JPMORGAN GLOBAL GROWTH & INCOME: The £2.3bn ‘all-weather’ fund that seeks out the world’s best

Story by Jeff Prestridge •

It also pays shareholders an income linked to the growth in the trust’s assets. In simple terms, if the assets increase in value, shareholders see their dividends boosted.

For the current financial year to the end of June, it will pay quarterly dividend payments of 4.61p a share, 8.5 per cent higher than in the previous year (two have already been paid). They equate to an annual dividend of 3.2 per cent with the shares trading just above £5.30. The payments come from a mix of income from the portfolio and use of the trust’s income and capital reserves.

These factors – performance, investment clarity and growing income – have combined to turn this JP Morgan flagship trust into something of a must-have investment. As a result, demand for its shares from a combination of private investors and wealth managers is such that they trade just above the value of the trust’s assets – at a so-called premium.

It’s going to be ‘two steps forward, one step back’ with inflation, says JPMorgan’s Meera Pandit

This healthy position has persuaded the trust’s board to expand the fund by £40 million through a placing of shares and a retail offer. The placing is expected to be taken up by wealth managers keen to get clients on board while the retail offer will attract a mix of existing and new private investors. The offer shuts on Tuesday.

JPMORGAN GLOBAL GROWTH & INCOME: The £2.3bn ‘all-weather’ fund that seeks out the world’s best.

The numbers back what Cook says. Over the past five discrete one-year periods, the trust has delivered total returns of 17.1 (in the year to February 2024), 5.8, 18.9, 15.9 and 20.3 per cent. The triumvirate of fund managers is supported by some 80 in-house analysts who scour the world in search of companies that could fit into the fund’s all-weather portfolio. Currently, they have about 2,500 stocks on their radar, but only 52 sit inside the fund.

The trust’s portfolio is skewed towards the United States with 65 per cent of assets in the US and eight of the top ten holdings being big American companies.

Although some of the ‘magnificent seven’ US stocks are held – Amazon, Meta, Microsoft and Nvidia – it eschews Alphabet, Apple and Tesla because there are better alternatives.

The four it holds are primarily liked because they are at the forefront of the ongoing Artificial Intelligence (AI) revolution.

Other stocks that the managers are keen on include Swedish car and truck manufacturer Volvo and semi-conductor giants Taiwan Semiconductor Manufacturing Company and Dutch-based ASML.

Cook says that the trust’s expansion will not change the composition of the portfolio with the cash raised employed across all 52 stocks.

While Cook says company profit margins are likely to come down in the coming months as demand in the world economy decreases, he still thinks there are opportunities for astute managers to generate returns by identifying strong companies standing at attractive valuations.

The fund’s stock market ticker is JGGI and its identification code BYMKY69. Ongoing fund charges are competitive at 0.5 per cent.

The experts’ perfect fund pairings for investing in the UK

Experts reveal what funds they would buy to benefit from a revival of UK equities.

By Jean-Baptiste Andrieux,

Reporter, Trustnet

UK equities haven’t been particularly popular with investors in recent years, as their returns have significantly lagged those offered by their international competitors, in particular US mega-cap growth stocks.

The UK hasn’t helped itself either, as the country has been plagued with political instability and gloomy forecasts for the domestic economy.

As a result, UK equities are now trading on a forward price-to-earnings multiple of approximately 10.7x versus 16.5x for their global peers. Moreover, UK equities are also trading below their historic average, which means there may be room for a positive re-rating.

Jason Hollands, managing director at Bestinvest, said: “Those prepared to go against the herd now and buy, could see a significant uplift over time if UK stocks re-rate towards more normal levels.

“That could come from overseas predators on the hunt for a bargain, but also from companies themselves as a notable trend has been a significant uptick in companies using cash on their balance sheets to buy back their shares. Around half of UK companies are estimated to have announced buyback programmes over the past year.”

Below, three experts explain how investors can build a comprehensive allocation to the UK market by pairing complementary funds.

Simon Evan-Cook, manager of the VT Downing Fox funds range

Evan-Cook is enthusiastic about the prospects for UK equities, thanks to their attractive valuations, the opportunity set and strong corporate governance.

