Every October, traders brace for turmoil. From Wall Street’s 1929 collapse to Black Monday 1987, the month has long been branded the ‘jinx’ of global markets.

Yet, modern data paints a more nuanced picture: while volatility spikes in October, it doesn’t necessarily spell disaster. Instead, the month’s dark legend reveals as much about investor psychology as it does about market mechanics.

A Legacy of Historic Crashes

The roots of October’s uneasy fame run deep. On 24 October 1929, known as Black Thursday, the US stock market began its descent into the Great Depression. Just days later, Black Tuesday saw even more dramatic losses.

Fast forward to 19 October 1987 (Black Monday), and the Dow Jones Industrial Average suffered a staggering 22.6% drop in a single day, marking the largest one-day percentage decline in history.

These events have firmly established October’s reputation as a period of financial instability. Although the underlying causes of each crash varied, ranging from speculative excess in 1929 to the rise of automated programme trading in 1987, their shared timing has contributed to a widespread perception that October poses heightened risks for equity markets.

October has long been recognised as the most volatile month for equities. According to research from LPL Financial, the S&P 500 has experienced more daily swings of 1% or greater in October than in any other month since 1950.

This heightened activity is often attributed, in part, to the timing of US midterm and presidential elections, which typically occur in early November every other year and can introduce political uncertainty into markets.

In 2025, that uncertainty is compounded by an ongoing US government shutdown, with no resolution yet in sight. The shutdown has already disrupted federal operations and delayed key economic data releases, adding a layer of opacity to investor decision-making and fuelling concerns about fiscal dysfunction.

While September historically records more negative returns on average, October’s reputation for turbulence is reinforced by its association with several major market crashes. These include the Panic of 1907, Black Tuesday, Black Thursday, and Black Monday in 1929, as well as the dramatic collapse on Black Monday in 1987.

Interestingly, the triggers for both the 1907 panic and the 1929 crash emerged in September or earlier. However, the most severe market reactions were delayed until October, further cementing the month’s reputation as a flashpoint for financial instability.

Seasonal Patterns and Investor Psychology

Behavioural finance offers one explanation for October’s reputation. Investors may be more prone to panic during this month due to its historical baggage, creating a self-fulfilling prophecy. This phenomenon is compounded by media coverage that tends to amplify fears around anniversaries of past crashes.

Yet, data from the Federal Reserve Bank of St. Louis suggests that while October is more volatile than average, it is not the worst-performing month in terms of returns. According to Visual Capitalist, which compiled S&P 500 monthly performance data from 1950 using YCharts:

・September has the lowest average return at -0.72%, making it the weakest month historically for US equities.

・October shows an average return of +0.91%, indicating modest gains despite its reputation for volatility.

・November and December have historically strong performances, averaging +1.82% and +1.49% respectively.

These figures challenge the notion that October is uniquely dangerous. While the month is indeed volatile, it does not consistently produce negative returns. It is often followed by stronger performances in November and December, implying that perception may not always align with reality.

Modern Safeguards and Market Resilience

Today’s financial markets are equipped with tools that didn’t exist in 1929 or 1987. Circuit breakers, improved risk modelling, and diversified portfolios have made markets more resilient to sudden shocks. Moreover, central banks now play a more active role in stabilising markets during periods of stress.

In 2025, investors will navigate a complex landscape marked by inflation concerns, interest rate uncertainty, and geopolitical instability. These factors contribute to volatility, but they are not confined to October. The timing of market swings often depends more on macroeconomic developments than on the calendar.

The Verdict: Myth or Reality?

So, is October truly cursed? The answer lies somewhere in between. While historical crashes have given the month a dark reputation, the data does not conclusively support the idea that October is uniquely perilous.

Volatility tends to rise, but returns are not consistently negative. Investor psychology, media narratives, and seasonal patterns all play a role in shaping perceptions.

For long-term investors, the lesson is clear: don’t let calendar myths dictate your strategy. Diversification, discipline, and a focus on fundamentals remain the best defences against short-term turbulence. October may be dramatic, but it’s rarely decisive.

3 high-dividend investment trusts to consider for passive income

Looking for ways to target a reliable and market-beating passive income? Consider these dividend-paying investment trusts.

Posted by Royston Wild

Published 3 October

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

Dividends are never, ever guaranteed. Even the most dependable dividend share can slash, postpone, or even cancel shareholder payouts when a crisis rears its head. However, investment trusts that carry a basket of equities can take the sting out of this threat.

By holding a wide selection of shares, these trusts draw income from a mix of companies, industries and regions, thus reducing the impact of dividend shocks from one or two holdings.

With this in mind, here are three top investment trusts to consider. Today, their forward dividend yields comfortably beat the FTSE 100‘s 3.3% average.

