividends from company shares, income from funds or the interest from bonds. This might mean a lower level of income overall, but it means you won’t need to sell assets when their price has fallen.”

If you’re retiring in a period of economic downturn, adds Corbyn, it may be wise to be more conservative with withdrawals, at least initially.

Gerstler suggests it is also important to consider other savings and investments held outside of pensions as part of your whole retirement strategy.

Don’t forget about tax Whatever rule you use, experts say it is always important to consider the tax implications.

This is because beyond the 25% tax-free lump sum, you will need to pay income tax on withdrawals if you are earning above the tax-free personal allowance.

The 4% rule analysis doesn’t include a cash buffer but it is recommended that you have 3 year cash buffer in place just in case markets crash just as you start to withdraw your hard earned.

Here’s how I’d use the next stock market correction to try and aim for a million — with £30K Story by Christopher Ruane

When the stock market falls, that might seem like bad news for investors.

The reality, though, is that a falling stock market can be bad or good depending on how one reacts to it. For a canny investor, a stock market correction or crash can offer the opportunity to buy into some great companies at a cheaper price than before.

For now, the stock market continues to do well. The UK’s flagship FTSE 100 index has hit an all-time high this year. It is currently around 2% below that all-time closing high.

But sooner or later, as history shows us, there will be a stock market correction. Here is how I would use that to try and turn a £30k sum into a portfolio worth a cool million pounds down the line.

Taking advantage of weak prices

Imagine that I invest in a share portfolio that, on average, grows in price at 5% annually and has a 7% dividend yield. That is equivalent to a 12% compound annual gain.

Now imagine that a stock market correction sees that selection of shares fall by 15%. If I bought then, that 5% annual price gain would end up being a 5.75% annual price gain thanks to my lower purchase price.

Meanwhile, the average dividend yield would not be 7% but 8.05%, again thanks to my lower purchase price. So my compound annual price gain would be 13.8%.

This is where the long-term benefit of compounding really shines through. Compounding £30k at 12% annually, my portfolio would be worth over a million pounds after 31 years. At the higher 13.8% rate, though, hitting the million pound mark would take 28 years.

Getting ready now to hunt for bargains in future ?

Remember, this example presumes I spend the same amount buying the same shares. The only difference between the two scenarios is that in one I buy before a 15% price fall and in the other, afterwards. In a stock market correction, some individual shares may fall a lot more than that, giving me even more scope to scoop up bargains.

But just because a share falls does not mean it is cheap.

I still need to focus on quality – and in the midst of a market meltdown I might not have enough time to do the research. That is why I am updating my share watchlist now, to get ready to move when the next stock market correction comes.

One name on it is M&G (LSE: MNG).

During the 2020 stock market crash, the M&G share price fell sharply. If I buy it today, I could earn an already juicy 9.5% yield. But if I had snapped up the share at its 2020 low, I would now be earning a yield of over 18% annually!

With a customer base in the millions, strong ongoing demand for asset management, and a strong brand, I think the company is set for ongoing success. One concern is what the firm this month termed “elevated” geopolitical risk that threatens economic stability and investor confidence.

But, if the next stock market correction lets me snap up more M&G shares at a bargain price, I plan to.

The post Here’s how I’d use the next stock market correction to try and aim for a million — with £30K appeared first on The Motley Fool UK.

C Ruane has positions in M&g Plc. The Motley Fool UK has recommended M&g Plc. Views expressed on the companies mentioned in this article are those of the writer.

Financial myths that are told for the benefit of someone but not necessarily yours.

One.

Hold shares for a minimum of 5 years

A long time to wait to find you are long and wrong.

Two.

Buy an Annuity

Single life annuity at age 65, each £100,000 in your pension pot will give you a guaranteed annual income of around £4,968 a year, according to the Hargreaves Lansdown online annuity quote tool. That is a “level” income and will not rise in line with price inflation. If you want your annuity income to rise by 3 percent a year, your starting income in the first year will fall to just £3,282. Oct 2021

A huge gamble with your life long savings, at least Dick Turpin had the decency to wear a mask.

Buy an annuity.

Three.

Government bonds are a safe investment.Lifestyling

The Telegraph

A global rout in bond markets has unleashed chaos on British savers pension pots, forcing thousands to choose between delaying retirement or crystallising huge losses in their lifetime savings.

The value of American and British government bonds has been caught in a downward spiral this year, following a strong run of economic data and signs from the American central bank that it will keep interest rates higher for longer.

Bond prices typically fall when interest rates rise, because investors begin to ask for much higher yields to compete with a higher risk free rate. When prices fall, yields rise.

This has proved disastrous for millions of British pension savers who have been lifestyled toward a bond heavy portfolio.

Defined contribution pensions, which invest in stock and bond markets, change the way your savings are invested as you approach retirement if you are in the default funds.

Lifestyling typically involves moving money from stocks to bonds, as they are perceived as lower risk. However, for the past two years this has failed to protect savers pension pots as they approach retirement, following major sell-offs in bond markets.

