It’s interesting to see how timing plays a crucial role in maximizing returns. The chart clearly highlights the potential to double your stake with the right strategy. The current yield of 4.77% and the discount to NAV of 4.3% seem promising for investors. How does the timing of entry and exit impact the overall yield in this scenario?

If we refer back to the chart.

Around the covid low the price was 500p and the dividend was 29p a yield of 5.75%. At this time lots of shares reduced their dividends and that is one reason the Snowball invests mainly in Investment Trusts because they have reserves of your cash, if you are a long time holder, to use to top up the dividends in times of market stress.

At the recent low, marked on the chart, the price 660p and the dividend 35.4p a yield of 5.1%.

Its worth noting at the covid low buying price of 500p the current dividend yields 7%.

The Merchants Trust (MRCH) has been highlighted as having increased its dividend year on year for 41 consecutive years by AIC.

You would have been fearful to buy as the price might continue to fall but with a buying yield of 9% at the low, you could have thought it was time buy.

Nearly achieved the Holy Grail of investing, that you could take out your stake, and earn income at a zero, zilch cost.

Plus income from the dividends re-invested into your Snowball

Current yield 5.31% Discount to NAV 2%

09/04/2025

Merchants Trust PLC on Wednesday said its performance fell only slightly short of its benchmark in its recent financial year, saying recent global market volatility shows the advantages of investing in UK listings.

The investment trust, which dates back to 1889, invests in high-yielding UK large-cap companies.

Merchants Trust said net asset value on January 31, the end of its financial year, was 572.6 pence per share, up 7.9% from 530.9p a year before. NAV total return, including dividend payments, was 13.5%, compared to 17.1% for the FTSE all-share index.

The company said the lag was primarily due to its investments in mid- and small-cap stocks, while recently the market has favoured larger companies. It also said its focus on “high and rising income” from its investments takes priority over total return.

Merchants Trust declared a final dividend of 7.3 pence, bringing the total payout for financial 2025 to 29.1p, up 2.5% from 28.4p in financial 2024. It noted that financial 2025 represented its 43rd consecutive year of dividend growth.

Chair Colin Clark noted that the UK companies in which the trust invests have substantial global exposure, with revenue coming from around the world. “It is important to remember that being UK-listed does not mean a company’s fortunes are tied solely to the UK economy,” he said.

“This is particularly relevant at a time, such as now, when international investors, and sometimes even UK investors, are gloomy about the domestic economic outlook.”

Looking ahead, Clark said, “it remains challenging to predict when investor interest will return to the UK stock market, when UK valuations will re-rate to more ‘normal’ levels.”

He added that Merchants Trust will remain a “patient contrarian investor”. “Our manager believes that many opportunities exist to invest in well-managed, financially strong companies on attractive valuations.”

Here are ten closed-end funds (CEFs) with notably high distribution yields as of early 2025. These funds span various sectors, including fixed income, infrastructure, and energy, offering diverse opportunities for income-focused investors:

🔟 Top High-Yield Closed-End Funds

PIMCO Dynamic Income Fund (PDI)

Yield: 13.7%

Focus: Multi-sector bonds, including high-yield credit and mortgage-backed securities.

Strategy: Covered-call writing on a diversified equity portfolio, with significant exposure to the technology sector.

Top Holdings: Includes major tech companies, benefiting from sector growth. Seeking Alpha

BlackRock Credit Allocation Income Trust (BTZ)

Yield: 9.2%

Focus: Investment-grade and high-yield corporate bonds.

Advantage: Trades at a discount to NAV, offering potential value for investors.

⚠️ Considerations for Investors

Premiums and Discounts: Some CEFs trade at significant premiums (e.g., GUT), which can increase risk, while others at discounts (e.g., AVK, BTZ) may offer value opportunities.

Distribution Sustainability: High yields are attractive, but it’s crucial to assess whether distributions are covered by net investment income or rely on return of capital, which may not be sustainable.

Leverage Risks: Many CEFs use leverage to enhance yields, which can amplify both gains and losses, especially in volatile markets.

