Thanks to the cost-of-living crisis, some folk now have a second job, side hustle or other way to generate extra earnings. For example, renting out a room, parking space or driveway seems popular around my way. My solution is to make my money work harder for me by generating extra passive income.

For example, I could become a buy-to-let (BTL) landlord, renting out property to tenants. But my life experience has shown how tricky and involved this can be. At the very least, I’d have to maintain and repair another property, as well as my family home. Therefore, BTL investing really isn’t for me.

Another option people pursue is blogging, vlogging on YouTube or Instagram, publishing online and so on. But as a freelance financial writer, I already spend a lot of time sharing my opinions on screen. Hence, this is another no-go for me. My two favourite forms of earnings My two ideal forms of passive income come from my efforts to improve my finances. For the next few years, I’m concentrating on these two ‘money machines’.

Share dividends Dividends are cash payments made by some businesses to their owners — that is, shareholders. However, many listed companies don’t pay out any dividends. Some of these firms are loss-making, while others prefer to reinvest their profits into future growth.

What’s more, future dividends are not guaranteed. When companies get into trouble, some respond by cutting or cancelling their payouts. And if this happens, their share prices can slump.

By the way, some people claim that investing in shares is no better than buying lottery tickets. But I know that the National Lottery returns only half of ticket sales as prizes, delivering a loss of 50% for every draw. Conversely, the stock market has produced positive returns for investors over the long term.

In addition, when I buy shares, I know that I am buying part-ownership of businesses. If these firms are well-run and growing, then my shares should rise in value. Thus, I choose the companies I buy into very carefully, mostly from the UK’s FTSE 100 and FTSE 250, plus US powerhouses.

As my wife and I already have almost all of our wealth invested in shares, our share dividends are substantial. Even so, we keep investing these cash payouts into yet more shares to boost our future passive income.

Pensions My wife and I (both Gen X and turning 56 in 2024) have amassed a collection of state, company and personal pensions.

Being over 55, we could choose to start drawing on these pots now. However, as we don’t need this income, we’ll wait while watching our pensions grow. Also, we keep contributing to these plans, using our regular payments to buy yet more shares.

In summary, my wife and I have staked our family’s financial future on the capital gains and passive income that come from owning stocks and shares. And with global stock markets booming in 2023, this has been a great year for us!

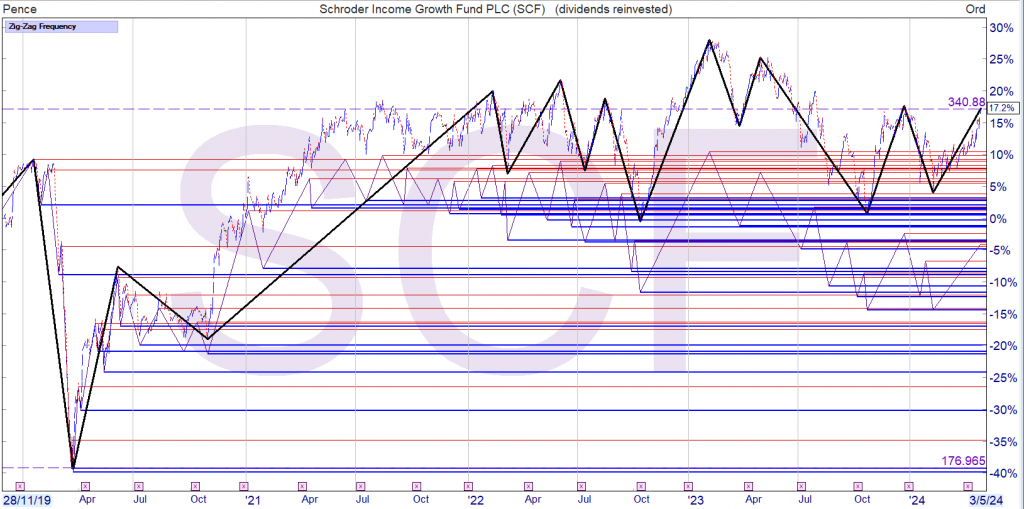

SCF has outperformed the index over the long term and boasts a premium yield to the market.

