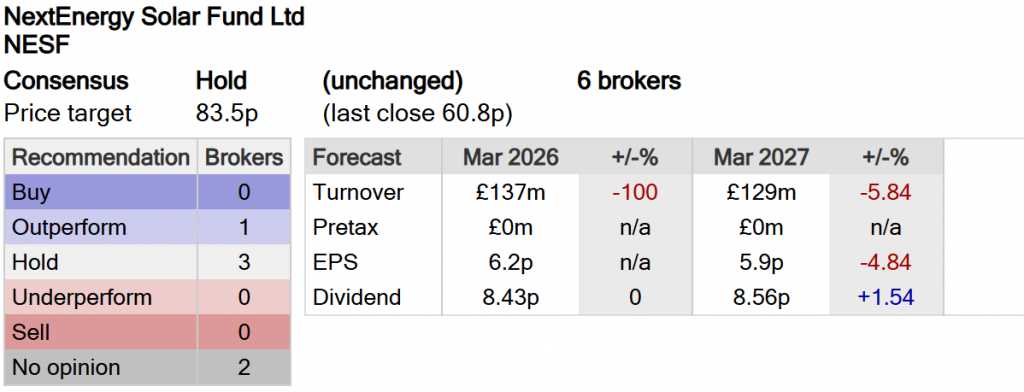

You are attracted to the Investment Trust because of its high yield, currently

13.8%.

It also trades at a 34% discount to NAV but the NAV could fall in time to nearer the price of the share, so lets call that a possible bonus.

Dividend:

· Total dividends declared of 2.10p per Ordinary Share for the Q1 period ended 30 June 2025 (30 June 2024: 2.10p), in line with full-year dividend target.

· Full-year dividend target guidance for the year ending 31 March 2026 remains at 8.43p per Ordinary Share (31 March 2025: 8.43p).

· The full year dividend target per Ordinary Share is forecast to be covered in a range of 1.1x – 1.3x by earnings post-debt amortisation.

· Since inception the Company has declared total Ordinary Share dividends of £407m.

· As at 20 August 2025, the Company offers an attractive dividend yield of c.11%.

The dividend of 8.43p is currently a covered dividend.

The share has a progressive dividend policy, although this year’s dividend is frozen at last year’s level.

If NESF stay in business, there is likely to be some amalgamation in the renewables sector, you could achieve

in seven years when all your cash has been returned and you could have a share in your portfolio that pays you income at zero, zilch, cost.

Because Mr. Market currently flags this is a higher risk share, it would reduce the risk if the dividends received were re-invested in another high yielder, increasing your yearly rate of return.

The fcast EPS are less than the fcast dividend so, the dividend could be trimmed, from its current level.

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

UK investors are spoilt for choice when hunting for shares with large dividend yields. Broadly speaking, the London stock market’s strong payout culture makes means it’s packed with top passive income shares.

With this in mind, here are three stocks with a yield above 10% to consider.

Henderson Far East Income: 10.2% dividend yield

Investing in emerging markets can sometimes be a bumpy experience. Political and economic conditions in regions like Asia can be volatile, impacting returns.

This hasn’t stopped Henderson Far East Income (LSE:HFEL) delivering large and growing dividends over time, though. Cash rewards have grown each year since the mid-2000s.

This reflects the investment trust‘s decision to prioritise passive income over growth. It’s also due to its wide range of holdings spanning different sectors and parts of the Asian continent. This diversified approach provides a smooth return over the economic cycle, and protects investors from weakness in specific industries and regions.

In total, Henderson Far East Income has holdings in 71 highly cash generative businesses. These include companies with enormous dividend yields like China CITIC Bank, Telkom Indonesia, and Evergreen Marine Corp Taiwan.

Roughly 58% of the trust’s assets are currently located in China, Hong Kong, and Taiwan. This leaves it vulnerable to current tough conditions in the region’s largest economy. But it could also help it outperform when the Chinese economy rebounds.

Global X SuperDividend ETF: 10% dividend yield

The Global X SuperDividend ETF (LSE:SDIP) offers similar diversification benefits that reduce risk and can enhance long-term returns.

This exchange-traded fund (ETF) also focuses on high dividend yield businesses across sectors, but does so with a more global flavour. US shares make up its largest single weighting, at 26% of the portfolio. Other well-represented countries include Brazil, Hong Kong, and the UK, providing investors with the stability of developed markets and the growth potential of emerging regions.

In total, Global X SuperDividend has 106 different holdings, including popular FTSE 100 stocks M&G and Phoenix.

