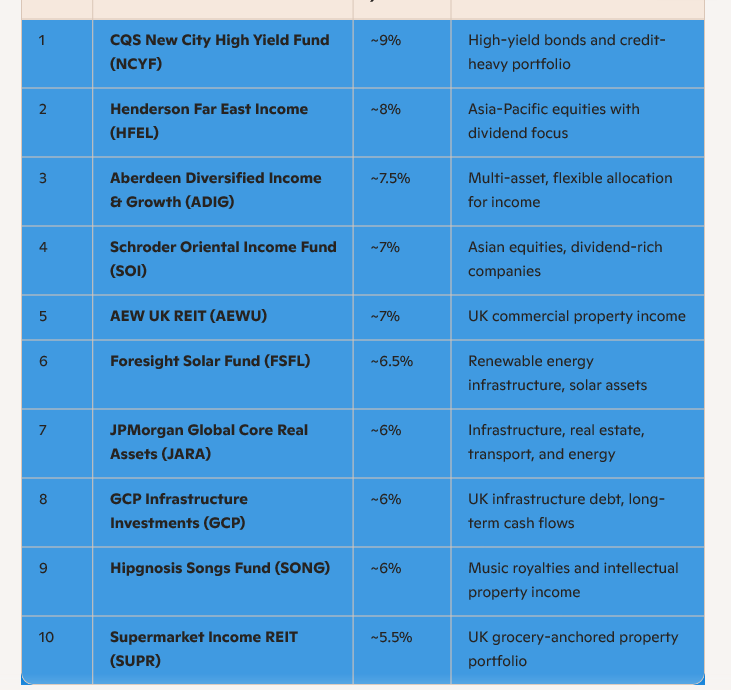

Here are ten of the highest-yielding investment trusts currently available in 2025, offering strong income potential for investors seeking dividends.

🔝 Top 10 High-Yielding Investment Trusts (2025)

📌 Key Insights

Credit-heavy trusts like NCYF and HFEL deliver the highest yields but carry interest rate and credit risk.

Property and infrastructure trusts (AEWU, SUPR, GCP, FSFL) provide stable cash flows tied to long-term contracts, though they are sensitive to property valuations and energy prices.

Asia-Pacific equity income trusts (HFEL, SOI) benefit from dividend-rich markets in Hong Kong, Singapore, and Australia.

Alternative assets like Hipgnosis Songs Fund show how investment trusts can generate yield from non-traditional sources such as royalties.

⚠️ Risks to Consider

Leverage: Many high-yield trusts use borrowing to enhance returns, which magnifies both gains and losses.

NAV erosion: High payouts can sometimes exceed earnings, leading to long-term capital decline.

Sector concentration: Property and infrastructure trusts are vulnerable to regulatory changes and economic cycles

Given the Snowball’s fascination with cycles of resilience and decline, these high-yield trusts are perfect case studies. They embody the tension between short-term income allure and long-term sustainability. For your creative projects, you could symbolize them as “Yield Sirens”—tempting investors with high payouts but demanding vigilance against hidden risks.

AI generated information contains many errors so even more critical you DYOR.

SONG no longer quoted, double check the yields.

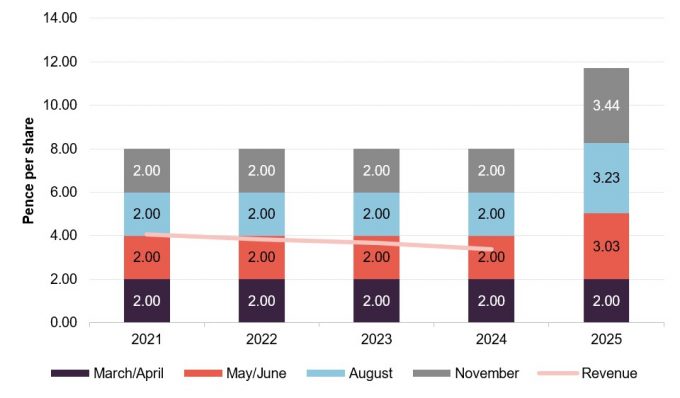

Price divided by the yearly dividends = yield

Example

SUPR 82p target dividend 6.1p = yield 7.5%

No dividends are 100% secure, all though some are more secure than others.

Here’s how I pick dividend shares to target a £20k retirement income

Are you considering using the stock market to supplement your retirement income? Our writer examines how dividend shares can help achieve those goals.

Posted by

Mark Hartley

Published 4 December

Image source: Getty Images

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

If you’re thinking of investing in dividend shares for retirement, you’re not alone. Thousands of Britons do exactly that, with the aim of achieving a steady income stream to supplement their State Pension.

The question is, where and how to start ? Many beginner investors feel overwhelmed by the sheer number of options available. For many, a lack of clarity and understanding leads to fear of losses, and they give up.

Should you buy Legal & General Group Plc shares today?

But with careful planning, patience and commitment, the risks can be minimised and the gains optimised.

A balanced approach

As with everything in life, picking the ideal dividend portfolio requires careful moderation. Choosing all the 10%-yielding stocks might seem logical, until half of them pause their dividends to finance debt.

Choosing all the stocks with the longest track record of payments is wiser — but the average yield might be underwhelming. Anything below 4% is barely outpacing a standard savings account.

A smarter option would be to mix some high-yielders with some reliable dividend heroes — those with decades-long track records. An average yield of 7% is realistic, requiring £285,700 to pay out £20,000 a year in passive income.

A 40-year-old investing £300 a month could reach that amount by age 65 (with dividends reinvested).

Identifying dividend gems

A typical investment portfolio includes between 10-20 stocks from a diverse range of sectors and regions. When it comes to dividends, some of the most popular sectors are finance, utilities, real estate, energy and consumer staples.

