CTYand Temple Bar Ord TMPL0 have entered the top 10 table as FTSE 100 shares continue to surge.

Temple Bar, whose shares have beaten all other UK income funds and trusts so far in 2025, looks to target underpriced shares, while City of London is known, among other things, for a long record of increasing its dividends. Both recently traded on share price dividend yields north of 4%, though the sheer popularity of the trusts means shares in both also trade on premiums to the value of their underlying portfolios.

Interest rates were held at 4% at the Bank of England’s last meeting in September, with the fund’s yield closely linked to the base rate. Money market funds may be held inside SIPPs, ISAs or general trading accounts.

Global trackers tend to have substantial exposure to the US equity market, but a more UK-focused global fund remains popular. Vanguard LifeStrategy 80% Equity A Acc (B4PQW15), which has a fifth of its portfolio in bonds, has roughly half of its equity exposure in the US, with around a quarter in the UK.

Brett Owens, Chief Investment Strategist Updated: October 2025

The manic market just dumped business development companies (BDCs), again. These three dividend stocks paying up to 11.7% are poised to bounce back when sanity returns.

BDCs, which lend money to small businesses, are on the “outs” with the Wall Street suits after multiple soft jobs reports. The spreadsheet jockeys fret about an unemployment-induced economic slowdown and miss the real story: small businesses are making more money than ever thanks to AI.

Here is what’s actually happening in the Main Street economy:

Employers—especially nimble small business owners—are implementing AI to streamline and even run their operations.

With AI tools, fewer humans are needed.

So, we are seeing soft jobs reports as companies rationally prioritize automation over human hiring.

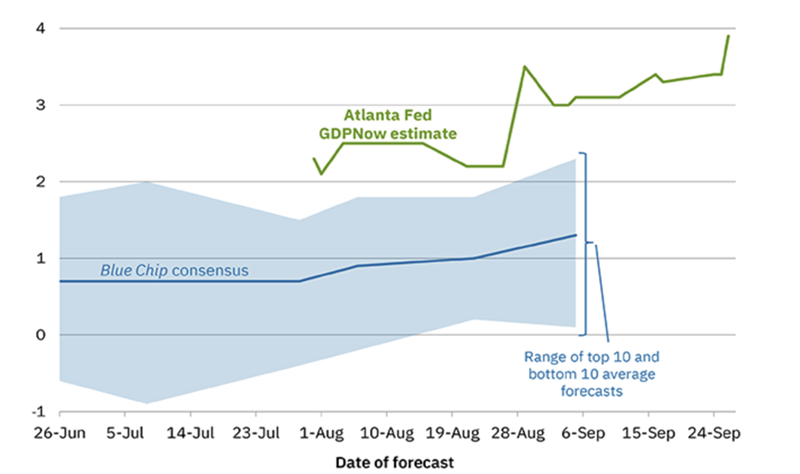

Small business profits are popping. While the unemployment numbers scream slowdown, the actual economy is booming. Check out the Atlanta Fed’s most recent GDPNow estimate—it’s up almost 4%!

Atlanta Fed Says Economy is Cookin’

We’ve been on this beat for months here at Contrarian Outlook. Automation is not slowing the economy. It is making it leaner and wildly profitable. While payrolls cool, output keeps rising. That’s no recession—it’s an efficiency boom!

This is music to BDCs’ ears. These lenders profit when Main Street’s cash flow swells.

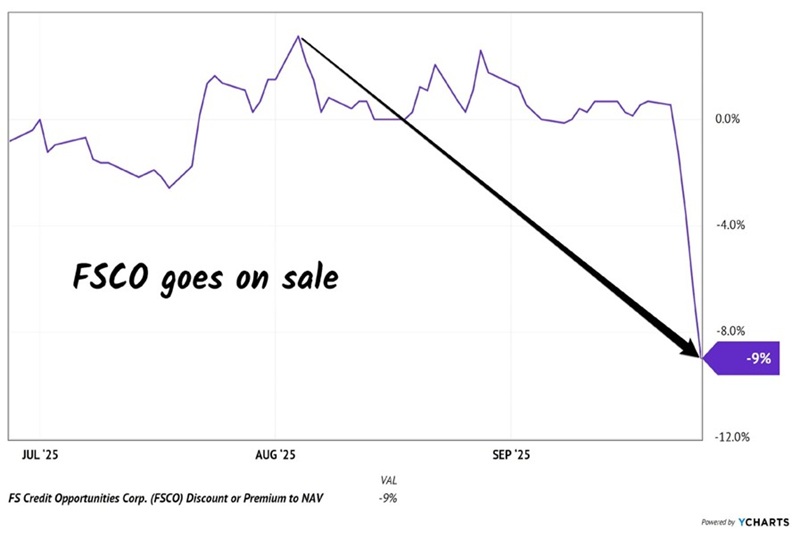

So, we thank knee-jerk sellers for giving us a deal on FS Credit Opportunities (FSCO), which yields 11.7% today. FSCO has been around for 10+ years but only traded publicly as a closed-end fund for the last two. CEF investors loathe newness, so FSCO fetched a discount to net asset value (NAV) until recently.

