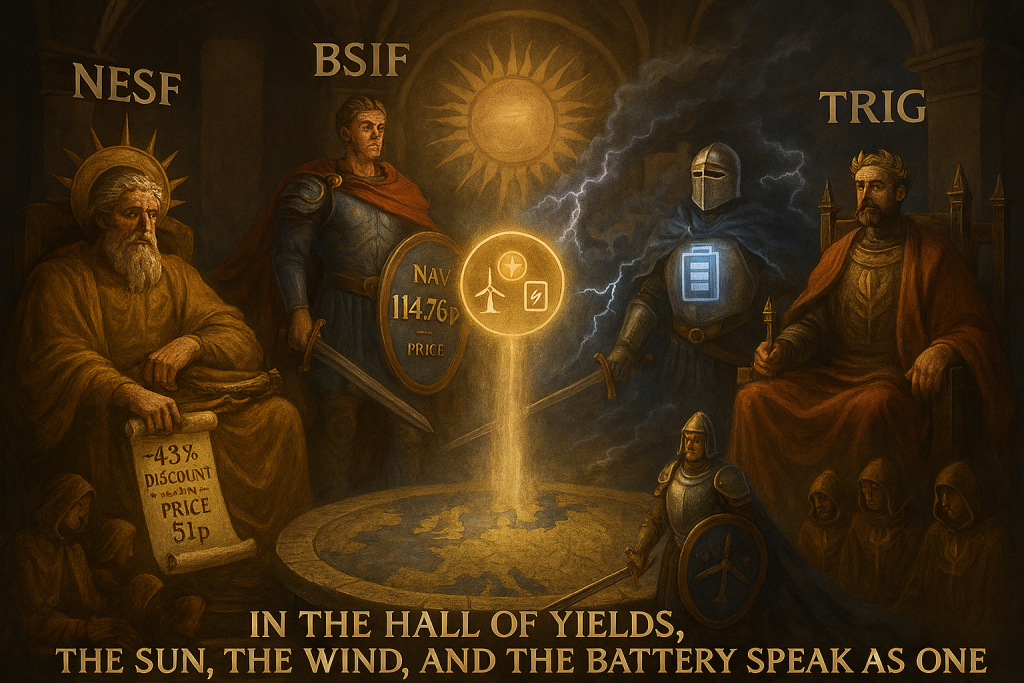

TRIG NAV falls on weaker power price outlook and higher offshore wind discount rates; shares slip

Fiona Craig

LSE:TRIG

Market News

16 February 2026

The Renewables Infrastructure Group (LSE:TRIG) posted a larger-than-anticipated quarterly decline in net asset value, as softer power price assumptions and higher discount rates for UK offshore wind assets weighed on valuations, pushing the stock 2% lower on Monday.

The renewable energy investment trust reported that NAV decreased 5.2% to 104 pence per share in the fourth quarter, down 5.7 pence from 109.7 pence at the end of September. The move translated into a negative total NAV return of 3.7% for full-year 2025.

Management attributed the decline primarily to a 1.8 pence per share reduction linked to lower consultant power price forecast curves, alongside a 1.2 pence impact from a 50 basis point rise in discount rates applied to UK offshore wind projects. A further 1.8 pence per share drag stemmed from generation coming in below budget and operational challenges.

An additional 0.6 pence per share reduction reflected changes to indexation of UK Renewables Obligation Certificates (ROCs), which will now be tied to the Consumer Price Index rather than the previous benchmark.

Electricity generation was 5% below budget during the fourth quarter, largely due to economic and grid curtailment in Sweden. However, this marked an improvement compared with the first half of 2025, when output fell 10% short of plan. Sweden accounts for roughly 14% of TRIG’s portfolio by NAV and has persistently underperformed expectations, analysts said.

“While generation missed budget by 5% in Q4, this is an improvement versus the performance earlier in the year,” said Joseph Pepper, analyst at RBC Capital Markets, which maintains an “outperform” rating on the stock with a 90 pence price target.

“We think management’s target future cover of 1.1-1.2x looks credible given inflation-linked cash flows and an improving debt amortisation profile, although we note that Sweden remains a consistently underperforming geography in the portfolio.”

TRIG reiterated its dividend target for fiscal 2026 at 7.55 pence per share, unchanged year-on-year. Net dividend cover for fiscal 2025 was reported at 1.0 times. On a gross basis, excluding annual amortising debt repayments, dividend cover stood at 2.1 times. Management continues to guide toward net dividend cover of 1.1 to 1.2 times over the medium term.

The company had previously cautioned that dividend cover would be “tight” for fiscal 2025.

Shares closed Friday at 69.20 pence, implying a discount of about 34% to the newly reported NAV, broadly aligned with the peer group average discount of around 35%.

“Given the quantum of the quarterly movement this morning we would expect shares to trade lower today,” Pepper said.

TRIG’s portfolio includes approximately 90 renewable energy assets across six countries, with about half of its exposure in the UK, leaving it sensitive to domestic regulatory developments and wholesale power price trends. The trust primarily invests in operational wind and solar projects, with UK offshore wind forming a substantial component of its holdings.