Be mindful, though, that a high weighting of financial services stocks may impact performance during economic downturns.

NextEnergy Solar Fund: 13.8% dividend yield

Renewable energy producers like NextEnergy Solar Fund (LSE:NESF) can be among the most stable dividend shares out there.

Electricity demand remains pretty inelastic across the economic cycle, giving predictable cash flows across the economic cycle. Profits can dip during periods of unfavourable weather, but largely speaking these companies are pretty reliable for passive income.

NextEnergy holds particular appeal for me given weather-related uncertainties. It has 101 solar assets spread across nine countries, a diversified footprint that helps compensate for poor conditions in certain places.

This has supported consistent growth in annual dividends since NextEnergy listed in 2014. Encouragingly, the investment trust is increasingly focusing on battery storage to diversify revenue streams and further reduce the weather factor, too.

My Favorite Fund for Retirement Income (Yields 8.3%)

by Michael Foster, Investment Strategist

I’m regularly struck by something American investors always seem to take for granted: The many choices we have available to gain financial independence.

And investors in closed-end funds (CEFs) make the most of these choices. These high-yielding funds kick out 8%+ dividends on average, and the portfolio of my CEF Insider service, which helps investors make the most of CEFs, pays even more, with its 18 holdings paying a rich average yield of 9.4%.

Plus, these funds offer stock-like upside, which makes them pretty much tailor-made for delivering financial freedom.

We’ll sketch out how two specific CEFs can help you find your way to an earlier, richer retirement in a bit. But first, back to that embarrassment of choices I mentioned a second ago.

What American Investors Take for Granted

Back in my 20s, when I was studying to get my PhD in Europe, I was told I had to pay into the national pension fund, and I would get that money back when I qualified for it. At that time, I qualified at 62, which seemed absurd – nearly 40 years for me (a severely underpaid academic!) to get back money I desperately needed today.

But as it turns out, I was lucky.

Europe’s mandatory retirement age is rising. Denmark, which currently has the oldest retirement age in Europe at 67, is raising that to 70. Germany, where a normal retirement age is currently 66, is discussing raising that to 73.

Whether you like the life of a worker or not, I’m almost certain that you like having the ability to choose that life without having to worry about governments changing the rules on you mid-game.

A Look at America

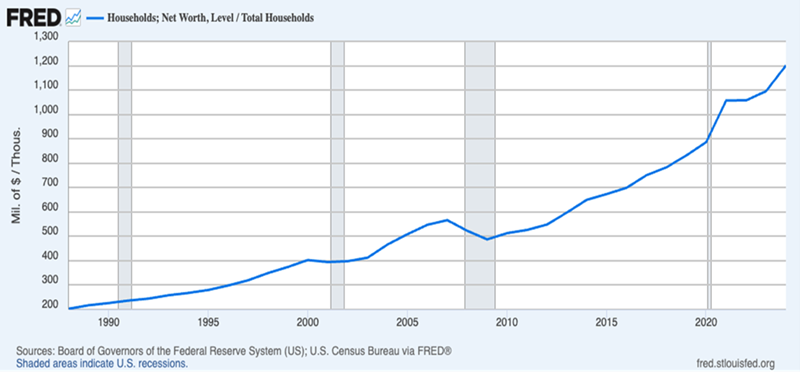

This lack of choice pushed me away from Europe in my 20s and led me back to America. Here’s what I found when I returned.

This chart shows that the average American household has gone from $200k in savings in the 1980s to $1.2 million now – and, no, that isn’t due to inflation. That $200k in savings would be $535k in 2025 dollars, so more than half of the jump to $1.2 million is due to actual value being created.

Of course, that wealth isn’t going everywhere. While all households have gotten richer on average, the top 0.1% of the population is attracting a greater proportion of overall wealth in the US, now near 14%.

The ethics of this aside, it’s clear that the households that have more wealth now have more choices – about when to retire, where to live, what lifestyle to adopt and so on.

In a way, it seems like Europeans have too little choice and Americans have so much that retirement investing can be tough for individual investors to navigate without either taking undue risks or locking themselves into weak returns.

CEFs: Your 8%+ Paying “Mini-Pension” (With Upside)

This is where CEFs come in, with their focus on assets from well-established companies. Plus their high yields almost act like a “mini-pension,” boosting your income without leaving you at the whim of the government.

This is the way I viewed CEFs in my late 20s, when I began using their high dividends to get the income I needed to make the choices I wanted. I still view them this way.

