Important information – the value of investments and the income from them can go down as well as up, so you may get back less than you invest.

Investment trusts that provide exposure to renewable energy projects such as solar and wind farms have been out of favour for several years, so it was interesting to see that three of these trusts were among the best-sellers on the Fidelity Personal Investing platform in July. This was the first time that these particular funds had featured in the year-to-date numbers.

The renewable energy sector is known for its high yields, which are often in excess of 7%, but the attractiveness of these income streams was undermined by the sharp rise in interest rates after the pandemic. Please note these yields are not guaranteed. It is likely that investors are being tempted back ahead of further possible rate cuts by the Bank of England.

The Renewables Infrastructure Group

In fourth place on the list of bestsellers was the two billion pound Renewables Infrastructure Group, which owns a diversified portfolio of wind farms and solar parks in the UK and Europe. These generate revenues from the sale of electricity and government-backed green benefits.

The trust aims to provide investors with long-term, stable dividends and to retain the portfolio’s capital value through re-investment of surplus cash flows. Its management has a total return focus, although much of this is in the form of dividends, with the target distribution of 7.55 pence for 2025 giving the shares a prospective yield of 9.2%.1 Please note this is not guaranteed.

As with all of these sorts of funds, the net asset value (NAV) calculation is extremely complicated with lots of assumptions so they only tend to be updated on a quarterly basis. The end of June figure of 108.2p suggests that the shares are available at a discount of around 24%, despite the active buyback programme.

Sixth on the list was the £484m Foresight Solar Fund that owns a portfolio of solar farms and battery storage assets in the UK and overseas. It aims to provide investors with a sustainable, progressive quarterly dividend and enhanced capital value, whilst facilitating the transition to a lower-carbon economy.

Foresight’s target dividend for 2025 is 8.1 pence, giving the trust a prospective yield of 9.4%.3 Please note this is not guaranteed. At the end of June the NAV was 108.5p, which equates to a discount of around 20%, although there is an active share buyback programme that has recently been increased to £60m.

The Board is trying to sell its Australian wind farms and intends to use the proceeds to reduce the level of gearing (debt to equity ratio) that currently stands at 40%. However, no bids have been received at time of writing.

In seventh position was the £568m Bluefield Solar Income whose main asset is a portfolio of solar farms located in the UK. It aims to provide shareholders with an attractive return, principally in the form of quarterly distributions, with the target dividend for the 2024/25 financial year of not less than 8.90p giving the shares a prospective yield of 9.3%.

Bluefield’s latest available NAV at the end of June was 117.8p, which implies a discount of 19%. The Board is exploring strategic options to address this and maximise shareholder value.

One important feature that differentiates it from its peers is the significant pipeline of development assets identified by the Investment Advisor that provide a future platform for growth. Another is the strategic partnership with a group of UK pension funds, which gives Bluefield a means of recycling capital from its existing projects.

Brett Owens, Chief Investment Strategist Updated: August 22, 2025

Let’s talk about three dividends averaging 12%. I bring them up because everyone on Wall Street hates them.

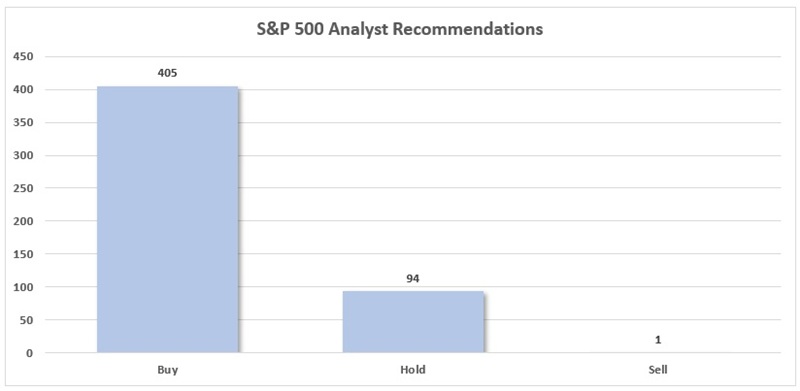

This is notable because the suits are paid to be bullish. Sell calls are rare, especially among S&P 500 stocks. In fact, analysts shun just one index component today!

Just 1 “Sell” Call Out of 500! Source: S&P Global Market Intelligence

Buy calls? They are numerous—405 out of 500. Eighty-one percent!

Are 81% of the companies in the S&P 500 really buys? Normally, no, but now—especially not. AI is disrupting business models and many of these Buy-rated names are doomed companies.

Here’s another problem with Buy ratings—there is no room for improvement. Sells are better. They set the stage for upgrades! And it doesn’t take much for analysts to flip a stock from a Sell to a Buy.

Which is why savvy contrarians dig through the Sell bin.

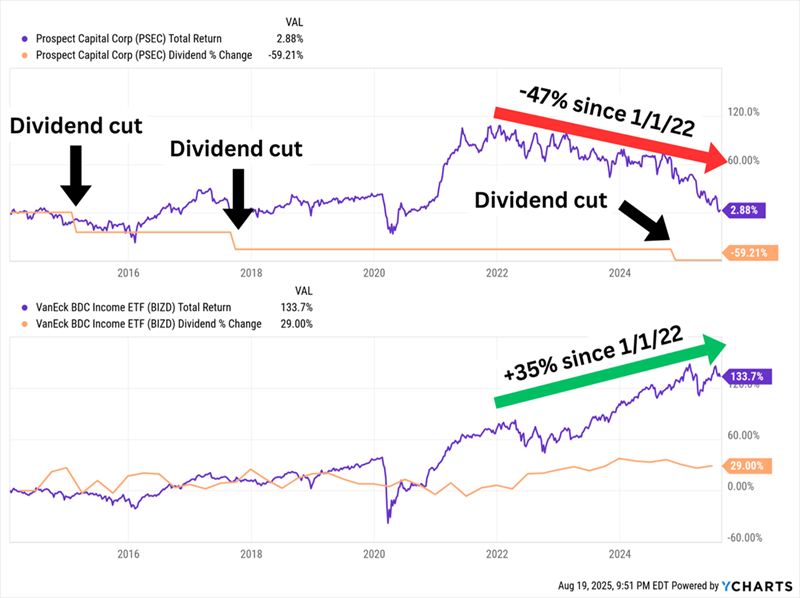

Today we’ll discuss three hated names yielding from 6.1% to 15.7%. Before getting to those, let’s use Prospect Capital (PSEC, 18.7% yield), as a cautionary tale and highlight the difference between being contrarian and being foolish.

