Published on March 24, 2026

by John Baron

Iam sometimes asked why the portfolios, in pursuing their individual remits, remain invested across the various asset classes – particularly when I am cautious on markets, and the portfolios are underweight equities relative to corresponding benchmarks. Why not maintain higher cash balances? Other related questions refer to the portfolios’ higher yields relative to benchmarks. The answers are multi-layered, but a key factor is one which is often underestimated by investors – the magic of compounding. This was allegedly described by Einstein as the eighth wonder of world. It is perhaps more relevant than ever given the current geopolitical and economic challenges, and volatile markets.

Compounding in action

Compounding is the regular reinvesting of dividends with the effect of creating higher total returns (capital gains/losses, plus income) over time. The policy of reinvesting dividends to buy more shares, which themselves pay dividends, and then reinvesting those, and so on, significantly increases portfolio returns. Finding and reinvesting dividends is a key determinant of growing wealth over time and is less problematic than short-term trades in the hope of enhancing capital gains. To fully harvest these dividends, investors need to stay invested – another reason why time in the market is better than market timing.

The extent in the difference in total returns is worth highlighting. Legendary investor Jeremy Siegel highlighted in his 2005 book The Future for Investors, that over the previous 130 years, 97 per cent of the total returns from stocks came from reinvested dividends. He suggested $1,000 invested in 1871 would have been worth $243,386 by 2003, but the figure rises to nearly $8mn had dividends been reinvested.

A shorter timeframe is perhaps more helpful. Research suggests $10,000 invested in an S&P 500 index fund in 1960 would be worth just over $1mn by 2025 by capital growth alone, but this would have increased to over $6.4mn had dividends been reinvested – more than six times higher.

Investors Chronicle

For compounding to work its magic, time and a good rate of return are required. The earlier an investor can start investing, the greater the compounding effect. By its nature, the magic works best towards the end of a decent period, when funds have accumulated. It is also important that a portfolio’s asset allocation and risk profile are adjusted as an investment journey progresses towards its financial objective. However, in general, an investor should if able start early, avoid being buffeted by market noise and remain invested, keep investment costs low and refrain from spending their portfolio dividends – so as not to interrupt the magic of compounding. They will then usually be surprised at how well they’ve done.

Investors may also be surprised at how well the investment style of their equity holdings has performed. If it is right that stagflation is now upon us, it is worth remembering that history suggests low growth combined with higher and more volatile inflation usually favours value stocks. These tend to include the well-managed and financially sound income stocks increasingly sought by fund managers. After the Alice-in-Wonderland world of quantitative easing and artificially low interest rates distorted both reality and asset prices, which in turn favoured growth stocks, value has once again regained its crown. Dividends are back in fashion and for good reason – in an unpredictable world, they should also offer some solace.

While never complacent, adherence to this wonder has helped the two portfolios covered in this column outperform their benchmarks since their introduction in 2009. Indeed, it is an approach we adopt when sharing with members how we manage all 10 live investment trust portfolios on the website www.johnbaronportfolios.co.uk. They achieve a range of investment strategies and income levels – this range ensures there is a portfolio for most investors, from those first investing to those approaching a financial goal. The holdings below are held in the 10 portfolios and offer some good yields. They cover a range of sectors, including equities, corporate bonds, renewable energy, commodities, specialist lending and commercial property.

Dividends in action

Henderson High Income (HHI)

This trust focuses mainly on larger UK companies to generate a high and growing level of income, although the manager has latitude to invest across the market cap spectrum, and currently has 10 per cent of its assets invested overseas. Since David Smith took over more than 10 years ago, the company has enjoyed a good record over most timeframes relative to its benchmark (80 per cent FTSE All-Share index/20 per cent ICE BofA Sterling Non-Gilts Index). The progressive dividend policy is supported by meaningful revenue reserves – the dividend equating to a yield of 6 per cent at time of writing. The company’s bond exposure assists with some of the portfolios’ objectives by complementing existing bond exposure.

Murray International (MYI)

The fund seeks income from an international portfolio of mostly blue-chip equities, while also looking to grow capital and dividends in excess of inflation. The portfolio’s composition has broadly a one-third split between North America, Europe including the UK, and Asia Pacific and Latin America – which fits well with our view of the relative merits of the markets involved. Recently announced results for 2025 show a total return of 21.9 per cent, against 12.6 per cent for its benchmark index. Asia in particular assists with the company’s income remit, with the company’s dividend equating to a yield of 3.6 per cent.

