Is SOHO a no go? Is this Social ‘Housing landlord, all REIT or a REIT off ? The Oak Bloke

One of my readers asked me to look at SOHO and I’m slowly working through my backlog. So what about this, the third of Triple’s UK offerings? Is this getting sold down too?

Surprisingly no.

In fact the first thing to say is SOHO is a 97 super stock on stocko, it trades at 65.7p, delivers an 8.6% yield (0.85X covered) and NAV is 114.15p a share as at 31/3/24. So a 41.3% discount to NAV. Although HL imagines its NAV is 129.47p a share (incorrectly).

SOHO have 493 properties (with 3,421 units) costing £594.9m in invested funds, and valued at £678.4m today – 14% higher. That’s £1.37m average per property and £198.3k per unit average.

We live in an age when investors are obsessed with central bankers’ actions and words. To cut or not to cut seems to be the question on everyone’s mind. In truth, investors have always been worried (and excited) about macroeconomic policy, but the current environment is especially focused on rate decisions. We unpack the importance of interest rates for investors in a simple ten-step way.

By David Stevenson•05 Sep, 2024

Over the last few months, stock markets have zig-zagged up and down based on worries about interest rates, especially in the U.S. – remember that U.S. stocks overwhelmingly dominate global equity markets. Last week, the first major signs of the much-anticipated interest rate pivot emerged. The Federal Reserve chair Powell observed,

“Overall, the economy continues to grow at a solid pace. But the inflation and labour market data show an evolving situation. The upside risks to inflation have diminished. And the downside risks to employment have increased. As we highlighted in our last FOMC statement, we are attentive to the risks to both sides of our dual mandate. The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks. We will do everything we can to support a strong labour market as we make further progress toward price stability. “

In plain English – We are more worried now about rising unemployment than we are about surging inflation, which could imply a recession, so the time for interest rate cuts is fast approaching.

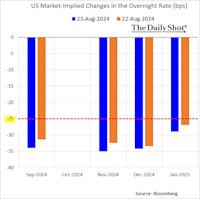

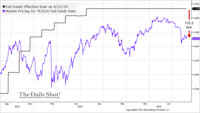

Within minutes of this gnomic declaration the market was pricing in a higher possibility of a 50 bps cut at each upcoming Federal Open Market Committee meeting. The next two charts show market reactions from a week or two ago via the excellent macro-economic news service, The Daily Shot.

Overall, investors are now pricing in 105 bps (1.05%) of rate cuts for this year. Personally,, I think that is a little overcooked, but the market is betting that the U.S. interest rate will be closer to 4% than 5%. And what starts in the U.S. will almost certainly apply to the UK— most investors now expect UK interest rates to stabilise somewhere between 4 and 4.5% by early 2025.

This all sounds terrifically exciting if you are a dismal economist – or potential mortgage applicant – but why does it matter to ordinary investors? As a market observer, I’m painfully aware that analysts and strategists get carried away with jargon and make bold assumptions about investors’ knowledge. For instance, it’s almost a given that investors join up all the dots about rate cuts, whereas my guess is that most investors only have the simplest understanding of why rate cuts matter.

To help bridge that gap, I thought I’d zip through ten reasons why investors should care about interest rate cuts. Forgive me if it’s a bit simplistic, but the point is simple – investors should care greatly about these cuts.

Interest rates are a signalling device, telling markets what central bankers are worried about. Read that statement by Powell carefully, and it’s obvious he and his colleagues are growing more concerned about increasing unemployment and a weak labour market. That suggests the concerns of an economic slowdown in the U.S. are real and valid. That should concern investors because it suggests that central bankers are worried that the miraculous soft landing – much anticipated – might be replaced by a bumpy landing. That implies you should take seriously if you are a bond investor, the risks of increased corporate defaults (which have been steadily increasing for the last year). That means you need to demand a higher risk premium for lending to risky corporates.

Declining interest rates are good news, by contrast, for indebted corporate borrowers, especially in the real assets (infrastructure and real estate) sector. These sectors are interest rate-sensitive, and thus, declining rates, all things being equal, should mean lower refinancing costs.

