I do not drop many remarks, but i did a few searching and wound up here The Snowball – Passive Income. And I do have a couple of questions for you if you tend not to mind. Is it only me or does it give the impression like some of the responses look like left by brain dead folks? And, if you are writing on other sites, I’d like to follow anything new you have to post.Would you make a list of all of all your communal sites like your Facebook page, twitter feed, or linkedin profile?

££££££££££££££

I only post here, no plans to post anywhere else but I am considering writing an e book with examples of how I achieved a 12% yield well ahead of target, with all sales and purchases posted at the time of the trades.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

Investing in property is a proven and powerful strategy for earning a second income. After all, with tenants paying rent each month, it generates a predictable and recurring source of revenue. That’s one of the main reasons why buy-to-let became so popular in Britain.

Sadly, not everyone has the money to buy rental property, especially now that mortgage rates have shot up. Fortunately, there’s another way – one that doesn’t require going into debt.

Should you buy LondonMetric Property Plc shares today?

In fact, with just £5,000, investors can potentially start earning impressive passive income, overnight. Here’s how.

Earning real estate income

The easiest way to invest in property in 2025 is through a real estate investment trust (REIT). This special type of business owns, manages, and leases a portfolio of properties, collecting rent that’s then paid out to shareholders, typically every three months.

REITs come with a lot of advantages. Since they trade like any other stock, investors can put money in and take money out almost instantly.

At the same time, someone with just a few thousand, or even a couple of hundred pounds, can snap up some shares and begin generating a passive dividend income. And in many cases, the yields offered by REITs are much higher compared to the standard dividend payout of London-listed shares.

Best of all, they can even be held inside a Stocks and Shares ISA, allowing all this income to be tax-free – a massive advantage that traditional buy-to-let doesn’t have.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

A FTSE 100 REIT with lots of potential

The UK’s flagship index is filled with several REIT stocks. And one that I’ve already added to my income portfolio is LondonMetric Property

Following a series of acquisitions, the firm’s become one of the largest publicly-listed commercial landlords. This expansion ultimately led to the group’s inclusion in the FTSE 100 earlier this year. And its diverse portfolio contains a combination of logistical centres, retail parks, petrol stations, and even healthcare centres, among others.

Intelligently, most of its properties are rented under a triple net lease structure. That means the tenants are ultimately responsible for maintenance, insurance, and taxes. And consequently, LondonMetric benefits from lower operating costs and more predictable cash flows.

In fact, that’s how the REIT has delivered a decade of continuous dividend hikes, generating inflation-linked passive income for shareholders.

Risk versus reward

While I remain quite bullish on this business, there’s no denying there are critical risk factors that investors must carefully consider.

With the bulk of net profits paid out to shareholders, LondonMetric is highly dependent on external financing. As such, the balance sheet’s quite highly leveraged, making the group very sensitive to interest rates. And this exposure’s only amplified by the impact interest rates have on property valuations as well.

So far, the firm generates more than enough cash flow to cover both debt servicing costs and shareholder payouts. However, with several lease renewals on the horizon, cash flows could be adversely impacted if rents are negotiated lower by key tenants.

This risk is why the shares currently offer such a juicy 6.7% yield. Yet for me, the risk is worth the reward.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

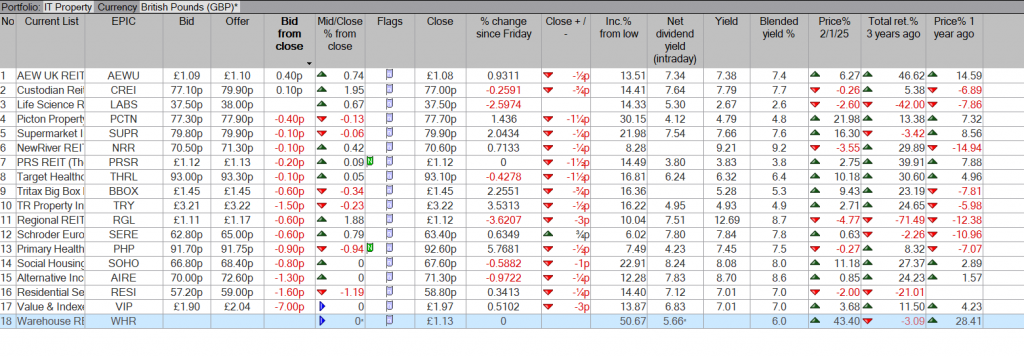

Over the last six months, the FTSE 250 has enjoyed some strong performance, climbing by more than 14%. However, not all of its constituents have been so fortunate, such as Primary Health Properties (LSE:PHP).

Like many other businesses in the real estate sector, the healthcare-focused landlord has suffered from generally weak investor sentiment, resulting in the share price slipping back below £1. Yet despite this, dividends have continued to flow. And as a result, the REIT now offers a tasty-looking 8% dividend yield.

Should you buy Primary Health Properties Plc shares today?