Tax Implications: Consider the tax treatment of distributions, especially if investing through tax-advantaged accounts.

Given your location in England, it’s important to consider currency exchange risks and potential tax implications when investing in U.S.-based CEFs.

If you need further information on any of these funds or assistance in aligning them with your investment goals, feel free to ask !

10.7% and 12.3% yields ! 2 dividend stocks to consider in May

Looking for ways to make a supercharged passive income over the next year? Here are two top dividend shares to consider.

Posted by

Royston Wild

Published 30 April

FGEN NESF

Image source: Getty Images

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.Read More

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

2025 is shaping up to be a tough one for global stock markets. With the global economy under growing stress, the opportunity for investors to make healthy capital gains may be limited. In this climate, the best way to target a positive return may be by buying high-yield dividend stocks.

Following recent stock market volatility, investors have an excellent chance to make a market-beating passive income this year. Dividend yields across the London Stock Exchange have shot higher, and many top shares now offer yields miles above the 3.6% average for FTSE 100 shares.

2 top dividend shares

With this in mind, here are two of my favourites to consider in May.

While dividends are never guaranteed, here’s why I think these passive income stocks merit a close look.

Green machine

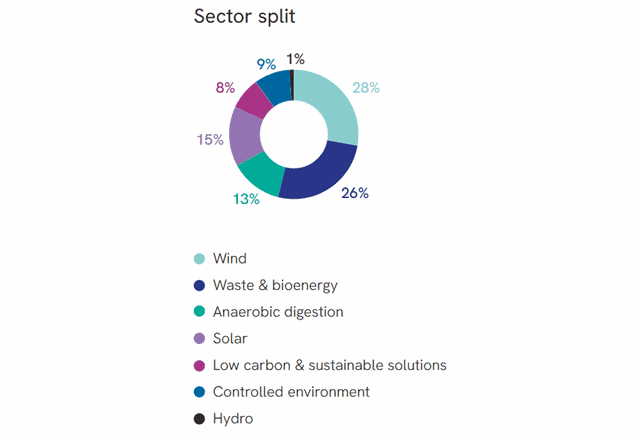

Despite recent pushbacks against the ‘green agenda,’ companies that produce renewable energy, promote sustainability and champion resource efficiency still have tremendous investment potential, in my book. Foresight Environmental Infrastructure is an investment trust whose broad operations support the long-term fight against climate change.

The company owns more than 40 assets in the UK and Mainland Europe. These range from Scottish wind farms and energy-from-waste plants in Italy, to battery storage projects and wastewater facilities in England.

What’s more, the company’s portfolio is diversified intelligently across these assets types. This provides resilience when, for example, cloudy weather conditions impact power generation from its solar assets. Dividends here have risen each year since 2011, underlining the stability that its operations provide.

Source: Foresight Environmental Infrastructure

For 2025, the predicted dividend is covered 1.2 times by operational cash flow, providing a decent margin of error. I think it’s a top defensive dividend share to consider, even though earnings could be impacted by rising inflation that pushes interest rates higher.