PSEC is a business development company (BDC) that provides capital to middle-market companies, primarily through first lien and other secured debt. It has a diverse portfolio of 114 companies across 33 industries. And it’s one of the largest BDCs at well more than $1 billion in market cap.

But despite being a monthly dividend payer with a yield that could be confused for a credit card APR, and despite being the cheapest BDC on the market, Wall Street can’t find a reason to like it. It has just two covering analysts, and only one of them has a rating on the stock (Sell, unsurprisingly). While that smacks of too small a sample size, the lack of coverage itself is telling. Research firms would prefer not to bite the hands that provide them with access, to the point where many would choose to temporarily stop covering a company over calling a spade a spade.

Why the lack of love? Among other reasons, how about three dividend cuts in the past decade, including a 25% reduction less than a year ago.

BDCs as a Whole Haven’t Set the World on Fire, But at Least They’re Not All PSEC

All right. What about a BDC with a slightly less bearish camp? BlackRock TCP Capital Corp. (TCPC, 15.7% yield) is technically a consensus Sell call, but the majority of analysts covering it say it’s a Hold. So at least as far as pro ratings go, it’s not a disaster.

TCPC is a middle-market lender that prefers companies with enterprise values of between $100 million and $1.5 billion. It currently boasts more than 150 portfolio companies across 20 different industries, and its deal mix is heaviest (82%) in first-lien debt, and the vast majority (94%) of its lending is floating-rate in nature.

The case for BlackRock TCP Capital Corp. is BlackRock. The BDC is externally managed by a BlackRock subsidiary, which gives it access to BlackRock resources. In theory, that should make TCPC competitive.

In Practice, It Doesn’t

Again, the pros likely have a legitimate case here. TCPC is in the process of restructuring deals amid credit issues in the portfolio, and management fees have been waived to make up for some of the financial slack. The dividend—which BlackRock TPC cut earlier this year, just a few months after I flagged the potentially brewing trouble in its distribution—isn’t necessarily at risk yet, but it bears watching if portfolio losses continue.

Hated BDCs might be asking for it. Let’s look at other high-yield acronyms instead.

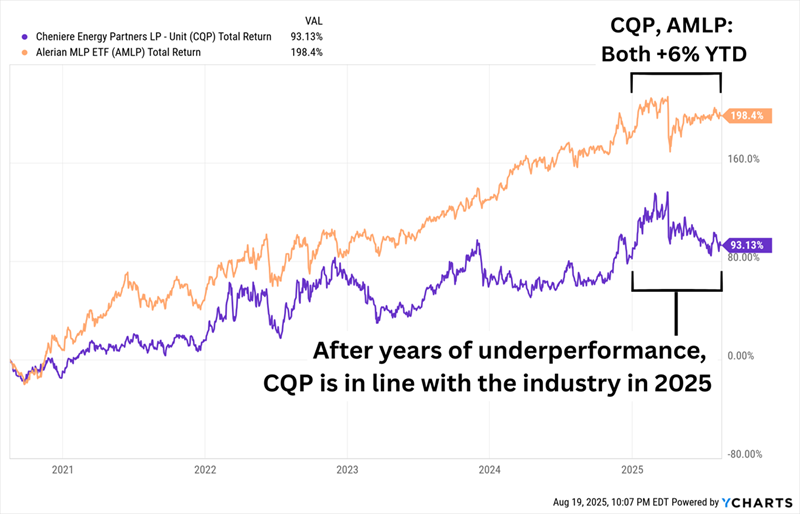

Cheniere Energy Partners LP (CQP, 6.1% yield) is a midstream subsidiary of Cheniere Energy (LNG). It owns the Sabine Pass LNG (liquefied natural gas) terminal in Louisiana, which includes natural gas liquefaction facilities and regasification facilities. It also owns the Creole Trail Pipelines, which connects the Sabine Pass terminal with inter- and intrastate pipelines.

Cheniere Partners owns the Sabine Pass LNG terminal located in Cameron Parish, Louisiana, which has natural gas liquefaction facilities with a total production capacity of over 30 mtpa of LNG. The Sabine Pass LNG terminal also has operational regasification facilities that include five LNG storage tanks, vaporizers, and three marine berths. Cheniere Partners also owns a Corpus Christi liquefaction facility and a connected pipeline, as well as Creole Trail Pipeline, which interconnects the Sabine Pass LNG terminal with a number of large interstate and intrastate pipelines.

CQP is pouring itself into expansions at its Sabine Pass and Corpus Christi facilities—big capital outlays that required Cheniere to reduce its variable distribution in 2024. That payout came up a smidge earlier this year, however, and the company’s underperformance last year has turned into more respectable performance this year.

Shares Stabilizing as Cheniere Builds Toward the Future

There’s no telling what the master limited partnership (MLP) will do in the short term as its various project details are fleshed out. But if these projects do bear fruit, CQP could be looking at a potential explosion of distributable cash flow (DCF) generation a few years down the road.

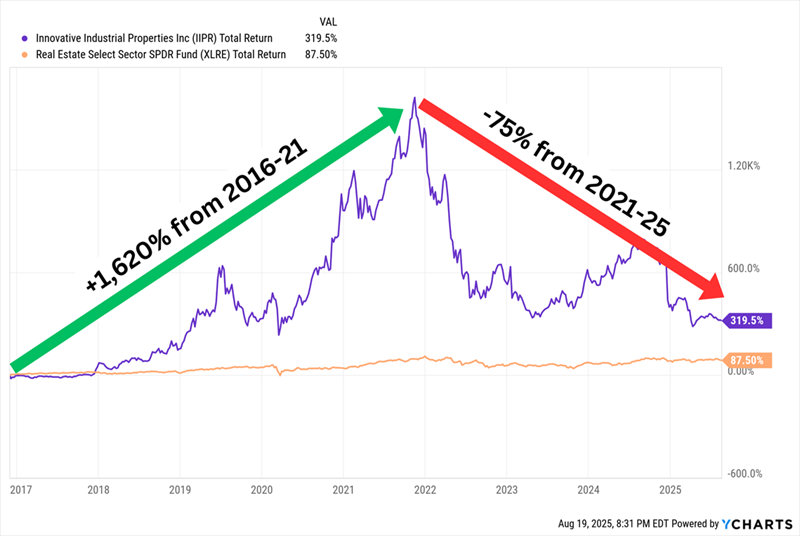

Innovative Industrial Properties (IIPR, 14.4% yield), a REIT tied to the marijuana industry, is what I call a “bearish Hold.” Most of the pros say it’s a Hold or a Sell, but a lone Buy call raises its consensus average.