Portfolio manager Andrew Beckman and his team are skilled at “layering” credit—structuring loans with different levels of protection—so that FSCO is positioned to get paid back first even if credit conditions worsen. It’s an ideal fund to own if you were worried about the economy. This cash cow keeps collecting through slowdowns.

FSCO extends high-quality loans that are not subject to the daily whims of the public markets. These are private credit vehicles held by sophisticated investors who don’t care about recent job reports—they want their yield!

As do we income investors.

The vanilla dividend chasers finally found their way to FSCO this summer, sending it to a record 3% premium to NAV. But these weak hands fled when FSCO paid its monthly dividend (uh, the price drops because you just got paid, people!) and weak employment numbers weighed on the BDC sector.

The result? FSCO slipped from a 3% premium to a nifty 9% discount last week. Investors panicked but the strength of FSCO’s loans didn’t change:

FSCO Shares Went on Sale

FSCO continues to post strong credit metrics and cover its payout comfortably. Its high loan yields led Beckman and his management team to raise the monthly dividend multiple times this year:

FSCO Pays Monthly, Raises Often

FSCO looks good here, and it’s not alone. Ares Capital (ARCC), the largest BDC in America with $22 billion in assets, is killing it.

Ares is the big bully on the block—it sees the best deals before anyone else. And it shows. Non-accruals—loans that aren’t paying—remain a mere 2% of the portfolio, a hefty 20% below the industry average of 2.5%. No wonder ARCC’s net investment income (NII) has consistently covered its quarterly dividend, now $0.48 per share, with a small surplus each quarter!

And this bully loves economic turbulence. It thrived in 2020, growing book value through the Covid panic while smaller rivals stopped lending. And we have evidence that the punier BDCs are retrenching again, leaning into existing borrowers rather than pursuing new loans.

When the smaller fish throttle back, the bully turns up the volume. ARCC yields 9.5%, a payout supported by current income. That’s a rare combo of yield and quality in this market. We’ll keep collecting the digital checks.

ARCC’s Well-Covered Dividend

Last but not least, Main Street Capital (MAIN), is the steadiest grower in BDCLand. Not only has it paid monthly since 2008—hasn’t missed a beat—but it also adds quarterly “specials,” rewarding shareholders when portfolio income exceeds expectations.

MAIN invests in small, privately held businesses—between $25 million and $500 million in annual revenue—and takes both debt and equity stakes. This dual role lets it profit as a lender and as a partial owner when its companies thrive.

In the main, MAIN’s portfolio remains broad and balanced—about 190 companies across diverse industries, with no single position over 4%. That diversity keeps MAIN steady through economic cycles.

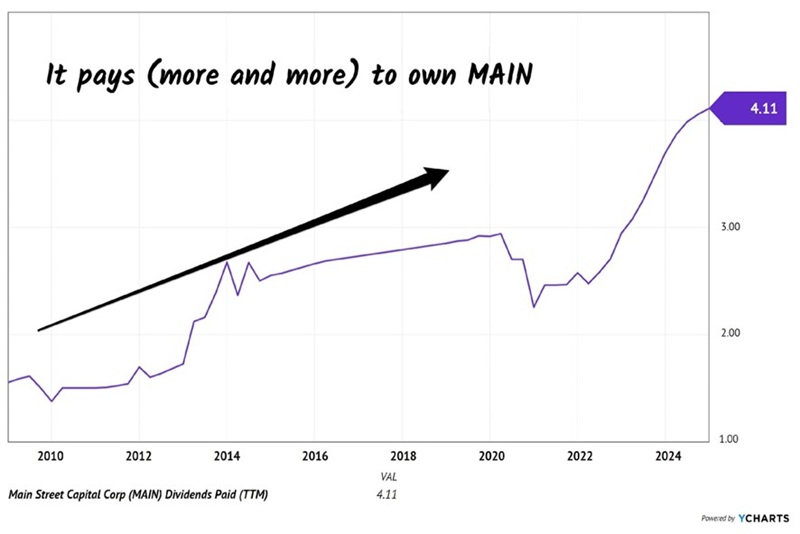

Since 2009, total annual dividends have jumped from $1.50 to more than $4 per share, a 170%+ climb that few serious dividend payers can match. The current yield sits around 6.8% today:

MAIN Regularly Raises Its Monthly Dividend

MAIN currently pays a generous 6.8%, with the majority delivered through dependable monthly payments. Check out this pretty payout picture:

MAIN pays monthly while ARCC “only” dishes its dividend quarterly.

