I’ve sold WHR for a profit of £132.00 including the earned dividend.

Investment Trust Dividends

I’ve sold WHR for a profit of £132.00 including the earned dividend.

Mark Peden, Investment Manager, Aegon Asset Management

04 July 2024

Back in 2020, I penned an article titled ‘The Dividend Dilemma’. It was the depths of the Covid-induced market selloff; companies were cutting or suspending dividends left, right and centre; and analysts were predicting big cuts to global dividends from which they would take years to recover. I anticipated a fall of around 30%.

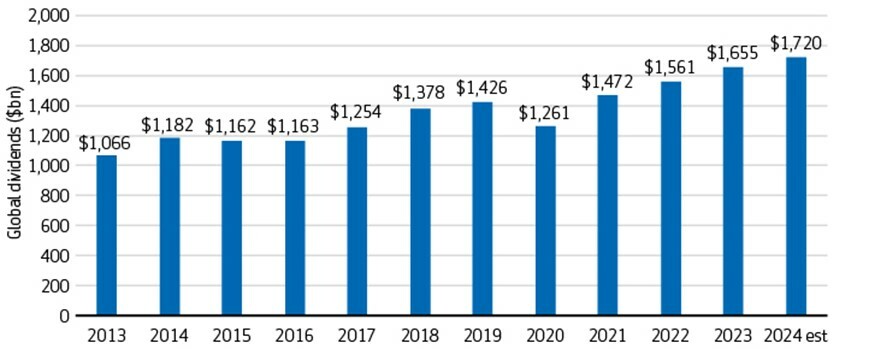

Yet for all the cataclysmic predictions, payouts took just one year to bounce back. 2021 was a record-setting year for global dividends at $1.47 trillion, a mark that was subsequently bettered in 2022 and again in 2023. We have now gone from the dividend dilemma to the dividend deluge and, with 2024 predicted to set yet another record at $1.72 trillion, there are no signs of the momentum fading. In addition, share buyback authorizations are also at all-time highs, meaning the picture is clear – companies are returning record amounts of capital to shareholders.

Exhibit 1: Global total annual dividends are climbing (USD, billions)

Source: Janus Henderson Global Dividend Index Report, as of February 29, 2024

The past few years have seen financial markets affected by bouts of volatility caused by factors such as Covid lockdowns, spiking inflation, historically steep interest rate rises and geopolitical tensions. Through all of this, dividends have reinforced that they are typically much less variable than earnings and can provide an important source of total return, regardless of the market environment. They also have a solid track record of keeping pace with inflation, meaning there was less erosion in real terms than we saw in payouts from most other asset classes during the inflationary spike in 2022 and 2023. All in all, the importance of dividends should not be overlooked.

A focus on quality dividend-paying companies

So where does this leave us now? Deep value areas of the market, characterized by companies with lower-quality earnings and high debt levels had their day in the sun in 2022. Such rallies tend to be sharp but also short-lived, as was illustrated by the strong comeback in growth stocks through 2023. That said, the growth rally has been very narrowly driven by a handful of US-listed, mega-cap, tech-related names known as the ‘Magnificent 7′. We do not see another sharp value rally on the horizon and would question whether the narrow market leadership seen recently can continue over the longer term.

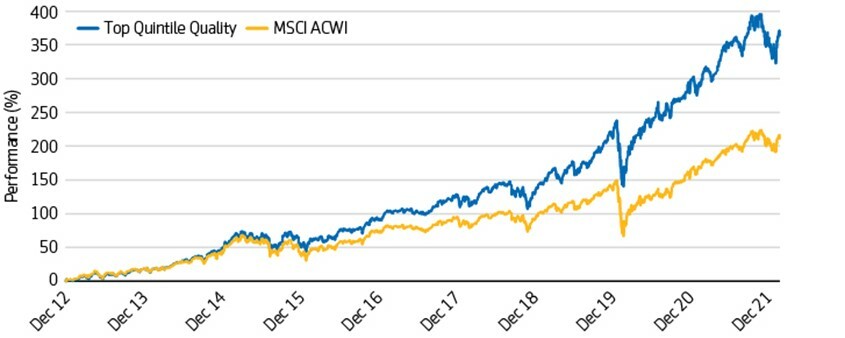

Instead, we believe a focus on ‘quality’ dividend paying companies with strong balance sheets and high returns on equity can be a powerful factor over time. As shown in Exhibit 2, the top quintile of companies, based on quality within the MSCI All Country World Index, has significantly outperformed the wider market over time.

