The current plan for the Snowball is to re-invest all earned dividends back into the portfolio with an income target of £14,500.

If you have longer to retirement, compound interest growth starts to accelerate the longer you stay invested.

If we use CTY as the working example, your capital should increase if you have an unexpected call on your cash. No guarantees though.

Also the earned dividends would be re-invested, either back into the share or another Trust, earning more dividends to re-invest in the portfolio.

The options for you cash, the totals are the unknown.

An annuity yielding 7% but you have to surrender all your cash.

Interest rates may be lower a lot lower, that’s the gamble.

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year. Oct 22

So not an option for me.

The 4% rule.

To use the 4% rule your 100k would need to have grown to £360 k.

Good luck with that.

Also if you want to pass on any of your wealth, your fund could be depleted depending on how long you live.

OR

You could have a foot in each camp, if you are not retiring soon.

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors. As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

Are you wondering when the best time is to retire, and how much you should take from your pension pot? We explain how the 4% rule could help you retire comfortably

Accessing your hard-earned pension pot when you are ready to retire is a major milestone in life.

After years of setting money aside, you will have the freedom to withdraw money as you please, and spend it on the lifestyle you desire.

But deciding when to start taking money from your pension savings, and how much to withdraw, can be tricky.

Get 6 free issues + water bottle gift

Try MoneyWeek magazine today for unparalleled financial insight, analysis and expert opinion.

As well as hopefully enjoying the returns from your pension savings, money still needs to be available for bills and possibly your own long-term care.

That is especially important as the cost of retirement is rising. Inflation rose to 2.5% in December, and could increase to 3.7% later this year, according to the Bank of England. Inflation will eat into the real value of your pension pot over the long term.

“It’s well known that most people are starting to plan for their retirement too late in life and do not have enough saved for a comfortable retirement,” Brian Byrnes, head of personal finance at Moneybox, tells MoneyWeek.

The latest research from the Pensions and Lifetime Savings Association, a trade body, suggests retirees need an income of £43,100 per year a “comfortable retirement”. For a couple, the joint figure needed is £59,000 a year.

However, a little-known rule called the 4% pension rule may be able to help you plan your retirement, and ensure your money lasts as long as you do. We explain what it is and how it works.

What is the 4% pension rule?

The rule states that retirees should take 4% of their fund in the first year of withdrawals, and the same monetary amount (adjusted for the rate of inflation) each year.

For example, if your pension pot is worth £500,000, you could withdraw £20,000 in the first year of your retirement. If inflation is 2% during that year, then in the second year you would withdraw £20,400.

This should ensure that your pension pot will support you through a 30-year retirement, in almost any economic environment. For that reason it is often referred to as the “safe withdrawal rate”.

Academics at the American Association of Individual Investors devised the 4% rule in 1998 after researching a sustainable withdrawal rate for a retirement pot that wouldn’t deplete the savings.

It looked at data from 1926 to 1995 and found that a rate of 3-4% is “extremely unlikely to exhaust any portfolio of stocks and bonds”.

“As a rule of thumb, the 4% rule is a good place to start when thinking about how much you need to save for retirement,” Olly Cheng, director of financial planning at Rathbones Group, tells MoneyWeek. “It is a nice benchmark rate to use, and therefore lets people set a simple target to see if they are on track with their savings.”

Can I rely solely on the 4% rule?

It is worth thinking about when to start accessing your pension pot, as market returns will have an influence on the success of the 4% rule.

A study from Morningstar in 2022 argued that 3.3% is the “safe” level of drawdown in order to protect a portfolio’s value over the long term.

However, this was based on the fairly downbeat market conditions at the time. Morningstar’s latest insight on the matter suggests that, with today’s more favourable market conditions, a 4% starting drawdown is once again safe.

Market conditions impact the 4% rule because it is based on the assumption that, over a 30-year period, a balanced portfolio (usually modelled as a 50/50 or 60/40 portfolio) will generate sufficient returns to cover the impact of 4% withdrawals annually.

This is true on average, over a 30-year period. Some years, though, a balanced portfolio will grow at less than 4%, and it may even fall in value.

According to Morningstar, in 2022 the average 50/50 portfolio lost 16% of its value. This is why Morningstar recommended a lower safe withdrawal rate for people retiring that year; withdrawing the full 4% would have further compounded their pension pot’s losses during the bad year, before it had a chance to gain value in any good years.