Asia focus

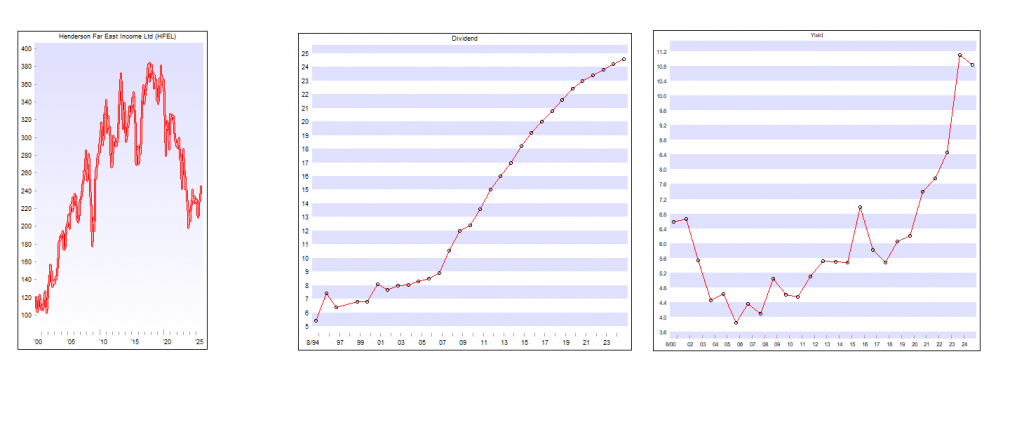

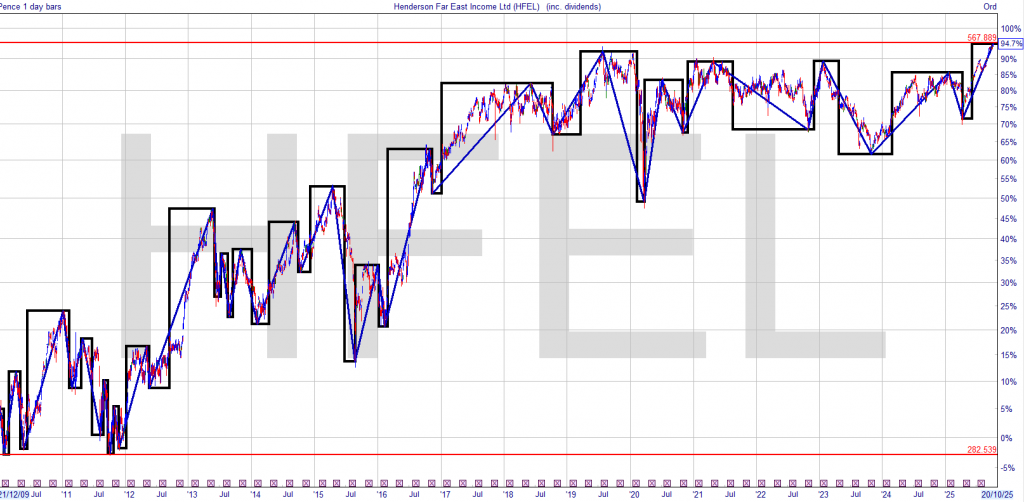

Henderson Far East Income (LSE:HFEL) seeks to capture the enormous investment potential of Asian markets. From a dividend perspective it’s a high performer, having risen annual payouts each year since 2007.

Dividends are also on the large side, and for this year its yield is an enormous 10.2%.

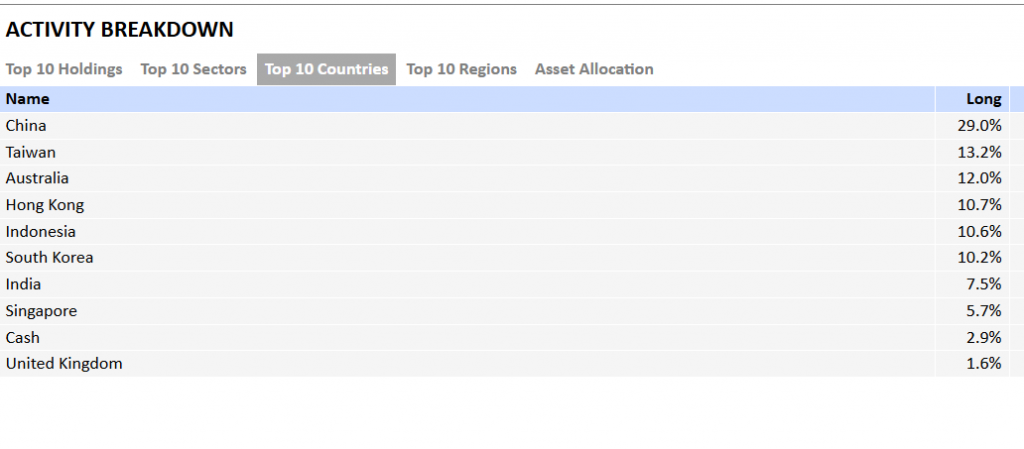

Focusing just on Asia means it carries greater regional risk than global funds. Yet this strategy also leaves it laser-focused on some of the world’s largest and fastest-growing economies like China, India and the Philippines.

In total, this Henderson Fund holds shares in 73 different companies, ranging from cyclical shares such as Taiwan Semiconductor Manufacturing and HSBC to defensive stocks including Power Grid Corporation of India. This balances the portfolio nicely and provides a more stable return across the economic cycle.

Euro star

The European Assets Trust (LSE:EAT) has a more continental flavour than Henderson Far East Income. Some 70% of its funds are wrapped up in eurozone nations, with non-euro-trading European nations accounting for almost all the rest.

Again, this narrow regional strategy carries higher risk. But that’s not all — as with those other trusts we’ve discussed, more than 90% is allocated to shares in cyclical and sensitive industries. This can leave it vulnerable during economic downturns, as illustrated by recent dividend cuts.

The good news though, is that this allocation means each of the trusts can outperform when conditions improve. In this case, major holdings include building materials supplier Heidelberg Materials and Bank of Ireland.

European Assets Trust carries a robust 5.9% dividend yield for 2025. Despite its recent problems, I think it’s worth serious consideration.

Closer to home

The Chelverton UK Dividend Trust (LSE:SDV) has raised yearly dividends reliably since the early 2010s. For 2025, it carries a Footsie-busting 8.4%.

You’ll see this is another investment trust focused on a specific region. In this case, its success is highly geared to Britain’s economy which — if many forecasters are correct — could experience prolonged growth issues. Some 92% of it is tied up in UK-listed shares, which may be a problem.

Yet Chelverton’s ability to overcome similar issues over the last decade and deliver healthy regular growth is a good omen. Since 2020, annual payouts have grown at a decent yearly rate of 6.3%.

The trust holds shares in 66 companies in total spanning multiple sectors. These are as diverse as financial services, consumer goods, energy and telecoms, providing excellent balance.