Still, Wall Street really doesn’t like this stock—a massive change of fortune to a stock that over the past decade has been among both the sector’s biggest success stories and its biggest flops.

One Ticker, But Two Totally Different Stocks Since 2016

IIPR provides capital for the regulated cannabis industry through a sale-leaseback program. It buys freestanding industrial and retail properties (most of which are marijuana growth facilities) from cannabis operators, then leases them right back to the sellers. This provides cannabis operators with much-needed influxes of cash that they can use to expand their operations, and provides the REIT with ongoing cash flow. Currently, IIPR owns 108 properties in 19 states, representing nearly 9 million square feet, which it leases out to 36 tenants.

It’s not like Innovative Industrial Properties has operationally reverted to where it was 10 years ago—not even close. The company went public in 2016 and generated negative $7.5 million in funds from operations (FFO). It has cleared $210 million in FFO in each of the past three years, including $231 million in 2023 and $230 million in 2024.

However, the stock exploded even more than the business did, and the past few years have seen shares come back to earth. And everything’s not exactly rosy in the core business, which still is dealing with a cracked, state-by-state regulatory environment. That’s a big reason why IIPR recently invested $270 million into IQHQ, a life science real estate platform with more than $2 billion in assets—a move that could provide much-needed stability and growth.

It’s worth noting, however, that FFO has been declining significantly over the past few quarters, driving its adjusted FFO payout ratio to nearly 95%; that’s uncomfortably higher than the 85% ratio IIPR averaged between 2017 and 2024.

Avoid the Retirement ‘Death Spiral’: Collect 8% or More for Life

Most retirement investors wouldn’t go near many of these stocks in the first place because they’re outside their safety zone.

You know the drill. Buy blue chips and bonds. Dollar-cost average in. Slow and steady wins the race.

Unfortunately, if you’ve saved and invested “by the book,” you’re already behind—and all it might take to realize that is one poorly timed downturn in retirement.

That could force you to sell a much bigger chunk of your portfolio to withdraw the income you need to pay the bills, and suddenly, you’re way behind the 8-ball for the rest of your post-career years.

But you can avoid the retirement “death spiral” by making sure you live on dividends alone so you never have to touch your capital.

My 8% “No Withdrawal” Retirement Portfolio can do just that: produce a high level of income (without the big question marks posed by the likes of PSEC and IIPR) that allows you to retire on dividend and interest income alone. That means never touching a penny of your nest egg.

If I could leave you with just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are.

Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $87,560 by 2023, or 87x your money.

But the same $1,000 in the non-dividend payers would have grown to just $8,430 — 90% less.

That’s why I’m a dividend fan.

The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up!

There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives us dividend investors such an edge.

When you lock in an 8%+ yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

So let’s wipe the false promises of mainstream finance from our minds and start thinking the “No Withdrawal” way…

Step 1: Forget “Buy and Hope” Investing

Most half-million-dollar stashes are piled into “America’s ticker” SPY.

The SPDR S&P 500 ETF (SPY) is the most popular symbol in the land. For many 401(K)’s, this is all there is.

And that’s sad for two reasons.

First, SPY yields just 1.2%. That’s $6,000 per year on $500K invested… poverty level stuff.

Second, consider 2022 for a moment (and only a moment, I promise!).

SPY was down nearly 20% that year. That is no bueno, because that $500K would have been reduced to $400K.

The last thing we want to do is lose the money we’re getting in dividends (or more) to losses in the share price. Which is why we must protect our capital at all costs.

Step 2: Ditch 60/40, Too

The 60/40 portfolio has been exposed as senseless.

Retirees were sold a bill of goods when promised that a 60% slice of stocks and 40% of bonds would somehow be a “safe mix” that would not drop together.

Oops.

Inflation — plus an aggressive Federal Reserve, plus a (thus far) persistently steady economy — drop-kicked equities and fixed income before they went on a serious bull run in 2023 and 2024.

It just goes to show that bonds are not the haven guaranteed by the 60/40 high priests. They could easily plunge just as hard (or harder) than stocks in the next economic crisis.

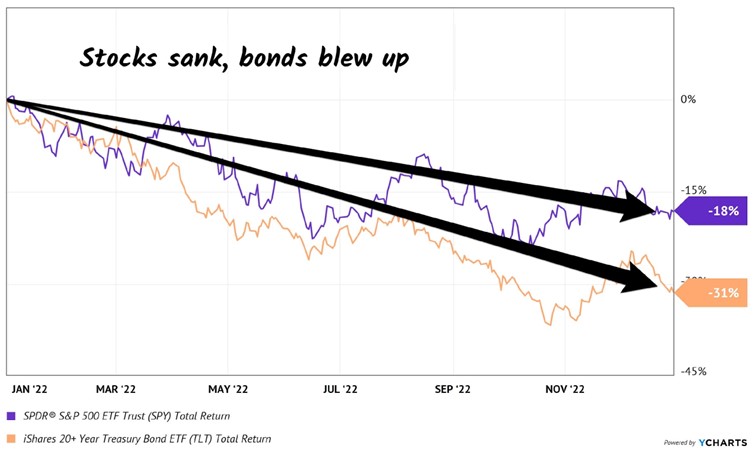

Just like they did in 2022 (sorry, we’re only going to spend one more second on that disaster of a year). US Treasuries plunged, which resulted in the iShares 20+ Year Treasury Bond ETF (TLT) getting tagged.

Sure, it still paid its dividend. But even including payouts, the fund was down 31% — worse than the S&P 500. Ouch!

When stocks and bonds are dicey, where do we turn? To a better bet.

A strategy to retire on dividends alone that leaves that beautiful pile of cash untouched.

Benstead on Bonds: are long gilts at 5.5% a no-brainer?

Some gilt yields are at their highest since the late 1990s, but should you invest?

20th August 2025 09:18

by Sam Benstead from interactive investor

If someone offered you a guaranteed annual return of 5.5%, locked in for the next 20 to 30 years, would you take it?

