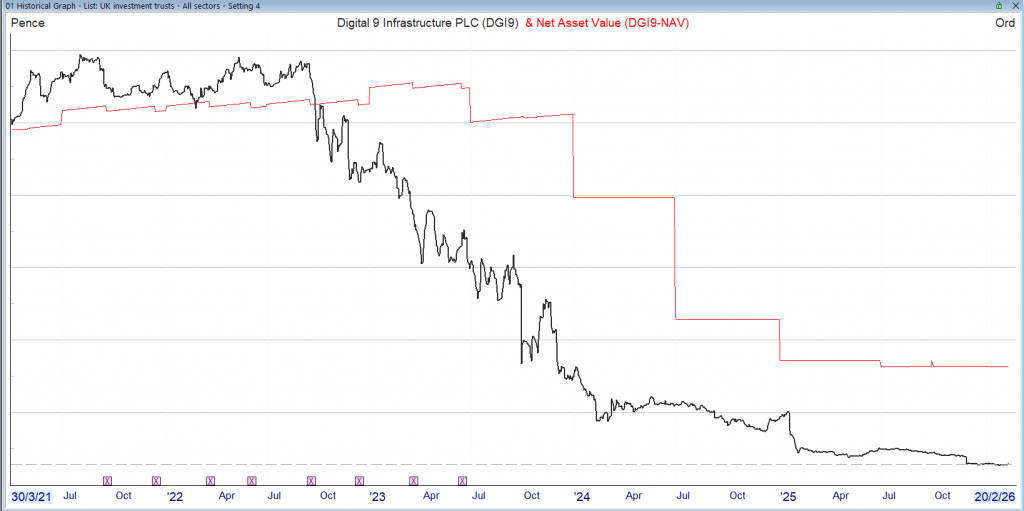

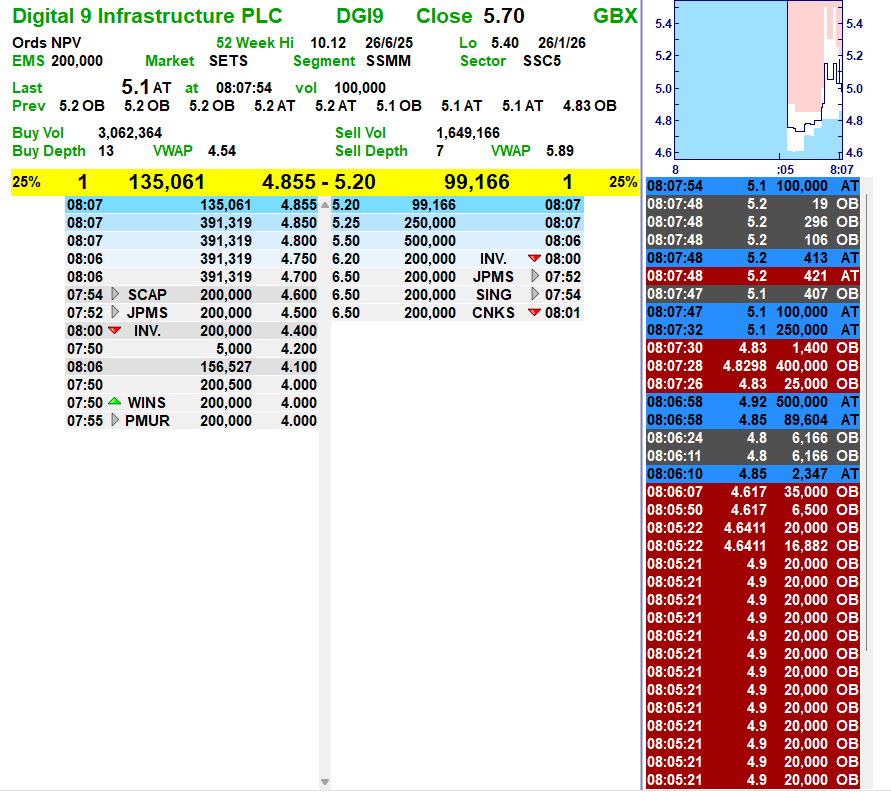

A working example of Rule 2

Digital 9 Infrastructure

Although it would have been uncomfortable to take a loss, the funds could have been re-invested in another high yielder.

Thus avoiding the chance of a complete wipe out.

Investment Trust Dividends

A working example of Rule 2

Digital 9 Infrastructure

Although it would have been uncomfortable to take a loss, the funds could have been re-invested in another high yielder.

Thus avoiding the chance of a complete wipe out.

The SNOWBALL has a comparator share VWRP where if 100k had been invested in the ETF at the same time as the start of the SNOWBALL, the value would be £155,414, not too shabby.

The value of the SNOWBALL’s dividends are the only thing that is tracked as the intention is never to sell any of the SNOWBALL’s shares and live on the natural income. Remember to leave some of your capital to the local cat and dogs home.

The comparison is what ‘pension’ you could receive, we have already ruled out an annuity, although if you a pension pot of 1 million, you could take out an annuity and concentrate on spending your income. But for lesser mortals the comparison is using the 4% rule, although some research states that 3% would be better and then hope you don’t run out of money.

The latest figures for a pension would be

The SNOWBALL 10k

VWRP, let’s be generous and use the 4% rule £6,200

The gap should continue to grow, especially when the next market crash occurs.

Even starting from scratch at 60, investing £1,500 a month with a SIPP could build a pension pot worth close to half a million pounds! Here’s how.

Posted by Zaven Boyrazian, CFA

Published 7 February

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

When it comes to building a retirement nest egg, few investing tools match the power of a Self-Invested Personal Pension (SIPP).

When starting early, depositing as little as £100 a month can be all it takes to secure a much more luxurious retirement in the long run. But what about those starting later… much later?

An estimated one-in-six of people in the UK aged 55 and above don’t have any retirement savings beyond the State Pension. That’s despite it being nowhere near enough to live a comfortable retirement.

