Can dividend hero trusts survive the shift to buybacks?

By Dave Baxter

Investors’ Chronicle

Once criticised as a ‘Jurassic Park’ of stock exchanges due to its obsession with dividends, the UK market has changed tack recently. UK-listed companies are boosting returns via an enormous volume of share buybacks, sometimes at the expense of dividends.

This has already had a big effect on how UK equity income trusts operate. Temple Bar (TMPL) addressed this “distributional shift” earlier in the year by changing its dividend policy and increasing its payout using capital reserves. Dunedin Income Growth (DIG) has just followed suit, announcing a dividend increase and saying it would draw on both capital and income reserves to “provide greater investment flexibility”.

With the buyback rush showing no sign of slowing down, there’s reason to suspect we might see more UK income trusts start doing this.

This switch might prove easier for some than others. But certain trusts will be feeling the pressure – for instance those with a long record of increasing their dividends.

The DIG board, for example, referenced its presence in the AIC’s “next generation of dividend heroes” list (trusts with between a decade and 20 years of dividend growth) when announcing its policy change. Plenty of UK income trusts sit in such lists, including the original dividend heroes cohort of those that have upped payouts for 20 consecutive years or more.

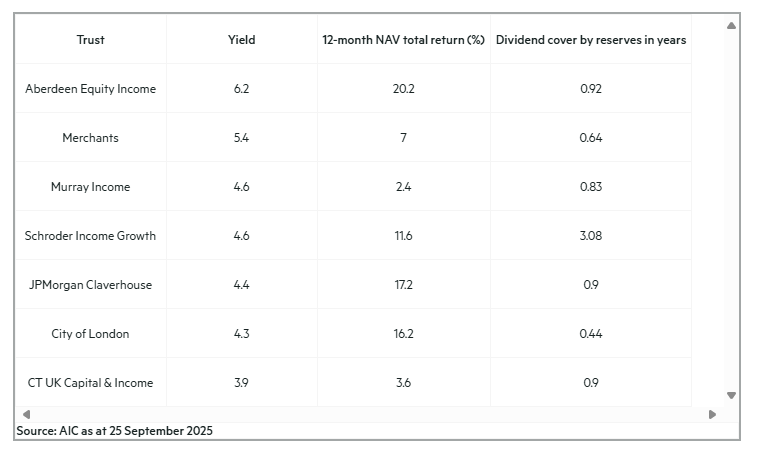

Among these, City of London (CTY) has increased its dividend for 59 consecutive years, with JPMorgan Claverhouse (JCH) and Murray Income (MUT) on 52 years. This list also includes Merchants (MRCH), CT UK Capital & Income (CTUK), Schroder Income Growth (SCF) and Aberdeen Equity Income (AEI).

With buybacks boosting returns, it should theoretically be easy for a trust to use those gains to make up for any lost dividends. Good underlying total returns and a decent level of revenue reserves, where present, will also help trusts switch policies in this way. Conversely, a fund that already has a high dividend might find this harder to sustain or increase.

The data shows a mixed picture on this front. Aberdeen Equity Income, City of London and JPMorgan Claverhouse have enjoyed especially strong net asset value returns over a 12-month period.

That could offset certain challenges, from the Aberdeen fund’s relatively high share price dividend yield of 6.2 per cent to the fact that City of London has limited dividend cover from its revenue reserves. According to AIC data, these would cover less than half a year of its current dividend payouts.

The challenges might be greater still for Murray Income and CT UK Capital & Income, which have some revenue reserves but have struggled in terms of performance, at least recently.

The issue is that trusts that perform badly could find themselves compounding this by selling assets to fund a dividend payment. Meanwhile, running down reserves might leave funds stretched in a crisis that sees companies pause their payouts, as happened in 2020.

If income streams remain less abundant than they once did, shifting to a capital and income payout policy could make trusts look more attractive than open-ended income funds, which simply pay out the dividends they receive. The latter might thus pay out less in future.

But trusts do need to weigh up the costs, and risks, of such a shift.

Supermarket Income REIT plc (LSE: SUPR) has today declared an interim dividend in respect of the period from 1 July 2025 to 30 September 2025 of 1.545 pence per ordinary share (the “First Quarterly Dividend”).

The First Quarterly Dividend will be paid on or around 21 November 2025 as a Property Income Distribution (“PID”) in respect of the Company’s tax-exempt property rental business to shareholders on the register as at 24 October 2025. The ex-dividend date will be 23 October 2025.

Please note that there is no scrip dividend alternative available for the First Quarterly Dividend and it will be paid in full as cash. The Board will keep under consideration the offer of a scrip dividend alternative in respect of future quarterly dividends.

Some passive income ideas really are simple. Here’s one!

Story by Christopher Ruane

While the theory of passive income is straightforward, in practice some ideas sound complicated to

Why I like this idea

When it comes to passive income, I like this idea for a few reasons.

I can match it to my own available funds, even if I have a fairly small amount of money to invest.

I am investing in proven businesses, not unproven concepts. On top of that, a large established company can do things that are simply out of my capability if I tried to do them myself.

Instead of struggling to set up an online business selling t-shirts, I could simply buy into a giant like Amazon or JD Sports that can achieve economies of scale I never would on my own.

Putting the idea into practice

So, for example, although JD Sports does pay a dividend, its current yield is 0.9%. That means that for every £100 I invest today, I will hopefully earn 90p a year in passive income.

By contrast, the dividend yield of FTSE 100 asset manager M&G (LSE:MNG) is over 10 times higher at 9.9%.

When hunting for passive income ideas in the stock market, I start by looking for great businesses with attractive share prices. I then look at yield.

Bear in mind that no company’s dividend is guaranteed to last. For example, M&G saw more policyholders pull money out of its main business than they put in during the first half of this year. If that trend continues (for example, because M&G’s asset managers underperform compared to rivals), it could lead to lower earnings and ultimately perhaps a dividend cut.

Looking for potentially lucrative dividend shares to buy

Still, while I see the risk, I continue to own M&G shares and earn dividends from them.

I like the fact it operates in a market where the customer demand is simply massive and is likely to remain that way over the long run. While that attracts strong competition, M&G benefits from its well-known brand, an existing customer base in the millions, and a proven ability to generate sizeable free cash flows.

Weighing such positive attributes against risks, then considering the value offered by the share price (and finally the current dividend yield) is the approach I take when looking for passive income ideas in the stock market.

Setting up a second income not just for next year, or even the next decade, but the rest of my life appeals to me.