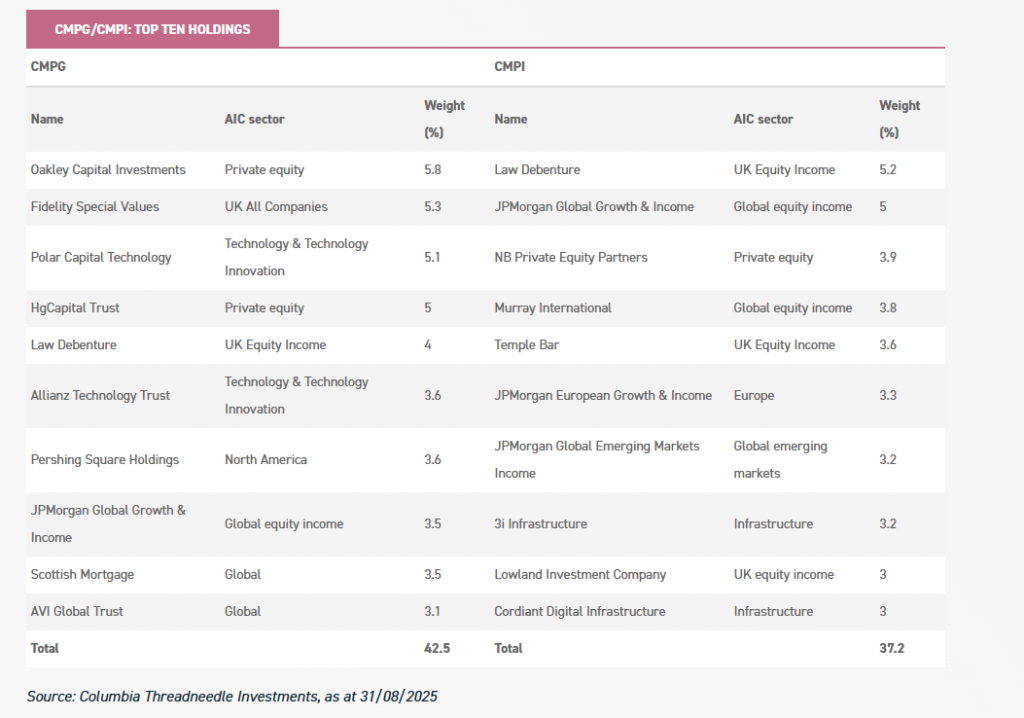

CMPG/CMPI offer exposure to best-in-class managers in the investment company universe.

Overview

CT Global Managed Portfolio Trust provides exposure to attractive investment themes through two Portfolios of investment companies via two share classes: CMPG, which aims to deliver capital growth, and CMPI, which focuses on income. Since June 2025, the trust has been managed by Adam Norris and Paul Green, who succeeded long-standing manager Peter Hewitt, who will retire at the end of October. Together, the new managers bring 35 years of investment experience.

Since taking over, Adam and Paul have increased exposure to themes where they see strong opportunities, including US and emerging market equities, which they expect to deliver robust earnings growth. They have also added to private equity-focused investment companies where realisations are emerging, such as Oakley Capital Investments (OCI) in the growth share class. Finally, the managers have identified attractive total return potential in the AIC Infrastructure sector, topping up their holding in Pantheon Infrastructure (PINT) in both CMPG and CMPI portfolios.

Moreover, while the basic strategy remains unchanged, Adam and Paul aim to adopt a higher-conviction approach, holding fewer investment trusts in larger size positions. They also plan to increase the allocation to global equities while reducing the UK weighting. In fact, this process is already underway, with additions to JPMorgan Global Growth & Income (JGGI) across both share classes and the exit of Lowland Investment Company (LWI) and Finsbury Growth & Income (FGT) from CMPG’s portfolio.

Assuming no unforeseen circumstances, the board expects CMPI to pay a Dividend of at least 7.6p for the current financial year, implying a prospective yield of c. 6.5%. At the time of writing, CMPG and CMPI were trading at Discountsof 3.3% and 2% respectively.

Analyst’s View

The new managers’ plan to increase the allocation to global equities and to build higher-conviction portfolios over time is, in our view, an exciting development. This should enable both share classes to capture a broader opportunity set, particularly in faster-growing regions, while the stronger emphasis on the managers’ best ideas could enhance long-term performance and reduce overlaps, albeit with greater sensitivity to the performance of individual holdings.

CT Global Managed Portfolio Trust offers exposure to promising themes, including US and emerging market equities, which are expected to deliver robust earnings growth, as well as private equity strategies benefiting from realisations. In fact, Adam and Paul see significant pent-up value in private equity-focused closed-end funds, which could be unlocked when IPO activity resumes and M&A activity picks up. While CMPI captures these opportunities to a lesser extent due to its income mandate, we think it offers an attractive prospective yield of c. 6.5%, well above that of the FTSE All-Share Index and the average constituent of the AIC Global Equity Income and UK Equity Income sectors.

Finally, we note that several closed-end funds are still trading at wide discounts, particularly those focused on alternative assets. While this reflects the challenges these sectors have faced over the past three years, it could also mean that both CMPI and CMPG portfolios are well positioned to capture a potential recovery. In particular, we believe that closed-end funds in more interest rate-sensitive areas, such as renewable energy infrastructure, could benefit from a more supportive rate environment.

