I really like your blog.. very nice colors & theme. Did you create this website yourself or did you hire someone to do it for you? Plz respond as I’m looking to construct my own blog and would like to know where u got this from. thank you

The blog uses wordpress, no coding required, if you can copy and paste you are good to go.

Brett Owens, Chief Investment Strategist Updated: October 8, 2025

The manic market just dumped business development companies (BDCs), again. These three dividend stocks paying up to 11.7% are poised to bounce back when sanity returns.

BDCs, which lend money to small businesses, are on the “outs” with the Wall Street suits after multiple soft jobs reports. The spreadsheet jockeys fret about an unemployment-induced economic slowdown and miss the real story: small businesses are making more money than ever thanks to AI.

Here is what’s actually happening in the Main Street economy:

Employers—especially nimble small business owners—are implementing AI to streamline and even run their operations.

With AI tools, fewer humans are needed.

So, we are seeing soft jobs reports as companies rationally prioritize automation over human hiring.

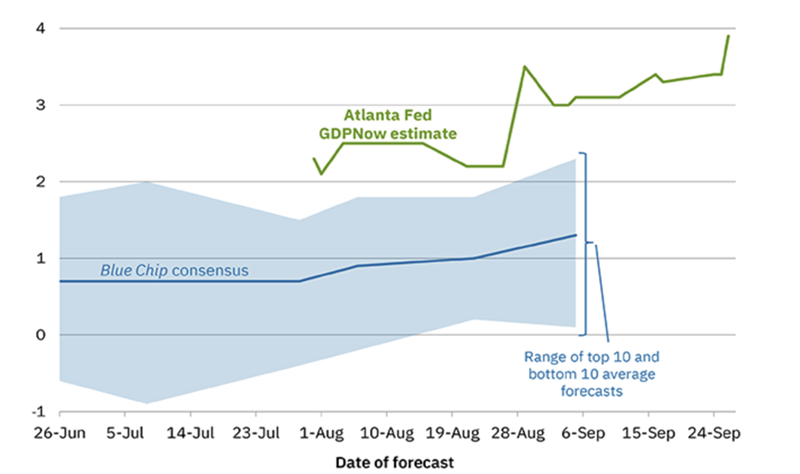

Small business profits are popping. While the unemployment numbers scream slowdown, the actual economy is booming. Check out the Atlanta Fed’s most recent GDPNow estimate—it’s up almost 4%!

Atlanta Fed Says Economy is Cookin’

We’ve been on this beat for months here at Contrarian Outlook. Automation is not slowing the economy. It is making it leaner and wildly profitable. While payrolls cool, output keeps rising. That’s no recession—it’s an efficiency boom!

This is music to BDCs’ ears. These lenders profit when Main Street’s cash flow swells.

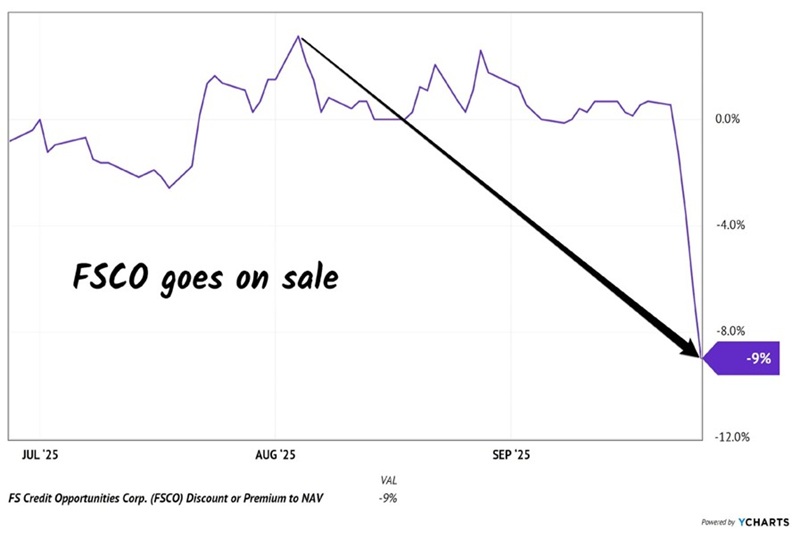

So, we thank knee-jerk sellers for giving us a deal on FS Credit Opportunities (FSCO), which yields 11.7% today. FSCO has been around for 10+ years but only traded publicly as a closed-end fund for the last two. CEF investors loathe newness, so FSCO fetched a discount to net asset value (NAV) until recently.