For that reason, it pays to check the economic outlook carefully, and research the safe withdrawal rate for your first year in retirement before jumping straight in with a 4% withdrawal rate. The good news is that it is only during particularly bad years that 4% isn’t a safe initial drawdown rate, which is why this rule of thumb has, on the whole, stood the rest of time.

When should you retire?

Timing your retirement is a key decision. Ideally, you’ll retire in a good year for your portfolio. In any given 30-year period there are bound to be some bad years, but you want your pension pot to have registered some gains during the good years before these come around.

While hard to predict in advance, it is worth checking the economic outlook when you first start thinking about retiring. If the outlook is bad, and you feel you can still manage a year or two more of work, then it could be worth delaying your retirement and giving your pension pot a better chance of getting off to a good start.

This has the added benefit of fattening it up through your working income beforehand, and reducing the amount of time it will need to last you. All these factors swing the maths in your favour, and increase your chances of enjoying a comfortable retirement.

Of course, it is impossible to know in advance whether next year will be a better or worse year to retire than this one. Plus, there are many reasons why you may not want, or be able, to postpone your retirement for an extra year.

For this reason, John Corbyn, pensions specialist at the wealth manager Quilter, suggests making more conservative withdrawals early in your retirement, especially if you do happen to retire during a period of economic downturn.

What else do I need to know about the 4% rule?

Like all rules of thumb, says Corbyn, the 4% concept is based on certain assumptions.

“It needs to be overlaid with someone’s state of health and propensity to spend, which is likely to be higher for younger clients and lower for older clients,” he says.

“Care needs to be taken to ensure the attitude to risk and propensity for loss is also built into these assumptions.

“Depending on your risk tolerance, investment strategy, and the actual returns you get, you might consider a slightly more conservative withdrawal rate.”

Corbyn says it is crucial to continuously review and adjust your strategy based on your actual investment returns, spending needs, and the broader economic landscape.

“Ultimately, pensions are a long-term savings vehicle and potentially may need to pay for someone’s income for up to 30-40 years, and care needs to be taken if the fund is accessed early, as short-term gain may lead to long-term pain so getting advice is key,” he adds.

According to Cheng, retirement expenditure isn’t usually a flat annual amount, with the early years sometimes showing a higher expenditure when people want to travel, before expenditure starts to reduce slightly. He comments: “In the final years of their lives, many people will then see a further spike in expenditure as care is required.”

It’s important to note that this strategy may not work for everyone and is just one of many factors to consider when planning to retire.

Make a retirement plan

What you plan to do with your retirement will also have a huge impact on when you should start accessing your pension pot, so it’s a good idea to know what you want to do and the costs of doing it.

“If you have dreams of travelling the world then you might need much more retirement income than if you are content with a quiet life at home,” says Corbyn.

“It’s essential to have a realistic projection of your monthly and yearly expenses, including contingencies for unexpected costs.”

Cheng echoes this, saying “there is often a real benefit to undertaking some more detailed cash flow planning and speaking to an adviser”.

According to Moneybox data, just 11% of people are confident they will have a comfortable retirement. It is therefore vital that retirees have access to the right drawdown advice, and understand when to retire, and how much to withdraw, says Byrnes.

Pensions tax

Whatever rule you use, experts say it is always important to consider the tax implications when withdrawing money from a pension.

This is because beyond the 25% tax-free lump sum, you will need to pay income tax on withdrawals if you are earning above the tax-free personal allowance.

It may not take much to go above the £12,570 personal allowance, given the full new state pension is currently more than £11,500 a year.

“Tax planning is a crucial aspect of accessing a pension, and those who are thinking for instance of buying an annuity accessing a pension flexibly by withdrawing taxable amounts should take note if they are earning or taking taxable income from elsewhere, including the state pension,” says Alice Haine, personal finance analyst at the investment platform Bestinvest.

“For someone drawing the full flat-rate state pension at the moment, additional income – whether from work or a private pension – of [just over £1,000] will take them over the personal allowance and into basic-rate tax.

“For those with larger pensions or higher incomes, there will be the potential risk of being taken into the higher or even additional-rate tax brackets, and some savers in drawdown should moderate their pension income to avoid this.”

