Foresight Solar Fund: Simple maths tells us investors should start warming to the sector

Last updated: 10:48 01 Nov 2025 GMT

Is the sun finally going to shine again for the UK solar sector? The UK’s 10-year government bond yield has slipped to 4.39%, its lowest level this year, and that is good news for funds such as Foresight Solar Fund Ltd (LSE:FSFL), whose share price tends to move in the opposite direction to gilt yields.

It comes down to simple maths. Renewable energy trusts are long-term, income-paying assets, not so different from bonds, so when government borrowing costs fall, their relatively generous dividends start to look more appealing.

Historically, the link between gilt yields and renewables valuations has been almost one-for-one, and investors appear to be betting on more of the same as markets look ahead to a possible rate cut from the Bank of England in December.

Foresight Solar has other reasons to feel cheerful. Operationally, this year has brought record sunshine across the UK, helping the company deliver strong generation figures.

Meanwhile, it has locked in favourable power prices through hedging, essentially fixing future revenues in advance, giving the fund a solid cushion of dividend cover for 2025.

At the current share price, Foresight Solar is yielding just over 10% on a 1.3 times covered dividend.

That means its cash generation comfortably exceeds what it needs to pay investors, even after accounting for debt repayments. The trust has never missed a payout since listing in 2013 and has gradually increased its dividend each year.

Support for renewables remains a rare point of stability in Westminster. Ed Miliband, the energy secretary, was one of the few to keep his role in Labour’s recent reshuffle, underlining the cross-party consensus around clean energy investment.

Foresight has also been selling some assets to pay down debt, which should strengthen its balance sheet further. For now, investors are being paid to wait while the market discount, the gap between the share price and the value of its underlying assets, narrows.

With gilt yields on the slide and a steady dividend stream, the outlook for Foresight Solar is starting to look brighter once again.

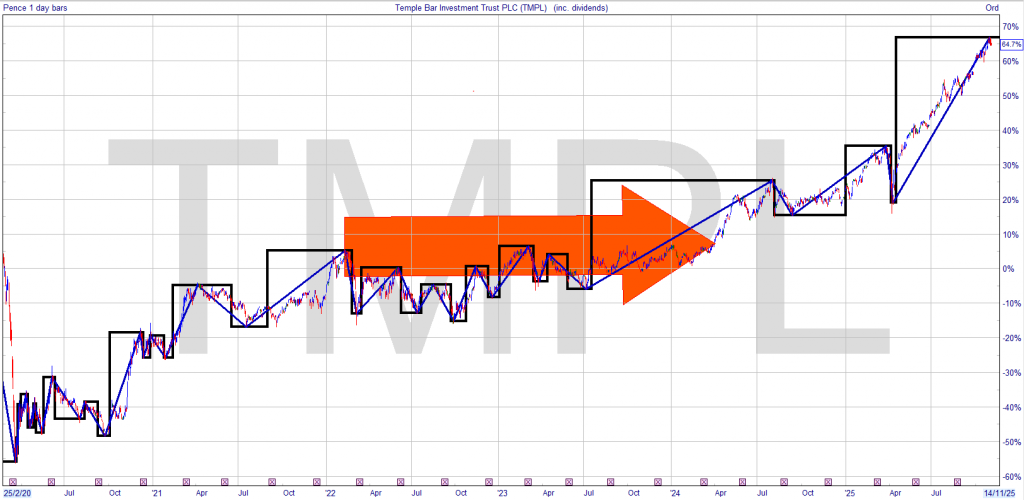

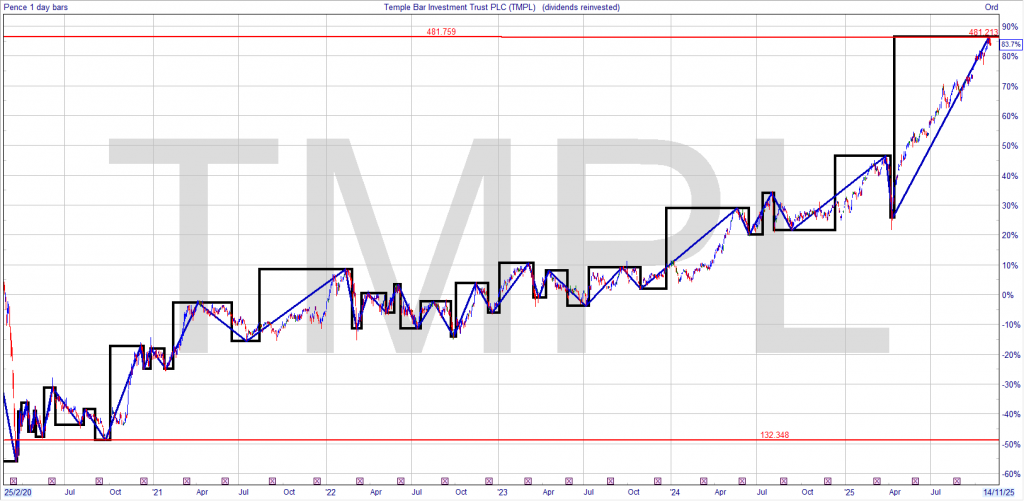

If you look closely at the TMPL graph, you will note that, even including dividends, you made, zero, zilch nothing for 2 years.

The same pattern can be seen with the control share. Mr. Market stays in business by persuading the great unwashed that the market will go up forever and then dumps on them. Maybe watch the share to get a feel for the market direction.

The blog whilst it’s a record of all trades it’s meant to be educational as well.

I understand it’s different strokes for different folks and life is life, but I intend to start a pair trading strategy with the current cash for re-investment. Because Mr. Market is at a new all time highs, the split will not be 50/50.

I will look to buy, GCP Infrastructure and TMPL Temple with a 80/20% split a blended yield of 8%. When Mr. Market falls, it’s not if but when, I could add to the TMPL position.

