No guarantee but unless something unexpected the dividends look ‘safe’.

Stick to your plan until it sticks to you.

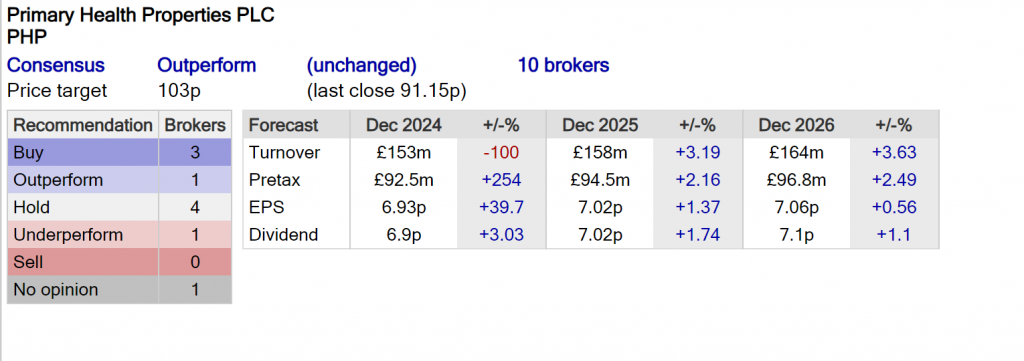

Investment Trust Dividends

No guarantee but unless something unexpected the dividends look ‘safe’.

Stick to your plan until it sticks to you.

by Ben McPoland

Getting started

I find it amazing that anyone can start investing quite modest sums every month and work their way to a million pounds in around three decades.

This would entail investing £125 a week (or £6,504 a year) and securing an annualised 8.5% return.

We can see how the large the compound returns start to become over time. Indeed, this £1m would double in around another seven years, if allowed to continue compounding without interruption.

This is the real power of compound interest, and it explains why Warren Buffett has generated over 90% of his wealth since he turned 65.

Unpredictable

Now, there are a couple of assumptions and caveats here. The first concerns the 8.5% return. I’ve used that because it’s the long-term average return of the FTSE 100 (7%) and S&P 500 (around 10%) combined together.

I believe investing in both indexes would give me better diversification. But there’s no guarantee that they’ll produce such an average return over the next 30 years. It could well be less (or more).

Second, both of these figures are total returns, with dividends reinvested. The easiest way to emulate this is through a low-cost index tracker that reinvests dividends back into the fund (known as accumulating) rather than paying them out (known as distributing).

Finally, the annual returns from the stock market are highly unpredictable and non-linear. For example, the FTSE 100 went up 12% in 2019, before declining 14% the next year. Then it rose 14% in 2021. Last year, it basically ended flat.

Thursday 21 March

abrdn Private Equity Opportunities Trust PLC ex-dividend payment date

BlackRock World Mining Trust PLC ex-dividend payment date

Diverse Income Trust PLC ex-dividend payment date

Globalworth Real Estate Investments Ltd ex-dividend payment date

Gore Street Energy Storage Fund PLC ex-dividend payment date

Triple Point Energy Transition PLC ex-dividend payment date

NextEnergy Solar Fund Limited

(“NESF” or the “Company”)

1GW Milestone and 50MW Energy Storage Asset Online

NextEnergy Solar Fund, a leading specialist investor in solar energy and energy storage, is pleased to announce that the Company’s maiden standalone 50MW energy storage asset, named Camilla, has successfully begun commercial operations. This is a significant milestone for the Company as it increases NESF’s total installed net capacity above 1GW to 1,014MW.

Camilla connected to the National Grid in December 2023 and progressed successfully through its final phases of commissioning early this year. Camilla is a 50MW 1 hour lithium-ion battery located in Fife, Scotland, which has been pre-configured for augmentation to 2 hours. Camilla is the first asset to be delivered through the Company’s £300m Joint Venture Partnership programme with Eelpower Limited.

The Company is encouraged by the recent progress made by the National Grid as it continues to make improvements in the dispatching capability of batteries in the Balancing Mechanism and the introduction of additional reserve products. This is positive for new operating assets entering the market at this point, such as Camilla, as it represents additional revenue opportunities.

On 20 February 2024 National Grid ESO published the provisional results of its T-1 Capacity Market Auction for delivery in 2024/25. Camilla successfully bid and secured a contract with a clearing price of £35.79/kW. The contract was secured with a derated capacity of 5.659MW and is expected to generate £202k (£4k/MW on a total capacity basis) of additional contracted revenue for the period 1 October 2024 through to the end of September 2025.

The Company’s disciplined approach to capital allocation focuses on accretive investment activity, consistent with the Company’s investment objective of providing ordinary shareholders with attractive risk-adjusted returns, principally in the form of regular dividends.

