Dividends earned £10,976 beating both the fcast and the target.

An update tomorrow on the 2025 fcast.

A healthy New Year to all.

Investment Trust Dividends

Dividends earned £10,976 beating both the fcast and the target.

An update tomorrow on the 2025 fcast.

A healthy New Year to all.

Goldman Sachs analysts, for example, project the S&P 500 may only generate an average annual return of 3% over the next 10 years due to high valuations and the resulting concentration of value in the index’s biggest holdings.

JPMorgan analysts believe the index will deliver an annual return of just 6% over the next decade.

U have 100k to invest for your retirement in ten years time.

If u buy a S&P tracker and let’s be optimistic and use the 6% growth figure, your 100k could be worth

£179k, could be more could be less.

If u use the 4% rule that would give u income of £7,160 pa, u would need a cash buffer but at the present time u could earn 4% on that cash buffer.

If u buy an annuity, lets be generous again and use a 6% figure, income of £10,174 pa

Canada Life figures show the 65-year-old with a £100,000 pension pot could buy an annuity linked to the retail price index (RPI) that would generate a starting annual income of £3,896. That’s up from £2,195 in the New Year following a 77% spike in rates this year.

Oct 22

It could be less and u have to surrender all your capital but it’s only your retirement u are gambling with.

If u invest in a portfolio of income producing Trusts u could earn 8% and if u compound the dividends at 7% u would have income of 16k pa.

If u leave the funds uncrystallized 25% of that would be tax free and all future dividends would also be 25% tax free. U could pass on your fund to your nearest and dearest but remember those wee cats and dogs.

It’s only your retirement u are gambling with so it depends if u are a gambler or an investor. GL

Dividend Wealth Journal:

The Power of Dividends in Bear Markets

Investing in dividend stocks is a favourite strategy of mine and it might be even more important if we see a Bear Market.

A lot of famous people are telling us a major correction is coming soon.

Are they right?

Not necessarily. They’ve been predicting a huge crash for two years now.

But if we do see a crash, wouldn’t it be great if we didn’t care?

How do we do that?

Dividends.

Here’s why dividends are great during Bear Markets.

1. Consistent Income in Uncertain Times

When stock prices decline, dividend-paying companies still give us regular cash payouts. This income stream can help us deal with the blow of falling portfolio values, offering a tangible return even in a declining market.

For long-term investors, dividends provide a source of steady income that can be reinvested to buy more shares at lower prices. This compounding effect enhances returns over time, helping to offset the losses incurred during a bear market.

2. Lower Volatility

Historically, dividend-paying stocks have less volatility than non-dividend-paying stocks or the market. During bear markets, this reduced volatility translates to smaller declines, helping us preserve more of capital.

For example, during the financial crisis of 2008, high-quality dividend-paying stocks declined far less than the broader market. This stability, relatively speaking, makes them a valuable addition to our portfolios during periods of high market uncertainty.

3. Outperformance in Historical Bear Markets

Looking back at past bear markets, dividend-paying stocks have consistently outperformed market indexes. For example:

During the 2000–2002 dot-com bust, high-dividend-paying stocks declined far less than the tech-heavy NASDAQ index.

In the 2008 financial crisis, dividend-paying stocks provided more stability and a quicker recovery compared to non-dividend payers.

These patterns show us the resilience of dividend stocks during market downturns.

4. Psychological Benefits of Dividends

In a bear market, fear and panic often drive investors to sell, locking in losses. Dividend stocks provide a psychological advantage by giving out consistent income, which can help us stay calm and maintain a long-term perspective.

Knowing that we’re earning a return, even as prices fall, makes it easier to avoid emotional decisions and stick to your investment strategy.

Final Thoughts

Bear markets are challenging, but dividend stocks offer a way to weather the storm. Their consistent income, defensive nature, and lower volatility make them a great choice for preserving wealth and generating returns in down times.

The Snowball will be back before the end of this year with a look forward to 2025 and a wrap for 2024.

VPC Specialty Lending Investments PLC

(the “Company”)

UPDATE

As noted in the Company’s half-yearly results announcement, the Company has now completed the process of removing its currency hedges. Net cash released as a result which was being held against the potential for margin calls on the hedges will be applied to reduce the Company’s gearing.

