If you used T56 as a core constituent of your Snowball, you would receive two payments a year with a total yield of 5.46%. If held in a tax free account you could buy and forget about the Gilt, it’s likely the capital value may fall a touch but as you intend to buy and hold forever it’s of no concern.

A minimum blended yield of 7% for your Snowball is recommended, as if this is re-invested at a yield of 7% plus this doubles your income in ten years.

If for comparison purposes only, you pair traded with NESF

The blended yield would be 16.5%, you have reduced the overall risk to your portfolio and achieved a yield of 8%. This could then be re-invested into your portfolio.

Two funds in Vanguard’s LifeStrategy range rose in popularity last week. Costing 0.22%, the version that has 80% invested in equities and 20% in bonds rose one place to fourth, while the 100% equities version rose three places to sixth. They are “funds of funds”, built using Vanguard’s own index funds, providing a useful one-stop shop for investors seeking global stock and bond market exposure.

0.44%, which rose three places to third. It has a dividend yield of 8.5% and owns wind farm assets across the UK.

The final riser was Fidelity Index World, which was a new entry in 10th. This fund was one of three global equity passive funds to make last week’s top collectives list. It tracks the MSCI World index of developed market shares for a 0.12% annual fee.

0.05% dropped in popularity last week but held on to their spots on the most-bought list. Respectively, they are actively managed portfolios of income and shares and growth shares.

UK equity income investment trust City of London dropped off the list.

Cash Will Be King Soon, 4 Out Of 5 Market Top Signs Are Here

Aug. 15, 2025

Summary

I’m selling into market strength, as underlying weakness and red flags suggest we’re near a market top, despite record index highs.

Key sectors like transportation, consumer discretionary, and real estate are showing signs of strain, while jobs data is weakening.

Market breadth is dangerously narrow, margin debt is at record highs, and speculative trading is rampant—classic signals of a topping market.

I’m raising cash now, believing caution is wise; cash will be king when the next market pullback offers better opportunities.

Daniel Grizelj/DigitalVision via Getty Images

The stock market is doing great and it has been making new record highs. The momentum could carry it higher for a while, but I am using this as an opportunity to sell into strength, because not all is well when you dig deeper and beyond the major indexes. I am not a huge bear, and I am keeping my core holdings for the long term, but I am skeptical and I believe cash will be king as soon as this Fall. Let’s take a closer look below at some points of concern and also at 5 of the indicators that often signal a market top.