Sue Noffke has been the lead manager of Schroder Income Growth (SCF) since July 2011 and focuses on achieving two main objectives – providing real income growth, meaning it exceeds the rate of inflation, and growth in investors’ capital. Sue and her team invest predominantly in UK stocks, ensuring that the portfolio blends companies that have sustainably high yields with lower-yielding companies offering much stronger future growth prospects. Each company also needs to showcase traits the team deem desirable, such as healthy finances, proven management or a strong competitive advantage others in the industry may struggle to compete with . The team are stock pickers at heart, valuing the importance of fundamental, bottom-up analysis and placing a strong emphasis on exploiting market inefficiencies, whereby a company, which in their view has strong fundamentals, has been valued inappropriately by the market.

Under Sue’s tenure, this strategy has proved effective, comfortably outperforming the index, buoyed by strong stock selection in small- and medium-sized companies, the latter in particular. Over the last 12 months, however, SCF has lagged the index, largely down to its bias towards these companies. They are tied more closely to the prospects of the UK economy, so the adverse investor sentiment associated with weak economic issues led to valuations falling as a result, although as sentiment has improved since October, performance has picked up a little .

SCF boasts a premium Dividend yield to the market, and over its latest financial year increased dividends by 4.6%. The board has increased dividends for 28 consecutive years and feature on the AIC ‘Dividend Heroes’ list. At the time of writing SCF is trading at a wider Discount to both its five-year and AIC sector average, though this has narrowed meaningfully since October, owing largely to the bounce back in the FTSE 250.

£££££££££££

U want to include some growth Trusts in your portfolio but also wish to earn some dividends to re-invest in the market when it is weak.

The current blog portfolio plan is to earn a yield of 7%, which when compounded doubles your income in ten years, whatever the markets do in between.

Using SCF as the working example, it currently yields 5%, so u would have to pair trade it with another Trust yielding around 9%. If after doing your own research and u like a Trust that yields less, that’s ok, belt and braces GRS but GR.

If u had re-invested the dividends and without using a high risk strategy, u could have doubled your hard earned. Once it doubles u could take out your stake and try to do it all over again.

Why Schroder Income Growth offers investors the best of both worlds…

Jo Groves

Kepler

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Schroder Income Growth. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

It’s been a tale of two cities (or countries…) for US and UK equities over the last year. Fuelled by excitement around AI, US technology mega-caps have headed into the stratosphere while UK equities have flat-lined. None of this will come as any surprise to investors given the column inches dedicated to ‘unloved’ and ‘ailing’ UK equities facing their ‘darkest days’ to name but a few of the most popular descriptions.

But one adjective features more than any other and that’s ‘cheap’. It’s fair to say that the numbers support this view, with the FTSE All-Share Index trading below its long-term average at a forward price-earnings of 12, compared to 19 for the MSCI World Index (as at 22/04/2024). That said, capital growth is only one component of total returns and UK equities have long appealed to income-seekers for their premium roster of high-dividend payers.

However, investors have traditionally faced a trade-off between income and capital appreciation: the FTSE 100 blue-chips may top the table for dividend yields but lag some of their smaller counterparts when it comes to growth potential. The solution to this perennial challenge may well lie in an actively-managed fund such as Schroder Income Growth (SCF) which aims to offer the best of both worlds, blending higher-yielding companies with lower-yielding companies offering higher growth potential.

A cut above

As mentioned earlier, UK equities have been a traditional refuge for income-seeking investors, offering some of the highest yields amongst their peer group. In fairness, they have faced mounting competition from other asset classes in recent years, with cash-based investments offering attractive returns after a decade of ultra-low rates.

However, UK equities also offer a cash yield above and beyond their dividends. The last two years have seen record levels of share buybacks by FTSE 100 companies, with billions of pounds returned to shareholders. As the chart below shows, this pushed up the overall yield to almost 7% in 2023, comfortably eclipsing the return from the other asset classes.

THE FTSE 100 OFFERS A HIGH YIELD

Source: AJ Bell, Bloomberg (as at 22/04/2024)

The AIC ‘dividend hero’ status of SCF is testament to the strong income offered by UK companies, with SCF achieving a 28-year track record of consecutive dividend increases. SCF aims to deliver a dividend return in excess of inflation, which it has achieved over the last 10 years (and the life of the trust).