Lower interest rates imply that central bankers are much less worried about surging inflation. There is still every chance that core measures of inflation might crawl back up again, possibly breaching the 3% before coming back down again. But the substantive point is that central bankers are NOT worried about a massive inflation surge pushing past 5% year on year. That might mean the inflation assumptions for many funds invested in real assets might have to be notched down again, which cut into revenue growth if they own inflation-linked assets

Lower interest rates will reduce the implied real interest rate to more sustainable levels. I’ve already discussed in these articles why real interest rates (the nominal interest rate minus the market forecast for inflation rates in the not-too-distant future) have been heading steadily towards zero for decades but shot up in the last two years. Sustained positive real rates tend to slow down investment spending and generally hinder economic growth. Lower real rates – I guess they’ll stabilise at around 1% in the U.S. and the UK – might mean faster economic growth and improved capex spending. All in all, that’s good news for equities in general.

Lower interest rates have another very important transmission mechanism via the risk-free rate, widely used in discounted cash flow models and investment trust NAV calculations. You will often see mention of net asset values calculated with reference to a discount rate. A real asset produces a stream of cashflows (rents, payments), which are then plugged into a forward-looking cash flow model. A number is generated representing the potential future value of those cash flows, but then it is discounted back using the risk-free rate. The risk-free rate is the return you could get from holding cash, i.e., it is risk-free, assuming you have bank guarantees. The lower the interest rate, the lower the risk-free rate, the lower discount and the higher the NAV. This risk-free mechanism will take time to work its way through to fund valuations – maybe as long as a year, but the impact should be positive.

That lower risk free rate also has a wider impact across all asset classes. When savings rates and risk-free government bonds paid you 5% or more, many investors were reluctant to go all in for risky equities. 5% risk-free is a great return, and money flooded into money market funds. Cash savings and money market account returns will seem less attractive as rates decline. That, in turn, makes equities more attractive. Dividend-paying, higher-yielding equities might be particularly attractive, especially if the sustainable dividend yield is well above the risk-free rate, i.e. above 4 to 5% per annum.

Lower interest rates in the U.S. make the dollar less attractive. Over the last few years, high U.S. interest rates – relative to Europe and Japan – have made the U.S. Dollar a desirable currency. The dollar index, which measures the dollar against a basket of currencies, has been historically quite high but has weakened in recent weeks. Even sterling has shown some strength in recent months, as has the Japanese yen. Overall, a weak dollar is good news for indebted emerging market economies and good news for gold. But a weaker dollar and a stronger pound is bad news for UK investors in U.S. equities.

Central bankers have not entirely given up worrying about inflation, but interest rates are not their only mechanism for controlling the economy. They also run extensive balance sheet processes such as buying up bonds and, in Japan, ETFs. In recent decades, these activities have mushroomed into huge quantitative easing (QE) programmes worth hundreds of billions. Central banks have been keen to rein back in these programmes and have initiated quantitative tightening (QT) measures. That’s resulted in central banks quietly selling assets and marking up losses. These losses must be paid for by treasuries, crimping government spending programmes. Lower interest rates usually tend to go along with quantitative easing, i.e. central bankers are worried about increasing recession risks and flooding the market with bank cash. However, central banks are also keen to unwind those QE programmes via QT in the long term. The 64 trillion dollar question is whether QT will continue, which might crimp global liquidity and cause financial stress or retreat their QE programmes.

Lower interest rates are also good news for indebted governments, including the U.S. and the UK. Lower debt costs help improve the government fiscal position as interest rate costs on gilts decline. However, that could be offset by the losses accumulated on past QE programmes, which are being passed on to treasuries (as noted above). It’s also worth remembering that much of government debt is fixed at long-term rates, so the immediate impact isn’t always direct. However, the UK government borrows heavily using inflation-linked gilts and shorter-term debt, and these costs will fall markedly, allowing the government more headway to spend more (or cut taxes). That’s a positive for the UK economy.