To benefit from a UK equity revival, he suggested pairing VT Cape Wrath Focus with VT Castlebay UK Equity.

Performance of funds over 10yrs vs sector and benchmark

Source: FE Analytics

Evan-Cook said: “To my mind the epitome of the perfect pairing is Marmite and toast. I wouldn’t normally use this to represent a fund pairing though, as both parties would object to being the love-it-or-hate-it Marmite. But in the case of Adam Rackley and his VT Cape Wrath Focus fund, I suspect he’ll take it as the compliment it is.

“This fund is Marmitesque because it’s small-cap, UK-focused and run on a contrarian value basis. These are things that, apparently, cause many professional fund buyers to be a bit sick in their mouth. Rackley is unapologetic for this. He knows, as do we, that if you want to make the highest long-term returns, there’s no richer hunting ground than small-cap value.”

Yet, Evan-Cook warned that investors in this fund are in for a bumpy ride, which is why it should be held alongside a few other UK equity funds that can compensate when it’s out of favour.

This is where VT Castlebay UK Equity, managed by David Ridland, intervenes. The fund focuses on quality companies higher up in the market-cap scale.

Evan-Cook said: “Pairings like these are bread and butter (plus spreads) for us within our Downing Fox funds. We want our investors to benefit from holding great active funds, but we also want them to have an emotionally easier journey than holding just one by itself.”

Over five years, the two funds have a 0.69 correlation with each other, according to FE Analytics.

Jason Hollands, managing director at Bestinvest

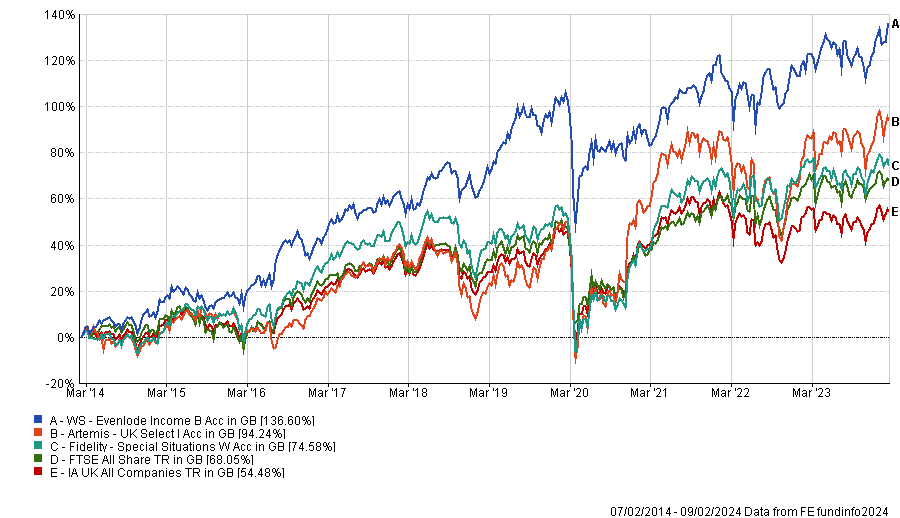

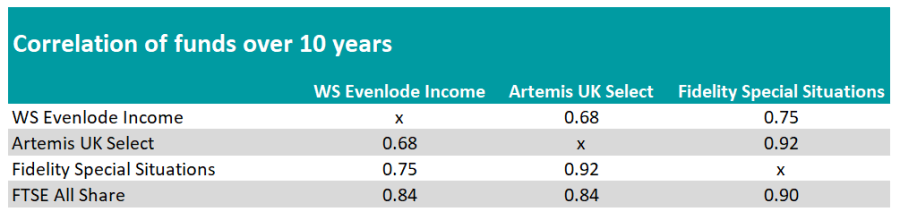

For his ideal allocation to UK equities, Hollands picked WS Evenlode Income, Artemis UK Select and Fidelity Special Situations.

Performance of funds over 10yrs vs sector and benchmark

Source: FE Analytics

WS Evenlode Income has a quality-growth bias and a strong international flavour, as most of its investee companies generate their earnings overseas, despite being based in the UK.