Portfolio manager Andrew Beckman and his team are skilled at “layering” credit—structuring loans with different levels of protection—so that FSCO is positioned to get paid back first even if credit conditions worsen. It’s an ideal fund to own if you were worried about the economy. This cash cow keeps collecting through slowdowns.

FSCO extends high-quality loans that are not subject to the daily whims of the public markets. These are private credit vehicles held by sophisticated investors who don’t care about recent job reports—they want their yield!

As do we income investors.

The vanilla dividend chasers finally found their way to FSCO this summer, sending it to a record 3% premium to NAV. But these weak hands fled when FSCO paid its monthly dividend (uh, the price drops because you just got paid, people!) and weak employment numbers weighed on the BDC sector.

The result? FSCO slipped from a 3% premium to a nifty 9% discount last week. Investors panicked but the strength of FSCO’s loans didn’t change:

FSCO Shares Went on Sale

FSCO continues to post strong credit metrics and cover its payout comfortably. Its high loan yields led Beckman and his management team to raise the monthly dividend multiple times this year:

FSCO Pays Monthly, Raises Often

FSCO looks good here, and it’s not alone. Ares Capital (ARCC), the largest BDC in America with $22 billion in assets, is killing it.

Ares is the big bully on the block—it sees the best deals before anyone else. And it shows. Non-accruals—loans that aren’t paying—remain a mere 2% of the portfolio, a hefty 20% below the industry average of 2.5%. No wonder ARCC’s net investment income (NII) has consistently covered its quarterly dividend, now $0.48 per share, with a small surplus each quarter!

And this bully loves economic turbulence. It thrived in 2020, growing book value through the Covid panic while smaller rivals stopped lending. And we have evidence that the punier BDCs are retrenching again, leaning into existing borrowers rather than pursuing new loans.

When the smaller fish throttle back, the bully turns up the volume. ARCC yields 9.5%, a payout supported by current income. That’s a rare combo of yield and quality in this market. We’ll keep collecting the digital checks.

ARCC’s Well-Covered Dividend

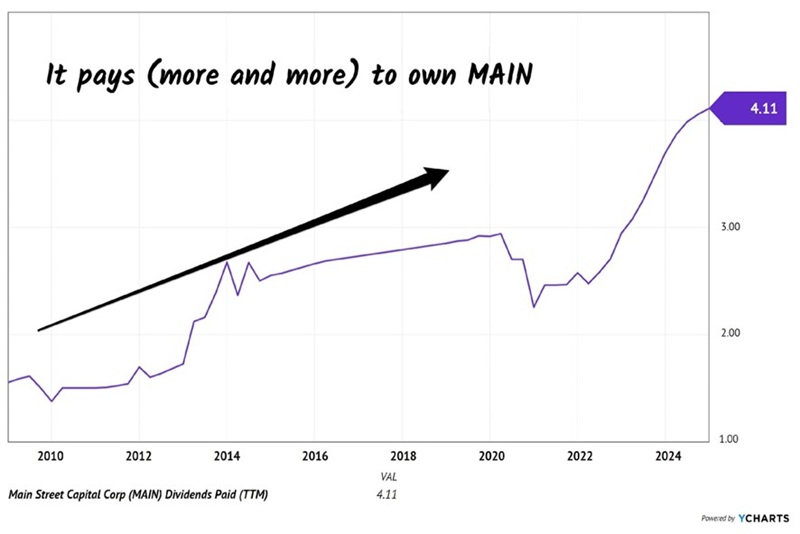

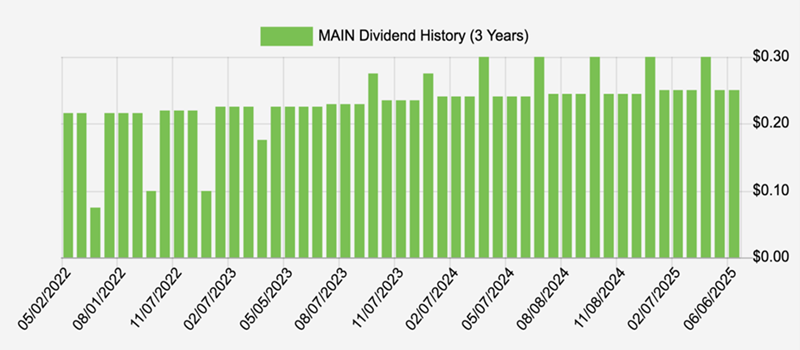

Last but not least, Main Street Capital (MAIN), is the steadiest grower in BDCLand. Not only has it paid monthly since 2008—hasn’t missed a beat—but it also adds quarterly “specials,” rewarding shareholders when portfolio income exceeds expectations.