I first wrote about VSL back in October 2023. It wasn’t an “idea of the year” or anything like that. It was something I already held, and the reporting had always been pretty dire so when they announced a wind down, I decided to try to write about it trying to make head or tail of it, if I could. Over 5 articles which were roughly looking at the semi-annual updates I continued to be hopeful it could turn around. The company reports showed a pathway to realisations.

The Oak Bloke’s Substack

Part of this optimism was the fact that some holdings notably WeFox was also held by Chrysalis. Good company and all that.

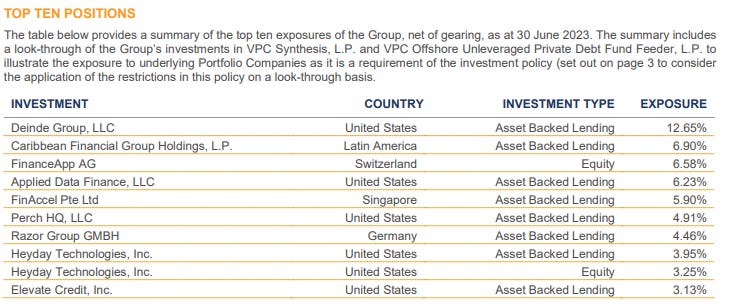

In October 2023 VSL was £200m Asset-backed loans delivering a 14% yield, £150m of near term maturities, -£75m of liabilities, over £100m of equity (plus options) and a £150m market cap. So the thesis was based on VSL info the fund would be debt free and 50% of the market cap returned before we reached 2026. That was the theory; the reality was very different.

These were asset-backed loans with great geographic diversity, a spread of counter parties, the prospect of 12% yield for several years. We’ve had no great recession, no great crisis, and the stock market has been at record levels. Rising interest rates and inflation took their toll on holdings. A lack of exit opportunities and a depressed Venture Capital and M&A environment really didn’t help either. As I write in February 2025 sentiment has improved a little but VC is hardly back to anything approaching real bullishness and positivity.

This was the near term expected cash realisations back in October 2023:

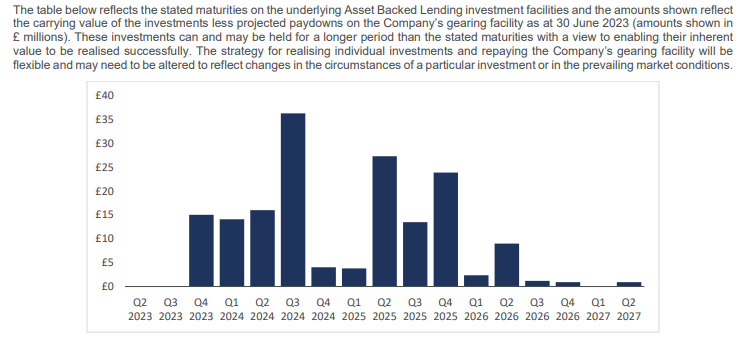

Maturities as at 30/06/23

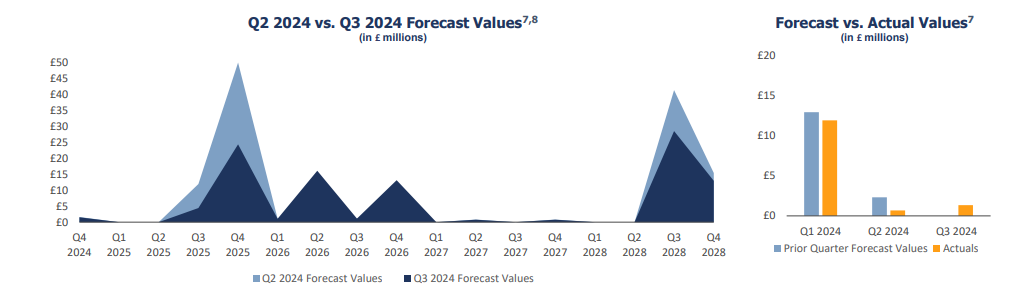

The reality however was, the timelines being reported by the fund proved hopelessly optimistic. Actual maturities have been pushed back and pushed back, quarter after quarter. Even recently this continues to happen. See 2Q24 and 3Q24 below. Have you ever known such a forgiving lender? Payment holiday no problem Mr Customer. We’ll just bump our investor cash forecast back another few years. VSL shrugs.

