BRLA leaves the Watch List as the Trust is no longer a candidate for the Snowball. As the price rose the yield fell below 6%

* VPC are returning capital so the future yield is the unknown

Remember although a capital gain is always welcome the only consideration for inclusion in the Snowball is the yield, either the buying yield or the current yield.

How much passive income could a £20K Stocks and Shares ISA have made in the past decade?

Stuffing a Stocks and Shares ISA with dividend shares as a passive income idea is one thing — but what might the results be in practice?

Posted by Christopher Ruane

Published 16 May

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

A Stocks and Shares ISA is a long-term investment vehicle.

Different investors use it in different ways. Some want to target capital growth by buying shares cheaply and later selling them for a profit. Some focus on passive income: a regular stream of dividends, or putting the dividends to work to try and earn more income down the road.

So, how much passive income could a £20K Stocks and Shares ISA realistically have earned over the past decade?

The straightforward dividend approach

One variable is the average dividend yield. I will use three to illustrate: the current FTSE 100 average of 3.6%, then 5% and what I see as a high yield, 8%. In today’s market, I think both 5% and 8% are possible while sticking to carefully selected blue-chip shares.

Taking dividends out as they are paid, over a decade, 3.6% would have generated £720 each year – a total of £7,200 over a decade.

Five percent would have been £1,000 each year – a total of £10,000 in a decade. At 8%, the ISA would generate £1,600 a year in dividends. That means the £20K would have generated £16K of passive income over my chosen timescale.

On top of that, an investor may benefit from capital gains when the price goes up (although share prices can fall as well as rise).

Taking the Warren Buffett approach

A second approach is to do what billionaire investor Warren Buffett does.

He has run Berkshire Hathaway (NYSE: BRK.A) (NYSE: BRK.B) for decades but during his tenure it has only paid one dividend. That is despite it generating huge cash flows thanks to owning a lot of successful businesses outright while also holding shares in steady dividend payers like Coca-Cola.

It makes sense for Berkshire to keep some cash on hand. It operates in the insurance industry and there is always a risk that an event — like a hurricane — could suddenly push up its short-term cash needs to meet claims. But Berkshire has hundreds of billions of dollars of cash on hand today!

Rather than doling it out as dividends, Buffett aims to put it work to try and earn even more money in future, by making more investments (although the current cash pile means Berkshire hasn’t done as much of that lately).

Compounding an ISA

A similar approach (known as compounding) can be applied to the dividends received in a Stocks and Shares ISA.

Compounding a £20K ISA at 3.6% for a decade, it would be worth over £28,400 – enough to earn £1,025 in dividends at a 3.6% yield.

Compounding at 5%, the ISA would be worth over £32,500 after a decade. That could then earn around £1,628 each year in dividends.

Meanwhile, compounding the £20K ISA at 8% for 10 years, it would be worth over £43K and could then earn £3,454 in passive income annually.

Compounding would have meant sacrificing dividends for a decade but hopefully earning bigger ones from this year onwards (or whenever the investor chose to stop compounding and start withdrawing).

Selecting the right shares is key, but the costs of a Stocks and Shares ISA can eat into overall returns, especially over the long So a savvy investor will start by comparing different ISAs on the market and decide which one suits their needs best.