Well, that’s what investors can get today if they put money into long-maturity gilts. The latest data puts gilts maturing in 20 years’ time at a yield-to-maturity (YTM) of 5.5%, 25 years at 5.6% and 30 years at 5.6%.

The YTM figure assumes that coupons are reinvested and accounts for both capital and income, giving a pretty accurate estimation of annualised returns over the life of a bond.

And this yield figure is high! For comparison, 20-year government bonds in France are at 4%, Germany at 3.2% and Japan at 2.6%. It’s generally only emerging markets that yield more, and long gilt yields have not been this high since the late 1990s.

Moreover, a way of looking at the value of government bond yields is to assess the “spread”, or excess yield, that you get from owning corporate bonds. For sterling bonds, this is a little under 1%, which is historically low. This means corporate bonds are poor value compared to government bonds, because why would you take on the extra risk for just 1 percentage point of extra yield?

When I say “guaranteed” return from gilts, I am assuming that the British government does not default given that it never has before. While this admittedly does feel increasingly possible, gilts are still as close to being risk-free as investment markets can offer, at least in terms of getting your money back and collecting the two coupons per year.

But there are some other risks with a buy-and-hold gilts strategy. The biggest in my view is inflation – if prices rise at 4% a year for 20 years and your gilt pays you 5.5%, then you are only really increasing your wealth by 1.5% a year, which isn’t much. For comparison, UBS calculates that since 1900, US shares have made on average 8.4% “real”, meaning that they have made 8.4% ahead of the inflation rate over that period. The figure for UK equities is 7.1%.

Inflation in the UK is currently 3.8% and expected to hit 4% in September, before falling back to the Bank of England’s 2% target at the end next year or in early 2027. While it may return to 2% and stay there, there are no guarantees. One useful indicator of where investors think inflation will be is to look at the yield offered on index-linked gilts, which pay a return ahead of the RPI inflation rate.

A 20-year index-linked gilt currently has a yield of 2.4%, according to Tradeweb, which suggests that RPI will be about 3% a year over the next 20 years, based on the difference in yield between a 20-year inflation-linked gilt and a 20-year regular gilt. For investors worried about inflation, and who think it will be above this figure and are eventually proved right, the index-linked option could make a better investment.

While gilt returns are (nearly) guaranteed, investors must be aware that gilt prices will fluctuate a lot, particularly those that mature in 20 to 30 years. On their way to return £100 per gilt owed to the holder on maturity, prices will move due to changes in market conditions.

gilt, maturing in 25 years’ time. The price today is £35 and on 22 October 2050 it will mature and pay the owner £100. Along the way, 62.5p in coupons are paid each year. Taken together, the YTM is 5.4% annualised.

However, that 5.4% yield may become too generous or too dear depending on what happens in markets.

For example, if interest rates shoot up, then bond prices will have to fall so that yields will come into line with market prices. This would mean a big paper loss for gilts.

And a big jump in yields is definitely possible. Peter Spiller, manager of Capital Gearing Ordinary investment trust for more than 40 years, sees lots of risks ahead for gilts, especially longer maturity ones, where prices are sensitive to the creditworthiness of the UK government.

He says: “One of the most significant issues facing this government is rising interest costs against a backdrop of spiralling debt.

“The behaviour of yields on long-term gilts – the government’s cost of finance, a proxy for market confidence in public finances – suggests a fear that fiscal dominance, where interest rates are dictated by the budgetary needs of government, is a real threat.”

Jason Borbora-Sheen, a fixed-income portfolio manager at Ninety One, says that very few investors really have a time horizon long enough to hold 30-year gilts until maturity, and that the sweet spot for investors looking at gilts is normally below 10 years. His view is that there is a lot of risk in longer-term gilts and investors are better served at the shorter end of the yield curve.

He said: “The UK has a reliance on external funding and is in a poor financial position, which makes long gilts a risk proposition. Any duress in fixed-income markets will be felt hardest in these long gilts.”

So, while investors know that they will get £100 back per gilt owed, they could see their gilts drop in value over their life, which although not a financial problem if there is no need to sell, will definitely not feel great, especially if it’s a large position. On the other hand, long-term gilts could rise in value, giving holders a big paper gain.

High or low coupon gilts?

It is important to look at the size of the coupon as well if considering a long-maturity gilt. If the coupon is in line with today’s yield of around 5.5%, then the gilt will trade at around its £100 redemption value. This means that the return will come from coupons and not capital gains, which may suit investors better if they want to generate a reliable annual income from their investment.

On the other hand, if the return predominantly comes from capital gains (which are tax free outside an ISA and SIPP), then the pull to par (the £100 redemption value) is what can make up the bulk of returns. Gilts that have coupons below the market yield today will trade at a discount to the redemption value, which means that capital gains will form part of the return. The lower the coupon, the lower more impact capital growth will have.

Because this tax break is well known, it has pulled lots of capital into low-coupon gilts compared with higher coupon gilts maturing at a similar time, which has had the effect of lowering yields.

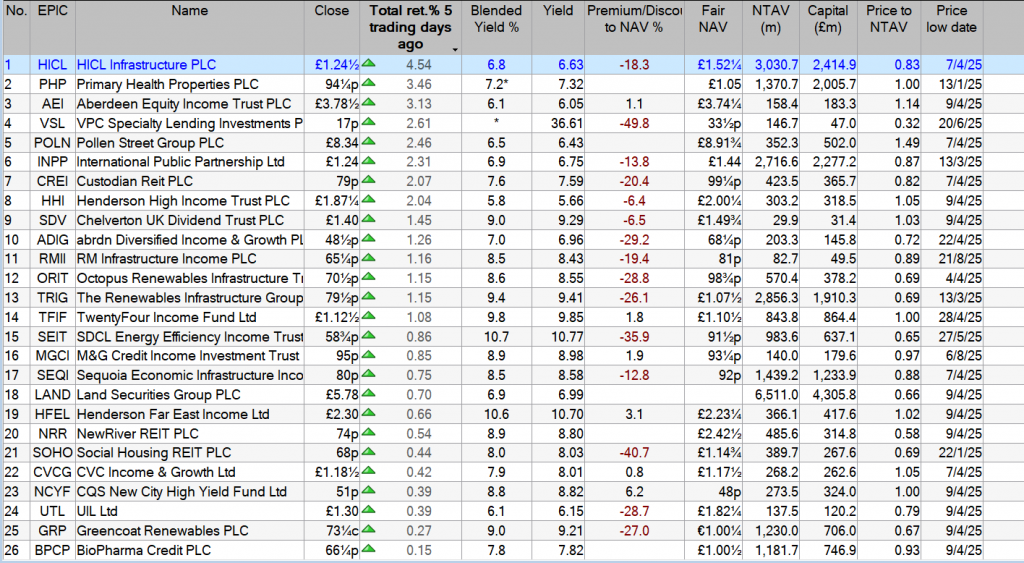

If you’re looking at long gilts, then here are some popular ones that could be researched further. I’ve included a selection of high and low coupon gilts.

