Not Naval Gazing, that’s a completely different subject.

Octopus Renewables Infrastructure Trust PLC (LSE:ORIT) Full Year 2024 Earnings Call Highlights:

GuruFocus News

31 March 2025

In this article:

Positive Points

Octopus Renewables Infrastructure Trust PLC (LSE:ORIT) delivered a positive NAV total return of around 2.5% for the calendar year 2024.

The company paid an on-target fully covered dividend of 6.02p per share, marking the third consecutive year of dividend increase in line with inflation.

A successful share buyback program was implemented, initially set at 10 million pounds and later increased to 30 million pounds, contributing to NAV per share accretion.

The acquisition of the Ballymacarni solar complex and the Harliton project expanded their portfolio, adding significant megawatt capacity.

The company achieved a 7% increase in generation from its portfolio, with new projects receiving higher electricity prices and reduced operating costs, leading to increased EBITDA margins.

Negative Points

Despite a positive NAV return, the net asset value declined due to capital returned to shareholders and running costs.

The company faces challenges in reducing leverage, with a goal to bring it below 40% of gross asset value.

There is uncertainty in the market due to policy and government rhetoric that sometimes suggests a move away from renewables.

The company is reliant on capital recycling, with significant asset sales required to maintain financial health.

The UK market is undergoing changes in grid access reform, which could impact project timelines and costs. Warning ! GuruFocus has detected 3 Warning Sign with LSE:ORIT.

Q & A Highlights

Q: Can you provide an overview of Octopus Renewables Infrastructure Trust’s performance in 2024?

A: During 2024, we delivered a positive NAV total return of around 2.5%, primarily driven by dividends in line with our target. Despite a decline in net asset value due to capital returns to shareholders and running costs, we paid a fully covered dividend of 6.02p per share, marking a 4% increase from the previous year. We also announced a further inflation-linked increase in the dividend target for 2025. (Unidentified_2)

Q: What strategic acquisitions and sales did the company complete in 2024?

A: We completed the purchase of the Ballymacarni solar complex and the Harliton project, totaling 241 megawatts. Additionally, we sold the Lung Bon wind farm for EUR 70.4 million, achieving an 11.3% return. Our asset sales have realized GBP 161 million, a 12% uplift to holding value, surpassing our listed peers in the renewable space.

Q: How has the company’s generation capacity and revenue evolved over the past year?

A: Our generation capacity increased by 7% year-on-year due to new projects and acquisitions, despite some asset sales. Revenue and EBITDA grew even more, thanks to higher electricity prices from new projects and reduced operating costs, leading to an increased EBITDA margin.

Q: What are the company’s goals for 2025?

A: We have set three clear goals for 2025: extending our share buyback program by an additional GBP 20 million, reducing leverage to below 40% of gross asset value, and selling up to GBP 80 million of assets.

Q: What is the company’s approach to recent acquisitions and developer partnerships?

A: Our recent acquisitions focus on the developer side, aiming for higher returns with limited capital deployment. We are supporting Nordic Renewables in Finland and BLC in the UK, providing additional capital to advance their projects, particularly in solar and battery storage.

Finally, the markets are far more researched than they ever were in the past. Buffett is famous for voraciously reading reports and accounts to find the next business to back. From the start of his career, he scoured financial statements to unearth assets that had yet to be exploited. That is possible if you are very good at scanning balance sheets and if no one else is taking the trouble. But there is far more information around now than there was when Buffett was starting his career. The hedge funds and private-equity houses are all looking at the same information and trying to spot the same opportunities. Artificial intelligence will streamline that process even more.

It is hard to imagine that a couple of guys in Omaha, no matter how smart they were, could spot something that the rest of the world had somehow missed. Buffett’s reputation is completely deserved. But it seems unlikely there will ever be another investor who does quite as well as he did. The investment world has changed too much for anyone to turn themselves into one of the five richest men in the world simply by investing well. The next Buffett doesn’t exist – and there is no point in looking for him.

This article was first published in MoneyWeek’s magazine. Enjoy exclusive early access to news, opinion and analysis from our team of financial experts with a MoneyWeek subscription.

Second Return of Capital through the B Share Scheme

The Board of VPC Specialty Lending Investments plc (the “Company“) is pleased to announce a second return of capital via the B Share Scheme.

The Company’s managed wind-down investment policy was approved by shareholders in June 2023. Since the initial B-Share distribution in April 2024, the Company has made progress in realising value both through debt repayments and the sale of equity securities. On 9 May 2025, the Company received full repayment of the Senior Secured Note of $50.3 million from the refinance of the Deinde Group, LLC (d/b/a, Integra Credit) (“Integra“) senior secured term loan. After the refinance, the Company still holds a residual term note of $18.7 million in Integra which consists of the existing non-interest-bearing term note and uncollected accrued interest at the time of the transaction.

After considering the Company’s projected working capital requirements, the Board has decided to make a second distribution to shareholders of £43 million through the issue and redemption of B Shares. The capital to be returned represents approximately 29.3 percent of the Company’s Net Asset Value as at 31 December 2024.