Bull

Higher-conviction portfolios and greater global diversification could boost returns

Offers exposure to promising growth themes

Could benefit from a recovery in alternative-focused sectors

Bear

Retirement of long-standing manager

Trust of investment companies approach results in high overall cost of investment

Gearing on underlying trusts and income share class can exaggerate

Source: Columbia Threadneedle Investments, as at 31/08/2025

The new managers also see strong total return opportunities in the infrastructure space and have introduced Pantheon Infrastructure (PINT) into both CMPG and CMPI portfolios. PINT provides exposure to infrastructure assets across North America, Europe, and the UK through co-investments. With its focus on areas such as data centres and other digital infrastructure, Adam and Paul see significant growth potential in PINT’s portfolio and believe that future realisations could be supported by private equity capital. Adam and Paul have also introduced Cordiant Digital Infrastructure (CORD) into CMPI’s portfolio. As of 16/09/2025, CORD holds six companies that own infrastructure assets embedded in the digital economy, including communication towers, fibre-optic networks, and data centres, primarily in Europe. The investment company follows a ‘buy, build and grow’ approach, aiming to acquire companies, develop them to increase revenues, and expand their asset base. Adam and Paul note that CORD is highly cash-generative, which has enabled the company to increase its dividend each year since its launch in 2021 (offering a yield of c. 4.5% at the time of writing), while also reinvesting to grow its capital base, providing attractive NAV growth prospects. Given its strong total return potential, Adam and Paul do not rule out introducing CORD into CMPG’s portfolio in the future.

Finally, the new managers have increased CMPI’s holding in BioPharma Credit (BPCR), which specialises in providing loans to companies in the life sciences industry. These companies have struggled to raise capital through equity, as investor appetite for higher-risk, speculative ventures has waned amid a higher interest rate environment. They have also faced regulatory and political risks, including the Trump administration’s plans to introduce drug price controls and the vaccine scepticism of Robert Kennedy Jr., the new Secretary of Health and Human Services. As a result, companies in the life sciences sector have become more reliant on debt. Adam and Paul also note that BPCR charges high interest on its loans, incentivising companies to repay early and incur substantial prepayment fees, which have historically been used to pay special dividends. At the time of writing, BPCR offered a prospective yield of c. 7%.

Having skin in the market is often a good way to build up your knowledge of Investment Trusts, so could be a starter option.

CMPG Higher risk as TR only.

CMPI Lower risk as even if your timing is wrong you still have the dividends to re-invest.

Or you could have a 60/40 split and re-balance as profit/losses occur.

Let’s assume you were lucky and bought when it fell at £5.00. You decided to

and re-invest the dividends back into the share.

The 2020 dividend was 27p a yield on buying price of around 5%

The 2024 dividend was 43p a yield on buying price of around 8.5%

You have achieved the

without taking high risks, with your hard earned, and can open a new position that pays a dividend and if you keep your initial investment it will pay you income at a zero, zilch cost and if you are lucky you could do it all over again.

Three High-Yielders Up to 10.8%, 36 Dividend Checks a Year

Brett Owens, Chief Investment Strategist Updated: October 14, 2025

Own a portfolio stocked with S&P 500 stocks? Or maybe an S&P 500 index fund?

It’s okay if you do. We won’t judge (well, maybe a little bit!). But answer me one question (without checking your brokerage account).

How much in dividends will you collect in November?

If you’re like most people, you don’t know. And if you do, you have a much better handle on your quarterly paying holdings than most (or maybe you’re using our AI-powered dividend tracker, Income Calendar!).

It’s understandable if you can’t come up with this number off the top of your head. Let’s drop a fictional $100K into five major Dow Jones Industrial Average stocks—Coca-Cola (KO), Procter & Gamble (PG), UnitedHealth (UNH), International Business Machines (IBM) and Boeing (BA)—and see what Income Calendar comes back with.

Popular Stocks Generate “Cash-Flow Chaos” Source: Income Calendar

Lumpy and, well, pretty lame—just a 2.1% average dividend! But I’ll tell you who likely can tell you exactly how much dividend cash they’ll bank next month: investors who hold monthly dividend payers in their portfolios.

These stocks and funds nicely balance out any quarterly payers we may own by providing a predictable monthly payout we can think of as a baseline, rolling in just as our bills do.

We’ll dive into three strong monthly payers that are precisely the right tools for this job below. First, let’s split our $500K among them and flip them into Income Calendar so we can see what kind of monthly dividend we can expect:

Big, Steady Payouts Dividends From These 3 Monthly Payers Source: Income Calendar

That’s better! Plus, we get TRIPLE the yield here—6.7% on average! (And as we’ll see below, thanks to the special dividends offered by one of our picks, we could end up with more than that.)

I chose to focus on three tickers because they come from the top-three places to find monthly payouts: closed-end funds (CEFs), business development companies (BDCs) and real estate investment trusts (REITs).

Let’s start with the CEF, since it sports the biggest yield of our trio—an outsized 10.8%. And it’s thrown off the odd special dividend, too.

DoubleLine Income Solutions Fund (DSL) Dividend Yield: 10.8%

Few people realize it, but yields on long-term bonds—10-year Treasuries, specifically, are capped. Think they’ll break 5%? Think again! These days, Treasury Secretary Scott Bessent is running some “yield-curve control” that, I’ll be honest, makes the capitalist in me cringe.

These moves are likely to mean lower interest rates for borrowers, with the 10-year yield setting the pace for consumer and business loans of all types—including mortgages.

The DoubleLine Income Solutions Fund (DSL) is our play here.