This ship sailed a while ago but everything crossed for a market crash, one strategy might be as you wait for a market crash is to re-invest the dividends from the pair trade into the growth share. Hopefully given time TMPL will produce a capital gain to accelerate the income in the Snowball.

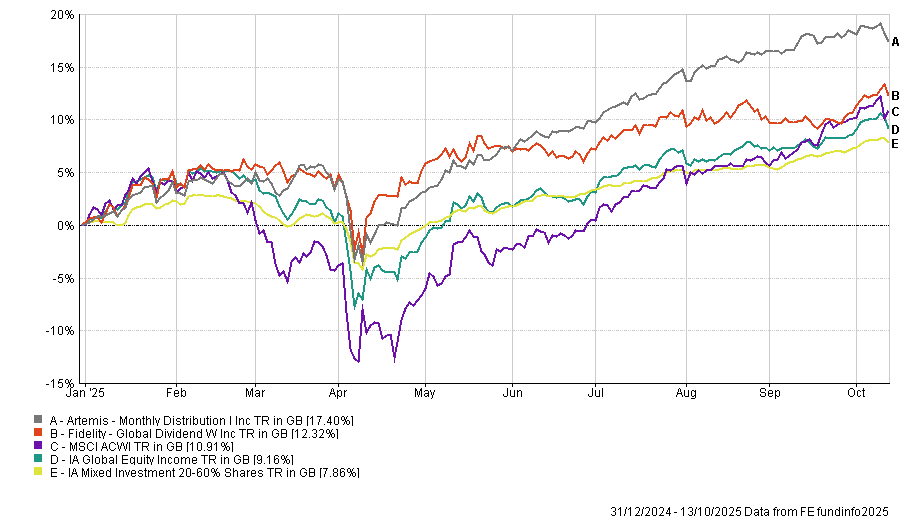

Equity income has had a positive year so far – here are five vehicles to get exposure.

By Matteo Anelli

Deputy editor, Trustnet

Income is back in fashion, as lowering interest rates and higher volatility around the world are pushing investors towards larger and more established companies that pay a dividend.

Fears of companies becoming overvalued and concentration in growth-focused areas of the market have also made investors more interested in other, not-so-crowded trades, with value investing and its key by-product, income generation, being an obvious place to look.

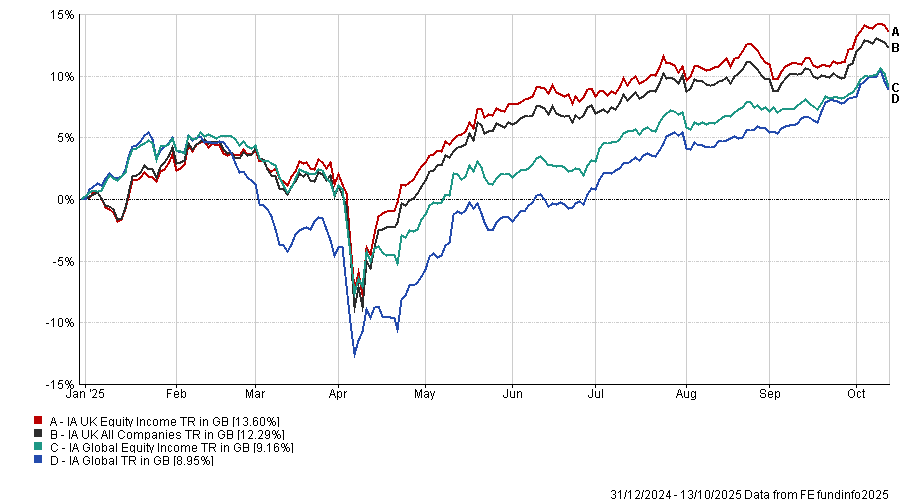

Equity income Investment Association (IA) sectors have pushed slightly ahead of their broader equity counterparts this year, so below, experts highlight their favourite income funds in the UK and globally.

Performance of sectors over the year to date Source: FE Analytics

UK equity income

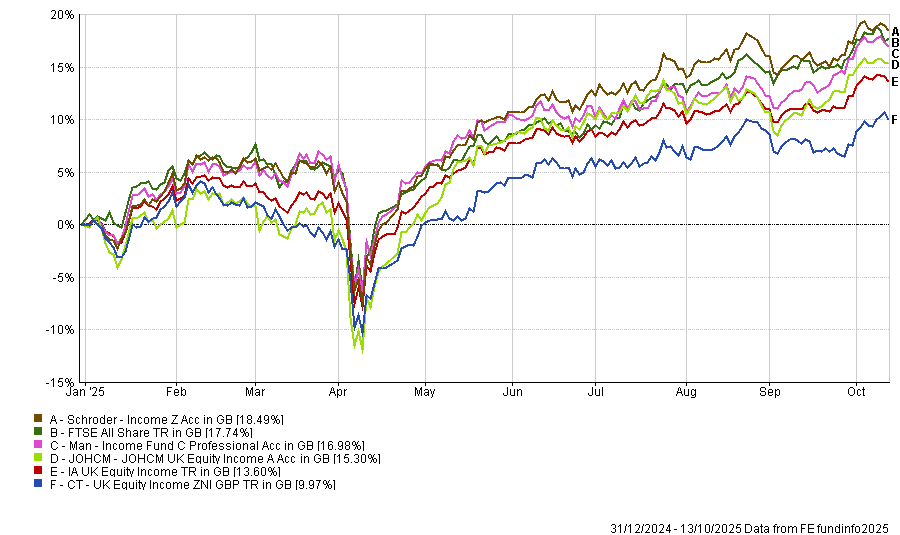

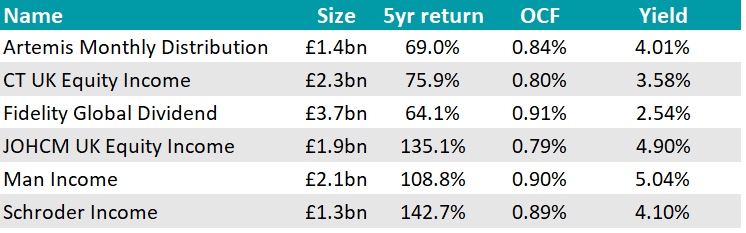

We begin with the UK, where FundCalibre managing director Darius McDermott chose CT UK Equity Income.