Sun king

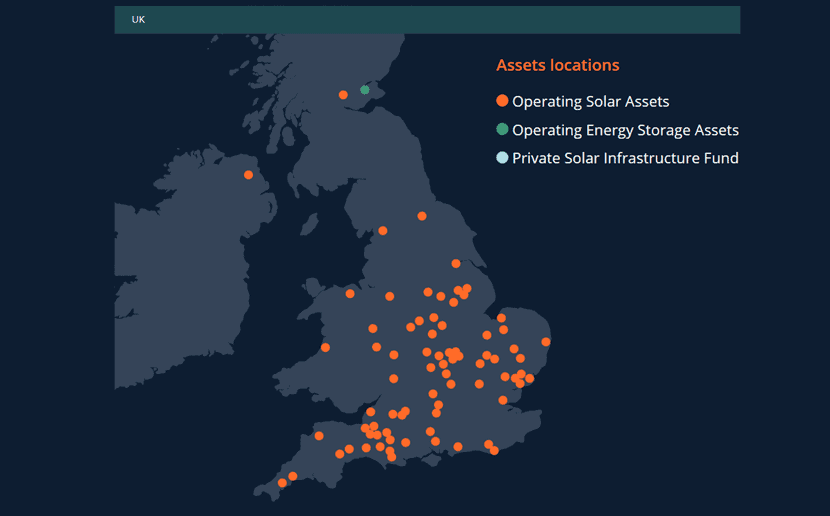

NextEnergy Solar Fund is another renewable energy stock I feel is worth close look. With a dividend yield above 12%, it’s one of the highest yielding dividend shares across the whole London stock market.

Unlike Foresight Environmental Infrastructure, its operations aren’t divided across a wide range of technologies. As its name implies, the lion’s share of its portfolio is dedicated to solar farms (it currently has 101 operating projects on its books). Meanwhile, its energy storage asset base comprises of just one operating site.

While this creates greater risk, this isn’t to say that NextEnergy Solar isn’t still well diversified. Its UK farms cover the length and breadth of the country. It also owns solar projects in Italy, Spain and Portugal.

Source: NextEnergy Solar Fund

Dividends here have risen each year for around a decade, and it has returned around £346m in cash rewards since its IPO in 2014. With a strong balance sheet — it’s also undertaking share buybacks of up to £20m — I’m expecting the fund to remain a great dividend payer.

As a long-term investor, I like buying shares in good businesses at fair prices. Also, my investing style nowadays favours value shares and passive income. Thus, when share prices plunge — as they did during the recent market meltdown — I see these falls as opportunities to buy at a discount.

Hence, I’m often drawn to cheap shares offering market-beating dividend yields to patient shareholders. As my family doesn’t need this income right now, we reinvest our dividends by buying more shares. Over time, this increases our corporate ownership and boosts our total long-term returns.

Passive income from dividends

Though share dividends are my favourite form of passive income, they’re no sure-fire route to riches. Indeed, returns from value/income investing have lagged behind those from growth investing for most of the last 15 years. Also, these three problems can cause problems:

Future dividends aren’t guaranteed, so they can be cut or cancelled at short notice. For example, during 2020-21’s Covid-19 crisis, dozens of UK companies slashed their payouts to preserve cash.

After paying out dividends, companies have less cash at hand. Therefore, paying out excessive dividends can weaken companies over time.

After paying out dividends, companies have less cash at hand. Therefore, paying out excessive dividends can weaken companies over time.

Super-high dividend yields, say, 10%+ a year, can warn of future problems. History has taught me that double-digit cash yields rarely last. Either share prices rise, or dividends get cut, dragging down yields.

Three shares would deliver an average dividend yield of 9.8% a year. Therefore, a mini-portfolio of equally weighted holdings in all three stocks would generate passive income of £1,961 annually. Furthermore, this cash stream would be tax-free inside a Stocks and Shares ISA.

In particular, I like the look of M&G as a long-term producer of passive income. M&G was founded in 1931 and launched the UK’s first unit trust that same year. The current share of 186.75p translates into a huge cash yield of 10.8% a year. But this yield has leapt due to recent falls in the M&G share price. This is down 13.4% over one month and 7.2% in a year, but is ahead 43.4% over five years (excluding dividends).

Then again, what if things turn sour again for financial markets, as happened recently? With £312bn of assets under management, M&G’s profits and cash flow could get slammed if stock and bond prices plunge further. Even so, I note that its yearly dividend has risen from 15.77p a share for 2019 to 20.1p for 2024. In short, this passive income looks sound to me!

The post This £20k ISA delivers £1,961 of cash passive income a year appeared first on The Motley Fool UK.

Of course, there are plenty of other passive income opportunities to explore. And these may be even more lucrative:

We think earning passive income has never been easier

Do you like the idea of dividend income?

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

What is the current forecast for the Snowball’s total value, and what is the plan to achieve a 20% income on seed capital within ten years ?