Regional REIT Ltd – real estate investment trust – Shore Capital says the company is “positioned to rebuild value creation for shareholders through a series of actions including capital investment to upgrade core assets and either repurpose or dispose of non-core assets”. In a trading update in May, Regional REIT had announced continuous positive leasing momentum in the first quarter of 2025 as rent collections “remained strong”. It had cited an emerging supply and demand imbalance outside of London for office space. Shore says: “A recent survey from Savills also paints a more optimistic picture for regional offices with improving take-up, reduced new supply and more high quality refurbished existing space coming onto the market expected to drive improved rents.” Shore adds: “Regional REIT is now a business in robust strategic shape and with management initiatives expected to drive both improvement in earnings and net tangible assets over the next three years that should improve the investment case.” Regional REIT will publish its results for the first half of 2025 on September 9.

See how you could target a £1m SIPP starting with £25,000

Harvey Jones shows how it’s possible to turn a relatively small sum into a £1m pension pot by purchasing FTSE 100 stocks inside a SIPP.

Posted by

Harvey Jones

Published 22 August

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

Building a Self-Invested Personal Pension (SIPP) worth £1m sounds like a dream, but it’s not beyond reach for patient investors who start early. A SIPP lets money grow free of tax, and with time and regular contributions, it can build into a life-changing sum.

Let’s imagine a 35-year-old has just transferred £25,000 from legacy pensions or other savings into a new SIPP. They aim to stop working at 67, which gives them 32 years for their investments to compound. If their initial £25k grew at 8% a year, roughly the long-term average total return from the FTSE 100, and with all dividends reinvested, the money would rise to £293,427 by retirement without a single extra contribution.

That shows the power of compound growth. But while nearly £300,000 is a tidy sum, it won’t be enough to fund a comfortable retirement three decades from now. Someone starting with £25,000 at 35 has a solid beginning, but they’ll need to pick up the pace to reach their £1m goal.

FTSE 100 stocks build wealth

To hit that seven-figure milestone, our investor would need to contribute £450 a month. That might look daunting for someone juggling the financial responsibilities of midlife, but pension tax relief helps soften the blow. That £450 will only cost a 40% taxpayer £270, which shows why SIPPs are such an efficient long-term vehicle.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

I’d also suggest increasing contributions gradually over the years to accelerate growth. Personally, I prefer to buy individual shares rather than simply tracking the index, as that gives me a shot at delivering a superior performance. There are risks, but I reduce those by investing in a well-diversified mix of around 15-20 blue-chip stocks.

The long game

Building a £1m retirement pot takes time, discipline and a willingness to stick with the plan through good markets and bad. The earlier investors start, the easier the journey becomes. With regular saving, smart stock selection and plenty of patience, the end result could transform life in later years.

Realty Income stands out for its diversified, reliable cash flow and impressive 50-year operating history, making it a top contrarian pick.

The company boasts a strong dividend track record with 111 consecutive quarterly increases and a 4.2% annualized yield.

O’s massive $14 trillion addressable market and S&P 500 dividend aristocrat status offer significant long-term growth potential.

A key risk is valuation, as reliance on equity funding and limited upside could cap returns near 10%, especially in a downturn.

jabkitticha/iStock via Getty Images

Realty Income (NYSE:O), or the monthly dividend company, was recently released as our contrarian investment pick based on diverse and reliable cash flow. The company’s earnings, recently released, indicate a continued ability to source valuable transactions, which as we’ll see in this article, make the company a valuable investment as rates are expected to decline.

Realty Income Overview

The company is one of the largest REITs with impressive global operations.