“With interest rates no longer anchored at zero, we’re likely to see periods where value outperforms, just as it has done in previous rate-tightening cycles,” he said. “A key by-product of value investing is income generation and CT UK Equity Income is a great example of that”.

Managed by the “highly experienced” Jeremy Smith, the fund takes a contrarian, unconstrained approach, seeking out overlooked UK companies with resilient balance sheets and the capacity to deliver sustainable dividend growth.

It focuses on long-term capital preservation and real income generation, underpinned by bottom-up research.

“With the UK equity market still trading at a discount to global peers, CT UK Equity Income is well positioned to capitalise on the re-rating potential of high-quality, undervalued businesses,” McDermott continued.

“For income-seeking investors, it’s a compelling value option in today’s market.”

Other options exist however, with Dzmitry Lipski, head of funds research at interactive investor picking Man Income. Managed by Henry Dixon and co-manager Jack Barrat, it seeks superior capital returns to the FTSE All-Share along with a higher level of yield, which is currently 5.0% compared with about 3.5% for its benchmark.

“The fund has an excellent record of delivering on its objectives,” noted Lipski.

In addition to strong recent performance, over the mid and long-term the fund has outpaced peers and benchmark convincingly. Over both five and 10 years, for example, the fund has outperformed the benchmark and has almost doubled the average return of its equity income peer group over the decade.

Meanwhile, Dennehy Wealth discretionary investment manager Joe Richardson selected two further alternatives: Schroder Income and JOHCM UK Equity Income.

The former he described as “the grandaddy of UK value income funds”, highlighting its “solid, consistent” strategy with “a great record of growing payouts” year after year.

JOHCM UK Equity Income was praised for its strong yield, its value tilt and its “very strong” growth in payouts. He also appreciated its allocation to mid- and small-caps to give investor more breadth than the usual big-dividend names.

“Being UK income funds, both fit with the broader value story: the UK market in general looks incredibly cheap, not just versus history, but also compared to other regions,” said Richardson.

“However, if we get a widespread recession, dividends can be cut. That’s why we always stress the importance of a defensive layer, ideally with a few years of income set aside, so you don’t have to sell at the wrong time or rely on payouts that may be under pressure”.

Performance of funds against index and sector over the year to date Source: FE Analytics

Global equity income

For global income seekers, Lipski opted for Fidelity Global Dividend. Since its inception in 2012, the fund has been led by Dan Roberts, who brings more than 20 years of experience to the table and is supported by the research team and resources at Fidelity.

It aims to achieve a mix of growth and income with low volatility versus the MSCI All Country World index. The yield aim is 25% more than the income produced by the companies included in the index.

“From an income perspective, the fund’s yield fell as low as 2.2% in the aftermath of the Covid pandemic, but has since been rising steadily to a level of 2.5% today,” said Lipski.

Finally, the head of fund research pointed out that not all income-paying funds are necessarily found in equity income sectors.

Artemis Monthly Distribution, for example, combines bonds and global equities, with the objective of providing a regular monthly income along with capital growth over a five-year period.

Performance of funds against index and sectors over the year to date Source: FE Analytics

Managed by four experienced specialists, Jacob de Tusch-Lec and James Davidson are responsible for managing the equity sleeve of the portfolio with Jack Holmes and David Ennett in charge of the fixed-income allocations.

“The strategy has a strong track record, ranking in the top quartile of the IA Mixed Investment 20-60% Shares peer group since inception,” Lipski noted.

“Income has also been consistent over time, with a yield of at least 4% since inception to 2020, where it understandably dropped but has since re-established at pre-2020 levels, currently 4.0%.”

Disclosure – Non-Independent Marketing Communication

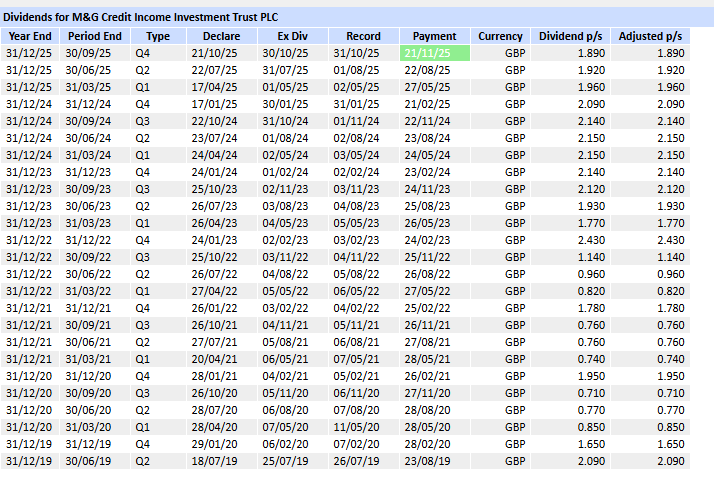

This is a non-independent marketing communication commissioned by M&G Credit Income (MGCI). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

MGCI can be thought of as the best of M&G fixed income

M&G Credit Income (MGCI) offers an alternative to an investment in the conventional bond sectors, generating a yield similar to a high-yield bond fund from a portfolio of investment-grade quality and with minimal duration. While credit spreads look tight by historic standards and the UK and European economies look troubled, MGCI generates a high-dividend yield while taking low credit risk. The historic yield is 8.5%.

Manager Adam English can invest across all public and private bond sectors to achieve his objective of an attractive yield with low NAV volatility. It is the investment in private debt that is key: private debt typically allows much higher yields to be earned by lending to companies with a given credit quality. The extra yield is compensation for the illiquidity and the complexity of the deals, which require a high level of expertise to participate in.