Exhibit 2: Higher-quality companies have historically outperformed

Source: Bloomberg, Aegon AM as of March 31, 2022. Quality is defined by low net debt to EBITDA and high return on equity.

This quality approach will, we believe, be as important as ever in the coming months. Economic growth remains healthy in the US but is more sluggish elsewhere. Inflation has fallen back from recent peaks but the final leg of the journey back to target is proving difficult. Consequently, investors have scaled back their expectations for both the timing and scale of interest rate cuts this year. Add in geopolitical tensions and the looming US presidential election and clearly there is uncertainty out there. We believe well established companies with strong balance sheets, good returns on equity and well covered dividends have the potential to fare well, whichever path the market takes.

Indeed, despite the uncertainty in the market right now, more than 10 companies in a representative global equity income portfolio have increased their dividends by double digit percentages so far this year – well above the rate of inflation. These increases suggest companies are generating plentiful free cash flow and returning it to shareholders, signalling what we believe is a healthy confidence in their financial situation.

A golden period for dividend investing

All of this suggests we may be in a golden period for dividend investing. Companies are returning record amounts of capital to shareholders and are doing so while recording payout ratios that are below long-term averages, meaning these dividends should remain even in the face of slowing growth. In the past several months, we have even seen some members of the Magnificent 7 initiate their first-ever dividends, suggesting dividends are in fashion, even for high-growth companies. While the yields on these companies remain relatively low compared to the wider market, we will monitor developments very closely to see how they progress over time.

Dividend strategies themselves tend to come into their own in more uncertain market environments, where income streams become an even more crucial part of total returns and a lower beta approach may offer some protection from volatility. With equity markets close to all-time highs in many countries and valuations looking fairly full, investors may look to incorporate these characteristics in their portfolios through a dividend focused approach. If nothing else, the shape of global dividends today should provide investors with opportunities going forward.

Passive income text with pin graph chart on business table Provided by The Motley Fool

by Charlie Keough

I’m always looking for ways to generate passive income. And as Warren Buffett once said: “If you don’t find a way to make money while you sleep, you will work until you die.”

Here are some things to consider.

The first thing is to work out where to put my money. And I think the best place to start is the stock market. With rampant inflation leading to base rates around the world reaching attractive levels, including 5.25% in the UK, some investors may opt to leave their money in savings accounts. However, what these savings accounts fail to offer is growth opportunities.

So, if the stock market is where I decide to put my money, what’s next? Well, it’s about selecting the right companies.

For this, I’d use the FTSE 100. The index is the home to high-quality stocks. On top of that, the average dividend yield is around 4%. This year, it’s predicted that it will return £78.7bn to shareholders via dividends.

How To Invest Your Money Effectively

Within the Footsie, I’d also do my due diligence and find stocks that I see providing stable growth in the years ahead. Additionally, finding companies with a solid track record of paying out to such as Dividend Aristocrats, a step I’d take.

Dividend payments can be unstable. And major events such as the global financial crash of 2008, or more recently the pandemic, can lead to these payouts being reduced or stopped altogether. However, selecting businesses with a stable history would provide me with more confidence.

As well as the above, there are a few further factors I’d consider.

On top of that, I’d also think about the bigger picture. When I buy a stock, I don’t think in weeks or months. Instead, I plan to hold it for the years and decades ahead.

So, let’s put this into practice. If I invested £1,000 with an average 7% return, after one year I’d have earned £70 in passive income. While that’s not much, after 30 years, I’d be making closer to £250 a year.

On top of that, by investing an additional £150 a month, by year 30 I’d be making nearly £13,000 a year in passive income. What’s more, my pot would be worth nearly £195,000.

Of course, a 7% return isn’t always guaranteed. However, by doing my research and selecting the right companies, while also topping up my pot and thinking long-term, I’m confident over time I could see some healthy returns.

Royston Wild

by The Motley Fool

The London stock market is a great place to discover top dividend shares. It’s packed with companies with strong records of dividend growth. What’s more, years of share price underperformance also mean many of these offer some staggeringly high dividend yields.

Dividends are never guaranteed. But if broker forecasts are correct, a £25,000 lump sum invested equally across them would provide me with a £1,750 second income over the next 12 months.

I’m confident too these high-yield shares will steadily increase shareholder payouts over the long term. Here’s why I think they might be great buys for dividend investors.

Renewable energy stocks like Greencoat UK Wind have significant earnings potential for long-term investors.

Adverse weather conditions can impact power generation from time to time, putting a drag on revenues. But over an extended time horizon, wind farm operators could enjoy exceptional growth as the world switches from fossil fuels to cleaner energy sources.