Realty Income Investor Presentation

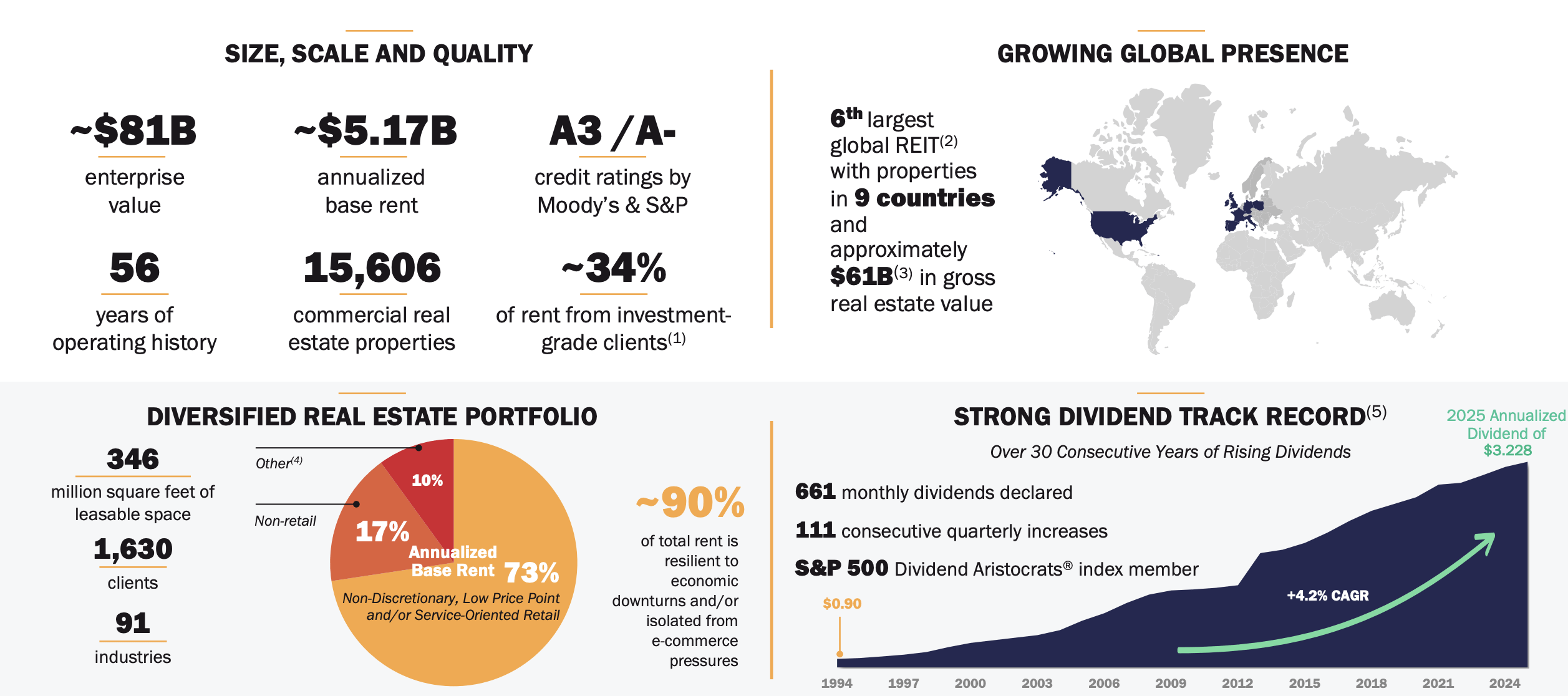

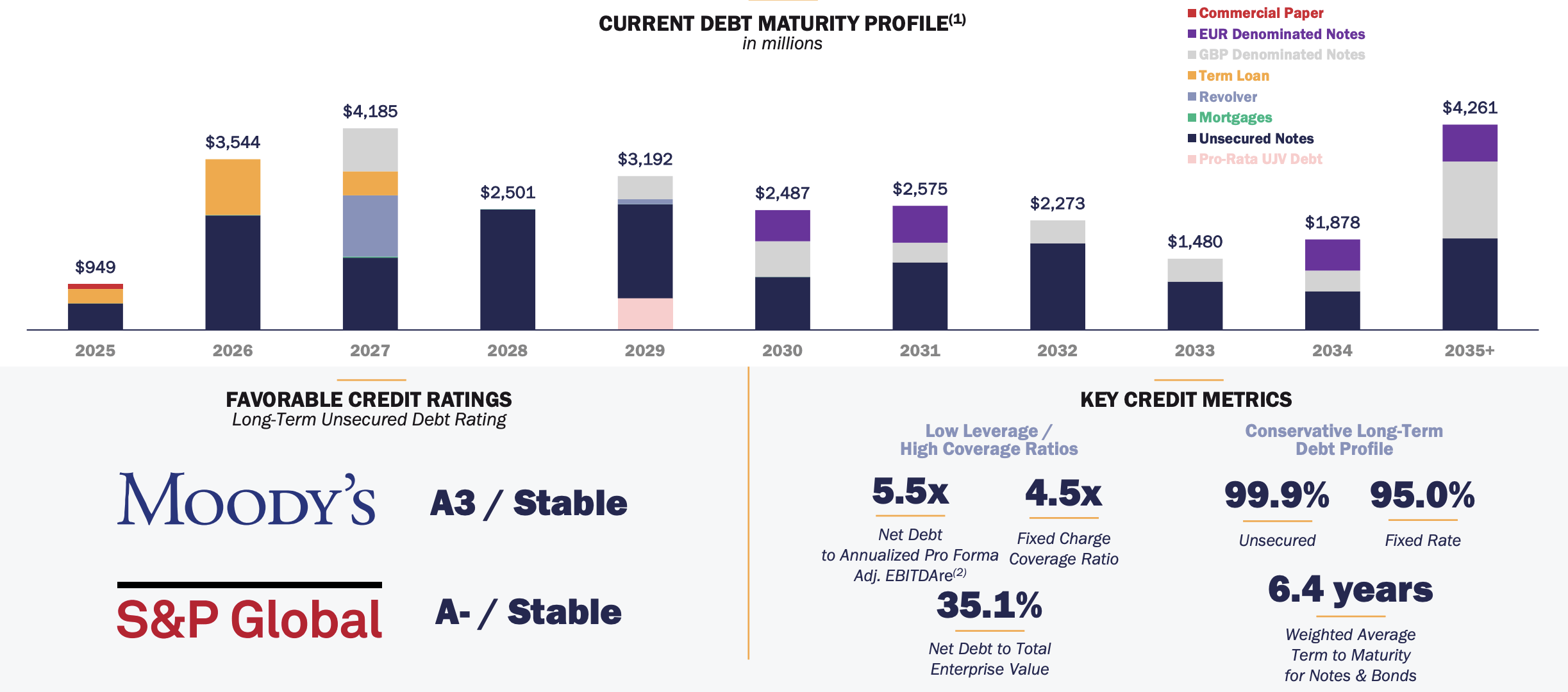

The company has more than 50 years of operating history with a ~$81 billion enterprise value and more than $5 billion in annualized base rent. Versus its market cap, that’s an almost 10% annualized based rent yield. The company’s business is spread across an incredibly high credit rating due to investment grade clients and more than 15 thousand commercial real-estate properties.

The company is known as the monthly dividend company with 111 consecutive quarterly dividend increases and 661 monthly dividends at a 4.2% annualized dividend yield. It’s a strong history of dividends from a diversified history.