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Impressive dividends

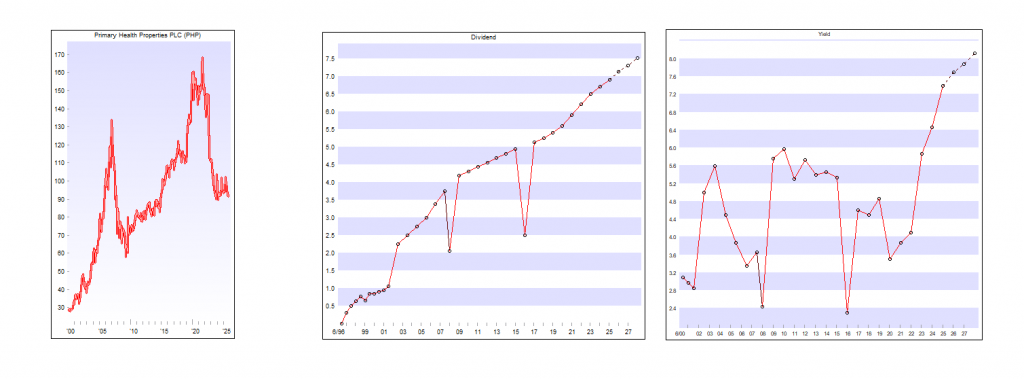

As a quick crash course, Primary Health Properties is one of the biggest healthcare landlords in the UK. It owns and leases a diversified portfolio of GP surgeries, pharmacies, and dental clinics primarily to the NHS.

With a government entity being one of its largest tenants, the company has enjoyed fairly resilient and predictable cash flows over the years. And it’s one of the main reasons why, despite the challenges within the real estate sector, the group has continued to reward shareholders with ever-increasing dividends for more than 25 years in a row.

But if that’s the case, why are investors seemingly not rushing to capitalise on the stock’s impressive yield?

Headwinds and challenges

Even with a resilient business model, the group has encountered several challenges both internally and externally. It’s no secret that higher interest rates have created numerous headaches for property owners, especially REITs that often carry significant debt burdens.

In the case of Primary Health, the group’s rental cash flows have continued to grow steadily, but rising debt costs have increased the pressure on net earnings.

At the same time, management’s contending with some protracted rent increase negotiations with the NHS. Should these talks fail, its currently impressive 99.1% occupancy might start to slip alongside its net rental income. After all, finding new tenants in the healthcare niche can be a bit trickier compared to the residential sector.

With that in mind, it’s not surprising that investors aren’t as keen to buy shares while the macro environment remains unfavourable.

Still worth considering?

The continued pressure of financing costs and delays in rent revaluations indicates that margins are at risk of being squeezed. This could also hinder rental income growth, squeezing the coverage of existing dividends and any potential future growth.

Nevertheless, the business continues to have an ace up its sleeve. Primary Health ultimately benefits from structural long-term demand for primary healthcare infrastructure. And that’s an advantage that doesn’t change even during economic downturns.

The balance sheet does carry a large chunk of debt. But it appears to remain manageable. And with interest rate cuts steadily emerging, the pressure from its outstanding loans should slowly alleviate over time while simultaneously helping boost the value of its property portfolio.

That’s why, despite the risks, I think this FTSE 250 REIT’s worth a closer look.

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Henderson High Income (HHI). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

HHI’s blend of equities and bonds has supported outperformance and dividend growth over the past decade.

Overview

Henderson High Income (HHI) has been managed by David Smith since 2012, with a clear focus: to deliver a dependable income stream alongside long-term capital growth. Unlike many peers that focus solely on equities, HHI blends equities with an allocation to bonds. This mix, managed in collaboration with Janus Henderson’s fixed-income team and funded largely through structural Gearing, has helped enhance the trust’s yield, smooth income streams and dampen overall volatility.

On the equity side, David takes a disciplined bottom-up approach. He targets businesses with straightforward, defensible models, strong cash generation and robust balance sheets, whilst keeping a close eye on valuation. Importantly, he looks for companies with the capacity to grow dividends over time. Rather than simply pursing the highest yielders, he focusses on his income sweet spot of 2–6% yields, where he finds payouts tend to be more sustainable and supported adequately by long-term growth potential. Recent Portfolio activity reflects this philosophy, with new positions in Aberdeen and Telecom Plus, both cash-generative businesses offering reliable dividends.

Performance has also proved resilient. Over the past year, HHI delivered a 15.6% NAV total return, outpacing its composite benchmark and comparable with the broader UK market, despite maintaining a near 12% allocation to bonds. Notable contributors included Phoenix, benefitting from stronger-than-expected cash generation, and M&G, buoyed by a new partnership with Japanese insurer Dai-Ichi Life.

Today, the trust offers a yield of 6.0%, well above the UK market and the AIC UK Equity Income sector average. At the same time, it trades on a 6.7%Discount, wider than its five-year average of 4.2%.

Analyst’s View

Over the past few years, the UK market has often been cast as a slow-growth story compared with the US. Concerns over economic uncertainty, escalating political tensions and the looming budget have only reinforced this view. Yet over the past year, UK equities have delivered returns comparable with many other global markets, despite the lack of high-profile tech names. Moreover, valuations remain historically low, whilst fundamentals across many companies continue to be robust. For investors seeking a differentiated route into this opportunity, HHI offers a distinctive solution.

A key strength of the trust lies in its blend of equities and bonds. Structural gearing funding the bond portfolio adds an extra layer of differentiation and with borrowing costs below the yield achieved on these assets, HHI benefits from positive carry, enhancing income without introducing undue risk. Its flexible approach spans large- and mid-cap UK companies, alongside selective overseas holdings, providing diversified exposure beyond the dominant dividend payers of the FTSE 100 Index. Disciplined stock selection, focussing on understandable business models, strong cash generation and sustainable dividend growth, underpins a portfolio that’s outperformed its composite benchmark over one, five, and ten years.