Such dividends are never guaranteed, but by diversifying a portfolio across a number of different shares, hopefully there will always be some income even if individual shares reduce or cancel their payouts along the way.

To put that into perspective by the way, FTSE 100investment trustScottish Mortgage last cut its dividend per share almost a century ago, after the famous 1929 Wall Street crash !

With a spare £10 a week, here is the approach I take to building such passive income streams.

What to look for when buying dividend shares

I think it is too easy – and potentially unhelpful – to complicate things when it comes to the stock market. So like billionaire investor Warren Buffett, I tend to think of a share as a small stake in a company.

I would not invest in a company I do not understand. Nor would I buy into one unless I felt upbeat about its long-term prospects – and felt the price I was paying represented good value for what I was getting.

Gilt Investment for Beginners: The Ideal Low-Risk Choice

Story by Money Marshmallow

Introduction

Gilts are bonds issued by the UK government. In recent years, they have become increasingly attractive to individual investors due to increasing interest rates and tax efficiency.

What are gilts?

Gilts are a type of government bond. When you buy a gilt, you effectively lend money to the UK government in exchange for periodic interest payments (coupons) and the return of your initial investment (the principal) when the bond matures.

UK government bonds are known as ‘gilts’ because their past paper certificates had gilded (golden) edges. The name also reflects their security and reliability, as the UK Government has never failed to make repayments.

Key features of gilts:

Issued by the UK government – Issued by the UK government, gilts are generally considered safe investments. The UK government has solid investment grade credit ratings of Aa3, AA-, and AA from Moody’s, Fitch, and S&P respectively.

Fixed interest payments – gilts pay a fixed rate of interest that is set at the inception of the bonds. These payments are known as ‘coupons’. The interest payments are typically made every 6 months.

Different maturities – Maturity is the time when the bond has come to the end of its life and the investor receives their money back. This ranges from a few years to several decades.

Traded in the market – meaning their prices can go up or down.

Return of principal at maturity – the issuer (HM Treasury) issues gilts with a promise to return your capital at maturity.

Low risk: Since they are issued by the UK government, gilts are considered very safe.

Tax benefits: Capital gains from gilts are not taxed, making them attractive for investors.

Predictable returns: You know how much you will receive at maturity, and can see a schedule of period interest (coupon) payments.

Liquidity: Gilts can be easily bought and sold in the market.

Cons:

Low returns: Compared to stocks or corporate bonds, gilts usually offer lower potential profits.

Interest rate risk: Buying a gilt at a 3.75% yield may seem attractive now, however, if interest rates were to rise you would be locked into a lower rate. This causes investors to sell legacy gilts with lower rates and can lead to their prices falling.

Inflation risk: Like all investments, inflation will eat away at the real value of returns. For example, if a gilt is yielding 4%, and inflation is 2%, the real return is 2%.

Why is now a good time to buy gilts?

In the past, gilt yields were very low, as central banks lowered interest rates to try and stimulate borrowing after the 2008 financial crisis, and then again during the COVID-19 pandemic. However, recent years have seen central banks attempting to combat inflation by increasing interest rates, causing yields to rise and the prices of older gilts issued with low coupons fall.

This presents an opportunity for individual investors to buy them at a discount, and benefit from their tax-free capital gains when they mature.

For example, take a gilt maturing in 2026 with a low coupon of 0.125%:

It is currently trading at a discount (<100).

The taxable income component of its return (0.125%) is negligible.

When it matures, the price will return to its full value (100), giving you a capital gain.

Since this gain is considered capital rather than income, the bulk of the yield is tax-free, making it very tax-efficient.

This tax advantage makes low coupon gilts an efficient way to earn returns, especially for higher-rate taxpayers.

Comparing gilts to other investments

Gilts vs. Corporate Bonds: Corporate bonds often offer higher yields, but they come with more risk as companies can default. Generally speaking, corporate bonds will have higher coupons, as such they are more commonly held within ISA wrappers.

Gilts vs. Stocks: Stocks are more volatile than gilts, and provide less capital protection. However, they have higher expected returns, which minimises the risk of not receiving a required return target. Stock market index trackers can be a solid choice for investors looking to maximise long-run returns, especially if held within an ISA wrapper.

Gilts vs. Cash Savings: Cash savings provide the greatest protection of capital (providing for the FSCS limit). Further, flex savings accounts can be accessed on demand without needing to sell a bond at the prevailing market price. However, cash savings are income products (taxed at your income tax rate), making the rates available less competitive if held outside a tax wrapper.

Who should invest in gilts?

Gilts may be suitable for you if:

You want a safe and predictable investment.

You are looking for tax-efficient ways to invest, especially outside of a tax wrapper such as an ISA

You need to preserve capital.

You prefer stability over risk.

You are looking for a hedge against stock market volatility.

How to invest in gilts

You can buy gilts through a broker, most investment platforms will offer gilts. You can also gain exposure to gilts through pooled products such as ETFs, however, pooled products will not be subject to the same tax treatment (free of capital gains tax).

Steps to buying gilts:

Determine your investment objectives – Why are you investing? Will you need your money back in a year, or a few years? How much will you need to earn to meet your objective? Your investment objectives will help you narrow down a suitable range of gilts.

Choose a platform – Open an account with an investment platform or broker. For example, WiseAlpha allows you to start investing with just £100 per gilt.

Review tenors and yields – Check the current market yields for gilts with different tenors (the length of time until they are repaid). Choose a gilt that matches your investment goals.

Place an order – Buy directly through your chosen platform.

Conclusion

Gilts have become an attractive investment for individuals due to recent economic changes and their tax efficiency. While they may not offer the highest returns, they provide a safe and predictable way to grow your money, especially in uncertain times.

Key takeaways:

Gilts are low-risk government bonds suitable for conservative investors.

They offer tax benefits, making them efficient, especially for higher-rate taxpayers.

The current market environment makes discounted gilts a unique opportunity.

While they are safer than stocks or corporate bonds, they have lower return potential.

Gilts are easy to buy through brokers.

If you are a higher or additional rate tax-payer looking for a low-risk investment that can help preserve and grow your wealth with high levels of tax efficiency, gilts might be worth considering.

Pair trading.

Could be traded with a higher yielder to reduce the overall risk and still receive a blended yield for the target yield of 7%.

Remember a yield of 7% doubles your income every ten years, no matter whatever direction the markets travel.

Trading update for the first half ended 30 September 2025

Assura plc (“Assura”), the UK’s leading diversified healthcare REIT, today announces its Trading Update for the first half to 30 September 2025, in advance of the annual general meeting being held later today.