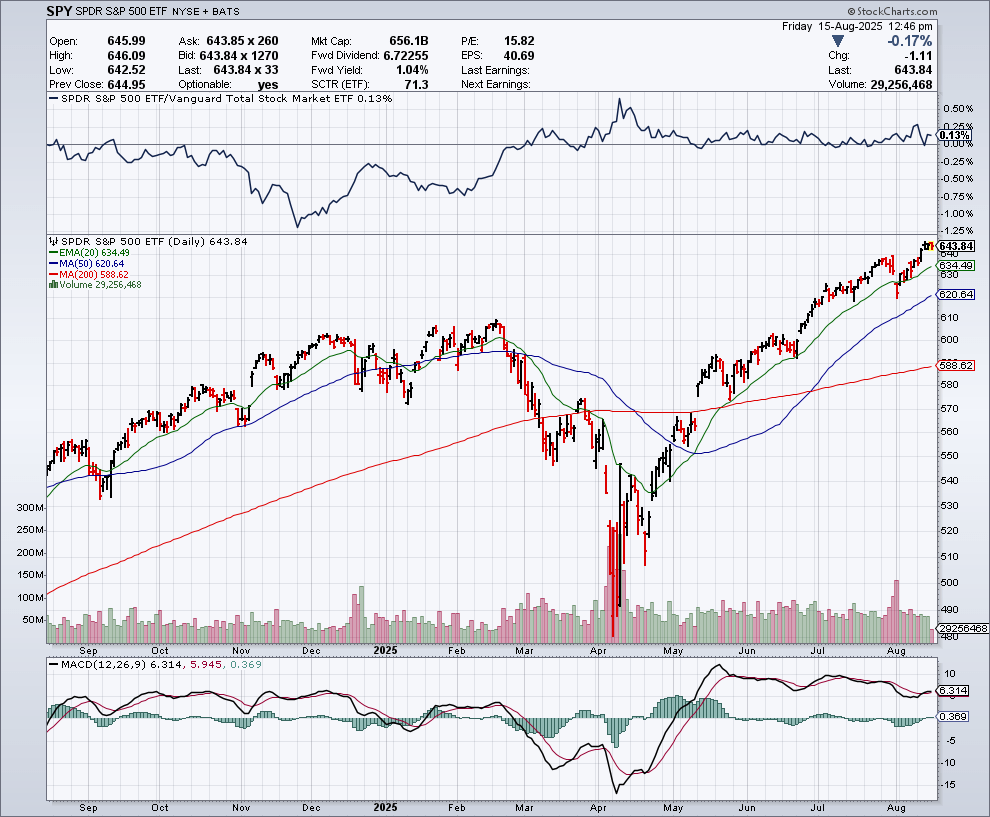

The Chart

When I look at the chart of the S&P 500 Index (NYSEARCA:SPY) below, it looks like we are potentially at or near the blow-off top stage of this bull market. I certainly do not look at this chart and say that this is when I want to be adding more money and risk to my portfolio.

StockCharts.com

Why Things Are Not So Great Under The Surface

The market strength in terms of the indexes looks great but there is underlying weakness in some important segments of the market such as the transportation stocks and consumer discretionary. For example, UPS (UPS) is trading near 52-week lows. FedEx (FDX) is way below the 52-week high. A major European container shipping company recently warned that high global tariffs could slow down volumes in the coming months. When things aren’t being shipped, it means they aren’t being sold and this weakness in shipping volumes is a major concern.

The real estate market appears to be in correction mode in many parts of the country. I am seeing price cuts where I live in California that I have not seen in years. I am also seeing homes sit on the market for months in many cases. Companies like Whirlpool (WHR) recently reported challenges with tariffs and weaker than expected results. Lower home prices could lead to weaker consumer sentiment as a potential negative wealth effect from real estate takes its toll.

The jobs market seems to be shifting rapidly and this could be the start of a new and very negative trend. On August 1, the Bureau of Labor Statistics released the jobs report which showed July non-farm payroll growth was just 73,000. This was much lower than the expectations for 110,000. But it gets worse, because payrolls for May and June were revised down by a total of 258,000. This means the job market weakness really started earlier this year and we are only starting to recognize the start of this potentially new trend now.

A Tariff 2.0 Growth Scare Could Be Coming

The stock market recovered from a brutal decline in April after President Trump announced the Liberation Day tariffs. The stock market is back at new highs, and consumers have not seemingly been hit with big price increases. So, it now seems like we can have a huge increase in tariffs that brings billions of dollars in new revenues to the U.S. Government and there is really no impact or downside.

However, this could be false hope, and we could be in the “quiet before the storm” period. That’s because there is a major lag time for tariffs to take effect and to hit with full impact. We have to realize that many countries were able to defer tariffs during the negotiation period and many companies stockpiled raw materials and other items. Many businesses have also held back on raising prices because there has been uncertainty as to whether or not tariffs would remain high or be negotiated away. A recent CNBC article says that higher prices might be coming in September, according to some analysts and this is based on seasonal inventory patterns and products that are working their way through the supply chain system. I believe it is way too early to suggest that we are in the clear when it comes to tariffs and the potential inflationary impact.

A Number Of Indicators Of Market Tops Are At Red Flag Levels Now

They often say that no one rings a bell at the market top, but there are multiple indicators that seem to be ringing a bell, for anyone who is willing to listen:

1) Narrowing Market Breadth: A healthy bull market has broad participation, but this bull market has been very dependent on mega-cap tech stocks which could be a warning sign of trouble ahead. A recent Goldman Sachs (GS) article points out that market breadth has been too narrow and it states:

“Although the S&P 500 has reached record highs, the median stock within the index is more than 10% below its 52-week high. This has lowered market breadth—a measure of how widely a market’s performance is reflected by its constituents—to its lowest level since 2023, according to Goldman Sachs Research’s market breadth indicator.

In the past, sharp declines in market breadth have often signalled below-average returns and larger-than-average drawdowns ahead.”