And in addition to their big dividends, these funds often chalk up strong returns, too, thanks in large part to their discounts to net asset value (NAV, or the value of their underlying portfolios). As these discounts – which only apply to CEFs, by the way – shrink, they put upward pressure on the fund’s price.

And the best part is that CEFs are easy to buy, trading on public markets just like stocks.

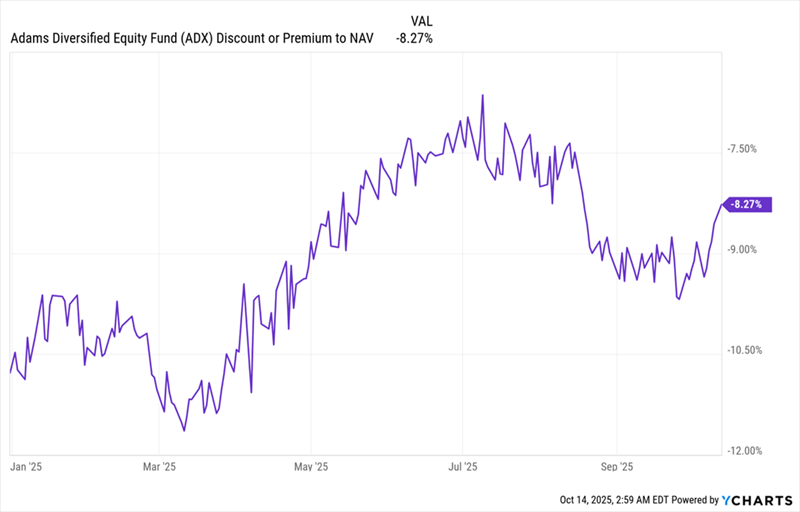

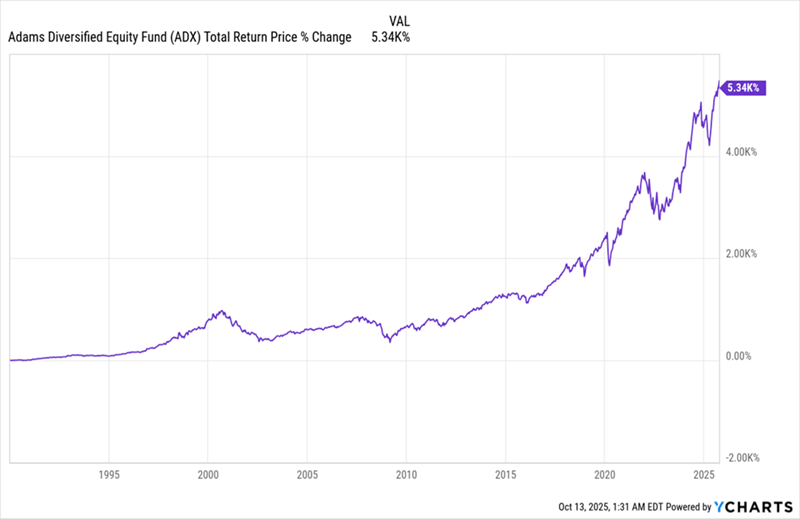

Consider the first CEF we’re looking at today, the Adams Diversified Equity Fund (ADX). It’s one of the oldest funds in the world, tracing its history back to the 19th century (and is a current CEF Insider holding, too).

This one is about as blue chip as it gets, with stocks like Microsoft (MSFT), Amazon (AMZN) and JPMorgan Chase & Co. (JPM) among its top holdings.

What’s more – and this is the key part – ADX trades at an 8.3% discount to NAV as I write this, and that discount is in the sweet spot, cheaper than it was a few months ago but carrying momentum as it steams toward par.

ADX Is a Rare Bargain in a Pricey Market

ADX has been paying dividends since before the Great Depression, and its 8.3% dividend yield is fully covered by the 13.3% total NAV return (or the return on its underlying portfolio) it’s enjoyed over the last decade. Moreover, ADX has delivered a 5,340% return to its shareholders, with dividends reinvested, since the late 1980s, when US household wealth just started to meaningfully tick higher.

ADX’s Long-Term Gains

That kind of performance – coming our way at a discount and with an 8.3% dividend – is exactly what we want from our “mini-pension,” and ADX delivers.

But, as I said, we do have choices here. And ADX isn’t the only US-stock-focused CEF that delivers a large income stream and has withstood the test of time.