As rates on cash wane, we think HHI’s premium dividend yield of 6.0%, fully covered by earnings and supported by improving revenue reserves, stands out, offering both income and potential capital growth. With a wider-than-average discount, it presents as an attractive option for investors seeking a differentiated income profile with meaningful long-term upside potential. Investors should, however, be mindful of potential headwinds. In fast-rising equity markets, HHI may lag pure equity strategies, and periods of sharply rising inflation or pressure on credit markets could impact bond performance.

Bull

Differentiated investment process combines equities and bonds to deliver a high, sustainable and growing income, alongside capital growth

Merger with HDIV has increased liquidity and enhanced asset base, lowering costs and broadening appeal

Unique approach to gearing helps boost income and capital growth, alongside reducing volatility in the portfolio

Bear

Allocation to bonds may see the trust struggle to keep pace with a strongly rising market, relative to a pure equity strategy

Tilt to mid-cap companies may bring more sensitivity to state of the UK economy

Whilst the approach to gearing helps dampen some volatility through bond exposure, it will still magnify losses in down marke

Passive income plans can come in all sorts of weird and wacky forms.

But the whole point of passive income is that should be (more or less) effortless.

So my own approach is based on a few basic principles – I want it to be passive and I want to have a strong chance of earning income.

Why reinvent the wheel?

Many businesses already know how to generate income.

In fact, they generate so much more income than they need for their own business needs that they give some of it to shareholders on a regular basis, in the form of dividends.

At the start of June, it had £108m of cash and cash equivalents. Over the next six months, its operations generated £133m of cash. Even after spending on product development and sending a cheque to the taxman, Games Workshop divvied up £61m among its shareholders.

Yet it still ended the period with around £18m more in cash and cash equivalents than it began with.

In recent years, the FTSE 100 company has paid shareholders five dividends a year. All they need to do is spend money buying the share, sit back, and let the money roll in.

Taking a smart approach to income generation

But there are risks. Games Workshop’s concentrated manufacturing footprint means that if a key factory goes offline for any reason, sales could fall sharply. It plans a new factory in Nottingham, due to be completed next year.

Even a great, proven business can run into difficulties. So the savvy investor spreads money across multiple businesses to help mitigate the risk that one will do badly and reduce or cancel its dividends.

That does not necessarily take a lot of money – it is possible to buy shares even with a modest budget.

How much money could someone earn?

I use this strategy myself but I do not own Games Workshop shares, even though I think its fantasy universe and intellectual property are excellent competitive advantages.

Why ? The share looks pricy to me.

That is not bad: in fact it is in line with the FTSE 100 average. But I am earning much higher yields owning other shares, like 8.6%-yielding Legal & General and M&G, with its 9.5% yield.

Those are different companies to Games Workshop and each has their own risks as well as positive points. But by carefully selecting a diversified range of companies, I earn passive income from the hard work and proven business models of large blue-chip firms.

That need not be complicated.

An investor can start with how much they can spare, set up a share-dealing account or Stocks and Shares ISA then – having learnt something about key stock market concepts like valuation – start looking for income shares to buy.

The post This passive income plan is boring and unimaginative. That’s why it actually works ! appeared first on The Motley Fool UK.

In the 1800s, investing was largely the preserve of the wealthy, with limited options available to the smaller investor. Foreign & Colonial pooled investors’ money and invested it in a diversified portfolio, spreading risk across a basket of assets.

The closed-ended structure, which provided a stable pool of long-term capital, made these investment companies ideal vehicles for financing the expansion of the British Empire and the rapid industrialisation of the Americas. As global investment markets grew and diversified, the range of investment options available to investors with investment trusts expanded, and the range of trusts available also expanded.

Investment trusts have a fixed capital base

Open-ended vehicles, such as exchange-traded funds (ETFs), unit trusts and open-ended investment companies (Oeics) issue or eliminate excess shares at the end of each day to ensure the NAV and the share price match. This means there’s no room for a discount or premium to emerge.

This also means the capital base can shrink dramatically if the number of sellers consistently exceeds the number of buyers (and the price of shares in the fund falls). As the capital base shrinks, the vehicle has to continue selling assets to fund investment outflows. If those assets are challenging to sell, this can lead to a liquidity crunch. That’s why investment trusts tend to be the best vehicle for holding illiquid assets. They have no obligation to sell the assets, no matter how wide the discount to underlying NAV may become.

Infrastructure isn’t the only asset class that lends itself well to the investment-trust structure. Trusts are ideally suited to owning portfolios of mixed assets, such as bonds, gold and stakes in hedge funds or private-equity investment funds. BH Macro (LSE: BHMU) has a position in the global macro hedge fund Brevan Howard, giving investors access to a fund that would otherwise be unavailable.

HarbourVest Global Private Equity (LSE: HVPE)is just one investment trust in the private-equity sector, offering investors exposure to this asset class via the trust structure. RIT Capital (LSE: RIT) and Caledonia (LSE: CLDN)are two examples of trusts making the most of the flexibility offered by the structure. Both are majority-owned by their founding families and own a broad portfolio of assets, from private-equity holdings to direct investments in other companies and portfolios of equities.

The structure of the investment trust also lends itself well to borrowing money. Investment trusts that specialise in acquiring illiquid assets – such as wind farms, property and infrastructure assets – can borrow against those assets to increase growth and build the asset base. These companies can also borrow to invest in equities. Borrowing money to invest in shares can be risky, but trusts can often mitigate some of the risk by issuing long-term fixed bonds.