2) Excessive Euphoria And Margin Debt: We are hearing things that suggest we are in a new “Golden Age” and we are in a new era with AI and humanoid robots coming, all of which can seem limitless in terms of potential. Past market tops also had concepts that were touted as having incredible potential, such as the Internet/dotcom bubble. I believe there is excessive euphoria now and this often leads to investors believing that buying stocks is a no-can-lose proposition over the long run, even to the point where they are borrowing money to buy stocks. According to the latest statistics from FINRA, margin debt levels just went over $1 trillion in June 2025 and this is a new record. Since margin debt levels often hit record levels at or near market tops, I view this as another bell or warning signal that is going off right now.

3) Rising Interest Rates: This is often a problem for the stock market, but we are not seeing rising rates now, so this is the one indicator that is neutral and not ringing a bell. However, there is a case to be made that interest rates have been held up high for too long and that the damage might already be done. I think some of this damage is starting to show up in the jobs data.

4) Declining Economic Indicators: Earlier in this article, the weakening labor market was discussed, and this could be a major indicator of economic weakness, but there are others as well. New factory orders and durable goods orders fell in June and the ISM Manufacturing PMI showed in July that manufacturing is in a state of contraction. The ISM services index also declined in July, which is yet another potential warning sign. Lumber prices have plunged in recent weeks and this could be another sign of looming weakness in the economy.

5) A Surge In Speculative Trading: In the past couple of weeks we have seen a renewed meme stock rally whereby investors are buying into highly speculative stocks, which in some cases have very poor fundamentals. This is yet another potential red flag warning sign as this type of behavior is often seen at or near the market top. The record levels at which many cryptocurrencies trade is another sign of speculation. The stock market and other assets classes have clear signs of froth in certain areas and that will likely need to be flushed out.

In Summary

There are multiple signs that seem to suggest we could be at or near a market top. I definitely think it makes sense to be cautious when others are being greedy, and even using record levels of margin debt to buy stocks. I also believe that new stock market highs are being fuelled by a narrow part of the market and that this is masking some of the underlying weakness that has just started to appear in some of the manufacturing and services data as well as the jobs data. I think this is a great time to raise cash, and that cash will be king again and much smarter to deploy in the next big market pullback.

Just turned 40? Here’s how much you could have by retirement if you invest £500 a month via a SIPP

Worried about having enough money to retire on ? Investing regularly with a SIPP could potentially build a multi-million-pound nest egg!

Posted by

Zaven Boyrazian, CFA

Published 17 August, 7:21 am BST

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The Self-Invested Personal Pension (SIPP) is one of the best retirement preparation tools available to British investors. While taxes do eventually re-enter the picture, the elimination of dividend and capital gains tax, along with income tax relief, drastically accelerates the wealth-building process. So much so that even when starting later at the age of 40, it enables investors to accumulate a substantial nest egg. Here’s how.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Potential retirement wealth

Let’s assume an investor has just turned 40, is planning to retire at 65, and is currently in the Basic income tax bracket, paying a rate of 20%. Depositing £500 into a SIPP entitles them to 20% tax relief, transforming this monthly lump sum into £625. And investing this capital at the average stock market return of 8% a year for 25 years, compounds into a £594,392 pension portfolio.

Looking at the latest data from the Office for National Statistics, that’s just over four times what the average 65-year-old has saved up in 2025. And when following the 4% withdrawal rule, it’s enough to generate a retirement income of £23,775 a year.

Combining with the extra £11,973 from the UK State Pension, this simple investing strategy would put someone on the path to having a £35,748 passive income. And according to the Pensions and Lifetime Savings Association, that’s just over the £31,700 threshold needed to enjoy a moderate retirement in 2025.

Yet, when factoring in inflation, that threshold’s bound to rise over the next 25 years. Therefore, investors may need to aim a bit higher.

Brett Owens, Chief Investment Strategist Updated: August 14, 2025

The market-at-large is expensive by historical metrics. So let’s look past the pricey, low-yielding ETFs in favor of cheap dividend stocks.

That’s right, good ol’ value investing bargains. With high yields too! We’re talking about divvies of 5%, 8% and even 11% that we’ll discuss in a moment.

The spring market dip sure was brief, wasn’t it? The S&P 500 sank into near-bear territory in roughly a month, then snapped back just as quick.