It is your duty to check the announced current dividends and any future dividends for the shares in your Snowball.

Two 9% Dividends on Sale (Up to 17% Off). Thank the Software Selloff.

Michael Foster, Investment Strategist Updated: February 16, 2026

The recent plunge in software stocks is another reminder that AI is rattling through the economy, setting off rapid change and disruption wherever it goes.

Investors sold software stocks on fears that new AI tools will make it easier for individuals to create their own apps, potentially taking business from software developers.

This is a big change—and here’s some news that might surprise you: For income investors, it sets up another way to tap AI’s growth for dividends. We welcome that; in the early days of AI, the only real ways to get in were through low- (or no-) payers like NVIDIA (NVDA).

Just last July, research had shown that software developers actually coded more slowly when using AI tools. Now that Claude Code and updated versions of Codex from ChatGPT are rolling out—and OpenAI is promising more tools for developers soon—software is turning into something users make for themselves, rather than buy from someone else.

Investors’ focus, as a result of this development, has been on software companies, specifically how vulnerable their businesses really are to this shift. But we’re not going to focus on that today. We’re more interested in the productivity gains these new tools will unleash—and exactly what impact they’ll have on our dividends.

Productivity in Overdrive

The bottom line here is that if everyone can create software, it will result in a consumer surplus that will support the economy. That could come in the form of consumers and companies saving money on software subscriptions; building their own, personalized tools; or requiring fewer developers.

This is a compelling story for investors, and it’s another in a long line of AI innovations behind the S&P 500’s 16% gain over the last year, ahead of its 10.5% average annual return. I see above-average stock performance continuing as these new tools boost productivity and free up more cash for other spending.

But let’s pause for a moment and try to come to grips with exactly how much of a productivity boost we can expect here.

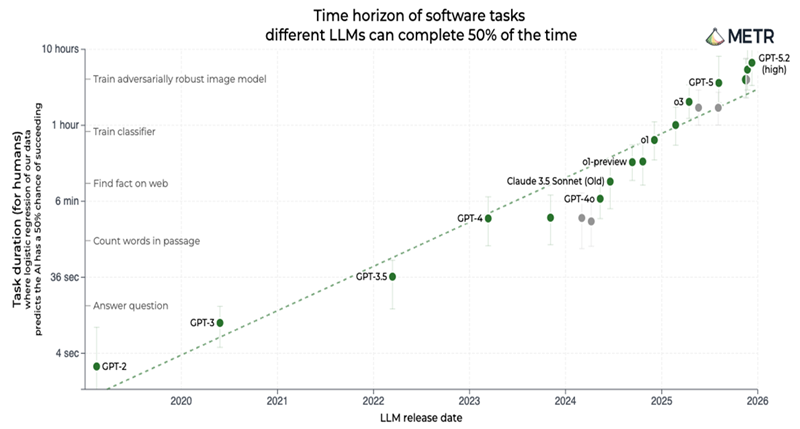

This is a pretty popular (and controversial) chart in the AI world. It tracks how long of a task an AI model can successfully perform. Right now, it shows that our third-best model can perform a task that would normally require 6.6 hours of human labor.

Our best models haven’t been tested yet because they were literally released in the last couple of weeks (things are happening that quickly!).

So while we do not know how much better our best models are, we do know that they are better. Time will tell. But what this really signals is that we’re past the debate of whether AI makes engineers more productive. We’re now debating how much more productive it will make them.

What’s the Dividend Play Here?

Those who hear “AI” and think “buy NVIDIA” are behind the curve (and not only due to the stock’s lame 0.02% yield!).

That said, we want to keep buying tech, even after the sector’s run-up in the last few years, but we want to focus on other sectors primed to benefit from AI’s strong potential, too: Utilities, for example, are well-known plays on AI’s soaring energy use, and data-center demand is likely to help real estate investment trusts (REITs).

Such a broad-based bullish story is best for income investors who are broadly invested in the market and have strong income to tide them over during micro-panics like the one that hit software stocks.

That’s why, rather than try to pick individual stocks, we look to CEFs that benefit from rising productivity across the economy.

This 9.3% Dividend Is a Smart Play on a More Productive Economy

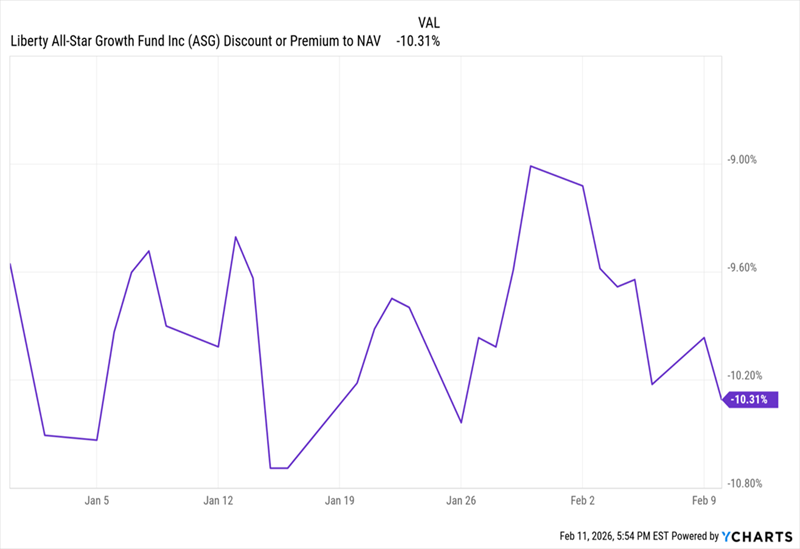

There are a lot of high-yielding closed-end funds (CEFs) that fit that bill. One of my favorites is the Liberty All-Star Growth Fund (ASG). This fund, a holding of my CEF Insider service, yields 9.3% as I write this.