The investment trust structure also offers an advantage for income-seeking investors, by allowing trusts to hold up to 15% of annual income in reserves. Although SCF has typically paid covered dividends, dipping into reserves allowed SCF to continue to increase dividends even through the global financial crisis and covid pandemic.

Powering growth

As mentioned earlier, SCF takes a differentiated approach to some of its peers, balancing both income and capital growth by allocating the fund to different areas of the market: some to higher-yield, lower-growth companies, some to average yield (but better-than-average growth) companies, and the remainder to lower-yield but higher-growth companies.

Higher-yield companies include FTSE 100 stalwarts such as HSBC, Shell, Legal & General and BT from the utilities and financial sectors. At the other end of the scale, the higher-growth companies drive capital returns and, unlike some equity income funds, span the full market-cap spectrum. The managers believe that there is currently a great opportunity in mid and small-sized companies given their compelling valuations in absolute terms, and relative to large companies. As a result, the fund is significantly overweight small and mid-cap companies relative to the FTSE All-Share Index.

Managers Sue Noffke and Matt Bennison have a combined investment experience of more than four decades, and can draw on the expertise of the wider Schroders equity research team. The trust is style-agnostic, unlike the traditional value-orientation of many UK equity income funds. The managers can invest 20% of the portfolio overseas but are currently not using this option due to the attractive valuations of UK equities. However, the trust still has global reach through existing UK holdings which often derive a significant proportion of revenue from overseas.

Themes include companies positioned to play a key role in the energy transition, such as mining companies Anglo American and Glencore which should benefit from the forecast increase in demand for commodities to support decarbonisation. Sue and Matt also favour companies with resilient franchises, including Hollywood Bowl and 3i Group, and companies able to weather the higher-inflationary environment of the last few years.

A stock-picker’s paradise

Coming back to valuation, the UK All Share Index remains below its 10-year average, as well as global peers. In a recent Kepler webinar, Sue discussed how the disparity in valuation is often attributed to the “Jurassic Park” of sectors in the UK stock market relative to the US. However, she challenged this view by noting that most UK sectors are trading at a discount of 25% to 50% of the forward price-earnings ratio of their equivalent sector in the US (as at 31/01/2024).

As a result, current valuations present significant upside opportunity for an actively-managed fund such as SCF. A recent addition to the portfolio was food manufacturer Cranswick, which Sue describes as a ‘multi-bagger’ (offering a multiple return on the initial investment). The company has been a consistent performer, having delivered a ten-year total return of more than 290%, compared to just over 50% for the FTSE 250 (ex-IT) Index (as at 18/04/2024).

However, Cranswick has suffered a widening divergence between its valuation and fundamentals due to negative investor sentiment towards companies further down the market cap scale in recent years. The company’s price-earnings ratio fell from 25 to 14 in the two years to 30/09/2022, despite the company achieving a 39% increase in earnings per share during this period. Its valuation has subsequently risen on the back of a positive outlook, including expansion into the pet food market via a partnership with Pets At Home (another SCF portfolio company).

SCF has a proven track record of delivering against its dual mandate of income and capital growth, achieving a net asset value total return of 24% over the last five years, together with a current dividend yield of 5.1% (as at 19/04/2024), which compares favourably to the FTSE All-Share Index’s yield of around 3.9%. This also puts the trust in the top two of the investment trusts in the AIC UK Equity Income Sector on the basis of capital growth and dividend yield.

The increased level of interest from corporate and private equity buyers, together with an improving macroeconomic environment, may prove the catalyst for the long-awaited recovery in UK equities, as we explored in our recent note.

The timing of this recovery is harder to predict but investors willing to take the plunge ahead of the crowd may reap the best returns. In the meantime, funds such as SCF offer investors an attractive income stream as well as potential upside from the managers’ stock-picking skills.

I’d build passive income streams the same way Warren Buffett does. Story by Christopher Ruane

When it comes to passive income, there are quite a few things I like about simply buying shares in proven companies. I can benefit from the work of blue-chip businesses and can invest as little (or as much) as my financial circumstances at that moment allow. When investing for passive income, I have learnt some things from billionaire Warren Buffett.