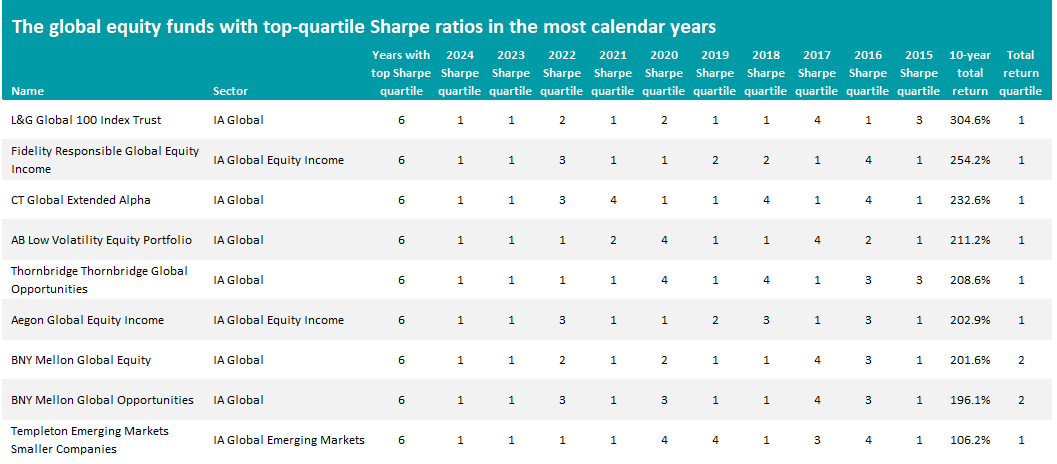

Nine global funds with the highest Sharpe ratios year in, year out

16 May 2025

Trustnet looks for global funds with high Sharpe ratios in most years of the past decade.

By Gary Jackson

Funds run by Legal & General Investment Management, Columbia Threadneedle and Fidelity are among the handful of global equity strategies that have consistently made their sectors’ highest Sharpe ratios, Trustnet research has found.

The Sharpe ratio measures the risk-adjusted return of an investment by comparing its excess return over the risk-free rate to its standard deviation. A higher Sharpe ratio indicates more return per unit of risk, making it a useful tool for evaluating the efficiency of investment performance.

In this series, Trustnet is looking at the Sharpe ratios of funds over the past decade to find out which ones have spent at least six of those years in their sector’s top quartile for this closely watched risk/return metric.

We start with funds that have a global reach, putting the IA Global, IA Global Equity Income and IA Global Emerging Markets sectors under the spotlight.

Across these three peer groups, there are 381 funds with a track record of 10 or more years, but only nine have been in the top quartile for Sharpe ratio in six of the past decade. They can be seen in the table below, along with their total return over the entire period.

Source: FE Analytics. Total return in sterling between 1 Jan 2025 and 31 Dec 2024.

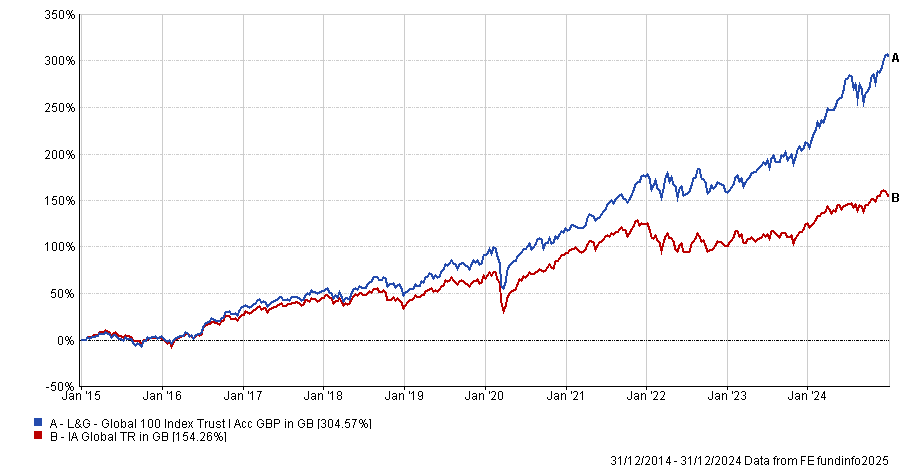

At the top of the table is L&G Global 100 Index Trust, which has made the highest total return of the nine shortlisted funds – it was up 304.6% over the decade under consideration, compared with a rise of 154.3% for the average fund in the IA Global sector.

The £1.8bn tracker physically replicates the S&P Global 100 index, which is made up of the largest 100 companies from across the globe. This means the portfolio’s biggest holdings are the likes of Apple (11.8%), Microsoft (10%) and Nvidia (9.3%), resulting in a hefty skew towards the US (78.6% of the portfolio).

Performance of L&G Global 100 Index Trust vs sector between 1 Jan 2015 and 31 Dec 2024

Source: FE Analytics. Total return in sterling between 1 Jan 2015 and 31 Dec 2024

The remaining eight funds on the shortlist are active strategies, with Fidelity Responsible Global Equity Income putting in the second-best performance after making 272.7% since the start of the period we examined.

It has been managed by Aditya Shivram since July 2021, although he has run the offshore Fidelity Global Equity Income fund since its launch in 2013. The approach behind the £189m fund looks for sustainable, higher quality companies with stable and/or improving returns on capital, reasonable valuations, low leverage and predictable, stable business models.