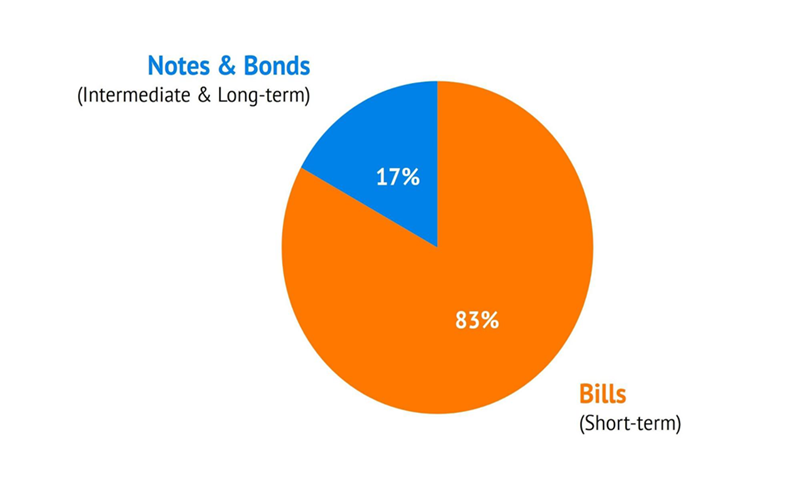

Bessent is leaning on short-term issues to fund Uncle Sam’s massive debt. It’s a practice Janet Yellen started, and Bessent once criticized—but then not only continued but amped up when he took over. Nowadays, he’s funding 83% of debt issuance short term.

The takeaway is that these moves lower supply of long-term Treasuries, boosting their prices and cutting their yields—pushing down long-term rates in the process.

Bond funds trade opposite interest rates, so that’s thrown a floor beneath corporate-bond funds like DSL.

That’s the macro side of our case. The micro side is this one is run by the “Bond God,” Jeffrey Gundlach, who has a long record of being right—and whose recent call for gold to hit $4,000 just came true.

He’s built a portfolio of mainly below-investment-grade corporates with relatively long durations (around 5.4 years on average). This is where the best bargains lie.

Moreover, longer-duration bonds will likely rise in value as rates fall. That’ll juice DSL’s portfolio and its divvie, which has rolled in steadily since inception, only pulling back a bit in the COVID chaos. And as you can see, big special dividends abound:

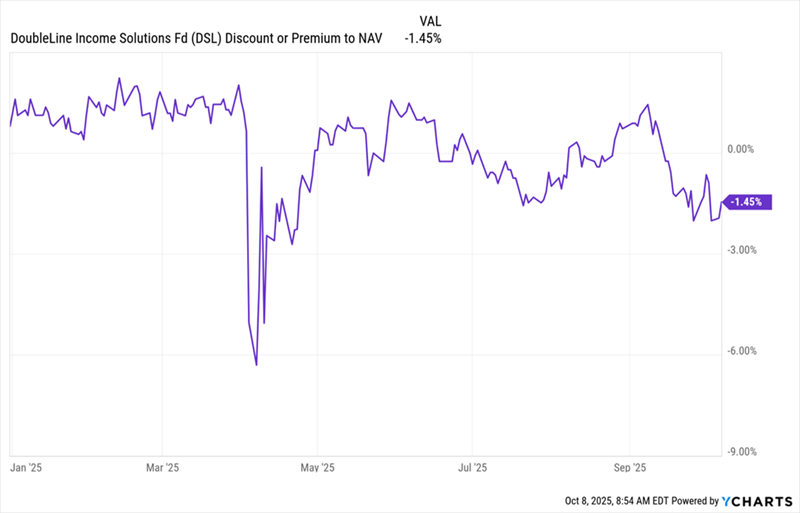

And we’ve got another sweet setup, too, courtesy of DSL’s discount to net asset value (NAV, or the value of its underlying portfolio).

Everything Is Going DSL’s Way—and Mainstream Investors Still Missed It

As you can see, this one has traded at a premium for most of the last year but has suddenly dropped to a discount. With the tailwinds behind DSL, there’s no reason for this deal. Let’s buy in before it’s gone.

Main Street Capital (MAIN) Dividend Yield: 7.4%

BDCs also gain from this rate setup. That’s because these companies, which lend to small and mid-sized businesses, have a large slice of their loans tied to the Fed funds rate (which, as we’ve been discussing, is likely to keep falling).

That would hurt BDCs’ loan rates, but we’re talking about a slow move. The economy is still strong, with the Atlanta Fed’s GDPNow indicator—the most up-to-the-minute gauge we have—estimating healthy 3.8% growth for the just-finished third quarter.

That means more chances for BDCs to spur new loans—with MAIN, one of the biggest BDC players, likely to grab a healthy share. Moreover, while MAIN doesn’t get specific, it did note in a recent investor presentation that its floating-rate loans “generally” include minimum “floor” rates.

The firm also says that 79% of its outstanding debt obligations are fixed rate, while on the lending side, 66% of its debt investments (i.e., loans outstanding) are floating-rate. That gives MAIN some built-in insulation on both sides of the balance sheet.