Hollands said: “The fund is managed with a team-based, collegiate approach from a barn conversion in Oxfordshire and targets companies with low capital intensity and high returns on capital that generate strong free cash flow, which can compound returns over time.

“The approach has a quality bias, with companies bought on a buy-and-hold, long-term basis. The investment process of avoiding companies involved in activities that require constant investment in plant and machinery means it has no exposure to capital intensive sectors like energy, but instead it has high relative weightings to industrials, consumer staples and technology.”

The Artemis UK Select fund offers a different sector exposure, with energy giants such as BP and Shell as well as banking stalwarts Barclays, Natwest and HSBC among its top holdings.

The fund’s managers, Ambrose Faulks and FE fundinfo Alpha Manager Ed Legget, roam across the whole UK market-cap spectrum to identify the best ideas, although they tends to focus more on large- and mid-cap stocks rather than smaller companies.

Hollands said: “The managers seek out companies they believe have good earnings growth prospects but where they believe the current valuations are too conservative and therefore have the potential to be rerated. While the fund isn’t a dogmatic ‘value’ fund that is solely focused on cheap shares, it does have a modest value style bias.”

Another particularity of the fund is its flexibility to take selective short positions in stocks the managers believe have got too expensive and/or where the share price could decline. It currently has three short positions.

Finally, the role of Fidelity Special Situations is to provide exposure to UK small and mid-cap companies. Although they have been out of favour in recent years, Hollands highlighted that ‘smid’-caps have historically provided “significant opportunities” for generating high returns over the long-term.

“Managers Alex Wright and Jonathan Winton are contrarian investors who seek out unloved companies with the potential for positive change. This can mean companies that have seen a change of management, which are undergoing a turnaround, have been hit by worries about regulatory disruption or where the competitive environment is improving,” Hollands explained.

“Backing these companies early enables the managers to benefit from re-rating as the wider markets eventually recognise the improving situation.”

Nick Wood, head of fund research at Quilter Cheviot

Nick Wood, head of fund research at Quilter Cheviot, recommended building an allocation to UK equities with Schroder Recovery and Liontrust UK Growth.

Performance of funds over 10yrs vs sector and benchmark

Source: FE Analytics

Schroder Recovery is a value fund, which currently has a meaningful bias down the cap scale relative to the index.

Wood said: “Schroder Recovery is one of the few pure value managers in the UK, with a track record of managing in the same way counted in decades.

“The team has been adept at managing through periods in which their style is somewhat out of favour, with the last 10 years primarily favouring growth investors, yet the fund proving able to match the market over that period.”

Liontrust UK Growth is the polar opposite of Schroder Recovery, as it follows a quality-growth style and has little exposure to the small and mid-cap space. Over 10 years, both funds have a correlation of 0.76 according to FE Analytics.

Wood added: “The team looks for companies with sustainable structural advantages and has a bias towards higher quality growth companies. There is a bias towards industrials, consumer and energy stocks, although the manager tends to avoid miners and banks.”

JLEN Environmental Assets Group Limited (“JLEN” or the “Company“), the listed environmental infrastructure fund, announces that its unaudited Net Asset Value (“NAV“) at 31 December 2023 was £777.7m (117.6 pence per share). This reflects a decrease of 2.1 pence per share since 30 September 2023 after paying the quarterly dividend of 1.9 pence per share.

Highlights in the period

· Solid operational performance with continued strong cash generation from investments

· Near term price fixes achieved in excess of valuation assumptions, partially mitigating downward movements from updated power price forecasts and actual inflation

· Continued focus on asset enhancements in the portfolio to increase operational efficiencies

· Acquisition of the remaining 30% shareholding in Bio Collectors Holdings Limited creating the potential for JLEN to deliver operational synergies across its portfolio of food waste anaerobic digestion plants

· Steady progress on development and construction assets in line with expectations

· Prudent balance sheet management maintaining low levels of gearing

Summary of changes in NAV:

Item

Pence per share movement

NAV at 30 September 2023

119.7p

Dividends paid in the period

-1.9p

Power prices (downward revision from forecasts offset by value accretive price fixes)