ASG isn’t exclusively a tech fund, as it holds a basket of other stocks of all sizes, including property manager FirstService (FSV) and Pennsylvania-based Ollie’s Bargain Outlet Holdings (OLLI). But it does hold NVIDIA, alongside other blue chip tech stocks like Alphabet (GOOGL), Amazon.com (AMZN), Microsoft (MSFT), Apple (AAPL) and Meta Platforms (META).

Crucially, ASG also sports a wide discount to net asset value (NAV, or the value of its underlying portfolio). That’s because conservative income investors, in response to the pullback in software stocks, have oversold this growth-oriented fund.

ASG’s “Discount Dip” Serves Up a Solid Entry Point

The result is that we can buy ASG’s diverse portfolio for around 90 cents on the dollar.

We also like ASG for its dividend policy, as it ties its payout to the performance of its portfolio. So the better the fund’s portfolio performs, the faster the payout grows—a sweet setup in an economy getting a nice productivity boost.

A Deep-Discounted 9.6% Payer for Aggressive Investors

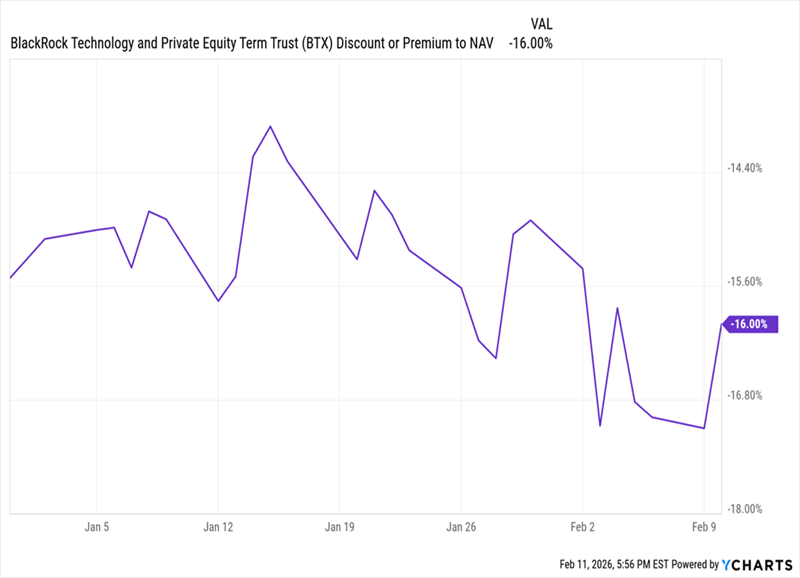

Another, more speculative option is the 9.6%-yielding BlackRock Technology and Private Equity Term Trust (BTX). As the name says, it has a wide variety of high-tech companies both public and private, such as NVIDIA (NVDA), quantum-computing firm PsiQuantum, Fabrinet (FN), whose technology helps manufacturing firms improve their processes, and AI infrastructure firm Celestica (CLS).

Gains from these stocks have helped shore up the fund’s dividend, so we’re looking at more income security in the near term.

And since most CEF investors are more conservative—and thus more easily spooked by negative headlines—this fund’s discount tends to fluctuate more widely than that of the more broad-based ASG. The recent software selloff has pushed it deeper into bargain territory.

Oversold BTX Trades for 84 Cents on the Dollar

Let me leave you with the idea that there are hundreds of CEFs that are well-positioned to profit from this revolution in automation. That shift is not being priced in because markets are moving too slowly to keep up with AI. That gives us a rare opportunity to buy high-yielding funds like these, whose discounts are unusually wide in relation to their history.

My 5 Top Monthly Dividend CEFs Pay Out 60 Times a Year (and Yield 9.3%, Too)

These two are just the start. Truth is, equity CEFs focused on rising productivity are at the very heart of my “60 Paycheck Dividend Plan.”

As the name suggests, the 5 CEFs that make up this “plan” each pay dividends monthly. That’s 5 dividend payouts a month, or 60 every year! They throw off a rich 9.3% average dividend between them, too.