Adam allocates across these sectors with a relative value approach, looking for where the yield is attractive relative to the risks involved. Currently, he is cautiously positioned given that spreads generally look narrow across many sectors. That said, he is still able to generate a portfolio yield of 7.5% from a defensively positioned, 70% investment-grade-quality portfolio. The dividend target is SONIA (the interbank lending rate) plus 4% of NAV annualised, calculated quarterly. As we discuss in the Dividend section, this means the portfolio yield is currently not quite covering the dividend. However, the trust continues to pay its dividend target of SONIA plus 4%, making a small contribution from capital, and Adam is waiting for volatility to throw up better opportunities to add yield.

Analyst’s View

We think MGCI looks extremely attractive as an alternative to a high-yield fund at this juncture, given the current state of the markets and the different sources of risk in its portfolio. There isn’t really any hiding place in public-debt markets. Government bonds look vulnerable to concerns about fiscal sustainability, while inflation continues to erode what might seem like reasonable nominal yields: volatility seems certain. These factors may have driven investors to the corporate bond market, where they have driven in spreads to very narrow levels where they offer little yield pick-up. To generate a high yield in public markets requires braving the sub-investment-grade space, where narrow spreads could easily come under pressure if the UK and European economies continue to weaken. MGCI has a portfolio of investment-grade-quality debt, which offers a yield equivalent to a high-yield fund, and a duration of less than one compared to 7.7 in the investment-grade market, meaning it should be much less exposed to volatility in the rates market. Investors should remember that there is no free lunch, and the extra yield comes from the illiquidity and complexity of the portfolio, but we think M&G is ideally placed to assess and manage those risks given its size and expertise across the fixed income and private assets space.

The portfolio yield being below the dividend target is something to watch but not to worry about in our view. Adam argues that low NAV volatility and a conservative approach are both key things investors expect from the fund, and he won’t compromise on that in the short term. His view is that volatility and opportunities are inevitable, and this should allow him to boost the portfolio yield above target in the fullness of time without having to accept prices he thinks aren’t attractive for the risks he has to take.

Bull

High yield linked to interest rates, with average investment-grade-quality credit

Offers access to private-debt markets, providing attractive risk/return characteristics and diversification

NAV should prove resilient due to many defensive characteristics

Bear

Complexity makes it harder for investors to understand exposures

Limited capital gain potential, including from duration

The current market is all about momentum, but investors don’t need to buy overpriced high-growth stocks to participate in gains.

If you dig deep enough, you can find undervalued stocks with growth potential in both the short term and the long run.

Across varied sectors like healthcare, technology, and finance, as well as non-U.S. countries with growth potential, a select group of stocks can combine those qualities.

The four companies highlighted here have a common thread: Quant Strong Buys that are reasonably priced relative to earnings potential, yet positioned in industries with room to expand.

I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Alpha Picks, which selects the two most attractive stocks to buy each month, and also determines when to sell them.

courtneyk/E+ via Getty Images

GARP Wins vs Mega-Cap Growth

After years of easy money and growth-at-any-price investing, the market’s mood is bound to shift, and now is a good time to look for more reasonable valuations. With inflation still above comfortable levels, and U.S. economic growth expected to flatline (from 1.9% this year to 1.8% in 2026), investors are wise to begin looking for companies that can grow earnings without depending on a booming economy. This doesn’t mean sell all your growth stocks. It means focusing on reasonably valued businesses with solid balance sheets, consistent cash flow, and clear growth drivers.

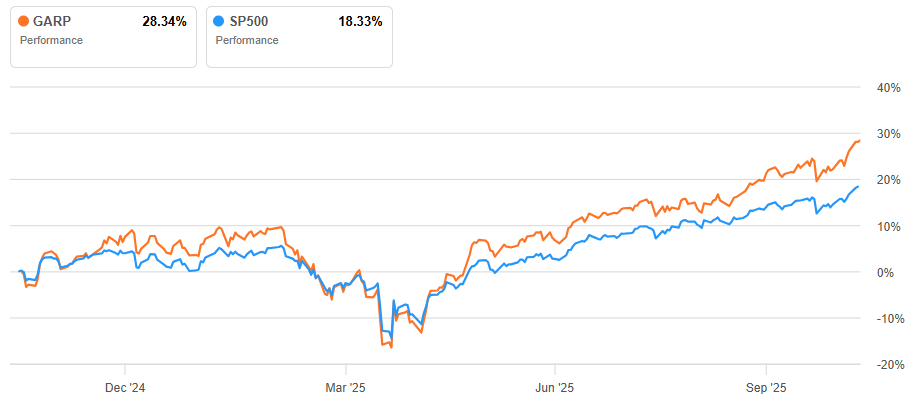

When looking at “growth-at-a-reasonable-price” stocks, we can see how selecting companies with a lower PEG compared to the S&P 500 can still outperform, and this trend may continue as the high-growth, mega-cap names finally begin to lose momentum. Here we measure these stocks by the iShares MSCI USA Quality GARP ETF (GARP) and compare to the cap-weighted S&P 500:

GARP vs S&P 500: 1-Year Performance

Seeking Alpha

Across sectors as varied as healthcare, technology, and finance, as well as non-U.S. countries with growth potential, a select group of stocks now combines those qualities:

Proven revenue growth

Credible earnings momentum

Share prices that haven’t yet caught up to their potential

Capturing growth and value is why I’ve selected four standouts that can coexist, even in a cautious market.

How I Chose the Best Value and Growth Stocks

The current market is all about momentum, but investors don’t need to buy overpriced high-growth stocks to participate in gains. If you dig deep enough, you can find undervalued stocks with growth potential in both the short term and the long run.

The leading selection criterion was valuation and the secondary was growth, both of which placed emphasis on forward potential. So, these stocks tend to be more tilted toward value than a traditional GARP selection. I eliminated microcaps and placed preference on sectors and industries that can thrive in a growing economy with slowing momentum.

