Dividend stocks are possibly the only investment where you have the opportunity for capital growth as well as income.

It’s truly empowering once you see the impact that dividend stocks can make on any account size.

Imagine the peace of mind that could give you, knowing that your nest egg could be growing without having to make massive annual contributions.

Or slaving away at the computer screens trying to pick some miracle stock.

The key ingredient is DIVIDENDS.

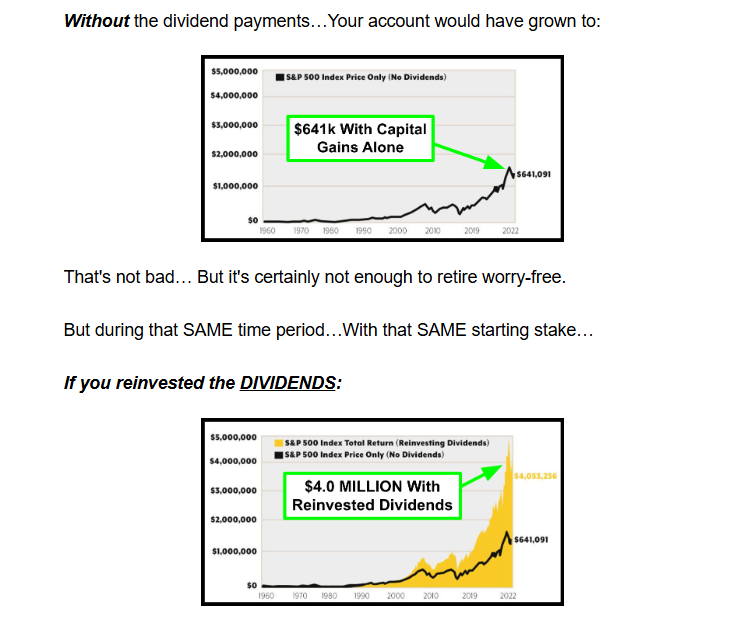

And when you look at it over the scope of time, the difference dividends make is truly mind boggling.

Just visualize a $10k investment in the S&P 500 since 1960 with me.

That means dividends were the ONLY difference between not having enough to make it through retirement.

Or retiring in the TOP 1% of all U.S. Households!

And the best part is, there’s no extra legwork on your end to collect these dividends – just sit back and watch.

As long as a company doesn’t cut its dividend, you’re guaranteed cash!

££££££££££££

Sadly I will not be able to show you how to become a multi-millionaire but I can post some building blocks for a better retirement by earning passive income every day, even when markets are closed, of £25 a day gently increasing as dividends are re-invested.

Aberforth Split Level Income Trust ex-dividend payment date Abrdn European Logistics Income PLC ex-dividend payment date Balanced Commercial Property Trust Ltd ex-dividend payment date BlackRock Sustainable American Income Trust PLC ex-dividend payment date Capital Gearing Trust PLC ex-dividend payment date Downing Strategic Micro-Cap Investment Trust PLC ex-dividend payment date Edinburgh Investment Trust PLC ex-dividend payment date Henderson European Focus Trust PLC ex-dividend payment date JLEN Environmental Assets Group Ltd ex-dividend payment date Riverstone Credit Opportunities Income PLC ex-dividend payment date Utilico Emerging Markets Trust PLC ex-dividend payment date VH Global Sustainable Energy Opportunities PLC ex-dividend payment date

Some observations, I believe they are now called bullet points.

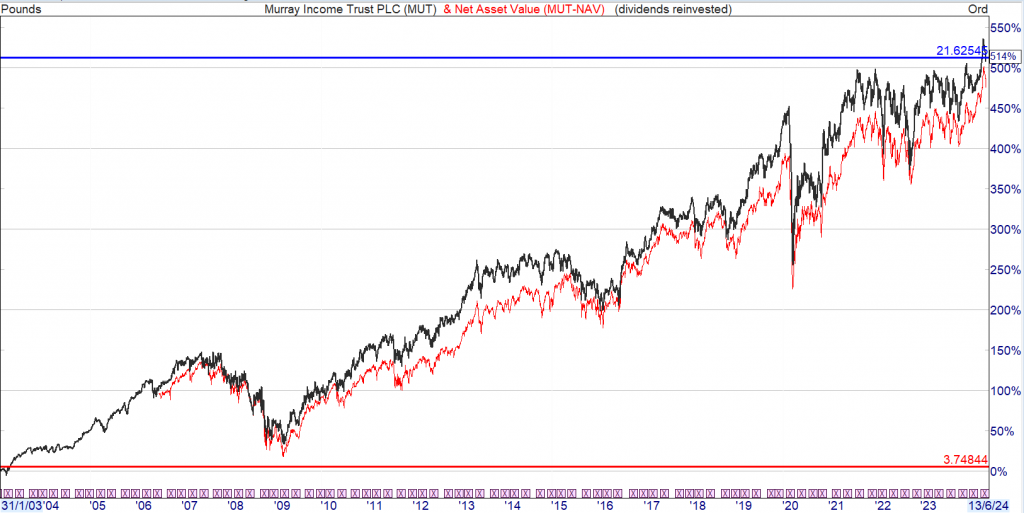

MUT pays a ‘safe’ modest dividend. From 2003 thru 2009 if u were a long term holder u hadn’t made a bean. Although there was an opportunity to book some profit and to re-invest lower down. Even without the dividends the Trust has provided enough capital to re-invest in a higher yielder.