The good news is, even for a 60-year-old aiming to retire at 68, investing a good chunk of change in a SIPP each month can have a significant positive impact on retirement lifestyle. Here’s how.

Unlike other tax-efficient investing vehicles like an ISA, any money put into a SIPP receives tax relief. In oversimplified terms, that effectively translates into deposits being topped up by the government, refunding any income tax previously paid.

Sadly, when starting this late in life, some near-term sacrifices are going to have to be made. And if an individual can put aside up to £1,500, that’s when things get more interesting.

Assuming a 60-year-old is paying the 20% basic tax rate, a £1,500 monthly deposit translates into £1,875 of investable capital each month. And if a portfolio matches the stock market’s long-term average return of 8% a year, doing this for eight years will grow a roughly £251,000 pension pot.

Following the 4% withdrawal rule, that’s enough to earn an extra £10,000 on top of the State Pension, providing a lot more financial flexibility.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Following the upcoming hike to the UK State Pension in April, this extra £10,000 would generate a total income of £22,547.60 a year. But by using a stock-picking strategy, investors could end up with a lot more.

Instead of trying to match the stock market’s 8% annual average with index funds, investors can aim to beat it by investing directly into the best businesses. And over the last eight years, that’s something Premier Foods‘ (LSE:PFD) shareholders have experienced first-hand.

Since February 2018, shares of the branded food producer have been on a bit of a rampage following a strategic pivot under new leadership. Including dividends, investors have earned a 394% total return. That’s the equivalent of a 22.1% annualised gain – enough to transform £1,875 a month into £485,190, or an extra £19,408 in annual retirement income (almost double!)

With around 90% of British households buying at least one of Premier Foods’ brands each year, the company has enormous market penetration in the UK. And right now, management’s seeking to replicate this success in new territories like Australia and North America.

Of course, international expansion carries significant execution risk. Its new target markets already have a wide range of established brands that the group needs to disrupt – a task that’s far easier said than done. And if it fails to deliver, the firm’s long-term growth prospects could be severely limited.

Nevertheless, with the leadership demonstrating its savvy capital allocation skills in recent years, Premier Foods may still be worth a closer look for investors seeking to build retirement wealth in a SIPP today.

Investors are going for a diverse range for their Stocks and Shares ISA choices as we get close to 5 April. Here are a few top picks.

Posted by Alan Oscroft

Published 10 February,

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

The ability to invest up to £20,000 in a Stocks and Shares ISA and not pay tax on any gains surely provides one of the best encouragements UK investors have. And there’s less than two months to go before time runs out to use up as much of our 2025-26 limit as we can.

In the early weeks of 2026, private investors are still piling their spare cash into UK shares. And more than any recent month I can remember, it looks like January was characterised by diversification. So what are the most popular stocks?

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

According to interactive investor, Aviva (LSE: AV.) was the individual stock most bought by ISA investors in January, with Fresnillo second. The immediate attraction of Fresnillo seems apparent — it’s the world’s largest primary producer of silver. And few will have failed to notice how that metal has soared along with gold — though it’s fallen back from its peak of over $100 per ounce.

Fresnillo shares looks like they’ve been a bit of a short-term thing to me. Those who bought in January hit the highest-price month for silver ever. And that might turn out to be unfortunate timing.

I’m more impressed to see the persistent popularity of Aviva. Aviva is dull and boring, and very much a long-term investment in my view. It’s come through its painful refocus in good shape. And I’d rate it as likely to be less volatile than any stocks related to precious metals at the moment.

Oh, and Aviva has a forecast dividend yield of 5.7%. I like Aviva — it’s one of my own holdings.

My main fear is that a forward price-to-earnings (P/E) ratio of 14 might be a bit high. That doesn’t seem to offer a lot of safety margin in what can be a cyclical sector. And it could keep the share price back. But for the long term, it’s one of my top Stocks and Shares ISA considerations.

Scottish Mortgage Investment Trust was the most popular investment trust in January. And it regularly makes the top few places throughout the year. It shows UK investors want a taste of the Magnificent 7 tech stock action, but with a bit of diversification thrown in.

I can’t stress the importance of diversification enough. And it’s why I think newcomers to ISA investing should seriously consider starting with investment trusts. City of London Investment Trust is a popular ISA pick, for example. It holds a wide range of top UK stocks — including HSBC Holdings, Shell, Unilever… and a whole lot more.

Looking outside the UK, the US tech stock volatility of late has pushed Nvidia down the popular ISA rankings. But Microsoft made a new entry in interactive investor’s January list.

It’s easy to run out of ideas with the ISA deadline approaching. But looking around at what others are buying can help kickstart our thoughts. And every stock mentioned here has to be worth considering, in the right circumstances. Just as long as we diversify — or did I mention that already?

And

By Brad Thomas, Wide Moat Research

As I’ve said before, and I’m sure I’ll say again, avoid “sucker yields” at all costs.

For the uninitiated, a sucker yield is a dividend yield that looks too good to be true because – more often than not – it is. Put another way, it’s a dividend that’s just begging to be cut.

But that doesn’t mean that every high-yielding stock is a sucker yield.

The best high-yield opportunities typically occur when a company has durable cash flows and a disciplined balance sheet… but it has temporarily fallen out of favor for some reason.

In the case of real estate investment trusts (“REITs”), virtually the entire sector has fallen out of favor. The S&P Real Estate Sector came in dead last in 2025 – printing only 3.2% against the S&P 500’s 17.9%.

But here’s the good news…

That relative underperformance is concealing some strong companies. And the temporarily depressed share price means they have generous yields that are also reliable.

If we are in the early innings of a REIT Renaissance, then there’s a good chance these yields won’t be this high for long. Today, I thought we might have a look at some high-yielding REITs that can still let you sleep well at night.

Healthpeak Properties (DOC) is a health care REIT that owns 673 properties, including:

The company recently announced it was spinning off that latter collection to form a new REIT called Janus Living. Healthpeak will retain a substantial majority ownership in this venture, making the remaining shares available in an IPO that will probably take place before July.