Quant Sector Ranking (as of 10/29/2025): 32 out of 976

Quant Industry Ranking (as of 10/29/2025): 16 out of 474

Sector: Health Care

Industry: Biotechnology

Seeking Alpha

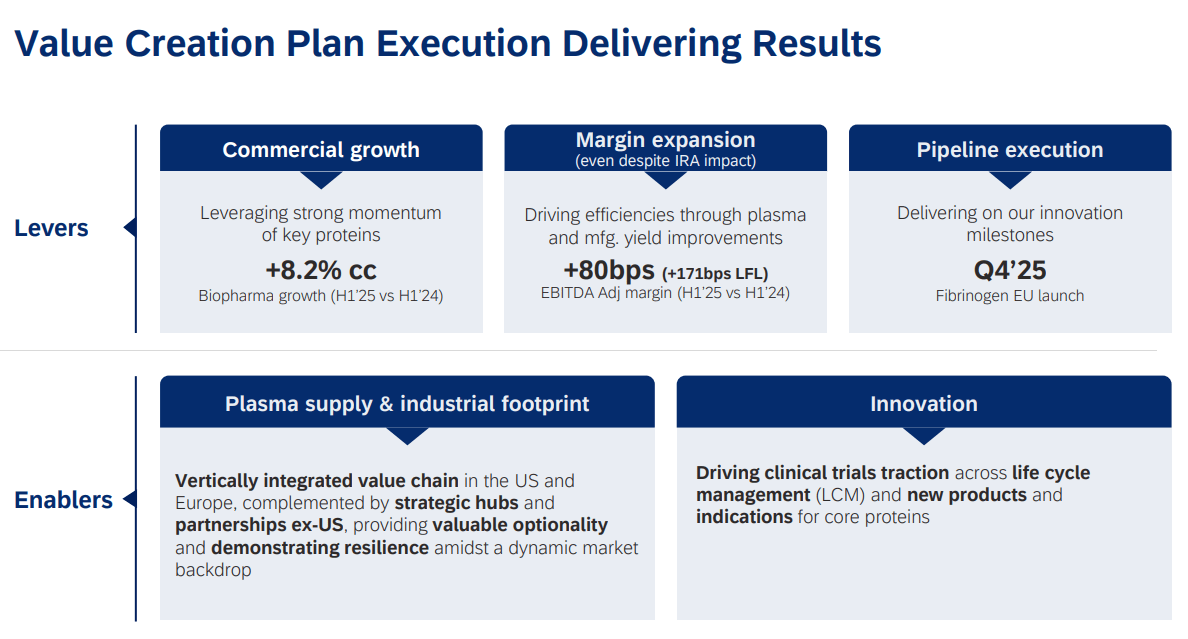

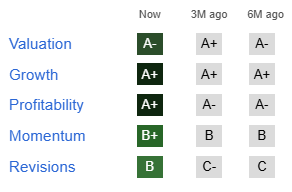

Grifols is a global healthcare company based in Spain that specializes in plasma-derived medicines used to treat immune deficiencies and bleeding disorders. After years of heavy investment, the company is now refocusing on profitability and paying down debt. For investors, that transition could unlock meaningful value, as the stock trades at a discount to historical averages, even as demand for its therapies remains steady.

Seeking Alpha

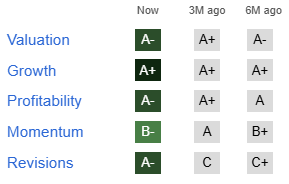

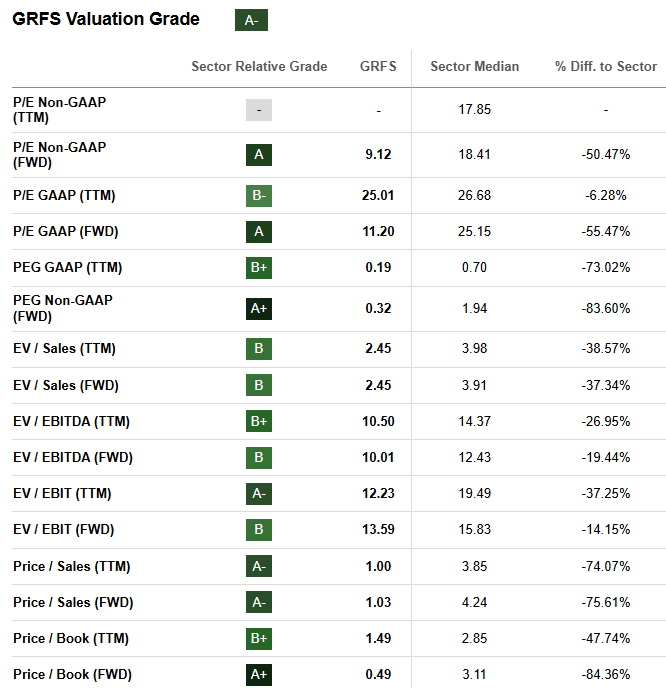

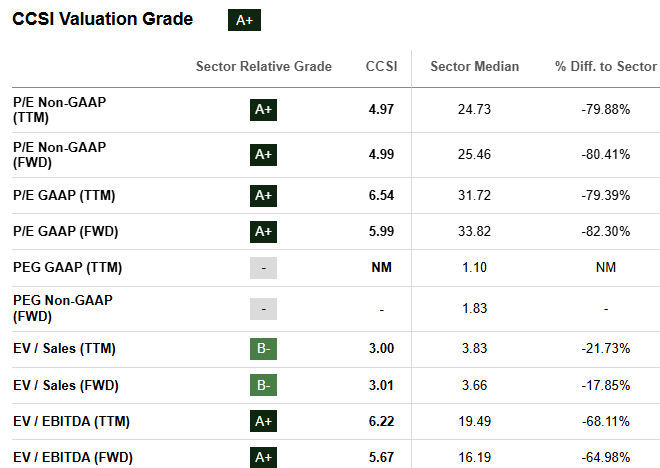

Grifols’ A- valuation grade is supported by the 9.12 P/E ratio, which is half that of the sector median, and its 0.49 forward Price/Book ratio, coming in at a fraction of the 3.11 peer metric. My favorite value metric, forward PEG, is 0.32, which is significantly more attractive than the peer median of 1.94. The growth side of Grifols’ value story is told by their focus on solid FCF and its impressive, peer-beating EBITDA increase, expected at 14.54%. The value-plus-growth story can continue as the company continues to plan value creation and deliver results with commercial growth, margin expansion, and pipeline execution.