Jonathan Murphy, CEO, said:

“I am proud to report on a strong trading performance over the first six months of the financial year, in what was a period of uncertainty for the business. This is testament to the hard work and dedication of our team members, the strength of Assura’s business, and the vital role we play within the UK healthcare infrastructure.

“We have delivered strong rental growth, which has flowed into the positive property valuation uplift, and have continued to identify opportunities to deliver new healthcare developments for both the NHS and independent sector.

“There remains critical need for investment in healthcare buildings to enable the provision of high-quality health services. Assura’s specialist team has the skills and expertise to partner with our customers to meet these needs.”

Continued track record of delivery to enhance portfolio value and earnings

• Rent reviews completed in the first half generated:

o Like-for-like increase of 5.6% on £25.5 million of rent roll reviewed

o Weighted average annual uplift of 2.9%

• Annual equivalent uplift of 2.7% on OMR reviews, 3.0% on RPI and other

• 15 asset enhancement lease events (renewals, regears and net lettings) completed covering £1.0 million of rent roll, adding 11 years on average to those leases

• Commenced roll out of rooftop solar commercialisation project

o First installation at Crompton Health Centre in Bolton fully energised and moving on site with a further 10 sites by December

o Each installation will generate a significant reduction in carbon emissions, reduce energy costs for tenants and generate an attractive investment yield

o Total spend on the first projects is expected to be £1 million, with a pipeline of further 40 future schemes now under detailed review

Ongoing development activity

• Construction underway on a £18 million primary care scheme in Weston-Super-Mare pre-let to the NHS on a 25 year lease subject to 5 yearly CPIH rent reviews. This is the first development funded through the £250 million joint venture with USS

• Construction to commence shortly on a new £19 million independent hospital in Peterborough pre-let to a tier one independent health provider on a 25 year lease subject to 3 yearly RPI rent reviews

• Agreements to commence £7 million extension on two existing independent hospital sites to provide further on-site clinical capacity

• Three existing on site developments in Ireland continue to progress well (total cost £31 million of which £17 million has been spent to date)

Attractive pipeline of opportunities to support health care system

• £250 million development pipeline capable of commencing in the next 2 years

o £160 million of large independent sector projects

o £90 million of NHS primary care schemes

• 31 asset enhancement lease events covering £5.6 million of existing rent roll in the current pipeline

Portfolio positioned to deliver strong future cash flows

• Portfolio now stands at 602 properties with an annualised rent roll of £179.5 million (March 2025: 603. £177.9 million) and a WAULT of 12.3 years (March 2025: 12.7 years)

• Following active portfolio management, portfolio rent reviews consist of: c.54% OMR, c.46% indexed, fixed or other

• Highest-ever admissions into the independent sector generating record growth in our private hospitals operational profitability, improving rent cover to 2.6x from 2.3x

• Portfolio management activities and rent reviews have contributed to valuation uplift of approximately £12 million in the first half. Portfolio Net Initial Yield 5.23% (March 2025: 5.21%)

Primary Health Properties PLC (“PHP”) offer for Assura and delisting from the London Stock Exchange (“LSE”) and Johannesburg Stock Exchange (“JSE”)

On 5 September 2025, at the request of PHP, Assura made requests to the FCA and the London Stock Exchange respectively to cancel the listing and trading of the Assura Shares on the Equity Shares (Commercial Companies) category of the Official List and Main Market of the LSE (the “LSE Delisting”). It is anticipated that the LSE Delisting will take effect no earlier than 7.30 a.m. on 6 October 2025.

STIFEL RAISES PRIMARY HEALTH PROPERTIES TO ‘BUY’ (HOLD) – PRICE TARGET 105 (92) PENCE

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources, and more.

Fancy earning some untaxed income from high-yield shares to help fund retirement?

It can be within reach if we use a Stocks and Shares ISA. According to the latest data, there are nearly 5,000 ISA millionaires in the UK. In fact, since the statistics were published in late 2024, the number might have already exceeded that.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

High yield

What do I mean by high-yield shares? A large number of UK companies are mature, and pay out spare cash to shareholders as dividends. My ‘high yield’ decision depends on a few things — more than just a current headline big dividend.

A track record of beating the index average is a good start. Some companies stubbornly pay out while not having the cash to keep it going. Inevitably, something has to break, and it usually means a dividend cut. So, I want to see sufficient earnings to cover the annual dividends comfortably — and see it translate to strong cash flow.

And the business has to convince me it can keep going profitably for decades into the future. That means providing essentials, having barriers to entry, safety margins, and things like that.

A fat 8%

Primary Health Properties (LSE: PHP) ticks my boxes, so I’ll use that as an example to work out what we might achieve.

Primary Health is an investment trust. It owns and rents out a portfolio of health facilities, with its biggest client being the NHS. That business model means I see good defensive qualities and good cash prospects from long-term leases. And at the moment, we’re looking at a forecast 8% dividend yield.

With interim results, CEO Mark Davies said the trust “has delivered a strong operational and financial performance driven by rental growth across our portfolio, a value-accretive acquisition in Ireland, valuation gains and another period of dividend growth“. And he spoke of an “improving rental growth outlook“.

Analysts forecast continuing dividend raises in the coming years too. And if they’re right, rising earnings could drop the price-to-earnings (P/E) ratio under nine by 2027.

The secret is to reinvest the annual dividend income to buy more shares. So what might Primary Health’s 8% per year compound up to?

The road to £2,000

One way to hit our goal could be to invest a full ISA allowance of £20,000 every year for 10 years. That should build up to a pot of a bit over £300,000. And an annual 8% of that would get us to £2,000 per month.

We can’t all invest that much. But £600 each month could get us there in 19 years. It’s up to each of us to do the best we can.

Dividends can’t be guaranteed. And if the trust misses an expected raise, the share price could suffer. Investing in healthcare carries political risk, too, as policy can change.

So, diversification is essential. I use high-yield shares as one prong of my long-term investing strategy. And I do think investors seeking long-term income should consider including Primary Health in their Stocks and Shares ISAs.

Market optimism has waned as investors weighed mixed data, Fed guidance, and sector-specific risks after the S&P 500 hit eight record highs in September.

Strong GDP and jobs data have tempered rate cut expectations, resulting in a slight market pullback, though 89% of traders still predict an October rate reduction.

Beyond shifting rate cut expectations, seasonal weakness, upcoming earnings, and concerns around stretched valuations could contribute to market volatility.