This year’s income fcast is £9,120 with a target of £10,000.

If the target is achieved and the income is re-invested at a yield of

7% or greater the income received will double in ten years time.

Over the total time frame it may not be able to re-invest the dividends in Investment Trusts at 7%, although there are usually Investment Trusts that are out favour, then it would have to be re-invested with an element of capital gain.

If you’re ready to take a risk on the stock market, be sure to use our tips in the right way.

James Baxter-Derrington Investment Editor. Richard Evans

There are profits to be made with a prudent and well-diversified investment strategy Credit: Daniel Ceng/Anadolu

Investing is a volatile game. In the space of just a few weeks a stock can double in value or be completely wiped out, and it can require nerves of steel to see through the red numbers.

Since 1945, we have witnessed more than a dozen bear markets, defined as a sustained period in which stock markets collapse more than 20pc in value. During the Global Financial Crisis, stocks fell over 50pc, more than halving your investment on paper.

But zoom out and these cataclysmic financial events pale in comparison to the returns investing offers over the long time. Had you invested £10,000 in the S&P 500 at the highest level before the 2008 crash – the “worst time” to buy – it would have fallen as low as £4,300 – but had you left it invested, it would’ve been worth over £37,000 at the end of 2024.

Stock markets are comprised of individual companies, and we feel there are excellent profits to be made by picking the right firms as part of a prudent, well-diversified investment strategy.

Had you put that £10,000 into, for example, Games Workshop, on that same day in October 2007, it would have been worth £505,100 at the end of 2024. If you’d put it into Lehman Brothers stock, it would be worth £0.

To avoid wipe-out and ensure you reap the benefits of investing, we’ve put together this short guide to how our Questor tips should be used.

When we say a stock is a “buy”, we mean that we have good reason – based usually on the opinions, and more importantly the actions, of professionals whose job it is to scrutinise stocks – to expect the price to rise. But nothing is certain in investment and even the most experienced, intelligent and well-informed professionals can have their expectations confounded by events.

In fact, fund managers sometimes say they are doing well if 60pc of their holdings make money.

Faced with these odds, we urge readers never to follow individual tips in isolation. Instead, it is vital that investors protect themselves against the risk of severe, even total, losses of money by the most potent protective medicine in stment: diversification.

So if you are a new Questor reader and have read a column you believe makes a convincing case for buying a particular share, by all means act on it – but in such a way that the stock forms part of a portfolio of shares and does not become the sole home for your hard-earned savings.

Let’s imagine you have £100,000 to invest for your retirement. You read a convincing case in Questor, or elsewhere, for buying a particular stock. Whatever you do, no matter how strongly you believe in that stock, do not commit your entire £100,000 to it.

Instead, limit your purchase to £10,000, or ideally less, and continue your stock research until you have identified another nine shares, or more, into which you are equally happy to commit your money. In other words, spread your cash among at least 10 shares and preferably nearer 20.

These shares should not include more than a couple that are particularly risky or speculative, normally labelled as such in this column. Aim to own companies that operate in a variety of sectors and are exposed to different aspects of the economy.

The only time you should feel free to disregard the advice above is when you are committing sums small enough to be regarded as punts. An investor with £100,000 in total might feel comfortable putting £1,000 into one stock on the basis that if it does go bust the loss is bearable.

But for serious investors who intend to commit the bulk of their life savings to stocks, diversification is essential.

If you do want to put serious sums into the stock market but do not wish for any reason to do the work necessary to identify the 10 or more stocks needed for a prudent level of safety, invest your money in funds instead.

It is still better to invest in a selection of funds than commit all your money to one, but the latter course is much less risky than it is with individual shares.

Anyone who has already put large sums into one or two of our stock picks is advised to sell the bulk of those holdings as soon as possible and reinvest the money in several other shares so as to build the kind of diversified portfolio outlined above.

Finally, remember that even with a portfolio of stocks there is still a risk the entire market could fall severely. Be prepared to hold your stocks for enough time to ride out the ups and downs.