For example, Scottish American (LSE: SAIN) issued £95 million of long-term debt between 2021 and 2022 with a blended interest rate of under 3%, maturing between 2036 and 2049. The trust, which owns a portfolio of equities, as well as property and infrastructure via other investment trusts, used the cash to reinvest into the portfolio.

The ability to borrow money is particularly helpful for the real-estate investment trust (Reit) segment of the market. Reits are a version of the typical investment trust, but with tax benefits when the majority of the portfolio is deployed into property. Companies like Supermarket Income (LSE: SUPR)and PHP (LSE: PHP)have leveraged this structure to build property portfolios designed around supermarkets and healthcare facilities, respectively.

MoneyWeek has always preferred investment trusts to open-ended funds for the above reasons – and the fact that they have historically outperformed other actively managed, open-ended funds. However, this has started to change in recent years. Investment trusts, particularly in equities, have struggled to keep up with the performance of other funds. As a result, investors have drifted away, and discounts to NAVs have risen sharply.

But there’s still a place for trusts within investors’ portfolios. Thanks to the structure of trusts, they are invaluable to build exposure to specific themes such as small caps, emerging markets, property and infrastructure. There are virtually no mass-market alternatives to the infrastructure offering, and trusts such as BH Macro, RIT and Capital Gearing (LSE: CGT) offer the sort of portfolio diversification that just can’t be found elsewhere.

Risk appetite is a personal decision as only you can decide what level of risk you can tolerate emotionally and relative to your financial circumstances and time horizon.

If you would like greater balance in a portfolio, look to own bonds alongside shares. Multi-asset funds invest in both, with options including Vanguard LifeStrategy, BlackRock MyMap, Legal & General Investment Management’s Multi-Index funds and Aberdeen’s MyFolio Index range. The funds have different risk levels. Basically, the more exposure to shares, the higher the risk of the fund.

However, there’s also the risk of being too cautious, particularly for those with lots of time on their side. Those who take too little risk may not achieve their long-term goals.

For a medium-term time frame of five to 10 years, global funds are worthy contenders. Due to their diversification in having a spread of companies across the world, such funds are core holdings that investors can tuck away.

It’s important to consider how funds invest. Index funds and ETFs aim to deliver the return of the global stock market by following its movements. Active funds, those overseen by a professional fund manager, pick a selection of shares they think are the cream of the crop in an attempt to outperform the index, although there are no guarantees that will happen.

While both proponents of passive and active funds tend to be dogmatic, it’s important to remember that it’s not an either/or decision, as you can use both approaches.

You could choose an active fund that invests very differently from the global market, such as Fundsmith Equity or Dodge & Cox Worldwide Global Stock, and pair it with a global index fund or ETF, with options including Vanguard LifeStrategy 100% Equity, Fidelity Index World, or iShares Core MSCI World ETF USD Acc GBP SWDAwhich all invest in developed markets. For some emerging market exposure, options include HSBC FTSE All-World Index, and Vanguard FTSE All-World UCITS ETF GBP VWRL

You could also look to investment trusts F&C Investment Trust Ord FCITand Alliance Witan Ord ALW

They both own hundreds of global shares across various industries and sectors, which spreads risk.

One thing to remember is that global funds, particularly tracker funds, have a large weighting to US shares. For example, the MSCI World Index, which follows the ups and downs of 1,320 global stocks across 23 developed markets, holds 72% in US companies. Therefore, if you already have US exposure through US index funds, ETFs, or active funds, there’s the risk of doubling up.

Long-term goals

While global funds are core holdings, having smaller positions in satellite holdings investing in smaller companies, emerging markets, Asia-Pacific, and specialist themes, means you move further up the risk scale.

As a rule of thumb, having 70%-80% in core funds, and the remainder in satellite funds, helps to ensure you don’t have too much of your portfolio in adventurous areas that could all fall sharply at the same time.

Those investing for the long term – 10 years or more – have much more time on their side to ride out the greater volatility associated with higher-risk or adventurous funds.

Emerging market and Asia-Pacific funds invest in faster-growing, but less economically mature, economies. This area of the globe has more youthful populations than the West and growing middle classes. Options in interactive investor’s Super 60 list of investment ideas are: iShares Pacific ex Japan Equity Index, Fidelity Asia, Guinness Asian Equity Income, Fidelity China Special Situations Ord FCSS

Fidelity Index Emerging Markets, JPMorgan Emerging Markets Ord JMG and Utilico Emerging Markets Ord UEM0

Smaller company-focused funds are also higher risk than funds investing in larger companies, but historically the returns of smaller companies have been higher. WS Amati UK Listed Smaller Companies is a Super 60 fund, as are Fidelity Special Values Ord FSV and Diverse Income Trust Ord DIVIbut while the latter two have a bias to UK smaller companies, they invest across companies of all sizes.

Other options include funds targeting high long-term returns from specific sectors of the economy. There are numerous themes, but the main ones include artificial intelligence (AI), battery technology, cloud computing, clean energy, and demographical trends, such as the world’s ageing population.

Investing in technology shares is a well-established theme, with investment trust duo Polar Capital Technology Ord (LSE:PCT) and Allianz Technology Trust Ord (LSE:ATT) providing broad exposure.

Other funds focus on a sub-theme within the broader technology sector, such as Sanlam Global Artificial Intelligence, L&G Cyber Security ETF (LSE:ISPY), iShares Automation & Robotics ETF (LSE:RBTX), Pictet Robotics and First Trust Cloud Computing ETF (LSE:FSKY).