Pursuant to the authority received from shareholders at a general meeting of the Company held on 5 April 2024 B Shares of 1 penny each will be paid up out of the reserves of the Company and issued to all Shareholders by way of a bonus issue pro-rata to their holding of Ordinary Shares held at the Record Date of 6 p.m. on 21 May 2025. The B Shares will be issued on 22 May 2025 and redeemed at 1 penny per B Share. The Redemption Date in respect of this initial return of capital is 29 May 2025. The proceeds from the redemption of the B Shares will be sent to uncertificated Shareholders through CREST or via cheque to certificated Shareholders on or around 12 June 2025.

Shareholders are reminded that the issue of B Shares will not reduce the number of the Company’s ordinary shares in issue. However, following the issue and redemption of B Shares, the NAV (and NAV per ordinary share) will be reduced by the total amount of capital returned and the share price is likely to reflect the reduction in NAV. The pence per ordinary share amount of any dividends is therefore expected to reduce as a consequence of the reduction in NAV and, over time, through the changing composition of the portfolio.

The Company will continue to realise value from its debt and equity positions and will allocate the proceeds as between required dividend distributions and further returns of capital through the B-Share scheme and/or alternative forms of return after considering the working capital needs of the Company. The Board is not able to specify the timing and amount of future returns, which will continue to depend on the repayment of the Company’s debt assets as well as the sale of other securities. One of the advantages of the B Share Scheme is that returns of capital can be made to shareholders on a more cost-effective basis than, for example, through a tender offer and this would allow for smaller and potentially more frequent returns to be made.

Terms used and not defined in this announcement have the meanings given to them in the circular to the Company’s shareholders dated 15 March 2024.

Buffett Made 19.9% a Year. Here’s How We Can Beat Him (and Get Paid Monthly)

Michael Foster, Investment Strategist Updated: May 8, 2025

Can you and I beat the legendary returns of Warren Buffett? Absolutely. What’s more, we can do it while “translating” a slice of our gains into a big income stream (with special dividends on the table, too).

I’ll show you how in a moment.

First, we need to talk about how the 94-year-old Oracle of Omaha, who is now stepping back from the position of president and CEO of Berkshire Hathaway (BRK.A), has changed the course of investing over the years.

Every year, as you likely know, Buffett releases a simple letter to investors showing what’s happened with Berkshire’s portfolio. While there have been a few lean years, his outperformance is astounding: a 5,502,284% return on every dollar invested at the start of his 60-year career.

That amounts to a 19.9% annualized gain, nearly double the S&P 500’s 10.4% in that time.

That gap is impressive enough, but compounding makes it a difference of millions of percent. This just proves one of Buffett’s main arguments: One needs to stay in the market, patiently outlasting all the short-term panics (like the recent tariff hysteria) and patiently buying when assets are oversold.

Second, it’s worth noting that stocks themselves did well in that time, with double-digit profits. That means retirement is more attainable than most people expect.

If you could turn, say, half of that 19.9% yearly return into income, you could score a healthy six-figure income stream by investing a little over a million dollars. That’s what that fund I mentioned off the top can do for us. We’ll talk about this off-the-radar ticker in just a few more seconds.

First, I do need to rain on Buffett’s parade a bit here: The truth is, most of his outperformance stems from the early years of Berkshire Hathaway’s operations.

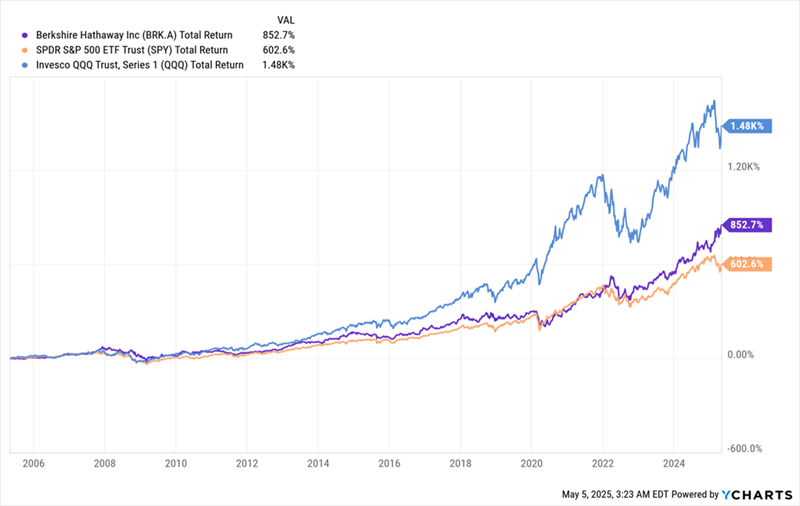

Berkshire’s Strong—But Waning—Returns

Some quick numbers: Berkshire Hathway (shown in purple above) has had a 19.1% total annualized return over the last 45 years, as we just discussed. But over the last 20 years, its return has slipped to 11.9% annualized, just ahead of 10.2% from the S&P 500 (in orange above). It’s also less than the NASDAQ 100, in blue, at 14.8%.

In fact, since the 2000s the tech- (and growth-) focused NASDAQ 100 has beaten both the S&P 500 and the value-investing strategies of Mr. Buffett.