MAIN invests in small, privately held businesses—between $25 million and $500 million in annual revenue—and takes both debt and equity stakes. This dual role lets it profit as a lender and as a partial owner when its companies thrive.

In the main, MAIN’s portfolio remains broad and balanced—about 190 companies across diverse industries, with no single position over 4%. That diversity keeps MAIN steady through economic cycles.

Since 2009, total annual dividends have jumped from $1.50 to more than $4 per share, a 170%+ climb that few serious dividend payers can match. The current yield sits around 6.8% today:

MAIN Regularly Raises Its Monthly Dividend

MAIN currently pays a generous 6.8%, with the majority delivered through dependable monthly payments. Check out this pretty payout picture:

MAIN pays monthly while ARCC “only” dishes its dividend quarterly.

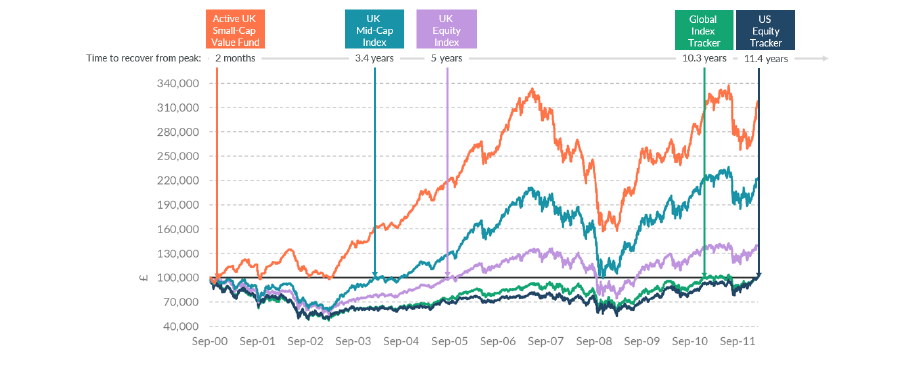

Market corrections: something to fear – or a buying opportunity? Market corrections can make novice investors nervous

Sitting tight is often better than selling up

The best mindset is to see corrections as buying opportunities Wednesday, 8th October 2025

Dear Fellow Fools,

Years back, I remember reading an angry message from a poster on an Internet investment forum. He’d been investing in an index tracker on an investment platform, it seemed, and – as happens from time to time – there had been a market correction.

The market had ‘corrected’ – that is, fallen – by 10% or so. And so, naturally enough, the value of our hero’s index tracker investment had also fallen. By exactly 10%.

How could this happen, he raged. How could the index tracker’s managers have been stupid enough not to liquidate the tracker’s underlying investments at the first sight of trouble, when – apparently – a 10% market correction was blindingly obvious for all to see?

Our hero could not be mollified, despite the best efforts of other forum members. It mattered not to him that an index tracker’s job is to track the index, and that it had done just that. Perfectly, at low cost.

He was down 10%. And investing, he raged, was a total scam.

ADVERTISEMENT

Get your first year of access to our flagship share‑picking service for just £149 £69! (SAVE £80) Two fully vetted and timely stock recommendations each month, AND ongoing coverage for all of our previous picks.

Access to our investing team’s Best Buys Now – the 6 shares they believe offer investors great value opportunities right now.

A bundle of Exclusive Premium Reports – meticulously researched and designed to potentially help you prepare for more of the uncertainties ahead.

PLUS! Your membership will be covered by our 30-day subscription-fee refund guarantee. To lock in this incredible saving, click here now !

Timing the market is a rare gift Clearly, he was mistaken on many, many fronts.

And it’s true that the managers of a different kind of investment fund might indeed have liquidated a part of its holdings – but only a part.

Because if there’s one thing that more difficult than judging when liquidating investments might be prudent, it’s judging when to buy back in.