Healthpeak will also serve as Janus’ external manager. This involves a $10 million annual management fee under an initial three-year term, with successive one-year renewal periods after that… all while receiving a pro-rata share of regular distributions.

So it’s no wonder that Healthpeak sees no problem with continuing its annual $1.22-per-share dividend after the IPO.

Now, a primary reason for the spinoff is that, based on DOC’s current valuation, it isn’t being rewarded for its premium housing assets as-is. Shares currently trade at 10.2 times compared with 40.5 times for Welltower (WELL), a pure-play senior housing REIT.

That enormous difference doesn’t make sense considering how Healthpeak’s MOBs and life-science buildings generate steady and predictable income. The company just reported earnings last night.

In the fourth quarter of 2025, funds from operations (“FFO”) per share was $0.47, exceeding consensus estimates of $0.46. For fiscal year 2025, adjusted FFO (“AFFO”) per share was $1.69 compared with an annualized dividend amount of $1.22 per share (payout ratio of 72%).

For all of 2025, Healthpeak saw new lease executions of 562,000 square feet and renewal lease executions totaling 889,000 square feet with 72% retention and up 5% cash releasing spreads on renewal.

But, as I wrote two months ago concerning pureplay life-science landlord Alexandria (ARE)… the life-science space has been hit hard with oversupply, even causing that impressive company to cut its dividend last year. So Healthpeak is suffering from association.

What critics don’t realize is that it’s actually held up decently despite the drama. Not perfectly, mind you, but decently.

For the record, Healthpeak’s fourth-quarter earnings did beat expectations. But lab occupancy declined 390 basis points (“bps”) sequentially on a backend-loaded basis to 77.1%.

The REIT issued guidance for the year as well, missing The Street’s adjusted FFO projection by 5.5%. And same-store life science NOI guidance specifically is now down 7.5% year over year.

On the plus side, DOC expects lab occupancy to pick up in the second half of 2026 with around 1.5 million square feet of leasing in its pipeline.

As the FAST Graphs chart below shows, DOC trades at 10.2 times price to AFFO (P/AFFO) compared to its normal 16 times multiple. At least it was trading that way last night. I’m sure the earnings news will have a further negative impact on its shares.

However, this all represents an attractive margin of safety – and with a well-covered 7.1% dividend yield to boot.

Just keep in mind that the actual company isn’t expected to grow much either this year – or next. As such, my best-case forecast is that DOC will return 20% in 2026 between its dividend and price appreciation.

Source: FAST Graphs

I plan to interview Healthpeak’s management team later this week, information I’ll exclusively share with my Wide Moat Letter members.

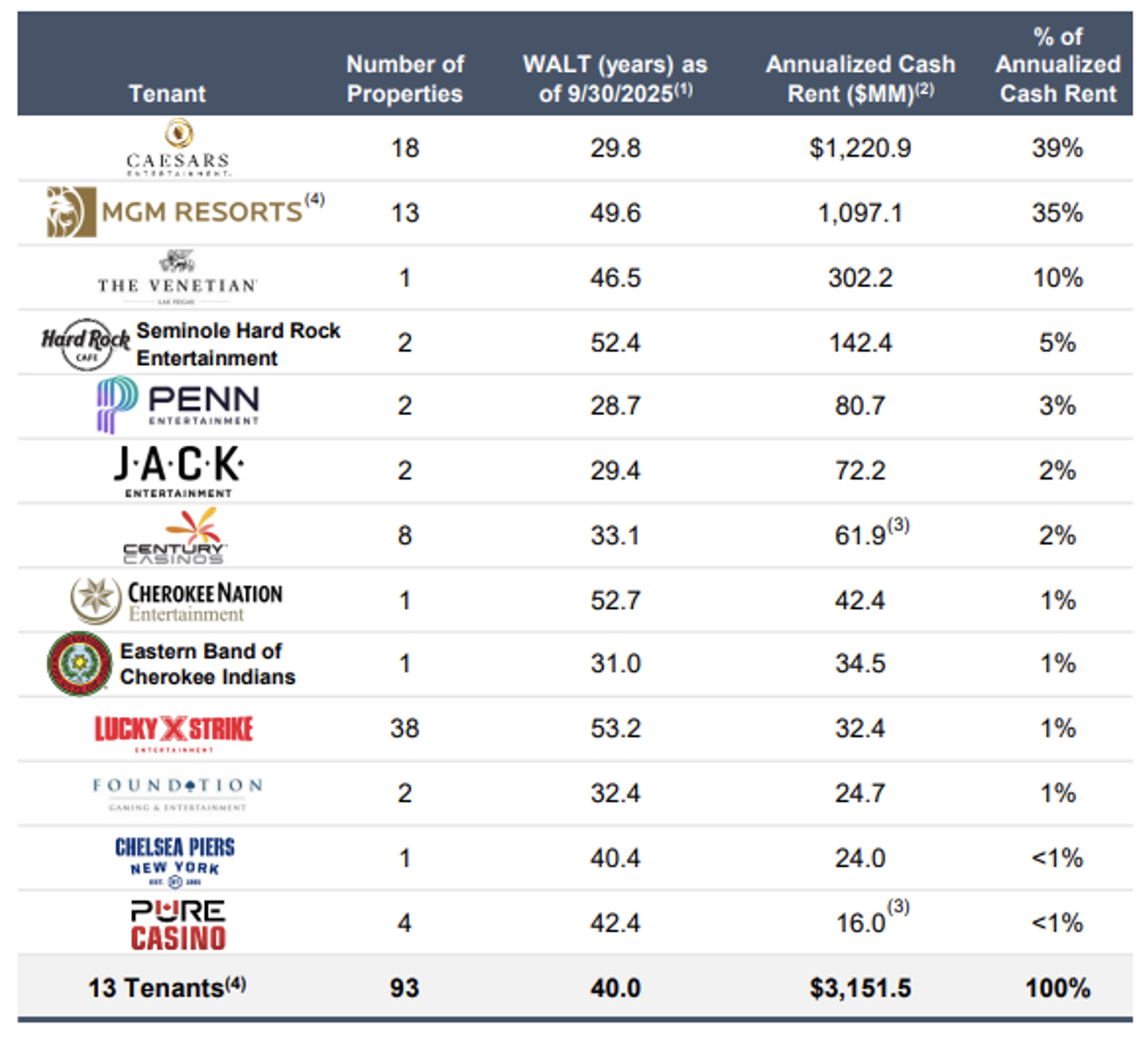

VICI Properties (VICI) is a net-lease REIT with a target niche investing in experiential properties. Since Caesars Entertainment (CZR) spun VICI off during its bankruptcy reorganization, it’s become quite the growth story.