-1.5p

Battery storage revenue forecasts

-0.6p

Actual inflation

-0.7p

Other movements (including actual performance)

+2.6p

NAV at 31 December 2023

117.6p

Valuation factors

Key valuation movements include the negative impact from reductions in independent power forecasts (-2.3p), partially offset by the subsequent Electricity Generator Levy movement and favourable price fixes secured in the period (+0.8p). In addition to this, reductions in the gross margin forecasts for battery storage assets, prompted by independent consultants reappraising the available revenue opportunities, led to a -0.6p reduction. Lastly, there was also downward revision from the recognition of actual quarterly inflation finishing the calendar year below forecasts (-0.7p). The Investment Manager continues to monitor macroeconomic markers, including UK gilt yields, and consequently discount rates remain unchanged this period.

Gearing

At 31 December 2023 project level gearing was 17% and overall fund gearing was 30%, with the Company’s Revolving Credit Facility (“RCF“) £148.1m drawn from a total facility size of £200m. The Company continues to maintain sufficient headroom in its RCF to finance its firm commitments relating to construction assets held within the portfolio and earmarked follow-on investments.

Capital allocationstrategy

The Investment Manager continues to make good progress on selective asset disposals with several credible opportunities being pursued, in line with the Company’s capital allocation strategy.

As stated in previous announcements, surplus capital generated from the portfolio and from asset sales will be prioritised towards existing commitments, compelling follow-on investments and value enhancements, alongside managing the RCF to maintain a robust balance sheet and the potential for share buybacks.

Dividend

The Company also announces a quarterly interim dividend of 1.9 pence per share for the quarter ended 31 December 2023, in line with the dividend target of 7.57p per share for the year to 31 March 2024, as set out in the 2023 Annual Report.

Dividend Guidance Reaffirmed with Earnings Cover for the Full Year of Approximately Two Times

Bluefield Solar (LON: BSIF), the London listed UK income fund focused primarily on acquiring and managing solar energy assets, has today announced the Unaudited Directors’ Valuation as at 31 December 2023, equivalent to a Net Asset Value (“NAV”) of £831.3 million, or 136.0 pps (September 2023 136.4 pps, June 2023 139.7 pps).

Unaudited Net Asset Value as of 31 December 2023

Key movements in the NAV since 30 September 2023 include recognition of value from the Company’s Renewable Energy Guarantees of Origin certificates (“REGOs”) until 2030, which have been included in the valuation for the first time owing to sustained market prices over the last 12 months and expectations of future value from forecasters. In addition, the Company has recognised a slight uplift in expected power prices due to a small increase in long term power forecasts whilst short term hedging has predominantly offset reductions from near term power price weakness. There was additionally a minor negative adjustment due to operational cost updates and working capital movements.

The discount rate being applied remains unchanged at 8.0% (30 September 23: 8.00%) and inflation assumptions also remain unchanged from 30 September 23 (2024:3.5%, 2025-2029:3.0%, 2.25% thereafter). All other core assumptions also remain unchanged.

Pence per Ordinary Share

Unaudited NAV as at 30 September 2023

136.4

REGOs

0.9

Power prices

0.4

Operational cost update

-1.0

Other movements

-0.7

Unaudited NAV as at 31 December 2023

136.0

Full details on the movements for the 6 month period to 31 December 2023 will be outlined in the Company’s Interim Statement due for release on 28 February 2024.

Share Buyback Programme

The Board notes the recent weakness in the Company’s share price and the significant discount that the current share price represents to the value of the Company’s assets. Adjusting for the first interim dividend , the closing price of 99 pence per share (as at 14 February 2024) represents a discount of 26% to the 31 December 2023 NAV.

The Board of the Company keeps its capital allocation policy under regular review, evaluating the relative merits of further investment (into both new and existing assets), the management of debt and returning value to shareholders via dividends or through other methods such as share buybacks. As part of this review, and in the context of addressing what the Board views as the excessive discount at which the Company’s shares currently trade relative to the underlying NAV, the Board announces its intention to commence a share buyback programme. In the first instance it has allocated £20 million for the purchase of its own shares.