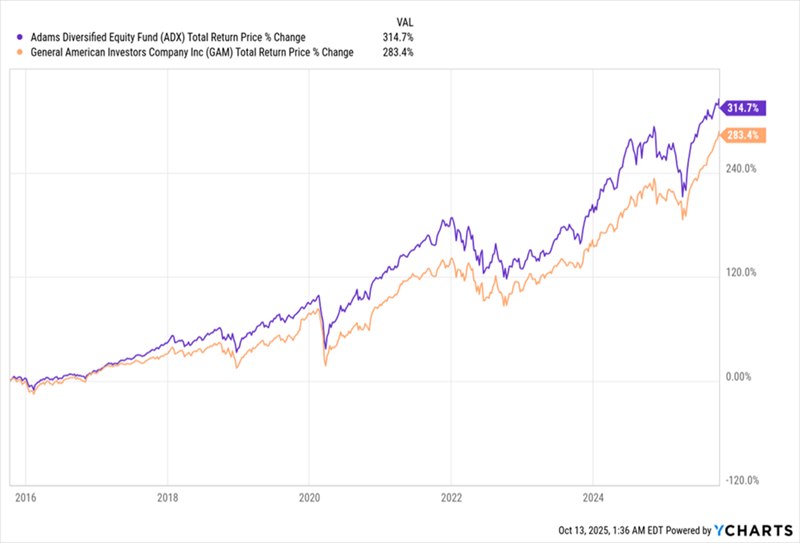

Another is the General American Investors Company (GAM), which was launched in 1927 and yielded an impressive 9.4% to investors in 2024. GAM also holds large caps, with Alphabet (GOOGL), Berkshire Hathaway (BRK.A) and Apple (AAPL) among its top holdings.

And, like ADX, this fund’s market pricebased return has been strong over the last decade – though not quite as strong as ADX – with a 14.4% annualized return.

2 Strong Funds, But ADX Has an Edge

Moreover, GAM’s 9.3% discount sounds like a good deal, but that’s near its smallest-ever level, so we’re not rushing out to buy the fund today. But it is worth watching, and gets tempting when that discount drops to double digits.

But the larger point remains: With high-yielding CEFs like these, we can start generating a meaningful income stream we can choose to use however we like

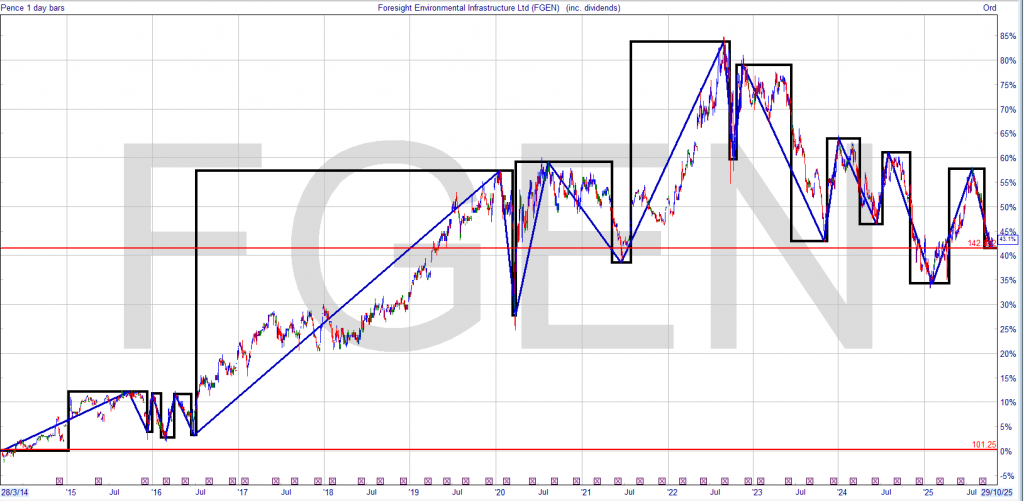

If you want to track the history of FGEN in the Snowball, type FGEN in the search box and the history of the share should be there.