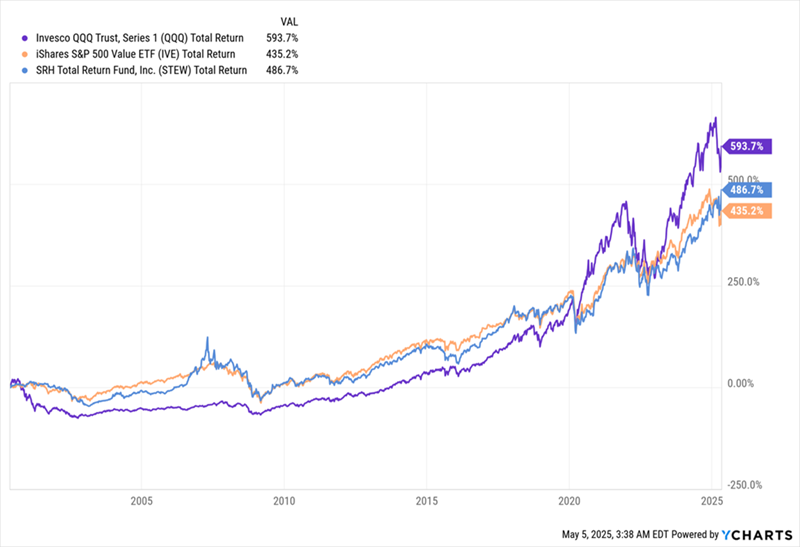

We can clearly see that in the performance of the NASDAQ 100, shown through its main index fund in purple below. The NASDAQ has easily outrun the value-focused iShares S&P 500 Value ETF (IVE), in orange below.

The most “Buffett-like” closed-end fund (CEF), the SRH Total Return Fund (STEW), in blue, has also been dusted by the tech-heavy NASDAQ. STEW invests half its assets in Berkshire and the rest in Buffett favorites like JPMorgan Chase & Co. (JPM).

NASDAQ 100 Outruns “Buffett-Like” Funds

A key thing to note about this chart is that the NASDAQ 100’s outperformance has been accelerating. That’s because it’s tilted toward tech, and our economy is becoming more tech focused. So tech stocks will likely rise more than those favored by value investors over the long haul.

A CEF That “Translates” Buffett-Beating Gains Into Income

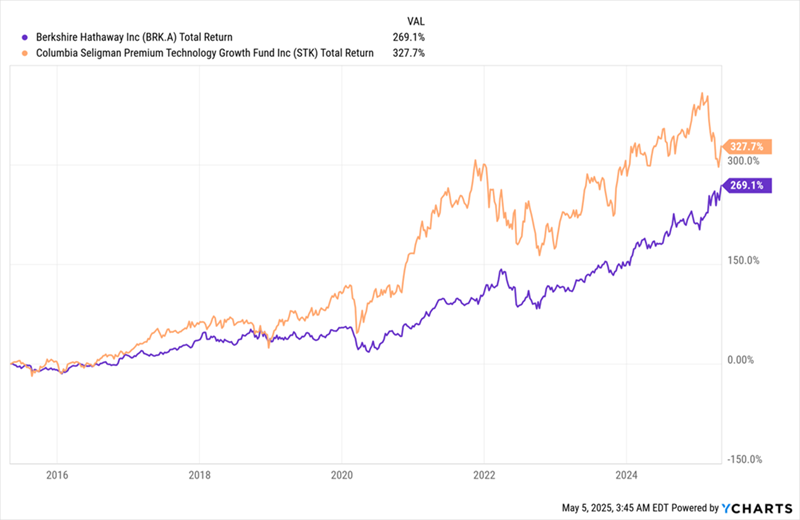

That’s the perfect segue into the CEF I want to spotlight today, the Columbia Seligman Premium Technology Growth Fund (STK). As you can see below, STK (in orange) outperformed Berkshire (in purple) over the last decade.

STK Tops the Oracle

In fact, not only has STK outperformed, but it’s delivered a large slice of those gains as income. The fund yields 6.6% as I write this, and its normal payouts have stayed rock steady over the last decade. Plus, STK has paid out a lot of special dividends (the spikes below) that make its total yield to investors even bigger.

Even ignoring those special payouts, investors who stuck with STK over the last decade would now be enjoying a 9.8% yield on their original buy, since STK’s unit price has nearly doubled in that time. So they’d be getting a bit less $100,000 per year for every million dollars invested, again before we consider those special dividend payments over the years.

Will this continue? It depends whether tech will stop being a major part of our lives and whether Wall Street will forget the value-investing strategies Buffett espoused. I think you’ll agree that neither scenario is very likely.

Michael Foster, Investment Strategist Updated: May 8, 2025

Can you and I beat the legendary returns of Warren Buffett? Absolutely. What’s more, we can do it while “translating” a slice of our gains into a big income stream (with special dividends on the table, too).

I’ll show you how in a moment.

First, we need to talk about how the 94-year-old Oracle of Omaha, who is now stepping back from the position of president and CEO of Berkshire Hathaway (BRK.A), has changed the course of investing over the years.

Every year, as you likely know, Buffett releases a simple letter to investors showing what’s happened with Berkshire’s portfolio. While there have been a few lean years, his outperformance is astounding: a 5,502,284% return on every dollar invested at the start of his 60-year career.