Residential property markets are a significant driver of consumer spending-dominated economies like the UK. A huge wealth of data suggests that when house prices have stopped falling and are rising again, consumers feel wealthier and spend more. The same argument also applies to equity markets, i.e., when the S&P 500 surges in the U.S., wealthy Americans spend more. All things being equal, lower rates should help stabilise housing markets, even though most mortgage holders have locked in their rates for a few years. Again, that’s potentially great news for the domestic economy and thus corporate profits.

The Results Round-Up – The Week’s Investment Trust Results

Global Opportunities remains conservatively positioned, while International Public Partnerships delivers another solid performance. abrdn UK Smaller Companies Growth continues to outperform, and it’s onwards and upwards for Onward Opportunities.

Frank Buhagiar•06 Sep, 2024

Global Opportunities (GOT) staying conservatively positioned

GOT’s objective is to generate real long-term total returns by investing in undervalued assets. Because of this, the fund does not follow a particular benchmark. But not to worry. For Chairman Cahal Dowds dishes out a couple of indices with which to compare the fund’s +3.1% NAV total return for the latest half year -the FTSE All-World Index, up +12.2% on a total return basis, and the Bloomberg Global Aggregate Bond Index, off -2%. The fund’s +3.1% total return down to what Executive Director Dr Sandy Nairn describes as a “conservatively positioned” portfolio. And that in turn is down to operating in “an environment with elevated valuations and meaningful government debt overhangs.”

No plans to change the cautious stance anytime soon, it seems “We anticipate that the stark economic choices facing the major economies will prove increasingly difficult to ignore and will become ever more evident in company results/forecasts. Combining this with an unfolding election season and the global geopolitical tensions suggests that the seemingly unshakeable optimism of equity markets will be severely tested.” The conservative positioning, focus on identifying attractive investments and avoidance of any meaningful broad equity market risk have worked wonders for the portfolio’s volatility – the portfolio has had a volatility level around one third of equity markets. Dr Nairn however believes “There will come a time when it is appropriate to take a more sanguine view of risk and we are prepared to do this when the potential returns justify.” Just not now. Market keeping its powder dry too it seems – GOT shares closed 2p lower on the day at 294p.

Winterflood: “Portfolio remains conservatively positioned in light of manager’s concerns over equity market valuations remaining at historically high levels implying substantial risk. As at 30 June, cash and equivalents accounted for 33.8% of portfolio value, with 44.0% in equities, 14.9% in long-short fund and 7.3% in Private Equity fund.”

International Public Partnerships (INPP), solid

INPP Chair Mike Gerrard described his fund’s half-year performance as “solid”despite a slight decline in NAV to £2.8 billion (3 December 2023: £2.9 billion). That followed a c.30bps increase in the weighted average of the discount rates used to value the underlying investments. As the half-year report notes, the increase in the discount rate “is designed to reflect perceived changes in the rates of return currently required by investors and, ultimately, ensure that these point-in time valuations reflect prevailing market conditions.” Back to the solidity Gerrard refers to. According to the Chairman, this is based on “the resilience of its diversified, low-risk portfolio and fundamentals of the investment case.” All of which has enabled the infrastructure fund to deliver on its progressive dividend policy every year since its 2006 IPO. “Moreover, the strength of the portfolio is such that no further investments are needed to continue this policy for at least the next 20 years.” All sounds, well, solid.

And yet, as Gerrard notes, the shares trade at a discount to net assets. The Board thinks this materially undervalues the fund. No need to take their word for it. For having raised c.£235 million through disposals in the last 18 months, the “realisation proceeds achieved were in line with the last published valuations.” What’s more, “The Company expects further divestment activity and, as a consequence, also expects to extend its existing share buyback programme, increasing the programme to up to £60 million. This demonstrates our confidence in the Company’s valuation.” Investors happy to pay up for a solid company – shares tacked on 3.2p to close at 130.8p.

Liberum: “The H1 results were largely uneventful at the portfolio level, which is a good thing.”