And as we saw after the financial crash of 2007-2009 – when the FTSE 100 fell 48% – the difficulty of timing when to buy back in caught out plenty of those who decided to ride out the worst of it in cash.

I saw plenty of people back in late 2010 and 2011 who realised, ruefully, that they’d left it far, far too late.

Given the old adage about “time in the market” being better than “timing the market”, it’s often better, in my view, to just ride out the storm. That way, you’re at least sure of catching the upwave when it comes.

Don’t sell – buy! But our investor missed another important point.

Rather than selling, he should have bought. Market corrections can make a perfect time to ‘average down’ an existing holding, or get a good entry price for a new holding.

For income investors, there’s yet another attraction: with an unchanged dividend, a 10% drop in the share price delivers an 11% increase in the yield. Do the maths – see for yourself.

And bigger price falls produce a commensurately higher yield, of course.

Seasoned investors recognize this, of course. It’s what “buying the dips” means.

When to be greedy And occasionally – as with the financial crash of 2007-2009, or Black Monday in the 1980s, or Covid, or the aftermath of the Brexit referendum – falls in the market can be precipitous.

Rather than liquidating their investments and getting out of the market, many seasoned investors see such events as a rare opportunity to load up on quality businesses that have been marked down by general market turmoil.

American-British investor Sir John Templeton – the Warren Buffett of his era – summed it up well: “Buy when there’s blood in the streets”.

Warren Buffett himself said much the same thing: “Be fearful when others are greedy, and be greedy when others are fearful.”

It can call for strong nerves, I grant you. But when normal market valuations return, the resulting portfolio will be its own reward.

Until next time,

Malcolm Wheatley Investing Columnist, The Motley Fool UK

A market correction is an opportunity, unless your plan is to use the 4% rule and if that happens just as you start to spend your hard earned it’s a disaster.

With hindsight it’s easy to see the bottom of the market but in real time it’s much more difficult but as prices fall the yields rise and if you are happy buying the yield the risk is reduced. Remember there is no such thing as a risk free trade. GL

Bubble Can Push S&P 500 to 9,000 By End of 2026, Julian Emanuel Say

“It’s bigger, more, grander every time,” says Julian Emanuel, chief equity and quantitative strategist at Evercore ISI, as he sees a 30% chance that a bubble scenario can push the S&P 500 to 9,000 by the end of next year.

SMIF Current profit of £708 of which £408 are dividends.

I’ve booked the ‘profit’ of £300 which when added to the current cash and the dividends next week from RECI and RGL, which could be added to the ORIT position.

In the US on Tuesday, Wall Street ended lower, with the Dow Jones Industrial Average down 0.2%, the S&P 500 down 0.4% and the Nasdaq Composite down 0.7%.

“Investors took a breather from buying US stocks yesterday, near all-time highs, as a report showing Oracle’s profit margins were much lower than expected dampened the euphoria that followed the OpenAI and AMD announcements earlier in the week,” Swissquote’s Ipek Ozkardeskaya said. “But data centre demand is expected to rise exponentially through 2030 largely driven by AI…That outlook helps explain why dip-buyers stepped in as Oracle shares fell to around USD270. And that small bump will likely be forgotten quickly, with this morning’s news that Nvidia is considering investing USD20bn in Elon Musk’s xAI.”

She continued: “The real question isn’t whether AI will grow, but whether market pricing has run ahead of itself. And no I don’t buy for a second that AI models won’t generate revenue. There will certainly be losers, but also major winners.”

Ozkardeskaya noted that “the question of a bubble looms” but added: “Evercore ISI, in a note titled

A Big Beautiful Bubble, argues that while the S&P 500 is indeed in bubble territory, it likely has room to expand possibly pushing the index to 9,000 by the end of next year with a 33% probability.

“Eye-popping, yes, but they argue that rate cuts, improving sentiment, stronger earnings, reduced uncertainty and productivity gains from AI could keep investors piling in before the bubble eventually bursts…There’s also still ample room for leveraged investors to join the rally, given that net short positions in the S&P 500 remain deeply negative. The takeaway ? Don’t fear the bubble play along.”

Equity markets could make investors nothing in the next 10 years, warn managers

19 September 2025

Downing’s Simon Evan-Cook and Orbis’ Alec Cutler explain why investors should be wary of a downturn.