Dividend

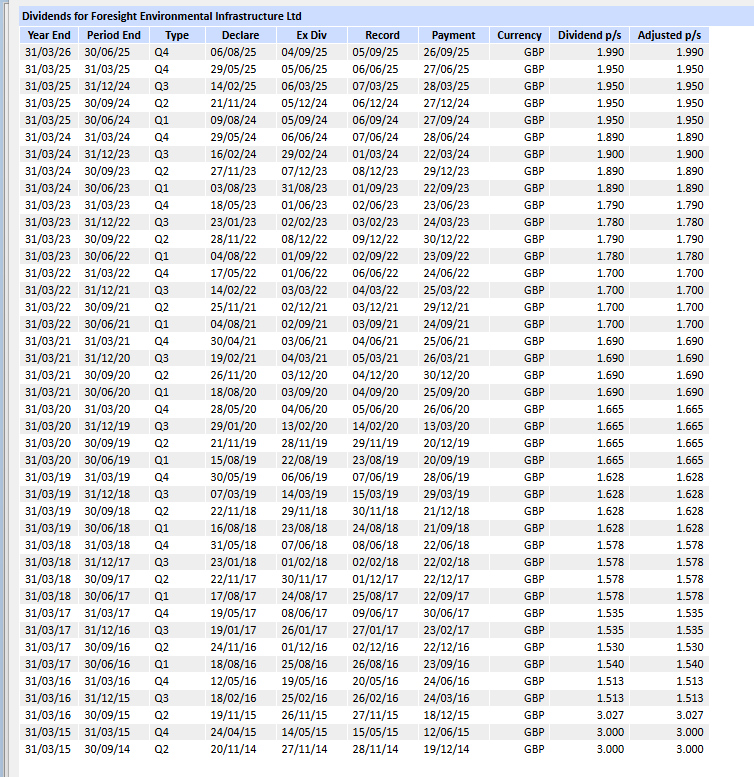

The Company also announces a quarterly interim dividend of 1.99 pence per share for the quarter ended 30 June 2025, in line with the dividend target of 7.96 pence per share for the year to 31 March 2026, as set out in the 2025 Annual Report – which represents a yield of 9.7% on the closing share price on 5 August 2025.

Current price 69p dividend 7.96 a yield of 11.5%

Foresight Environmental Infrastructure Ltd (FGEN) may appeal to income-focused investors, but caution is warranted due to recent performance and valuation metrics. Here’s a breakdown of the key factors to consider before buying:

📉 Performance & Valuation

Share Price: Currently trading around GBX 68.40, down roughly 21% over the past year.

Net Asset Value (NAV): Estimated at GBX 104.86, suggesting the stock trades at a significant discount to NAV.

Dividend Yield: Offers a high yield of ~11.5%, which may attract income investors.

Earnings: Recent net income is negative (-£2.84M), and EPS is effectively zero, indicating weak profitability.

Forward P/E: Estimated at 6.84, which is low, but reflects earnings uncertainty.

🏗️ Portfolio & Strategy

FGEN invests in a diversified portfolio of environmental infrastructure assets, including renewable energy and waste management.

Formerly known as JLEN, it has a long-standing focus on sustainability and infrastructure resilience.

⚠️ Risks & Considerations

Low RSI (26.22) suggests the stock may be oversold, but also reflects bearish sentiment.

Beta of 0.27 implies low volatility, which may suit conservative investors.

No consensus analyst rating or price target is currently available, making it harder to benchmark expectations.

🧭 Bottom Line FGEN could be a value opportunity for long-term investors seeking high yield and discounted NAV, especially if you believe in the resilience of environmental infrastructure. However, negative earnings and weak recent performance suggest caution. If you’re building a narrative around institutional cycles, this might symbolize a fund in a trough—potentially poised for recovery, or emblematic of structural headwinds.

Foresight Environmental Infrastructure Ltd (FGEN) trades at a deeper discount and offers a higher yield than its peers, but its recent underperformance and negative earnings make it a riskier bet. Greencoat UK Wind (UKW) and The Renewables Infrastructure Group (TRIG) offer more stability and scale, though they too face headwinds.

Here’s a comparative snapshot to help you sharpen your metaphorical lens:

🔍 Valuation & Yield Comparison

Sources:

🏗️ Portfolio Focus & Strategy

FGEN: Broad environmental infrastructure—anaerobic digestion, hydro, solar, and waste. Smaller scale, more niche.

UKW: Pure-play wind—onshore and offshore UK assets. Large scale, inflation-linked dividends.

TRIG: Mixed renewables—wind and solar across UK and Northern Europe. Diversified geography and technology.