Dividend stocks become more attractive vs. bonds as rates fall, and their steady payouts and stable cash flows help cushion portfolios against volatility.

SA Quant has explored its universe of top dividend stocks and selected five options for investors based on their exceptional Quant factor and dividend grades.

I am Steven Cress, Head of Quantitative Strategies at Seeking Alpha. I manage the quant ratings and factor grades on stocks and ETFs in Seeking Alpha Premium. I also lead Alpha Picks, which selects the two most attractive stocks to buy each month, and also determines when to sell them.

Lemon_tm/iStock via Getty Images

Mixed Signals: Economic Data Fuels Fed Uncertainty

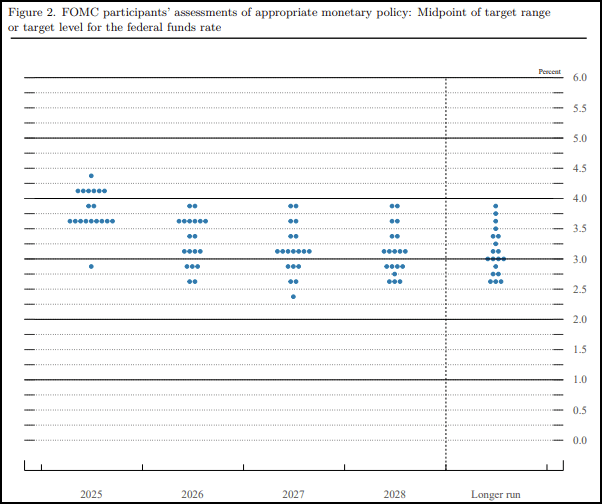

U.S. market exuberance began to fade last week as investors tried to assess the crosscurrents of mixed economic data, Fed guidance, and sector-specific risks. The Fed’s 25 bps rate cut helped the S&P 500 reach eight record highs in September alone. Market enthusiasm was further supported by expectations of future rate cuts; the FOMC’s Sept. 17 dot plot showed policymakers projecting two additional quarter-point rate cuts by the end of 2025.

The FOMC Projects Two More 25 Basis Point Cuts in 2025 (as of Sept. 17, 2025)

The Federal Reserve Summary of Economic Projections

However, the market’s rally began to stall as Fed Chair Jerome Powell emphasized two-sided risks, warning of persistent inflation, while labor market risks are growing. Markets faltered further when expectations for an October rate cut were tempered by stronger-than-expected GDP growth and lower jobless claims. Despite the deluge of mixed data, markets still anticipate another rate cut in October, though expectations have narrowed slightly, with 11% of traders expecting rates to stay the same for the October Fed meeting.

While major averages started the week on a more optimistic note, potential volatility driven by shifting rate expectations could be exacerbated by seasonal factors. Although September delivered an uncharacteristic rally with multiple record highs, October is the second-worst-performing month for the S&P 500.

Several unknowns could fuel additional swings in the weeks ahead: Pressure from upcoming corporate earnings, continued macroeconomic uncertainty, and concerns over stretched valuations.

Dividend Shields: Top 5 Income Stocks

Dividend stocks are appealing in both falling-rate environments and during periods of market volatility, which often coincide. As policy rates drop, bond yields tend to decline, making steady dividend payouts more attractive for income investors. Dividend-paying companies, which are often more stable with consistent cash flows, can help cushion portfolios against market fluctuations and offer a reliable income stream when uncertainty spikes. This stability makes them a wise choice for investors looking for both upside and protection in choppy, unpredictable markets. SA Quant has explored its universe of top dividend stocks and selected five options for investors based on their exceptional Quant factor and dividend grades.

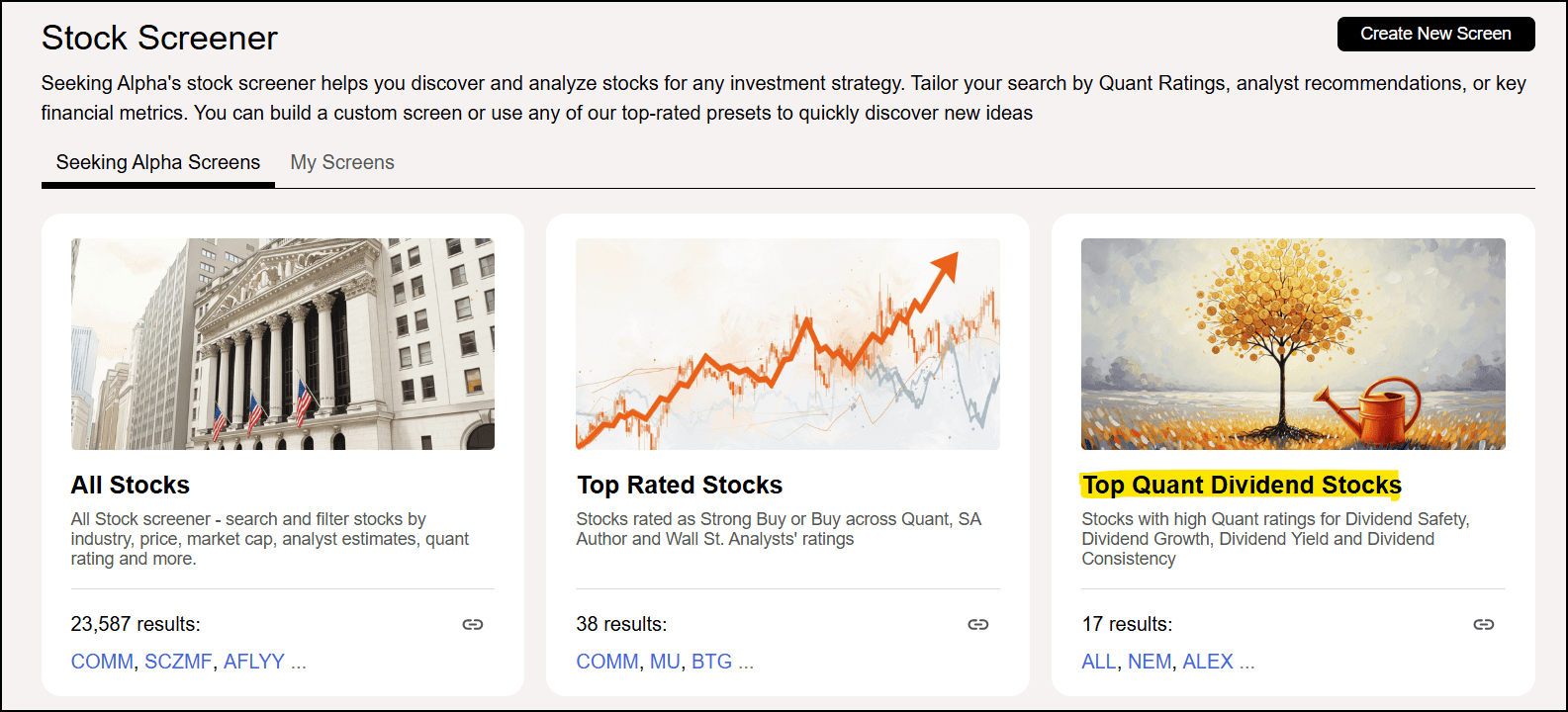

When evaluating dividend stocks, I try to look beyond headline yields, analyzing the safety and growth potential of a given dividend. Leveraging Seeking Alpha’s stock screener, I selected “Top Quant Dividend Stocks” to get my initial universe of high-quality income stocks.