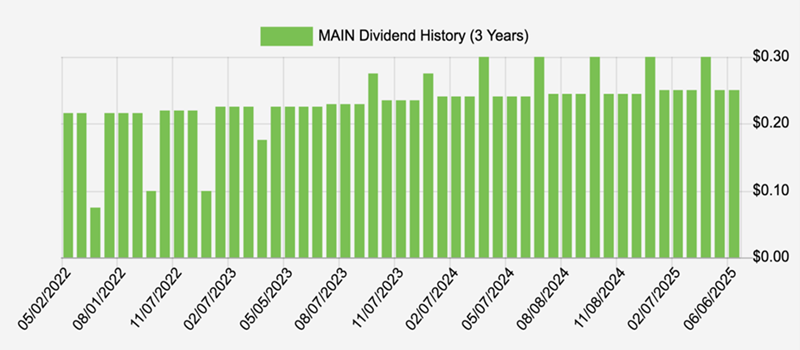

Then there’s the 7.4% yield, including MAIN’s regular special dividends. Moreover, over its 18-year history, this ironclad lender has never cut or suspended its regular payout, even during the pandemic or financial crisis. Check out this lovely payout picture:

(And to be clear, those dips in the chart above aren’t reductions—they’re those “supplemental” payouts I just mentioned, as are the spikes.)

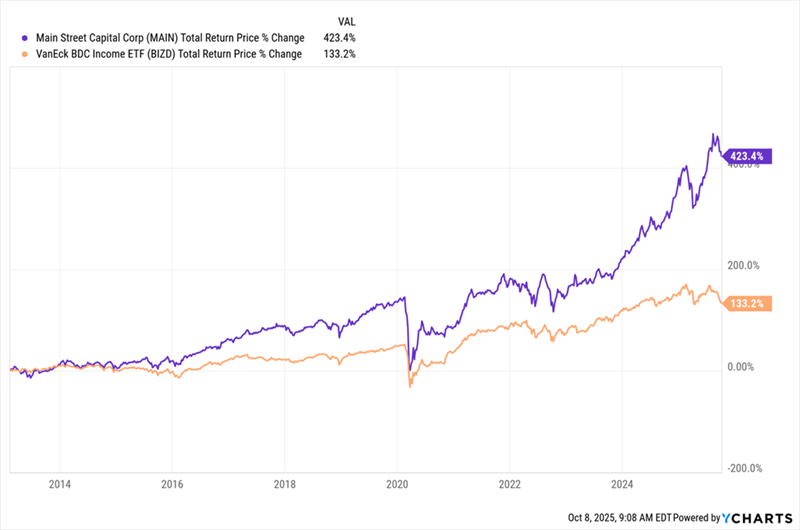

No wonder MAIN has trounced the BDC index fund since that fund’s launch in 2013:

MAIN Gives Us ETF-Style Diversification—While Crushing ETFs

I expect more from this generous payer as rates quietly shift in its favor—and mainstream investors, fixed as they are on what the Fed is doing, slowly start to notice.

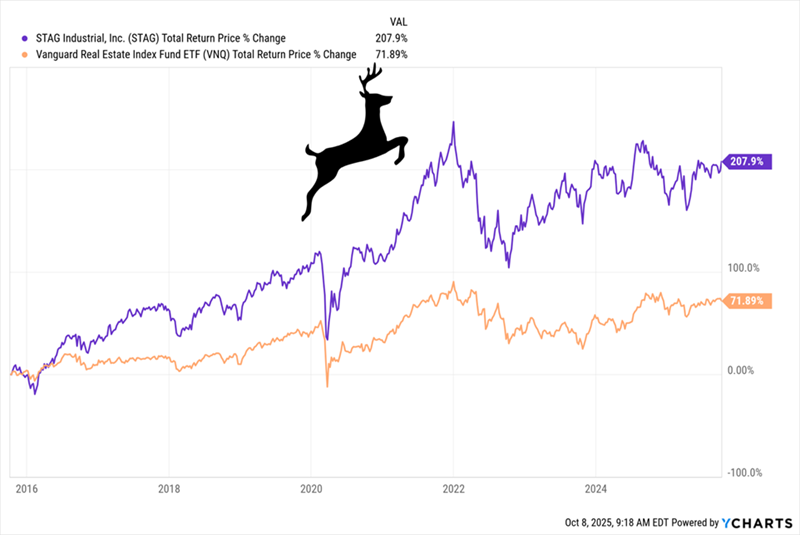

STAG Industrial (STAG) Dividend Yield: 4.1%

STAG Industrial (STAG) is profiting as more US companies come home—a trend we’ve been talking about for years—driving up demand for warehouse and factory space.

The thing I like most about STAG (beyond the payout!) is that management has put on a masterclass in risk management, making sure no tenant accounts for more than 3% of annualized base rent. STAG is also picky about who it chooses to rent to: 84% of tenants have revenue above $100 million.

Then there’s the dividend, which yields 4.1% and is paid monthly. That is a smaller yield than MAIN and DSL, but that makes it very reliable: As I write this, the dividend occupies 68% of the midpoint of STAG’s 2025 FFO forecast—very safe for a REIT.

The firm has more than made up for that in price gains: in the last decade, STAG has tripled investors’ money, compared to a “meh” total return for the go-to REIT ETF.