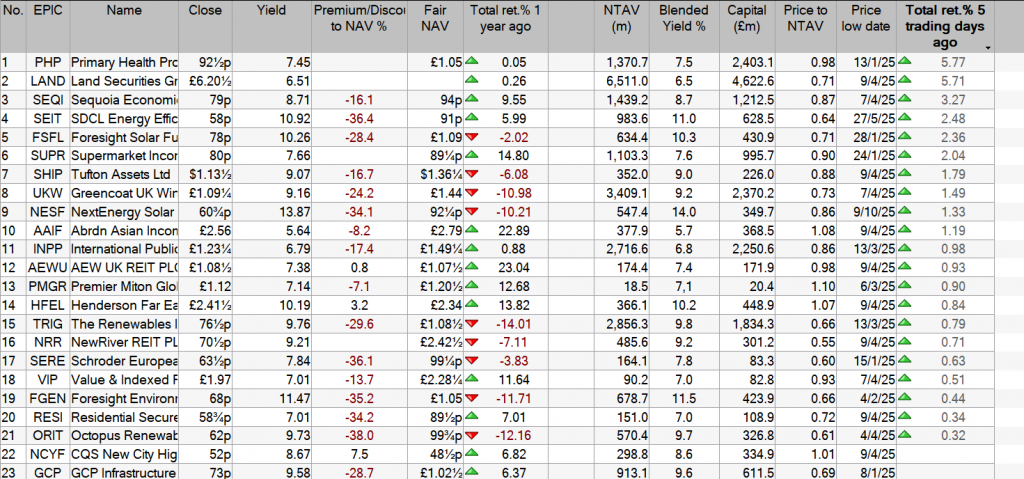

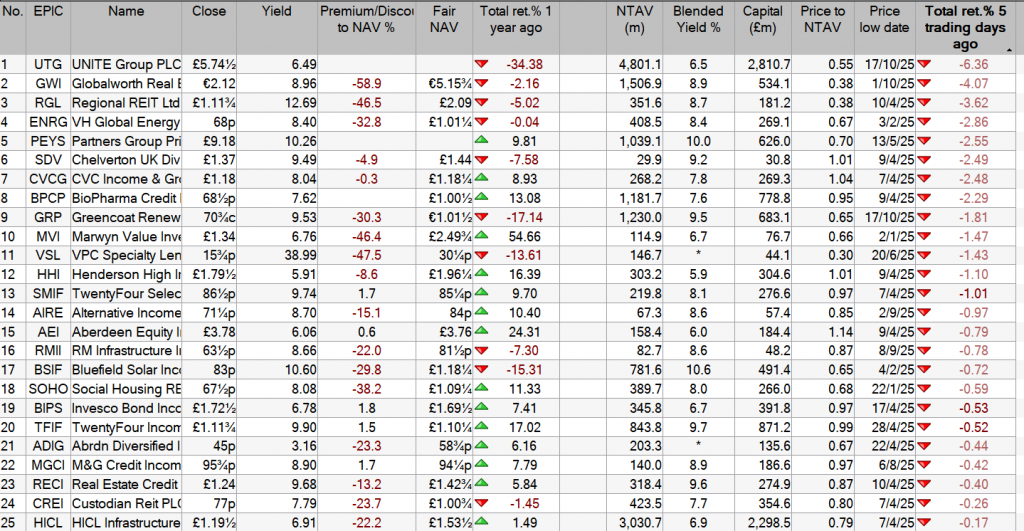

Gold glitters most but a September sell-off leaves one infrastructure fund yielding a sparkling 12%

15 October 2025

Last month was a great one for investment companies exposed to gold, biotechnology, emerging markets and corporate actions aimed at restoring shareholder value. Infrastructure fund prospects look less than golden with high interest rates and declining power price forecasts, but one £422m renewables portfolio perhaps deserves a closer look with shares on a wide 35% discount.

September’s risers and fallers

The historic rally in gold, racing 11.5% to a new high in September, and up 57% this year, continues to propel listed mining funds with Golden Prospect Precious Metal (GPM) shares leaping 30.5% last month. That makes the New City managed closed-end fund the biggest riser in our table (see left column in our first table).

After a 143% surge this year, the Guernsey investment company is rapidly closing in on a £100m market valuation that could put it on the radar of more investors.

Stable mate CQS Natural Resources (CYN) and BlackRock World Mining (BRWM), which also have exposure to smaller gold miners, gained 28.4% and 21.9% respectively. CYN’s recent run up may have frustrated Saba Capital as the activist hedge fund exited at a much lower price in a tender offer. Geiger Counter (GCL), a £70m uranium mining fund run by the Golden Prospect team, also put on 20%.