That amounts to a 19.9% annualized gain, nearly double the S&P 500’s 10.4% in that time.

That gap is impressive enough, but compounding makes it a difference of millions of percent. This just proves one of Buffett’s main arguments: One needs to stay in the market, patiently outlasting all the short-term panics (like the recent tariff hysteria) and patiently buying when assets are oversold.

Second, it’s worth noting that stocks themselves did well in that time, with double-digit profits. That means retirement is more attainable than most people expect.

If you could turn, say, half of that 19.9% yearly return into income, you could score a healthy six-figure income stream by investing a little over a million dollars. That’s what that fund I mentioned off the top can do for us. We’ll talk about this off-the-radar ticker in just a few more seconds.

First, I do need to rain on Buffett’s parade a bit here: The truth is, most of his outperformance stems from the early years of Berkshire Hathaway’s operations.

Berkshire’s Strong—But Waning—Returns

Some quick numbers: Berkshire Hathway (shown in purple above) has had a 19.1% total annualized return over the last 45 years, as we just discussed. But over the last 20 years, its return has slipped to 11.9% annualized, just ahead of 10.2% from the S&P 500 (in orange above). It’s also less than the NASDAQ 100, in blue, at 14.8%.

In fact, since the 2000s the tech- (and growth-) focused NASDAQ 100 has beaten both the S&P 500 and the value-investing strategies of Mr. Buffett.

We can clearly see that in the performance of the NASDAQ 100, shown through its main index fund in purple below. The NASDAQ has easily outrun the value-focused iShares S&P 500 Value ETF (IVE), in orange below.

The most “Buffett-like” closed-end fund (CEF), the SRH Total Return Fund (STEW), in blue, has also been dusted by the tech-heavy NASDAQ. STEW invests half its assets in Berkshire and the rest in Buffett favorites like JPMorgan Chase & Co. (JPM).

NASDAQ 100 Outruns “Buffett-Like” Funds

A key thing to note about this chart is that the NASDAQ 100’s outperformance has been accelerating. That’s because it’s tilted toward tech, and our economy is becoming more tech focused. So tech stocks will likely rise more than those favored by value investors over the long haul.

A CEF That “Translates” Buffett-Beating Gains Into Income

That’s the perfect segue into the CEF I want to spotlight today, the Columbia Seligman Premium Technology Growth Fund (STK). As you can see below, STK (in orange) outperformed Berkshire (in purple) over the last decade.

STK Tops the Oracle

In fact, not only has STK outperformed, but it’s delivered a large slice of those gains as income. The fund yields 6.6% as I write this, and its normal payouts have stayed rock steady over the last decade. Plus, STK has paid out a lot of special dividends (the spikes below) that make its total yield to investors even bigger.

Even ignoring those special payouts, investors who stuck with STK over the last decade would now be enjoying a 9.8% yield on their original buy, since STK’s unit price has nearly doubled in that time. So they’d be getting a bit less $100,000 per year for every million dollars invested, again before we consider those special dividend payments over the years.

Will this continue? It depends whether tech will stop being a major part of our lives and whether Wall Street will forget the value-investing strategies Buffett espoused. I think you’ll agree that neither scenario is very likely.

Can you and I beat the legendary returns of Warren Buffett? Absolutely. What’s more, we can do it while “translating” a slice of our gains into a big income stream (with special dividends on the table, too).

I’ll show you how in a moment.

First, we need to talk about how the 94-year-old Oracle of Omaha, who is now stepping back from the position of president and CEO of Berkshire Hathaway (BRK.A), has changed the course of investing over the years.

Every year, as you likely know, Buffett releases a simple letter to investors showing what’s happened with Berkshire’s portfolio. While there have been a few lean years, his outperformance is astounding: a 5,502,284% return on every dollar invested at the start of his 60-year career.

That amounts to a 19.9% annualized gain, nearly double the S&P 500’s 10.4% in that time.

That gap is impressive enough, but compounding makes it a difference of millions of percent. This just proves one of Buffett’s main arguments: One needs to stay in the market, patiently outlasting all the short-term panics (like the recent tariff hysteria) and patiently buying when assets are oversold.

Second, it’s worth noting that stocks themselves did well in that time, with double-digit profits. That means retirement is more attainable than most people expect.

If you could turn, say, half of that 19.9% yearly return into income, you could score a healthy six-figure income stream by investing a little over a million dollars. That’s what that fund I mentioned off the top can do for us. We’ll talk about this off-the-radar ticker in just a few more seconds.

First, I do need to rain on Buffett’s parade a bit here: The truth is, most of his outperformance stems from the early years of Berkshire Hathaway’s operations.

Berkshire’s Strong—But Waning—Returns

Some quick numbers: Berkshire Hathway (shown in purple above) has had a 19.1% total annualized return over the last 45 years, as we just discussed. But over the last 20 years, its return has slipped to 11.9% annualized, just ahead of 10.2% from the S&P 500 (in orange above). It’s also less than the NASDAQ 100, in blue, at 14.8%.

In fact, since the 2000s the tech- (and growth-) focused NASDAQ 100 has beaten both the S&P 500 and the value-investing strategies of Mr. Buffett.