Here are two diverse UK dividend shares to consider, each complementing a retirement portfolio in their own way.

Legal & General (LSE: LGEN) has long been a top choice for UK retirement portfolios, offering a combination of high yield and structural appeal. The company operates in life insurance, pensions and asset management — sectors directly tied to retirement savings and long-term demographic trends like population ageing.

The key attraction, of course, is its predictable, dividend-focused cash generation. With a business model that centres around pension risk transfer and workplace retirement solutions, it enjoys recurring revenue streams largely insulated from short-term economic cycles. This close relationship with retirement planning makes it a natural fit for income-focused investors to consider.

The combination of high yield (9%+) and reliable track record make it a rare find — but it’s still at risk from interest rate sensitivity. As an insurance and annuities company, its profitability and solvency are heavily dependent on interest rate movements.

By contrast, National Grid offers a much smaller yield but benefits from more defensive, inflation-linked income. As a regulated electricity and gas supplier, its earnings are set on a multi-year basis. This gives it long-term visibility over cash flows, supporting a dividend policy that grows in line with UK inflation.

The bottom line

When selecting dividend shares, consider balancing yield with sustainability, as higher yields can reflect market concerns about dividend safety. Diversifying across multiple dividend sectors helps manage risk while maintaining steady income streams.

The above options are just two examples of how yield and sustainability can be balanced. There’s a host of similarly attractive UK dividend shares to choose from on the FTSE 100 and FTSE 250. One of the hardest steps is getting started – after that it just requires committed monthly contributions and a big dollop of patience.

The Board of Directors of the Company has declared an interim dividend of 1.44 pence per share in respect of the period to 31 December 2024. The dividend will be paid on 31 December 2025 to shareholders on the register as at 12 December 2025. The ex-dividend date is 11 December 2025. This distribution is necessary to make sufficient distributions so that no corporation tax liability will arise in the Company as noted in the Company’s 2024 Annual Report and Accounts.

The next dividend declaration is likely to be announced in February 2026, then every year thereafter. The dividends will not be less than 85% of net revenue return of the period distributed, as previously disclosed.

The Company has elected to designate all of the interim dividend as an interest distribution to its shareholders, thereby “streaming” income from interest-bearing investments into dividends that will be taxed in the hands of shareholders as interest income. No income tax will therefore be deducted at source from this, or from future interest distributions.

The Snowball has a position in VPC and will be sold when the balance of cash is returned, the next date is February.

The sale will be at a loss, even allowing for the income earned on £5,345 of re-invested dividends but an un-expected dividend of £180 to be added to the total.

If I could just advise you of just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are.

Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $96,970 by 2023, or 97x your money.

But the same $1,000 in the non-dividend payers would have grown to just $8,990 — 91% less.

That’s why I’m a dividend fan.

The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up!

There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives us dividend investors such an edge.

When you lock in an 8%+ yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

So let’s wipe the false promises of mainstream finance from our minds and start thinking the “No Withdrawal” way…

I’ve bought for the Snowball 13680 shares in NewRiver REIT plc for 10k.

Current yield 8.9% NTAV £485.6 Capital £311.9m

NewRiver REIT plc

(“NewRiver” or the “Company”)

Dividend Declaration

As announced on 2 December 2025, the NewRiver Board has declared an interim dividend of 3.1 pence per share in respect of the six months ended 30 September 2025. This dividend will be paid as a Property Income Distribution (PID).

The dividend payment date will be 30 January 2026 and the dividend will be paid to shareholders on the register at close of business on 12 December 2025. The ex-dividend date will be 11 December 2025.

Shareholders can receive additional new ordinary shares in the Company instead of their cash dividend, with no dealing charges or stamp duty incurred, under the Company’s scrip dividend scheme. To receive the scrip dividend, shareholders need to make an election ahead of the dividend election date on 9 January 2026.

As NRR only pays a dividend twice a year, the dividend for the Snowball will be £424.00

I’ve sold the recent purchase of ENRG for a profit of £158.00.

The current profit on the recent sells is £1,370.00, although the Snowball’s Raison d’être is only to earn dividends to reinvest to earn more dividends, I am risking the current profit to provide an approximate buffer of 1k for the 2026 Snowball.

Current earned dividends for January £539.00

I intend to re-invest the funds to earn another dividend for next year.

BlackRock American Income Trust – And now for something completely different

27 November 2025

QuotedData

And now for something completely different

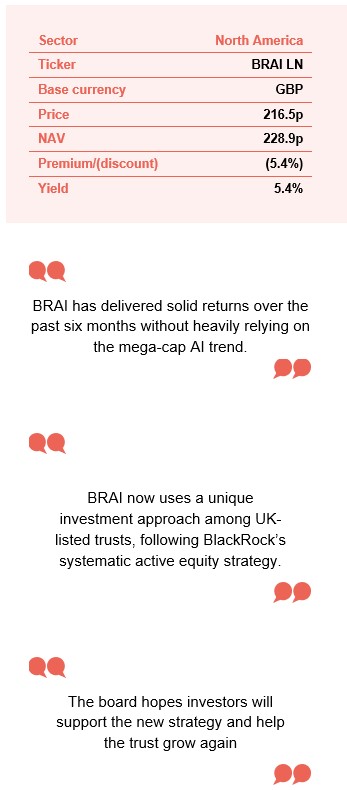

Earlier this year, BlackRock American Income (BRAI) announced a radical shake up. It asked shareholders to approve a new investment objective and policy, announced a new enhanced dividend policy, cut management fees drastically, and offered shareholders a 20% tender at a 2% discount to NAV (after costs).