A world-leading gaming and experiential REIT, it boasts:

As shown below, VICI has a diversified asset base, though with outsized exposure to three large gaming tenants. Caesars generates 39% of its revenue, MGM Resorts (MGM) accounts for 35%, and The Venetian another 10%.

Source: VICI Properties

So it does face concentration risk. However, it also boasts multiple holdings in one of America’s most valuable, supply-constrained locations: The Las Vegas Strip.

This space is built out. You cannot create new comparable assets there without knocking something else down.

VICI owns 10 trophy assets on the Strip, including 660 acres of underlying land, 41,400 hotel rooms, and 5.9 million square feet of conference, convention, and trade show space.

It also owns 26 acres of undeveloped land strategically located adjacent to The LINQ and behind Planet Hollywood, as well as seven acres of Strip frontage property at Caesars Palace. All of these are subject to and part of a master lease with Caesars.

Here’s another thing going for VICI: Whether in or outside of Vegas, gaming licenses create regulatory barriers that keep competitors at bay. Casino operators must obtain state gaming licenses and comply with strict approval requirements… conduct background checks… and undergo regulatory oversight.

Put simply, you can’t just open up a new Caesars Palace across the street.

Also, VICI’s leases are typically signed for 30 to 50 years. They’re triple-net, too, which means the tenant pays taxes, insurance, and maintenance. That gives the REIT bond-like income, inflation protection, and minimal landlord responsibility.

In fact, VICI’s general and administrative expenses (G&A) as a percentage of revenue were just 1.6% in the third quarter of 2025. That’s the lowest you’ll find among its net-lease REIT peers.

Yet VICI shares are underperforming, trading at 11.8 times compared with their normal 15.4 times. This gives it a 6.4% dividend yield with a 75% payout ratio (using AFFO per share).

The primary reason for this devaluation is because of consumer sentiment in Las Vegas. Specifically, Ceasars has experienced a 28% decline in earnings before interest, taxes, depreciation, amortization, and restructuring or rent costs (“EBITDAR”) since 2021. Compared with 13% rent increases, coverage ratios have declined to 1 times.

That has left many investors nervous about where its landlord stands.

I visited VICI’s headquarters in New York City a few weeks ago to meet with the management team about all of this. As they pointed out, the leases in question are master-leased and corporately guaranteed by Caesars Entertainment.

