NextEnergy Solar Fund, a leading specialist investor in solar energy and energy storage, is pleased to announce its second interim dividend of 2.11p per Ordinary Share for the quarter ended 30 September 2025, in line with its previously stated target of paying dividends of 8.43p for the year ending 31 March 2026.

The second interim dividend of 2.11p per Ordinary Share will be paid on 31 December 2025 to Ordinary Shareholders on the register as at the close of business on 14 November 2025. The ex-dividend date is 13 November 2025.

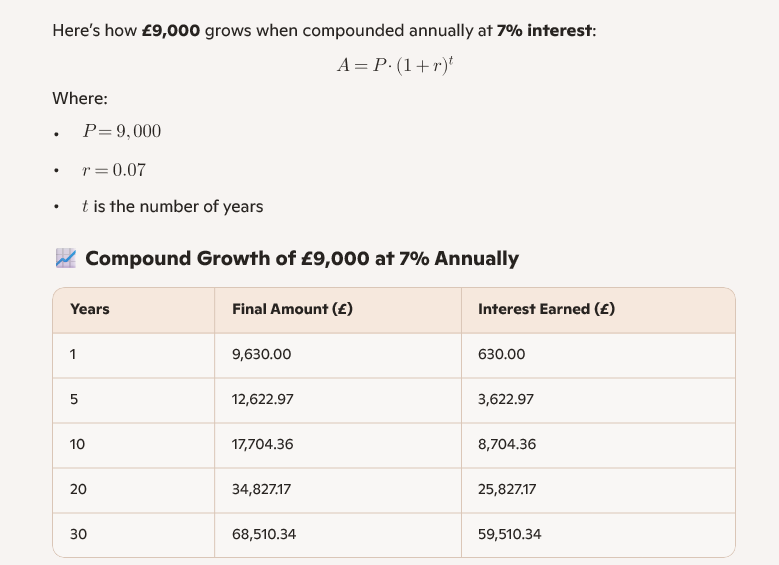

The miracle-growth of compound interest, or how to make £100,000 without really trying

13 February 2020 | by Dominique Riedl

£100,000 may seem like an unreachable goal when you first put money aside but the incredible force of compound interest can transform regular, small payments into large, life-changing sums.

The miracle-growth of compound interest, or how to make £100,000 without really trying.

Albert Einstein reputedly called compound interest the Eighth Wonder of the World.

Warren Buffett calls it the most important factor in successful investing.

Better still, every single investor can profit from man’s greatest invention. (Albert Einstein), not just geniuses or billionaires.

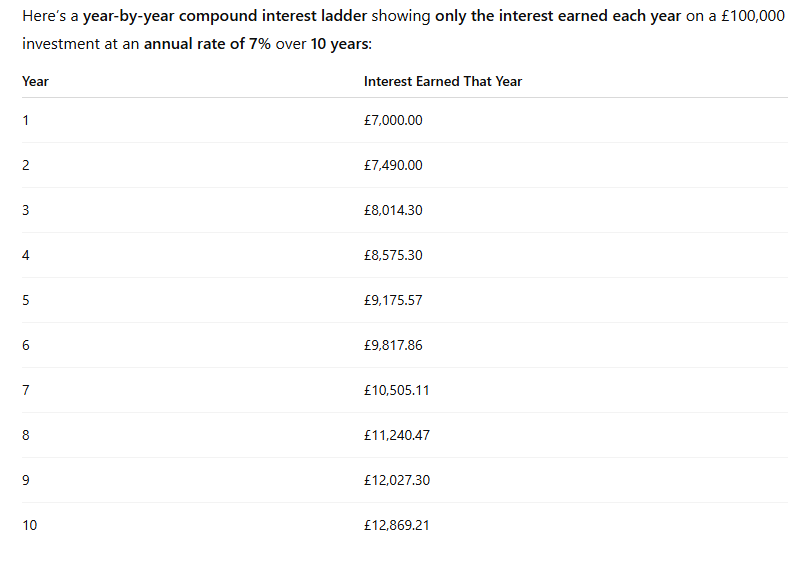

The compound interest effect refers to the snowball of money that grows on your behalf when you reinvest your interest.