The proposals were welcomed by investors, with more than 99% of those voting giving their approval. The tender offer was undersubscribed, with just 16.15% of BRAI’s shares validly tendered.

In its new form, the trust is following an investment approach distinct from any other investment company listed in the UK – investing using a systematic active equity approach devised by BlackRock (which uses data-driven insights to identify and take advantage of mispriced stocks). This note seeks to explain BRAI’s new approach and the corporate structure that supports that. Whilst we have included some historical performance data for reference in the charts on this page, further analysis of it feels redundant. Instead, we have focused on BRAI’s returns since the strategy change.

The portfolio continues to focus on income and capital growth from US value stocks, offering diversification for investors mainly exposed to large US tech stocks. There has been a major change in how investments are chosen, detailed further below.

Attractive income and growth from US value stocks, using a systematic active equity approach

BRAI aims to provide long-term capital growth, whilst paying an attractive level of income (1.5% of NAV per quarter, around 6% of NAV per annum). BRAI follows a systematic active equity approach that aims to provide consistent outperformance of the Russell 1000 Value Index (the benchmark).

At a glance

Share price and discount

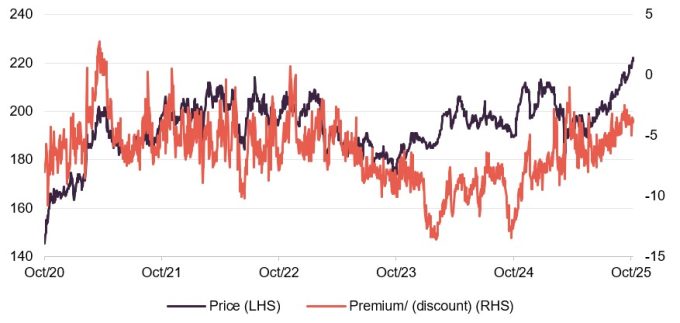

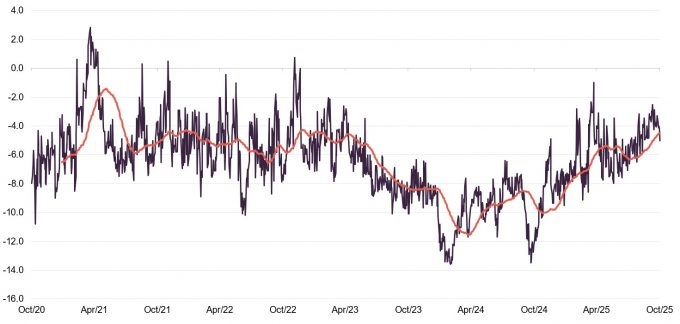

Over the 12 months to 31 October 2025, BRAI’s shares traded at a discount to NAV ranging from 11.9% to 1.0%, averaging 6.3%. As of 26 November 2025, the discount stood at 5.4%.

The discount increased during 2023 as markets were led by the Magnificent Seven and value stocks lagged. BRAI’s rating started to recover in October, helped by the expected tender offer, and is now at a more reasonable level. The board hopes investors will support the new strategy and help the trust grow again.

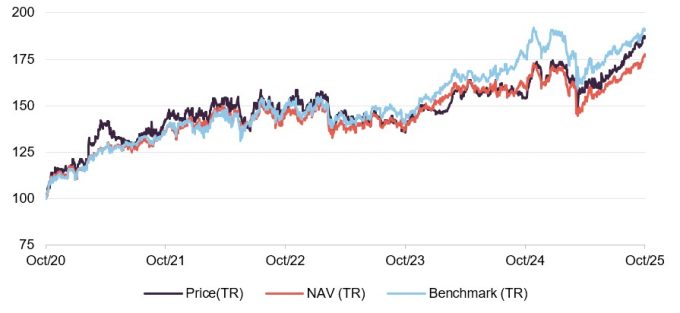

Time period 31 October 2020 to 25 November 2025

Source: Bloomberg, Marten & Co

Performance over five years

As mentioned earlier, we do not consider BRAI’s returns before the strategy change relevant, however the graph here shows BRAI’s share price and NAV performance compared to its benchmark over the past five years. Figure 7 on page 9 illustrates BRAI’s strong start, regularly outperforming its objective. The S&P 500’s gains have been driven by a few large AI-related companies, while BRAI’s benchmark is more diversified. Notably, BRAI has delivered solid returns over the past six months without heavily relying on the mega-cap AI trend.

Time period 31 October 2020 to 31 October 2025

Source: Bloomberg, Marten & Co

More information is available on the trust’s website

How does new BRAI differ from old BRAI?

The portfolio continues to focus on income and capital growth from US value stocks, offering diversification for investors mainly exposed to large US tech stocks. There has been a major change in how investments are chosen, detailed further below.

The largest holding in any single stock is now capped at 1.5%. The number of stocks has increased from around 60 to 232 as of September 2025, reducing risk from individual companies.

Previously, the investment policy excluded some stocks for ESG reasons, but the new approach allows for a broader range of investments.

Costs have been significantly reduced, with the base management fee halved and a new tiered structure introduced (see page 11). Dividends have also increased to 1.5% per quarter, or about 6% a year (see page 9).

Regular exit opportunities linked to performance have been introduced, and investors will also have an exit option if the trust does not grow (see page 10).

What is systematic active equity?

Data-derived insights to spot mispriced stocks

BlackRock’s Systematic Active Equity (SAE) team uses data-driven insights to identify and take advantage of mispriced stocks. By September 2025, BlackRock managed over $313bn with this strategy across a range of global and regional portfolios, including long-only, partial short, hedge funds, and a London-listed investment company – the first of its kind. The SAE team has over 100 investment professionals in San Francisco and London, drawing on more than 40 years of experience in active investment management. While BRAI’s investment universe is no longer limited by ESG criteria, ESG analysis remains part of the research process.

