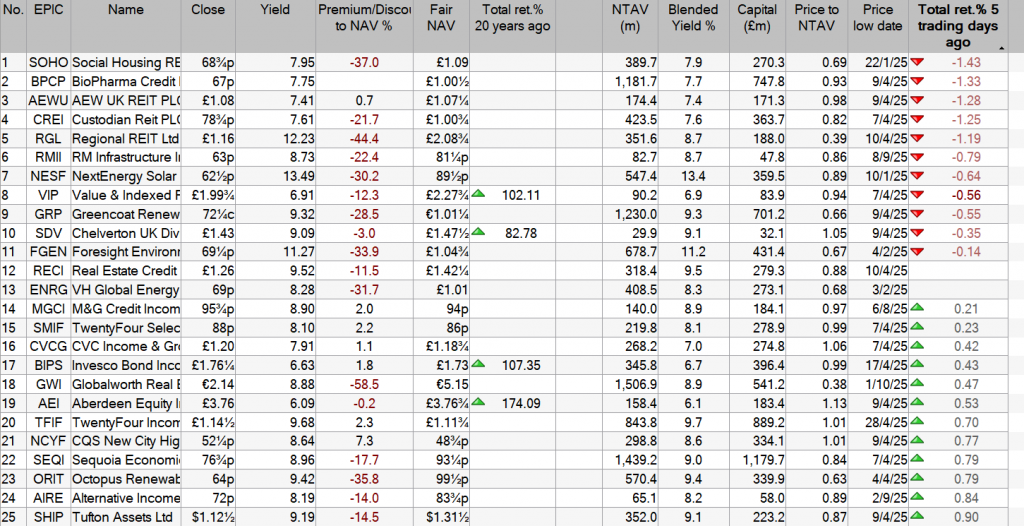

This 7.6% Dividend’s New “Rights Offering” Lets Us Buy Cheap (for Now)

Brett Owens, Chief Investment Strategist

Updated: September 30, 2025

We contrarians live for the “one-off” shots at extra income (or gains!) our favorite dividend plays throw our way.

One of these “special situations” just landed in our lap: A shot at buying a megatrend-powered 7.6% dividend that’s rarely cheap. And we’re picking it up for a song.

It’s a long-time holding of our Contrarian Income Report advisory, and it’s sitting right in the tracks of the surging AI buildout. In fact, it may be the last “cheap” AI play on the board! This one’s dropped from trading for more than its portfolio is worth to a lot less.