The compound interest effect: Interest on interest An interest (or dividend) payment you put to work in the market today will generate more interest for you tomorrow. That’s because your interest also earns interest. And the longer you give your interest to pile up, the mightier your snowball becomes. Let’s look at a practical example to illustrate the compound interest effect…

If you invest £10,000 at a 5% rate of return then you will earn £16,288.95 over ten years, not just £15,000.

The compound interest effect creates an extra £1,288.95 that you would not have earned if you had just spent the interest every year.

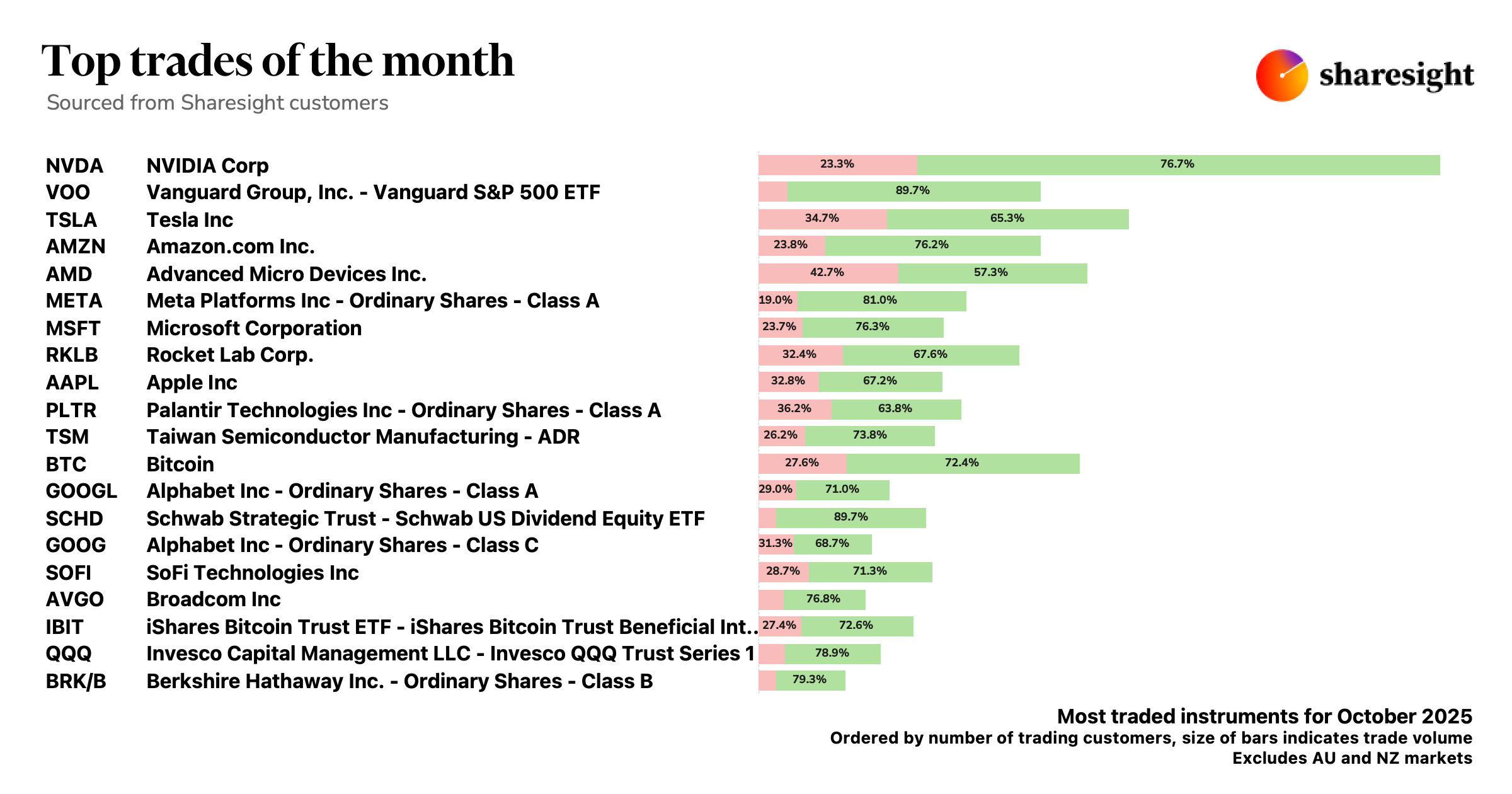

Top trades by global Sharesight users — October 2025

by Stephanie Stefanovic, Content Manager, Sharesight | Nov 5th 2025

Welcome to the October 2025 edition of Sharesight’s monthly trading snapshot for global investors, where we look at the top 20 trades made by Sharesight users around the world, excluding Australia and New Zealand (which we cover separately). Below we will reveal the top trades by our global userbase, highlighting some of the most popular stocks and the market-moving news behind them.

Top trades in October 2025

This month’s top trades were led by NVIDIA (NASDAQ: NVDA), which saw its share price reach all-time highs. The top trades were followed by Vanguard’s S&P 500 ETF (ARCA: VOO) and Tesla (NASDAQ: TSLA).

It should be noted that the assets in our trading snapshots are ordered by the number of Sharesight users trading that asset, while the size of the bars indicate the actual trade volume. So while there were more customers trading in VOO, the volume of TSLA trades was higher, meaning that while there were fewer people trading in TSLA compared to VOO, they made more trades.

Let’s look at the market-moving news behind some of this month’s top stocks:

NVIDIA (NASDAQ: NVDA)

With 1,500% share price growth in three years, is NVIDIA in a bubble?

NVIDIA becomes world’s first company worth US$5 trillion

Tesla (NASDAQ: TSLA)

Tesla share price falls as investors underwhelmed by new lower-cost cars