BRAI’s universe is no longer constrained by ESG criteria

Continuous innovation

The SAE team is constantly innovating to improve results for investors. While quant-driven strategies have existed for years, managers now have access to much more data. Their role is to decide which information is useful, when to use it, how different datasets work together or during specific economic periods, and how much weight to give each insight when making investment decisions.

Few asset managers have the scale to succeed in this area

The SAE team was an early adopter of AI and machine learning

Processing this information requires significant computing power, which only a few asset managers can access at scale. The managers note that while early fundamental value data was structured and easy to analyse, most current datasets are unstructured text. The SAE team adopted AI and machine learning early to interpret this data effectively.

Beyond traditional company analysis, the SAE team uses hundreds of independent data sets, such as analyst reports, news articles, online search trends, transaction volumes, footfall, and app usage. On average, they assess 10 new data sets each month. Macroeconomic indicators are also included, using “now-casting” to gauge the economy’s current state.

Insights are thoroughly tested for their ability to predict company fundamentals and returns, with tools that can run a five-year back test in under two seconds. Managers retain final decision-making, and may delay trades during major market shocks.

The SAE approach leads to higher portfolio turnover (about 100%–200% per year), but trading costs are considered in every decision. Many trades are matched within BlackRock, helping to keep transaction costs down.

The output

The analysis covers:

Company fundamentals, including profitability, growth, financial strength, valuation, and management quality.

Market sentiment, considering analyst and investor views, management outlook, and investment flows. It also looks at whether the wider market environment and similar businesses support the stock.

Macroeconomic themes across industries, countries, and investment styles.

ESG risks, including how a business is exposed and what steps it is taking to manage them, how companies treat their staff, customers, and suppliers, and whether they face risks from the move to a carbon-neutral world.

The managers use a set of signals to score each stock, blending these scores to form an overall view. Stocks with higher scores are expected to deliver better returns, guiding the portfolio’s construction to balance risk and return after costs.

The portfolio usually holds 150 to 250 large- and mid-cap stocks. While BRAI can invest up to 20% of assets outside the US, it is now likely to be fully invested in US equities.

The macroeconomic backdrop

Markets have recovered from the selloff associated with Liberation Day

President Trump’s policy agenda, especially his tariff policy, has had a major impact on global markets. After quickly imposing tariffs on imports from Canada and Mexico, the key moment came on “Liberation Day” (2 April 2025) when tariffs were announced on almost all imports. Markets reacted negatively, prompting a temporary reduction of most tariffs to 10%. This led to a market recovery, helped by announcements of various trade deals, though not all are finalised, which encouraged a return to risk-taking.

The AI investment boom, which started in March 2023 with ChatGPT-4, faced its first major challenge in January 2025 when DeepSeek claimed to have developed a new large language model at much lower cost than US rivals. This caused a sharp sell-off in the Magnificent Seven tech stocks, with money moving into other US stocks and overseas markets. These large US tech companies were also affected by the Liberation Day market falls. Despite this, investment in AI infrastructure continued strongly, helping to restore confidence.

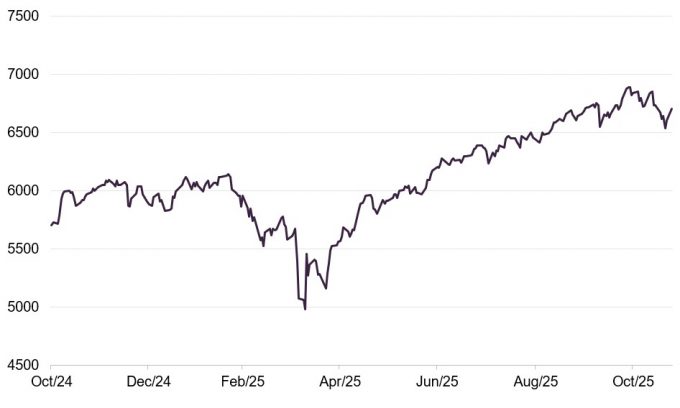

Today, US mega-cap tech stocks once again lead the S&P 500. For investors who want US exposure but prefer not to concentrate too heavily on these giants, BRAI offers useful diversification.

BRAI offers a way of diversifying US exposure away from the Mag 7

Figure 1: S&P 500 Index over 12 months to end October 2025

Source: Bloomberg

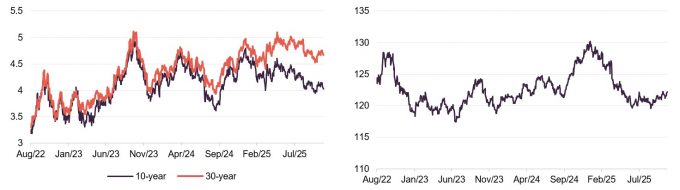

The US president has pushed for lower interest rates, but the Federal Reserve has resisted, citing worries about inflation from tariffs. Threats to dismiss Fed board members and its chair could hurt confidence in US bonds. US inflation has been rising anyway.

Debt investors are also worried about the long-term impact of the One Big Beautiful Bill (OBBB), which is expected to add trillions to the US deficit. If government borrowing costs also rise, this could cause further issues.

Figure 2: US long-term government bond yields

Figure 3: US dollar trade-weighted index

Source: Bloomberg

Source: Bloomberg

These concerns have likely weakened the US dollar, which has dropped sharply from its February peak on a trade-weighted basis. The decline could continue if investors move more money out of US assets.