He said: Pension providers created this method because people used to buy an annuity when they reached retirement, which are priced according to gilts.

But for most of the past decade annuity rates have been really poor. They have become much more popular in recent months, but still the majority of people just go straight into drawdown.

A pension enters into a drawdown when savers keep their money invested in the stock and bond markets, but begin to take an income from their pot.

Mr Cook said: Most workplace pension schemes follow the default option of moving their older savings to bonds and this has had a catastrophic effect because of the sell off.

Some clients have either had to piecemeal move their money back into the market, because they had been lifestyled out without realising. Others have had to delay their retirement or accept a much lower income.

For example, the pension provider Aegon automatically switches some of its savers in its default pension into its Scottish Equitable Retirement plan when they are one year away from their target retirement date.

The plan, which is invested heavily in gilts and cash, has lost savers 7pc in the past year alone. In the past three years, it has dropped by 41pc.

Retirees who manage their own money in self-invested personal pensions or a Sipps have also been caught out.

For example, the Vanguard LifeStrategy 20pc Equity fund, which has 80pc invested in bonds, has delivered the worst return across the range over the past two years, at a loss of 13pc. The LifeStrategy 80pc Equity fund, which only has 20pc bonds, is flat.

Doug Brodie, of the financial adviser Chancery Lane, argued the 60/40 strategy, which encourages investors to invest two-fifths of their portfolio in bonds, was in urgent need of reform.

The blind following of this mantra has come home to roost, he said. Since the beginning of the pandemic, US Treasury bonds over 10 years have collapsed by 46pc. To give some perspective, in the dot com crash stocks fell by 49pc.

The core difference is that equities simply jumped back up. You are not going to see that with bonds, it’s going to be a long and slow recovery.

The reason pension providers have invested so much in bonds is because they are usually less volatile, and because they are legally obliged to pay an income. With shares in companies, the dividends are discretionary.

Overall only around 10pc of our money is in fixed income. We are very cautious about funds that invest in bonds because unless they are hugely diversified we do not think it is worth the risk, and by that point you may as well just sit in cash anyway because at least you know you will not be clobbered by higher interest rates.

But this will offer little comfort to workers who are holding on for the right time to retire, especially those in Britain whose savings are more concentrated in the gilt market. It could take more than a decade for gilts to recover from this properly, Mr Cook said. We just do not know.

Oh my goodness! an amazing article dude. Thank you However I am experiencing concern with ur rss . Don’t know why Unable to subscribe to it. Is there anybody getting equivalent rss downside? Anybody who is aware of kindly respond. Thnkx

11 trusts saw their share prices trade at year-high discounts last week, but which one may well not feature in the next Discount Watch after a strong share price bounce? More importantly, what seems to have triggered the share price recovery?

By Frank Buhagiar•23 Sep, 2024

We estimate 11 investment companies saw their share prices trade at 52-week high discounts over the course of the week ended Friday 20 September 2024 – one less than the previous week’s 12.

No less than eight of the eleven 52-week high discounters featured in the previous week’s list. Among the eight is Vietnam Enterprise (VEIL). Chances are though the £1billion market cap won’t be in next week’s Discount Watch. That’s because the share price has since bounced strongly off the year-high discount that had been set on 18 September. The next day, the shares added 10p to close at 578p and, by the end of the week, had tacked on a further 6p to close at 584p. That was enough to narrow the discount to -20.93% from 22.93% two days prior.

The reason behind the share price bounce, well the 50-basis point cut in US interest rates, is the obvious choice – lower US rates reduce the cost of borrowing in US dollars, thereby easing liquidity conditions, while lower yields on US assets make those of other assets more attractive. The US interest rate cut may be the obvious choice but, in this case, it might not be the correct one. For the Federal Reserve cut rates on 18 September, but that was the day VEIL’s share price discount to net assets hit its 52-week high. Compare that to peer VinaCapital Vietnam Opportunity’s (VOF) share price – the discount narrowed on the day of the cut to -22.62% compared to -23.79% the day before. So, VOF saw a bounce on the day of the US cut, whereas VEIL’s discount actually widened, and that was despite the trust buying back its own shares that very day.

Another explanation is required. And there is one easy to hand. 19 September, the day the shares started their bounce, VEIL published its Half-year Report. The numbers make decent reading: +6% NAV per share return for the first half of 2024 bang in line with the Vietnam Index’s (VNI) +6.0% (both in US$ terms). In GBP terms, VEIL’s NAV per share was up +6.9%. Good old-fashioned news flows in the form of positive NAV performance, the difference it seems. As VEIL’s Chair Sarah Arkle wrote in her half-year statement “We believe that the key to narrowing the discount will be stronger NAV performance and an improvement in investor sentiment towards Vietnam.” Based on the share price reaction, looks like the Chair is spot on – in the end, it all boils down to performance.