Buying into brilliant companies Buffett looks for passive income in obvious places.

Most of his shareholdings are in large, well-known and long-established companies.

A lot of far less successful investors spend ages trying to find little-known firms they think could yet take the world by storm. Buffett, by contrast, is happy to buy shares in businesses that have already proven their business model and staying power over the course of decades. Take his holding in Coca-Cola (NYSE: KO) as an example. Buffett started buying into the company back in 1987 and completed his stake-building in 1994.

When he started buying those shares, Coca-Cola had been listed on the New York Stock Exchange for 68 years. It had already raised its dividend annually for over two decades (and has continued to do so ever since Buffett invested).

So the Sage of Omaha was not looking for ‘the next big thing’. He was buying into an existing big thing. Today his company, Berkshire Hathaway, earns over $700m annually in Coca-Cola dividends. That is over half of what it paid in total for the entire stake.

With a large customer base, proprietary brands and strong pricing power, Coca-Cola is a classic Buffett pick. It faces risks, such as increasing concern about sugary drinks leading many consumers to prefer healthier alternatives. But, for now at least, the sweetest thing about Buffett’s long-term Coca-Cola stake is its incredible financial rewards.

Investing for the long term Is it an accident that those rewards have built over the course of decades? No.

Warren Buffett is the epitome of a long-term investor. He says that if someone would not be willing to own a share for 10 years, they should not even consider owning it for 10 minutes.

Buffett’s Coca-Cola dividends have grown steadily for decades even though he has not added to his shareholding for 30 years.

As the old saying goes, over the long term, “quality in, quality out”.

Compounding dividends Although Warren Buffett has not bought more Coca-Cola shares since 1994, he has not used the massive dividend streams to pay dividends to his own Berkshire shareholders.

Instead, like all of Berkshire’s earnings, he has retained them to use in other ways, from buying different shares to taking over whole businesses.

We’re fund managers and these are the six big investment lessons we’ve learnt over the years Story by Rosie Murray-west

As the children across Britain sharpen their pencils and go back to school, there are some financial lessons that their parents can learn too.

We asked Britain’s foremost investment managers to share the most important ones they’ve learnt – and how they’ve put them into practice.

What are the most important investment lessons? We ask the experts by This Is Money

Lesson One: Too much debt just makes companies vulnerable

Early mistakes have led to caution for Richard de Lisle, who manages the VT De Lisle America Fund. He began his investment journey at just 16, only to lose his hard-earned pocket money on a risky bet.

‘I read everything on my paper rounds and did well from Patrick Sergeant in the Daily Mail and Jim Slater in The Telegraph. Those were my favourites. Yes, the Mail had a hand in my career.

‘The FT 30 had fallen more than half in two years. Stock prices were so low that I was seduced by the glamorous Court Line [a former shipping company that became a holiday provider]. It was leading the new package holiday boom, opening up the Spanish Costas to people who’d never been abroad before.’

Despite his tender years, De Lisle even looked at the valuation, including the price-earnings ratio, which shows how much profit a company is making per share. As a rule of thumb, the lower the ratio, the cheaper the company.

‘Its P/E ratio was under four; the yield was 17 per cent. What could go wrong?’ De Lisle asks.

Quite a lot, it turns out.

‘Five months later, Court Line went bust because of too much debt and I lost all my hard-earned cash. My friend’s father, who owned the fish and chip shop, did much better. He put everything he had into five blue-chip companies and more than doubled his money in six weeks.

‘Warren Buffett says that debt just speeds things up and so it does. Today we run a value-based fund. While we like cheap, we don’t like debt. Lesson learned.’

Lesson Two: You’re almost always wrong before you are right

For Laurence Hulse, who manages UK smaller companies’ specialist Onward Opportunities, an internship at Barclays Capital when he was 18 brought a lesson he has lived by all his life.

‘You’re almost always wrong before you are right. This was one of the first ‘lessons’ I was ever taught,’ Hulse says. During his time at Barclays under revered equity trader Howard Spooner, Hulse learned that because you do not usually time the market perfectly, your investment is likely to fall at first.