By Patrick Sanders

Reporter, Trustnet

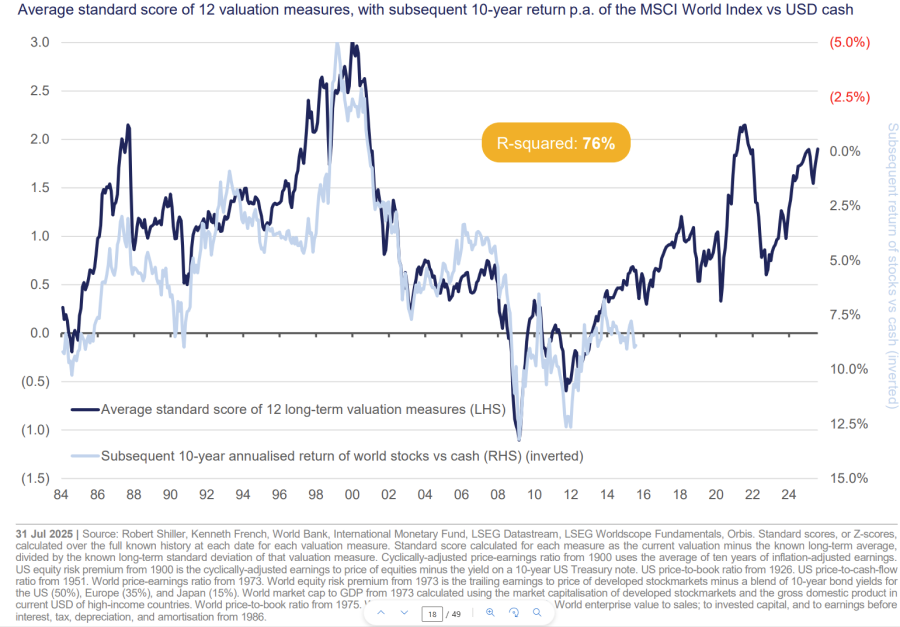

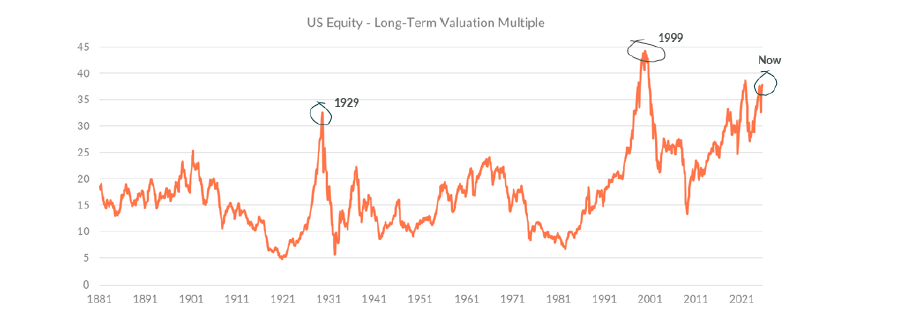

Equity markets have posted stellar returns over the past decade but extreme valuations and historical precedent indicate that this could be about to reverse, according to managers.

“People seem to think that equities are guaranteed a positive return. They aren’t. They could absolutely make zero in the next 10 years,” he said.

It seems “realistic” that equity markets deliver nothing or even lose money, thanks to the dominance of US stocks, which make up roughly 70% of the MSCI World index.

Since 2011, the S&P 500 has delivered a “spectacular” average yearly return of 14%, but this is based on unsustainable expectations, according to Cutler.

“To produce 14% again, you need valuations to go from already extreme 24x [price-to-] earnings to almost 40x earnings. You need corporate earnings, profit margins and valuations, which are near record highs, to increase further,” Cutler concluded.

The far more likely outcome is that the US equity market corrects and drags the rest of the global market down with it, he said. The average annual return of the S&P 500 is around 7%, so to return to that level, equity markets would post an average return of zero for “at least the next 10 years”.

This may sound absurd, he noted, but it has happened before. The chart below shows the average expected return on equities over 10 years, from different market valuations.

Source: Orbis Investments

“If you look back in history as far as you can get, whenever we’ve been at this level of valuation, markets returned zero over the next 10 years,” the Orbis manager explained.

On top of this, the US government’s “financial mismanagement” in relation to escalating debt levels and investors pulling out of American markets (both bonds and equities) could lead to a weaker dollar. This in turn could fuel further capital exodus from the country, sparking a US downturn.