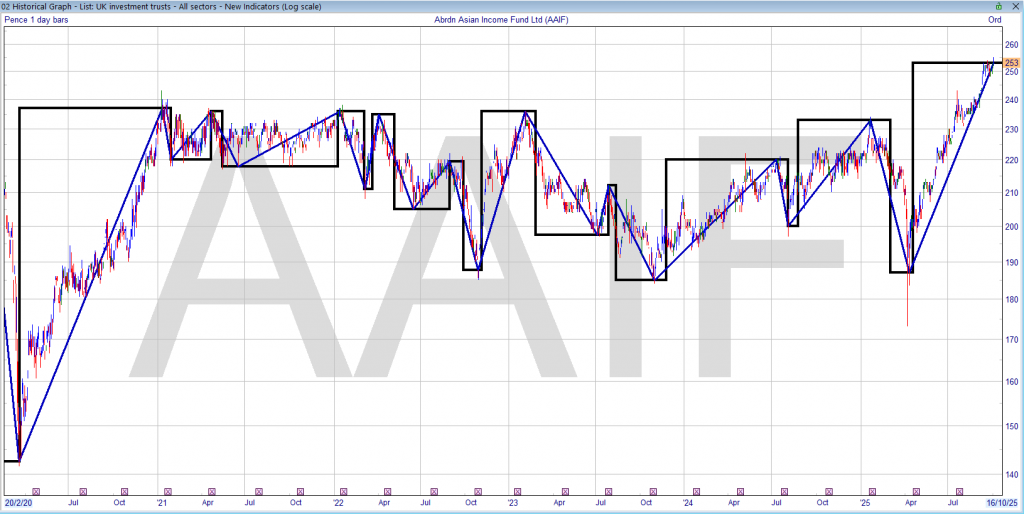

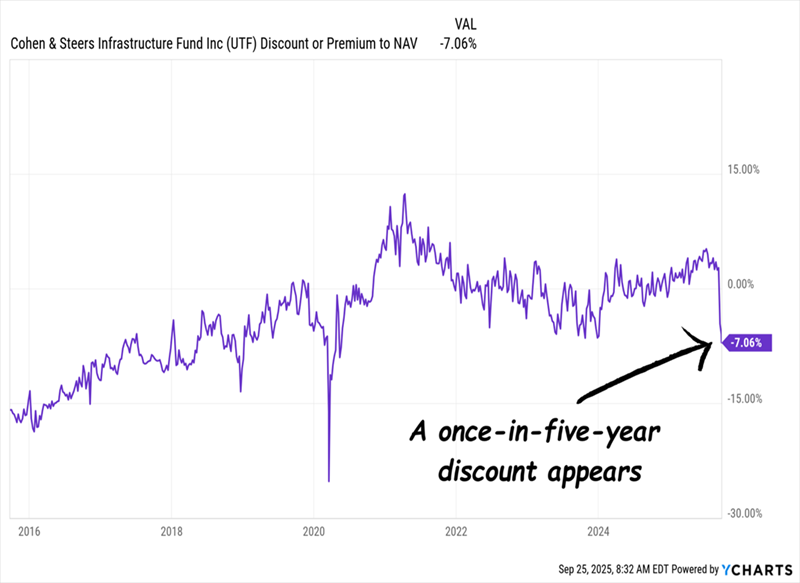

A 7.6% Dividend Bargain We Haven’t Seen Since 2020

As you can see, this fund dropped from trading 6% above its net asset value (NAV, or the per-share value of its portfolio) to 7.1% below, as of this writing.

It’s a huge drop, and it stands out because, as you can see above, this fund, the 7.6%-yielding Cohen & Steers Infrastructure Fund (UTF), is rarely cheap for long.

Rock-Solid 7.6% Dividends Rarely Get This Cheap, This Fast

UTF’s latest tour in our Contrarian Income Report portfolio started in November 2020, and this reliable utility fund has been humming away since, handing us a 7.8% yield on our original buy, plus a monthly payout that’s rolled in like clockwork.

Source: Income Calendar

That’s exactly what we bought it to do. And it’s handed us a 41% total return in that time, too. And now we have a shot at buying it cheaper than we did five years ago!

Let me put all of this in dollars and cents for you.

In the past year, UTF’s average premium has been 1.8%. If the discount reverts to that level, price upside of around 10% is on the table here. And that’s before we factor in the growth of its portfolio. Let’s talk about that now.

From Falling Rates to “Back Door” AI Gains

We bought UTF in late 2020 because its utility-stock holdings—including big players like NextEra Energy (NEE), Duke Energy (DUK) and Southern Co. (CO)—are essentially “bond proxies.”

When rates fall, as they did then, utilities rise. Nowadays, we have a similar setup. As we discussed in last week’s article on some of our favorite gold dividends, long rates are essentially capped, and short-term rates (controlled by the Fed) are falling.

Plus we have another, far bigger driver: AI’s limitless power demand.

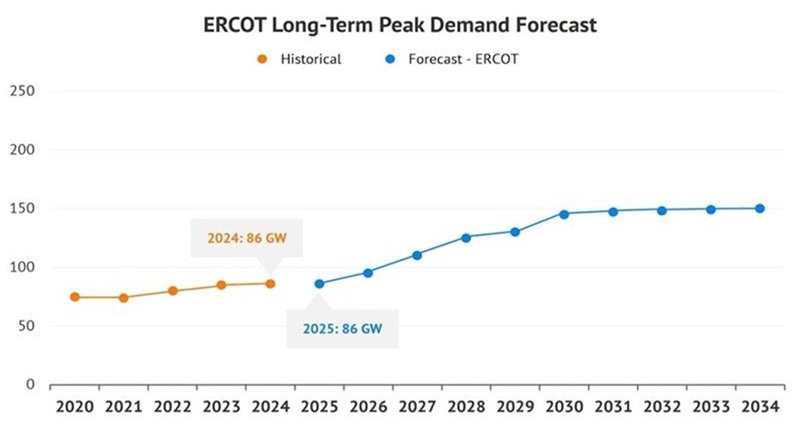

Let’s take Texas, ground zero for the AI power boom. Microsoft (MSFT), Alphabet (GOOGL), Amazon.com (AMZN) and Meta Platforms (META) have built data centers there. According to the Electric Reliability Council of Texas (ERCOT), Texas alone expects a 62% surge in power demand by 2030 as these data centers multiply.

That’s just one state, utilities nationwide are racing to add capacity.

The Deal on the Discount

To be sure, this AI-utility trade is far from a secret, so why the discount on UTF?