There have been substantial write offs of equity since October 2023 (-29.2%) but also write offs of asset-backed loans too. (-8.35%)

The fund trades on a 57% discount and once again is and “should be” very tempting. But this RNS at Christmas time was the clincher. Razor is £17m loan and £12m equity so £29m of the £167m NAV. ~20% of the NAV and ~40% of the share price.

VSL had a buy of 70.8p when I first wrote about it. I sold at just 27.2p. So a 43.6p loss. Factor in a capital return of 3.2p and dividends of 11.12p then the loss is a net 29.28p = a 41.3% loss.

Lessons to learn?

As some kind readers have pointed out you can’t win ‘em all and you win some and lose some. Inevitably the hope is to learn lessons.

Of course one lesson is to be sceptical over statements like “overcollateralised protection”. The reality was this protection proved to not be much protection whatsoever.

Should investors not take information at face value? The annual report is subject to audit and PWC were the auditors here and reported no material misstatements.

Should macro considerations have been considered more seriously? A share which lends money at high enough levels of return to sustain a 12%+ yield of course is susceptible to the danger of its customers, already burdened with expensive debt (from VSL) to implode when higher interest rates and rapid inflation tipped them over the edge. That’s entirely plausible and likely, and that is the lesson to learn here.

Anyways, this is the Oak Bloke calling time on VSL. Good luck to remaining holders.

“Diversification is an established tenet of conservative investment” – Benjamin Graham

One of the most prevalent mistakes made by investors is a lack of diversification within their portfolio.

Before diversifying, each investor should first assess and attempt to understand underlying risks across their asset allocation, their tolerance to those risks, their time horizon, and their goals.

We are investing in a VUCA world i.e. one which is Volatile, Uncertain, Complex and Ambiguous. There is so much out of our control and the fate of a particular company; its stock can change overnight. For example, Patisserie Valerie, Carillion, Theranos*(privately held), 4D Pharma, Credit Suisse, and the Woodford Equity Income Fund all had experienced unexpected changes to their predicted returns.

Failing to diversify investments across different asset classes, sectors, and geographical regions can result in heightened risk. By spreading investments across a variety of asset classes, investors can reduce the impact of any single investment’s poor performance and potentially enhance their long-term returns. Case in point, many ISA investors are mainly UK-centric investors and this has led to their investment portfolios lacking exposure to US listed stocks which in the main have significantly outperformed UK listed stocks, especially the US best-performing tech behemoths during the past ten years.

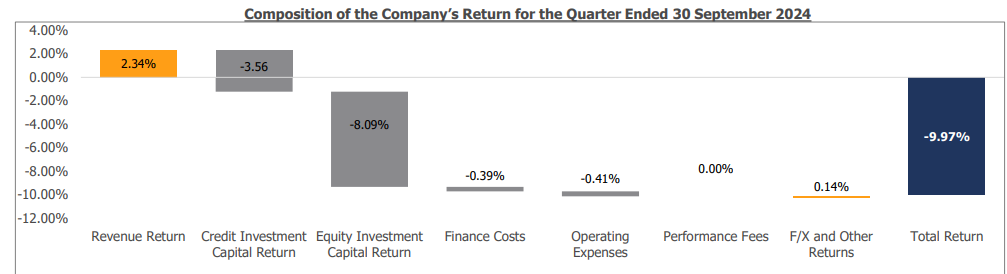

The Company also announces a quarterly interim dividend of 1.95 pence per share for the quarter ended 31 December 2024, in line with the dividend target of 7.80p per share for the year to 31 March 2025, as set out in the 2024 Annual Report – which represents a yield of 11.1% on the closing share price on 13 February 2025.

Eight Common Investing Mistakes Made by Private Investors

|Posted on 2nd February 2024 | By Peter Higgins

“Investing success is two-thirds avoiding mistakes, one-third doing something right.”- Ken Fisher

Private investing offers the opportunity for individuals to take control of their finances and even achieve financial freedom. However, without proper knowledge and preparation, private investors can unknowingly make mistakes that hinder their portfolio investment returns. Of course, because we are human, it is natural for us to make mistakes, and we will be more successful through our continuous learning. To make life a little easier though, this article will look at some of the common mistakes that private investors make and provide insight on how to reduce and even avoid them, ensuring a higher chance of long-term success for your investment journey.