Fidelity Responsible Global Equity Income has a much lower allocation to the US than many global portfolios. It has just one-third of its portfolio in US companies, compared with 64.6% in its MSCI AC World benchmark. Six of its top 10 holdings are from outside of the US, including Deutsche Boerse, Munich Re Group, Relx and Unilever.

CT Global Extended Alpha came in third place. Like all the funds on the shortlist, it was top quartile in its sector for Sharpe ratio in six of the 10 full years we examined and made a 232.6% across the decade.

This fund has been run by Neil Robson since 2012 and, unlike the typical global equity fund, follows an ‘equity extension strategy’ that allows proceeds from short positions to be used to extend the portfolio’s long positions – thereby offering more exposure to the strongest investment ideas.

As can be seen, most of the consistent top Sharpe ratio funds are in the IA Global sector while two reside in IA Global Equity Income. Only one – Templeton Emerging Markets Smaller Companies – is in the IA Global Emerging Markets sector.

Templeton Emerging Markets Smaller Companies has been run by Chetan Sehgal since 2017, with FE fundinfo Alpha Manager Vika Chiranewal joining as co-manager in 2020. Like all Templeton emerging market funds, it takes a valuation-oriented approach with a focus on bottom-up analysis and little emphasis on top-down views.

While the nine funds in the table above are the only ones to have achieved top-quartile Sharpe ratios in six of the past 10 full years, there are 35 without a single year in the first quartile.

Among them are Pictet Global Megatrend Selection, CT Global Equity Income, Jupiter Merlin Worldwide Portfolio, TM Stonehage Fleming Global Equities and abrdn Emerging Markets Equity.

The Sharpe ratio is a composite metric which reflects two closely related attributes of an instrument, the reward and ‘risk’. In general, if the risk is expected to be higher then the expected return should also be higher to compensate for the higher chance of a lower or negative return.

The Sharpe ratio is defined as the mean (average) return minus a risk-free return divided by the standard deviation of past returns. Note that the risk-free rate should reflect the periods used (e.g. don’t use an annual risk-free rate for monthly periods). Regardless of the periods selected, the Sharpe ratio value is given as a monthly figure.

Furthermore, the Sharpe ratio graphically represents the slope of a portfolio’s capital market line. Because of this, it can be interpreted also as an amount of additional reward required by an additional 1% of risk. Higher Sharpe ratios are better

Are these fears overblown ? Perhaps. UK GDP growth reached 0.7% in March, defying pessimistic expectations. Inflation is relatively under control, and as such the Bank of England has leeway to keep reducing interest rates, unlike its US counterpart the Federal Reserve.

Increased European defence spending could prove a boon for UK aerospace and other sectors.

Research from the Association of Investment Companies (AIC) shows UK equities have been more resilient than global counterparts. In the year to 8 May, the average UK All Companies investment trust is up slightly over 10%, compared to 1% for the average Global sector trust.

“It may be that the UK market has already started its rebound after several years of underperformance,” says Annabel Brodie-Smith of the AIC. “We certainly aren’t out of the woods, but with two trade deals signed and interest rates on their way down, the stars may finally be aligning for UK companies.

The tariff turmoil produced winners and losers, and to trust managers surveyed by the AIC, the UK economy has good exposure to those sectors that came off best.

Which sectors have driven UK resilience?

The composition of the UK stock market, particularly the FTSE 100, is a large driver of the resilience that the UK has seen.

Large caps in the UK stock market are typically in highly defensive sectors like consumer staples, says David Smith, portfolio manager of Henderson High Income Trust (LON:HHI). In these sectors, “earnings are typically more resilient in an economic slowdown,” he adds.

With global stock markets having largely fixated on growth stocks, like the Magnificent Seven, for the past decade and more, the defensive sectors that make up much of the UK’s stock market have become relatively undervalued.

“We have been finding new investment opportunities in domestically orientated cyclical areas, such as industrials, advertising and staffing,” says Wright, “while also selectively adding back exposure to real estate stocks and housing related names, where demand appears to be stabilising and valuations remain attractive.”

While the retail sector is much-maligned, for contrarians like Wright now is the perfect time to buy in. He explains that FSV has been increasing its exposure to “retailers specialising in big-ticket items such as kitchens and sofas, where sales are 10% to 25% below historical volumes.” Improving growth outlooks and the prospect of falling interest rates, he says, could lift this sector in the future.