Best performers

Investment company

Share price return (%)

Investment company

Underlying net asset value (NAV) return (%)

Golden Prospect Precious Metal

30.5

Golden Prospect Precious Metal

31.1

Petershill Partners

29

Geiger Counter

21.1

CQS Natural Resources Growth & Income

28.4

CQS Natural Resources Growth & Income

20.8

BlackRock World Mining Trust

21.9

International Biotechnology

15

Geiger Counter

20

BlackRock World Mining Trust

14.8

JPMorgan China Growth & Income

13.8

JPMorgan China Growth & Income

14

International Biotechnology

13.6

Biotech Growth

13.6

Biotech Growth

13.2

UIL

11.6

UIL

13.1

Polar Capital Technology

10.1

Schroders Capital Global Innovation

13

Pacific Horizon

9.8

Source: Bloomberg, Marten & Co. Total returns exclude investment companies with market capitalisation below £15m.

Petershill pole vaults

Elsewhere, investment company corporate actions aimed at remedying poor shareholder returns resulted in a spectacular change in fortunes for Petershill Partners (PHLL).

Shares in the £2.5bn Goldman Sachs fund investing in alternative investment managers jumped 29% last month after unveiling plans to delist and return cash to shareholders. That more than halved the gap between the share price and underlying net asset value (NAV) with the discount falling from nearly 35% to under 16%. This puts it at the top of our list of “more expensive” London-listed funds (see right column of our third table below).

Emerging markets and biotech funds were also in favour with JPMorgan China Growth & Income (JCGI) and UIL (UTL), a sister fund and investor in Utilico Emerging Markets (UEM), both rising over 13%. At the end of the month UIL issued proposals for an annual £4m return of capital for the next three years until it delists that QuotedData’s James Carthew thought “ungenerous“.

Worst performers

Investment company

Share price return (%)

Investment company

Underlying net asset value (NAV) return (%)

JPMorgan Emerging EMEA Securities

-20.5

JPMorgan US Smaller Companies

-4.1

NB Distressed Debt Investment Extended Life

-15.6

NB Distressed Debt Investment Extended Life

-3.8

Aquila European Renewables

-13.7

STS Global Income & Growth Trust

-3.6

Life Settlement Assets

-12.5

Finsbury Growth & Income

-3.4

Gore Street Energy Storage Fund

-10.7

Scottish Oriental Smaller Companies

-3.3

Octopus Renewables Infrastructure

-9.3

Vietnam Holding

-3.3

Foresight Environmental Infrastructure

-9

VinaCapital Vietnam Opportunity Fund

-3.2

Globalworth Real Estate Investments

-8.7

Vietnam Enterprise

-2.9

Oryx International Growth

-6.7

Montanaro European Smaller Companies

-2

Scottish Oriental Smaller Companies

-6.7

Dunedin Income Growth

-1.7

Source: Bloomberg, Marten & Co. Total returns exclude investment companies with market capitalisation below £15m.

Russian doubts jolt JEMA

The Russian court of appeal upholding $439m in damages to VTB Bank against eight JP Morgan entities, including the JPMorgan Emerging Europe, Middle East & Africa Securities (JEMA) investment trust, dented the speculative bubble around the £83m fund’s shares which retreated 20.5% last month. As a result the erratic share price premium tumbled from 332% over NAV in August to a slightly less enormous 231% (see last table below).

Infrastructure investment companies suffered another poor month as yields on 30-year UK government bonds, or gilts, maintained their highs of around 5.5%, diminishing the value of the funds’ long-term cash flows.

Aquila European Renewables (AERS), down 13.7%, was the biggest faller in the peer group a month after writing down its valuation following the withdrawal of a potential bidder for some of its assets.

Octopus Renewables Infrastructure (ORIT) declined 9.3% despite announcing a five-year recovery plan on 23 September.

Share issuance and buybacks

Investment company

£m raised

Investment company

£m returned

Fidelity European

446.3

Scottish Mortgage

103

City of London

12.8

Monks

54.3

TwentyFour Select Monthly Income

10.9

Worldwide Healthcare

42.8

Invesco Global Equity Income

7.8

Alliance Witan

31

Invesco Bond Income Plus

7.5

Finsbury Growth & Income

29.2

Source: Bloomberg, Marten & Co. Excludes investment companies with market capitalisation below £15m. Figures based on the approximate value of shares at 30/9/25.

Data last month showed a spike in withdrawals from open-ended funds after jittery investors withdrew £1.8bn in August. These high outflows read across to investment companies whose average share price discounts, excluding highly-rated private equity giant 3i Group (III), widened to 14% from 13.1% in September, according to broker Winterflood.

That trend saw more share buybacks across the market as investment companies sought to draw a line in the sand under their share prices. Scottish Mortgage Trust (SMT), the £12.6bn Baillie Gifford flagship, bought back an estimated further £103m of its shares in response to the lack of investor demand.