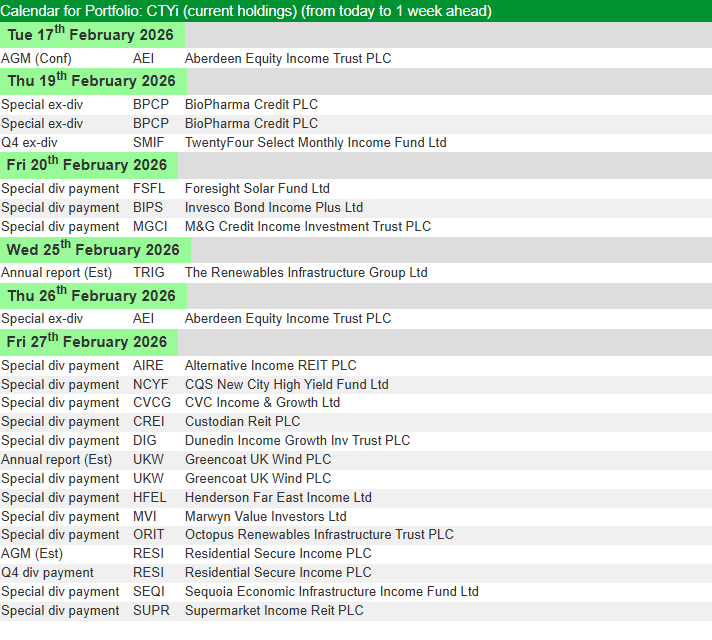

BioPharma Credit PLC ex-dividend date Greencoat Renewables PLC ex-dividend date Impax Asset Management Group PLC ex-dividend date Mountview Estates PLC ex-dividend date Shires Income PLC ex-dividend date

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Even with the UK stock market reaching new record highs lately, there are still plenty of FTSE shares offering generous dividend yields. And if these payouts can be maintained, investors could go on to earn an absurd amount of passive income.

That’s what’s brought Greencoat UK Wind (LSE:UKW) back in my sights. Renewable energy stocks continue to be unpopular in 2026. But new evidence is emerging that Greencoat shares could be a phenomenal long-term opportunity. And if that’s the case, its 10.6% payout could pave the way to exceptionally lucrative results.

So, is now the right time to go against the crowd and aim to earn a massive passive income?

Why is the yield so high?

Despite hiking its dividend by more than 130% since its IPO, Greencoat’s double-digit dividend yield stems from a painful fall in Greencoat’s share price.

Down around 35% since the start of 2023, the shares now trade at a 26.6% discount to net asset value (NAV). And to be fair, there are some valid concerns to justify this large discount.

In April this year, the Renewable Obligations (RO) scheme will be switching its inflation index from the retail price index (RPI) to the consumer price index (CPI). While CPI is a generally more accurate measure, it’s also often 1% to 2% lower than RPI, resulting in a significant reduction in long-term subsidy revenue for green energy generators.

At the same time, with more energy capacity being added to the national grid, long-term power price forecasts have been steadily dropping, placing further pressure on Greencoat’s projected cash flow. Combining all that with some fairly weak wind speeds over the last few years, it’s not surprising to see investor sentiment sour.

A hidden buying opportunity?

Despite some valid criticisms, investor pessimism looks like it could be overblown.

The near-30% discount to NAV doesn’t align with what’s happening in the private markets. The fact that Greencoat’s recent asset sales have occurred at NAV is evidence of that. And it shows there is a real disconnect between perceived value and actual value.

This valuation gap is something management has already been taking advantage of. By systematically buying its own stock at a substantial discount, not only is the firm boosting the NAV per share, but it’s also opening the door to a higher dividend per share simultaneously.

What’s more, policy uncertainty surrounding the RO scheme is now resolved. Meanwhile, looking at the group’s performance in the final quarter of 2025, even wind speeds have also started picking up again, with energy generation coming in just 1.6% below budget versus 14% across the first half of the year.

So, where does that leave investors?

Fluctuations in wind speeds remain a persistent threat. And prolonged periods of calm weather could be catastrophic for Greencoat, particularly given its fairly leveraged balance sheet.

However, with the share price barely moving despite substantial policy uncertainty being removed from the equation, it’s hard not to be tempted by the double-digit yield. Even more so, given that dividends are still entirely covered by cash flow.

So, with a favourable risk-to-reward ratio, Greencoat shares could be worth mulling over. But it’s not the only high-yield opportunity on my radar today.