Amedeo Air Four Plus Ltd ex-dividend date AVI Japan Opportunity Trust PLC ex-dividend date BlackRock Latin American Investment Trust PLC ex-dividend date Finsbury Growth & Income Trust PLC ex-dividend date Gore Street Energy Storage Fund PLC ex-dividend date JPMorgan Asia Growth & Income PLC ex-dividend date JPMorgan Emerging Markets Investment Trust PLC ex-dividend date JPMorgan Emerging Markets Investment Trust PLC ex-dividend date Merchants Trust PLC ex-dividend date Mid Wynd International Investment Trust PLC ex-dividend date Primary Health Properties PLC ex-dividend date Ruffer Investment Co Ltd ex-dividend date US Solar Fund PLC ex-dividend date

The current value of the control share is £147,908, not too shabby. Using the 4% rule it would give you a ‘pension’ of £5,916.00.

Maybe now is not the best time to buy, as you can see from the chart you could have multi years of contributing to your ‘pension’ of zero, zilch, nothing.

Over the past few years the Group has maintained an enviable record of collecting 100% of its rent. Provided this remains the case and in the absence of any unforeseen circumstances, the Board has announced that it is targeting a dividend of no less than 5.6pps for the year ending 30 June 2026. The resetting of this dividend target, which is lower than the previous year, is entirely due to increase in financing costs of the new facilities.

The new target for AIRE is a yield of around 7.75% on current buying price, so although a cut, the share remains in the Watch List.

Brett Owens, chief strategist of the Contrarian Income Report high-yield investing service.

To make our investments give us enough dividend cash to live on without having to invest seven figures, we really need yields in the 8% to 10% range, and even higher.

And that’s exactly what today’s overlooked 11% payer allows you to do.

And the key to our opportunity here is the fact that this isn’t just your typical mutual fund or ETF — it’s a special kind of fund called a closed-end fund (CEF).

CEFs are like “regular” stocks and ETFs in that they trade openly on the public markets.

You can buy and sell them easily from almost any standard brokerage account. And CEFs hold the same assets that ETFs hold.

You can buy CEFs that hold blue chip stocks, corporate bonds, real estate investment trusts (REITs), you name it.

The difference? Dividends! Right now, for example, the average CEF yields around 8%.

So simply by “swapping out” your ETFs and individual stocks for CEFs, you could go from, say, the 1.1% average dividend the typical S&P 500 stock pays to north of 8% — a nearly sevenfold increase!

And that’s just the yield on the average CEF. Many, like this 11% payer, deliver MUCH more — massive dividends yielding 10%+ are readily available in the CEF market.

That’s EXACTLY what makes CEFs such incredible wealth generators.

And they are proven. We’ve ridden these income generators to big gains again and again in my Contrarian Income Report high-yield investing service.

Here are just a few of the returns, including dividends, we’ve posted in CEFs over the years:

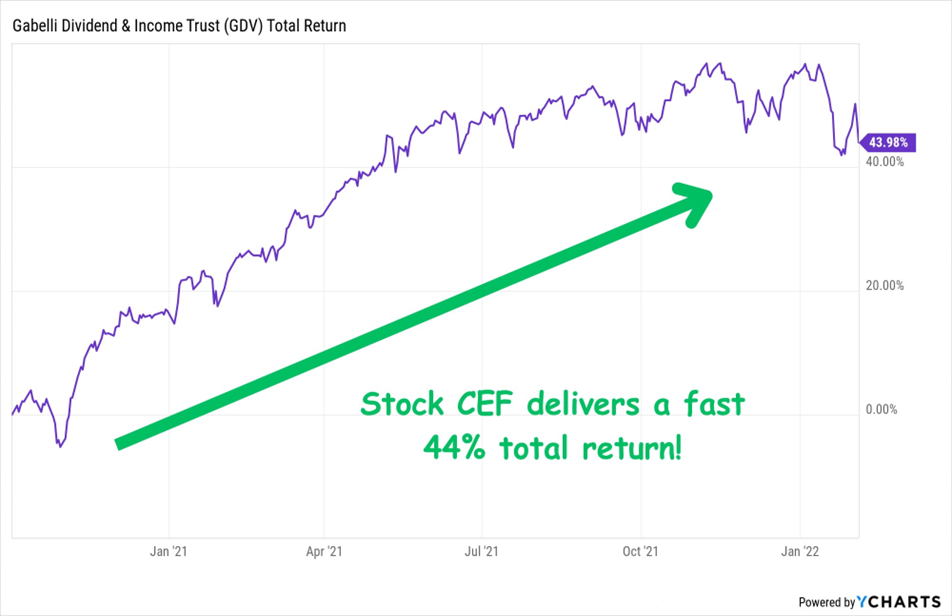

A Blue Chip Stock CEF That Returned a Sparkling 44% in 15 Months

14.6%-Paying Bond CEF Has Returned 43% in a Little Over 2 Years

A “Boring” Infrastructure CEF That Delivered a 95% Return

And talk about dividends!

That blue chip fund, the Gabelli Dividend & Income Trust (GDV), paid a healthy 7.3% when we bought.

The PIMCO Dynamic Income Fund (PDI)? An incredible 14.6% at the time.

And the utility-focused Cohen & Steers Infrastructure Fund (UTF) was throwing off an 8.8% cash stream, nearly triple what the typical utility yielded.

Do all of our calls work out like this? Of course not. I wouldn’t insult your intelligence and suggest they do. Investing involves some risk, even with top-quality funds like these, and you can lose money.

But I think you can see where I’m going here: Buying attractively valued CEFs with big dividends and savvy managers is a proven way to build wealth over time.

And the bond-buying pro running the fund we’re targeting today is, hands-down, the savviest of the bunch.

Morningstar previously named him a Fixed Income Manager of the Year, and he has been inducted into the Fixed Income Analysts Society Hall of Fame.

When he took the top job at his management company, he displaced the firm’s founder — a legend who revolutionized bond trading in the ’70s and ’80s. His long-term track record is a matter of public record.

Check out the drubbing he’s laid on the corporate-bond benchmark (orange line) through another of his firm’s CEFs since he took over as his Group CIO (knocking off that bond legend I just mentioned) a little over a decade ago (in purple):

Our Income Pro Clobbers Corporate Bonds

That’s no fluke. Here’s how one of his company’s most established mutual funds has performed since 2007, the year he became its portfolio manager:

Another Big Win for Our Bond Pro

Our manager also has a team of 4 other bond experts backing him up that, between them, boast 90+ years of experience.