Seeking Alpha

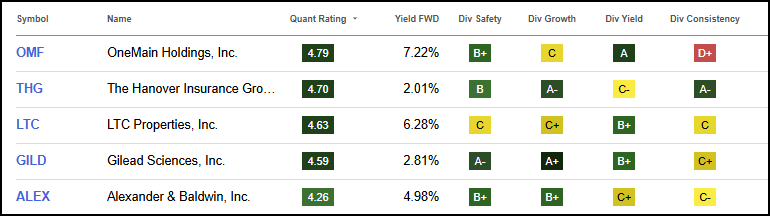

From there, I selected five stocks from the list that represent a blend of sectors and industries, favorable dividend grades, and forward yields. This basket of five stocks has an average dividend yield of 4.66%, well above the 1.10% for the S&P 500 and 1.65% for Vanguard Dividend Appreciation Index Fund ETF Shares (VIG).

Top 5 Dividend Stocks for Steady Income Have an Average FWD Yield of 4.66% versus the S&P 500’s 1.10%

SA Premium

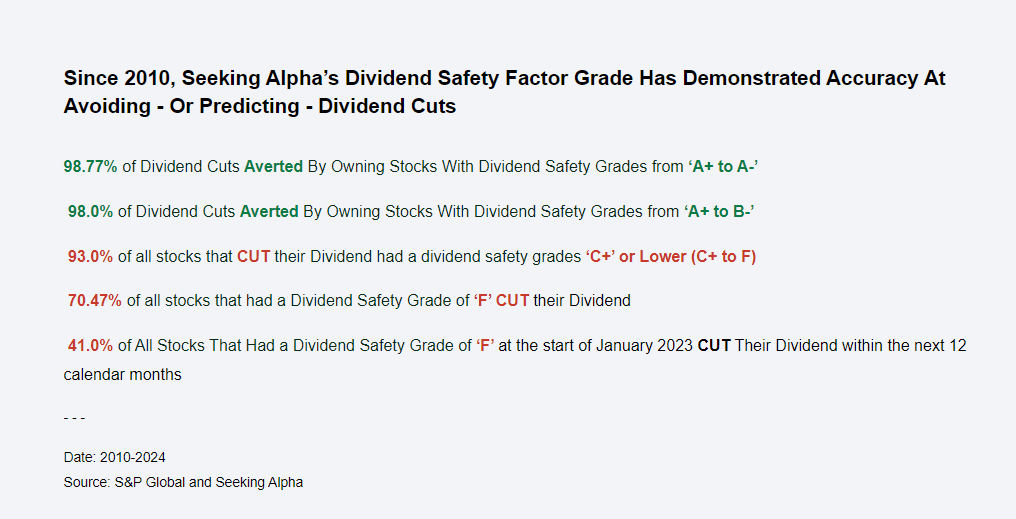

As I mentioned, these stocks were evaluated along multiple dividend grades, including safety and growth. The dividend safety grade leverages a sophisticated data-driven approach to offer a reliable assessment of a company’s ability to keep paying its dividends and avoid dividend cuts.