1. Overconfidence

“Overconfidence is a powerful source of illusions, primarily determined by the quality and coherence of the story that you can construct, not by its validity”. – Daniel Kahneman

Most investors are overly optimistic about the prospects for the shares they own, & overconfident in how much they know about said company they are invested in.

The more research undertaken, the more overconfident we can become. Without a strategy to realise our overconfidence and how to mitigate that, every investor will eventually fail.

Psychologists believe overconfidence increases whenever there’s a higher level of expertise associated with a task. It is often said that people who consider themselves to be very smart actually perform worse as investors. Warren Buffet’s business partner, Charlie Munger, put it simply when asked what was the key to his success at Berkshire Hathaway; he said simply one word: “rational”.

My £5-a-day starter plan to build a regular second income by 2030 and beyond

Story by Mark Hartley

My £5-a-day starter plan to build a regular second income by 2030 and beyond.

What’s a second income worth ? How much effort’s considered a fair amount to dedicate to building towards one ? Many people take on two jobs to earn an extra income, waking early and working late into the night.

Set and forget

A core tenet of this strategy is ‘set-and-forget’. Once it’s set up, it can be left to do its thing without further action. All it requires is saving £5 a day and investing it into the portfolio. With certain accounts, this can be automated to occur monthly.

This is considered a good strategy for beginner investors because it avoids the risk of panic-selling. Investors lacking market experience are more likely to make mistakes by trying to actively manage a portfolio. Often, a portfolio has a better chance of growing if left to its own devices.

That is, assuming the right stocks are chosen. Volatile growth stocks in emerging industries are not the way to go here, as their futures are uncertain. A better option could be an investment trust or index fund with a long history of solid performance.

The ETF’s enjoyed annualised growth of 8.7% over the past 10 years. Since it’s highly diversified across almost all markets in the world, it’s resilient against a downturn in any individual region or industry. Even though past performance isn’t indicative of future results, I believe its growth trajectory’s fairly reliable.

An investment of £5 a day could grow to around £13,600 in five years. Even with a decent dividend yield, that would only return around £100 a month of income. That’s why it’s best to start as soon as possible and think long-term. Investing in the stock for 20 years could grow the pot to £100,000. Shifting that much capital into a portfolio of high-yield dividend stocks could pay out around £670 a month.

While that may not sound like much, it requires a small investment, little effort and minimal risk. A fiver a day seems like a small price to consider.

The post My £5-a-day starter plan to build a regular second income by 2030 and beyond appeared first on The Motley Fool UK.

We think earning passive income has never been easier

Do you like the idea of dividend income?

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

Are you excited by the thought of regular passive income payments, as well as the potential for significant growth on your initial investment ?

Investment trusts offer a world of opportunities to tap into but how can investors sort the wheat from the chaff ? In our Investing Analyst column, experts run the rule over what’s on offer.

In this column, Thomas McMahon, Head of Investment Companies Research, at Kepler Partners, looks at how to get really get trusts to deliver on dividends.

The activism of Saba Capital, which I discussed in my last column, has created a challenge for all boards of investment trusts and we are already seeing its effect.

It certainly seems possible that this was behind the series of measures announced by abrdn Asian Income Fund (AAIF) recently.

The trust will now hold a continuation vote every three years, and has also decided to massively boost the dividend it pays out, which should rise to c. 7 per cent on an annualised basis, when accounting for the current discount.

These measures had an instant impact on the share price, which saw a decent bounce in the following days. I’m pretty sure it will have been the dividend policy that has led to this reaction, judging by past such announcements.

What the board has decided is that they will pay out a fixed percentage of the net asset value (NAV), which is essentially the value of the underlying holdings.

This is to be 1.5625 per cent of NAV each quarter, which equates to 6.25 per cent annualised. As the trust’s shares are on a discount, the implied yield on the share price is higher, at c. 7 per cent at the time of writing.

This is almost 2.5 percentage points higher than the 10 year gilt yield, and from a portfolio which has the growth potential of Asian equities to offer too.