With the dividends simply re-invested, remembering it only pays a modest dividend. No skill required apart from being a bump on a log.

Like the weather, I just ignore the weather. I just try to invest whatever capital I have as best I can and take the results as they fall. I just seize whatever opportunities I can and I hope I get my share.

The blog gets its share by investing in Trusts that pay a dividend to buy more Trusts that pay a dividend. U only need to check one thing when the Trust announces news:

Is the dividend ‘safe.’

Flatlining is good.

Increasing even better.

Or has it been cut or just trimmed. The outcome determines if the Trust stays in the portfolio or is sold.

U have read about 78billion of passive income and would like to receive your share but are concerned u might buy the wrong share at the wrong time. One option could be, to own a tiny slice of all the FTSE dividend paying shares.

The top 10 holdings

As it’s an ETF it will trade around its NAV and the yield is more variable than an Investment Trust as there are no reserves. Xd this month so u will not have to wait long for your first dividend payment.

Variable yield currently 5%. Another option would be AIE current yield 7.3% sometimes trades on a wide spread so caution required when trading.

That is approximately how much FTSE 100 companies paid out in dividends to shareholders last year. The only thing those shareholders had to do to earn that passive income was to own shares.

That may have meant buying them last year. In some cases people who had not spent a penny buying shares for decades would still have seen the work-free cash rolling in, as long as they still owned the shares.

That enormous passive income pot is easily accessible, in my view. Simply by buying FTSE 100 dividends, I would hopefully get some of it for myself.

Is it really that easy?

Having said that, it is worth noting a couple of important points.

One is that dividends are never guaranteed. A company paying them now can decide tomorrow to stop. So I take care to diversify my passive income streams across a number of different companies, carefully assessing each one’s financial prospects before buying.

Also, to buy shares, I need money.

Setting up an investment strategy

How much money is up to my own financial circumstances. It is possible to start investing in the stock market even with just a few hundred pounds.

To get going, I would set up a share-dealing account or Stocks and Shares ISA. I would put the money I wanted to invest in that, ready to buy dividend shares.

Finding shares to buy

With passive income as my goal, the search field for shares would narrow. I might like a growth company like Tesla but I see little prospect of it paying dividends any time soon.

What would I be looking for?

Passive income here is essentially the extra cash the business earns that it does not need to spend on something else, like future growth. So I would look for a business I felt I could understand, with a sustainably strong position in a market I expect to benefit from ongoing customer demand.

I would consider whether the share is attractively valued. After all, what I earn in dividends could be effectively cancelled out if the share price falls lots while I own it.

Putting the theory into practice

As an example, consider one share from which I am currently earning passive income: M&G (LSE: MNG).

The FTSE 100 asset manager has a large addressable market. Within that, a number of things help it compete effectively. For example, it has a well-known brand, established customer base spanning over two dozen markets, and long asset management experience.

That has helped it generate cash flows to fund a generous dividend since it listed as an independent company in 2018. Currently, the dividend yield is 9.8%. So, if I invested £10,000 in it today, I would hopefully earn almost a thousand pounds in passive income annually.

Whether that continues depends on how the business performs. One risk I see is that any economic downturn could hurt investor sentiment, leading them to withdraw funds from M&G. That could be bad for its profits.

Still, I own the share precisely because I believe in its long-term prospects – and am earning passive income from it along the way!

The post £78bn of passive income? It’s easily available! appeared first on The Motley Fool UK.

The £80-a-week investment strategy that could make you a millionaire by retirement.

Story by RKE

When to start investing, how much to save, how quickly can you become a millionaire? Experts have calculated it. Many of us dream of becoming millionaires. Investment industry experts believe this dream can be achieved through relatively simple steps. According to them, saving just £80 a week might be key. The question is when to start.

One must remember to save

The information presented by the USA site can be particularly useful for residents of the United States but can also serve as motivation. What do financiers advise as the first step? Start saving, preferably before reaching the age of 25. According to the Milken Institute, this gives a chance to accumulate adequate retirement funds amounting

to £882, 000.

How much needs to be saved? Experts have estimated that £80 a week invested in the market at an annual gain of 7 percent can bring impressive savings. Under the right conditions, this can achieve millionaire status by age 65.

Bloomberg notes that following the path recommended by professionals can be a challenge for young people, especially considering that many students have educational loans. Therefore, setting aside £320 a month might seem difficult.

£££££££££££££££

Whilst u may not have a spare £320 a month to invest, any amount will compound, although in the beginning the amount compounded will seem miniscule. Stick to to your task until it sticks to you.

Five completely different stocks, all listed in the UK, that tick a wealth of ESG boxes as well as looking good for the long term!