So we can be sure we’re getting the cream of the crop working for us here — and that’s particularly critical in the small world of fixed income, which isn’t as “democratic” as stocks.

Well-connected managers get the first call when new issues roll out, and our top-flight manager and his team are at the top of the “to-call” list.

This, by the way, is why we always go with CEFs over ETFs for our bond picks. ETFs are simply tied to a “robotic” bond index — so there’s just no way they can compete.

Whispers of rate cuts pushed AGNC to market-beating returns; the cuts have arrived and will benefit earnings.

The benefit is cumulative over time, not instantaneous for AGNC.

Collect monthly income and enjoy as your capital climbs in value.

Looking for a portfolio of ideas like this one ?

PM Images/DigitalVision via Getty Images

Co-authored by Treading Softly

There’s a well-known Wall Street adage that says, “Buy the rumour, sell the news.”

Many investors were expecting interest rate-sensitive investments to immediately spike once interest rates were cut, if they were cut, and as such, a lot of interest rate-sensitive investments were climbing on the expectation of rate cuts to occur.

The Federal Reserve cut its target rate by 25 bps, with one dissenter who wanted to cut rates by 50 bps. Another rate cut is widely expected in October. While there is plenty of time for economic reports to change expectations, it is clear that the Federal Reserve is increasingly concerned about the labor market and believes that the risks of unemployment rising are higher than the risk of inflation.

Interestingly, after the rate cut decision, both the general market (SPX) as well as REITs (VNQ), which generally benefit from interest rate cuts, sold off. This isn’t expected to be a long-term trend, but for the market itself, it meant that there was more information given in the update from the rate cut that concerned investors than the excitement over the rate cut itself. It also followed the very well-known adage: once the rate cut was news, people were selling, trying to lock in any gains they benefited from by buying the rumor ahead of time.

Today, I want to look at an investment that we have covered previously that benefits tremendously from rate cuts. These kinds of benefits, though, don’t happen overnight. They happen over time, and we can expect those benefits to accumulate even more so as additional rate cuts occur, if they do.

Let’s dive in!

I’m Still Buying Rate-Sensitive Opportunities

Interest-rate-sensitive stocks benefit from a dovish Fed, and there are few stocks that are more interest-rate-sensitive than agency mREITs like AGNC Investment Corp. (NASDAQ:AGNC), yielding 14.4%.

AGNC primarily invests in “agency MBS”, which are mortgage-backed securities that are guaranteed by the agencies Fannie Mae or Freddie Mac. If a borrower defaults, the agency buys the mortgage back at par value. Agency MBS typically trade with a very high correlation and at a relatively tight spread over US Treasuries, because they are considered very low risk from a credit perspective.

However, since mortgages can be prepaid whenever a borrower wants, and often are prepaid through refinancing, selling the house, or making extra payments, agency MBS does diverge from US Treasuries. If you buy a 30-year Treasury Bond, you know you won’t be paid back until maturity in 30 years. If you buy a 30-year agency MBS, you can expect to get most of your money back in 5-7 years. The life expectancy of agency MBS can be projected, but it cannot be known because it is very dependent upon interest rate movements.

AGNC takes advantage of the difference by borrowing short-term using a form of lending known as repos. Repos are very low risk for the lenders because they have the right to the underlying collateral, in this case, agency MBS. Also, the contracts are typically less than 90 days, creating a very low duration risk for the lender. As a result, the lending rate on repos is typically very close to the Federal Reserve’s target rate.

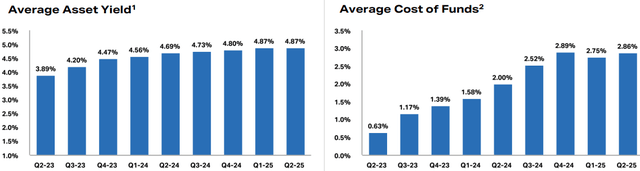

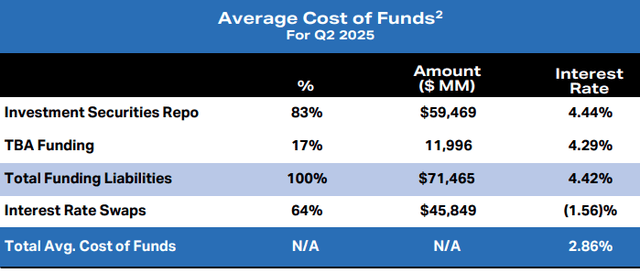

The risk is that AGNC’s assets are MBS that can be expected to remain outstanding for several years. The risk to AGNC is that its cost of borrowing can exceed the yield it receives. AGNC’s cash flow will be directly impacted by its average asset yield minus its cost of funds: Source

AGNC Q2 2025 Presentation

The Federal Reserve’s target rate was above AGNC’s average asset yield for a couple of years. Today, it is 4-4.25%, providing a comfortable cushion.

Yet if we look at AGNC’s cost of funds, we can see that it is 2.86%, which is much lower than the Fed rate. This is caused by AGNC’s hedging portfolio, specifically its interest-rate swaps. Contracts where AGNC agrees to pay a fixed interest rate and receives a floating interest rate. AGNC aggressively bought up swaps when interest rates were super low. Those swaps have been maturing, and we can see AGNC’s cost of funds drift upward.

