The portfolio earned £9,422.00, calendar year 2022/23.

The current year to date the portfolio has received £3,861.00 in dividends.

Dividends declared for May £492.00

Total year to date £4,343.00 at the end of May, which is ahead of target.

The plan is to re-invest all dividends earned to earn more dividends The Snowball.

The fcast remains dividends of 8k and a target of 9k.

To achieve the ten year plan for The Snowball at the end of

2024 £7,490.00

2025 £7,980.00

It’s possible The Snowball may achieve its 2027 target of £9,170.00 but that’s only a possible. The ten year plan is to invest 100k without adding further funds to achieve a ‘pension’ of between 14-16k.

If u have a longer time frame u will benefit from the eight wonder of the world, compound interest. If compound at 7%, u will double your Snowball in ten years and u only need one or two Trusts to re-invest in which don’t have to be any of your current portfolio.

£20,000 in savings? Here’s how I’d aim to turn that into a £1,231 monthly second income.

Generating a sizeable second income can be life-enhancing, and it can be done from relatively small investments in high-dividend-paying stocks.

Simon Watkins

Published 18 April

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

One income is good, but a second income brings with it a broader range of options in life. A new house perhaps, more exotic holidays, or an earlier and more comfortable retirement.

The best way I have found of generating a high second income is by investing in shares that pay me dividends regularly.

I recently added HSBC (LSE: HSBA) to my high-yield portfolio. It currently generates a dividend payout of 7.7%.

Aside from this, it also has a strong core business – essential for sustaining high dividends over time. In 2023, profit before tax rose by $13.3bn (£10.7bn) to a record $30.3bn.

One risk is that this falls, as declining interest rates reduce the bank’s profit margins. Another risk is a new global financial crisis.

However, consensus analyst expectations are that its revenue will grow 3.5% a year to the end of 2026. Forecasts are that return on equity will be 11.7% by that time.

Another positive factor for me is that it looks around 56% undervalued against its competitor banks on a discounted cash flow basis. This reduces the chance of big share price falls wiping out my dividend gains.

Reinvesting dividends is key

So, if I invested £20,000 now in the stock, I’d make £1,540 this year in dividends. If I withdrew that money to use elsewhere, then next year – if the yield stayed the same – I’d be paid another £1,540.

Repeating this process would result in me having made £15,400 in dividends after 10 years. Not bad at all, but it’s nowhere near how much I would make if I reinvested those dividends back into the stock.

This is the same principle as compound interest in bank accounts. However, dividends are reinvested instead of interest.

Doing this would give me £43,089 instead, after 10 years. After 30 years, I’d have £200,007 if I’d reinvested the dividends and the yield had averaged 7.7% over the period.

This would pay me £14,777 a year in second income from dividends, or £1,231 a month!

Doing the same, but from £0 in the bank

Surprisingly to many perhaps, such big returns can be made from a standing start of £0 in the bank.

Saving just £5 a day — £150 a month – and investing it in HSBC stock would give me £211,748 after 30 years.

This would pay me £15,583 a year, or £1,299 a month in second income from dividend payments!

This is provided the yield averaged 7.7%, although it will move up and down as dividend payments and the share price fluctuate.

Inflation would reduce the buying power of the income, of course. And there would be tax implications according to individual circumstances.

However, it highlights that a significant second income can be generated from relatively small investments in the right stocks if the dividends are reinvested.

If u want a FTSE QUASI tracker that currently pays a variable yield of around 6%. As it’s an ETF, no reserves or discount to NAV. But if u can choose when to sell, GRS but GR.

ACTIVITY BREAKDOWN Top 10 Holdings

Name Holdings

HSBC Holdings PLC 5.2% Vodafone Group PLC 4.6% British American Tobacco PLC 4.6% Rio Tinto PLC Registered Shares 4.4% Imperial Brands PLC 4.2% Legal & General Group PLC 4.2% Lloyds Banking Group PLC 3.8% NatWest Group PLC 3.7% BP PLC 3.6% Aviva PLC