Now? If We’re Buying the Market, We’re Buying Even Higher

In doing so, Mr. and Ms. Market took valuations to high levels. The S&P 500’s forward price-to-earnings (P/E) ratio of 22.1 remains in rarefied air, last reached during the COVID rebound, and before that, the dot-com bubble.

Which is fine. We’ll leave the 22 P/Es to the vanilla investors while we focus on bargains with respect to two “cash is king” metrics:

Big dividends: These generous stocks dish out 4x to 9x the market’s yield.

Cheap price-to-cash-flow: These companies are priced dirt cheap with respect to the cash flow they generate.

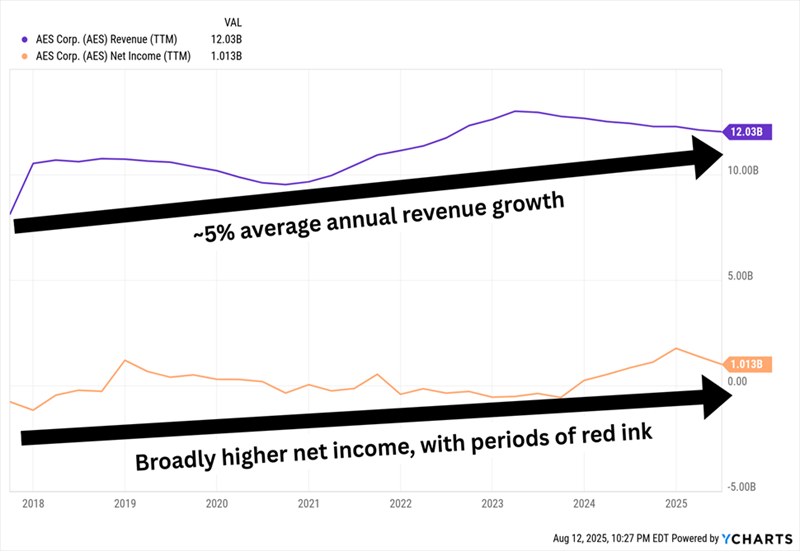

Let’s start with Virginia-based electric utility AES Corp. (AES, 5.5% yield), which we recently discussed as a low-beta name. This means AES, being a safe, stodgy utility, is more insulated from market pullbacks than run-of-the-mill dividends.

AES also has upside potential. Its renewable energy-selling business gives it growth potential that many utility stocks don’t have.

Potential, But So Far, It Hasn’t Shown Up Much in Practice

It’s also cheap. AES trades at a cheap 5 times cash-flow estimates, as well as a 0.6 PEG that implies it’s also cheap compared to its growth estimates. (Remember: A PEG under 1.0 signals that a stock is inexpensive.) The stock yields more than 5%, to boot, which is better than the already generous utility sector.

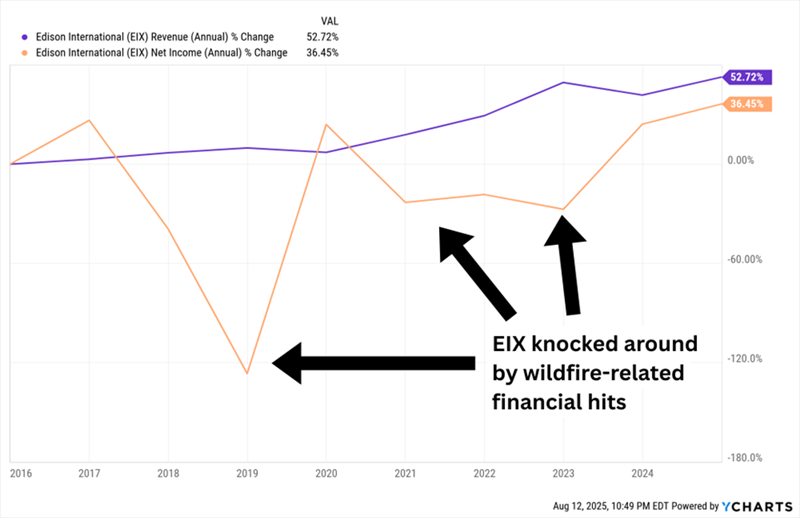

Edison International (EIX, 5.9%) is another utility company—this one more typical of the sector. It’s the parent of regulated utility Southern California Edison (SCE), which serves more than 15 million customers and generates much of its electricity from renewable sources including solar, wind, and hydro. It does, however, have a second business—Trio (formerly Edison Energy), a global energy advisory firm that serves large commercial, industrial and institutional organizations.