Strategic Review and Commencement of Formal Sale Process

BSIF has built a strong position in the UK renewable energy sector, consistently delivering attractive returns and demonstrating operational excellence. In the year ended 30 June 2025, the Company generated some 800,000 MWh of clean energy, enough to power around 300,000 homes, and avoided over 140,000 tonnes of CO₂e emissions. With a 1.4GW development pipeline, robust dividend coverage, and a proven record in asset optimisation, BSIF remains well-positioned under its existing business model to deliver returns to its shareholders.

Despite these strengths, the Board has nonetheless recognised the structural challenges facing listed renewable investment companies. As highlighted in the Interim Report published on 27 February 2025 and the 2025 Annual Report published on 21 October 2025 (the “Annual Report”), BSIF’s shares have traded at a persistent discount to NAV for over three years, limiting access to equity markets and constraining growth. Earnings have been directed toward dividends rather than reinvestment, leaving the Company unable to fully benefit from its platform, proprietary pipeline and growth potential.

As discussed in the Annual Report, the Board has considered transitioning to a more integrated and growth-oriented business model (an “IPP”) to unlock long-term value, which could have included an internalisation of the Investment Adviser and a change to the dividend policy to unlock long-term value inherent in its pipeline. Following extensive engagement with its shareholders, it has become clear that such a transition is unlikely to be the preferred strategic direction of shareholders as a whole. The Board received a variety of views from its shareholders including some support for the existing business model and strategy. However, a majority of shareholders expressed a clear preference for alternative value-maximising options, such as the potential sale of the Company or its assets. This feedback has directly informed the Board’s decision to initiate a coordinated Strategic Review and Formal Sale Process.