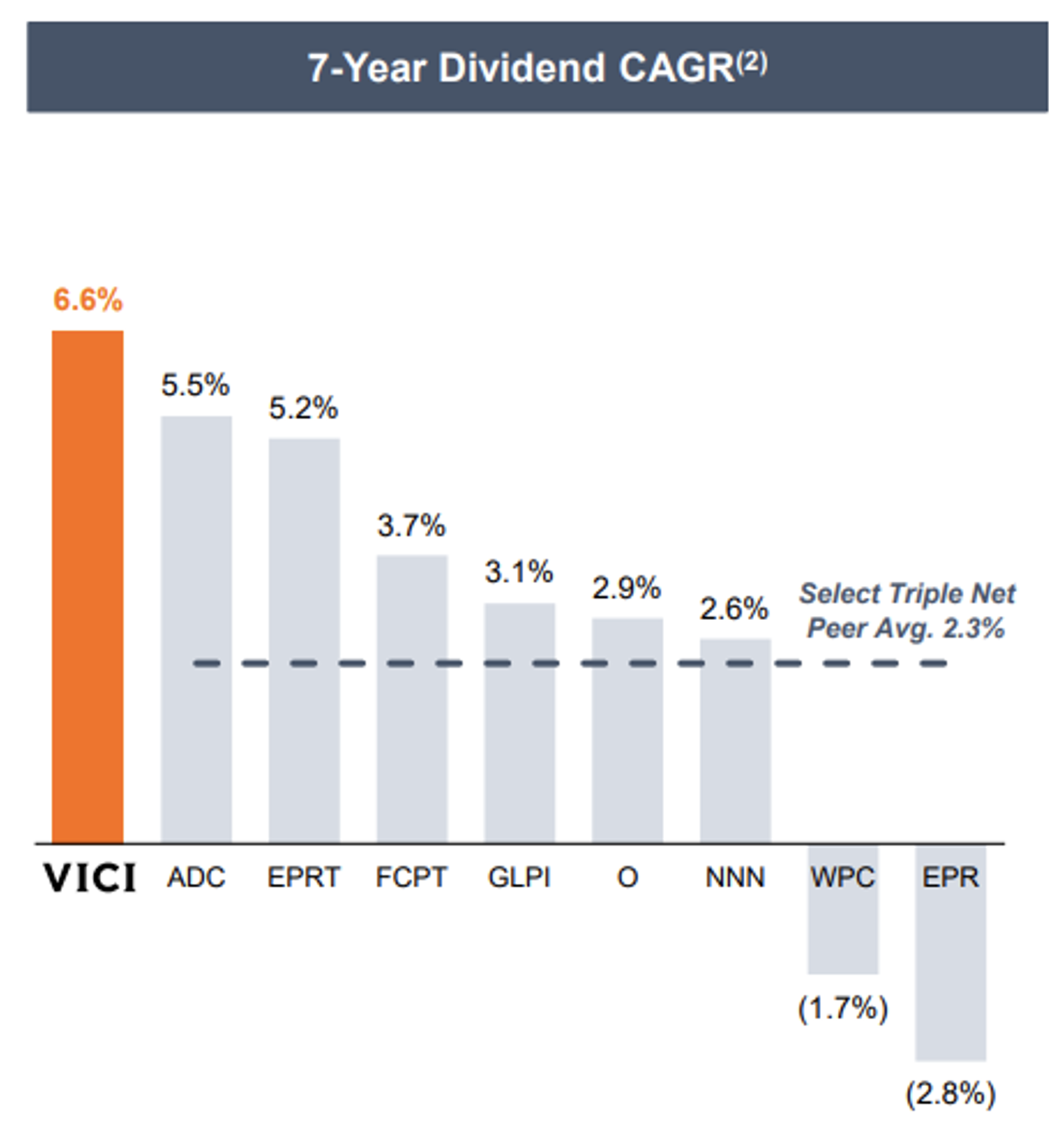

Plus, VICI has taken prudent steps to maintain a disciplined balance sheet (rated BBB- by S&P and Fitch, and Baa3 by Moody’s). It’s also proud of the fact that it has consistently grown its dividend at a 6.6% compound annual growth rate (“CAGR”) since inception – the highest in the net-lease REIT sector.

That’s a track record it takes very seriously and works very hard to build upon.

Source: VICI Investor Presentation

As a result, I believe VICI’s underperformance is a buying opportunity. Analysts forecast growth of 3% in 2026 and 2027. Between that, its 6.6% yield, and 15% discount, we estimate shares could return 25% over the next