Helen Mahy, Chair of NextEnergy Solar Fund Limited, commented:

“I am pleased that NESF has achieved commercial operations of its first standalone energy storage asset, Camilla a 50MW battery in Fife Scotland. Camilla is conveniently located adjacent to the Glenniston substation and is already connected to the National Grid, supporting constraints on Grid interconnector capacity to areas of high demand. Energy storage assets will play a crucial role in the UK’s transition to net zero and we are proud to play a central role in achieving this.”

Michael Bonte-Friedheim, Founding Partner and CEO, NextEnergy Group, commented:

“I’m delighted to confirm that Camilla’s energisation increases NESF’s total installed net capacity to over 1GW, alongside the recent energisation of NESF’s first two international solar co-investments. Expanding into energy storage complements NESF’s existing large portfolio of solar assets on a standalone and co-located basis and provides multiple diversification benefits for shareholders.”

Mark Simon, CEO of Eelpower, commented:

“Eelpower is very pleased that the 50MW project at Camilla Farm has entered commercial operations and are proud to have delivered it with our partners NESF. We look forward to Camilla joining the market-leading assets we have commissioned over the last seven years, delivering on the promise that flexible battery assets represent for Scotland and supporting the transition to net zero in Great Britain.“

If u start out investing for compound interest with limited capital, the compound effect can seem very slow.

If u have many years of investing too look forward to, u may decide to go for some growth and accept a lower yield.

Risk versus Reward.

If your growth shares print a profit u could use those profits to re-invest in the higher yielding Trusts and grow your Snowball quicker.

If they don’t print a profit, u will still have some dividends to re-invest.

If u are near to retirement, u may decide the safety of Investment

Trust dividends are safer for your hard earned.

The emotional benefits of dividend re-investment.

In fact, with this investment strategy you can actually welcome falling share prices.

Belt and braces, where even if your share pick disappoints u can still be right.

The blog portfolio earns passive income from investing in a portfolio of Investment Trusts.

The seed capital was 100k, whilst u may not have the cash to invest u can add to a SIPP, where the government adds to your payment and build your dividend stream.

The current 10 year fcast for the portfolio is 14 – 16k dividends a year to be used for a ‘pension’, with no further capital to be added.

A current annuity for 100k is around 7k pa and u have to forego all your capital.

This year’s fcast is 8k with a target of 9k, the portfolio’s dividend stream is currently ahead of the target.

If u have longer than ten years before u need the income, u could let the power of compound interest grow your Snowball even bigger.

The Motley Fool

Story by Christopher Ruane

Imagine earning over a million pounds a day on average in passive income from a single shareholding. Legendary investor Warren Buffett does not need to imagine that. His company Berkshire Hathaway receives that much in dividends simply from one of its holdings, Coca-Cola (NYSE: KO).

My own passive income streams will never be anything like that large. But I still think I can learn from Buffett when it comes to building them.

Here are a few simple lessons from investing the Buffett way I believe can help me build income streams that are genuinely passive and do not require me to work hard.

Invest for the long term

The Coke stake is lucrative for Buffett and it has become more so over time. The company is a Dividend Aristocrat, having raised its dividend annually for over half a century.

So although the last time Buffett bought a Coke share was decades ago, his income streams from the shareholding have grown regularly over time.

Market value of Warren Buffett’s conglomerate nears $1 trillion

Taking a long-term approach to investing can pay dividends – not only metaphorically, but literally!

Avoiding yield traps

Some investors make the mistake of thinking a share that has a high dividend yield today will necessarily be a lucrative source of passive income.

But dividends are never guaranteed. Indeed, a high yield can sometimes reflect City fears that a company’s business might not support the sort of dividends in future that it pays now.

Think about where income comes from

Again, Buffett’s choice of Coca-Cola is instructive. It serves a large market that is likely to stay big, in the form of soft drinks. Its iconic brand and proprietary formula give the company a sustainable advantage over rivals.

The product is cheap to make but can be sold at a premium price, helping the business generate spare cash it can use to fund dividends.

That has been true in the past – but it also seems likely to be the case in the future. Of course, it may not. For example, growing health consciousness could hurt profits. Then again, this might open up opportunities for new products.

Like Buffett, when assessing the passive income streams a share might generate for me, I do not focus only on its dividend history. I think about how the business can generate income in the future.

Compounding dividends

Although Buffett has set up massive dividend income streams, Berkshire does not pay a dividend. Instead, it puts the money it earns to work by buying new shares and businesses.

As a private investor, I can do the same simply by compounding my dividends. That may reduce (or eliminate) the passive income I earn from shares for now. But it could lead to bigger passive income streams down the line.