Realty Income Investor Presentation

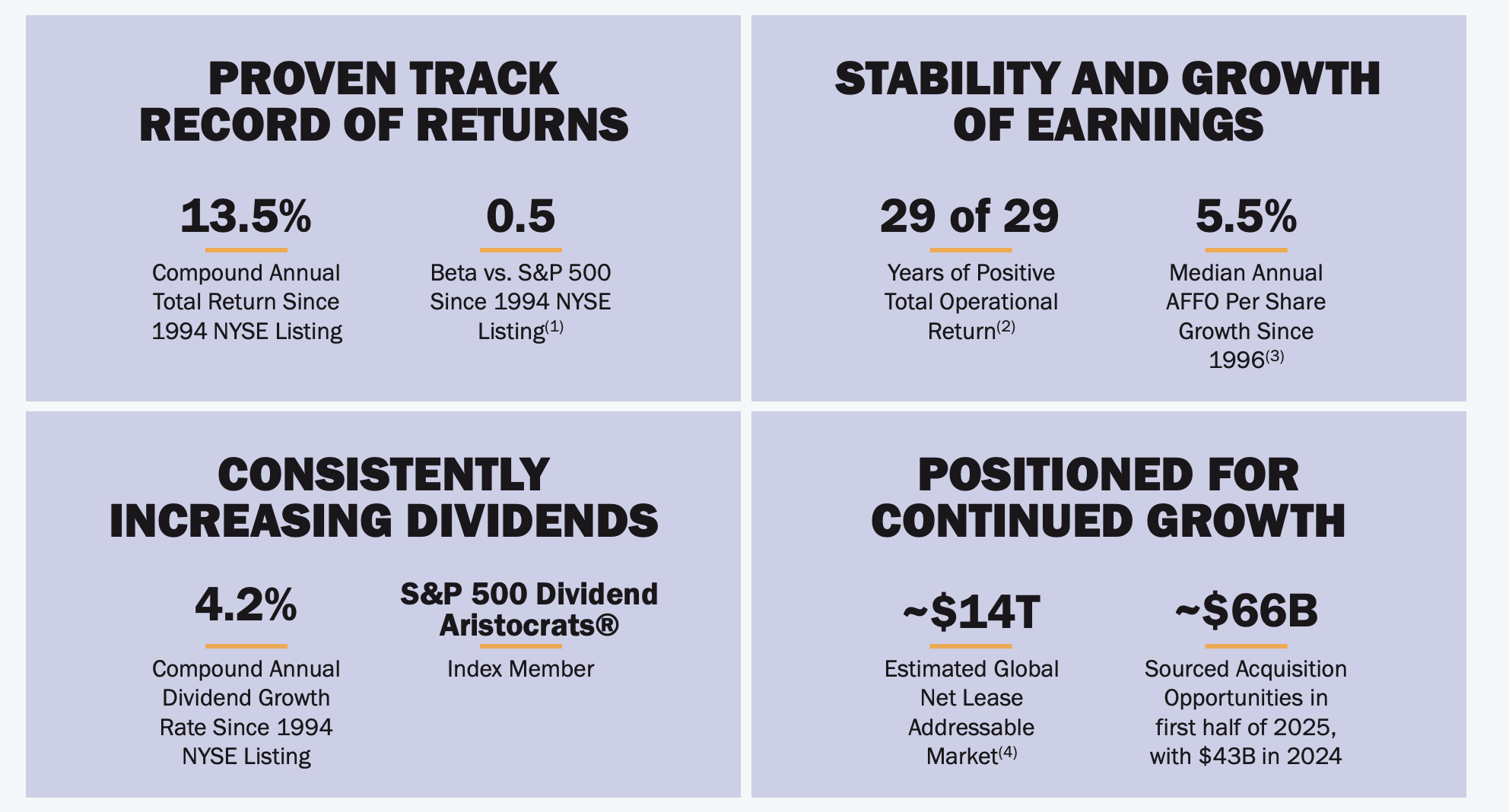

The company has returned 13.5% compounded annually since its NYSE listing with minimal volatility. Realty Income has managed to grow its median annual AFFO by 5.5% driving this, making the company a member of the S&P 500 dividend aristocrats. More importantly, the company has a massive addressable market versus its size.

The company’s estimated addressable market is ~$14 trillion, giving it continued room to grow despite its immense size.

Realty Income 2Q Results

Breaking out the specifics of its 2Q results, the company generated strong results.

Realty Income Investor Presentation

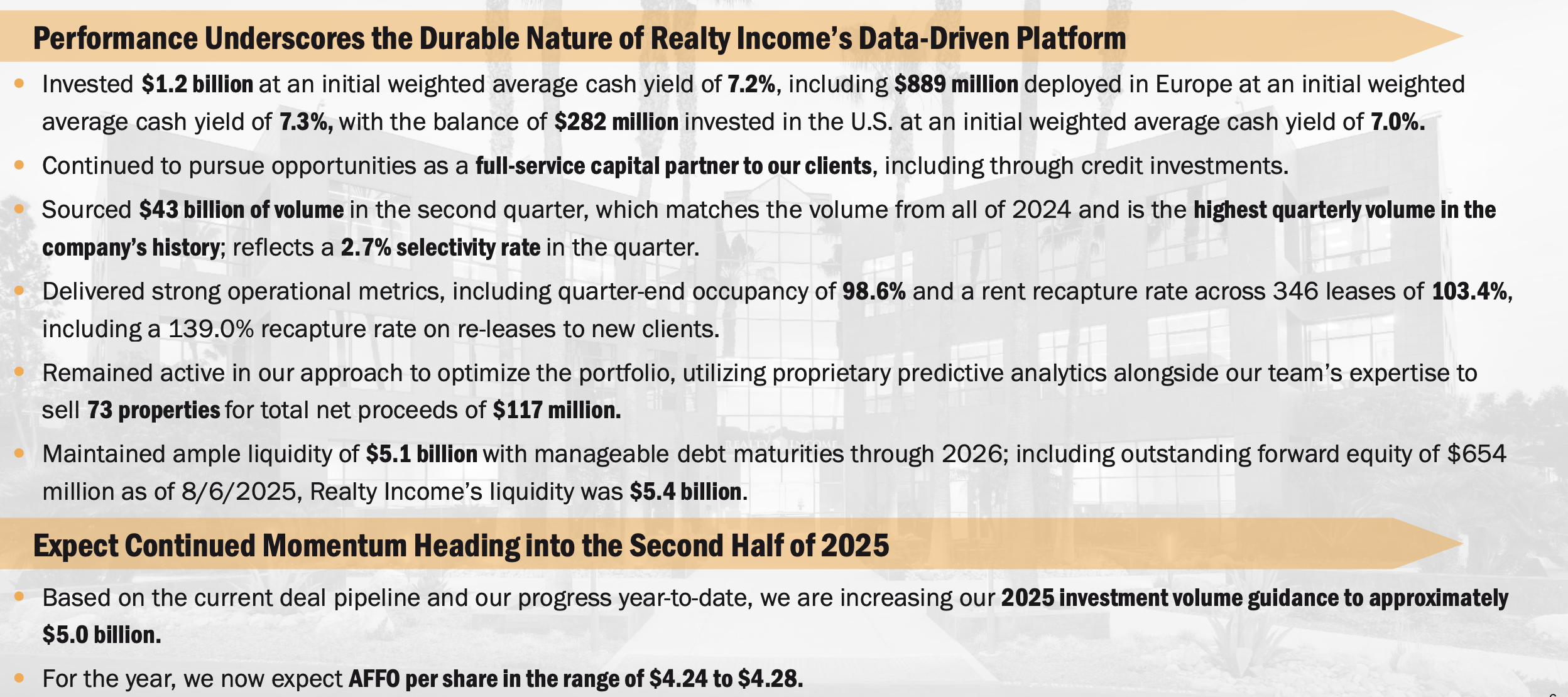

The company invested $1.2 billion in the quarter at an average 7.2% cash yield taking advantage of higher interest rates that enable it to lock in higher returns. Realty Income sourced $43 billion in volume, which shows that, despite its massive scale, it could maintain a 2.7% selectivity rate with 98.6% occupancy.