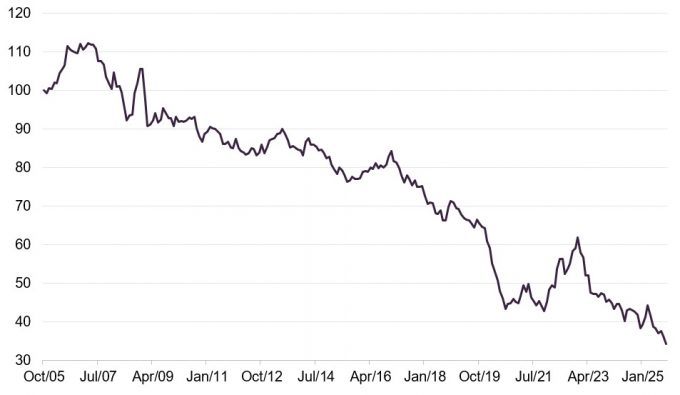

Figure 4: Value versus growth in US market

Source: Bloomberg (based on MSCI US value and growth total retu

For BRAI, the key issue is how value stocks perform compared to growth stocks. As Figure 4 shows, value stocks have lagged behind growth stocks over the past 20 years, mainly due to the long period of low US interest rates after the 2008 financial crisis.

In late 2021, expectations of rising interest rates sparked a rally in value stocks, but this peaked at the end of 2022. Since then, growth stocks have outperformed again, driven largely by the success of AI. Another potential value rally was cut short by Liberation Day.

The managers note that unpredictable US policy changes make their job more challenging but also create unusual investor behaviour, leading to more mispriced stocks.

The portfolio was fully realigned to the new strategy by 22 April 2025, with no cost to ongoing shareholders due to the manager’s contribution to expenses and the NAV uplift from the tender offer. Previously, almost 10% of BRAI’s portfolio was in non-US stocks, but it is now entirely invested in US stocks.

Marked shifts in sector and stock exposures

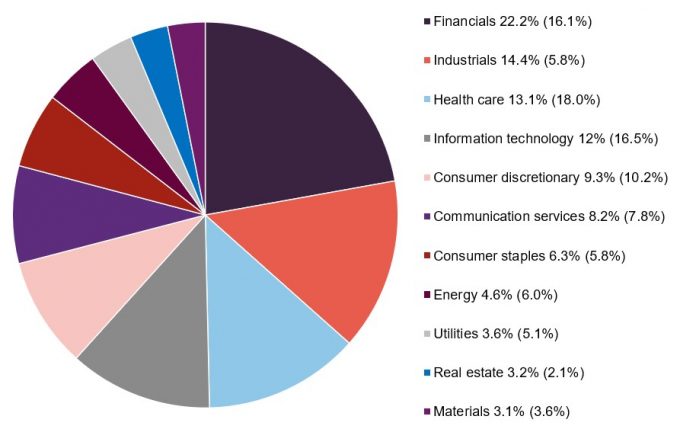

Figure 5 shows the portfolio breakdown by industry sector as at 30 September 2025, compared to the end of the last financial year (31 October 2024). There have been significant changes, with much higher exposure to financials and industrials, and lower exposure to healthcare and information technology. The net effect is that, on a sector basis, the portfolio now closely matches the benchmark, so most of the added value comes from choosing the right stocks.

Figure 5: BRAI asset allocation by sector as at 30 September 2025 (and as at 31 October 2024)

Source: BRAI

There is very little overlap between BRAI’s 10 largest holdings at the end of its last financial year (31 October 2024), before the new investment approach, and the top positions in the portfolio at the end of September 2025.

Figure 6: Top 10 holdings as at 30 September 2025

% as at 30/09/25

% as at 31/10/24

Change

JPMorgan Chase

Financials

3.2

–

3.2

Berkshire Hathaway

Financials

2.8

–

2.8

Walmart

Consumer staples

2.6

–

2.6

Amazon

Consumer discretionary

2.6

1.7

0.9

Bank of America

Financials

2.3

–

2.3

Alphabet

Communication services

1.9

–

1.9

Morgan Stanley

Financials

1.9

–

1.9

Johnson & Johnson

Health Care

1.8

–

1.8

Charles Schwab

Financials

1.7

–

1.7

Pfizer

Health Care

1.6

–

1.6

Total

22.3

Source: BRAI

Performance

Building a track record of outperformance

As mentioned earlier, we do not consider BRAI’s returns before the strategy change relevant here. Figure 7 shows BRAI’s share price and NAV performance compared to its benchmark and the S&P 500 Index.

The data indicate that BRAI has made a strong start, regularly outperforming its objective. The S&P 500’s gains have been driven by a few large AI-related companies, while BRAI’s benchmark is more diversified. Notably, BRAI has delivered solid returns over the past six months without heavily relying on the mega-cap AI trend.

It is still too soon to assess the volatility of these returns, but we will cover this in future reports.

Figure 7: Total return performance data for periods to end October 2025

Calendar year

1 month (%)

3 months (%)

6 months (%)

Since 22 April 2025 (%)

BRAI share price

2.3

8.6

17.7

16.6

BRAI NAV

3.6

8.1

17.2

21.4

Russell 1000 Value

2.9

5.9

15.1

18.5

S&P 500

4.9

9.0

25.6

32.3

Source: Bloomberg

Dividends

New enhanced dividend policy roughly 6% of NAV each year

From 17 April 2025, BRAI began paying a quarterly dividend equal to 1.5% of its NAV, or about 6% per year. The chart’s x-axis shows past ex-dividend dates, and future payments are planned for April, July, October, and January.

Figure 8 highlights BRAI’s dividend history over five years, with the final column showing the impact of the higher dividend policy.

To support these higher dividends and potential share buybacks, BRAI had £105.7m in distributable reserves at the end of April 2025. Paying dividends above net revenue is not new for BRAI, as its dividends have not been covered by earnings since FY 2017. This approach allows BRAI to invest flexibly across the US market, aiming to maximise total returns without needing to focus on high-yielding stocks.