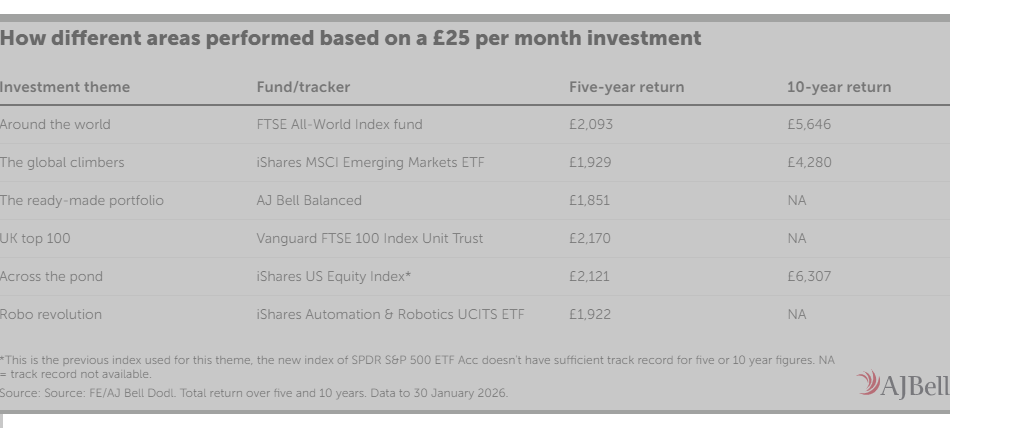

Investing just £25 a month could have netted you £6,300 in 10 years

Thursday, February 12

Laura Suter

Director of Personal Finance

Related news

When people think of investors they may imagine people with private yachts or thousands of pounds in the bank, but investing doesn’t have to mean big sums or expert timing to deliver decent results.

Putting away just £25 a month could grow into a sizeable investment pot over time, and the figures highlight the powerful impact of investing little and often. Over the past decade, even modest monthly contributions to global and US markets could have turned spare change into more than £6,000, underlining how time in the market can matter far more than the amount you start with.

If you put away just £25 a month, less than £1 a day, you could build up a tidy pot after a few years. Assuming 6% a year investment growth after charges, you’d have £1,793 after five years and £4,191 after 10 years. If you kept up the trend for 15 years, assuming those same 6% a year investment returns, you’d have just over £7,400 in your investment pot, or almost £11,700 after 20 years. The figures show how investing little and often can really add up.

Give your portfolio a pay rise

Often when people start investing they start small and set up a direct debit with the money invested automatically every month, making the process hassle free. This is a great way to reduce the time it takes to invest and means you don’t have to worry about trying to time the market. But the danger is that you start at £25 and never increase that amount, even when your earnings grow.

Typically, people’s wages grow over time, so you could also increase your contributions over your investment journey, to boost your investment pot over the long term. You could give your investment contributions a 5% pay rise every year, meaning they’d rise to £26.25 in the second year, up to around £38.75 a month by year 10. If you do this your portfolio benefits from a pay rise boost. If we assume the same 6% a year investment returns, you’d have £1,970 in your investment pot after five years, or £5,150 after 10 years. After 15 years that pot would have risen to £10,101 before hitting £17,612 after 20 years – almost £6,000 more than if you left the monthly savings at a static £25 a month.

Real world returns

If you want to start investing little and often you may find a simple tracker fund a good option, with many investment providers, like AJ Bell’s Dodl app, making it easy to choose from a range of funds and ETFs tracking a basket of assets.

Investing £25 a month into the FTSE All World Index Acc fund, Dodl’s global tracker of choice, 10 years ago would have left you with £5,646 today. Even if you’d only started five years ago, you’d be sitting on £2,093 today.

If you’d opted for a US focus, with the iShares US Equity Index, and invested £25 a month over the past 10 years you’d be sitting on £6,307 in your investment pot, or £2,121 if you’d invested over the past five years.

Tips for first-time investors

Before investing you’ll want to make sure that you’ve paid down any pricey debt, otherwise the interest you’re racking up on your credit card or overdraft will probably more than wipe out the gains you make investing.

Investing is also generally only suitable for money that you don’t plan to spend for five years or more. So, make sure that you’ve got your emergency savings in cash, as well as any money you’ll need in five years – for a big holiday, a new car or your first home, for example. Any savings goal that’s further out than five years could be ideal for investing.

Investing for the first time can feel daunting. If you don’t feel confident picking which countries or sectors to invest in you can defer asset allocation decisions to a professional. You can buy so-called ‘all in one’ or multi-asset funds that spread your money between different regions and across various asset classes, with an option of having more or less in stock markets versus bonds, gold and cash, depending on your risk appetite. Alternatively, first-timers could buy a cheap ‘tracker’ fund, which mimics the performance of a broad global index, such as the MSCI World.

Investors also need to make sure they understand what they’re buying, and why they think it will make money – whether it’s a fund or a share. All too often investors are lured in by the promise of high returns or invest because a friend has recommended it, but you need to make sure you understand how the investment works and all the risks before you commit your money.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Real estate investment trusts (REITs) are notorious for offering high dividend yields and generating chunky passive incomes. Sadly, with higher interest rates throwing a spanner into their debt-heavy balance sheets, many of these enterprises have struggled in recent years… but not all of them.

Several REITs remain in strong financial form and are favourites among some expert analysts in 2026. So for investors seeking to unlock a reliable long-term passive income, which REITs should they be considering right now?

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

1. Government-backed healthcare income

A top pick from both Berenberg Bank and Jefferies is Primary Health Properties (LSE:PHP). After completing its takeover of Assura in 2025, the REIT’s become the UK’s largest healthcare landlord with a portfolio of 1,142 properties spanning local surgeries, medical centres, private practices, and even a few hospitals.

With healthcare in continuous demand, the company’s had little trouble finding tenants or securing long-term leases.

As such, the average duration of its rental contracts currently spans 11 years, with occupancy standing at 99.1%. And since close to 90% of the group’s rent is paid by the NHS, the company essentially earns government-guaranteed income.