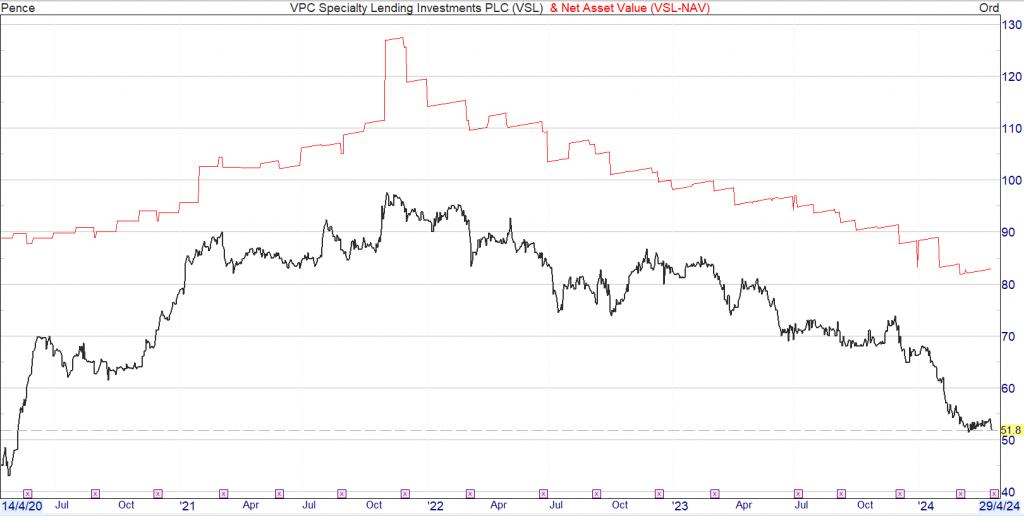

VPC are returning 4.2p per share as a return of capital. The NAV will fall by the same amount before any other adjustments.

The return of capital is not a dividend return but will be re-invested back into the market to earn more dividends. VPC a strong hold as we await further developments.

On 9 April 2024, the Board of VPC Specialty Lending Investments plc (the “Company“) announced an initial distribution to shareholders of $15 million, equivalent to approximately £11.9 million as at the date of release, through the issue and redemption of B Shares.

Pursuant to the authority received from shareholders at the General Meeting on 5 April 2024, B Shares of 1 penny each will be issued to all Shareholders on 19 April 2024 by way of a bonus issue at a ratio of 4.26159039 new B shares for each Ordinary Share held at the Record Date of 6:00 p.m. on 18 April 2024. The Redemption Date in respect of this initial return of capital is 25 April 2024. The B Shares will be redeemed at 1 penny per B Share. The Company will not allot any fractions of B Shares and entitlements will be rounded down to the nearest whole B Share. The proceeds from the redemption will be sent to uncertificated Shareholders through CREST or via cheque to certificated Shareholders on or around 10 May 2024.

Warren Buffett is among the most successful investors of all time. He’s amassed a fortune worth in excess of $120bn.

I could never hope to amass a fortune that large. However, I can certainly use his teachings to help me build my wealth over time.

We all have very different ideas of what it means to be rich. But for me, it would probably revolve around the notion of earning a passive income.

So maybe I could aim for a portfolio that could deliver double the average UK income in the form of passive income.

If I was starting from nothing, that could also certainly be considered ‘getting rich’. But is it possible? Absolutely, but it wouldn’t happen over night.

Here’s how Buffett can help me achieve it.

The power of compounding

“My wealth has come from a combination of living in America, some lucky genes, and compound interest“, Buffett has said.

And he’s been investing for a long time. In fact, he’s had nearly 70 years to help his portfolio grow.

But we can all benefit from compound returns because It’s not reserved for the wealthy or financial experts.

Warren Buffett Says, ‘The Poor Are Most Definitely Not Poor Because The Rich Are Rich

By starting early, investing wisely, and staying consistent, anyone can unlock the remarkable potential of compounding just by reinvesting year after year.

Over time, even small contributions can grow into substantial wealth, thanks to the snowball effect of earning returns on both the initial investment and its accumulated earnings.

Don’t lose money

Buffett’s “Rule 1: Never lose money. Rule 2: Never forget Rule 1” reflects his emphasis on capital preservation.

For him, avoiding losses is paramount because recovering from a financial setback demands disproportionately larger gains. For example, if I lose 50%, I’ve got to gain 100% to back to where I was.

This principle underscores the importance of thorough investment research, risk management, and a focus on the long term. It’s also why we see Buffett looking for a margin of safety on his investments.

He wants to invest in stocks that are undervalued because they may not have far to fall, but they could gain quicker than the index average.

How could I do it?

So what do I need to do? Well, bringing it all together, I need to do my research, use resources to help me make wise investment decisions, and reinvest my returns. But, of course, if I’m starting from nothing, I need to be making regular contributions.

Currently, the average income in the UK is around £30,000. And I’m going to assume it grows at 2% annually. So how much passive income would I need to earn to get double the average UK income.

Well, here’s how I think I can come pretty close to earnings twice the UK’s average income, at least according to my forecast.

The chart below shows wealth accumulation when contributing £250 a month — increasing at 5% annually — reinvesting, and achieving an annualised return of 12%.