“We believe the company can continue to take share in a fragmented market,” says Luke. “The shares trade on a mid-teens price-earnings ratio with a dividend yield of around 4%, and this has typically been supplemented by an additional annual special dividend given the strength of the balance sheet.”

Why the UK economy is appealing across all sectors

Stepping back, there are broader structural reasons that make the UK an appealing market for investment trust managers, across all sectors.

“There are a number of reasons to invest in the UK now,” says Smith. “The starting valuation of the UK equity market is low and trading at a discount to its long-term average and other global indices, especially the US, helping to absorb negative sentiment around trade tensions.”

Smith adds that the UK is not a large exporter to the US, so the impact of tariffs is relatively lower. That is also helped by the UK-US trade agreement reached week, which reduces the tariffs applied to some car exports to the US to 10%.

“The tariff shock is happening at a time when the outlook for UK-listed companies is improving, energy and food prices are falling, pressures on the UK consumer are easing, while the labour market remains healthy and savings are elevated,” says Luke.

“UK equities are valued attractively, especially compared to US equities, and UK equities have been consistently overlooked by international investors. It may be that, having monopolised investment returns for years, the attractions of the US equity market are beginning to wane.”

QuotedData’s Real Estate Monthly Roundup – May 2025

15 May 2025

Richard Williams

Winners and losers in April 2025

Best performing funds in price terms

(%)

Social Housing REIT

15.7

Urban Logistics REIT

12.0

Regional REIT

10.4

Helical

9.6

NewRiver REIT

9.5

Sirius Real Estate

9.4

Primary Health Properties

9.2

Shaftesbury Capital

8.7

Big Yellow Group

7.9

Land Securities

7.7

Source: Bloomberg, Marten & Co

Amid the global tariff turmoil brought on at the start of April by Trump’s so-called ‘liberation day’, real estate stocks have proved resilient, perhaps reflecting the sector’s defensive characteristics and income-generating traits. The average share price uplift was 2.7% over the month, and 4.6% in the year-to-date. Leading the way was Social Housing REIT, which appears to be making strong progress under its new manager Atrato Capital.

Urban Logistics REIT’s share price jumped on news that it was the target of LondonMetric (see the corporate activity section for details), which, after the month end, tabled a recommended cash and shares offer for the company. Promising signs that the bottom has finally been reached in secondary office values spurred on Regional REIT’s share price to a double-digit rise over the month. Its shares and the sub-sector will certainly be worth keeping an eye on over the rest of the year. Meanwhile, London office developer Helical successfully sold one of its developments for £333m during the month (see the news section for more details).

Worst performing funds in price terms

(%)

Grit Real Estate Income Group

(17.6)

CLS Holdings

(10.0)

Ground Rents Income Fund

(7.2)

Globalworth Real Estate

(5.0)

Life Science REIT

(2.0)

Real Estate Investors

(1.7)

SEGRO

(1.5)

First Property Group

(0.7)

Care REIT

(0.7)

Schroder European REIT

(0.3)

Source: Bloomberg, Marten & Co

Grit Real Estate’s share price seems to be on a downward spiral with yet another double-digit monthly share price fall in April. It is now down 33.3% during 2025, having already been derated significantly over the last few years. Office landlord CLS Holdings, which owns assets in the UK, France and Germany, is also struggling with downward share price momentum – not helped by severe illiquidity in its shares. Ground Rents Income Fund is another familiar name in the worst performing funds table as values continue to be hit by legacy issues and legislative changes. Life Science REIT’s share price cooled in April having jumped 30%+ in March after the company was effectively put up for sale. It was a similar story for Care REIT whose shares leapt almost 40% on news of its acquisition by a US REIT, which took effect after the month end (see the corporate activity section for more details). The industrial and logistics sector would appear most exposed to US tariffs with European manufacturing and exports set to take a hit, which was likely behind weakness in SEGRO’s share price in April.