Few REITs enjoy this level of revenue visibility. And as a result, management’s been able to consistently and intelligently allocate capital, ensuring steady growth, and 28 years of continuous dividend hikes – a pattern that experts believe will continue far into the future.

What could possibly go wrong? Having the NHS as a top tenant is a bit of a double-edged sword. While it ensures reliable and timely rent payments, it also means Primary Health Properties is at the mercy of government spending and political priorities.

If the NHS budget’s cut or efficiency initiatives reduce the required real estate footprint for healthcare, the group’s impressive occupancy could come under pressure. Similarly, it gives the NHS far more power when negotiating lease renewals that limit the group’s future cash flow growth.

These risks are something investors will need to consider carefully before adding this business to their income portfolio.

2. Warehousing & logistics income

With e-commerce volumes continuing to expand worldwide, demand for well-positioned logistics facilities continues to rise. And another top REIT from Berenberg to profit from this trend is Segro (LSE:SGRO).

As one of the largest commercial landlords in Europe, businesses such as Amazon, Deutsche Post DHL, and Tesco all rent from Segro to run their expansive operations. And with an impressive undeveloped landbank, this scale advantage is only becoming more prominent.

Occupancy stands at 94.3% with an average lease duration of 8.2 years as of June 2025. And just like Primary Health Properties, this long-term revenue visibility has enabled 11 years of continuous payout hikes.

However, unlike Primary Health Properties, Segro is more exposed to cyclical risks. Downturns in consumer spending directly impact demand for renewing old leases or signing new ones.

At the same time, if the wider market overdevelops new e-commerce capacity prior to a downturn, it could result in oversupply, putting downward pressure on rental rates. Nevertheless, Segro’s demonstrated a knack for navigating such environments in the past.

So once again, it might be a risk worth taking. But these aren’t the only REITs on my radar right now.

Dr James Fox explores whether it would could be possible to generate enough dividend income to live comfortably and stop working.

Posted by Dr. James Fox

Published 30 May, 2023

The content of this article was relevant at the time of publishing. Circumstances change continuously and caution should therefore be exercised when relying upon any content contained within this article.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing

Like many investors, I receive dividend income from the stocks I own. In my case, dividend-paying stocks represent the core part of my portfolio. But just how much would I need to earn from dividends to live off this income alone? And would it be possible?

Let’s take a close look.

How could it work?

Well, I’d want to build a portfolio of dividend stocks that collectively pay me enough money to live from. Let’s say this is £30,000, but I appreciate this might not be possible in London.

And I’d want to be doing this within an ISA wrapper. That’s because any capital gains, dividends, or interest earned within the ISA portfolio is tax-free.

So, if I was earning £30,000 from dividends, I’d actually be taking home more money than someone on a £45,000 salary — including student loan repayments.

Of course, unless I picked specific stocks, I wouldn’t expect this income to be spread evenly across the year. At this moment, the majority of my portfolio’s income comes around April and May, shortly after the end of the financial year. So that’s something to bear in mind.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

What would it take?

Well, to earn £30,000, I’d need to have at least £375,000 invested in stocks. That’s because I believe the best dividend I can achieve is around 8%. This would involve investing in companies, like Legal & General, that don’t offer much in the way of share price gains.

But what if we don’t have £375,000? And let’s face it, the majority of us don’t.

Well, I’d need to build a portfolio over time. And I could do that using a compound returns strategy. This involves reinvesting my dividends and earning interest on my interest. It’s very much like a snowball effect.

Naturally, there are several key variables here. The starting figure, the yield I can achieve, and the amount of money I contribute from my salary every month.

If I started with £10,000 and stocks yielding 8%, in theory I could reach £375,000 in 19 years. But this would require me to contribute £400 a month and increased this contribution by 5% annually throughout those 19 years.

And by contributing £400 a month, I’d fall way under the maximum annual ISA contribution of £20,000.

Compound returns isn’t a perfect science, and as with any investment, I could lose money. But it’s certainly safer than investing in growth stocks.

About the stocks

Of course, the above is great in theory, but I’d need to pick the right stocks. I’m looking for stocks with strong dividend yields, but I also need to be wary. Big dividend yields can be a warning sign, and the dividend coverage ratio is a good place to start.

View over Old Man Of Storr, Isle Of Skye, Scotland

Story by Zaven Boyrazian, CFA

Few investors come close to matching the exceptional track record of billionaire Warren Buffett. The ‘Oracle of Omaha’ has steered his investment firm to generate close to a 20% average annualised return since the 1960s. So it’s no surprise that when Buffett gives advice, investors listen… carefully.

And with the cost of living continuing to rise, his previous tips about the need to earn passive income are now more relevant than ever. After all, “If you don’t find a way to make money while you sleep, you will work until you die”, he famously said.

With that in mind, here’s how any investor can immediately start earning a passive income overnight.

The power of dividends

While many investment portfolios tend to be geared towards growth, it’s easy to overlook mature, boring dividend-paying stocks. After all, why would you invest in a dull self-storage enterprise when there are bleeding-edge biotechs curing cancer?