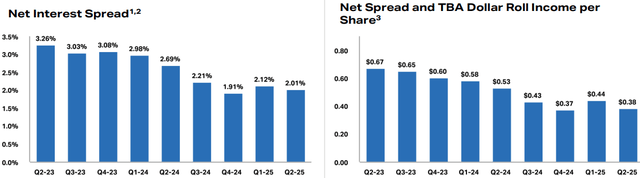

This directly caused AGNC’s spread income per share to decrease over the past two years. In this chart, we can see AGNC’s net interest spread (Average asset yield – cost of funds) and how it translated into AGNC’s per/share earnings: Source

AGNC Q2 2025 Presentation

What does the recent Fed cut mean? Let’s look at how “cost of funds” is calculated: Source

AGNC Q2 2025 Presentation

We can see that AGNC’s repo costs were 4.44%. That number can be expected to come down very close to exactly as much as the Fed’s target rate. So a 25 bps cut will result in that number coming down about 25 bps.

TBA (To Be Announced) are futures, where AGNC simultaneously buys and sells future contracts maturing in different months, with the “interest rate” being the implied financing costs of the transaction. That rate is impacted by numerous factors, including the expectation of future rate cuts.

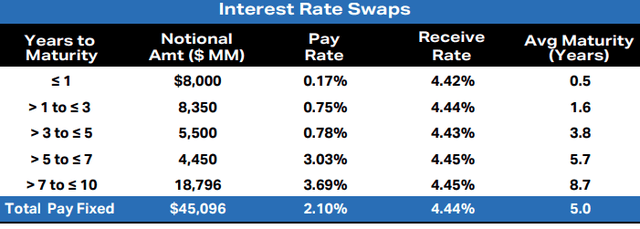

Then, the benefit of interest rate swaps is subtracted to arrive at the average cost of funds. Note that AGNC had $45.8 billion in swaps hedging $59.4 billion in borrowings.

The Fed’s 25 bps rate cut will immediately benefit the $13.6 billion in unhedged repo borrowings. 0.25% of $13.6 billion is $34 million in lower interest.

With the swapped portion, it is more complicated. AGNC has $8 billion in swaps where they are currently paying 0.17%, and those swaps are going to mature over Q3 and Q4: Source

AGNC Q2 2025 Presentation

If they don’t replace those swaps, they will be paying about 4.19% on the underlying repo after the Fed’s rate cut. That is better than 4.44%, but still a lot higher than the 0.17% they were paying. 4% interest on $8 billion is $320 million/year.

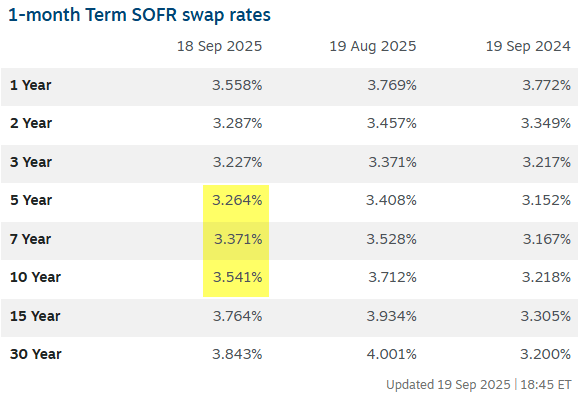

However, swap rates are also impacted by the expectation of Fed rate cuts. In the 5-10 year range, which is the sweet spot for agency mREITs, rates are currently 3.264%-3.541%. Source

Chatham Financial

Note, they were actually lower in 2024 when the market expected the Fed to be more aggressive with its rate-cutting cycle. AGNC will have the option of replacing its existing swap with a new one. If AGNC replaces the swaps, then they get a lower rate immediately than they are currently paying on their repo contracts. However, if the Fed does cut rates below 3.25-3.5%, then in the future they might be “overpaying”.

On the other hand, AGNC can just allow the swaps to expire and allow their interest expense to be unhedged. This would result in an increase to 4.19% today, but if the Fed cuts in October, it will be 25 bps lower. And their expense would be reduced directly with each cut.

This is a decision that AGNC will need to make as its swaps expire. It is important to note that through the end of 2025, the swaps expiring are going to have a larger financial impact than repo rates coming down. As calculated above, repo rates coming down will be a benefit of roughly $34 million per 25 bps in rate cuts. If we assume three rate cuts by year’s end, which is the consensus expectation, that would be roughly $100 million in savings.

On the other hand, the $8 billion in swaps that are paying only 0.17% now will be rolling off. If we assume 75 bps in repo cost reduction, they would still be paying 3.69% vs the current 0.17%, an increase of 352 bps. 3.52% of $8 billion is $281.6 million, or a $0.07/quarter headwind to earnings if AGNC goes completely unhedged. If AGNC chooses to enter into new swaps for some or all of the debt rolling off, the impact could be smaller.

So is the Fed rate cut good for AGNC’s cash flow? Yes. It does ultimately lead to AGNC paying less interest expense. However, we need to be aware that we aren’t going to see a huge spike in earnings from AGNC yet because they have these swaps maturing that have inflated earnings the past few years. That’s an approximately $0.07/quarter headwind, where each 25 bps fed rate cut is a $0.007/quarter tailwind.

AGNC has other tailwinds. For example, it can raise common equity at a premium to book value and issue preferred equity, and buy more new MBS. On a hedged basis, AGNC can easily deploy newly raised capital and generate a return on equity that is higher than its current dividend. At a high level, this works by increasing AGNC’s average asset yield, and higher revenues will also help offset the increase in interest expense as the swaps mature.

The bottom line is that declining rates are beneficial to AGNC, but we expect earnings in the near term will be relatively flat. We anticipate the tailwinds being generated by a lower Fed rate will primarily offset the maturity of the extremely favorable interest rate swaps, resulting in relatively flat earnings through the end of 2025. However, as we go into 2026 the pace of interest rate swap maturities is much slower, the swaps are already at a higher rate, and the Fed will have time to cut rates even more. As a result, the interest rate swaps that have restrained earnings growth in 2025 will be a much less relevant factor in 2026.

AGNC peers have been raising dividends, while AGNC has kept its dividends the same. This is largely because AGNC was already paying out a higher dividend relative to book value. The very attractive swaps it snagged in 2021 are a big reason why some peers had to cut dividends in 2022/2023, and AGNC didn’t. The swaps managed to last long enough to make it to an environment where AGNC can support its dividend without them.