Valuation moves

Company

Sector

NAV move (%)

Period

Comments

Life Science REIT

Offices/labs

(6.9)

Full year to 31 Dec 24

Like-for-like portfolio valuation down 4.0% to £385.2m

Phoenix Spree Deutschland

Europe

(10.4)

Full year to 31 Dec 24

NAV primarily due to portfolio sale during the year at substantial discount to book value

Source: Marten & Co

Corporate activity in April

LondonMetric Property made a proposal to acquire Urban Logistics REIT in a cash and shares offer. The proposal consisted of new shares in LondonMetric based on a NAV for NAV exchange ratio plus a fixed amount in cash. Under the terms of the proposal, shareholders in Urban Logistics would be entitled to receive 0.5612 new LondonMetric shares and 42.8p in cash – valuing Urban Logistics in a range of £675m to £700m (depending on LondonMetric’s share price).

Assura agreed to the terms of a recommended cash offer for the company by Kohlberg Kravis Roberts (KKR) and Stonepeak Partners. Under the terms, each Assura shareholder is entitled to receive 49.4p, in line with its EPRA net tangible assets (NTA) value at 30 September 2024, which was also a 31.9% premium to the undisturbed share price The deal values Assura at around £1,608m. In recommending the offer, Assura’s board also unanimously rejected Primary Health Properties merger (PHP) offer. PHP said it would continue to explore a merger.

Care REIT’s £448m acquisition by US-listed care home provider CareTrust will progress after shareholders voted overwhelmingly in favour (84.76%) of the deal at 108p per share (a 32.8% premium to the prevailing share price but a 9.4% discount to its last reported NAV). The company’s last day of trading was 8 May.

Supermarket Income REIT entered into a £403m, 50:50 joint venture (JV) with Blue Owl Capital. The JV was seeded with eight properties from the company’s existing portfolio, which were transferred at a 3% premium to book value. The partners will seek to grow the JV to up to £1bn over the coming years.

Empiric Student Property acquired Selly Oak Apartments in Birmingham for £9.0m. The 63-bed mixed studio and shared apartment scheme is fully-let for the 2024/25 academic year and is expected to deliver a yield in excess of 6% from September 2025. The company now has 430 beds in the Selly Oak cluster.

Tritax Big Box REIT updated on its non-core disposals following the acquisition of UK Commercial Property REIT almost a year ago. It has sold £235.7m of assets, representing half of the £475m identified, with a further £95.6m under offer.

Life Science REIT let 5,600 sq ft at the Innovation Quarter at Oxford Technology Park to Oxford Expression Technologies Limited, a biotech company specialising in protein production for vaccine development, disease research, and drug testing, at a new rental record for the park of £46.50 per sq ft per annum.

Helical sells City office to State Street for £333m

Helical sold 100 New Bridge Street, a City of London office development, to investment bank State Street for £333m. The 195,000 sq ft office will become the company’s new London headquarters, with the purchase price reflecting a 5% yield.

LondonMetric Property acquired a pre-let M&S logistics warehouse in Bristol for £74.0m, reflecting a NIY of 5.65%, in a forward-funding deal. The 390,000 sq ft regional logistics warehouse is pre-let to M&S on a 20-year lease with five yearly upward only rent reviews linked to CPI.

Great Portland Estates announced a further nine office lettings across its ‘fully managed’ offering, securing £7.2m of annual rent at an average of £215 per sq ft. This was 14.1% ahead of ERV and generated a 112% premium to an equivalent traditional office lease. The lettings were across 33,500 sq ft of newly refurbished office space in six GPE buildings.

Visit https://www.QuotedData.com for more on these and other stories plus analysis, comparison tools and basic information, key documents and regulatory announcements on every real estate company quoted in London

Manager’s views

A collation of recent insights on real estate sectors taken from the comments made by chairmen and investment managers of real estate companies – have a read and make your own minds up. Please remember that nothing in this note is designed to encourage you to buy or sell any of the companies mentioned.

2024 was a challenging year for leasing across the Golden Triangle (research and development hubs of Oxford, Cambridge and London), with life sciences take up of 460,000 sq ft, just over half the amount of 2023. The uptick in confidence which followed the general election proved short-lived and sentiment weakened post the budget. However, the Government has demonstrated its support for the sector, with planned investment into the Oxford and Cambridge region, including a new rail link, and the funding environment has strengthened.

In 2024, £3.7bn was raised for UK biotech funding, making it the strongest year since the 2021 peak. £2.2bn was raised through venture capital funding and a further £1.5bn was raised through follow on financings, suggesting a preference for well established, lower risk ventures. Inevitably it takes time for the impact of a successful fund raise to filter through to real estate decision making, but by the end of 2024, 300,000 sq ft of space was under offer to life sciences companies.