The current 2024 target for the blog portfolio is a snowball of 9k, only a target not the fcast.

If u compound 9k at 7% for 9 years that would equal ‘a pension’ of £16.5k

If u compound 9k at 8 % for 9 years that would equal ‘a pension’ of £19.8k

As Buffett once said: “The rich invest for income, the poor invest for capital gains“. As such, investors may be better off following his lead and letting compounding work its magic.

Instead of buying an annuity, I forgot to mention u keep all your capital.

Writer, Laith Khalaf

Thursday, March 14, 2024

AJ Bell

It’s not just cash savers and bond investors who are enjoying income yields above the rate of inflation, so are those buying investment trusts with exceptionally long records of increasing dividends.

Five UK Equity Income trusts are currently yielding above 5%, together providing an average yield of 5.8%. That compares to the best variable Cash ISA yielding 5.11% and the best fixed term cash ISA yielding 5.25%, according to Moneyfacts.

Of course, unlike cash, capital and income is not guaranteed when holding shares. However these trusts have increased their dividend each year for at least 23 years, through the dotcom crash, the global financial crisis, and the Covid pandemic. City of London investment trust has an unbroken dividend record stretching back to 1966, the year in which England won the football World Cup and number one records in the UK included songs from the Beatles, the Kinks and Elvis Presley.

There’s no guarantee of a rising income going forward, but the resilience shown by these dividend heroes over such a long time should provide investors with some comfort. Investment trusts can hold back income in the bad years to pay out dividends in the good years, a mechanism which has allowed some to continually raise their dividends for decades. This doesn’t increase the overall dividend yield produced by the underlying portfolio of shares, but it does offer investors a smoother ride, something which is especially prized by those relying on their investment portfolio to deliver a retirement income.

| Yield | 5-year annual dividend growth | Discount | Years of dividend increase | |

|---|---|---|---|---|

| City of London | 5.1% | 2.6% | (2.1%) | 57 |

| JP Morgan Claverhouse | 5.2% | 4.6% | (5.4%) | 51 |

| Merchants Trust | 5.2% | 2.2% | (1.2%) | 41 |

| Schroder Income Growth | 5.2% | 3.2% | (10.8%) | 28 |

| Abrdn Equity Income | 8.4% | 3.5% | (8.3%) | 23 |

| Average | 5.8% | 3.2% | (5.5%) | 40 |

Source: Association of Investment Companies, data as at 8 March 2024

Based on the historic dividend growth achieved by these trusts, after 10 years they could be yielding 8% a year on an investment made today (based on a 5.8% current yield rising by 3.2% per annum). This also makes them an attractive segue for investors approaching retirement and looking to beef up their future income. Until the income taps are turned on investors can reinvest dividends, further bolstering their eventual income when they come to draw on it.

These are of course not the only investment trusts available to investors, and others may offer a more appealing combination of income and growth prospects to some investors. However, these trusts do showcase the high income stream that can be generated by investing in UK stocks, alongside the prospects for a growing income stream too.

The prospect for both dividend and capital growth are key attractions provided by the stock market to income investors. This is in marked contrast to cash where over time the interest generated is dictated by interest rate changes in both directions, and where there is no long run upward trend that can be relied on.

In the near term it looks like cash rates are likely to fall, with the market pricing in three interest rate cuts from the Bank of England this year. Further falls are then anticipated until the base rate reaches a stable level of around 3.25% in two years’ time (source: OBR). So while headline cash rates look appealing right now, those who are saving money for the longer term face a declining return picture in coming years.

As the tax burden rises as a result of frozen income tax thresholds, so does the value of holding income-producing assets in an ISA. The dividend allowance is being cut to £500 from 6 April, and 2.7 million people are forecast by the OBR to be brought into paying higher rate tax over the next five years, with a further 600,000 more taxpayers tipped into the additional rate tax bracket.

The chancellor’s recent National Insurance cuts don’t alter this picture, and nor do they reduce the tax payable on dividends. A higher rate taxpayer investing £20,000 in a portfolio paying 5.8% with dividend growth of 3.2% per annum would save £2,842 over 10 years by using an ISA. A higher rate taxpaying couple using their ISA allowance at the end of this tax year and the beginning of next, so £80,000 in total, would save £14,744.

| Dividend tax saving by using an ISA after 10 years | ||

|---|---|---|

| Taxpayer | £20,000 single ISA contribution | £80,000 couple’s ISA contribution across two tax years |

| Basic rate | £737 | £3,822 |

| Higher rate | £2,842 | £14,744 |

| Additional rate | £3,314 | £17,190 |

Source: AJ Bell, based on 5.8% portfolio yield with 3.2% annual dividend growth

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