To the extent that AGNC can continue issuing equity over book value and grow in 2026, dividend raises could be on the table within the next few years.

Conclusion

For AGNC, the benefit of declining rates or interest rate cuts is not an instantaneous proposition. Likewise, if you were to take a 3-mile run today, you would not instantly wake up with a perfectly sculpted body tomorrow. No, the benefit is cumulative over time. The more you run, the more the benefit. The longer you run, the greater the benefit. Likewise, for AGNC, as rates remain lower than before and continue to decline, the benefits will accumulate over time.

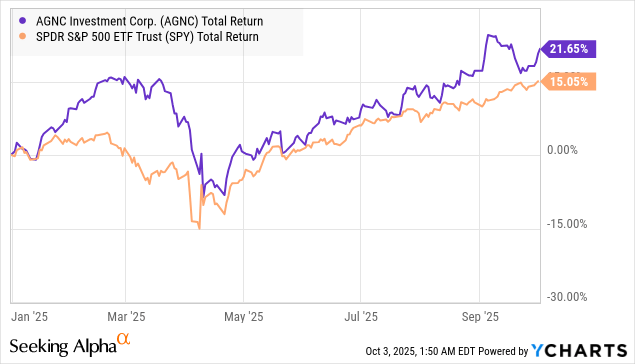

For traders who buy the rumor and sell the news, AGNC is going to move quickly into the category of no longer meeting any of their interests. This year, AGNC has strongly outperformed the market on the expectation of interest rate cuts, not that they’re here, we’re seeing traders exit their positions, bringing current returns closer to that of the overall market – traders locking in short-term gains:

For income investors who position their portfolio to benefit regardless of what interest rates are doing, AGNC continues to be a highly attractive opportunity to collect double-digit yields paid out monthly from ultra-safe investments in agency MBS. AGNC itself does add risk by adding in leverage to the scenario and so it does not carry the same ultra-low risk rating that Agency MBS would on its own. However, it is well-positioned to continue to benefit from additional interest rate cuts, as well as benefit from the newer, lower rate that we’ve just seen.

When it comes to retirement, collecting wonderful income that pours in from the market to your coffers is a great idea. Rarely does anything in life come for free, and with every time you put money to work, there’s going to be some risk that is tied to it. Even leaving money in a bank account has risk. Risk that the bank may collapse, risk that the government won’t honor its FDIC insurance, and the loss of value over time due to the eroding effects of inflation. Hiding your money under a mattress also comes with a risk of theft. If that cash is stolen, you can kiss it goodbye, and inflation still negatively impacts it there. By putting your money to work in the market, you can help balance that risk with reward by having your money earn more and be able to achieve the retirement that you’re dreaming of. Don’t let your finances be what stops you from having the retirement that you’ve always dreamed of. That’s where the unique Income Method within High Dividend Opportunities can massively benefit you by helping you unlock the potential of your nest egg.

That’s the beauty of my Income Method. That’s the beauty of income investing.

A Legit 13.7% Dividend with Unstoppable “Mob-Boss” Economics

SPONSORED AREA

Brett Owens, Chief Investment Strategist Updated: October 1, 2025

In most US industries, banks help businesses finance their buildings. The lenders also provide working lines of capital for the operations to grow.

Cannabis is different. It is tricky for operators to find money due to federal roadblocks.

At the national level, cannabis is still illegal. However, 40 states have legalized the drug in some fashion. Uncle Sam mostly looks the other way and lets states regulate their own markets—except when it comes to banking and taxes.

Banks cannot lend to cannabis operators. So, good luck financing that building.

Also, there is a tax code relic of the 1980s war on drugs (“Just Say No!”) called IRC Section 280E. It blocks cannabis operators from deducting ordinary business expenses. Which means their profits are artificially low and access to credit is denied due to poor-looking books and federal laws.

But if you live in a state where cannabis has been legalized, you know there is plenty of money flowing. Obviously, there is no shortage of demand to fund the countless dispensaries that have popped up in recent years. Where do these weed businesses find the money?

The answer is Innovative Industrial Properties (IIPR), which acts as the first landlord and primary lender of choice for cannabis operators. IIPR is the capital lifeline for the industry. And it’s a dividend cash cow that yields 13.7%!

IIPR buys dispensary facilities from the operators who are often short on cash and remember, could not finance their buildings. In the transaction, IIPR hands them a chunk of cash they badly need. Then it leases the facility back to the operator for 15 to 20 years.

The operators receive money upfront. IIPR collects long-term rent checks. And shareholders snag a fat dividend.

Because traditional banks won’t touch the space, IIPR negotiates incredibly favorable leases. They have long durations, built-in rent escalators and guarantees from the large corporate multi-state operator-lessees.

IIPR is essentially a “Godfather landlord” in a restricted industry. Cannabis peddlers need cash and have nobody else to turn to. So, they take the deal.

These rents fund a dividend that has grown steadily since the company’s IPO in 2016. The first quarterly payout was $0.15 per share. Cannabis stocks have been volatile but IIPR’s payout has been a steady staircase higher to $1.90 per share, a 12-fold increase:

IIPR’s Blazing Dividend History

IIPR’s balance sheet is clean and its leverage is low. It is a reputable publicly traded company with “mob-boss” economics. IIPR has “Prohibition pricing power!”

Why doesn’t this company command more per share (and pay less?). The stock is unloved today because it was too loved before. IIPR delivered dynamite 1,620% returns from 2016 to 2021, climaxing in a bubbly valuation. Investors paid sky-high multiples—30X to 40X funds from operations (FFO)—for a REIT yielding 2%.

Then the air came out. The stock deflated 75% from its peak. Analysts fled and downgraded. Today only one analyst rates IIPR a Buy. (By comparison, more than 400 of the S&P 500 have a Buy label. Those analysts are certainly a cheery lot!)

Which is perfect for us careful contrarians. We have a hated stock with plenty of cash flow.