This sort of manufactured or enhanced yield has become increasingly popular in recent years. It is one of the features of the investment trust structure that can’t be replicated in the open-ended or ETF world.

Assuming they have first received the right shareholder permissions under company law, boards can essentially decide what dividend they want to pay out without any regard to what income they have earned.

In the jargon, this is described as ‘paying from capital’. I think this jargon misleads some people though. it gives the impression that there is a separate pool of capital and one of income, but really these are just accounting fictions.

Trusts can invest the dividends they receive, and then sell their holdings when they have to pay a dividend. There is no requirement to keep income in cash for distribution.

This is a mistake people often make when considering another feature of income-paying trusts: revenue reserves. This refers to past year’s income which can be held back by a trust for distribution in future years.

While we talk about it as being placed in reserve, all that really means is that an account is written up on a virtual ledger, while the money is invested back into the portfolio. When trusts pay from revenue reserves or from capital, they don’t have to keep cash on hand through the year but can simply sell some assets and pay the cash out.

These features of investment trusts thus offer incredible flexibility to boards and really underline the credentials of the investment trust structure as the preeminent one for income-seekers. Boards can draw up a dividend policy without worrying about the income received from the portfolio changing from year to year.

While paying from capital has some critics, the market’s judgement overall is clear.

Consider JPMorgan Global Growth & Income (JGGI), for example. At c. £3bn in market cap, JGGI is one of the largest trusts in the sector, and sits on the mid-cap FTSE 250, just below the threshold for FTSE 100 inclusion. While most of the AIC Global Equity Income sector is trading on a wide discount, JGGI has been on or around a premium for most of the past five years.

Performance has been really good, the trust being ahead of all other vehicles in the Global or Global Equity Income sectors over five years, as well as ahead of global equity indices. The dividend policy is to pay 4 per cent of NAV each year, from capital wherever necessary. This means the managers are completely free from the need to worry about picking income stocks and they can just invest where they think the best growth is.

Paying a dividend from capital therefore allows income investors to invest in high growth areas while still earning a substantial yield, and I think it is this combination of yield and the strong performance from investing in global growth equities, that has led to the premium rating.

Could biotech be an income and growth opportunity?

Another good example of growth combined with income is International Biotechnology Trust (IBT). As the name suggests, it invests in companies developing new medicines, from those in clinical trials to those that are already generating sales and profits. These companies don’t pay dividends themselves, but IBT has a similar policy to JGGI, paying 4 per cent of NAV out each year in a dividend.

Biotechnology looks pretty cheap by historical standards, and has been out of favour as the market has adjusted to high interest rates. This means that, unlike for JGGI, the discount on the shares is considerable at the time of writing, around 12 per cent. This does show that an enhanced yield on its own is not enough to assure a narrow discount.

I think biotech could be an area to benefit if the market starts to broaden out from large-cap tech, which has taken so much investor attention and cashflow in recent years, while large-cap pharma companies are desperate to replace their expiring patents, which should see takeovers of the earlier-stage companies like those in IBT’s portfolio.

The other trusts getting innovative with dividends

There are plenty of other trusts which pay a dividend from capital spread across all the major equity sectors. JPM has a whole suite of funds from Asia to Europe and the UK with an enhanced dividend, all of which have a growth-heavy investment approach.

In fact, in AAIF’s own sector, there are now three trusts with an enhanced yield: AAIF, JPMorgan Asia Growth & Income and Invesco Asia Trust (IAT). Interestingly, AAIF has seen its discount move in from being the widest in the sector to being in line with these other two trusts, which have discounts between 10 per cent and 11 per cent. Schroder Oriental income (SOI) is trading on a much narrower discount of 7.1 per cent, but has a lower yield and does not pay out of capital, with the income being purely ‘natural’. I think the crucial factor here is size: SOI has a market cap of around £650m while the others are all below £300m.

With IAT soon to complete a combination with Asia Dragon that will more than double its size, it may be that this is a catalyst for the discount to narrow, as a broader pool of professional investors can consider it.

One of the additional secrets behind JGGI’s success may be its size, which means it can be invested in by wealth managers and institutions which need to own large blocks of shares as well as retail investors.

Paying from capital hasn’t always been possible, but regulations have changed over the years. One of the pioneers of this approach was European Assets Trust (EAT), which adopted it in 2001. The trust pays 6 per cent of the closing NAV of the previous financial year in dividends, and the historical yield is 6.6 per cent at the time of writing.

