There Is No De-Escalation

Mar 25, 2026

Eugenio Catone

Summary

- Current market optimism over U.S./Iran de-escalation is likely misplaced, as both sides’ demands remain irreconcilable and military escalation continues.

- Despite President Trump’s optimistic statements, Iran and the U.S. appear far from agreement, with each demanding terms the other cannot accept.

- I remain bullish on oil and the U.S. dollar and short-term bearish on gold and global equities, given persistent geopolitical risks and ongoing troop deployments.

- Historical analogs suggest the conflict’s market impact is far from over, with oil and equities yet to reflect full downside risk.

The market wants to follow President Trump

Markets desperately would like to believe that the U.S./Israel–Iran conflict is about to end anytime soon, and President Trump’s recent statements fueled the optimism.

They’re talking to us, and they’re talking sense. It all starts with, they cannot have a nuclear weapon. They want to make a deal so badly, you have no idea how badly they want to make it. We’ve won this war.

In addition, the U.S. sent Iran a 15-point plan to end the war. President Trump also claimed that Iran sent him a present “worth a tremendous amount of money” related to energy flows through the Strait of Hormuz. We don’t know what kind of present we are talking about, but above all, the controversial fact is that we don’t know who the president is dealing with. In fact, there is no mention of any Iranian official dealing with peace talks. As of now, from Iranian officials, we have just heard words that are far from reassuring:

Has the level of your inner struggle reached the stage of you negotiating with yourself? You will see neither your investments in the region nor the former prices of energy and oil again, until you understand that stability in the region is guaranteed by the powerful hand of our armed forces.

Ebrahim Zolfaghari, spokesperson for the Khatam al-Anbiya Central Headquarters.

One of the two leaders is definitely lying, but as of now, the market has decided to support President Trump’s vision. In fact, even though Iran denies peace talks with the U.S., the market wanted to believe that we are close to the end of the conflict. While I am writing, stock market futures are up more than 1%, oil is declining by 5% (both WTI (CL1:COM) and Brent (CO1:COM)), and gold (XAUUSD:CUR) is rebounding by 2% as the U.S. Dollar (DXY) weakens.

I don’t want to ruin the party, but I am rather confident that this market enthusiasm is just short-lived. The reason why I believe we are going to test new lows is that the two parties are too far apart to even think about reaching an agreement. Here is what I am talking about.

An agreement is still a long way off

Firstly, Israeli officials are claiming that they need several more weeks to complete all the war goals in Iran. So, if Israel continues to bomb, I don’t think it is reasonable to expect a ceasefire anytime soon. Regarding the U.S.–Iran agreement, the evidence shows us that they are asking for totally different conditions. This is what the US asks, according to WSJ:

- Dismantle the three main nuclear sites and end the uranium enrichment process permanently.

- Suspend the ballistic missiles program.

- Reopen the Strait of Hormuz.

If Iran follows these points, then it will be lifted from nuclear-related sanctions, and the domestic nuclear program will be assisted constantly by the U.S. In other words, what President Trump is asking is an unconditional surrender. Without ballistic missiles, Iran will not even be able to defend itself from future attacks, and it could no longer block the Strait to counterattack. At this point, you might think, if they end up reaching an agreement, why should Iran care about future attacks? Because both the U.S. and Israel have already attacked Iran twice during the negotiating talks.

Iran sees negotiations as a pretext for the U.S. to buy time and prepare for the next massive attack, resulting in a further escalation. Will this time be the same as in the past? Well, in my opinion, the probabilities are pretty high. While President Trump claims a potential agreement is close, the Pentagon has just sent 3,000 82nd Airborne Soldiers, and they are expected to reach the Middle East in the coming hours. In this conflict, weekends usually coincided with periods of escalation, and I am concerned about the next one. The recent market rebound might be completely wiped out in just one day following a potential escalation over the weekend. Signals are there.

Finally, to show you how distant the parties are, here is what Iran asks to end the war, according to WSJ:

- No more U.S. military bases in the Middle East. Basically, the U.S. should no longer have any influence in that region.

- Pay for all the damages done to Iran and lift all the sanctions.

- Israel must stop bombing Lebanon.

- No more wars in the region.

- The Strait of Hormuz must always be under Iranian control. In fact, Iran wants to charge ships up to $2 million if they want to cross this route.

As you can see, totally different peace conditions than the ones proposed by the U.S. I want to be optimistic, but recent news is really not helping. Iran has probably understood that it is more powerful than it thought by blocking the Strait of Hormuz. An important point that we should all consider is that Iran is not asking for simple peace conditions that would revert to the pre-war situation. It is not just about receiving the money to rebuild damaged infrastructures; it is about having total military and commercial control over the Middle East. They want Israel to stop any war, they oppose any sanctions, and they want the exclusive control of the Strait of Hormuz: each ship must pay a toll whenever it crosses.

So, if you are betting on a market recovery due to the end of the war, consider that both parties are asking for conditions that are almost impossible to agree on. In my opinion, this war can end only when we have a clear winner, and the loser must accept an unconditional surrender. As of now, we don’t have a clear winner.

Final thoughts

In my opinion, investors shouldn’t downplay this conflict. The market still believes that the U.S. can easily win this war or end it whenever it wants, but the evidence shows otherwise. Both parties are quite distant, and the U.S. is sending thousands more troops to the Middle East. As long as I don’t see words of peace from Israeli/Iranian leaders, the escalation continues. Therefore, I am still bullish on oil and the U.S. dollar and short-term bearish on gold and global stock markets.

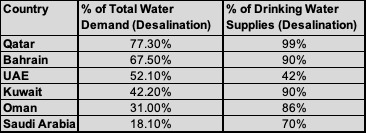

Now, a question arises: how do investors know when the escalation has reached its peak? Most people believe that it depends on oil prices, but I have a different opinion. The last phase of the escalation might be reached once the Gulf countries’ desalination plans are attacked. At that point, water would be worth more than oil.

These countries can’t survive without desalination plants, and Iran threatened to attack them if its energy infrastructures are hit once again. If this happens, I believe the market will start acting in panic mode, regardless of President Trump’s statements regarding peace. This weekend is very important to understand where this war is heading, as the Pentagon sent many more troops to the Middle East.

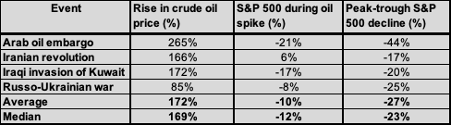

I think there won’t be any de-escalation anytime soon, and the similar historical events support my disbelief.

None of these events ended in a couple of weeks, and I don’t believe the recent oil crisis is less important than the Iraqi invasion or the Russo-Ukrainian war. The median oil spike during these kinds of events was +169%; now we didn’t get further than ~70% (~35% after the recent drop). In addition, the S&P 500 (SP500) peak to trough has always been at least -17%; now it has declined by just ~5%: we are likely not even halfway through.

Leave a Reply