We can clearly see that in the performance of the NASDAQ 100, shown through its main index fund in purple below. The NASDAQ has easily outrun the value-focused iShares S&P 500 Value ETF (IVE), in orange below.

The most “Buffett-like” closed-end fund (CEF), the SRH Total Return Fund (STEW), in blue, has also been dusted by the tech-heavy NASDAQ. STEW invests half its assets in Berkshire and the rest in Buffett favorites like JPMorgan Chase & Co. (JPM).

NASDAQ 100 Outruns “Buffett-Like” Funds

A key thing to note about this chart is that the NASDAQ 100’s outperformance has been accelerating. That’s because it’s tilted toward tech, and our economy is becoming more tech focused. So tech stocks will likely rise more than those favored by value investors over the long haul.

A CEF That “Translates” Buffett-Beating Gains Into Income

That’s the perfect segue into the CEF I want to spotlight today, the Columbia Seligman Premium Technology Growth Fund (STK). As you can see below, STK (in orange) outperformed Berkshire (in purple) over the last decade.

STK Tops the Oracle

In fact, not only has STK outperformed, but it’s delivered a large slice of those gains as income. The fund yields 6.6% as I write this, and its normal payouts have stayed rock steady over the last decade. Plus, STK has paid out a lot of special dividends, that make its total yield to investors even bigger.

Even ignoring those special payouts, investors who stuck with STK over the last decade would now be enjoying a 9.8% yield on their original buy, since STK’s unit price has nearly doubled in that time. So they’d be getting a bit less $100,000 per year for every million dollars invested, again before we consider those special dividend payments over the years.

Will this continue? It depends whether tech will stop being a major part of our lives and whether Wall Street will forget the value-investing strategies Buffett espoused. I think you’ll agree that neither scenario is very likely.

This 11% Dividend is Backed by the Steadiest NAV We’ll Ever See

Brett Owens, Chief Investment Strategist Updated: May 7, 2025

Vanilla investors fixate on price. We contrarians know better.

It’s all about the NAV. Net asset value, baby.

Price is what people pay at a given moment. But people panic. Many like to buy high—and sell low!

NAV, on the other hand, is what something is worth at that same moment. Price and NAV can become disconnected, especially during emotional market moments. When this happens, it is often a buying opportunity for careful contrarians like us.

Let’s take a pop quiz. Think about the funds you hold in your portfolio. What was your top performing NAV for the month of April?

I’ll share mine, with respect to our Contrarian Income Report portfolio. FS Credit Opportunities (FSCO) wins the top award for CIR with an unwavering NAV during April, the most volatile month since March 2020!

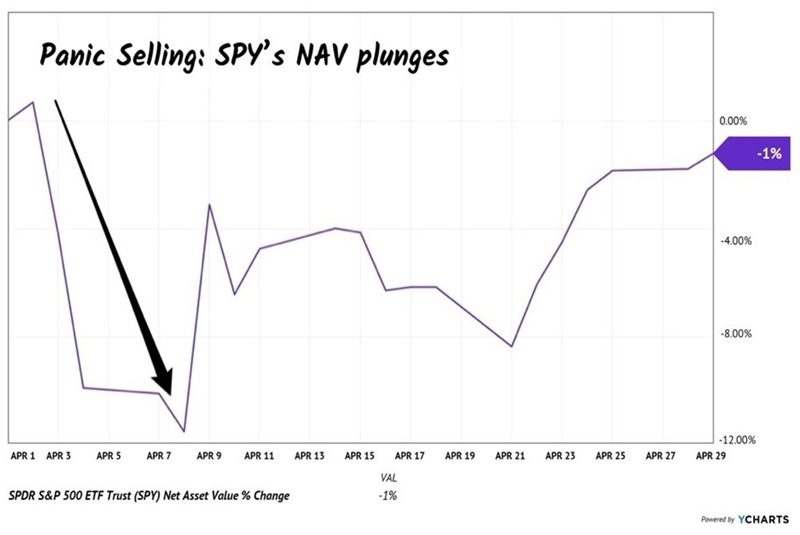

Dark it was. April 2025 began with a 12% drawdown in the S&P 500. “America’s ticker”—the SPDR S&P 500 ETF Trust (SPY)—took a licking! SPY’s NAV fell by an equal amount as its price—nearly 12% in 8 days—because investors dumped shares in the 503 stocks it owns. SPY’s NAV is “marked to market” constantly as its underlying shares trade.

This is the drawback of an NAV that is attached to other publicly traded positions. If the contents of the basket plummet in a panic, so does the fund’s NAV wrapper:

SPY’s NAV Plummets in April’s Panic

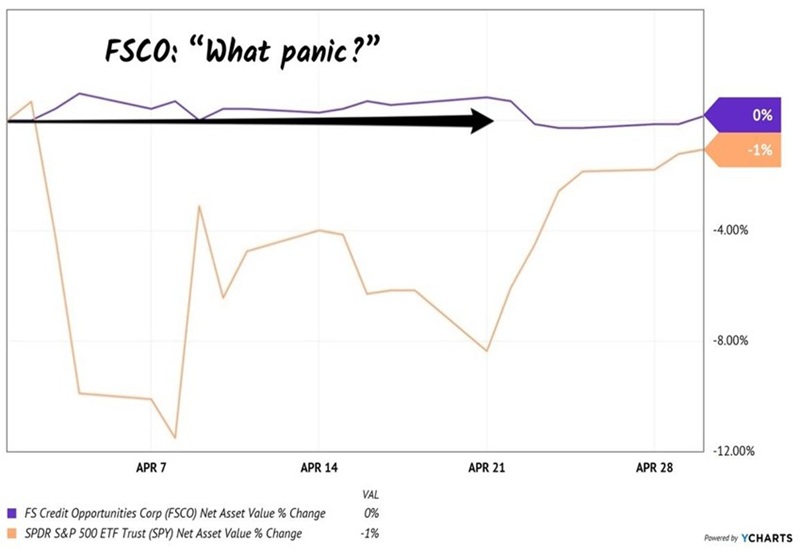

FSCO does not have this problem because its investments are in the calculated, relatively calm private markets rather than the manic, often-panicking public. The team extends private market loans, where FS can dictate favorable terms that secure its NAV.

Think of FSCO as a BDC (business development company) in a CEF wrapper. But it’s better than most BDCs. FSCO uses lower leverage and has a lower cost structure than the sector-at-large. Case in point, VanEck BDC Income ETF (BIZD) saw its NAV drop nearly 14% in the first eight days of April!

But while SPY and BIZD were in NAV freefalls, FSCO’s portfolio held up incredibly well. It didn’t budge!

FSCO’s NAV Unmoved in April’s Panic

With such an impressive pedigree, you might guess that FSCO trades at a premium to its NAV because every income investor on the planet would want in. The fund pays an 11% payout in monthly installments, and its NAV never moves. What’s not to like?

Amazingly, though, FSCO has traded at a discount since we first covered it here at Contrarian Outlook. In fact, when we added it to our Contrarian Income Report portfolio in October, it offered a 10% discount. Which meant this fine fund was a first-class find—available for just 90 cents on the dollar!

Why? The fund has been around for 10+ years but only traded publicly as a closed-end fund for the last two. CEF investors loathe newness. We want proof the income will last.

So. I called Josh Blum, Head of Investor Relations for FS Global Credit, to discuss. How is this incredible performance even possible during the most volatile month in recent memory?

“The NAV resilience reflects the focus on senior secured and structured credit strategies, which tend to exhibit lower correlation to the broader equity market movements,” Josh explained to me.

Portfolio manager Andrew Beckman and his team are skilled at “layering” credit, or structuring loans with different levels of protection, so that FSCO is positioned to get paid back first even if credit conditions worsen. Josh went on to explain that Beckman also deploys hedges from time to time to smooth out volatility.

“Strong underwriting fundamentals and limited mark-to-market exposure further supported the NAV stability,” Josh continued. His key point here is that FSCO is extending high-quality loans that are not subject to the daily whims of the public markets. These are private credit vehicles held by sophisticated investors who don’t care if the S&P 500 is down on a given day—they want their yield!

As do we income investors. Since we added FSCO to our Contrarian Income Report portfolio in October, this fund has been a rock with no NAV movement. This has not limited our gains, though! We have enjoyed total returns of 13.1% thanks to monthly dividends and price gains from FSCO’s shrinking discount window. These returns annualize to a terrific 23.4%.

FSCO Since October Add to CIR Portfolio

All looks great in the rearview mirror! But I wanted to know how conditions “on the ground” are looking to FS Credit today. Josh elaborated:

“We remain cautious credit pickers looking for value-based opportunities. Private credit remains a very large focus, but if public markets become dislocated due to tariff-driven volatility, we will migrate to that opportunity set from time to time.”

For us income investors, FSCO is a fantastic opportunity.

With funds like FSCO, we can turn our portfolios into monthly income machines.

Is now the time to go bargain hunting, and where might we look?

QuotedData

Global equity markets have been grappling with a wave of challenges in recent months, leaving investors navigating a landscape marked by uncertainty and contradiction. From the disruptive flare of Trump’s so-called “Liberation Day” tariffs – briefly lighting a match under global trade tensions before a swift retreat – to elevated concerns over inflation (will interest rates rise?) and the growing spectre of economic slowdown (or will they fall?), the macroeconomic backdrop remains fraught.

With signs that the administration in the US is prepared to step back from some of the more extreme versions of its tariff policy, markets have staged a recovery of sorts, though the foundations of this appear fragile. Volatility and value now coexist in uneasy tandem, and in this environment, it is easy to see why funds that have a strong emphasis on capital preservation – the likes of Caledonia (CLDN), Capital Gearing (CGT), Personal Assets (PNL), and RIT Capital Partners (RCP) – are attracting attention. However, while investors might be unnerved by the noise, some are inevitably looking for the opportunities – particularly outside the US. We thought we’d turn our attention this week to areas of the market that we think look interesting and could benefit if the outlook and confidence improve.

Global equity markets and the UK equity market, in particular, are awash with value at present. Digging deeper, Europe and the UK seem to have benefitted from the turmoil more than most, but they had previously been amongst the laggards, so there is an element of catchup and rebalancing here. However, most, if not all, global equity markets look cheap versus their longer-term averages, and even their valuations just a few short weeks ago. The investment companies that hold them have generally seen their already wide discounts expand further.