The portfolio is invested in European smaller companies, not typically a great source of dividends, but a market with great growth potential. I think like IBT this is a slumbering growth market which should produce great returns at some point in the future when the market environment shifts.

Are these really dividends?

Not everyone approves of this sort of policy, although perhaps fewer people object each year as it becomes more established.

Sometimes people object that it is not really a dividend at all but just drawing down from capital. Imagine you had a cash account of £10,000 which paid you 5 per cent a year in interest, and you took out 6 per cent each year. Then you would be drawing down your capital. But in the case of equities, they go up over the medium term.

Now, nothing in finance is as certain as a law of physics, but there are all sorts of reasons to think this will continue to be the case. So we should expect to see any growth in an equity portfolio more than offset any contribution from capital to the dividend, assuming the board have struck the right balance and not committed to a truly excessive contributions from capital.

And crucially, it is always possible for the end investor to reinvest their dividends, in which case this isn’t a concern at all.

People sometimes choose to focus on the effect in a falling market. If the NAV is falling, and the trust makes a contribution from capital to the dividend, then the portfolio value will fall by more than the market. This is true, but over a medium to long-term investment horizon, we should expect the market to rise, and again, investors can simply choose to reinvest their dividends.

There is a short-term negative effect from this dynamic though: if the capital paid out is higher than the income earned, the fund will shrink and so costs will be higher for remaining shareholders. But funds without an enhanced dividend will also be shrinking when this happens thank so the falling market, and their costs rising too, so what we are really talking about is slightly magnifying this risk we take by investing in pretty much all funds.

What you need to watch out for

One issue you do have to watch out for with these strategies is the variability of the dividends. Paying from capital typically involves paying a fixed amount of NAV each year. Dividends therefore change as the NAV does, which means that if the NAV falls, next year, or next quarter, depending on the exact policy, the dividend might be lower.

Some investors might not like the irregularity this brings. Investment trusts can use revenue reserves to smooth dividends and provide very reliable payments. There are at least 51 trusts which have maintained or held their dividends for at least 10 years, largely due to the ability to build up reserves for when income falls.

During the pandemic, when dividends were cancelled by many companies, almost all equity income trusts were able to maintain their distributions to investors, unlike open-ended funds which have to pay out all income earned.

Buying a trust with an enhanced dividend might, therefore, mean accepting less regularity in the income stream received. Any effect of this could be moderated by owning other trusts with a natural income stream, high revenue reserves and an obvious commitment by the board to maintaining the dividend.

Investors don’t seem to mind this feature, judging by the generally positive impact on the discount an enhanced dividend has had.

Where things have come unstuck though, is when boards have changed the policy too often. This was a major problem for Invesco Perpetual UK Smaller Companies (IPU).

The trust paid 4 per cent of NAV, like many others discussed, with a big contribution from capital.

During the pandemic, presumably nervous about the drop in portfolio income – and maybe listening to the critical voices about the impact of this policy in a falling market – the board slashed its dividend target to 2 per cent of NAV, leading to the share price plunging.

Despite reverting to the 4 per cent target later on, the trust has never regained the very narrow discount it used to enjoy pre-pandemic.

I think the lesson is that investors are comfortable with enhanced, or manufactured yields, and they are comfortable with the variability from quarter to quarter, but they want a consistent policy over the medium to long term they can use to help build a portfolio.

Investors have been sucked back into bonds in recent weeks, looking to take advantage of a spike in yields early in January. Eventually, they will time this right, although the last few years have seen expectations for interest rate cuts, which would see bond prices rise, pushed back and watered down again and again and again.

With UK equity valuations being low, yields are also pretty high in that market too, with greater potential for price appreciation if rates stay higher for longer.

There are high dividend ETFs out there with decent yields, the iShares UK Dividend ETF having a trailing yield of 5.6 per cent at the time of writing. But I think when it comes to income, the advantages of investment trusts means that passive is a poor option.

High yields can be earned from all sorts of underlying growth markets, some of which are supported by bulletproof revenue reserves and some of which are raised well above the yields on bonds or ETFs thanks to the use of enhanced dividends.

All in all, it’s never been a better time to use investment trusts for income.