Unlike other utilities, however, EIX is a bit more “exciting.” It spent years in court fighting litigation over wildfire damage and ended up having to pay multiple billion-dollar-plus settlements. And the legal drama has returned in 2025. Shares have lost more than a quarter of their value, with most of that coming in January amid Los Angeles County wildfires, including the massive Eaton Fire, which prompted multiple suits against SCE over allegations that the company had “violated public safety and utility codes and was negligent in its handling of power safety shut-offs.” SCE is also being investigated in connection with the Hurst Fire.

In Fact, Wildfire Woes Have Been Par for the Course

If, for a minute, we closed our eyes and ignored all that, there’s a lot to like about Edison. It’s expected to generate decent top-line growth and a significant snap-back in profits over the next couple years. The big drop in shares has launched EIX’s yield to nearly 6%. It trades at just 3 times cash-flow estimates. And its PEG, which at fractionally under 1 suggests the stock is only mildly underpriced, is substantially down from the nearly 3 it traded at when I evaluated the stock a couple years ago.

But we can’t ignore the fire liabilities—they’re why EIX’s valuations are so low. That makes Edison a much bigger high-risk, high-reward gamble than the average utility.

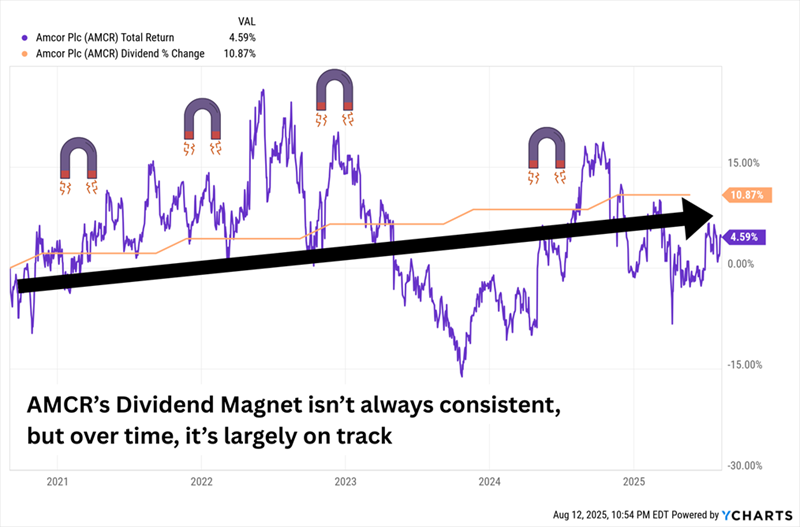

Amcor (AMCR, 5.2% yield) is technically a cyclical stock, but it acts defensively. That’s because, as a packaging specialist, it’s in the business of—well, other business’s business. It makes everything from high-barrier paperboard trays for beef and meats to glass dressing bottles to overwrap for home and personal care. And its applications go far beyond the grocery store: Amcor’s products are used in garden and outdoor products, agriculture, pet care, healthcare, even building and construction. So Amcor is simultaneously a play on the broader economy and all the businesses it supports, but it also fills a vital need across a diversified set of companies.

AMCR stands out for a few reasons:

It’s a Dividend Aristocrat with a 5%-plus yield, which is rare. The hallowed group of dividend growers know how to stack pennies over time, but their headline numbers often leave a lot to be desired.

Amcor’s shares tend to be less volatile than most.

The stock is cheap, at least as far as cash flow is concerned; P/CF is roughly 6x right now. It’s a little less attractive by other metrics; its forward P/E (12) is so-so, and its PEG (1.3), while cheaper than the market, is still a bit overpriced.