Another technology play, which is a much newer theme, are funds providing exposure to cryptocurrency-related companies such as VanEck Crypto & Blockchain Innovators ETF (LSE:DAGB) and Invesco CoinShares Global Blockchain ETF (LSE:BCHS).

Other examples of funds investing in themes, some of which are niche, include: Pictet Water, Regnan Sustainable Water and Waste, iShares Global Clean Energy Transition ETF (LSE:INRG), Guinness Sustainable Energy, Pictet Clean Energy Transition, EMQQ Emerging Markets Internet ETF (LSE:EMQP), Morgan Stanley Global Brands Equity Income fund, VanEck Video Gaming & eSports ETF (LSE:ESGB), iShares Healthcare Innovation ETF (LSE:DRDR) and Sarasin Food & Agriculture Opportunities.

It takes time to make a noticeable difference, which is great if you are just starting to invest.

Ian Cowie: this niche investment trust keeps paying its way

In uncertain times, our columnist finds plenty to like about this fund, which is his biggest source of tax-free income due to being held in an ISA.

16th October 2025

by Ian Cowie from interactive investor

Perhaps surprisingly, even very good news – like this week’s Gaza peace deal, when fighting ceased and hostages were freed – can be bad for some businesses. Everyone knows the old adage that it’s an ill wind that blows no good but fewer investors consider how benevolent events can have negative consequences.

For example, hopes that a permanent end to hostilities in the Middle East might fully reopen the Suez Canal to international trade have caused shipping freight rates to sink. To be specific, the Drewry World Container Index has lost more than half its value during the past year, with the going rate for 40-foot containers falling from $3,489 to $1,651 this month.

That’s not as bad as the 66% reduction in shipping traffic using this short cut between Asia and Europe, according to Office for National Statistics (ONS) estimates. This matters to many businesses because about 15% of all commercial marine vessels and 30% of container ships used Suez before Houthi rebels and others began attacking them.

Of course, the global trade war between America and China has also hit demand, while tit-for-tat tariffs on exports between Britain and the European Union have made a bad situation worse. Leaving the world’s largest free trade zone shortly before taxes soared on international imports looks riskier by the day.

On a brighter note, specialist investment trusts can help shareholders navigate uncharted waters of stock market returns in future.

As well as gaining exposure to a sector that few individuals could access directly, these closed-end funds can help us share the cost of dedicated professional asset management.

That includes diversifying over different types of shipping, which still carries more than 80% of global trade by volume, according to the United Nations Conference on Trade and Development (UNCTAD).

Coming down from the clouds of macroeconomics, one specific company in my portfolio shows how these potential risks and rewards can work in practice. Let me pipe aboard Tufton Assets Ord SHIP

(stock market ticker: SHPP for sterling shares and SHIP for dollar-denominated stock) where I paid 86p in August, 2021, for shares that cost only 85p on Thursday.

Put another way, SHPP shrank shareholders’ capital with a loss of 8.2% over the past year, following a total return or gain of 88% over five years, with no decade-long record after being launched in December 2017. At first blush that looks to be pretty poor performance but I intend to hang on to celebrate SHPP’s 10th birthday for several reasons.

First, quarterly dividends paid by this $352 million (£265 million) fund currently equal an eye-stretching 8.3% of the share price in total, according to Morningstar. Better still, payouts to shareholders have risen by an annual average of 7.4% over the past five years. Income-seekers should note that these shares go ex-dividend on Thursday 23 October.

It is important to beware that dividends are not guaranteed and can be cut or cancelled without notice. However, if the current rate of ascent could be sustained, SHPP would double investors’ income in less than a decade.

Second, the -18% discount or difference by which the share price trades below SHPP’s net asset value (NAV) looks excessive. To be specific, consider the rising income described above and the extent to which this fund has diminished capital losses despite sinking freight rates and stormy weather on global stock markets.

Third, there is growing anxiety about when the boom in technology shares might end with an almighty bust.

But fretting about an unknowable future won’t achieve much, while investing in old technology dividend-yielding businesses should diminish risk by diversification. Ongoing yearly charges of 1.05% don’t seem excessive for exposure to this specialist sector. All things considered, SHPP seems set fair to remain my biggest source of tax-free income, because I hold them in my ISA.

It’s also encouraging to see the fund managers Andrew Hampson and Nicolas Tirogalas, who have been at the helm since 2017 and 2023 respectively, report a NAV total return on Wednesday of 5% during the third quarter (Q3) of this year. That’s pretty impressive, especially when achieved despite the headwinds described above.

Avoiding container ships and focusing, instead, on product tankers – which can transport liquefied natural gas (LNG) or oil – and bulkers – designed to transport unpackaged cargo such as grain, coal, steel coils, or cement – seems to have helped.

Hampson added: “Compared to total gross capital raised since inception of $316.5 million, the company has returned $214 million of capital, including the Q3 dividend payable on 7 November, through dividends, share buybacks and capital redemption.”

So, short-term stormy weather for shipping might present profit opportunities for long-term investors willing to brave the waves. Or, as Shakespeare put it more poetically:

“There is a tide in the affairs of men Which, taken at the flood, leads on to fortune; Omitted, all the voyage of their life Is bound in shallows and in miseries. On such a full sea are we now afloat; And we must take the current when it serves, Or lose our ventures.”

Ian Cowie is a freelance contributor and not a direct employee of interactive investor.

Three High-Yielders Up to 10.8%, 36 Dividend Checks a Year

Brett Owens, Chief Investment Strategist Updated: October 14, 2025

Own a portfolio stocked with S&P 500 stocks? Or maybe an S&P 500 index fund?

