Here’s a 7-share passive income portfolio investors should consider over cash savings

Discover how holding a diversified range of UK dividend shares could generate a strong and stable passive income over time.

Posted by Royston Wild

Published 20 September

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

By some distance, Brits still prefer to hold cash on account for a passive income than to put their money in shares. To prove my point, latest data showed that 7.9m adults currently hold a Cash ISA, more than double the number that have a Stocks and Shares ISA (3.8m).

Given the spike in interest rates after 2021, it’s not a shock to see cash accounts have gained popularity. But with the Bank of England slashing their lending rates, continuing to prioritise savings over investing in the stock market could be an expensive mistake.

Should you buy Chelverton UK Dividend Trust PLC shares today?

Better returns

Investors have to balance risk and reward when deciding where to put their cash. And there’s no right or wrong answer, as it depends on each individual’s investment goals and risk tolerance.

But I prefer to put the lion’s share of my capital in dividend-paying stocks. By investing in a wide range of companies, too, I can mitigate the riskier nature of share investing versus saving, and chase a strong return without putting my money in too much danger.

Even if rates remain unchanged at 4%, the superior passive income that’s on offer from UK shares make stock market investing a ‘no brainer’ for me.

Seven dividend stars

Here’s a mini-portfolio of seven UK stocks investors could consider putting their spare cash in:

| Dividend share | Sector | Dividend yield |

|---|---|---|

| M&G | Financial services | 7.9% |

| Greencoat UK Wind | Renewable energy | 9.8% |

| HSBC | Banking | 4.8% |

| Persimmon | Housebuilding | 5.5% |

| Target Healthcare REIT | Real estate investment trusts (REITs) | 6.2% |

| Pennon Group | Utilities | 6.6% |

| Chelverton UK Dividend Trust | Investment trusts | 8.6% |

The average dividend yield across these shares is 7.1%, which is triple the average interest rate of 2.3% that savers currently enjoy. Dividends aren’t guaranteed, but assuming these companies meet brokers’ forecasts — and can print a 3% average share price rise, too — I could enjoy a total annual shareholder return north of 10%.

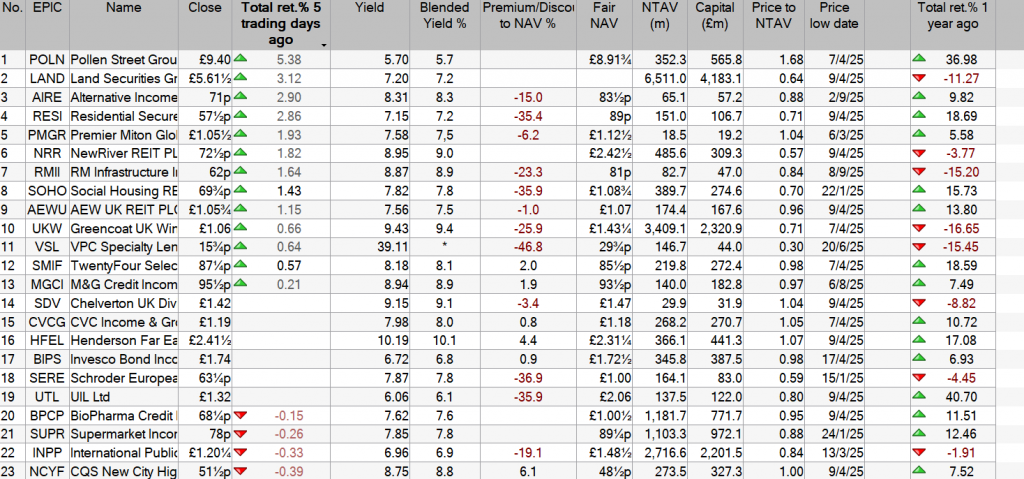

Spread across 73 different companies, this mini portfolio could help protect investors against regional-, industry-, or company-specific shocks. The Chelverton UK Dividend Trust is especially effective in delivering this diversification.

The trust’s objective is “to deliver a high and growing income through investments in mid to small-cap companies exclusively outside the largest 100 UK stocks“. Concentrating on non-FTSE 100 stocks comes with greater risk, but it also provides the potential for superior rewards.

Besides, with investment in 66 different businesses across 20 different sectors, risk is still pretty well spread, in my opinion. Chelverton’s record of 14 straight years of dividend increases illustrates this robustness.

My plan

I’m not saying that investors should consider avoiding cash accounts altogether. I myself hold money in savings to diversify my broader portfolio and provide access to emergency cash.

But, for me, the best way to target a life-changing passive income is by putting most of my spare capital in dividend shares.