By contrast, Fidelity European (FEV) issued around £446m shares in nearing completion of its merger with Henderson European which swells its assets to over £2.1bn and leaves it trading close to NAV on a narrrow 1% discount.

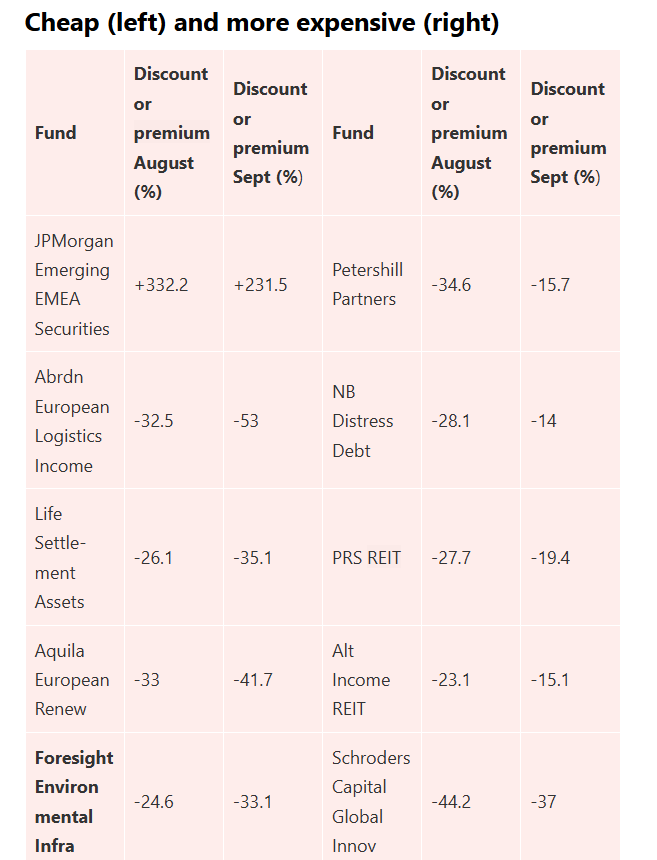

Cheap (left) and more expensive (right)

Source: Bloomberg, Marten & Co. Negative numbers show the discount or gap between share prices when they stand below their net asset value. Positive numbers show the reverse, the premium, or how much share prices stand above NAV. August data at 29/8/25 and September data at 30/9/25. Investment companies on the left have seen their discounts widen or premiums fall making their shares cheaper. Those on the right have seen their discounts fall or premiums rise to make them more expensive.

Fallen Foresight fund offers 11.6% yield

The continued derating of listed renewables funds last month has left eight of the sector’s 18 investment companies on double-digit dividend yields. That creates a fertile ground for bargain-hunting income investors.

One of those eight, Foresight Environmental Infrastructure (FGEN), catches our eye at the bottom of our last table after its share price discount widened from nearly 25% to 33% in September. The valuation gap has widened slightly since then with the shares trailing nearly 35% below net asset value where they offer an 11.6% yield against this year’s 7.96p dividend target.

Remarkably, the shares have slipped further since a continuation vote on 18 September when 94% of shareholder votes on a 59% turnout were cast in favour of the 11-year-old company’s continuation. Just over 6% voted to wind down the fund, slightly less than the 7.3% who did so last year.

At 69p, FGEN has fallen nearly 20% since the end of July and the shares have more than halved from their peak three years ago at 133p, having launched at 100p in 2014. Anyone thinking of buying now needs to consider two things: whether there will be further falls in the price, eroding the benefit of the 1.99p quarterly dividend; and whether the payout could even be cut in response to sector-wide pressures such as falling power price forecasts, low wind speeds and irradiation and grid constraints.

On the latter point, the company says its dividend in the last financial year of 7.7p per share was 1.3 times covered by earnings and it has consistently raised the dividend every year since launch. It operates a highly diversified portfolio, generating revenues from anaerobic digestion, bioenergy and hydro as well as wind and solar power. It expects 57% of next year’s revenues will be fixed on government subsidy or long-term contract, providing good visibility.

Moreover, following a strategic review in June, it is focused on core renewable energy assets with secure, long-term, inflation-linked revenues. As a result, it forecasts the future payouts will remain “healthily covered”.

In terms of the share price, FGEN holds a continuation vote if its shares trade below an average 10% discount over one year. That makes a further vote in 2026 very likely as things stand, providing a backstop that, if the derating continues, the company could be wound up and the value of its assets released. Meanwhile, the company is buying back its cheap shares having extended a £20m programme by £10m in March.