Investec: “INPP continues to trade at a material discount to NAV and we estimate that the implied returns at the current share price are c.9.3%. We remain comfortable with our Buy recommendation.”

abrdn UK Smaller Companies Growth (AUSC), a believer in the Matrix

for the year, almost double the 10% posted by the Deutsche Numis Smaller Companies plus AIM (ex-investment companies) Index. Share price total return fared even better up +21.0%. The investment managers are particularly pleased with “the consistency of outperformance” after the fund beat the index in nine of the 12 months. That outperformance “has predominantly been driven by stock specifics, companies reporting strong trading and earnings upgrades, with share prices responding appropriately, which is a distinct improvement on the situation over the last couple of years.”

As Chair Liz Airey notes, “The focus remains on the resilience of the companies in which the portfolio is invested and the experience and flexibility of the management teams to adapt their companies to the changes to the economic environment that are occurring.” Picking the right stocks has and continues to be key. Here the investment managers are helped by The Matrix, a screening tool that identifies companies it believes are displaying Quality, Growth and Momentum dynamics. According to the investment managers, “The Matrix will continue to be valuable as we move through economic cycles.” Anyone else feeling the urge to watch the 1999 Hollywood blockbuster – The Matrix? Perhaps enough investors did just that on the day of the results, as the share price closed unchanged.

Winterflood: “Both stock selection and sector allocation contributed to relative performance. Style headwinds have diminished and returns have been predominantly driven by company trading results and earnings upgrades. Managers observe ‘fairly smooth positive return pathway’ since October 2023. UK fund outflows are thought to have stabilised and ‘showing tentative signs of reversal’.”

Onward Opportunities (ONWD) marches onwards

ONWD maintained its good start to life as a public company: a +9.2% NAV total return for the latest half year brings the 12-month tally up to +20.6%. That trumps the UK AIM All Share’s +3.1% with room to spare. As for where that ranks the fund in terms of its peers, fourth out of the 26 trusts in the AIC UK Smaller Companies sector. The strong performance enabled the company to raise a further £4.7m by issuing new equity, thereby increasing the capital base by a quarter. Small wonder ONWD was named ‘IPO of the Year’ at the Small Cap Awards. And as Chair Andrew Henton points out, “the important point to observe over the 18-month trading period since inception of ONWD is the strong, positive NAV growth within the portfolio – and this notwithstanding the vagaries of macro events.”

Henton believes there’s more to come “It remains the view of the Board that there is more upside opportunity in smaller company valuations than downside risk, and any market rerating which does take place will represent a fillip.” Continued strong performance will help continue to grow the size of the fund (currently total assets stand at £20 million). And as the fund grows in size this “will allow the Company to be marketed to a wider range of prospective institutional investors, many of whom are presently excluded from buying shares due to a combination of technical thresholds including minimum ticket sizes and maximum ownership stake.” Shares were unchanged on the back of the results, no doubt taking a well-deserved breather before resuming their onwards and upwards trajectory.

No broker commentary on the latest results at the time of going to press, but below is an extract from ONWD’s IPO of the Year Award back in June 2024:

“Onward Opportunities Ltd was set up by Dowgate Capital to invest in undervalued smaller companies – generally under £100m market capitalisation. It was seeking companies with qualities such as asset backing, cash flow, growth potential and strong management. On 30 March 2023, the company raised £12.75m at 100p/share. A portfolio of predominantly AIM companies has been built up. In a time of tough markets, the NAV has grown to 120.14p/share by the end of May 2024. That makes it one of the top performing smaller company-focused investment companies.”

2 shares I’ve just bought for income and growth in my Stocks and Shares ISA

Story by Ben McPoland

A Stocks and Shares ISA is the perfect place to build wealth over the long run. The keys are consistency, patience, and finding the right investments.

With this in mind, here are two shares that I’ve added to my portfolio in the past few days.

FTSE 250 dividend stock

This is a FTSE 250 investment company that focuses on owning and managing infrastructure projects through public-private partnerships.