Dividend Cuts Can Be Avoided With Strong Dividend Safety Grades

Seeking Alpha

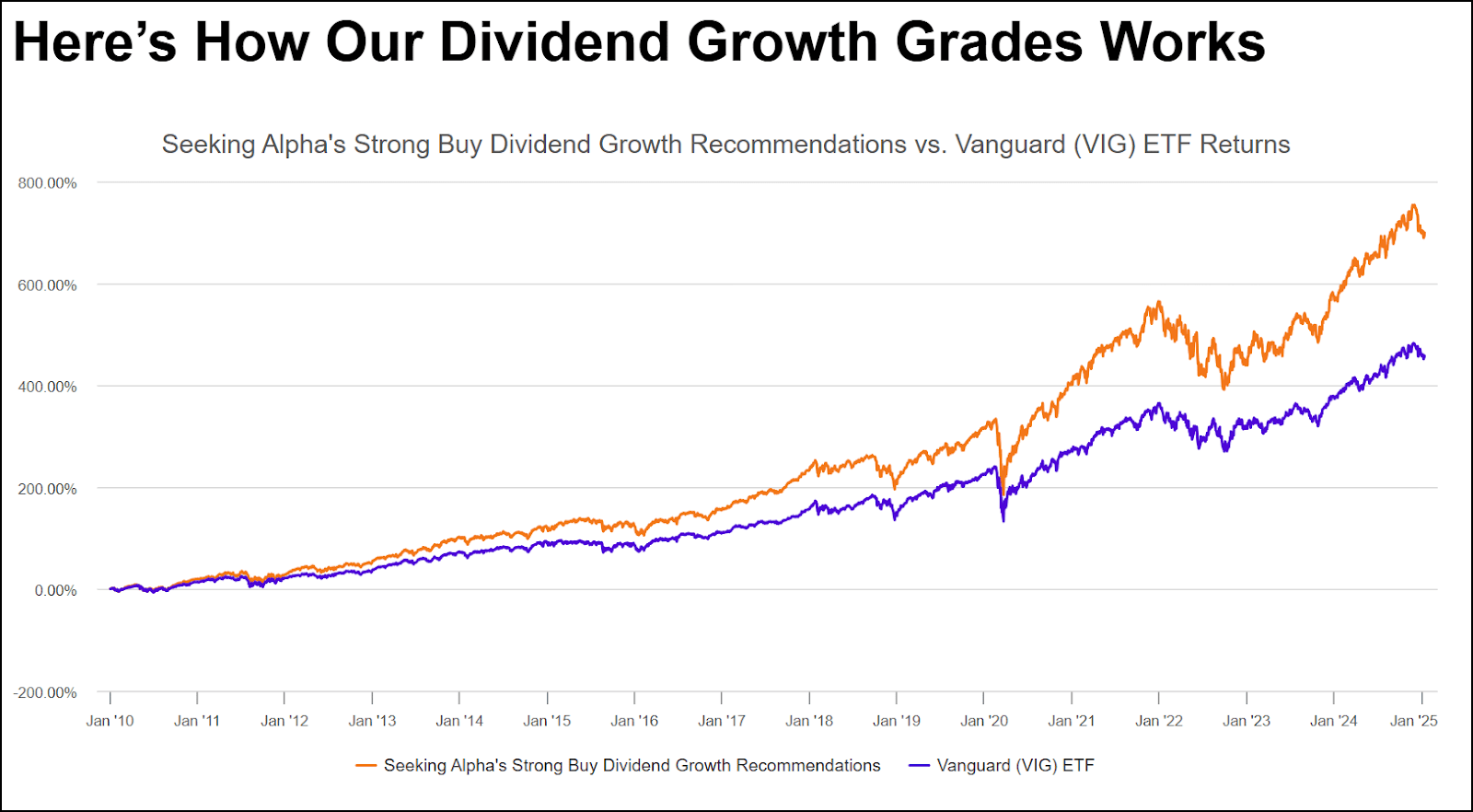

Similarly, based on data-driven analysis, the dividend growth grade provides an instant characterization of a company’s ability to grow its dividends. This tool is valuable for income-focused investors who want to target companies with the potential for capital appreciation as well as pinpoint companies with better dividend growth prospects.

Seeking Alpha

Note that because these stocks were holistically evaluated across factor and dividend grades, they do not represent the highest-yielding dividend stocks. Instead, they are a combination of dividend yield, safety, and growth, in addition to high factor grades and a Quant “Strong Buy” recommendation.

If you’re looking for stocks with the highest potential for capital appreciation, consider Alpha Picks. While it doesn’t target dividends specifically, about a third of the selections do generate income alongside their growth potential. Alpha Picks highlights Seeking Alpha Quant’s best monthly ideas, chosen from hundreds of Strong Buy–rated stocks, and focuses on high-quality opportunities with strong financials and attractive valuations.

Quant Sector Ranking (as of 9/30/2025): 34 out of 688

Quant Industry Ranking (as of 9/30/2025): 5 out of 38

Quant Rating: Strong Buy

FWD Yield: 7.22%

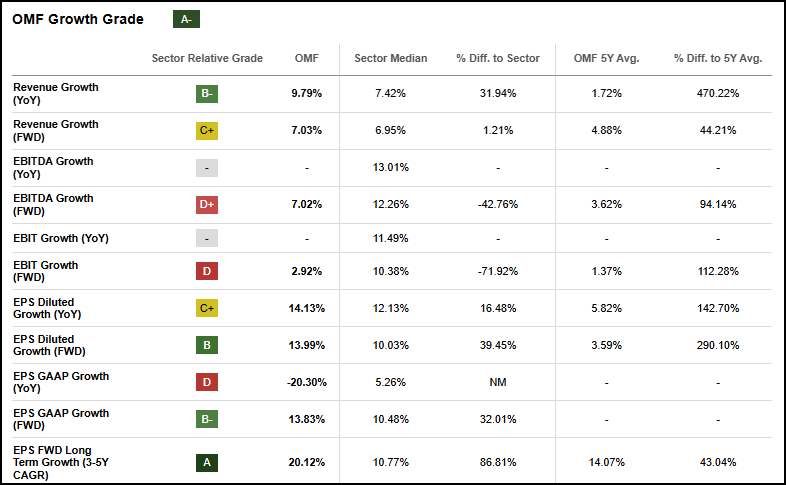

As a leading provider of personal and auto loans for non-prime consumers, OMF offers its services through both branches and digital channels. Strong originations of high-quality loans, improved credit trends, and disciplined balance sheet management have contributed to the company’s ‘B+’ Profitability. The company offers an ROE of nearly 21%, which is 90% above the sector median, alongside nearly $2.9B in cash from operations.

Strategic initiatives such as loan consolidation offerings, increased automation, and cross-selling between credit cards and loans have enhanced the firm’s growth. From a Quant perspective, growth highlights include an EPS FWD Long Term Growth (3-5Y CAGR) that is almost 87% above the sector median and a FWD EPS diluted growth of nearly 14%.

OMF Growth Grade

SA Premium

OMF’s FWD dividend yield is 134% above the sector median and has delivered five consecutive years of increases. The dividend is also backed by a “B+” Dividend safety grade, supported by a cash dividend payout ratio that’s 64% below the sector median. OMF’s success in the face of macroeconomic uncertainty, including solid credit improvement and expanding high-quality loan originations, bodes well for its future potential.

Quant Sector Ranking (as of 9/30/2025): 50 out of 688

Quant Industry Ranking (as of 9/26/2025): 7 out of 52

Quant Rating: Strong Buy

FWD Yield: 2.01%

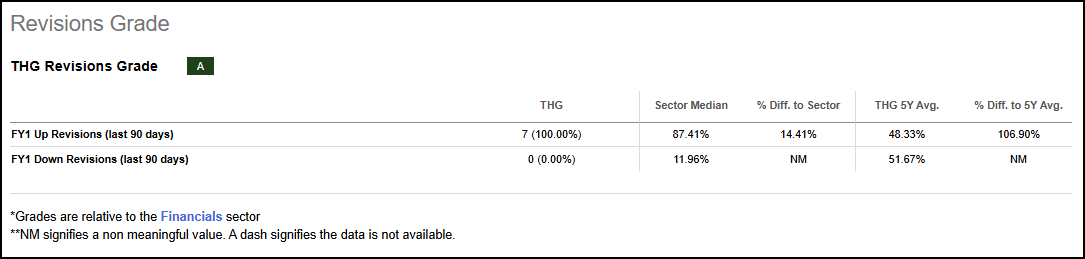

Property and casualty insurer THG has been propelled by a combination of record-setting financial performance, strategic business execution, and positive sector sentiment. The company’s exceptional Q2 earnings beat, including 25% earnings growth on an ex-catastrophe basis, has led to universal upward analyst revisions.