Share repurchases will be carried out under the existing shareholder authority granted at the last Annual General Meeting, held on 28 November 2023, which allows for purchases of Ordinary Shares by the Company in the market for up to 14.99% of the Company’s issued share capital. Any share repurchases will be funded from a combination of available liquidity, excess operating cash flows from the portfolio and the proceeds from any asset sales as already announced. It is expected that any share repurchases will be accretive to NAV per share.

The Company expects to announce its interim results for the half year ended 31 December 2023 on Wednesday, 28 February 2024. Until such announcement, the Company remains in a closed period in respect of those results and thus unable to buy its own shares, but the Board intends to commence share buybacks following the release of the interims and while the Company’s shares continue to trade at an excessive discount to NAV.

Dividend Guidance Reaffirmed

Shareholders will be aware that the Board of Bluefield Solar has recently declared a first interim dividend for the current financial year of 2.20 pps and has reiterated its target dividend for the full year of not less than 8.80 pps. This represents a dividend yield of 8.9% based on the closing share price of 99p per share on 14 February 2024. The Company’s operations remain robust, trading conditions are attractive, and the Board expects this year’s dividend to be approximately two times covered.

In line with the Company’s dividend policy, for the year ended 30th September 2023, four quarterly dividends of 3.42 pence were paid to shareholders. For the year to 30th September 2024, in the absence of unforeseen circumstances, a quarterly dividend of 2.76 pence per share will be paid. This represents an annual dividend of 4% of the Company’s NAV as at 29th September 2023.

Here’s how I could turn £15K into a £478K retirement pot by investing in FTSE 100 shares

Story by Sumayya Mansoor

I reckon it’s possible to build a retirement pot by investing in quality FTSE 100 shares.

Let me explain a method as to how I could do this with an initial £15,000 investment.

Breaking down the numbers

Since 1984, the UK’s premier index has returned 7.5% annually. This is a pretty good return, in my view. It’s much more than a low-yielding savings account that I could leave my money in. By the time I’m ready to retire, I would have nowhere near having enough money to retire on if I did that!

The first thing I would do is put £15K into a tax-efficient Stocks and Shares ISA

Next, I’d invest this amount into quality FTSE 100 shares

As well as my lump sum, I’m going to add £250 a month for 30 years

If I were to receive dividends, I would reinvest these too

I’m going to put a time frame of 30 years on my plan

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

The chart below shows how my investment could pan out.

Source: thecalculatorsite.com

It’s worth mentioning that dividends aren’t guaranteed and I’m conscious that past performance isn’t a guarantee of the future, so a 7.5% return may not come to fruition. Conversely, the rate of return could be higher!

Investing the right stocks is key. I would focus on diversification. So I would buy quality stocks from a number of sectors. For example, some banking and financial stocks, tech stocks, house builders, defence stocks, and more.

One pick I like

BAE Systems (LSE: BA.) is one of the world’s biggest defence businesses.

The shares have been on a great run recently. Over a 12-month period they’re up 38% from 888p at this time last year, to current levels of 1,234p.

I reckon a big reason for the recent rise has been geopolitical tensions across the world pushing up defence spending. I’m wishing for speedy and peaceful resolutions across all conflicts. However, it’s worth mentioning that defence spending covers much more than wars and weapons.

According to Statista, global defence spending is at all-time highs, and could continue on this trajectory. BAE’s excellent track record, reputation, and deep-seated relationships with leading governments puts it in a great position to boost performance and returns for years to come.

Next, the fundamentals at present look good. The shares trade on a price-to-earnings ratio of 19. This isn’t the lowest, but I’m willing to pay a fair price for a wonderful business. In addition to this, a dividend yield of 2.3% would boost my passive income.

All investments come with risks and BAE is no different. There is a chance defence spending could be scaled back if conflicts come to a resolution, impacting performance and BAE’s share price. However, defence covers much more than wars, such as cyber security, so I’m not too worried here. Another risk is if a BAE product were to fail, it could cause financial and reputational damage to the business.

I don’t have £15K right now but using the maths and method above, I could employ this to help me retire comfortably.