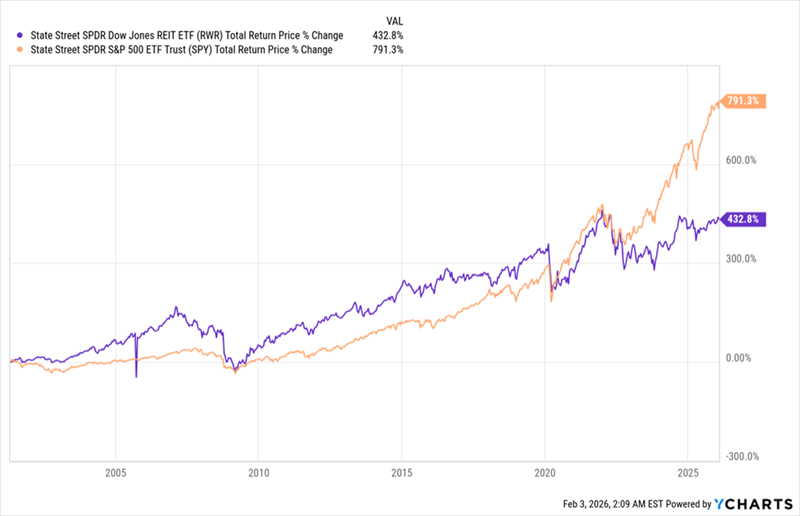

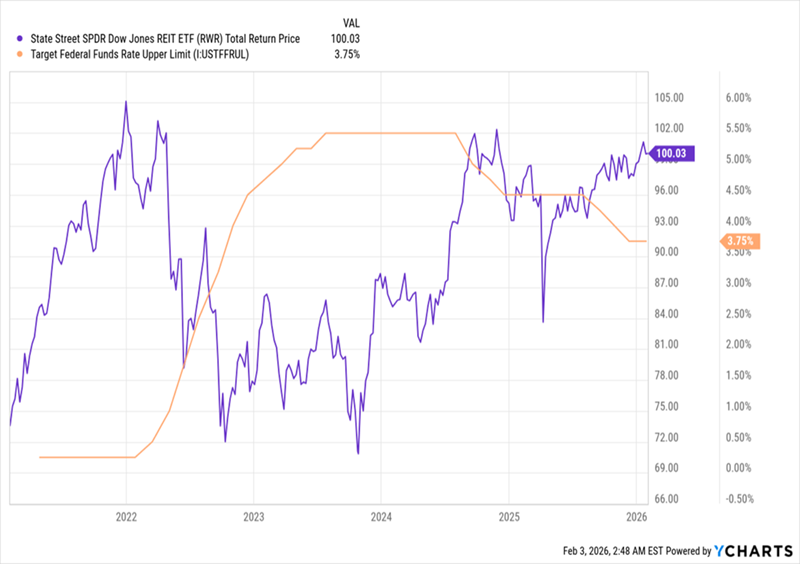

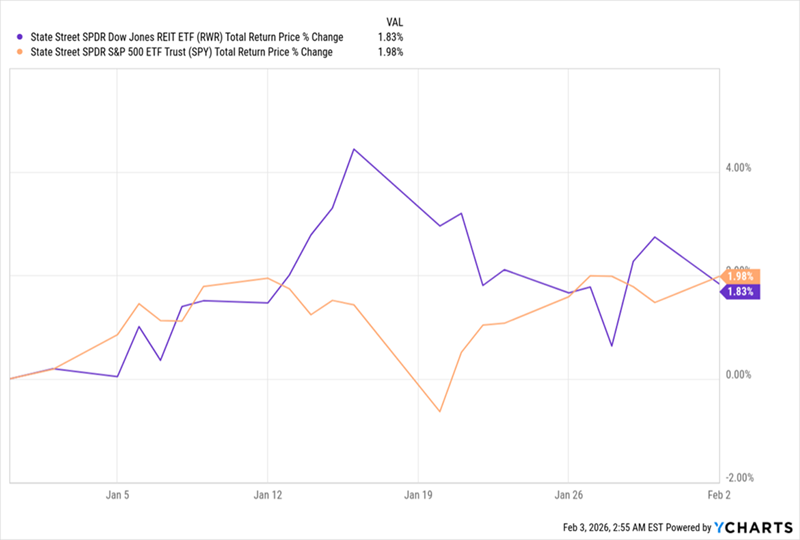

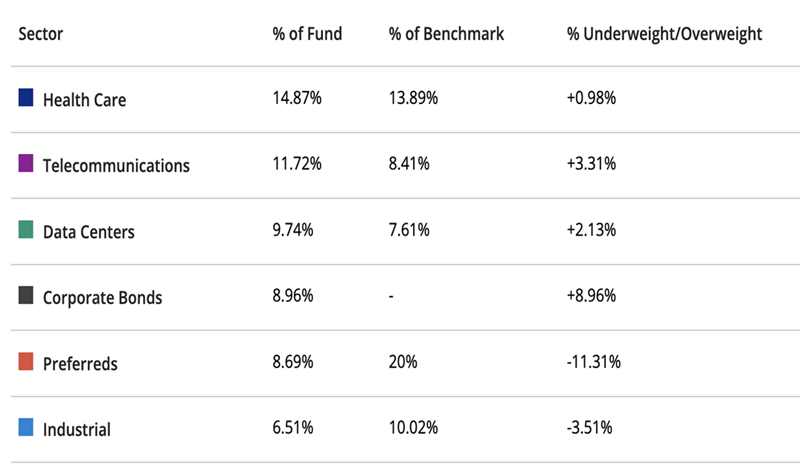

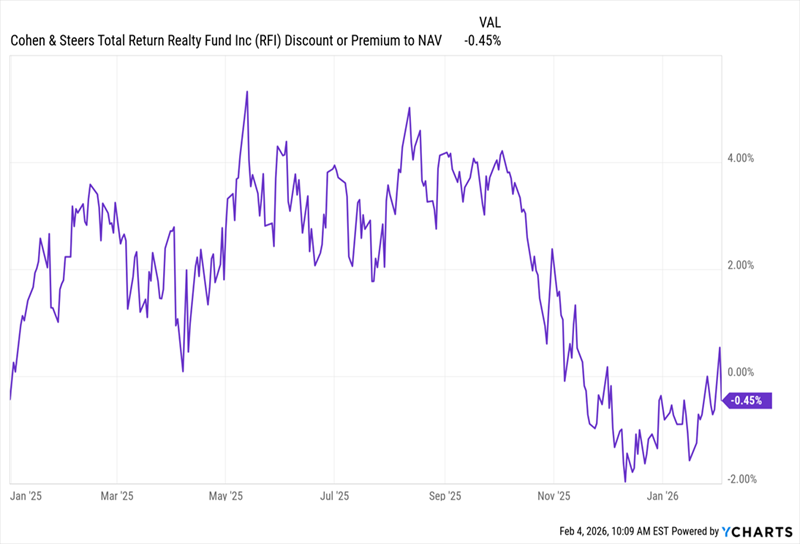

Our 8.6% Dividend Play on a “REIT Revival” by Michael Foster, Investment Strategist At times like these, we look to 8%+ paying closed-end funds (CEFs) to reap the strongest dividends and potential upside. I say this as REITs, long-time market outperformers, have been stuck in an unusually long slump. Remember when stocks ricocheted hard after the early days of the pandemic? REITs (with their benchmark ETF shown in purple below, compared to the main S&P 500 ETF, in orange) rebounded, too. But not nearly as much. REITs’ Slow Recovery  Why REIT Headwinds Are Diminishingand Setting Up to Reverse There are lots of reasons why REITs have lagged in the last six years, and none of them are really secrets: Work-from-home hit office demand. Interest rates jumped, hitting REITs’ bottom lines, as these companies borrow heavily to invest in their properties. Lower immigration into the US also had an effect on both housing and workspace demand. That last point – immigration into America – still applies. But both of those other barriers, which are far more meaningful, have either flipped or are in the process of doing so. Work-from-home? It’s largely been replaced by either a full-time return to the office or hybrid work. Interest rates? This is where things get intriguing. Rates Fall, REITs Start to Respond  REITs, as mentioned, borrow to invest in real estate, so rate cuts go straight to their bottom lines. The cuts the Federal Reserve has delivered since mid-2024 (in orange above) have come more slowly than markets expected. So it follows that the boost to REIT profits, and therefore their share prices, is real (purple line), but smaller than investors hoped. That leaves REITs in a strong position – still underpriced, but starting to show momentum. And with the first month of 2026 now behind us, we can see the current state of play here: REITs Nearly Reeled In Stocks in January  As you can see, in January, REITs (again with their benchmark in purple above) almost met the stock market’s returns. Now, one month does not make a trend, but that’s a switch from what we saw in 2025, when the S&P 500 gained over 17% and RWR returned a mere 3.2%. The takeaway: The lead stocks have held over REITs is finally starting to fade. And if interest rates fall faster than the market expects – quite possible if President Trump’s nominee for Fed chair, Kevin Warsh, is confirmed – REITs could not just match the S&P 500 but beat it this year. That would finally end REITs’ six-year lag. Let’s buy in before that happens. How? My favorite avenue is through those aforementioned CEFs. Consider, for example, the Cohen & Steers Total Return Realty Fund (RFI), a holding in my CEF Insider service that yields 8.6% as I write this. The fund is a solid play here, thanks to that 8.6% dividend, which has been rock-steady for years. The fund pays that dividend monthly, to boot. Source: Income Calendar RFI is also nicely diversified, boasting a portfolio that gives us exposure to AI’s infrastructure needs, with significant weightings in data center and communications (think cell-tower) REITs.  Source: Cohen & Steers Source: Cohen & SteersIt also holds industrial REITs, giving us broad exposure to both the reshoring and automation of factories. That top allocation to healthcare is also a plus, letting us tap into the aging of the US populations – a trend that still has decades to run. Finally, its allocations to bonds and preferred shares add stability. The fund is cheap, too. As I write this, we can buy RFI at a 0.5% discount to net asset value (NAV, or the value of the fund’s portfolio). I know that doesn’t sound like much of a deal, but it’s far below the premiums at which RFI traded for most of last year:  The kicker? That “small” discount is also well below RFI’s average premium of 3.7% over the last five years. That makes now a good time to buy this overlooked bargain, before other investors pick up on the many tailwinds shifting in RFI’s favor. 5 More “Built-for-2026” Income Plays You’re Not Too Late On (Yields Up to 10.7%) CEFs are, hands-down, the top plays on disconnects like the one we’re seeing shape up with REITs today, for three reasons:CEFs pay us (mostly) in cash, thanks to their rich dividends (around 8% on average).CEFs give us a double discount – on both washed-out stocks (or in this case REITs) themselves and on the fund itself through its discount to NAV.CEFs put our investments in the hands of a professional who knows their asset class inside and out. |