THG Revisions Grade

SA Premium

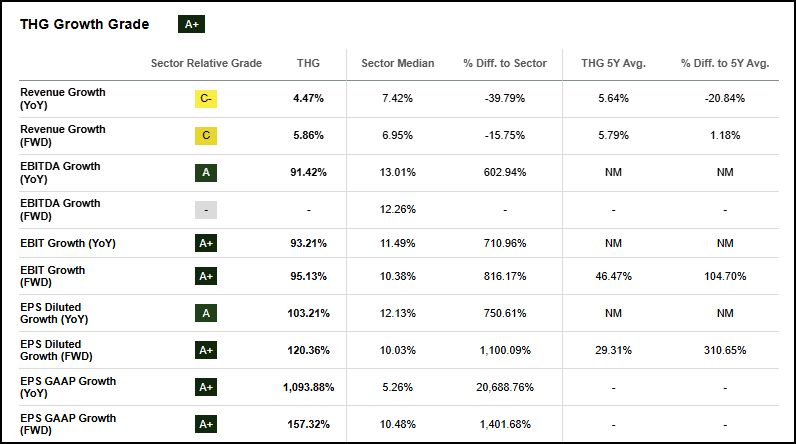

Margin improvements across all core segments have contributed to the stock’s solid profitability. THG boasts an ROE that is 78% above the sector median and has $854M in cash from operations vs. the sector’s $175M. Several strategic initiatives, including tech and operational investments and geographic diversification, have helped the company secure sector-leading growth. The company possesses both year-over-year and forward-looking earnings growth in excess of 100%.

THG Growth Grade

SA Premium

From an income perspective, THG’s dividend growth potential stands out with a one-year growth rate that’s 50% above the financials sector, accompanied by 18 consecutive years of increases. THG’s track record of strong execution, ongoing investments and technology, and capital allocation discipline indicates that both its share price and dividend are well-conditioned for continued growth.

Quant Sector Ranking (as of 9/30/2025): 11 out of 176

Quant Industry Ranking (as of 9/30/2025): 2 out of 17

Quant Rating: Strong Buy

FWD Yield: 6.28%

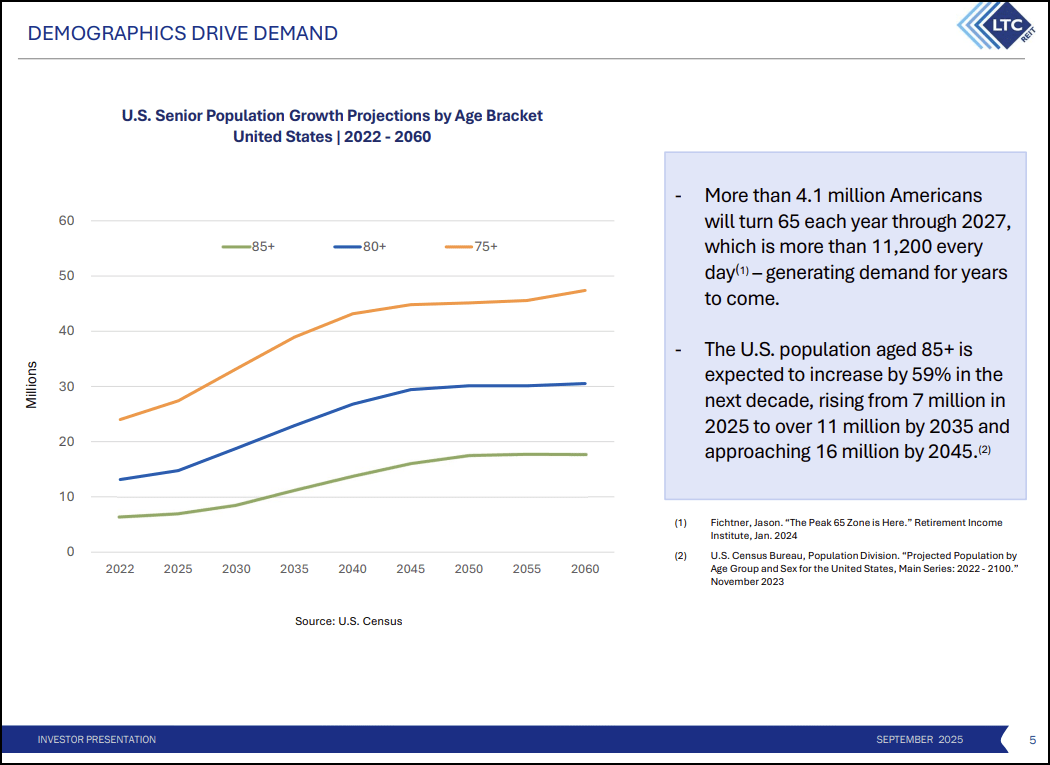

I recently wrote an article titled REITs for A Rate-Cut Rebound: My Top 5 Picks, focused on stocks that could benefit from easing monetary policy. My next stock selection is the No. 2 Quant-ranked Health Care REIT. LTC Properties focuses on senior housing and healthcare properties through investments in assisted living, memory care, and skilled nursing facilities. The company is poised to capitalize on a seismic demographic shift as more than four million Americans turn 65 each year through 2027. LTC is in the process of transitioning from a triple net lease REIT to an owner and operator model, aligning interests and creating opportunities for growth.

Propelled by robust occupancy trends, the company boasts incredible profitability supported by an AFFO margin of 63%, as well as an interest coverage ratio of 3.6x. LTC’s disciplined financial management provides a measure of safety to the company’s outstanding 6.28% dividend yield. LTC’s enticing valuation is supported by solid underlying metrics, including a FWD price/AFFO that’s 15% discounted to the REITs sector. This unique combination of yield, growth, profitability, and value makes LTC a standout in the rapidly expanding senior care market.