If you are not able to accommodate these risks, do not put money in the stock market.

laire Boyle, Chair of Life Science REIT plc, commented: “As announced on 14 March 2025, the Board is currently undertaking a strategic review to consider the future of the Company and to explore all options available to maximise value for shareholders. The background to this decision was set out in that announcement and reflects the significant headwinds the Company has faced since IPO, including higher inflation and elevated interest rates, which have driven a fundamental slowdown in leasing activity and negatively impacted investor sentiment. Coupled with the Company’s size and low levels of liquidity, these factors have resulted in the Company’s share price trading at a significant discount to net asset value for a prolonged period of time. The Board is confident that the Company’s assets, which are focused on the “Golden Triangle” research and development hubs of Oxford, Cambridge and London’s Knowledge Quarter, will prove attractive to a number of parties. Given the uncertainty inherent in the possible outcomes of the Strategic Review, these results have been prepared on a going concern basis with material uncertainty. In addition, in recent weeks, the Board has successfully reached an agreement with Ironstone Asset Management (“Ironstone”), the Company’s Investment Adviser on a revision of the Investment Advisory Agreement, which will deliver cost savings of c. £1.0 million per annum based on the December 2024 net asset value. In the meantime, the team remains sharply focused on capturing upside from the portfolio; £1.5 million of contracted rent has been captured since the interim results in September 2024, a further £1.1 million is in solicitors’ hands, and occupier engagement is encouraging.”

STRATEGIC REVIEW Strategic Review underway Commenced 14 March 2025 to explore all strategic options available to maximise value for shareholders, including a possible sale or managed wind down of the Company

FINANCIAL HIGHLIGHTS Development and leasing progress supporting rental growth, but slower than expected Contracted rent for the investment portfolio increased to £15.3 million (31 December 2023: £14.0 million), with a further £0.6 million from developments, taking total contracted rent to £15.9 million Adjusted earnings of £5.9 million (31 December 2023: £6.7 million), impacted by higher financing costs Adjusted EPS of 1.7 pence per share (31 December 2023: 1.9 pence per share) Future dividends suspended pending the outcome of the Strategic Review Valuations stabilising in the second half with yield expansion reducing Portfolio value £385.2 million (31 December 2023: £382.3 million), a £2.9 million increase on an absolute basis o H224 like-for-like decline of 0.3% compared to a 3.8% decline in H124 Like-for-like valuation down 4.0% driven by 30bps outward movement in the net equivalent yield (“NEY”) to 5.6%, more pronounced in H1, partially offset by like-for-like ERV growth of 13.7% o Laboratory space down 3.7%, with ERV growth strong at 8.6%; o Space defined as offices down 5.3% EPRA net tangible asset per share of 74.4 pence (31 December 2023: 79.9 pence per share); reflecting the portfolio revaluation loss (£17.4 million) and dividend payments (£7.0 million), partially offset by positive adjusted earnings Balance sheet: Loan to value at 30.4% (31 December 2023: 24.7%), with the increase driven by development progress in the year and corresponding debt drawn Debt fully hedged at 4.5% interest payable to March 2025 and 5.5% until September 2025

OPERATIONAL HIGHLIGHTS Leasing activity improved, but transactions taking longer to conclude than expected: Five new leases commenced in 2024, adding £1.9 million to total contracted rent Occupancy increased to 84.4% (31 December 2023: 79.0%); like-for-like occupancy increased to 83.6% (31 December 2023: 79.0%) Since the interim results in September 2024, £1.5 million of new rent has been captured, compared to the target set of £3.2 million, with a further £1.1 million in solicitors’ hands Current contracted rent increased to £16.5 million, including breaks exercised at Rolling Stock Yard of £0.7 million Cambourne repurposing project completed, delivering 8,800 sq ft of fully fitted space 57,000 sq ft completed at Oxford Technology Park (fully let to Fortescue Zero Ltd); formal practical completion of Buildings 6 – 9 comprising 183,000 sq ft delayed to Q2 2025, but unit 6A is effectively complete and fully let.