Published 20 May

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Many investors aim to align their personal values (in relation to environmental protection, social justice, and ethical governance, or ESG) with their portfolios. This is where sustainable shares come in. And here in the UK, there are many stocks that allow investors to support companies that share their values while still creating wealth over the long term… Sounds pretty Foolish to me!

Croda International

What it does: Croda International sustainably creates speciality chemicals to enhance products in a wide range of

By Oliver Rodzianko. Croda International (LSE:CRDA) has “committed to becoming the most sustainable supplier of innovative ingredients on the planet”.

Not only is the company leading in environmental preservation efforts, but it’s also making a handsome profit in the process. Over the past 10 years, the shares have grown 78% in price. It also has a net margin of 10%, which is great for its industry.

Recently, it has hired sustainability expert Aris Vrettos. Bringing 15 years of top-class experience, I think this is going to even further deepen the sustainable future of Croda.

Now, I must mention that in the past, it has faced legal action over negative effects on the environment from a plant it operated. There’s some chance that something like this could happen again, which would be bad reputationally.

But overall, this company looks very strong to me. I appreciate its efforts in getting toward a cleaner, safer work culture.

Oliver Rodzianko does not own shares in Croda International.

Gore Street Energy Storage Fund

What it does: Gore Street Energy Storage Fund invests in power retention assets across Europe and the US.

By Royston Wild. If renewable energy is to take over from dirtier sources, the energy supplied by wind, solar and tidal sources will need to be reliable. Regular power cuts are not acceptable for any developed economy.

This is why Gore Street Energy Storage Fund (LSE:GSF) has a large and growing market to exploit. This small cap invests in utility-scale power storage assets with the aim of providing regular dividend income to its shareholders.

Today its objective is to provide annual dividends equivalent to 7% of net asset value (NAV) per ordinary share, or 7p per share, whichever is higher. It’s a strategy that creates a chunky 5.1% dividend yield for the current financial year.

Gore Street’s share price, like those of many renewable energy and property stocks, has been under pressure due to higher-than-normal interest rates. This could remain a problem, too, if inflation fails to drop significantly.

However, at current prices I think the trust is worth serious consideration. At 60.3p per share, it trades at a whopping 43% discount to its estimated NAV.

Royston Wild does not own shares in Gore Street Energy Storage Fund.

Renewi

What it does: Renewi is a European waste management company that uses most of the waste collected for recycling or energy production. By Christopher Ruane. When Australian infrastructure-focused asset manager Macquarie made a takeover bid for Renewi (LSE: RWI) last year, it was rejected as undervaluing the company.

Since then, Renewi shares have fallen below the bid level. But the share price has still grown by an impressive 72% over the past five years.

Renewi shares trade on a price-to-earnings ratio of 12, which I think looks cheap. Whether that turns out to be the case depends partly on Renewi maintaining or growing its earnings. The past couple of years have been good, however the track record is inconsistent.

The business is highly cash generative but has a net debt that outstrips its market capitalisation. That is a risk to long-term profitability.

I like the business’ clear strategic focus, its extensive operational footprint and its proven business model. I see long-term revenue growth opportunities. If the company can reduce its indebtedness, I think those revenues provide a solid basis for profitability.

Christopher Ruane does not own shares in Renewi.

Tesco

What it does: British multinational high street supermarket chain selling groceries and general merchandise.

By Mark David Hartley. Founded in London in 1919, Tesco (LSE:TSCO) is now one of the largest retailers in the world. It has a strong focus on sustainability initiatives, often ranking near the top of lists for environmental, social and governance (ESG) scores. I like that it uses ethical sourcing and is known for giving back to local communities, including support for local farmers and suppliers. In its stores, I often see promotions for fair trade products and healthy, budget-friendly food options for customers.

However, it could improve more by reducing its reliance on plastic packaging and making efforts to reduce emissions from transportation and logistics. There is also some evidence to suggest its fair labour practices could be better. Overall, it scores higher than most of its competitors when it comes to ESG. I think it strikes a good balance of committing to realistic sustainability efforts without threatening its bottom line.

Mark David Hartley owns shares in Tesco.

The Renewables Infrastructure Group

What it does: The Renewables Infrastructure Group is an investment trust with a portfolio of onshore and offshore wind farms and solar parks in the UK and Europe.

By Ben McPoland. A FTSE 250 stock that I’ve been buying opportunistically over the past year is The Renewables Infrastructure Group (LSE: TRIG). It’s down 27% in two years.

One silver lining to this falling share price is that the dividend yield now stands at 7.3%. And the forecast yield for this financial year is a very attractive 7.6%.

Beyond the passive income potential, what I like here is the diversification in both assets (wind and solar farms and battery storage assets) and geography (six countries).

Unfortunately, the clean energy sector has fallen out of favour due to higher interest rates. Green projects often require significant upfront investment, and higher rates make borrowing for them more expensive. We don’t know when or by how much rates will come down. This adds uncertainty.

However, I can’t help feeling this is already more than reflected in the current valuation. The shares are trading at a whopping 23.1% discount to the estimated value of the firm’s assets.

Overall, I think there is a lot of value on offer here for patient investors.

Ben McPoland owns shares in The Renewables Infrastructure Group.