STAG Leaps Past Other REITs

With 97% of its operating properties occupied and rental revenue rising sharply—up a fit 9% from a year earlier in the latest quarter—the company’s outlook is solid. That makes this 4.1% monthly dividend a nice pickup to bring some monthly predictability to the quarterly payers you’re now holding.

One of the world’s top economic bodies has warned of the risk of an AI-fuelled stock market bubble.

Pierre-Olivier Gourinchas, the IMF’s chief economist, said: “We are seeing valuations that are quite stretched.” He added: “Our job is to look for potential risks and this is certainly one of the risks… There are echoes in the current tech investment surge with the dotcom bubble of the late 1990s. It was the internet then, it is AI now.” Mr Gourinchas said there was a risk that stock markets could “reprice sharply”, with knock-on impacts for people’s finances and the wider economy.

The IMF’s Global Stability Report said share prices could “collapse” if tech firms fail to deliver. It warned that, on some measures, the dangers were “substantially higher than during the dotcom bubble.”

Its warning follows a growing number of respected bodies, central banks and industry chiefs about a possible stock market bubble. It comes after Bank of England Governor Andrew Bailey said a stock market bubble could be about to burst as fears grow over the inflated value of AI tech companies.

In a letter to G20 ministers, he said increased debt levels and a failure to fully implement agreed financial reforms would lead to increased vulnerability. Mr Bailey, ahead of the latest IMF meeting, cautioned that there could therefore be a “disorderly adjustment”, which would see asset prices slump from recent highs.

Jamie Dimon, the boss of investment banking giant JP Morgan, is among those to have warned that there is a significant risk of a slump in stock valuations in the next six months to two years.

Nvidia, the chipmaker whose technology is integral to the roll-out of AI, has seen its shares leap 40% this year and has a market valuation of £3.5trillion, making it the most valuable company in the world. It was only founded 12 years ago.

There are also worries about the circular nature of the money flowing around the AI industry. A number of the deals struck by Nvidia have been seen as the chipmaker financing its customers to buy its chips. These types of agreements were said to be a characteristic of the dotcom boom.

Ruchir Sharma, from research firm Rockefeller International, estimated that 40% of America’s economic growth this year was due to AI spending.

Warren Buffett’s stock market valuation indicator, which divides the total US stock market capitalisation by the latest quarterly GDP estimate, recently surged past 200%, implying that US stocks are highly overvalued

In 2001, Buffett had described the metric as ‘probably the best single measure of where valuations stand at any given moment.’ The Oracle of Omaha had stated that the market would be ‘playing with fire’ when the indicator rose too high

Although the indicator is not recommended for timing the market, it signals the potential risk of investments. The current indicator reading implies that the gap between stock prices and economic output is unusually wide, fueling concerns about future returns.

However, note that today’s stock market is not the same as those decades earlier. Back then, the market was dominated by smokestack industries and cyclical companies. At present, the S&P 500 is dominated by megacap tech giants like Apple, Alphabet, Nvidia, and Microsoft, known for generating robust free cash flow and recording market share gains consistently. These companies could also be relatively less tied to economic cycles.

Buffett’s ‘Mr. Market’ Advice

Buffett’s core investment advice is about a character called ‘Mr. Market.’

‘Mr. Market is there to serve you, not to guide you. It is his pocketbook, not his wisdom, that you will find useful,’ Buffett had stated.

The metaphorical ‘Mr Market’ was invented by Buffett’s mentor, Benjamin Graham, who is known as the father of value investing. Graham created ‘Mr. Market’ to explain stock market behaviour. He taught Buffett at Columbia Business School and later hired him at his investment firm.

‘Mr. Market’ represents the market’s daily mood swings, which could be wildly optimistic or deeply pessimistic. Prices often reflect emotions rather than business fundamentals, which creates opportunities for disciplined investors to reap profits. Mr. Market offers to trade shares at different prices daily based purely on emotion.

Other times, Mr. Market gets ‘depressed and can see nothing but trouble ahead for both the business and the world. On these occasions, he will name a very low price, since he is terrified that you will unload your interest on him.’

‘The more manic depressive his behaviour, the better for you,’ Buffett had stated. This is because extreme mood swings lead to pricing errors.

‘When Mr. Market is euphoric, he’ll overpay for your shares. When he’s depressed, he’ll sell quality businesses at bargain prices. The wider his emotional swings, the more profit opportunities he hands you,’ according to the legendary investor.

The Berkshire Hathaway chair explained that ‘declining prices for businesses benefit us, and rising prices hurt us,’ adding that the most common cause of low prices is pessimism, which is ‘sometimes pervasive, sometimes specific to a company or industry.’

Buffett said he wants to do business in such an environment, ‘not because we like pessimism but because we like the prices it produces.’