While the Company’s previous private sales process, limited in scope as outlined in its Annual Report, did not result in a transaction, it yielded valuable insights into market perceptions of BSIF’s strategic positioning and potential. The Board noted that prospective bidders tended to favour integrated platforms that combine operational assets with the Investment Adviser’s Platform and development expertise. As such, Bluefield Partners, as investment adviser and manager to BSIF, would support the sale of its businesses in tandem with BSIF’s operational assets and development pipeline in order to optimise the potential value of a transaction and open the sale process up to the widest possible pool of potential acquirers. The Board and its advisers believe a Formal Sale Process in the public domain is the best method to attract interest from a diverse range of potential acquirers, therefore giving the best chance of maximising value for Shareholders.

Notwithstanding the initiation of the Formal Sale Process, the Board remains open to all options and will continue to evaluate the optimal path forward in the best interests of shareholders.

Formal Sale Process & Takeover Code Considerations

The Strategic Review will be undertaken under the mechanism referred to in the Takeover Code as a Formal Sale Process, which will enable conversations with parties interested in making a proposal to take place on a confidential basis.

Parties interested in submitting an expression of interest should contact Deutsche Numis or Rothschild & Co using the contact details below. It is currently expected that any party interested in submitting any form of proposal for consideration in connection with the Formal Sale Process will, at the appropriate time, enter into a non-disclosure agreement and standstill arrangement with the Company on terms satisfactory to the Board and on the same terms, in all material respects, as other interested parties before being permitted to participate in the process. The Company will update the market in due course regarding timings for the Formal Sale Process.

The Board reserves the right to alter or terminate any aspect of the process as outlined above at any time, and to reject any approach or terminate discussions with any interested party at any time, and in such cases will make an announcement, as appropriate. The Company is not currently in discussions with, or in receipt of an approach from, any potential offeror at the date of this announcement.

The Takeover Panel has granted a dispensation from the requirements of Rules 2.4(a), 2.4(b) and 2.6(a) of the Takeover Code such that any party participating in the Formal Sale Process will not be required to be publicly identified under Rules 2.4(a) or (b) and will not be subject to the 28 day deadline referred to in Rule 2.6(a) of the Takeover Code for so long as it is participating in the Formal Sale Process. Following this announcement, the Company is now considered to be in an “Offer Period” as defined in the Takeover Code, and the dealing disclosure requirements summarised below will apply.

Shareholders are advised that this announcement does not represent a firm intention by any party to make an offer under Rule 2.7 of the Takeover Code and there can be no certainty that any offers will be made as a result of the Formal Sale Process, that any sale, strategic investment or other transaction will be concluded, nor as to the terms on which any offer, strategic investment or other transaction may be made. Shareholders are advised to take no action at this time.

As a consequence of this announcement, an ‘Offer Period’ has now commenced in respect of the Company in accordance with the Takeover Code, and the attention of shareholders is drawn to the disclosure requirements of Rule 8 of the Takeover Code, which are summarised below in “Disclosure Requirements of the Takeover Code”.

DIY investors on picked out these investment trusts as their favourites during October:

Header Cell – Column 0

Investment Trust (Interactive Investor)

Investment Trust (Fidelity Personal Investing)

1

Scottish Mortgage

F&C Investment Trust

2

Polar Capital Technology

Temple Bar Investment Trust

3

Greencoat UK Wind

Schroder Oriental Income Fund

4

City of London

Schroder Japan Trust

5

Temple Bar Investment Trust

TwentyFour Income Fund

6

Golden Prospect Precious Metals

International Public Partnerships

7

Henderson Far East Income

M&G Credit Income Investment Trust

8

Fidelity China Special Situations

CQS New City High Yield Fund

9

NextEnergy Solar

GCP Infrastructure Investments

10

JPMorgan Global Growth & Income

JP Morgan European Growth & Income

Source: Interactive Investor, Fidelity International

There is less overlap on the investment trusts that investors favoured on each platform, though Temple Bar appeared on both lists.

Investors do seem to have used investment trusts in part to diversify away from the US and towards Asia during October, with investment trusts focusing on investing in China, Japan and other Asian markets featuring on both lists.