Source: Greencoat UK Wind Provided by The Motley Fool

Real estate investment trusts (REITs) can also be a great way to source an income over the long term. They are required to pay a minimum of 90% of their annual rental profits out to shareholders.

Urban Logistics REIT is one I expect to thrive as e-commerce steadily grows. As an operator of storage and distribution hubs, it provides an essential service that allows manufacturers, retailers and delivery companies to get product to online consumers.

In fact, this part of the property market is experiencing a huge shortage. And so like-for-like rents (which grew 19% here last year) look set to continue growing strongly.

High interest rates pose an ongoing problem for its net asset values (NAVs). But on balance, I think Urban Logistics is worth a close look.

Growing political and social turbulence in Georgia threatens to derail the country’s banks like TBC Bank Group.

Financial product penetration’s low in the Eurasian country. And it’s been soaring in recent years as the economy there has boomed.

TBC’s own profits have jumped 111% over the past five years. But it’s performance could slow sharply if turbulence in Georgia continues.

The current cash, after the capital return from ADIG of £3,7333 is £5,855.17. The return has not been included in the Snowball as it’s not a repeatable payment.

The funds are going to be re-invested in the RGL share subscription

59,100 shares at 10p

Now, u don’t need to use a calculator to realise that is short of the entitlement amount but the dividend tomorrow of £331 from RGL will take the Snowball over the line.

The closing date for subscription is the 14th of July.

The Snowball will be overweight with RGL but the intention is still to pay a reduced dividend, so the position will be sold into, overtime.

The subscription shares are trading around 13p but this price may fall after the share consolidation as the newly issued shares find a new home. One option is to sell some shares in the market and replace them with the subscription shares, when issued.

Here’s how I’d turn FTSE 100 dividend shares into a second income for life Provided by The Motley Fool

by Harshil Pate

There’s a lot to like about dividend shares. For one, they can make an excellent source of passive income.

Once the shares are bought, there’s very little left to do except wait. Long-term investments require a long-term mindset, after all.

Doing so can have a snowball effect after several years, due to the compounding effect.

Finding the best dividend shares

I’d begin by searching for quality shares that offer both growth and income. After all, dividends need to be paid from earnings. So growing earnings can lead to growing dividends.

I’d also look for a long track record of consistently paying dividends. This shows a company’s long-standing approach to distributing cash to shareholders.

Of course, there’s no guarantee that earnings will grow and no certainty that dividends will continue to be paid. But a substantial dividend history can reduce this risk.

Risk can also be lowered by owning a selection of shares, across a variety of sectors. Doing so avoids putting all my eggs in one basket.

Digging for growth

One large-cap share that meets this criteria is Footsie mining giant Rio Tinto (LSE:RIO). It has consistently paid dividends for over a decade.

Bear in mind that it’s a cyclical business though, and demand for its iron ore can fluctuate. But as a low-cost producer, I reckon Rio could withstand such swings in demand.

Also, more than half of its sales are from China. When China expands construction projects, it can have a material effect on Rio’s earnings. But of course, the opposite is also true.

Future growth is likely to come from metals needed for the energy transition and ongoing urbanisation. Rio expects demand to grow by 3.9% per year for the next nine years.

It’s all about the dividend

For shares like Rio Tinto, dividends can have a weighted effect on total returns. For instance, over the past decade, its share price has risen by around 5% a year. If that sounds mediocre, I’d probably agree.

But by factoring in dividends, its total return amounted to a healthier 10% a year. That significantly beats the FTSE 100 average of 6%.

Right now, Rio has a dividend yield of 6.5%. It also ticks some boxes when it comes to business quality. For instance, it offers a return on capital employed of 16% and an operating profit margin of 27%, both meeting my double-digit requirement.

Just like Rio Tinto, I can find several other FTSE dividend shares that tick my boxes. IG Group and BP come to mind. If I had available cash, I’d buy all three to target a solid second income for life.

££££££££££££

remember to leave some of your retained capital to those wee cats and dogs.

GL

Menhaden Resource Efficiency recommences its share buyback programme, Riverstone commits a further £20m to its buyback programme and Tritax Big Box gets a rating upgrade.

By Frank Buhagiar 09 Jul 2024

Menhaden Resource Efficiency (MHN) put out a short and sweet press release announcing that it was recommencing its share buyback programme in light of the Company’s wide share price discount to its net asset value. The shares have been trading at around a 40% discount to net assets, not far off the 52-week high discount of 42%.