Thursday 12 February

Alternative Income REIT PLC ex-dividend date

BlackRock American Income Trust PLC ex-dividend date

BlackRock Income & Growth Investment Trust PLC ex-dividend date

Fair Oaks Income Ltd ex-dividend date

Franklin Global Trust PLC ex-dividend date

GCP Asset Backed Income Fund Ltd ex-dividend date

GCP Infrastructure Investments Ltd ex-dividend date

Greencoat UK Wind PLC ex-dividend date

ICG Enterprise Trust PLC ex-dividend date

Impax Environmental Markets PLC ex-dividend date

International Public Partnerships Ltd ex-dividend date

JPMorgan Emerging EMEA Securities PLC ex-dividend date

Majedie Investments PLC ex-dividend date

Murray Income Trust PLC ex-dividend date

NextEnergy Solar Fund Ltd ex-dividend date

Octopus Renewables Infrastructure Trust PLC ex-dividend date

Pershing Square Holdings Ltd ex-dividend date

Target Healthcare REIT PLC ex-dividend date

Dividend payouts are stable, unlike share prices – and could power future returns.

David Stevenson

04 February 2026

People on the cusp of retirement finally have something to cheer about after dividends paid by global companies rose to record levels.

Those regular cheques provide a valuable source of natural income for older investors looking for an alternative to high annuity rates.

According to Capital Group, global dividends hit a third-quarter record of $519bn (£379bn) last year, with a bumper 6.2pc increase in that quarter alone.

Crucially, those dividend payouts are stable – unlike share prices, which are volatile – and nearly nine in 10 companies increased payouts or held them steady, according to Capital.

Dividends can seem a little “old school” when compared to share buybacks, which have been all the rage in recent years – especially in the US, even amongst the tech giants.

But bear in mind one crucial issue: buybacks are volatile and tend to stop rather arbitrarily.

In Europe, for instance, analysts warn that the Continent’s leading energy companies are likely to scale back their buyback programmes. By contrast, most large corporations have been reluctant to chop dividends or even slow down dividend growth.

But dividends have a much more profound significance.

Academic economists have crunched the data on dividends from major stock markets over more than a hundred years and they’ve come to a powerful conclusion. In some decades dividends, the growth in that dividend payout and their subsequent reinvestment in the underlying stocks accounted for the majority of total returns.

That’s not true for recent decades, where valuations and capital gains have powered total returns – but it could be true for the next decade if markets wobble.

Dividends also matter a great deal to many older investors seeking what’s been called a natural income in their later years.

A growing majority of older investors have most of their wealth tied up in defined contribution pensions and Isas, and their primary goal is to preserve that capital for the remainder of their lives and generate a steady income.

Annuities provide an answer and rates are currently very high but there’s a clear drawback – you don’t have any capital left when you die.

That might be fine if you want a steady income but for many other investors, that loss of capital is a major drawback.

At that point, many investors encounter the 4pc rule – a rule of thumb that says you can withdraw 4pc of your retirement portfolio in the first year, adjust that amount for inflation each year after and not run out of money for at least 30 years.

The concept was born in 1994 when William Bengen, the financial planner, published a landmark study analysing historical market data dating back to 1926.

He found that even if you retired at the absolute worst possible moment – just before the Great Depression or the stagflation of the 1970s – a 50/50 mix of stocks and bonds would have survived a 30-year retirement with a 4pc initial withdrawal rate.

For decades it was the gold standard for US-based retirees seeking income while preserving their accumulated capital.

The bad news, though, is that depending on who you talk to, that number in the UK is probably somewhere lower – and quite possibly much, much lower.

A study covering 19 developed countries found that the 4pc rule would have failed in about half of them, including major economies such as Japan, France and the UK.

Doug Brodie, a financial planner from Chancery Lane, thinks the safe max in the UK is probably closer to 3pc than 4pc.

Helpfully, that 3pc to 4pc range aligns with the typical income from dividend-oriented equity funds that invest in UK or global equities.

Crucially, Brodie prefers equity income investment trusts where the board can accumulate past income from the portfolio into reserves and then pay it out in the future, keeping the dividend progressively increasing year after year.

This has spawned a whole sub-sector of investment trusts that are called “dividend heroes”, defined as funds that have increased their dividend payouts every year for at least the last two decades without fail, even during the pandemic.

The average yield on equity income investment trusts varies between 3.5 and 4pc per annum and you still get to keep the upside from owning risky equities.

Also, there’s strong evidence to suggest that corporates tend to increase their dividends at a rate that is above inflation, thus potentially inflation-proofing your income.

Here’s one last crucial upside when thinking about how volatile equities can be.

Although dividend-focused equities tend to underperform their peers, especially tech-oriented growth stocks, during booming bull markets, their downside losses during a sell-off are usually – though not always – more subdued.

The real trick for fund managers is to combine this income focus on dividends with a keen eye for what’s called “quality” which in investment terms means looking for companies that have strong balance sheets and are steadily compounding earnings growth.

This way, you avoid stocks that boast high yields simply because they are value traps: businesses that are in trouble and deserve their low share price and high dividend yield.

Analysis by Brodie suggests that, over many decades, this focus on quality stocks in dividend-hero equity income investment trusts not only grows your yearly income payout but also increases your final capital sum – unlike annuities, where you’ll have nothing left to hand over at the end.

| Charlotte GiffordSenior Money Reporter |

If you’re currently sitting on the sidelines waiting to invest, you’re not alone.

Last year, British investors pulled £6.7bn from equity funds as they cashed in on record high markets.