Grifols Q2 2025 Results

Note that GRFS has been rumored to be a potential takeover target by Brookfield (BAM). A previous bid was rejected by Grifols management, who denied media reports that it was in talks with the private equity fund for another takeover bid.

Grifols’ valuation is attractive, with a potential upside driven by EPS growth and market expansion in plasma-derived products. In an environment of moderate inflation and slower global growth, Grifols’ pricing power and defensive healthcare qualities stand out, making GRFS a classic “growth at a discount” opportunity.

Quant Sector Ranking (as of 10/29/2025): 22 out of 976

Quant Industry Ranking (as of 10/29/2025): 11 out of 474

Sector: Health Care

Industry: Biotechnology

Seeking Alpha

Incyte is a mid-size U.S. biopharmaceutical company best known for its cancer and autoimmune treatments, including the blockbuster drug Jakafi. The firm has a strong track record of research success and continues to expand its pipeline into dermatology and rare diseases. Despite that growth outlook, the stock trades at a valuation below many biotech peers, giving investors an entry point into a profitable, cash-generating innovator.

INCY’s A- valuation grade is supported by its forward P/E of 15.89, which compares to 25.15 for the sector, while key value and growth metric, PEG, is an extremely attractive 0.07, which is a fraction of the sector’s 1.94.

Seeking Alpha

Digging into the growth side, INCY’s forward EBITDA growth is expected at 37.70% while its EPS forward long-term (3-5y CAGR) growth rate is estimated at over 200%, primarily supported by its strong pipeline. CEO William Meury stated in this week’s quarterly earnings call that Incyte delivered a strong quarter and highlighted, “The fundamentals around Jakafi, Opzelura and our hem/onc business, Niktimvo and Monjuvi namely remains strong.”

Incyte’s diverse lineup and steady revenue base help buffer against potential economic weakness, while its upcoming drug launches can drive growth through 2026.

Quant Sector Ranking (as of 10/29/2025): 7 out of 686

Quant Industry Ranking (as of 10/29/2025): 1 out of 53

Sector: Financials

Industry: Property and Casualty Insurance

Seeking Alpha

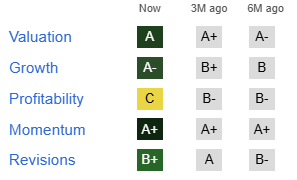

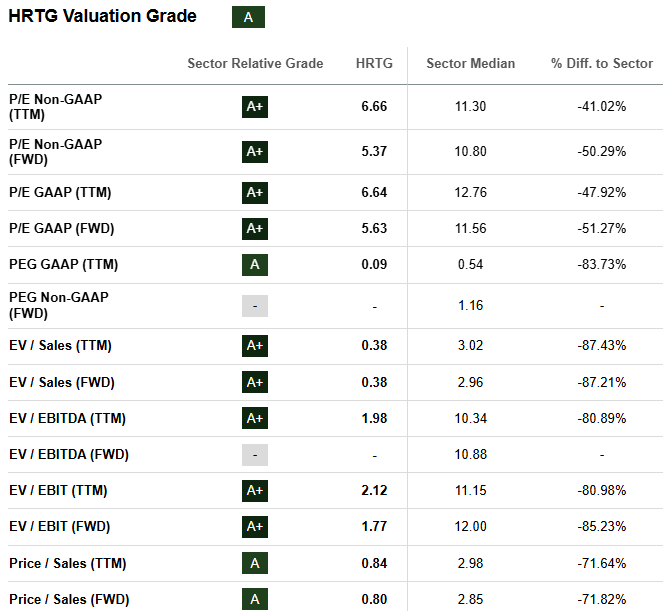

Heritage Insurance is a Florida-based property and casualty focused on homeowners and small commercial coverage across several southeastern states. Insurance isn’t exciting like Stellar Stocks Flying High on AI, but in today’s market, HRTG combines two things investors seek: low valuation and rising profits. Above-average interest rates allow insurers to earn more on their investment portfolios, and Heritage has been improving investment results amid a slow hurricane season followed by several challenging ones. HRTG trades at a single-digit P/E ratio while earnings have the potential to grow into 2026.

Seeking Alpha

As you can see in the chart, HRTG’s forward P/E of 5.63 is about half that of the sector median, while the growth/value metric, PEG, is outstanding at 0.09, which is a fraction of the sector median’s 0.54. On the growth side, HRTG’s forward EBIT of 42.51% is expected to come from a combination of decreasing overhead and an increasing customer base. At its Q2 earnings call, CEO Ernesto Jose Garateix emphasized the successful implementation of strategic initiatives, citing rate adequacy, managed exposure, and enhanced underwriting discipline as key drivers of earnings power. He said, “We are at an inflection point in our business, where we expect our personal lines policies in-force to slowly increase through the second half of this year as our new business production continues to ramp up.”

For investors who appreciate steady returns without overpaying, HRTG fits the bill: a value stock with solid fundamentals and limited sensitivity to slow or moderate economic growth.

Quant Sector Ranking (as of 10/29/2025): 25 out of 540

Quant Industry Ranking (as of 10/29/2025): 6 out of 182

Sector: Information Technology

Industry: Application Software

Seeking Alpha

Consensus Cloud Solutions provides secure digital document and data exchange services, primarily for health care and financial institutions. Its software helps organizations move away from paper-based processes while meeting strict privacy and compliance requirements. The company’s recurring revenue model generates consistent cash flow, yet CCSI trades at a valuation far below typical software peers. That disconnect creates an appealing setup for investors: modest risk, recurring revenue, and a path to gradual growth.