First up is BBGI Global Infrastructure (LSE: BBGI).

For this year, the dividend is 8.4p per share, which is 6% higher than last year. The forward yield is 6.2%, which is comfortably above the FTSE 250 average

While no dividend is bullet-proof, I’d say this one is very much on the safer side of things.

Moreover, I reckon the share price, which is down 22% over the past two years, could bounce back strongly as interest rates fall and infrastructure projects start to pick back up.

That’s not guaranteed, mind you. A resurgence of inflation could quickly put the handbrake on falling interest rates while negatively impacting the trust’s portfolio value.

However, right now, the trust is trading at a 10% discount to the value of its underlying assets. That’s against a five-year average premium of 12.8%.

With a well-supported 6%+ yield, I like the risk-reward ratio here.

Created at TradingView

US growth stock

Next, I invested in a very different stock:Uber Technologies (NYSE: UBER). The share price has risen 22% so far in 2024, but I think it could rise much higher over the next decade.

The reason is that the ride-hailing and food delivery firm is quickly becoming a cash machine. From negative cash flow in 2021, the company’s free cash flow is expected to approach $10bn in 2026.

Talk about scaling up

This is being driven by efficiency savings and ongoing global adoption of the Uber app, which is displacing local taxi firms at a rapid clip.

In Q2, gross bookings grew 21% year on year at constant currency. For Q3, management sees gross bookings of $40.2bn-$41.7bn, representing 18%-23% growth on a constant currency basis.

CEO Dara Khosrowshahi commented: “Uber’s growth engine continues to hum, delivering our sixth consecutive quarter of trip growth above 20%, alongside record profitability…more people are using the platform, and more frequently, than ever before.”

For the full year, Wall Street is forecasting revenue growth of at least 16%. I find that very impressive given how weak consumer spending is worldwide today.

Now, I appreciate that I’m taking on regulatory risk with Uber, particularly relating to whether drivers are classed as independent contractors or employees. There might even be bans in some countries.

However, the stock is trading on a price-to-sales multiple of 3.8. It’s been much higher than this in previous years.

Created at TradingView

Looking ahead, I think the likelihood of ongoing double-digit revenue growth and surging profitability make this a top tech stock.

The post 2 shares I’ve just bought for income and growth in my Stocks and Shares ISA appeared first on The Motley Fool UK.

I’d buy 14,290 shares of this UK dividend stock for £100 a month in passive income Our writer shines a light on a 6.2%-yielding stock from the FTSE 250 that he’s recently been buying to generate passive income.

Posted by Ben McPoland Published 6 September

BBGI

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in..

Investors looking to increase their passive income are truly blessed in the UK. That’s because there’s an abundance of options to choose from, both in the blue-chip FTSE 100 and mid-cap FTSE 250.

One of my favourites from the latter is BBGI Global Infrastructure (LSE: BBGI). Here’s why I recently bought a few more shares of this investment trust.

Stable income streams BBGI specialises in social infrastructure projects through long-term public-private partnership and private finance initiative contracts. It has 56 portfolio assets, including motorways, bridges, hospitals, and schools.

Top 10 Investments Weighting

Golden Ears Bridge (Canada) 11% Ohio River Bridges (US) 10% A7 Motorway (Germany) 4% Northern Territory Secure Facilities (Australia) 4% A1/A6 Motorway (Netherlands) 4% Victorian Correctional Facilities (Australia) 4% Liverpool & Sefton Clinics (UK) 3% M1 Westlink (UK) 3% Women’s College Hospital (Canada) 3% Poplar Affordable Housing & Recreation Centres (UK) 3% Remaining investments 51% These provide government-backed, inflation-linked income streams. Its partners are creditworthy public sector entities in countries with solid credit ratings (AA to AAA), such as Australia, Canada, Germany, the Netherlands, Norway, the UK, and US.

Geographical Split Canada 35% UK 33% Continental Europe 13% US 10% Australia 9% While I like this geographic diversification, these are locations where interest rates are high. And this has been a headwind for BBGI as infrastructure investments and valuations are sensitive to rate changes.