Today, IIPR trades for just eight-times FFO. This is quite cheap for a solid REIT. Thanks to its 13.7% dividend, a $50,000 position in IIPR pays almost $7,000 per year in cash income.

Dividend coverage is fine. The $230 million FFO haul keeps the payout flowing. More importantly, the stock looks frisky again to the upside. IIPR carved a bottom in the spring and, two months ago, bulls rejected another selloff attempt. Momentum is shifting.

Plus, IRC Section 280E is likely to be softened or removed in the coming years. Cannabis legalization has momentum at the state level. The federal restriction is a relic that, when repealed, will unlock tax relief and improve operator coverage ratios right away.

IIPR longs may not have to wait that long. The stock may pop on the next upgrade, with seven analysts as current holdouts. The bar is low and the yield stays sky high while we wait.

Deals like IIPR exist because Wall Street suits and mainstream financial advisors are unimaginative. Their jobs depend on herdlike mediocrity. So, they will lazily tell you that IIPR is risky—without doing any research about its leases, tenants or current cash flows!

This 7.6% Dividend’s New “Rights Offering” Lets Us Buy Cheap (for Now)

Brett Owens, Chief Investment Strategist Updated: September 30, 2025

We contrarians live for the “one-off” shots at extra income (or gains!) our favorite dividend plays throw our way.

One of these “special situations” just landed in our lap: A shot at buying a megatrend-powered 7.6% dividend that’s rarely cheap. And we’re picking it up for a song.

It’s a long-time holding of our Contrarian Income Report advisory, and it’s sitting right in the tracks of the surging AI buildout. In fact, it may be the last “cheap” AI play on the board! This one’s dropped from trading for more than its portfolio is worth to a lot less.

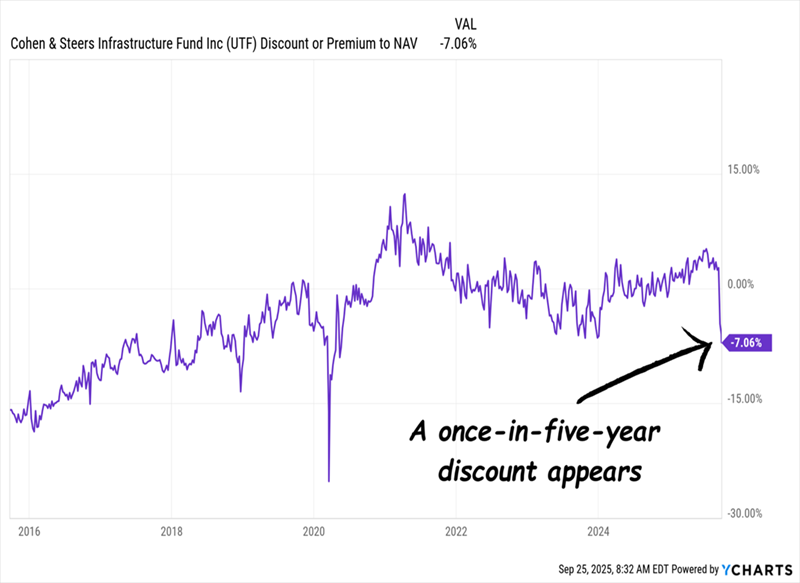

A 7.6% Dividend Bargain We Haven’t Seen Since 2020

As you can see, this fund dropped from trading 6% above its net asset value (NAV, or the per-share value of its portfolio) to 7.1% below, as of this writing.

It’s a huge drop, and it stands out because, as you can see above, this fund, the 7.6%-yielding Cohen & Steers Infrastructure Fund (UTF), is rarely cheap for long.

Rock-Solid 7.6% Dividends Rarely Get This Cheap, This Fast

UTF’s latest tour in our Contrarian Income Report portfolio started in November 2020, and this reliable utility fund has been humming away since, handing us a 7.8% yield on our original buy, plus a monthly payout that’s rolled in like clockwork.

That’s exactly what we bought it to do. And it’s handed us a 41% total return in that time, too. And now we have a shot at buying it cheaper than we did five years ago!

Let me put all of this in dollars and cents for you.

In the past year, UTF’s average premium has been 1.8%. If the discount reverts to that level, price upside of around 10% is on the table here. And that’s before we factor in the growth of its portfolio. Let’s talk about that now.

From Falling Rates to “Back Door” AI Gains

We bought UTF in late 2020 because its utility-stock holdings—including big players like NextEra Energy (NEE), Duke Energy (DUK) and Southern Co. (CO)—are essentially “bond proxies.”

When rates fall, as they did then, utilities rise. Nowadays, we have a similar setup. As we discussed in last week’s article on some of our favorite gold dividends, long rates are essentially capped, and short-term rates (controlled by the Fed) are falling.

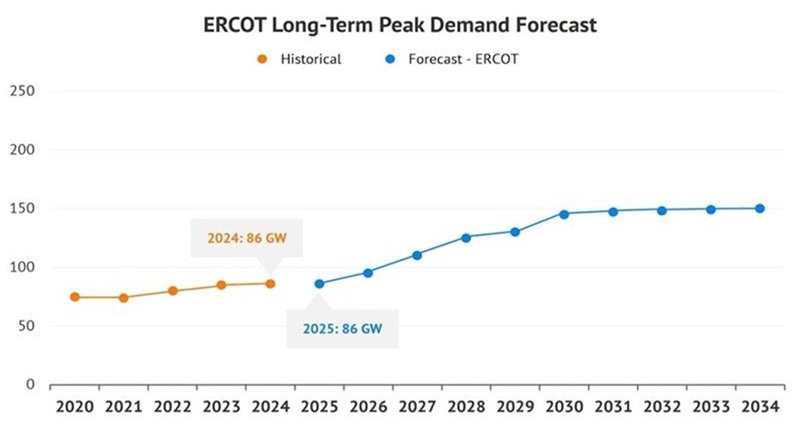

Plus we have another, far bigger driver: AI’s limitless power demand.