Seeking Alpha

CCSI’s stellar valuation grade starts at its low forward P/E of 4.99, which is less than 20% the size of the sector median’s 25.46. The low P/E is in part due to its below-average forward EPS earnings of 5.96%, but CCSI’s standout growth metric is its outstanding working capital position that has jumped 760% year-over-year, signifying solid liquidity and stability. These metrics, combined with its mission-critical services, make CCSI more of a strong value play with moderate growth potential in the tech space.

Conclusion: Best Value and Growth Stocks to Balance Risk and Return

In an economic and market climate where investors expect slower growth, sticky inflation, and potentially declining sentiment, finding a balance between value and growth may have never been so important. The four companies highlighted here have a common thread: Quant Strong Buys that are reasonably priced relative to earnings potential, yet positioned in industries with room to expand. Whether through healthcare innovation (GRFS and INCY), insurance profitability (HRTG), and digital transformation (CCSI), they offer investors a path to future growth without overpaying for it. In the months and year ahead, disciplined stock selection may take leadership from market momentum, potentially making the difference between steady gains and short-term disappointment.

Pair trading with the Snowball, is where you split your stake between a growth stock and a higher yielding share. In case, maybe just maybe your growth stock is a clunker.

If not you could use any capital gain from your growth stock and the income from your higher yielder to add to your Snowball or use the income to add to your growth stock, dependant on Mr. Market.

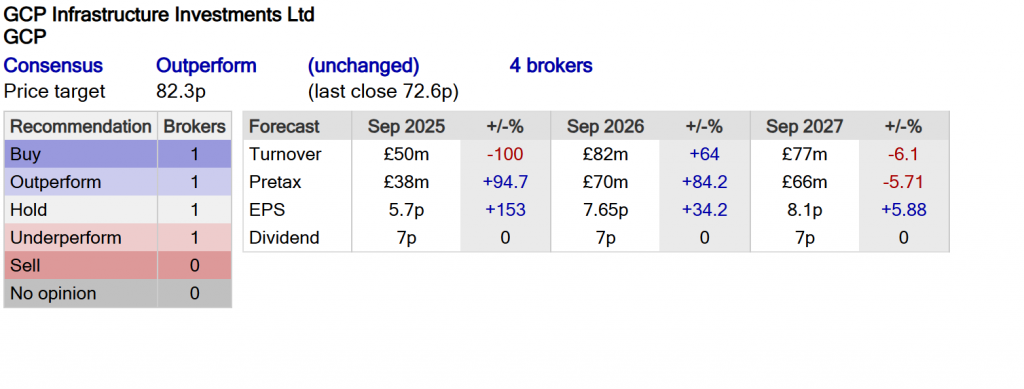

Investment policy: GCP Infrastructure Investments (GCP) seeks to provide shareholders with regular and sustained long-term dividend income whilst preserving the capital value of its investments through investing in a diversified portfolio of UK infrastructure projects with long-term, public-sector-backed revenues, with a focus on debt.

GCP Infrastructure Investments (GCP) was launched in 2010 to provide investors with reliable government-backed income, secured against essential UK infrastructure.

Unlike equity-focused funds, GCP lends to a diversified portfolio of infrastructure projects benefiting from long-term, government-backed cash flows, often with an element of inflation-linkage. These revenues tend to be resilient through economic cycles, offering investors both stability and diversification with a lower correlation to bond and equity markets.

The UK infrastructure landscape has undergone a significant transformation over the past 15 years. GCP’s diversified approach and early-mover strategy have enabled it to evolve with market dynamics, capturing enhanced returns and mitigating sector-specific risks. For example, within the renewables sector, the trust was able to lock in 9-10% yields from early investments in solar energy (in 2011), and anaerobic digestion (2013), significantly above the prevailing 0.5% base rate and the low single-digit yields offered to later lenders.

As solar and wind infrastructure markets have matured and risk-adjusted returns have fallen, GCP has reoriented its portfolio to take advantage of new opportunities, such as anaerobic digestion. This approach has helped GCP construct a portfolio that now generates enough clean energy to power almost a million homes each year.

Against a favourable policy backdrop, including the UK’s new £725 billion ten-year infrastructure strategy, GCP is well-positioned to benefit from rising public and private investment. With structural drivers such as decarbonisation, deglobalisation, ageing demographics and digital connectivity accelerating, the trust offers investors access to long-term trends through a defensive, income-oriented lens.

1) What is the investment trust’s goal?

To provide consistent, long-term dividend income and preserve capital through investing in a diversified portfolio of UK infrastructure assets that benefit from public-sector-backed cash flows, with a focus on debt.

2) Are investment decisions driven by a particular investment style?

GCP focuses on providing exposure to a diversified range of infrastructure assets in the UK which are underpinned by public-sector-backed cash flows, focusing on debt. These assets range from renewables, with revenues predominantly underpinned by government subsidies, PFI/PPP with unitary charge payments backed by the UK government, and public-sector-backed lease income from the supported living assets within the portfolio. Around half of the current portfolio is inflation-protected.

The team focuses on assets with high barriers to entry, monopolistic characteristics and low sensitivity to economic cycles. Rather than chasing capital growth, the trust prioritises risk-adjusted returns and capital preservation, seeking assets that deliver reliable income irrespective of the macro environment, with the diversified nature of the portfolio supporting this ambition.

GCP also favours projects with high upfront capital expenditure and limited ongoing operating risk, supporting dependable long-term returns, with just 1% of the portfolio exposed to construction.

3) How many assets does the trust typically hold?