“I would not be shocked if you get a 0% return from the global equity market from here,” he concluded.

Simon Evan-Cook, fund of funds manager at VT Downing Fox, agreed that this is a realistic concern. “There’s no God-given right that equity markets will go up every year, let alone to go up for another 15 years in a row,” he said.

While the past decade has been “mostly sunshine and rainbows” for global equities, strong performance is causing investors to develop “worrying” assumptions.

For example, many investors have concluded that active funds are no longer needed due to their underperformance compared to a surging global equity tracker.

“I completely understand why some people are asking themselves if they need an active fund, given that any attempt to do anything different has underperformed,” the Downing Fox manager said.

However, he warned that these assumptions were also around in the 1990s and backfired on investors as, in the following decade, the average global equity tracker “made you nothing”, Evan-Cook explained.

Performance of funds post 2000

Source: Downing Fox. Total return in sterling

The tech bubble collapse in 2000 was due to the high concentration of US equities, which had outperformed and become overvalued. When they corrected, they represented 50% of the global market and so dragged most portfolios down.

As Evan-Cook noted, while current valuations are not at the 1999 peak, they are approaching it. And global markets have become even more dominated by the US than they were 25 years ago.

If North America stocks re-rate, the resulting crash might look closer to the Nifty 50 downturn in the 70s, he suggested.

Long-term valuations of US Equities

Source: Downing Fox. CAPE Ratio, January 1881 to August 2025.

“Hence why it’s not outrageous to suggest that something as apparently reliable as a global tracker could go a long time without making money,” he said.

Not even the most popular stocks on the market would be immune. For example, in 2000, some investors thought Amazon would thrive due to the emergence of the internet, while others thought it was overvalued and heading for a fall. “Both investors would have been absolutely correct,” Evan-Cook noted.

Amazon shed almost 92% of its value between 2000 and 2005, but those that sold missed the rebound, he explained. This could happen again to some of the biggest stocks in the index, “despite how transformative things like artificial intelligence are”.

“Broadly, equity markets do go up over time”, Evan-Cook said “, but they can spend long periods of time that matter to investors going sideways or down. That’s a real risk right now.”

However, he said this is mostly a risk for global equity trackers and US mega-caps, with the outlook outside of US blue-chips being much more positive, as seen in the chart below.

The chart that proves you should stay invested in the US

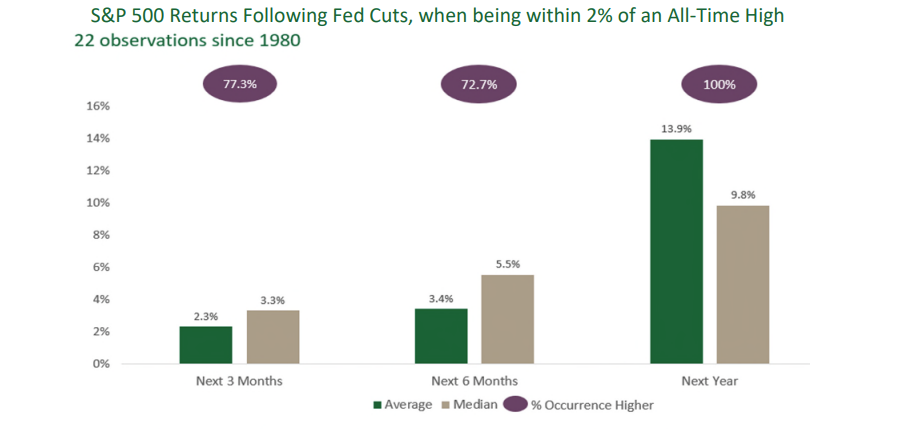

08 October 2025

The S&P 500 has always produced positive returns when rates were cut during all-time high valuations.

By Patrick Sanders

Reporter, Trustnet

Every time the Federal Reserve has cut interest rates with markets nearing an all-time high, the S&P 500 produced a positive return over the next year.

In over 40 years of market research, that has been true in 100% of cases, with the return averaging 14%, according to research by Carson Investment Research.

As the US has finally entered a rate-cutting environment, retreating would be the wrong move, according to Gerrit Smit, FE fundinfo Alpha Manager of the Stonehage Fleming Global Best Ideas fund, who said “investors should remain invested”.