Figure 8: BRAI five-year dividend history for financial years ending in October

Source: BRAI, Marten & Co

Premium/(discount)

Over the 12 months to 31 October 2025, BRAI’s shares traded at a discount to NAV ranging from 11.9% to 1.0%, averaging 6.3%. As of 26 November 2025, the discount stood at 5.4%.

The discount increased during 2023 as markets were led by the Magnificent Seven and value stocks lagged. BRAI’s rating started to recover in October, helped by the expected tender offer, and is now at a more reasonable level. The board hopes investors will support the new strategy and help the trust grow again.

Conditional tender offers

If BRAI does not outperform its benchmark by at least 0.5% a year after fees over three-year periods (the first ending 30 April 2028), it will offer shareholders a 100% tender at a 2% discount to NAV after costs. This tender offer will also be made if the company’s net assets fall below £125m at the end of any of these periods.

Figure 9: BRAI’s premium/(discount) over the five years ended 31 October 2025

Source: Bloomberg, Marten & Co

Structure

Capital structure

BRAI has 95,361,305 ordinary shares, with 38,949,167 held in treasury, leaving 56,412,138 shares with voting rights. Its financial year ends on 31 October, with AGMs usually in March. The board plans to announce the next annual accounts in January 2026. Shareholders approved the company’s continuation at this year’s AGM, with the next vote set for 2028 and every three years after that.

Fees and costs

From 17 April 2025, BRAI’s management fee is tiered: 0.35% on the first £350m of NAV and 0.30% on any amount above that. There is no performance fee.

The ongoing charges ratio for the year ended 31 October 2024 was 1.06%, based on the previous 0.70% management fee. With the reduced fee, this ratio should be significantly lower in this and future years. The board has estimated that over a full 12-month period under the new fee, the ongoing charges ratio is expected to decrease to around 0.70%–0.80%.

The managers

BRAI’s alternative investment fund manager is BlackRock Fund Managers Limited, while BlackRock Investment Management (UK) Limited serves as its investment manager and company secretary. The lead managers for BRAI are Travis Cooke and Muzo Kayacan.

Travis Cooke

Travis leads the US portfolio management group in BlackRock’s systematic active equity team, overseeing US long-only, partial long-short, and long-short equity strategies. He joined Barclays Global Investors in 1999, which merged with BlackRock in 2009, and was previously a portfolio manager for developed market strategies in the alpha strategies group. Travis holds a BA in Business Economics from the University of California, Santa Barbara (1998), an MSc in Finance from London Business School (2008), and has been a CFA charterholder since 2001.

Muzo Kayacan

Muzo is a portfolio manager and head of EMEA product strategy in the SAE division. He manages US, global, and European funds, and leads the EMEA product strategy team, which connects investment teams and clients.

Before joining BlackRock in 2010, Muzo was a senior associate portfolio manager at AllianceBernstein, where he implemented investment decisions for global equity portfolios and managed currency hedging strategies. From 2005 to 2007, he completed a graduate training scheme at M&G and then worked in product development. Earlier, he was a futures trader.

The board

BRAI has four non-executive directors, all independent of the manager. Alice Ryder stepped down as chair and director after the last AGM, with David Barron taking over as chair. Gaynor Coley is the newest director and now chairs the audit committee, replacing David Barron.

Figure 10: Directors’ length of service, fees, and shareholding

Role

Appointed

Length of service (years)

Fees (£)

Shareholding

David Barron

Chairman

22/03/2022

3.7

45,000

11,677

Gaynor Coley

Chair of the audit committee

25/06/2025

0.4

39,000

10,000

Solomon Soquar

Senior independent director

21/03/2023

2.7

32,500

10,000

Melanie Roberts

Director

01/10/2019

6.2

32,500

10,000

Source: Marten & Co

David Barron

David has 25 years’ experience in investment management. He was chief executive of Miton Group Plc until November 2019, after six years with the company. Before that, he spent over 10 years as head of investment trusts at JPMorgan Asset Management, joining Robert Fleming in 1995. He is now chairman of Baillie Gifford European Growth Trust Plc and, until its planned merger, a non-executive director of Fidelity Japan Trust Plc.

Gaynor Coley

Gaynor Coley is a chartered accountant with over 30 years’ experience in private and public sector finance, focusing on governance, compliance, and risk management. She is a non-executive director and audit committee chair at Foresight Enterprise VCT Plc and Lowland Investment Co Plc, and also chairs the grants committee and serves as a trustee for the Duchy Health Charity.

Solomon Soquar

Solomon Soquar has over 30 years’ experience in investment banking, capital markets and wealth management. He has held senior roles at major firms such as Goldman Sachs, Bankers Trust, Merrill Lynch, Citi and Barclays, most recently serving as CEO of Barclays Investments Solutions Limited. In recent years, he has taken on a range of roles, including non-executive director at Ruffer Investment Company Limited, chair of the Africa Research Excellence Fund, and business fellow at Oxford University’s Smith School of Economics and Enterprise.

Melanie Roberts

Melanie Roberts is a partner at Sarasin & Partners LLP with 29 years of investment experience. She joined the firm in 2011 and became head of charities in January 2023, focusing on strategy, stewardship, and client service for charity portfolios. Before this, she spent 16 years at Newton Investment Management managing charity, private client, and pension fund portfolios.

IMPORTANT INFORMATION

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on BlackRock American Income Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

I Am Betting Big On This Near-Perfect 8%-Yielding Income Machine For Early Retirement

Samuel Smith

Dec. 02, 2025

Summary

This 8%-yielding machine is positioned for very strong upside, growing passive income, and relatively low risk.