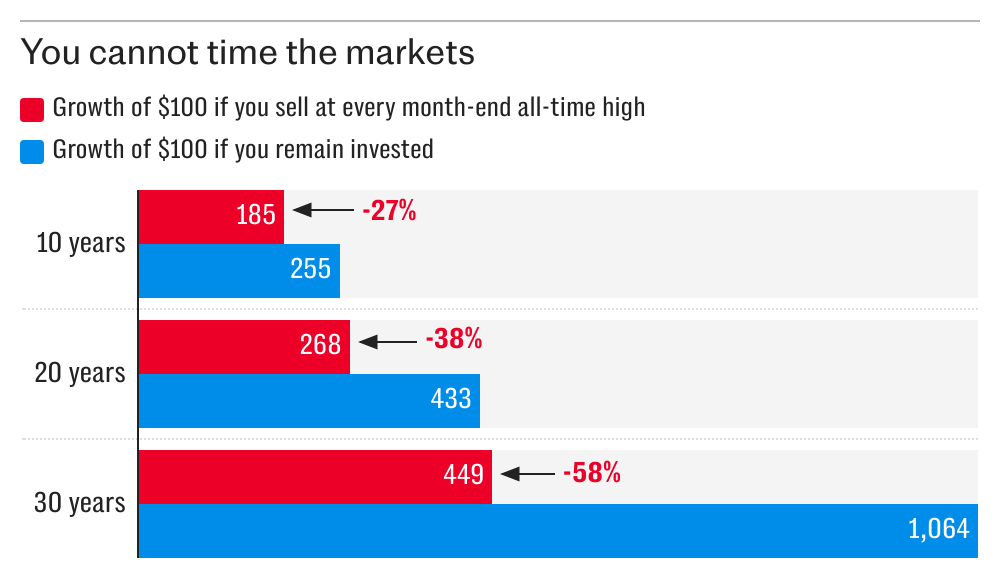

One of the toughest cognitive dissonances to shift is investing when markets are frothy. If the index is setting new records, there’s less room to grow and more room to lose out, surely?

That makes sense, but the data don’t agree. This week’s chart comes from Schroders’ head of strategic research, Duncan Lamont, who earlier this year attempted to assuage these fears.

As the chart shows, remaining invested will always be your best bet. If you were to cash out your investments at the end of a month that ends with an all-time high and then reinvest, you would be losing an enormous amount of capital – and that’s not even factoring in trading costs.

I’ve said it before and I’ll repeat it: don’t panic, do sit on your hands, and only ever take a risk you can afford.

Worried about the State Pension ? Here’s what I’m doing about it

The Triple Lock that protects the State Pension looks expensive. But Stephen Wright plans to build his own source of passive income in retirement.

Posted by Stephen Wright

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.Read More

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

It seems – to me anyway – that everyone thinks the Triple Lock that makes the State Pension rise every year is going to have to go sooner or later. So people like me need to take action.

The Triple Lock isn’t up to me directly. But I’m looking to act now to try and reduce the effect any changes might have on my retirement when the time comes.

Triple Lock

The full State Pension right now is £11,973 a year. And the Triple Lock means it increases each year by whichever’s highest out of inflation, average wage increases, or 2.5%. That’s a pretty nice deal, but it’s expensive. There’s disagreement about why and what to do about it, but I’m sensing a growing acceptance that it’s becoming hard to sustain.

If I’m right, thinking about other sources of income in retirement has never been more important. And the stock market’s top of my list.

There’s nothing quite like a government guarantee. But in the best cases, the income generated by owning shares in businesses can even outperform the Triple Lock.

Pension maths

Right now, I think an investor needs a portfolio worth around £299,325 to earn £11,973 a year. That’s based on a 4% average dividend yield, which looks realistic in today’s market.

Projecting ahead 30 years to when I retire, I think the State Pension could reach £29,061 a year (if the Triple Lock stays in place). That’s based on a 3% annual increase.

Assuming a 4% dividend yield, someone looking to retire at the same time as me will need a portfolio worth £726,525 to have a realistic shot at this. And that might be achieveable.

Starting from scratch, someone who invests £1,000 a month needs a 4.5% average annual return to reach £726,525 within 30 years. And that’s well below the 6.8% FTSE 100 has produced over the long term.

A stock to consider

In terms of specific names, Informa‘s (LSE:INF) stock I like a lot. The firm’s a leader in the trade show industry and high intangible assets mean these events have very attractive unit economics.

With one important exception, the firm’s increased its dividend at a rate above the Triple Lock each year for the last 10 years. In other words, it’s been a growing income stream for investors.

The exception is Covid-19. Remote working proved challenging for live events and this kind of disruption (though hopefully not this specifically again) is a risk for Informa’s trade show business.

Every business however, goes through difficult times and the firm’s rebounded strongly. In a lot of ways, this highlights the company’s resilience, which is crucial for a long-term investment.

Independence

Ultimately, I – and others like me – have a choice when it comes to retirement. We can either hope for the best with the State Pension, or we can think about trying to build our own income streams.

Relying on the State Pension looks risky to me. It’s expensive and decisions about it aren’t in my hands, which is why I’m looking at shares in companies like Informa..

The business made £800m a year in free cash last year with a market value of less than £12bn. It’s firmly on my radar at the moment, but it’s not the only one.

As the chart shows, remaining invested will always be your best bet. If you were to cash out your investments at the end of a month that ends with an all-time high and then reinvest, you would be losing an enormous amount of capital – and that’s not even factoring in trading costs.

As the chart shows, remaining invested will always be your best bet. If you were to cash out your investments at the end of a month that ends with an all-time high and then reinvest, you would be losing an enormous amount of capital – and that’s not even factoring in trading costs.