‘Other than in the unlikely event when you buy at the very lowest price or sell at the very highest price to the penny, you have got to be prepared to be wrong initially,’ Hulse says.

As a result of this lesson, he has learned not to make sudden swerves in his trading. ‘We very rarely trade into or out of a company in one transaction, as to do so would be to assume you have timed things perfectly.

Lesson Three: Work out whether you are investing…or gambling

John Husselbee, head of multi-asset at LionTrust, learned many of his investment lessons from his family.

‘My father taught me that whenever speculating at the racecourse or a casino, work out beforehand how much money you are prepared to lose betting, then put that amount in a separate pocket to treat as a sunk cost. Whatever is left in that pocket at the end of the day is your good fortune. However, if you have bad luck and your pocket is empty, never add to it – just walk away,’ he says.

From his grandfather, who bet on the horses as well as investing in shares, he learned the difference between investing and gambling.

‘Visiting my grandad on a Saturday morning, we would walk to the newsagent to buy a copy of the FT and the Racing Post. Back home, I would update the prices of Grandad’s shares in his ledger and calculate the profit/loss since purchase.

‘In the meantime, Grandad would study the form to select his bets for afternoon racing live on the telly. We would walk back to the newsagent; Grandad would give me pocket money for sweets and I would wait outside the bookies while he would place his bets.

‘The lesson learnt was the difference between investment and speculation – with the latter you need to be prepared to lose all your money!’

Lesson Four: It’s always darkest just before dawn

For a lesson he has never forgotten, Ian Lance, fund manager in the UK Value & Income team at Redwheel, casts his mind back to a despondent lunch in City of London oyster bar Sweetings, just as Britain was about to crash out of the European Exchange Rate Mechanism (ERM) in September 1992.

‘I calculated the payments on the mortgage my wife and I had taken out to buy our first home a few months earlier at the new interest rate of 12 per cent which the Government had just announced.

‘On finding that our payments were more than our combined salaries and the UK equity market was crashing, I headed down to Sweetings to drown my sorrows.

‘An hour or so later a colleague turned up and announced the stock market was soaring. The rest is history as Britain crashed out of the ERM, interest rates plummeted, and a new equity bull market began.’

What did he learn from this – apart from to take a long lunch now and then? ‘Markets look forward and will peer through the gloom to the sunlit uplands,’ he says. When all about you are despondent, it might be time for things to recover.

Lesson Five: You don’t know as much as you think you know

Jamie Ross, portfolio manager of Henderson Eurotrust, says that the facts available at our fingertips leave us more vulnerable than we know. The biggest lesson of his career, he says, has been that he always needs to focus on one important question when deciding whether to invest or not.

That question is: ‘What makes this a good company?’

‘It leads to all sorts of analysis, from understanding the competitive environment, to assessing pricing power to attempting to determine the sustainability of a company’s margins.’

Without this simple question, he says, it is easy to drown in information about a potential investment and to think you know everything about it.

‘Knowledge is not the same thing as understanding. Even experienced investors can sometimes miss the wood for the trees and suffer from familiarity bias – feeling more comfortable investing in something you ‘know’ lots about.

‘I think about this every time I start to work on a potential new investment.’

Lesson Six: Take the expert advice with a pinch of salt…

Edward Allen, investment director at Tyndall Private Clients, says that for all investment experts’ perceived wisdom they are ‘rarely cynical enough’, so you should never believe what you read from those who don’t have anything to lose from their predictions.

‘Economists and market forecasters have the luxury of being wrong. Investors do not,’ he points out.

‘Understand the biases of an author if you are going to follow their advice and remember that for every balanced, well-reasoned argument for doing something there will be many others for doing the opposite.

‘The investment world is perverse and often seemingly irrational.’

I’ve sold the portfolio shares in FSFL for a profit of £253.00 including the dividend earned but not received. The funds are earmarked for JLEN although trading at a slightly smaller yield, I feel more comfortable holding for the long haul.

A portfolio of shares to DYOR on. If u are growing your pot and time is on your side, u may be willing to take more of a risk and invest for growth and income. Better to have a dividend to re-invest when markets are weak.