Also, higher rates reduce the attractiveness of its dividend yield relative to other investments. While I expect these challenges to ease as interest rates fall, they’re worth bearing in mind. Inflation could always return.

Covered dividend At the end of June, there was no structural gearing at group level and no cash drawings on a revolving credit facility. The trust had net cash of £20.6m.

It reaffirmed its 6% dividend growth target for FY24, with a further 2% growth planned for FY25. And it expects its cash flow to be 1.3 to 1.4 times this year’s payout. So the dividend looks secure.

Over the medium term, we expect cashflows to continue to support a healthy dividend cover and provide ample headroom to sustain a progressive dividend policy well into the future.

Non-executive chair Sarah Whitney, H1 2024 earnings report Earning passive income At 136p, the current share price offers an attractive forward dividend yield of 6.2%.

This means a £19,434 investment in my ISA would get me around 14,290 shares, enough to pay the equivalent of £100 a month in tax-free passive income.

Moreover, the shares are trading at a 10% discount to net asset value. This compares to a five-year average premium of about 12%. I think this stock could be a steal for long-term investors like myself.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Foolish takeaway High levels of public debt combined with rising populations and the growing need for new infrastructure projects means specialist investors like BBGI are well-positioned to succeed.

De-globalisation is a megatrend that will require the onshoring of US manufacturing and an increased focus on energy security, driving significant demand for private infrastructure investments.

Meanwhile, the EU is aiming for Europe to become the first climate-neutral continent. The trust says this presents “a continuous flow of pipeline opportunities in the core infrastructure space“.

Finally, the Australian government is committed to investing A$120bn on projects over 10 years.

Even without further acquisitions though, management says the portfolio could continue to generate a rising dividend for the next 15 years.

While no payout is ever truly guaranteed, I’d be very surprised if this one was scrapped. I’d happily buy more shares with spare cash for a diversified portfolio.

Good day! Do you use Twitter? I’d like to follow you if that would be ok. I’m undoubtedly enjoying your blog and look forward to new updates. lee bet casino

SDCL Energy Efficiency Income Trust plc is a constituent of the FTSE 250 index. It was the first UK listed company of its kind to invest exclusively in the energy efficiency sector. Its projects are primarily located in North America, the UK and Europe and include, inter alia, a portfolio of cogeneration assets in Spain, a portfolio of commercial and industrial solar and storage projects in the United States, a regulated gas distribution network in Sweden and a district energy system providing essential and efficient utility services on one of the largest business parks in the United States.

The Company aims to deliver shareholders value through its investment in a diversified portfolio of energy efficiency projects which are driven by the opportunity to deliver lower cost, cleaner and more reliable energy solutions to end users of energy.

The Company is targeting an attractive total return for shareholders, with a stable dividend income, capital preservation and the opportunity for capital growth. The Company is targeting a dividend of 6.32p per share in respect of the financial year to 31 March 2025. SEEIT’s last published NAV was 90.5p per share as at 31 March 2024.

Something for the anoraks

SDCL Energy Efficiency update

SEIT, say it, sorted SDCL Energy Efficiency update The Oak Bloke

“The Oak Bloke from The Oak Bloke’s Substack” <theoakbloke@substack.com>

(“TENT” or the “Company”and together with its subsidiaries, the “Group”)

SPECIAL DIVIDEND

The Board of Triple Point Energy Transition plc (ticker: TENT) announces that, as part of the managed wind-down approved by shareholders on 22 March 2024, and as a result of timely realisations to date and taking into account feedback received from shareholders, it has declared a distribution by way of a special dividend of c.£25m, equivalent to c.29% of the Company’s NAV as at 31 March 2024.

This is equivalent to 25 pence per ordinary share in the capital of the Company (“Ordinary Share”), payable on or around 4 October 2024 to holders of Ordinary Shares on the register on 20 September 2024. The ex-dividend date will be 19 September 2024.