It’s okay if you do. We won’t judge (well, maybe a little bit!). But answer me one question (without checking your brokerage account).

How much in dividends will you collect in November?

If you’re like most people, you don’t know. And if you do, you have a much better handle on your quarterly paying holdings than most (or maybe you’re using our AI-powered dividend tracker, Income Calendar!).

It’s understandable if you can’t come up with this number off the top of your head. Let’s drop a fictional $100K into five major Dow Jones Industrial Average stocks—Coca-Cola (KO), Procter & Gamble (PG), UnitedHealth (UNH), International Business Machines (IBM) and Boeing (BA)—and see what Income Calendar comes back with.

Popular Stocks Generate “Cash-Flow Chaos” Source: Income Calendar

Lumpy and, well, pretty lame—just a 2.1% average dividend! But I’ll tell you who likely can tell you exactly how much dividend cash they’ll bank next month: investors who hold monthly dividend payers in their portfolios.

These stocks and funds nicely balance out any quarterly payers we may own by providing a predictable monthly payout we can think of as a baseline, rolling in just as our bills do.

We’ll dive into three strong monthly payers that are precisely the right tools for this job below. First, let’s split our $500K among them and flip them into Income Calendar so we can see what kind of monthly dividend we can expect:

Big, Steady Payouts Dividends From These 3 Monthly Payers Source: Income Calendar

That’s better! Plus, we get TRIPLE the yield here—6.7% on average! (And as we’ll see below, thanks to the special dividends offered by one of our picks, we could end up with more than that.)

I chose to focus on three tickers because they come from the top-three places to find monthly payouts: closed-end funds (CEFs), business development companies (BDCs) and real estate investment trusts (REITs).

Let’s start with the CEF, since it sports the biggest yield of our trio—an outsized 10.8%. And it’s thrown off the odd special dividend, too.

DoubleLine Income Solutions Fund (DSL) Dividend Yield: 10.8%

Few people realize it, but yields on long-term bonds—10-year Treasuries, specifically, are capped. Think they’ll break 5%? Think again! These days, Treasury Secretary Scott Bessent is running some “yield-curve control” that, I’ll be honest, makes the capitalist in me cringe.

These moves are likely to mean lower interest rates for borrowers, with the 10-year yield setting the pace for consumer and business loans of all types—including mortgages.

The DoubleLine Income Solutions Fund (DSL) is our play here.

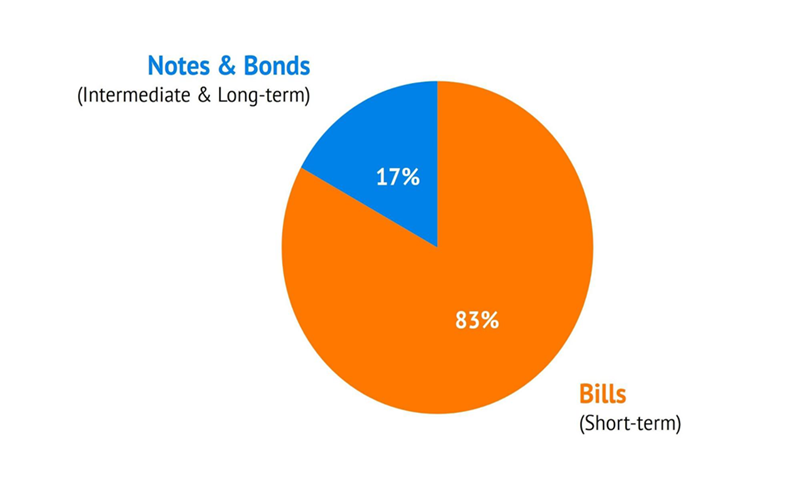

Bessent is leaning on short-term issues to fund Uncle Sam’s massive debt. It’s a practice Janet Yellen started, and Bessent once criticized—but then not only continued but amped up when he took over. Nowadays, he’s funding 83% of debt issuance short term.

The takeaway is that these moves lower supply of long-term Treasuries, boosting their prices and cutting their yields—pushing down long-term rates in the process.

Bond funds trade opposite interest rates, so that’s thrown a floor beneath corporate-bond funds like DSL.

That’s the macro side of our case. The micro side is this one is run by the “Bond God,” Jeffrey Gundlach, who has a long record of being right—and whose recent call for gold to hit $4,000 just came true.

He’s built a portfolio of mainly below-investment-grade corporates with relatively long durations (around 5.4 years on average). This is where the best bargains lie.

Moreover, longer-duration bonds will likely rise in value as rates fall. That’ll juice DSL’s portfolio and its divvie, which has rolled in steadily since inception, only pulling back a bit in the COVID chaos. And as you can see, big special dividends abound:

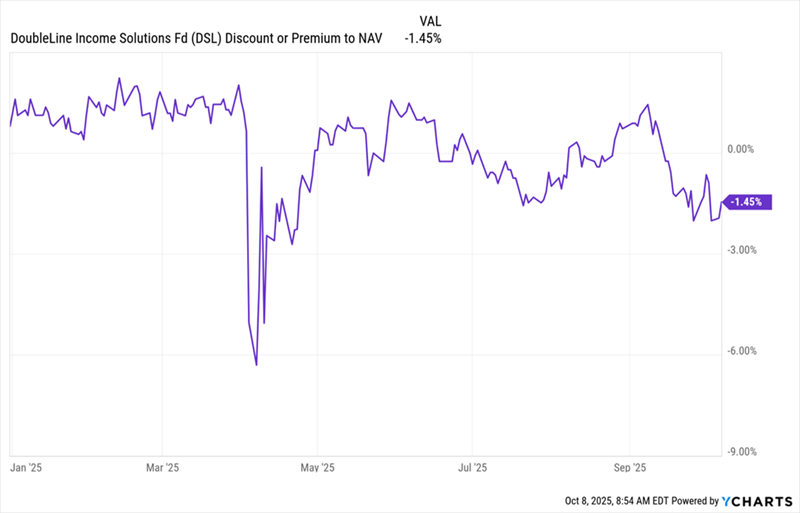

And we’ve got another sweet setup, too, courtesy of DSL’s discount to net asset value (NAV, or the value of its underlying portfolio).