The market is ignoring this unrivaled combination of quality, growth, and high yield.

Don’t miss out on three of my largest holdings.

RerF/iStock via Getty Images

I love investing in high-quality, high-yielding stocks that trade at attractive valuations because I believe that this is one of the surest paths to generating long-term total return on performance. This is because these types of companies do not need to deliver much in the way of growth. They still deliver a satisfactory 10 to 12% annualized total return that is in line with long-term averages for the S&P 500 (SPY) and dividend growth ETFs like the Schwab U.S. Dividend Equity ETF (SCHD).

However, by investing in individual stocks on a value basis, you can then overlay a capital recycling strategy to further accelerate the compounding process by selling these types of stocks once they appreciate the full value, and then recycling the capital to other attractively valued high-yielding opportunities.

In today’s article I am going to share are three of some of my highest conviction high-yield bets right now that I have significantly outsized positions in, and I believe will take me a long way towards achieving my passive income goals due to their high yields, high quality, and attractive valuations.

A Tax-Deferred Energy Infrastructure Gem

The first opportunity I’m going to talk about is Enterprise Products Partners (EPD). It is a leading midstream energy infrastructure MLP (AMLP) that issues a K-1 tax form. While some may view that as a deal breaker, I love it because it generally means that the distributions are tax deferred until I sell, and if I never sell my EPD units and I purchase more units over time to keep my cost basis above zero and then pass them on to my heirs, I will never pay taxes on them. Either outcome would be a win for me because if I sell my units, it means that they likely delivered significant total return outperformance, and I can still sell them at long-term capital gains rate, and if I never sell, then I get a lot of passive income tax-free and can pass on a high-quality income machine to my heirs.

EPD’s strength derives from its high-quality, fully integrated, and well-diversified portfolio of energy infrastructure, including pipelines, storage assets, processing plants, and export terminals for natural gas liquids, crude oil, and natural gas. Additionally, the vast majority of its cash flow is contracted and fee based, which means it is fairly well insulated against commodity price volatility.

Not only that, but it also has the only A- credit rating in the midstream sector, reflecting the fact that it has the strongest balance sheet among peers, including C-corporations like Enbridge (ENB) and Kinder Morgan (KMI). This is not surprising given that it has a 3.3x leverage ratio that is likely going to plummet next year as significant projects come online and begin generating EBITDA. Additionally, it has $3.6 billion of liquidity with a 17-year weighted average return to maturity on its debt.

Moreover, its distribution of nearly 7% on a next twelve-month basis is covered 1.5x by distributable cash flow, and that coverage ratio should only increase over the coming year as projects come online and it initiates a unit repurchase program that should, both of which should contribute to an improving distribution payout ratio. When you combine the company’s fundamental strength with its attractive yield and the potential for significant buybacks next year due to it authorizing a $3 billion buyback authorization with expected decline in growth capex by at least $2 billion next year, freeing up significant free cash flow, EPD looks very compelling right now.

High-Yield Exposure to Private Credit

The next income machine I am going to talk about is Morgan Stanley Direct Lending (MSDL), which is a business development company (BIZD) that is managed by Morgan Stanley (MS). My favorite thing about MSDL is that about 96% of its portfolio is invested in first lien senior secured loans. When combined with the fact that they are primarily sponsor-backed businesses with low-weighted average loan-to-values of about 40%, and the fact that MS is a reputable manager that owns about 11% of the underlying equity in MSDL and charges one of the most shareholder-friendly fee structures, I have a high degree of confidence in MSDL’s fundamental performance moving forward.

Thus far, it has done very well on that front, as non-accruals are only 1.2% of the portfolio cost and 0.6% at fair value, and PIK income remains one of the lowest in the sector at just 4% of total income, which is in fact about half of the sector’s average. The company also fully covers its dividend with $0.50 per share in net invested income this past quarter that is in line with its $0.50 per share quarterly dividend.

Additionally, it has been making improvements to its balance sheet by closing its first CLO at an attractive SOFR plus 1.7% rate, and also repriced its asset-based facility to SOFR plus 1.95%, which combined to help offset some of the headwinds against recent Federal Reserve rate cuts to net investment income per share. With the discount to NAV sitting at a mid-teens percentage at a time when peers like Ares Capital Corporation (ARCC) and Blackstone Secured Lending (BXSL) trade roughly in line with NAV, MSDL looks extremely cheap. In addition, it pays an 11.7% dividend yield that is fully covered by underlying net investment income, and even if it has to trim its sum due to future Federal Reserve rate cuts, it is still likely to remain at 10% or above on its current stock price for the foreseeable future, making it a very good source of passive income.

An Alternative Asset Manager with Massive Growth

The third income machine I am going to talk about today is Blue Owl Capital (OWL), which is an alternative asset manager similar to Blackstone (BX) and Brookfield Asset Management (BAM)(BN). It invests across three major business segments including direct lending, GP stakes, and real assets.

Its direct lending business represents about half of its assets under management and has been a big driver of its recent growth due to the boom in private credit and direct lending. GP stakes has also been performing well given the growing interest in alternatives and its real assets business has seen strong performance in its triple net lease business and explosive growth thus far in its digital infrastructure business as the company is making investments in the data center build-out for hyperscalers like Meta (META). With management fees up 29% year-over-year and company posting record fundraising of $57 billion over the past 12 months with $28 billion of undeployed capital that is expected to generate an additional $360 million in annual management fees as it is deployed, OWL has phenomenal growth momentum right now. In fact, at their latest investor day, management guided for an over 20% fee-related earnings per share CAGR over the next five years. When combined with its current 6% dividend yield and its investment grade balance sheet, OWL appears to be a very attractive combination of high current yield and very strong growth for the foreseeable future.