Quant Sector Ranking (as of 9/30/2025): 36 out of 971

Quant Industry Ranking (as of 9/30/2025): 15 out of 472

Quant Rating: Strong Buy

FWD Yield: 2.81%

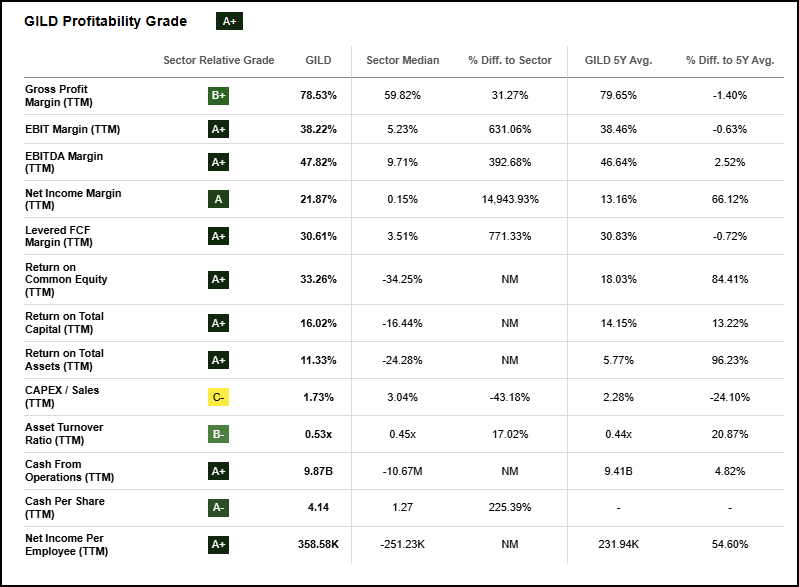

Global biopharmaceutical Gilead Sciences has a robust commercial portfolio across a variety of innovative therapies in virology, oncology, and more. The company is distinct from many of its peers in that its core products are largely manufactured in the U.S., making it less exposed to tariff-related cost pressures, which have weighed on the sector lately.

“Starting October 1st, 2025, we will be imposing a 100% Tariff on any branded or patented Pharmaceutical Product, unless a Company IS BUILDING their Pharmaceutical Manufacturing Plant in America,” Trump said in a social media post late Thursday.

Gilead CEO Daniel O’Day noted in the company’s Q1 earnings call that the “vast majority” of the company’s IP and more than 80% of its profits are recognized in the U.S. This structural difference should continue to advantage the company from a profitability standpoint, with an EBITDA margin that is nearly 400% above the sector median.

GILD Profitability Grade

SA Premium

GILD impresses across key valuation metrics, trading at a FWD PEG that’s 65% below the sector median as well as a price cash flow of 12.6x vs. the sector’s 14x. The company is projected to enjoy long-term earnings growth with a 3-5YR CAGR of 20%. While its 2.81% yield may be modest for dividend seekers, its growth potential is pronounced; GILD’s 10Y CAGR Dividend Growth Rate of 14% is double that of the sector’s. With excellent fundamentals and a steady but growing dividend, Gilead is well positioned within the sector for gains.

Quant Sector Ranking (as of 9/30/2025): 19 out of 176

Quant Industry Ranking (as of 9/30/2025): 2 out of 13

Quant Rating: Buy

FWD Yield: 4.98%

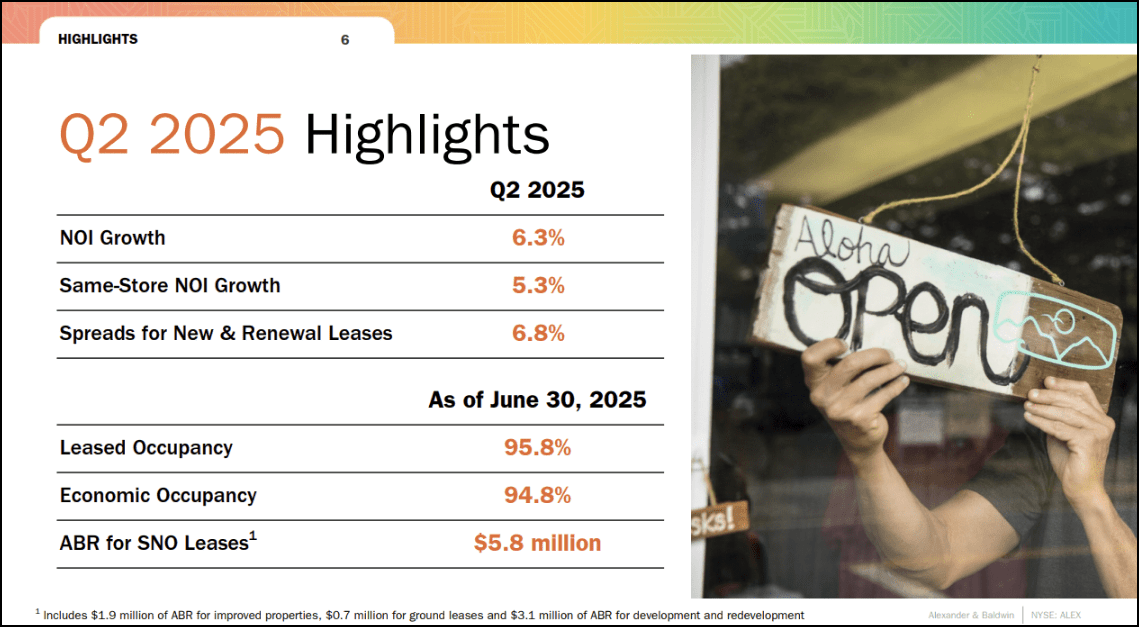

ALEX, which specializes in Hawaiian retail and office properties, has been a Quant “Strong Buy” or “Buy” since March. Its forward yield of 4.98% is supported by robust dividend safety metrics, including a dividend payout ratio that’s 132% above the sector median. The company stands out as a strong choice for the current moment, as the real estate sector stands to gain from Fed easing, potentially expanding growth for REITs like ALEX.

In Q2, the company experienced a strong double-beat driven by higher occupancy and major development wins. These gains have helped shore up the company’s ‘B+’ Profitability grade, with highlights including an FFO to Gross Margin of 92%. ALEX also sports compelling Quant growth metrics, including an AFFO FWD growth that’s nearly 300% above the sector median.

ALEX offers investors a reliable income through three years of steady dividend growth and strong fundamentals for those interested in the niche market.

Stay the Course, Collect the Yield

Market optimism began to fade last week as investors digested mixed data, Fed guidance, and sector-specific risks following eight S&P 500 record highs in September. Stronger-than-expected GDP and job numbers called future rate cuts into question, though the majority of traders still anticipate more easing in October. Beyond shifting rate cut expectations, volatility may intensify due to seasonal weakness, corporate earnings, and stretched valuations. Falling rates make dividend stocks relatively more attractive versus bonds, and their stable payouts provide a buffer against market swings. SA Quant has identified five top dividend stocks based on exceptional factor and dividend ratings, to help investors navigate this period. SA’s Quant Team used its stock screening tool to identify five dividend stocks with strong quant ratings, and excellent dividend growth and safety grades.

“Perhaps we should anchor to today’s multiples as the new normal”: Savita Subramanian at Bank of America (NYSE:BAC) echoed thoughts that AI growth and resilient earnings could justify today’s valuations – some approaching dot-com bubble levels.