Speaking to fund managers, they are not short of ideas and, if anything, face a problem of abundance. The consensus seems to be that, despite the turmoil being born in the US, that market still appears more fully valued than most, held up by its tech stocks. In contrast, European, UK and Asian equity markets are viewed as better pools to fish in.

Trump’s tariffs risk inflating prices for everyone, and against a risk of higher inflation and associated higher interest rates, already cheap growth stocks have de-rated even further. Cyclically exposed stocks have derated on concerns that the risk of recession or significant slowdown has increased. At the same time, more defensive allocations that are sensitive to interest rates – think utilities, infrastructure, renewable energy infrastructure etc – that tend to have long term debt – have been weighed down by concerns that interest rates may go up and may face less demand if there is a significant slowdown. In many instances this is a fallacy, as these assets frequently benefit from strong inflation linkages and so are able to pass through and may even benefit from a higher inflation environment over the longer-term. However, the economic impacts of Trump’s tariffs are broad, and it is little surprise that most areas are affected.

Of course, if it turns out that investors’ expectations turn to falling rates to combat lower growth, the reverse could be true. The window of opportunity to buy interest rate sensitive trusts might be small.

Turning to investment ideas, the UK still looks very cheap, with growth stocks and small cap stocks particularly affected. Funds such as BlackRock Throgmorton (THRG) and Montanaro UK Smaller Companies (MTU), both of which have particularly strong focuses on growth in the UK small cap space, repeatedly report that the underlying companies in their portfolios continue to perform well at an operational level but this is not being appreciated by the market. Both appear to have significant latent value within their portfolios and, having previously traded at premiums during more buoyant times, we think these could rerate strongly if the economic outlook improves and interest rates start to move down again.

As its name suggests, Baillie Gifford UK Growth is another UK trust with a strong emphasis on growth. Its manager tells a similar story of strong operational performance that is not being appreciated by the market. If the outlook for growth stocks improves, this could benefit from a significant rerating.

We have been saying that the prevailing discounts within the renewable energy infrastructure sector look too wide, with very limited exceptions. We like funds such as Bluefield Solar Income (BSIF), Next Energy Solar, Downing Renewables and Infrastructure, Foresight Environmental Infrastructure and TRIG. We think that all of these have competent management teams and dependable income streams with strong inflation pass throughs. However, their discounts don’t seem to reflect this.

Aquila European Renewables (AERI), currently in managed wind down, also warrants a mention in our view. It recently sold an asset at NAV (click here to read more) and while there can be no guarantee that all sales will achieve NAV, recent transaction history shows that sales of renewable energy assets regularly achieve their carrying values and it is not uncommon for these to be priced at a small premium to NAV. Given this context, AERI’s c.35% discount looks significantly overdone, even allowing for some uncertainty around the costs of liquidating the rest of the portfolio and winding up the trust.

We also like Greencoat UK Wind (UKW), although this has struggled against a backdrop of lower-than-expected wind resource for a few years.

In the renewables space, the recent bidding war over Harmony Energy Income (HEIT) highlights that the hefty discounts of the battery storage funds do not make sense – c. 40% for Gresham House Energy Storage (GRID) and c38% for Gore Street Energy Storage at the time of writing – and it is a similar story in infrastructure.

BBGI Global Infrastructure (BBGI) is trading at a small premium at the time of writing following a bid from the Canadian pension fund British Columbia Investment Management (BCI). Pension funds take a long-term view and so it is easier for them to look through the current market noise. Good arguments can be made that some of the NAVs are currently depressed by elevated discount rates (and lower power prices in the renewable energy infrastructure space that have potential to revert) and the reality is that BCI likely still sees value in BBGI’s assets given that it is prepared to pay a modest premium to NAV to acquire them. We like funds such as Pantheon Infrastructure (PINT), GCP Infrastructure (GCP), HICL Infrastructure (HICL) and Cordiant Digital Infrastructure (CORD). We also like 3i Infrastructure (3IN) and think this has recovery potential but its discount is not as attractive as the others.

HydrogenOne Capital Growth (HGEN) and Seraphim Space (SSIT) hold earlier stage speculative investments that have a significant proportion of their value discounted back from some point in the future. In both cases, the opportunity set is huge, and we think both could rerate strongly if the outlook improves and interest rates recede.

The recent stock market volatility seems to have subsided… for now. But that gives investors a chance to get ready for the next downturn.

Posted by Stephen Wright

Published 10 May

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.Read More

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services

The stock market seems to have shaken off the tariff announcements that caused prices to fall sharply. But it’s almost certain to crash again at some point the time to prepare is now.

Predicting when the next downturn is going to come is almost impossible. Despite this, there are things investors can do to make sure they’re as ready as possible.

When’s the next crash?

Share prices might have recovered from the effect of US tariff announcements. But I’m not sure the stock market is entirely out of the woods yet.

So far, there hasn’t been any sign of the impact of these policies on corporate profits. That, however, is likely to change over the next couple of months.

There are no guarantees – and I’m certainly not making predictions – but companies reporting lower profits and lowering guidance is a real possibility. And that could weigh on prices.

The strong recovery means anyone who felt uneasy when the market crashed in April now has a chance to get ready for the next downturn. And there are a few ways of doing this.