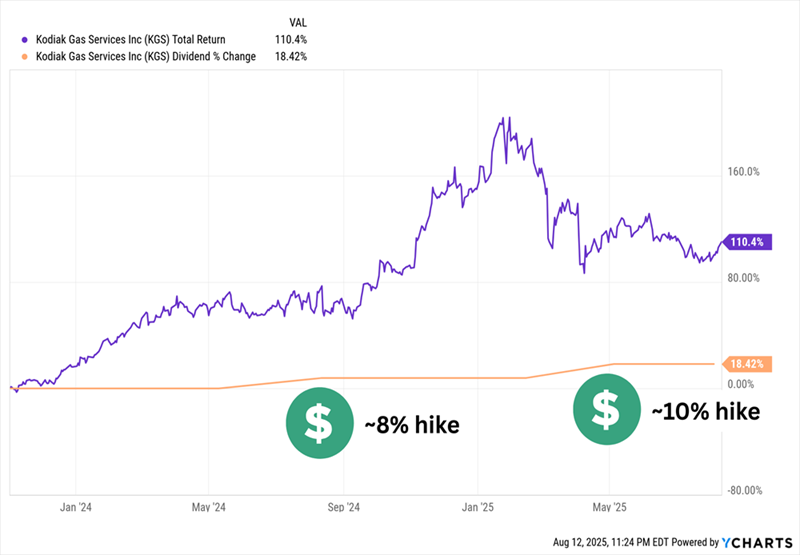

Kodiak Gas Services (KGS, 5.2% yield) is an energy services firm that provides natural gas compression services, mostly in the Permian Basin of Texas and New Mexico. Its compression units are critical to upstream and midstream natural gas firms, so it’s able to secure multiyear, fixed-revenue contracts. There’s nothing novel about the business model, though. Like other energy services firms, if natural gas/liquefied natural gas (LNG) is in demand, Kodiak will be in demand, so the fact that global LNG demand is expected to grow over the next few years bodes well for KGS.

That’s in large part because Kodiak is extremely well-positioned to capture that growth. In late 2023, KGS announced it would acquire CSI Compressco LP to create the industry’s largest compression fleet. Kodiak’s fleet is young, too (read: less maintenance and replacement costs).

There’s not much stock history to examine, however. Kodiak is a relatively new issue that went public just a few months before the CSI announcement. But the company has started a dividend and raised it twice since then, including a nearly 10% improvement announced in April 2025.

A Stock Doubler-Plus + A New and Rising Dividend. Nice Start!

Meanwhile, its yield has wafted up to over 5% amid energy’s weakness this year—and left shares relatively cheap. KGS trades at roughly 6 times cash flow estimates and a low PEG of 0.13.

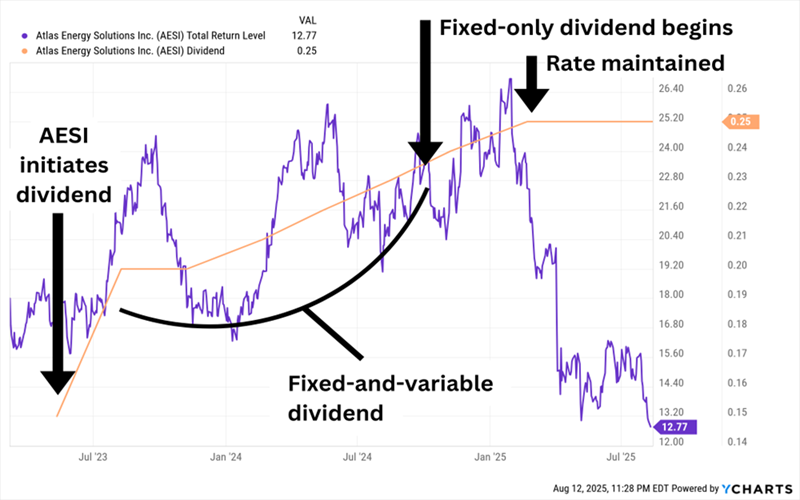

Atlas Energy Solutions (AESI, 8.4% yield) is another Permian Basin energy equipment and services firm, this one providing transportation and logistics, storage solutions, and contract labor services to oil and natural gas E&P firms, as well as other oilfield services companies. Its most important offering is mesh frac sand used in hydraulic fracturing (fracking). I had been keeping tabs on it because of its unorthodox streak of dividend hikes, but that streak stopped earlier this year.