Riverstone Energy tacks on another £20m to buyback programme

Riverstone Energy (RSE) announced it is committing a further £20m to its buyback programme. That represents around 9% of the fund’s market cap. RSE no stranger to buying back its own shares. Since October 2023, the company has acquired 110,407 of its shares at a total cost of approximately £0.7 million ($0.9 million). But that’s nothing compared to the 15,047,619 ordinary shares acquired via the tender offer earlier this year at a cost of £158 million.

Tritax Big Box gets a rating upgrade

Tritax Big Box (BBOX) noted Moody’s Ratings has upgraded its credit rating outlook on the logistics REIT to Baa1 (positive) from Baa1 (stable) and reaffirmed its long-term corporate credit rating. BBOX puts the upgrade down to growing scale, increased portfolio diversification and ‘a continued focus on high-quality logistics assets, which are supported by the recent acquisition of UK Commercial Property REIT Limited (UKCM).’

Dividend Watch

Artemis Alpha’s (ATS) total payout for the year came in at 6.8p a share, a 9.7% increase on the previous year’s 6.2p a share. That comes after the 4.26p final dividend was announced alongside the latest full-year results. ATS has a policy to “deliver growth in dividends at a rate in excess of inflation”.

The Telegraph says investors should put Alliance Witan on their watch lists, while MoneyWeek believes the combination of HarbourVest’s very strong performance record and ‘inexplicably high discount’ is hard to beat

By

Frank Buhagiar

09 Jul, 2024

Questor: Keep a keen eye on this investment trust about to hit the FTSE 100

The Telegraph’s Questor Column takes a closer look at the latest headline-grabbing deal in London’s investment company space, the proposed combination of long-established global trusts Alliance and Witan. As the article explains, the idea behind the deal is to create a one-stop shop, where investors can gain all their equity exposure via the new trust which will be known as Alliance Witan. Certainly, the two trusts appear a good fit with both adopting a multi-manager approach, whereby external fund managers are mandated to run the bulk of the two funds assets.

With both Alliance and Witan having market caps of over £1billion, the combined £5billion plus fund will likely be a shoe-in for inclusion in the FTSE 100. Promotion to London’s top-tier index not just a nice-to-have. The fund’s profile will be raised, making it easier and likely cheaper to trade in the shares. FTSE 100 inclusion will also put the fund on the radar of a deeper pool of investors. Those investors will also benefit from lower costs as management fees are to be reduced so that total ongoing charges will fall to under 0.6% a year, compared to Witan’s current 0.76% level and Alliance’s 0.62%.

As for performance, Alliance has the upper hand. Since April 2017 when Alliance adopted its multi-manager approach, the fund has grown assets by 102%, or 10.2% a year. That’s comfortably above Witan’s 60% return or 6.8% per annum. All of which leads Questor to conclude ‘investors should put Alliance Witan on their watch lists. A weakening in the share price before or after the transaction completes could provide a good buying opportunity’.

MoneyWeek: Should you invest in HarbourVest ?

The MoneyWeek article opens with a mystery. Private equity fund of funds HarbourVest Global Private Equity’s (HVPE) NAV is up +251% over 10 years and has doubled over five years. Yet the shares trade at a 40% discount to net assets. Why?

One possible answer is that those net assets are overvalued. Quite possible were stock markets selling off, the world hurtling towards recession and the portfolio’s holdings trading on steep valuations. But as MoneyWeek points out ‘markets have been rising steadily against a benign economic backdrop. The average valuation multiple for a representative sample of the portfolio at year-end was a reasonable 14 times cash flow, average cash flow having increased 15% in the year.’ And on valuations, MoneyWeek highlights that during the year ended 31 January 2024, around 10% of HVPE’s portfolio was sold at an average 24% premium to carrying value, suggesting a conservative valuation approach.

The article then runs through a check-list in an attempt to explain that hefty discount such as lack of buybacks, poor liquidity in the shares and high costs. No lack of buybacks though. Since September 2022, HVPE has bought back 2.9 million shares or nearly 4% of those in issue. And with the board allocating $150-$250 million to a buyback pool, more buying appears to be on the table. Nor should the liquidity of the shares be an issue as the private equity fund has a market value of £1.840 billion. As for costs, total expenses in the latest year came in at 1.8% of the average NAV, but as MoneyWeek points out ‘Managing private equity is expensive, with costs more comparable to a listed company than to a fund investing in listed shares, but the returns are significantly higher.’

So, unable to come up with a satisfactory explanation for that HVPE discount, MoneyWeek concludes ‘Within a very undervalued sector, the combination of HVPE’s very strong performance record and inexplicably high discount is hard to beat – especially with the board trying to narrow the discount and add to NAV by buying back shares’.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