GCP holds a well-diversified portfolio of almost 50 investments spanning 17 infrastructure sectors. Around 60% of the portfolio is invested in renewables (primarily solar, biomass, wind and anaerobic digestion), just over a quarter in PFI projects (with healthcare and education as the largest constituents), with supported living making up the remainder.

In terms of capital structure, the majority of the portfolio is invested in senior and subordinated debt, which offers greater security than equity exposure.

4) What is the trust’s dividend policy?

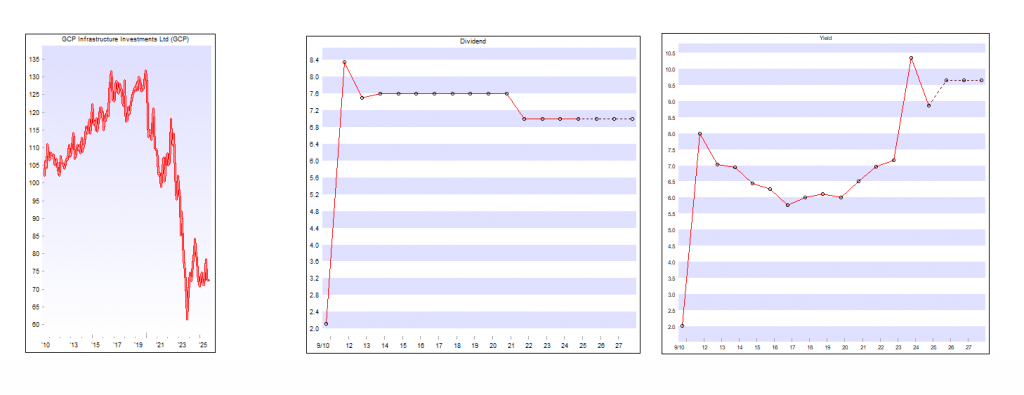

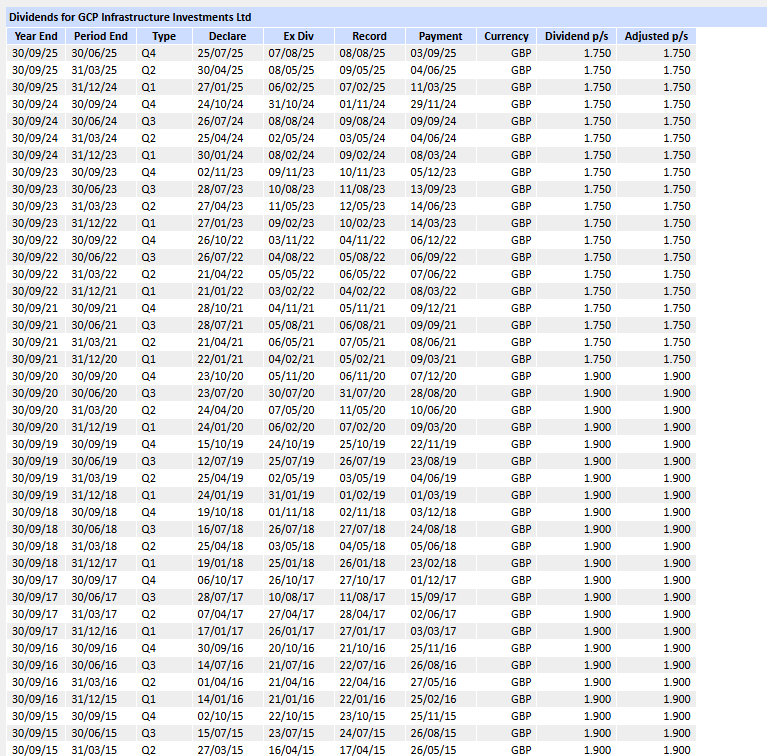

GCP has delivered consistent dividends for the last 15 years and is currently trading at a dividend yield of just over 9% (as at 08/08/2025). It set a medium-term 7.0 pence per share dividend target in 2020 and continues to deliver on this.

5) What are the trust’s ongoing charges?

GCP has an ongoing charge of 1.2% per annum (which is deducted from the net asset value and not from the shareholder).

6) Does the investment trust have performance fees?

No.

7) Does the investment trust use gearing and, if so, is it structural or opportunity-led?

GCP has a maximum allowable structural gearing of 20%, although this has typically been in the 10-15% range in recent years. It reported a net debt position of £36 million as of 30 June 2025, equivalent to 4.2% of NAV.

KEPLER

GCP Infra is pleased to announce a dividend of 1.75 pence per ordinary share for the period from 1 July 2025 to 30 September 2025. This is in line with the Company’s annual dividend target of 7.00 pence per ordinary share. The dividend will be paid on 9 December 2025 to holders of ordinary shares recorded on the register as at the close of business on 14 November 2025.

Expected timetable:

Shares quoted ex-dividend

13 November 2025

Record date for dividend

14 November 2025

Dividend payment date

9 December 2025

If you buy just before an xd date, you could receive 5 dividends in just over a year. With GCP that could equate to a yield of 12%. That would create a problem for next year but a lot of water to flow under a lot of bridges before then.

As a replacement share the Snowball is going to buy GCP Infrastructure.

GCP Infrastructure Investments Ltd (GCP) currently trades at a deep discount to NAV and offers a high yield, making it attractive for income-focused investors—but its elevated P/E ratio and sector headwinds suggest caution. Here’s a detailed breakdown to help you assess whether GCP fits your strategy.

📊 Valuation & Performance Snapshot

GCP Infra is a FTSE 250-listed, closed-ended investment company focused on UK infrastructure projects with long-term, public-sector-backed revenues.

It targets sustained, regular dividends, and its portfolio includes renewable energy, social housing, and PFI assets.

Recent buybacks suggest management sees value at current levels.

⚠️ Risks & Considerations

High P/E ratio implies stretched valuation relative to earnings.

Sector headwinds: Infrastructure and renewables have faced pressure from interest rate volatility and policy uncertainty.

Discount to NAV is wide, but may persist if sentiment remains cautious.