CQS New City High Yield (NCYF)

It seeks a high level of income by focusing on fixed-interest securities at the upper end of the yield curve, which should be more resilient should we be right about inflation, while supplementing this with a modest exposure to mostly high-yielding equities and convertibles. These latter investments assist in maintaining the company’s record of modestly increasing dividends over time, with help from its not-insignificant revenue reserves. The long-serving and respected manager, Ian ‘Franco’ Francis, has an excellent record of stewardship, with total return performance among the best in its peer group. Meanwhile, the 4.5p dividend equates to a yield of 9.1 per cent.

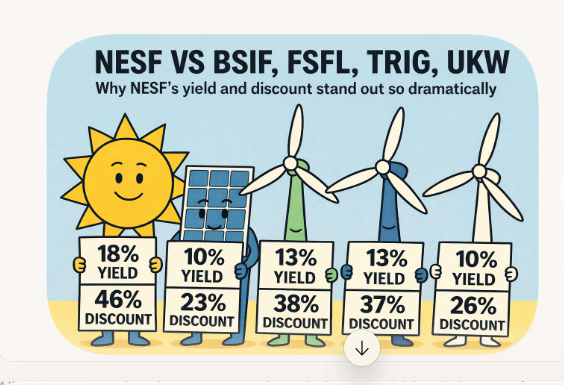

Foresight Environmental Infrastructure (FGEN)

The fund invests to provide a sustainable, progressive dividend alongside long-term capital preservation courtesy of a highly diversified portfolio of environmental infrastructure assets which are aligned with decarbonisation and resource efficiency. Around 70 per cent of the portfolio is in renewable generation, with the balance in complementary infrastructure, making it one of the most diversified vehicles in its peer group. The strategy focuses on long-term, stable and often inflation-linked cash flows, and currently supports a high, well-covered dividend – despite sector-wide valuation pressure and a wide discount.

Indeed, strong dividend cover of around 1.2 times, low gearing and a comparatively high and therefore conservative discount rate suggest, financial resilience. A key differentiator is the company’s trio of ‘growth assets’ – a UK controlled-environment glasshouse, the CNG biomethane refuelling network and a Norwegian land-based aquaculture facility. These are ramping up operations and are targeted for disposal in due course to crystallise capital growth and recycle proceeds into new opportunities across the energy transition space, without the need for additional fundraising. Meanwhile, the dividend equates to a yield of 11 per cent.

CQS Natural Resources Growth & Income (CYN)

It has an excellent record of generating capital growth and income, predominantly from a portfolio of smaller mining and energy companies. More so, the company is top of its peer group under the stewardship of its respected and long-serving managers, Keith Watson and Robert Crayfourd. Profits have recently been taken in precious metals (while remaining their largest exposure) in favour of increased weightings in oil and gas – the rebalancing being well-timed, having taken place before the US attack on Iran. We also favour the company because the enhanced dividend policy pays 8 per cent of net asset value (NAV) via quarterly distributions of 2 per cent of the preceding quarter-end NAV.

The managers have recently resigned from Manulife CQS Investment Management and are now serving their three-month notice period with no expected disruption to investment process or operations. They have also resigned from its sister funds Golden Prospect Precious Metals (GPM) and Geiger Counter (GCL), both being portfolio holdings. Given these managers’ excellent and consistent performance and stewardship of shareholders’ funds over many years, we will be voting to follow the managers in each case to their new management company – if, and when, we are given the opportunity to do so. Good fund managers deserve support.

Biopharma Credit Investments (BPCR)

This fund specialises in lending to the life sciences industry with investments secured by rights and cash flows from the sales of approved products and not early-stage or pre-approval products. This mitigates risk. The company has performed well over time. Because of its more defensive nature (ie the portfolio holds debt, not equity), the company assists those seeking diversification. In addition, it generates a high income, and this is often supplemented by royalty investments, which help to fund special dividends in addition to the regular dividend of 7¢ a share. A recent dividend announcement brings the total for the year to 9.95¢, which represents a yield of 10.5 per cent at current exchange rates.

Schroder Real Estate Investment Trust (SREI)

It seeks an attractive level of income and capital growth from a diversified portfolio of good quality UK commercial property assets mostly outside the south-east. The company is overweight the higher growth multi-let industrial and retail warehouse sectors, which we continue to favour. Importantly, the company’s debt has a maturity profile of around eight years at an average interest cost of 3.5 per cent, with the majority of this either fixed or hedged against movements in interest rates. As such, the company delivers a sustainable and growing level of income that currently equates to a yield of 7.2 per cent.

Leave a Reply