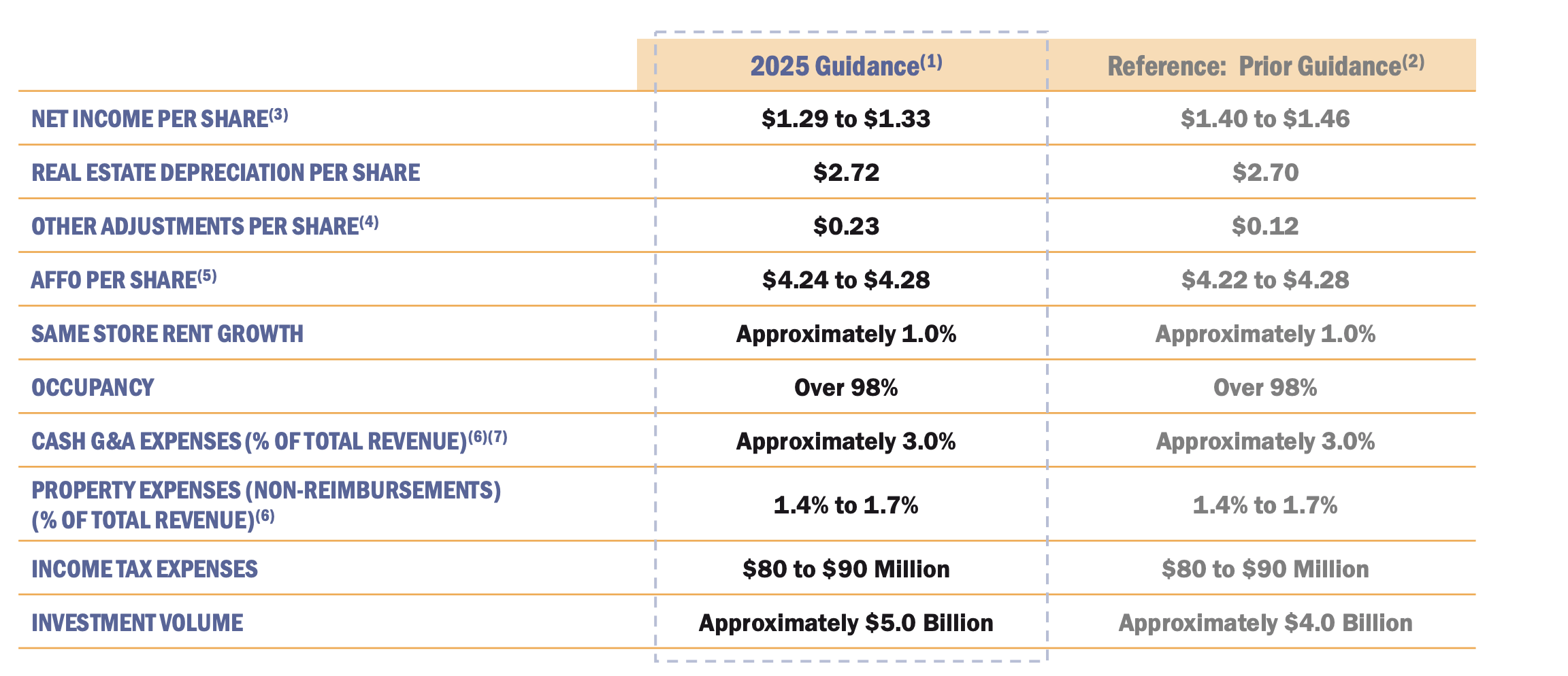

O had a 103.4% rent recapture rate, showing its ability to raise rents with higher inflation rates, and it’s continued to optimize its portfolio. Going into the 2H, the company expects to find additional investments with ~$5 billion in volume and ~$4.26 in AFFO.

Realty Income Investor Presentation

Overall, the company’s 2025 guidance is strong versus a $57.8 share price. The company expects 1% same store rent growth with flat AFFO / share and slightly lower net income. Property expenses and income taxes are expected to remain more than manageable while the company is guiding for higher investment volumes.

There is one concern here where the company’s 2024 AFFO was $4.19 / share indicating only 2% YoY growth not enough to support lofty dividend increases.

Realty Income Debt

Realty Income has one of the strongest balance sheets in the industry with low-interest rate debt.

Realty Income Investor Presentation

The company has 5.5x net debt to annualized pro forma adjusted EBITDA with $28 billion in net debt based on its enterprise value. The company’s debt is 99.9% unsecured and 95% fixed rate, both of which make it manageable with a 6.4 years weighted average term to maturity. With expectations for the FED to decline rates, the company can refinance debt at a lower rate.

The manageable debt load is expected to fund the company’s $5 billion sourcing for 2025 and enable AFFO to continue its growth.

Thesis Risk

The largest risk to our thesis is the company’s valuation. The company has a dividend yield of just under 5.6% and it uses dilutive equity to fund its business. The company expects to be able to achieve dividend growth in the mid single-digit range, but the best-case scenario here is ~10% return. With a downturn, it could be less, making the company a poor investment.

Conclusion

Realty Income is expected to see rates decline enabling the company to refinance its debt at a lower rate while continuing to earn strong returns from properties bought at a higher cap rate. The company has guided for increased acquisitions in 2025 as a result, acquisitions that it can comfortably afford to make. More so despite the size, the company has a large addressable market.

Realty Income is expecting to continue its growth and has an incredibly impressive track record of generating strong cash flow from these assets and using it to fund a multi-decade, growing dividend. Putting that all together makes Realty Income a valuable investment opportunity.

The market has reacted to both updates in a negative fashion.

The general chart interpretation is that when the price is above the cloud the sun is shining on your position but below the chart it’s raining on your parade.

In the cloud watch for the direction.

The reason the Snowball only invests in belt and braces shares.