So far, investors have not been following Smit’s advice. The recent Calastone Fund Flows index found £146m pulled from North American funds in the third quarter of 2025, despite the S&P 500 rallying back to form.

For Smit, however, current conditions in the US seem broadly constructive, meaning that the S&P 500 could be on course for another positive return.

Growth in the US is stronger than expected, with US GDP figures for the second quarter having recently been revised upwards, he noted. While the US is a very consumption-dependent economy, the consumer is in a “decent” position, which could contribute to further outperformance.

“It’s not that corporations and households in America are stretched. Their balance sheets are in a decent position and they could spend if they wanted to – they are just choosing not to,” the manager explained.

Additionally, significant amounts of capital expenditure are still being poured into the US economy, particularly from the artificial intelligence (AI) hyper-scalers and mega-caps.

“Total capital expenditure is already on a high base and accelerating – that’s more money going into the economy, which is clearly supportive for US equities,” Smit said.

He also argued that many investors and analysts have become “far too conservative, despite broadly supportive fundamentals”. Investors, particularly those with long time horizons, were burned by the global financial crisis, where they were too optimistic, and the market’s “appetite for disappointment” has shrunk alongside it.

However, Smit argued they are underestimating the potential for the strongest stocks in the US market to surprise on the upside and continue to deliver strong returns. He pointed to the second quarter of 2025, where many companies beat already-lofty expectations despite concerns over tariffs.

Companies are just far stronger than they used to be, he noted, with strong balance sheets, positive free cash flow and limited debt that makes comparison to the dot-com bubble not entirely accurate.

“Take a company like Microsoft or Alphabet. Despite all the capex they’re putting into AI, they still have positive free cash flow, so they don’t really need to worry about debt. That wasn’t really the case in 2001 and 2002,” the Alpha Manager said.

As a result, he has pushed the North American equity allocation within his portfolio to around 79.4%, a 15% overweight compared to the MSCI ACWI.

However, while remaining broadly constructive on US equities, he warned investors not to put all of their eggs in one basket.

Some companies just do not have the free cash flow and strong fundamentals of companies such as Alphabet, with Smit highlighting some of the cloud services businesses as having to “spend fortunes on Nvidia and Broadcom” chips to compete.

Additionally, with currencies such as the Sterling and Euro all performing well, it would pay for investors to diversify their equity exposure to avoid being trapped in one currency and take advantage of some rallying markets elsewhere, he explained.

“I haven’t got any reservations about US exceptionalism. But what I do think is true is that many investors are overinvested in the US and it may pay to start thinking about diversification,” Smit concluded.

Investors make record retreat from shares as AI crash fears rise

Story by Chris Price, Alex Singleton

Investors pulled a record amount of money from company shares in the third quarter – Jason Alden/Bloomberg

Investors pulled record amounts of cash out of equity funds during the third quarter amid concerns that an AI-fuelled boom in share prices could be poised for an abrupt halt.

Investors ran scared of “sky-high stock markets”, according to the data company’s latest Fund Flow Index.

The FTSE 100 and the S&P 500 ended last week at fresh record highs despite the turmoil caused this year by Donald Trump’s tariff campaign.

Excitement about the prospects of AI have driven markets higher, particularly in the US. On Monday, ChatGPT maker OpenAI announced a chip supply deal with AMD, sending the latter’s shares up 24pc.

Edward Glyn, head of global markets at Calastone, said it was “really unusual to see markets reaching record highs while investors are moving decisively for the exits across such a broad range of funds”.

He said: “There is a structural bias towards inflows over time as people save for their future so a prolonged period of net selling is noteworthy.”

Funds focused on the UK fared even worse, shedding £692m.

The beneficiaries were bond and money market funds, which gained £895m as investors sought out their perceived safety.

Mr Glyn added: “UK funds continue to shed capital, but selling has been more muted in the last four months in the context of a general pull-back from equities.

“Doubtless, seeing the UK market reach record levels while still not looking expensive has given some sellers pause for thought.

“But the doom loop of negative commentary on the UK economy with its dire fiscal position, soaring credit spreads, lack of growth and impending tax rises may now be winning out. Outflows are on the rise again.”

Europe defied the trend and attracted modest net buying despite the recent turmoil surrounding France’s government.

However, Sébastien Lecornu stepped down on Monday morning just 27 days after his appointment, sending the French stock market lower and its cost of borrowing higher