The Berlin property market has demonstrated a notable disparity in achievable sales values per square meter between condominiums (individually owned apartments) and PRS properties (apartment blocks intended for private rental). While condominium prices and transaction volumes have remained broadly stable, valuations for PRS properties have experienced a sharp decline since their peak in 2022. This trend was reflected in the company’s disposal progress in 2024, where condominium sales achieved average per sqm valuations that were 92% higher than those of individual PRS property sales. This polarisation has shaped the company’s strategy, which now prioritises unlocking value through increased condominium sales.

Although recent data indicates a recovery in transaction activity within Germany’s residential real estate market during the latter half of 2024, uncertainties persist regarding the potential effects of escalating macroeconomic risks – particularly those stemming from the current US administration’s imposition of higher trade tariffs – on investor sentiment and real estate asset demand.

Germany has embarked on a historic fiscal expansion, channelling €500bn into infrastructure modernisation (transport, energy, and digital networks) and an equal sum into defence. This dual-track spending surge marks a departure from decades of fiscal conservatism, driven by geopolitical tensions and aging infrastructure. Constitutional reforms to the Schuldenbremse (debt brake) underpin these initiatives. Previously capping structural deficits at 0.35% of GDP, the revised framework permits borrowing for “future-oriented projects,” including green energy and defence.

The bond market experienced significant volatility in early 2025, with German 10-year bond yields climbing 0.5% to reach 2.8% by March, as investors anticipated increased German debt issuance. This upward pressure later eased following the European Central Bank’s rate reduction and heightened demand for German bunds, which have been viewed as a relatively safer haven during escalating global trade tensions.

There remains a significant and growing shortage of available residential accommodation in Berlin metropolitan areas, particularly Berlin itself, driven by persistent supply-demand imbalances. Whilst the population of Germany has grown by over 1.3 million since 2020, new construction activity has fallen significantly. Project cancellations hit a record high in 2024, and annual apartment completions are projected to fall to 175,000 by 2025 – far below the Federal Government’s 400,000 unit annual target.

A widening cost-price gap has exacerbated supply challenges: since 2022 construction costs have risen by 28%, far outstripping new build price growth. This disparity has pushed tenanted multi-family property values 40% below replacement costs in many regions. New developments now typically focus on high-end or government-backed social housing, leaving Berlin’s middle-market segment (the Company’s core market) underserved.

Without policy support for development, supply-demand imbalances will deepen. Whilst the new coalition government aims to address the affordable housing crisis by accelerating construction through eliminating bureaucracy and financial incentives for cost-effective projects, it is unlikely that this will alleviate housing shortages in the near term. The outlook for Berlin rental values therefore remains positive.

IMPORTANT INFORMATION

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it. Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

(a non-cellular company limited by shares incorporated in the Island of Guernsey under the Companies (Guernsey) Law 2008, as amended, with registered number 57985 and registered as a Registered Closed-ended Collective Investment Scheme with the Guernsey Financial Services

Re: Dividend Announcement

The Directors of TwentyFour Select Monthly Income Fund Limited (“SMIF“), the listed, closed-ended investment company that invests in a diversified portfolio of credit securities, have declared that a dividend of 0.5 pence per share will be paid, in line with the Prospectus, representing the regular monthly targeted dividend for the financial period ended 30 April 2025 as follows:

Ex-Dividend Date 22 May 2025 Record Date 23 May 2025 Payment Date 6 June 2025

The Second Interim Dividend of 2.20 pence per Ordinary Share (May 2024: 2.20 pence per Ordinary Share) will be payable to Shareholders on the register as at 23 May 2025, with an associated ex-dividend date of 22 May 2025 and a payment date on or around 27 June 2025.

Dividend Guidance Reaffirmed

The Board is pleased to reaffirm its guidance of a full year dividend of not less than 8.90 pence per Ordinary Share for the financial year ending 30 June 2025 (30 June 2024: 8.80 pence). This is expected to be covered by earnings and to be post debt amortisation.

Actual Generation Vs Forecast

Combined generation for the period was 0.3% above forecast. Whilst solar generation had a very strong March (+26%), poor generation across January and February (-10% below forecast) led to solar generation for the quarter performing 9% above forecast. Wind speeds were consistently below forecast during the quarter (-9.7%), which in combination with equipment failure on 2 assets, led to wind generation being 20% below forecast for the quarter.