Risks & Investor Takeaway

Of course, no investment is risk-free. While EPD is a low-risk investment, its unit price does remain sensitive to energy price volatility in the near term, even if its cash flows are much more resilient. Additionally, it is heavily invested in NGL exports, which are dealing with some overcapacity challenges right now, and its significant investments in growth projects do expose it to execution risk, even if its track record is very strong.

MSDL is invested in the private credit space, which has been receiving a lot of negative press recently. While I believe that much of this is unwarranted hype, it is true that there is a possibility that the sector has engaged in risky lending practices and or a material economic downturn could lead to a spike in non-accruals. Additionally, the Federal Reserve’s potential to accelerate rate cuts under President Trump’s replacement for Jerome Powell next year could weigh heavily on net investment income per share and lead to a material dividend cut. However, this would likely affect the entire sector, so we do not think that MSDL will be penalized by Mr. Market for it. Instead, its performance will likely be much more dependent on its underwriting performance. Given the huge discount to NAV, we think the upside potential is much greater than the downside potential.

Finally, OWL is also exposed to private credit, which has been receiving a lot of negative press recently and is also invested in the digital infrastructure space, which is also suffering from concerns about an AI bubble. However, OWL’s private credit business has a 10-year track record with extremely low loss rates and is showing no signs of distress today. Moreover, its digital infrastructure business is grossly misunderstood as it has contractual guarantees in its arrangements to companies like Meta that help to insulate it from downside risks should the AI capex boom turn into a bubble and fail to deliver on current expectations.

Given my confidence and high degree of conviction in these businesses, I am making big bets on each of them. Between them, I enjoy an average yield of over 8%, giving me significant passive income in my push towards eventually achieving early retirement from dividends. It should therefore be of little surprise, then, that all three make up some of my largest positions at High Yield Investor.

How much more money would I have if I’d avoided every ISA mistake I made? Probably a fair bit, sadly. I can’t have my time again, but I can share what I have learnt here.

No early bird

The first time I had a bit of cash to spare was at 16, thanks to an unglamorous role at the local Kentucky Fried Chicken. Many hours assembling Zinger burgers and salting french fries netted me a few hundred quid a month. What did I spend it on ? I can’t even remember.

Perfectly balanced

My second ISA mistake was thinking that stocks and markets would even out. The US and other Western countries had been dominant, so why not look at China and developing countries instead? Why not look at stagnating companies over high-flying ones? They were bound to catch up, weren’t they?

Billionaire investor Warren Buffett would have had a field day with me. One of his most famous quips is: “For 240 years, it’s been a terrible mistake to bet against America.”

He could also point out that thriving stocks and stock markets stay near all-time highs. The FTSE 100 hit an all-time high this May. It’s still only a hair’s breadth away. The S&P 500 just hit an all-time high five minutes ago (as I write)!

Interest rates

My third ISA mistake was choosing the wrong type of account. I realised with a very visceral feeling how the first month returned around 40p, or so. Although modest, my life savings were in there. That I was getting nothing back for it felt like a gut punch.

Of course, I had opened a Cash ISA at near 0% interest rates. Had I known that these types of savings accounts don’t beat inflation by much – by design – then I might have looked elsewhere.

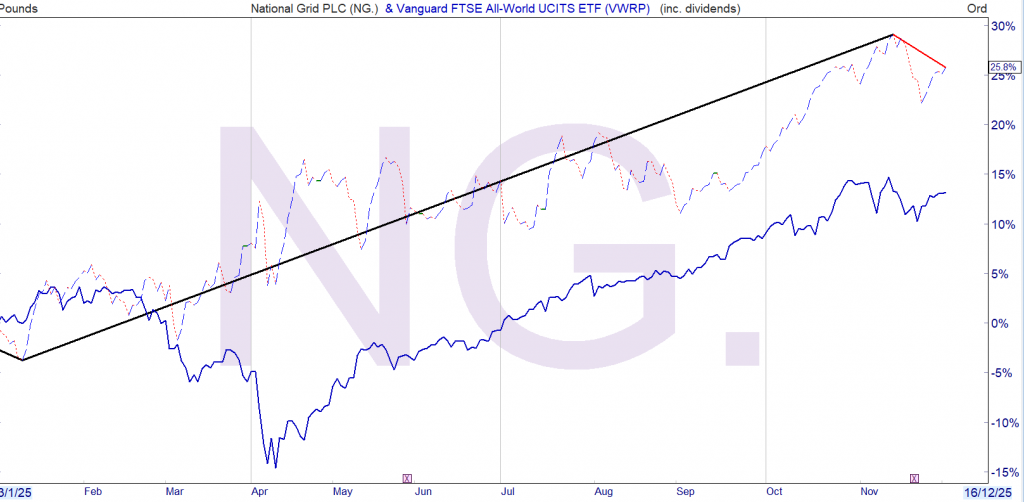

If I could roll back the years then the first step would be opening a Stocks and Shares ISA instead, and the second step would be going for an income stock like National Grid (LSE: NG). It’s a reliable dividend payer, yielding 5.24% at present. A steady and sizable stream of cash would be nice on its own but would also provide reassurance that my money was working for me.

Reliable really is the key word here too. The company has a monopoly on its UK operations which offer very stable cash flows. This allows the company to slowly increase dividends with its current 10-year growth rate at 2.9%.

The firm does face large capital expenditure as the country moves towards net zero obligations. Another downside is it’s a stock that will likely produce more income than growth in the years ahead. These are the main reasons it’s not in my portfolio today. But for the right kind of investor, this stock’s one to consider.

Note the date of the above article, NG has outperformed VWRP.