So how do investors tap into all this passive income potential? It’s simple. All they need to do is buy shares in a dividend-paying company, and wait for the money to come rolling in, usually once every quarter.

But is it really that simple?

Risk versus reward

The most lucrative dividend stocks over the long run aren’t necessarily the ones with the highest yields today. Instead, it’s the businesses that generate exorbitant volumes of consistent free cash flow that not only fund shareholder payouts but also enable them to grow over time.

That’s a lesson Buffett has learned firsthand with his investment in Coca-Cola (NYSE:KO). The soft drinks giant has used its consistent and steady cash flows to increase dividends every year for 63 years in a row. And consequently, Buffett’s now earning more than a 60% yield on his original investment in the late 1980s.

Sadly, past performance doesn’t guarantee future results. And if investors blindly buy previously successful income stocks without investigating the underlying risks or potential rewards, their passive income could quickly disappoint.

So let’s take a closer look at Coca-Cola.

Still worth considering?

Starting with the positives, Coca-Cola’s latest results show that the company continues to expand sales organically at impressive profit margins. And even after another round of price increases, thanks to the group’s brand driving pricing power, sales volumes have remained robust, indicating that customers are happy to pay a premium.

That all translates into yet more free cash flow, paving the way for its 64th consecutive dividend hike. However, there are some brewing headwinds to keep a close eye on. Rising global sugar taxes and rising economic constraints in key emerging markets undermine the group’s long-term momentum.

As such, even if dividends continue to rise, future payout hikes might be far less impressive. Put simply, there may be other better dividend growth opportunities to explore right now. Nevertheless, for investors seeking reliable passive income, this Buffett-style stock might be worth a closer look.

Three income powerhouses are trading at very compelling valuations right now.

Each offers attractive income with substantial upside potential.

Here’s why I’m overweighting them while the market is still giving them away at a discount.

Looking for a portfolio of ideas like this one? Members of High Yield Investor get exclusive access to our subscriber-only portfolios.

Sakorn Sukkasemsakorn/iStock via Getty Images

When looking to retire on passive income, I look to build a portfolio diversified by sector that is filled with high-yielding, high-quality businesses that have durable defensive business models, strong balance sheets, high and sustainable yields that are well-covered by underlying cash flows, and have the potential to either grow at a rate that meets or beats inflation or generate excess income that can be reinvested to generate growing income to offset the corrosive impacts of inflation.

While diversification is a sacred pillar of my investment strategy, at the same time, as a value investor, I do tend to overweight sectors that are opportunistically valued at the time. This is how I’ve been able to generate outsized total returns with below-market beta over time. With that in view, in this article, I’m going to detail what I think are three of the most undervalued, attractive, retirement-friendly income machines right now.

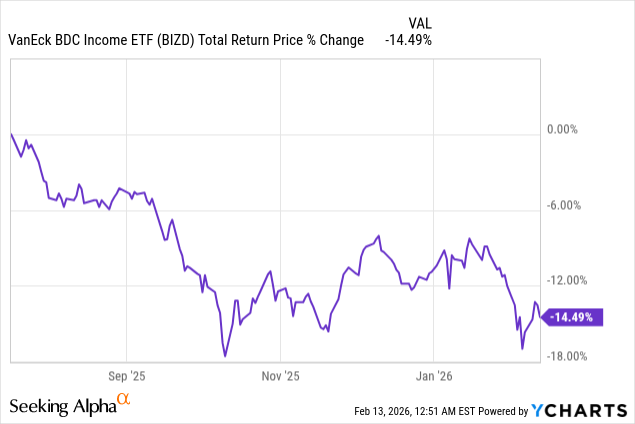

The Most Undervalued High-Yield Sector That Is Hated Right Now

The most undervalued high-yield sector right now is the business development company sector (BIZD), as it has sold off pretty aggressively since last July:

While there certainly are concerns about private credit in general due to the influx of capital into this space in recent years, the compressing spreads, the muted M&A activity, and, most recently, concerns about AI disruption of software, which does have a substantial place in many BDCs’ lending portfolios, I think that overall these concerns are largely overblown. This is especially true in the leading quality underwriters, as their portfolios continue to deliver strong underwriting performance and their internal risk metrics are not showing any material signs of growing weakness and potential credit defaults.

Within the BDC space, there are quite a few opportunities right now that offer attractive and sustainable yields that I would have no issues buying if I were an income-focused retiree as part of a well-diversified portfolio. If you want to go with the bluest of the blue chips, Main Street Capital Corporation (MAIN), Capital Southwest (CSWC), and Ares Capital (ARCC) are three great names to choose from, though I do not view them as being particularly cheap at the moment. If you want to move further into tech, you can go with the leading blue-chip Hercules Capital, Inc. (HTGC), which is a solid opportunity, albeit trading near fair value, in my view.

