The Motley Fool

5 Steps to earning an extra £500 monthly passive income in 2024

It’s a brand new year, and many investors are looking to start building or expanding their passive income streams as part of a New Year’s resolution. That’s hardly surprising, given that making money without having to work for it is arguably one of the best ways to achieve financial freedom.

There are a lot of different ways to go about this. My personal favourite is capitalising on the potential offered by the stock market. After all, it doesn’t take that much capital to get the ball rolling and is far less time-consuming than managing rental property or running a business.

With that in mind, let’s go over the five main steps to earning an extra £500 each month.

1. Start saving

Like anything in life, investors need money to make money. Depending on the company, a share price can range from a few pence to hundreds of pounds. But there are also trading fees to take into consideration. Even with commission-free investment platforms, hidden fees can quickly eat into capital if not properly managed.

Therefore, it’s prudent for long-term investors to save spare money from a salary each month inside an interest-bearing savings account. Once a lump sum of around £300-£500 has been accumulated, then it’s time to start putting this cash to work.

2. Investigate like a detective

While saving, investors shouldn’t sit idle. Picking stocks successfully requires detailed analysis and research. And investors can use the time in between trades to find promising and potentially lucrative opportunities in the stock market.

Executing this due diligence is by far the most important step. And, sadly, it’s also the most time-consuming, especially for newer investors who have to learn what to look for in a company that makes it investment-worthy. Fortunately, our Share Advisor Premium Service can help make this process far easier.

3. Determine the end goal

With money at hand and top-notch stocks identified, it’s important for investors to outline what their objectives are. If the main one is to earn a passive income, then how much monthly income is desired?

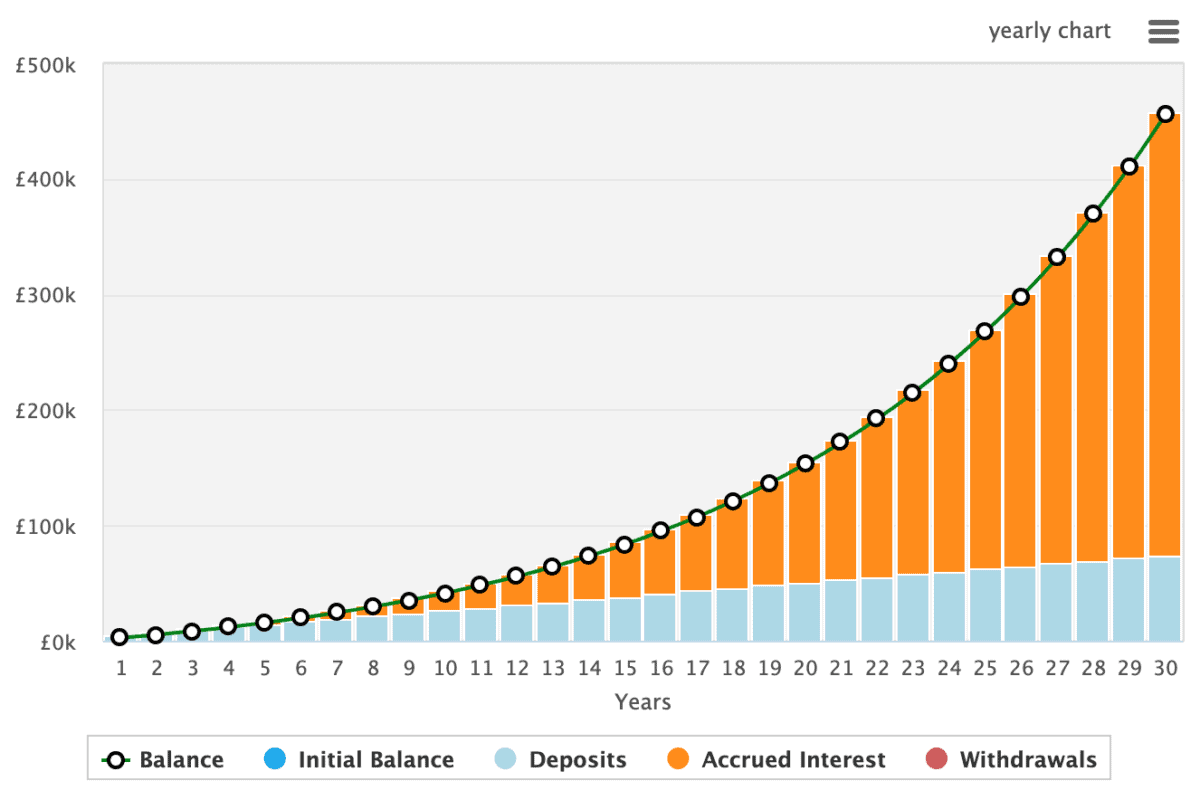

Knowing this enables building a timeline to keep expectations in check. For example, if I’m targeting an extra £500 a month, I need to earn £6,000 from my stock portfolio each year.

On average, UK shares offer a dividend yield of around 4%. By being more selective, it’s not unrealistic to push this to 6% a year without taking on too much additional risk. However, even at 6%, I’d still need a portfolio worth £100,000 to achieve my goal.

4. Invest!

Needless to say, £100k isn’t exactly pocket change. But don’t forget this is the destination, not the starting point. Given time, regularly investing £500 each month at a 10% annualised return would let me surpass this threshold within 10 years.

Of course, nothing’s guaranteed. The world of investing is rife with risk and uncertainty. And a poorly constructed portfolio may even destroy wealth instead of creating it. That’s why investors need to carefully consider the risks against the potential reward before making any investment.

5. Repeat

After adding the first top-notch stock to a portfolio, the final step is to start again. Regularly saving up money for investment allows for a steady drip-feed of capital into a portfolio, accelerating compounding and pushing investors closer to their passive income goals.