But what to do now? Many of us are staying in cash for the time being, with plans to hunt for bargains once stocks fall. The issue is, this fall isn’t happening.

The FTSE 100 hit record highs again last week having reached its previous all-time high in January. By waiting for the opportune moment to invest, many savers have already missed out on significant gains. Meanwhile, despite AI worries, the bubble has yet to burst and some experts maintain that comparisons between the AI-driven rally and the dotcom bubble in the 1990s is overblown.

For investors, this presents a conundrum. Do you wait to buy the dip – however long that takes – losing out on any potential gains in the meantime? Or do you invest now and risk heavy losses in a market crash?

British savers are often chastised for holding too much in cash. As a nation, we ploughed almost £70bn into cash Isas in 2023-24, according to the latest figures – more than double the £31bn we committed to stocks and shares Isas.

Yet research shows that stocks and shares outperform cash over the long-term. A one-off investment of £1,000 in 1999 would be worth over £6,000 today, according to stockbroker AJ Bell, whereas the same payment into a cash Isa would be worth just £2,000.

No one likes the idea of buying when prices are high and missing out on a good deal, but there is no way of identifying market dips in advance, or guessing correctly how much damage they could inflict.

Since 1870, the US stock market has seen 19 bear markets – defined as a period with a drop of 20pc or more over at least two months. While some crashes dragged on for years, others were strangely brief. The US stock market took only four months to recover from the Covid-19 crash, for example.

The investment management firm AQR recently tested 196 buy-the-dip strategies going back to 1965 and found that, in more than 60pc of scenarios, the investor would have been better off holding the S&P 500 passively. Returns were especially poor if the investor bought the dip at the start of a lengthy market downturn.

Of course, it’s possible to combine both strategies. You could hold the long-term while also retaining some cash to tactically buy stocks at the opportune moment – but you have to be quick about it. Last week, for example, there were buying opportunities after weak jobs data and new coding tools triggered a significant sell-off in the technology sector.

Generally, the best time to invest is when you have the money to do so. Advisers recommend holding between three and six months of expenses in an easy-access savings account in case of an income shock. Any more than this, and you might want to think about investing again, without worrying too much about your market timing.

Remember the market is likened to an elastic band, the further it is stretched the faster it will snap back.

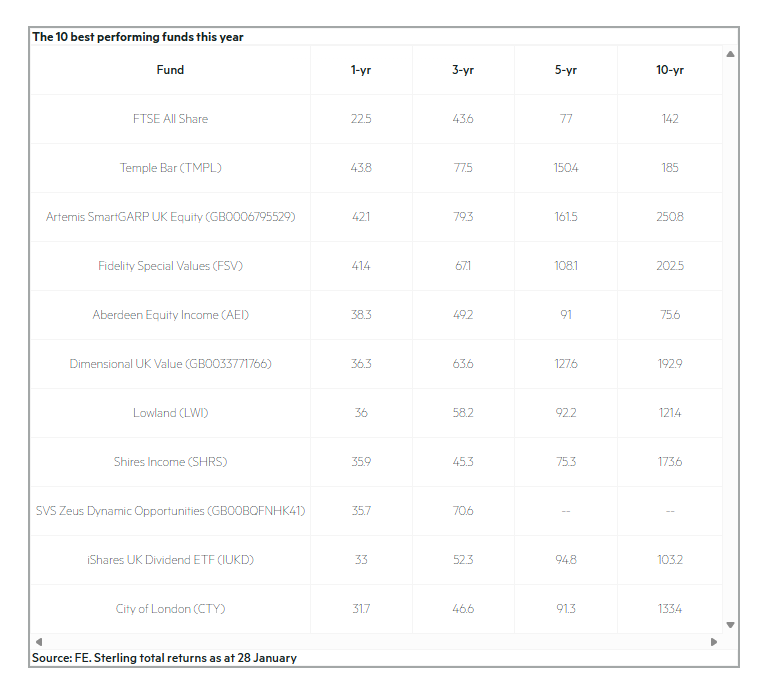

The past 12 months were all about value stocks. We look at the managers getting ahead of the market

Ten funds beating the FTSE this year

Published on February 6, 2026

by Val Cipriani

After a long malaise, it’s been a buoyant period for UK stocks, with the FTSE All-Share index returning 22.5 per cent in the 12 months to 28 January. One might have assumed such a strong result would be hard to beat for fund managers, but in fact a decent number of active funds comfortably outpaced the index.

The table below lists the 10 best performing funds over the period, spanning the UK All Companies and UK Equity Income sectors across both funds and investment trusts (using Investment Association sectors for the first and Association of Investment Companies sectors for the second; there are 302 funds in total across the four sectors). This is a short timeframe, but it is interesting to see which strategies have worked well in the current market.

The 10 best performing funds this year

Six out of the 10 funds in the list are investment trusts. While stock picking will have been a crucial driver of outperformance, gearing is likely to have helped too – trusts have the ability to borrow to invest, which can give them a real boost in rising markets (and exacerbate losses during downturns). The trusts in the table all deploy gearing to various degrees, with Shires Income (SHRS) currently the most geared at 14 per cent of the portfolio.

Some of these trusts also saw their discounts narrow meaningfully in the past year, as net asset value (NAV) performance helped stimulate demand – as at the end of 2024, Fidelity Special Values (FSV) was trading on an 8 per cent discount to NAV, Temple Bar (TMPL) on 6.6 per cent and Lowland (LWI) on 11.7 per cent. Fast forward to 29 January this year, and the first two are trading at around NAV, while Lowland is on a 6.5 per cent discount.

The list also includes one exchange traded fund (ETF), the iShares UK Dividend ETF (IUKD). Not all ETFs are included in the Investment Association sectors, so including any in our table is arguably a little partial. We have kept this one in because it is not just a broad market ETF – instead it tracks “the top 50 stocks by one-year forecast dividend yield”, with weightings determined by yield levels rather than market capitalisation. Its presence in the list also indicates that the top dividend-paying stocks delivered some of the best total returns over the past year.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