Portfolio allocation

In the last downturn, some stocks held up better than others, which is not at all unusual in a stock market crash. But investors should pay attention to what these might be.

Anyone who’s concerned about volatility in the near future might want to consider companies like Coca-Cola. While the S&P 500 fell sharply, the stock held up relatively well.

The time to consider buying this type of stock, however, isn’t when other investors are trying to find safety in a crisis. It’s when they aren’t thinking about this and are looking elsewhere.

Right now, I don’t think Coca-Cola looks like exceptional value. But there are some opportunities elsewhere that I think could be useful additions to a portfolio.

Unilever

FTSE 100 consumer products company Unilever (LSE:ULVR) is an interesting stock to consider. It has a lot of the hallmarks of a stock that can be resilient in a volatile stock market.

Demand for the firm’s products tends to be relatively resilient. It makes things that people need on a day-to-day basis regardless of what’s going on in the wider economy.

The risk with this type of business is that barriers to entry are low and this can make the space competitive. That means it’s important for a company to find a way to differentiate itself.

Unilever looks to do this with strong brands and wide distribution. These give the firm a big advantage when it comes to negotiating with retailers, which sets it apart from its rivals.

Long-term investing

Over the long term, having a strong competitive position in a durable and growing industry is valuable. And this is what makes Unilever attractive from an investment perspective.

I think it’s also an interesting stock for investors to consider as a way of preparing for the next stock market crash. I’m certain there’s going to be another one, the only question is when.

The time for investors to figure out how to prepare for this, though, isn’t when it’s already happening. With share prices having more or less recovered, the time is now.

These 10 FTSE income stocks could generate £33,137 a year in dividends

Our writer looks at the highest-yielding income stocks on the FTSE 350 and considers what level of return they might generate.

Posted by

James Beard

Published 10 May

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in

The 10 FTSE 350 income stocks with the highest yields are currently offeringreturns of 9.4%-14.1%, with an average of 11.3%. This means a £20,000 investment spread equally across all of them would generate annual passive income of £2,260.

But reinvesting the dividends couldgenerate better long-term returns. Using this approach, a £20,000 lump sum would grow to £290,676 in 25 years.

This assumes the annual return of 11.3% is maintained throughout the period and that all income is used to purchase more shares. If all goes to plan, after a quarter of a century, this 10-stock portfolio could be generating dividends of £33,137 a year.

Stock

Yield (%)

Diversified Energy Company

14.1

Ithaca Energy

13.0

Harbour Energy

12.8

NextEnergy Solar Fund

11.6

Ashmore Group

11.3

Energean Oil & Gas

10.8

Foresight Solar Fund

10.4

TwentyFour Income Fund

10.2

GCP Infrastructure Investments

9.5

aberdeen Group

9.4

Average

11.3

Source: Trading View at 9 May based on dividends paid during the preceding 12 months

However, we must not get too carried away.

Buyer beware

Although there’s nothing wrong with the maths in my example, it pays to be careful when a stock offers an apparently high yield.

For example, even though Diversified Energy Company is top of the list, it was yielding over 30% in early 2024. Soon after, it cut its dividend by two-thirds. Although it’s still number one, this does illustrate that double-digit returns should be treated with caution.

Some experts claim that if a stock’s offering a return twice that of the 10-year gilt rate (currently 4.45%), it’s probably not sustainable. In fact, all of the stocks on my list would break this rule of thumb.

Also, my analysis ignores any movements (up or down) in share prices.

Something in common

I think it’s interesting that seven of the stocks have exposure to the energy sector.

Some of them operate in renewables where long-term contracts and relatively fixed costs ensure earnings are, generally speaking, steady and predictable.

However, this doesn’t apply to Harbour Energy (LSE:HBR). As the largest oil and gas producer in the North Sea, its profit is at the mercy of energy prices, which are often volatile.

And its near-13% yield is partly due to a share price that, on the back of a slump in oil prices, has fallen 43% since May

Other issues

I suspect investors also have concerns that the group faces an effective tax rate of 78% on its UK profit. That’s why, in 2024, it acquired the upstream assets of Wintershall Dea.

Although it hasn’t helped the share price, the deal has transformed the scale of the group. This is evident from Harbour Energy’s most recent trading update. For the first quarter of 2025, revenue was $2.8bn, compared to $0.9bn a year earlier.

The acquisition means it’s now operating in Norway — and other countries — where taxes are lower.

On 7 May, the group blamed the ‘windfall tax’ for its decision to cut 25% of the workforce at its headquarters in Aberdeen.

And these cost savings are expected to offset some of the impact of lower energy prices. This means free cash flow, in 2025, is forecast to be only $100m lower than the $1bn previously estimated. The annual dividend currently costs $455m.

Earnings should also be helped by an upwards revision in forecast production.

For these reasons, I suspect Harbour Energy’s yield will start to fall over the coming months. Not because of a cut in its dividend but due to a rising share price. On this basis, those looking for an income share with solid growth prospects could consider the stock.

Note: Twenty Four Income yield is dependant on their final dividend, which is not guaranteed.

Current quarter dividend 2p. Recently paid final dividend 5.07p

12 May ’25

12 May ’25