The Trap Door Opened Soon After AESI Stopped Raising

It’s not ideal. Nor is the fact that AESI shares have been hammered to the tune of 45% this year. Again, energy services haven’t had a great 2025, but Atlas has been downright miserable amid slower-than-expected U.S. completion activity and droopy frac-sand prices. If there’s any silver lining to that, it’s that AESI shares now trade at just 5.7 times estimates for cash flows, as well as an attractive PEG of 0.75.

The dividend at least appears to be safe, too. While things look bad from an adjusted earnings perspective ($1.00 in dividends annually vs. forecasts for just 25 cents this year), Atlas has more than enough FCF to cover the payout. Example: Last quarter, it generated $48.9 million in adjusted FCF while paying out $30.9 million. Those cash flows are substantial because AESI is a low-cost operator—crucial for survival in this industry. But like any energy services provider, Atlas needs commodity prices to cooperate.

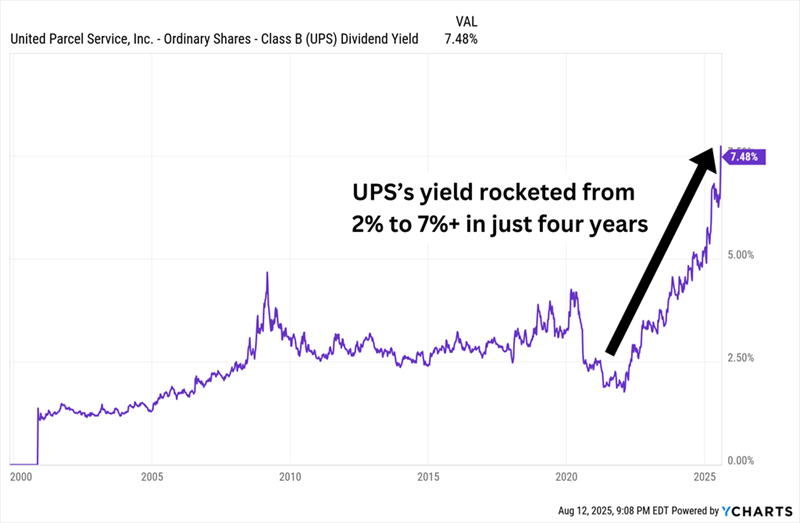

It’s unusual for a blue-chip stock like United Parcel Service (UPS, 7.5%) to yield north of 7%, but it’s also rare for a blue-chip stock like UPS to have its shares hemorrhage so much without a recession or broader bear market.

Lower-margin e-commerce volumes, higher costs because of its unionized workforce, and a weak freight environment hampered the company in 2024.

Then in early 2025, it spooked investors with a weak 2025 forecast and announced that—in hopes of shifting away from those lower-margin volumes—it would drastically reduce its business with Amazon (AMZN), which accounted for roughly 10%-12% of annual UPS revenues. The April tariff announcement also hit shares hard.

The result? UPS shares have lost nearly half of their value in just two years.

The upshot? UPS trades at roughly 8 times cash-flow estimates and has never offered a better yield in its 26 years of trading.

Sadly, Dividend Growth Had Little to Do With It

Is UPS a dividend trap? Perhaps. The company pulled its full-year revenue and profit forecasts in April, and didn’t bring them back in its late July report.

Meanwhile, Wall Street is expecting a roughly 15% drop in adjusted earnings, to $6.61 per share. That specific number matters: UPS has a target dividend payout ratio of approximately 50% of prior-year adjusted EPS. It currently pays $6.56 across four quarterly dividends. (That’s 99%!) CEO Carol Tomé continued to signal commitment to the dividend in the earnings call—“UPS is rock-solid strong and so is our dividend. The UPS dividend is backed by solid free cash flow and a strong investment-grade balance sheet,” she said—but if the delivery giant continues to struggle, simple numbers might force management’s hand.