After 30 years, I’d have £1.32m. And with that invested in stocks paying an 8% dividend yield (which is achievable today but maybe not in 30 years), I’d receive £105,600. That’s not bad.

The AIC dividend heroes are the investment companies that have consistently increased their dividends for 20 or more years in a row.

Company AIC sector Number of consecutive years dividend increased

City of London Investment Trust UK Equity Income 57 Bankers Investment Trust Global 57 Alliance Trust Global 57 Caledonia Investments Flexible Investment 56 The Global Smaller Companies Trust Global Smaller Companies 53 F&C Investment Trust Global 53 Brunner Investment Trust Global 52 JPMorgan Claverhouse UK Equity Income 51 Murray Income Trust UK Equity Income 50 Scottish American Global Equity Income 50 Witan Investment Trust Global 49 Merchants Trust UK Equity Income 41 Scottish Mortgage Investment Trust Global 41 Value and Indexed Property Income Property – UK Commercial 36 CT UK Capital & Income UK Equity Income 30 Schroder Income Growth Fund UK Equity Income 28 abrdn Equity Income Trust UK Equity Income 23 Athelney Trust UK Smaller Companies 21 BlackRock Smaller Companies UK Smaller Companies 20 Henderson Smaller Companies UK Smaller Companies 20

At the arrow, a bear trap. The market pushes higher before suddenly reversing. If u fail to act u have a big losing position or u have gave back a good part of any profit.

The best ways to monitor your investment portfolio Investing is a great way to build wealth so you can save towards major expenses such as a mortgage, or for your retirement.

It is important to check on your investment portfolio occasionally, explained Hargreaves Lansdown, when your investment objectives change “or if there have been some big changes in the markets”.

This is particularly true in the current climate as economic uncertainty such as high inflation, rising interest rates and war in Ukraine have been causing “turbulence” on the financial markets, said MoneyWeek, “potentially denting the returns enjoyed from certain funds”. Here is how to keep an eye on your investment portfolio.

Performance figures All investment funds will provide documents such as fund factsheets and value-assessment reports that outline their performance over a set period.

Historical returns “shouldn’t be a guide” to future performance, said The Times Money Mentor, but can be an “important gauge of whether a manager has delivered or not”.

Websites such as Trustnet and Morningstar also show how funds have performed compared with their own sector or benchmark.

Keep an eye on the commentaries accompanying this data, said Investors’ Chronicle, as “big moves in and out of different investments” may indicate problems while a change in style may mean the fund “no longer serves its chosen purpose”.

Some financial firms also produce regular reports that highlight good and bad performing funds.

One of the best known is investment platform Bestinvest’s Spot the Dog report, which “lists the bad mutts of the fund management industry”.

The report highlights funds or “dogs” that have failed to beat their own benchmark over three consecutive years by 5% or more.

Its latest report showed the number of dog funds rose from 44 to 56 and, the assets in those “misbehaving mutts” increased to £46.2 billion from £19.1 billion.

Similarly, Chelsea Financial Services publishes a regular RedZone report that “names and shames” the funds that have underperformed their sector average for three years in a row.

It’s generally seen as a “bad idea” to sell a fund based on poor performance alone, said interactive investor. But it “may make sense” if the fund manager shows no sign of taking action.

Do your research You can’t rely only on performance tables, said MoneyToTheMasses, as “no fund manager outperforms in every market condition”, but investors need to find the best funds to invest in “for the current environment”.

Different fund managers perform well in different circumstances, explained Willis Owen, and as time goes on, “your position and those of your investments will change”.

That makes it all the more important to understand how a fund is managed, said Charles Stanley, as well as knowing the reasons why it has performed the way it has and “what conditions it will likely perform best in going forward”.

Be careful about too many changes though. People invest for the long term, said Hargreaves Lansdown, so you shouldn’t be worried about what happens to the share or bond price “today or tomorrow”.

If investors stick to their long-term plan, they can avoid making decisions regarding their investments simply as a result of what is happening in the present.

As a “rule of thumb”, said MoneySavingExpert, five years typically gives “enough time to ride out any bumps in the market”.

Also, keep an eye on fund charges, said Which?, as while fund performance can vary, you’ll have to pay the charges “come rain or shine”, which can make a “huge difference” to your returns.

Marc Shoffman is an award-winning freelance journalist, specialising in business, property and personal finance. He has a master’s degree in financial journalism from City University and has previously written for FTAdviser, ThisIsMoney, The Mail on Sunday and MoneyWeek.

£££££££££££££££

5 years is a long time to wait to find out your IT has performed badly.