This Latest “Bank Panic” Is a Joke. Play It With These 8%+ Dividends

Brett Owens, Chief Investment Strategist Updated: November 4, 2025

Some of our favorite bond funds (yielding 8%+) just took a header. And it’s setting up the best buying opportunity we’ve seen in nearly three years.

We can thank panicked mainstream investors for our shot here.

CEF Investors Are Ultra-Conservative (and Easily Spooked)

This opportunity is coming to us in closed-end funds, which we love for a lot of reasons—not the least of which is the fact that they’re a small corner of the market.

As of the end of 2024, there were just 382 CEFs out there, with $249 billion in assets among them. Compare that to roughly $11 trillion in ETFs, as of the end of June. The CEF market’s small size keeps institutional players out, leaving these funds mostly in the hands of everyday investors.

And weak hands they are!

There’s a very predictable pattern of these investors (typically on the conservative side) getting spooked out of their holdings at any hint of bad news. It’s a pattern we can easily play—and we’ve got another shot now.

The trigger? The recent collapse of auto-parts supplier First Brands and subprime car-loan lender Tricolor. Both sparked worries of cracks in private credit markets.

JPMorgan Chase & Co. (JPM) CEO Jamie Dimon—never one to pass up a chance to play the Prince of Darkness—piled on, commenting that, “When you see one cockroach, there are probably more.”

History Repeats

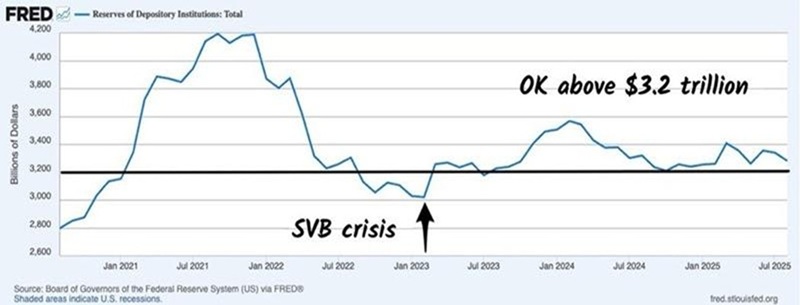

Weak-handed investors worry that smaller banks’ credit issues are resurfacing—echoes of March 2023, when Silicon Valley Bank collapsed. That turned out to be a buying opportunity.

And we have its sequel in front of us now—with a few key differences (all of which work in our favor).

Back then, aggregate bank reserves had plunged near $3 trillion, a danger zone for liquidity. The Fed was raising rates and beginning “quantitative tightening”—letting government bonds “roll off” its balance sheet.

Today bank reserves are healthy at $3.3 trillion. The Fed is cutting rates and, following last week’s Federal Open Market Committee meeting, said it would end quantitative tightening on December 1. Plus, as we discussed in last Tuesday’s article, Uncle Sam is buying Treasuries, putting downward pressure on long-term rates.

In other words, liquidity is plentiful. This money will keep flowing into bank balance sheets, cushioning credit markets and, by extension, high-yield bonds.

And yet, “first-level” investors are selling off high-yield bond CEFs, just as they did in March 2023.