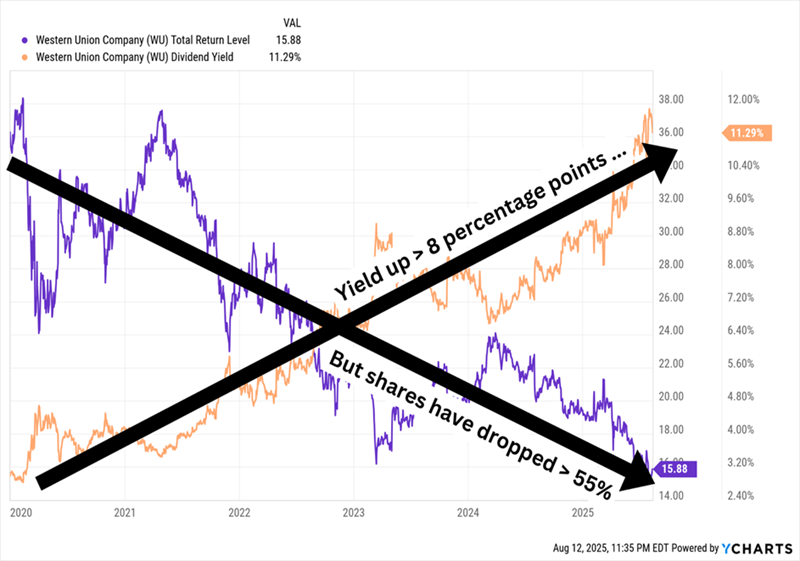

Western Union (WU, 11.3% yield), somehow, is still in business. Payment apps like PayPal, Venmo and Zelle have been taking business from the “OG” of money transfer. WU boasts a big yield but for the wrong reason—its divvie looks big because shares are (deservedly) way down!

Western Union Has Been Headed South for Years

WU, to its credit, has launched an initiative called “Evolve 2025” in which it’s rolling out new products, improvements and an operational efficiency program. It’s also expanding its digital wallet offerings in Mexico and Singapore. And its latest move, announced just a couple days ago, is the $500 million acquisition of Miami-based International Money Express (IMXI), aka Intermex, which serves some 6 million customers who send money from the United States, Canada, Spain, Italy, the United Kingdom, and Germany to more than 60 countries.

But c’mon man—this dog is dead. The business trades for 4x cash flow and a sub-5 forward P/E, but who cares? Not me.

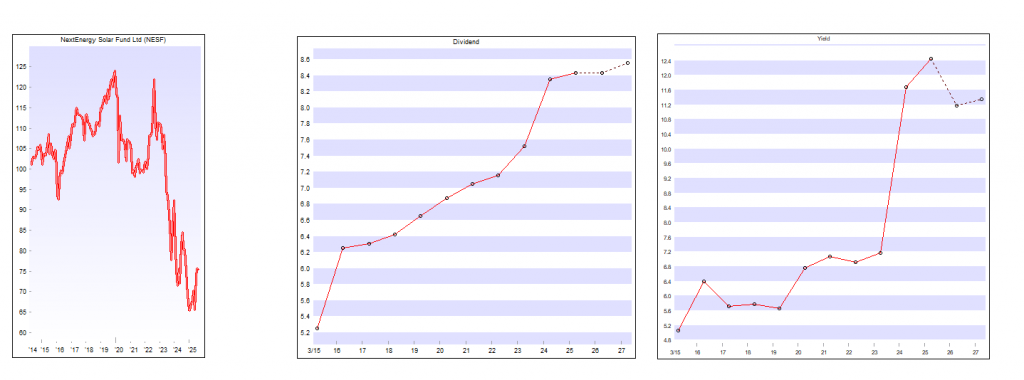

Dividends received £1,748, current yield eleven per cent. If NESF continues to pay a dividend in nine years the Trust should be producing income at a zero, zilch, nothing cost. Also unless NESF is taken over the Snowball should be this time next year be 25% closer to achieving the holy grail of investing.

NESF could be producing income at zero cost and the dividends re-invest into the Snowball should be producing income around 7% another £850.00.

The ‘belt’ is printing a small loss but the ‘braces’ are printing a good profit.

Remember the market could take back all the profit, so it’s often best to re-invest into the Snowball, even at a lower yield.

The Directors of TwentyFour Select Monthly Income Fund Limited (“SMIF“), the listed, closed-ended investment company that invests in a diversified portfolio of credit securities, have declared that a dividend of 0.5 pence per share will be paid, in line with the Prospectus, representing the regular monthly targeted dividend for the financial period ended 31 July 2025 as follows:

Ex-Dividend Date 21 August 2025

Record Date 22 August 2025

Payment Date 5 September 2025

Dividend per Share 0.50 pence (Sterling)

No special dividend announced, with any special dividends the blended yield is around 8%.