Let’s take Texas, ground zero for the AI power boom. Microsoft (MSFT), Alphabet (GOOGL), Amazon.com (AMZN) and Meta Platforms (META) have built data centers there. According to the Electric Reliability Council of Texas (ERCOT), Texas alone expects a 62% surge in power demand by 2030 as these data centers multiply.

That’s just one state, utilities nationwide are racing to add capacity.

The Deal on the Discount

To be sure, this AI-utility trade is far from a secret, so why the discount on UTF?

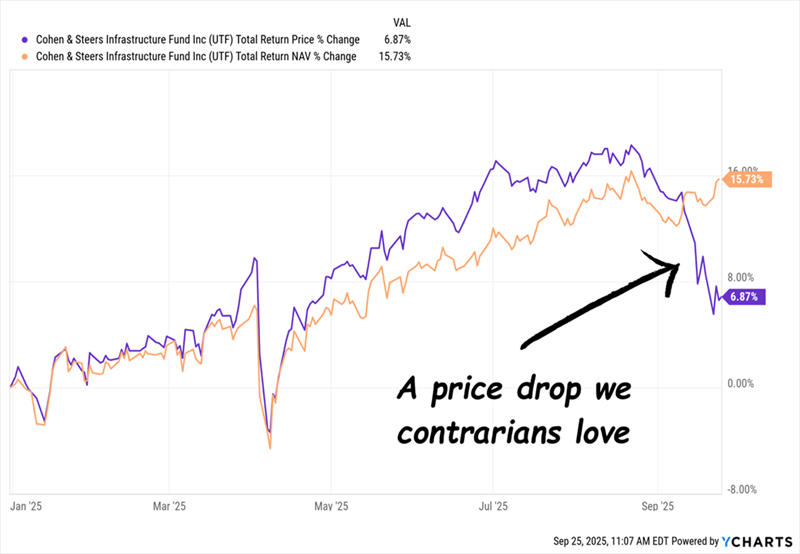

Look at the chart below. In orange, we have UTF’s total NAV return (again, the value of its underlying portfolio) for 2025. In purple we see its total return based on market price (or what investors are paying for the fund itself on the open market).

A Contrarian-Friendly Setup: NAV Climbs, Price Sags

As you can see, the total NAV return has continued its climb. The market-price return, meantime, has dropped, carving out that 7.1% “discount gap.”

This is the kind of sign we contrarians love because it shows that this discount is not because management blew a stock selection (or many). It’s all about investor sentiment. And we’re happy to take the other side of the bet when investors turn bearish on a solid fund like this one.

Why the sour mood? UTF’s management firm, Cohen & Steers, is doing something CEF managers rarely do: conducting a “transferable rights offering” on the fund.

Under this setup, if you held shares of UTF as of the “record date”—September 22—you get one “right” to buy new shares at a discount: Every five rights lets you buy one new UTF share.

Here’s how that will work: When the offer expires on October 16, the price of the new shares will be set at 95% of the stock’s average closing price on that date and the four trading days leading up to it. If the fund’s average price is below 90% of its NAV—again, the per-share value of its underlying portfolio—the price will be set at 90% of NAV.

That “floor” helps limit the offer’s downside pressure on the shares.

If you owned UTF as of September 22, you’ll be able to exercise your rights and even more, if there are leftover shares other investors don’t pick up. If you don’t want to get in on the action here, that’s fine—you can sell your rights—hence the “transferable” in the name. All of the details of the rights offering are on C&S’s website.

All of this, in a nutshell, is why UTF has dropped to a discount.. But how do I know this is a buying opportunity?

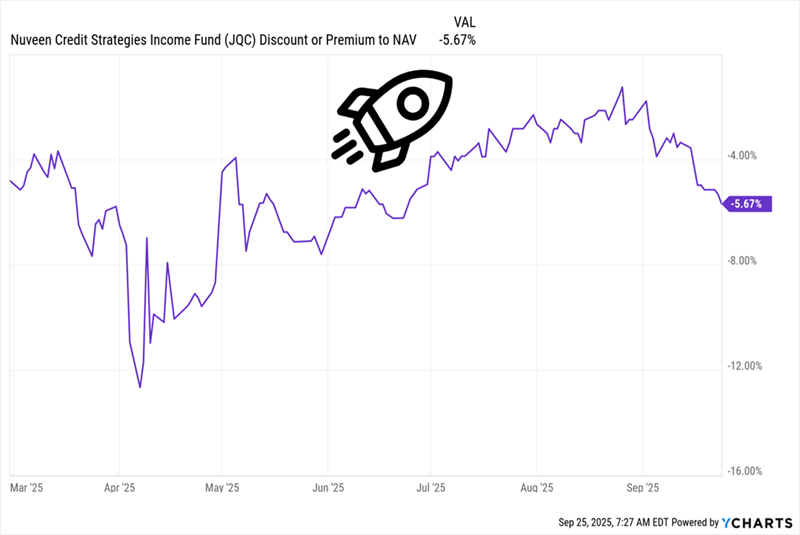

Let’s look at history. I did say earlier that rights offerings were rare for CEFs, but on March 19, Nuveen announced a similar deal on its Nuveen Credit Strategies Income Fund (JQC).

JQC’s Rights Offering Sets the Bar for UTF

JQS’s discount deepened on the offer’s announcement, then ground back toward its norm when the expiry date rolled around. I expect the same with UTF’s AI tailwind, capped interest rates and management’s ability to sniff out winning infrastructure plays. And thanks to the rights offering, they’ll have even more cash to work with.

If you own UTF, this is your chance to buy more at a bargain. If not, you still get to buy a rarely cheap fund for 93 cents on the dollar—and ride its closing “discount gap” higher.

Start With UTF’s Rare Discount, Then Buy These Cheap 9% Monthly Payers

Special situations like this put us “over the top” when it comes to retirement, putting a pop in our portfolios (and income streams) that regular investors can only dream of.

That’s right: Most people never see these opportunities. Stuck in mainstream stocks, they settle for meger payouts and sky-high valuations.