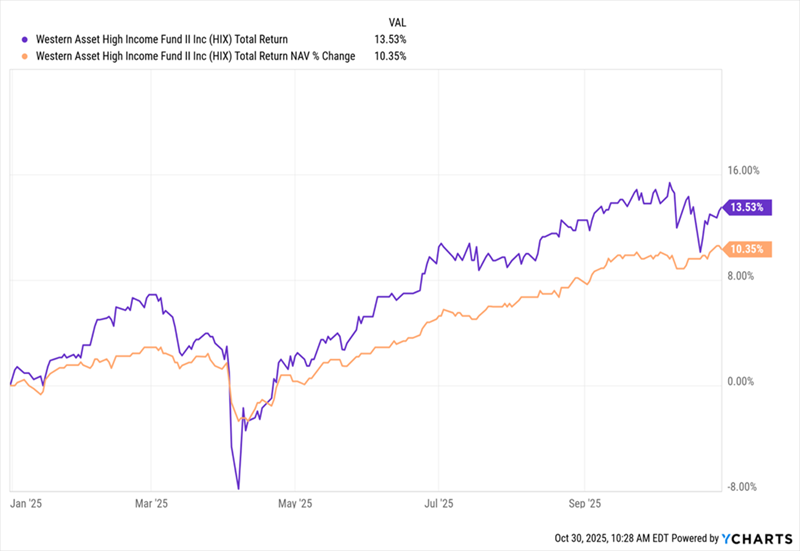

Take the Western Asset High Income Fund II (HIX), which holds about 62% of its portfolio in US-based high-yield corporate bonds.

Over the last few weeks, the fund has seen its market-price-based return (in purple below) slip as worried investors sold. Meanwhile its NAV return—or the return of its underlying portfolio, in orange—has sailed along:

HIX’s Price Drops, But Its Portfolio Is Fine …

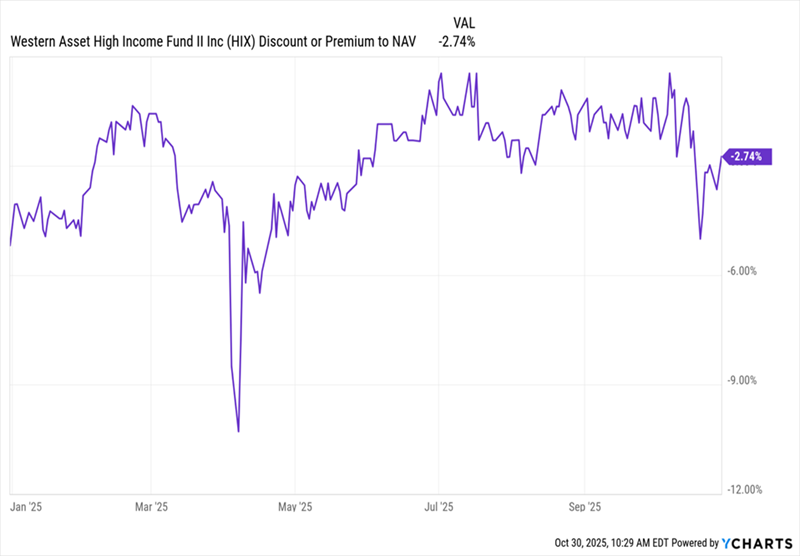

The result is that the fund, which had been trading around par for most of the year (save for the April “tariff tantrum,” another episode the first-level crowd overreacted to), trades at around a 2.7% discount to NAV as I write this. Not bad!

… Giving HIX a (Likely) Temporary Discount

This is a pattern we’ve seen across many of the bond funds in the portfolio of our Contrarian Income Report service. And it’s why I’m urging investors to buy them now.