However, if you want to go after more undervalued names while still insisting on quality, I think names like Golub Capital BDC (GBDC), Blackstone Secured Lending Fund (BXSL), Blue Owl Capital Corporation (OBDC), and several others offer an attractive combination of yields and value right now. While it is entirely possible that some of these BDCs – such as BXSL and OBDC – will cut their dividends in the coming quarters, it is also important to keep in mind that their current yields are high enough that even a 10-20% cut in their dividend would still leave them yielding over 10%. This is similar to how GBDC recently cut its dividend by 15%, yet still yields over 10%. This reduced dividend rate would then be quite sustainable, barring a very aggressive pace of rate cuts from the Fed and/or a material economic downturn. Meanwhile, their substantial discounts to net asset value, strong underlying balance sheets, and defensive portfolio posture, along with strong underlying performance, set them up to be dependable and relatively defensive income machines.

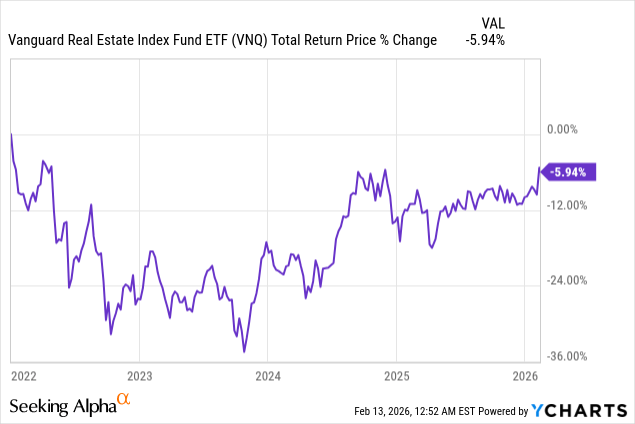

Why Residential REITs Could Be Near A Major Inflection Point

The second most undervalued high-yield income machine right now, in my view, can be found in the real estate investment trust space (VNQ), as it has been in the doldrums ever since interest rates began rising aggressively in 2022.

While triple-net lease is typically the bastion of sustainable income, with names like Realty Income Corporation (O) and NNN REIT, Inc. (NNN) headlining that space with fairly attractive yields, one of my favorite places to invest in the real estate sector right now is the residential space.

This is because there continues to be a general housing shortage in many markets in the United States, and rental rate dynamics in key Sunbelt markets are about to hit an inflection point where I think they will likely increase materially later this year and into 2027, as new supply is expected to be weak moving forward while demand continues to grow due to strong in-migration into these markets. Some of the most attractive ways to play it right now are Mid-America Apartment Communities, Inc. (MAA) for multifamily, along with Camden Property Trust (CPT) as another attractive option, and then in the single-family space, American Homes 4 Rent (AMH) and Invitation Homes Inc. (INVH) are both deeply undervalued as well.

All four of these REITs offer pretty solid dividend yields with strong dividend growth track records backed by rock-solid balance sheets, diversified portfolios of quality residential real estate in good markets, and yet all four of them trade at deep discounts to net asset value. Between their essential nature, attractive long-term growth prospects, status as a real asset inflation hedge, and deep value, I think these make for a very compelling place to allocate capital right now, especially in an environment where many other real asset investments, especially in the precious metals space (GLD) and commodity materials space (XLB), as well as increasingly the energy sector (XLE), have recently undergone strong rallies, making this one of the few real asset value plays remaining.

High Yields With Inflation-Resistant Growth

The third most undervalued high-yielding retirement income machine right now is midstream infrastructure (AMLP). Now, some midstream infrastructure is not discounted at all, such as Kinder Morgan, Inc. (KMI) and The Williams Companies, Inc. (WMB), which are quite richly priced after strong recent rallies. However, there are some attractive opportunities in this space yet that combine high yield with inflation-beating growth, very strong balance sheets, well-diversified and high-quality asset bases, and good management teams.

In particular, Enterprise Products Partners L.P. (EPD), Energy Transfer LP (ET), MPLX LP (MPLX), and several other K-1-issuing MLPs look very attractive right now, and in the 1099-issuing midstream side of things, there are also a few attractive opportunities, such as Plains GP Holdings, L.P. (PAGP). While they’re not as cheap as they were this past October, when I was pounding the table on them as my highest conviction pick at the moment, they still offer very attractive combinations of yield and inflation-resistant growth, as well as defensiveness thanks to their longer-duration, highly contracted cash flow profiles.

As a result, I think they still are a must-own as a substantial allocation in any income-focused retirement portfolio.

Risks & Investor Takeaway

While I’m very bullish on select undervalued high-quality BDCs, REITs, and midstream companies right now, none of them is risk-free. As already mentioned, BDCs are facing a plethora of headline and fundamental headwinds, whereas REITs remain highly interest rate sensitive, and residential REITs in particular need to work through some oversupply conditions in certain markets, which I think will happen soon. Finally, midstream infrastructure companies are mostly prone to commodity price volatility, impacting their equity valuations, even if their underlying cash flows are fairly resistant to it. Additionally, they have operational risk as they end up investing in growth projects that need to be executed on time and within budget to generate attractive returns.

Thanks to the attractive income yields and risk-reward profiles, these are three sectors where I currently have substantial allocations and very likely will continue to allocate capital to in the coming months, as long as they remain undervalued high-quality sources of attractive income and growth at High Yield Investor.