Everything Is Going DSL’s Way—and Mainstream Investors Still Missed It

As you can see, this one has traded at a premium for most of the last year but has suddenly dropped to a discount. With the tailwinds behind DSL, there’s no reason for this deal. Let’s buy in before it’s gone.

Main Street Capital (MAIN) Dividend Yield: 7.4%

BDCs also gain from this rate setup. That’s because these companies, which lend to small and mid-sized businesses, have a large slice of their loans tied to the Fed funds rate (which, as we’ve been discussing, is likely to keep falling).

That would hurt BDCs’ loan rates, but we’re talking about a slow move. The economy is still strong, with the Atlanta Fed’s GDPNow indicator—the most up-to-the-minute gauge we have—estimating healthy 3.8% growth for the just-finished third quarter.

That means more chances for BDCs to spur new loans—with MAIN, one of the biggest BDC players, likely to grab a healthy share. Moreover, while MAIN doesn’t get specific, it did note in a recent investor presentation that its floating-rate loans “generally” include minimum “floor” rates.

The firm also says that 79% of its outstanding debt obligations are fixed rate, while on the lending side, 66% of its debt investments (i.e., loans outstanding) are floating-rate. That gives MAIN some built-in insulation on both sides of the balance sheet.

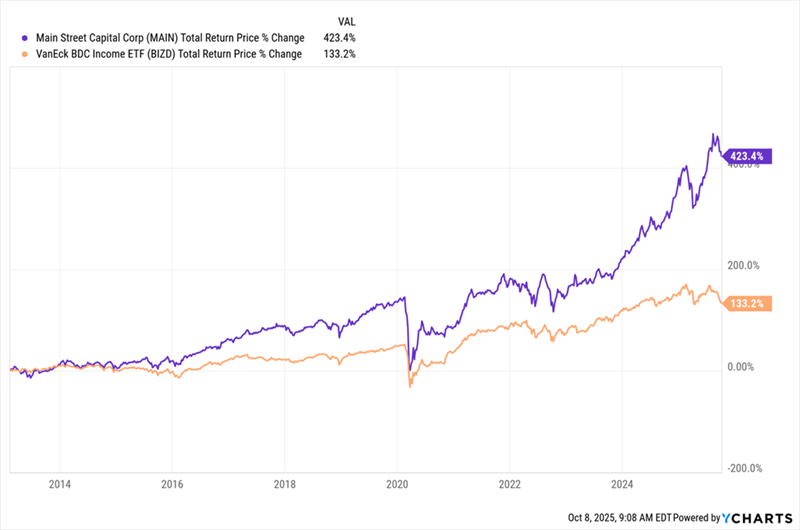

Then there’s the 7.4% yield, including MAIN’s regular special dividends. Moreover, over its 18-year history, this ironclad lender has never cut or suspended its regular payout, even during the pandemic or financial crisis. Check out this lovely payout picture:

(And to be clear, those dips in the chart above aren’t reductions—they’re those “supplemental” payouts I just mentioned, as are the spikes.)

No wonder MAIN has trounced the BDC index fund since that fund’s launch in 2013:

MAIN Gives Us ETF-Style Diversification—While Crushing ETFs

I expect more from this generous payer as rates quietly shift in its favor—and mainstream investors, fixed as they are on what the Fed is doing, slowly start to notice.

STAG Industrial (STAG) Dividend Yield: 4.1%

STAG Industrial (STAG) is profiting as more US companies come home—a trend we’ve been talking about for years—driving up demand for warehouse and factory space.

The thing I like most about STAG (beyond the payout!) is that management has put on a masterclass in risk management, making sure no tenant accounts for more than 3% of annualized base rent. STAG is also picky about who it chooses to rent to: 84% of tenants have revenue above $100 million.

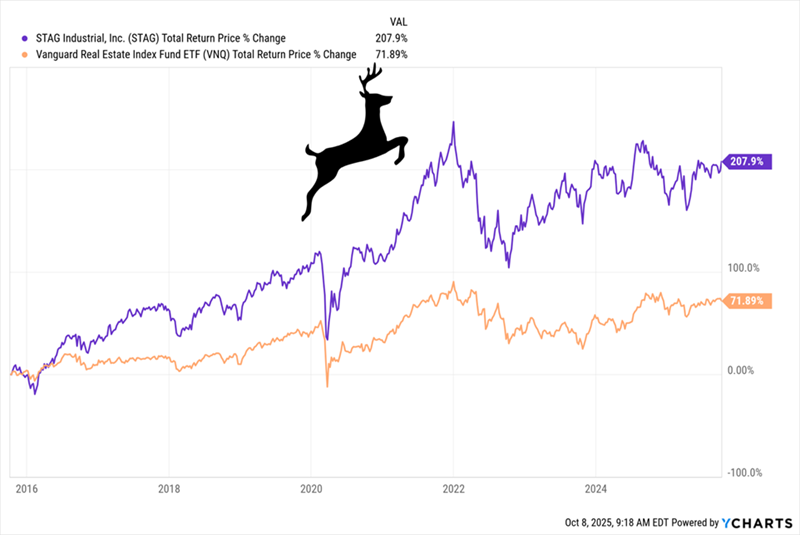

Then there’s the dividend, which yields 4.1% and is paid monthly. That is a smaller yield than MAIN and DSL, but that makes it very reliable: As I write this, the dividend occupies 68% of the midpoint of STAG’s 2025 FFO forecast—very safe for a REIT.