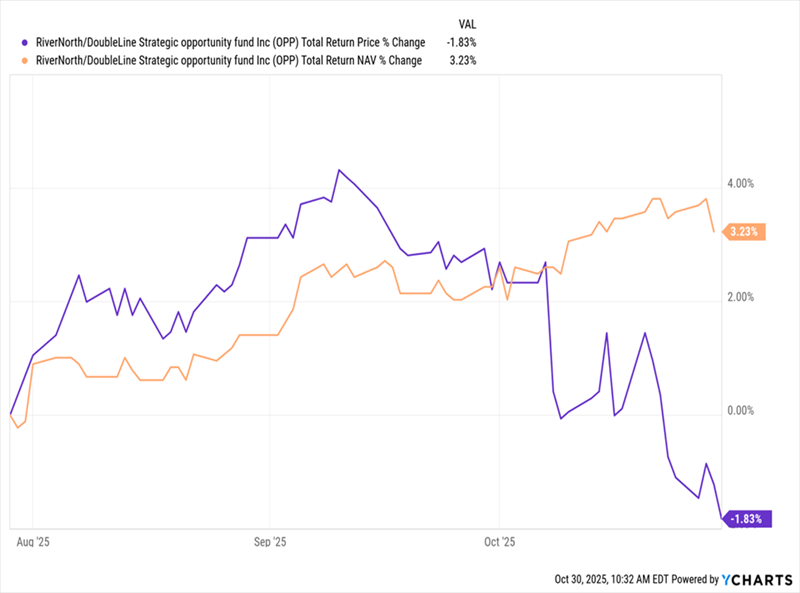

And consider this example: The RiverNorth/DoubleLine Strategic Opportunity Fund (OPP), which holds 52% of its portfolio in investment-grade debt and is managed in part by our man the “Bond God” Jeffrey Gundlach.

OPP yields 14%, but its weighting toward investment-grade debt (where bargains are harder to find), and its relatively small size (around $213 million in assets, as of October 28) are two reasons why we don’t recommend it in Contrarian Income Report.

Nonetheless, the fund does offer low volatility, with a five-year beta-rating of 0.64, meaning it’s 36% less volatile than the S&P 500.

No matter. Investors dumped it anyway. Check out the dip in OPP’s market-price-based return (in purple below) over the last few weeks, while its portfolio (in orange) has—you guessed it—motored along.

Investor Panic Is Easy to Spot Here

The result: an 8.5% discount, as of this writing, that’s well below the fund’s five-year average of 6.2%.

In a way, this is easy to understand: OPP’s focus on investment-grade debt means it’s likely held by more-conservative investors. In other words, the folks most likely to sell on the first negative headline.

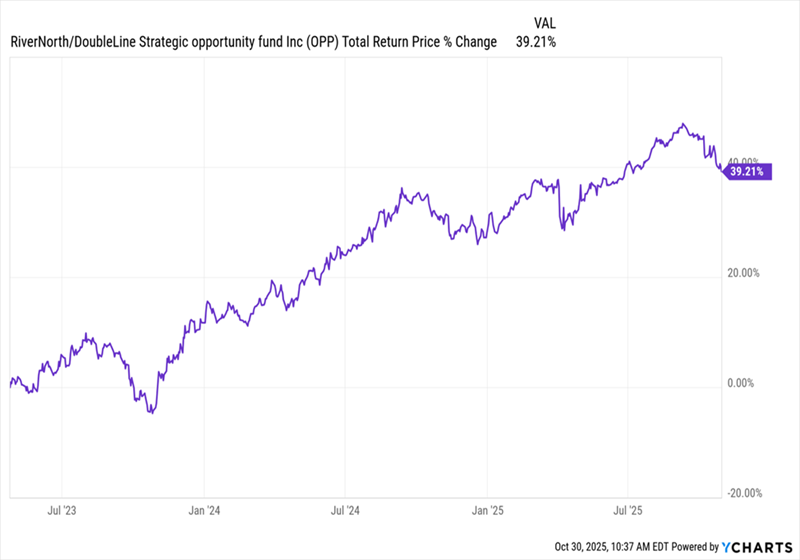

Something similar happened to OPP back in March and April of 2023. Back then, its discount bottomed out at 16%. That, too was a buying opportunity:

Last “Panic” Brought Big Gains to OPP Buyers

A 39% gain in two-and-a-half years! That’s a huge move for a bond fund, especially one weighted to investment-grade credit. And every pullback since has been a buying opportunity.

That’s the beauty of CEFs: When a big discount appears, we look deeper.

If it’s the result of the mainstream crowd selling in a panic, while NAV is chugging along, that’s almost always a great time to buy. This is the kind of window this private-credit “crisis” is giving us now.

IF GCP stays in business in it’s current form and the dividend remains the same, the picture would be

You would be earning, for ease of comparison ten percent on your seed capital and let’s say 7% on the dividends re-invested, income of £900 plus £600 a yield of 16% after ten years. Anyone lucky enough to have longer to invest the amount of income growth accelerates.

You would have earned income as you re-invested but for this comparison we will use it as a contingency.

Whilst you have little control of what the final value might be but with some care and intention you should be able to achieve the income figure.