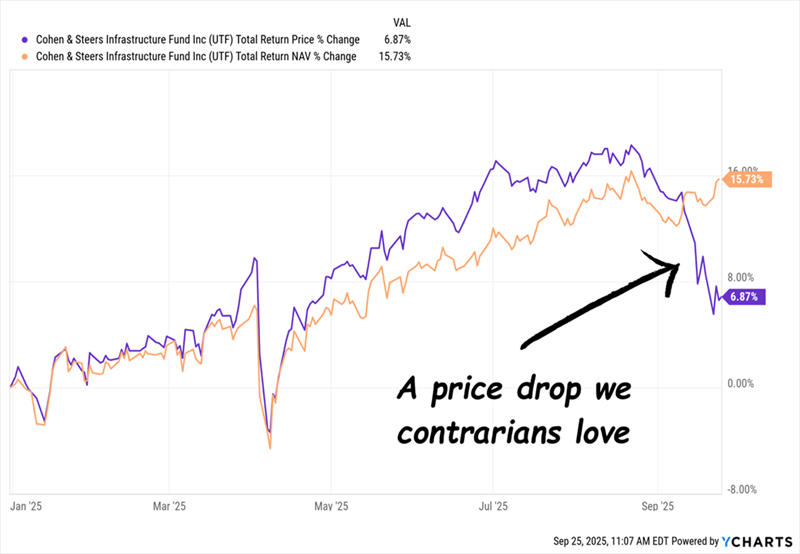

Look at the chart below. In orange, we have UTF’s total NAV return (again, the value of its underlying portfolio) for 2025. In purple we see its total return based on market price (or what investors are paying for the fund itself on the open market).

A Contrarian-Friendly Setup: NAV Climbs, Price Sags

As you can see, the total NAV return has continued its climb. The market-price return, meantime, has dropped, carving out that 7.1% “discount gap.”

This is the kind of sign we contrarians love because it shows that this discount is not because management blew a stock selection (or many). It’s all about investor sentiment. And we’re happy to take the other side of the bet when investors turn bearish on a solid fund like this one.

Why the sour mood? UTF’s management firm, Cohen & Steers, is doing something CEF managers rarely do: conducting a “transferable rights offering” on the fund.

Under this setup, if you held shares of UTF as of the “record date”—September 22—you get one “right” to buy new shares at a discount: Every five rights lets you buy one new UTF share.

Here’s how that will work: When the offer expires on October 16, the price of the new shares will be set at 95% of the stock’s average closing price on that date and the four trading days leading up to it. If the fund’s average price is below 90% of its NAV—again, the per-share value of its underlying portfolio—the price will be set at 90% of NAV.

That “floor” helps limit the offer’s downside pressure on the shares.

If you owned UTF as of September 22, you’ll be able to exercise your rights and even more, if there are leftover shares other investors don’t pick up. If you don’t want to get in on the action here, that’s fine—you can sell your rights—hence the “transferable” in the name. All of the details of the rights offering are on C&S’s website.

All of this, in a nutshell, is why UTF has dropped to a discount.. But how do I know this is a buying opportunity?

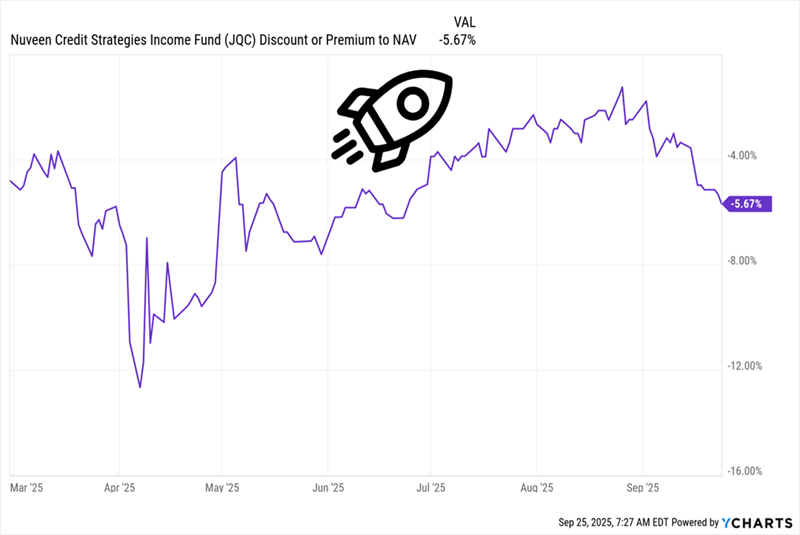

Let’s look at history. I did say earlier that rights offerings were rare for CEFs, but on March 19, Nuveen announced a similar deal on its Nuveen Credit Strategies Income Fund (JQC).

JQC’s Rights Offering Sets the Bar for UTF

JQS’s discount deepened on the offer’s announcement, then ground back toward its norm when the expiry date rolled around. I expect the same with UTF’s AI tailwind, capped interest rates and management’s ability to sniff out winning infrastructure plays. And thanks to the rights offering, they’ll have even more cash to work with.

If you own UTF, this is your chance to buy more at a bargain. If not, you still get to buy a rarely cheap fund for 93 cents on the dollar—and ride its closing “discount gap” higher.

Start With UTF’s Rare Discount, Then Buy These Cheap 9% Monthly Payers

Special situations like this put us “over the top” when it comes to retirement, putting a pop in our portfolios (and income streams) that regular investors can only dream of.

That’s right: Most people never see these opportunities. Stuck in mainstream stocks, they settle for meger payouts and sky-high valuations.