The firm has more than made up for that in price gains: in the last decade, STAG has tripled investors’ money, compared to a “meh” total return for the go-to REIT ETF.

STAG Leaps Past Other REITs

With 97% of its operating properties occupied and rental revenue rising sharply—up a fit 9% from a year earlier in the latest quarter—the company’s outlook is solid. That makes this 4.1% monthly dividend a nice pickup to bring some monthly predictability to the quarterly payers you’re now holding.

Turn Your Portfolio Into a 10.2% Monthly Income Machine

As I just showed you, there are plenty of monthly dividend stocks out there—you just need to go a little beyond the S&P 500 names most people stick with.

REITs, BDCs, CEFs and, yes, some regular stocks offer monthly payouts. But you still need to separate the winners from the pretenders.

Investors are being bombarded with messages about the rising risk of a stock market crash, and more specifically the bursting of the artificial intelligence (AI) ‘bubble’. Some observers predict a grim correction that will lay waste to portfolios, pensions and funds. In such an event, economic growth would also be jeopardised, given that the hundreds of billions of dollars of investments being pumped into AI are estimated to be driving 40 per cent of US GDP growth, while wealth generated by portfolio gains is supporting consumer spending. Others assert that while a correction or bear market is likely to happen, it will not approach the scale of the dotcom collapse because there are too many differences this time around. Former Scottish Mortgage Investment Trust manager James Anderson has nevertheless expressed concern about certain echoes of the turn of the century boom, namely the scale of AI-linked companies’ astonishing leaps in value (after a rocky start to the year, Nvidia has almost doubled its worth since April’s market lows) and a rising trend of ‘circular investments’ whereby companies support key customers by investing in them or offering finance deals. The Bank of England is also concerned about over-exuberance and circular deals. Even the tech giants’ own bosses admit it is a near-impossibility that their earnings can keep growing at the same pace indefinitely. Goldman Sachs warns that when AI investment slows, the knock-on effect on company valuations could wipe up to 20 per cent from the S&P 500. The counter-argument is that the steep rises in valuations of companies at the heart of the AI bubble are justified by factors that were not present in the dotcom bubble: staggering profitability and margins. Ben Barringer, head of technology research at Quilter Cheviot, adds that valuations are still well below previous bubbles – current valuations are half the peak of 60 times earnings seen in 2001 – while analysts at Capital Economics similarly note that forward price/earning ratios for big tech and the S&P 500 are not as high as they were at the peak of the dotcom era. Capital Economics’ view is that there will be a big correction in the S&P at some point once enthusiasm for AI in the market has peaked, but that this, barring some extraordinary development, will not be before 2027. It sees the S&P 500 hitting 7,000 at the end of this year, reaching 8,000 at the end of the next and then falling back to 7,000 at the end of 2027. How should investors prepare for a bear market, despite not knowing if it will happen soon or in a few years’ time? Crashes happen for a reason and there are plenty of possible triggers to make confidence drain away and pull the whole bull-market edifice down – disappointing US corporate earnings, cracks appearing in the AI story as benefits and promised productivity gains fail to materialise, or an unknown unknown. Investors will make their own minds up about whether such an event will happen sooner rather than later, but in light of the risk, it would be wise to conduct regular portfolio reviews with a view to adjusting weightings and being mentally prepared to avoid a panicked response. Like the mini earthquakes that precede volcanic eruptions (sometimes by years), we have already seen early warning signs in Tesla’s difficult year, Deepseek’s initial impact on Nvidia’s share price and trade wars causing stampedes for the exits. You may not want to sell down your US holdings if you have faith in your choices and in the long-term resilience of the US market. But you should bear in mind your time horizon: can you ride out a worst-case downturn lasting several years? The Nasdaq took 15 years to recover from the dotcom bust. Even if you are happy to keep backing US exceptionalism, you should pay attention to your tech exposure, which may now be far higher (and your portfolio far less diversified) than you intended with your original strategy. Many investors are still blind to the very significant chunk of Magnificent Seven exposure in their S&P 500 and global index trackers. You could reduce this risk by trimming holdings and reallocating to funds that have deliberately cut back on tech, as we outline here, or to defensive sectors and income generators. Fund flows show that many investors have been doing exactly that as they try to rebalance their portfolios ahead of an anticipated correction. Experienced investors know to stay focused on the long-term outcome, and that time in the markets, not timing the market, is what counts. It’s then a question of being prepared to ride out a correction and accepting the risks that some valuations may never recover, as happened during the dotcom fallout. Rosie CarrEditor

And, if you are writing on other sites, I’d like to follow anything new you have to post.Would you make a list of all of all your communal sites like your Facebook page, twitter feed, or linkedin profile?

And, if you are writing on other sites, I’d like to follow anything new you have to post.Would you make a list of all of all your communal sites like your Facebook page, twitter feed, or linkedin profile?