In the September quarterly report the Company noted work being undertaken in regard to the Razor Group following their business combination with Perch. More details on this will be included in the December quarterly report, but business performance over the last quarter has been poorer than anticipated and it is currently expected that the year-end valuation of Razor will be materially lower than at the last valuation point

These investment trusts are trading at whopping discounts to their net asset values (NAVs). Here’s why they could prove to be brilliant buys.

Posted by

Royston Wild

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

Investment trusts can deliver large returns while allowing investors to effectively diversify. But times have been tough for these companies more recently.

Victoria Hasler, head of fund research at Hargreaves Lansdown, notes that

She also notes that “over the last couple of years we have seen some good quality investment trusts trading on hefty discounts“. This remains the case as we head into the New Year.

So I’m searching for the best value trusts to consider today. Here are two of my favourites.

Donald Trump’s return to the presidency has sent a shockwave across renewable energy stocks. Even companies with little-to-no exposure to the US have slumped following November’s election.

This provides a terrific dip buying opportunity in my opinion. One such business that’s caught my attention is Octopus Renewables Infrastructure Trust (LSE:ORIT).

At 63.5p per share, it trades at a huge 38.7% discount to its estimated net asset value (NAV) per share of 103.6p.

Recent share price weakness has also turbocharged Octopus’ dividend yield to 9.5%. To put this in context, the average for FTSE 100 shares is way back at 3.6%.

I like this trust because of the excellent diversification it offers. It generates power from offshore and onshore wind turbines as well as from solar farms. This allows consistent power generation across all seasons, and boosts efficiency by using technologies that are tailored to different environments.

With assets across the British Isles, Finland, Germany, and France, it can also remain profitable despite poor weather or regulatory issues in one or two regions.

Importantly, it also has no exposure to the US, removing uncertainty over the future of green policies under President-elect Trump.

Such fears — however impractical — may continue to weigh on Octopus’ share price. But over the long term I think it could prove a robust investment.

The Gore Street Energy Storage Fund (LSE:GSF) shares several characteristics with the Octopus trust.

Its share price has declined due to falling confidence in renewable energy. This is because demand for its technologies are tied to growth in the renewables sector, where they provide a stable flow of energy even during unfavourable weather.

Gore Street is also vulnerable to higher interest rates that dampen asset values and increase borrowing costs.

But like Octopus, it also offers excellent value I find hard to ignore. At 50.6p per share, the trust trades at an 49.7% discount to its NAV per share of 100.7p.

Meanwhile, its forward dividend yield is a staggering 13.9%.

This is another share with considerable long-term potential as the world switches away from fossil fuels. Bloomberg estimates the global energy storage market will experience an annual growth rate of 21% between now and 2030.

And Gore Street is rapidly expanding to supercharge long-term revenues. Operational capacity leapt 45% in the 12 months to September, to 421.4 MW.

Tuesday, December 17, 2024 – 10:20

In some ways 2024 was unusual, because the consensus macroeconomic view played out exactly as expected – inflation cooled, there was no deep economic downturn (or even a downturn of any real kind) and interest rates started to fall, says AJ Bell Investment Director Russ Mould.

As a result, investors did not have to change much if they were to benefit: equities did well (again), led by technology and AI-related names (again), with the result that the US stock market outperformed, spearheaded by the NASDAQ (again), while Japan’s benchmark indices did better than those of Europe, which in turn generally did better than those of the UK, while emerging markets lagged, even as China put on a bit of a wiggle towards the end of the year.

| Capital return in 2024 (%) | |||

|---|---|---|---|

| Asset classes | Major stock indices | ||

| Bitcoin | 129.6% | NASDAQ | 33.3% |

| Gold | 30.2% | S&P 500 | 27.2% |

| Natural GAS | 26.8% | TSX 60 | 21.4% |

| Global equities | 18.8% | DAX | 21.3% |

| Commodities | 15.6% | Hang Seng | 20.1% |

| Emerging equities | 9.2% | Nikkei 225 | 17.6% |

| Global high-yield bonds | 2.4% | S&P BSE 100 | 17.1% |

| Global corporate bonds | (0.4%) | Shanghai Comp. | 15.5% |

| Global sovereign bonds | (3.6%) | FTSE 100 | 7.4% |

| Oil | (6.6%) | SSMI | 4.8% |

| CAC 40 | (1.6%) | ||

| Bovespa | (3.4%) | ||

Source: LSEG Refinitiv. Local currency. Data as of 10 December

Meanwhile, holders of benchmark, ten-year government bonds lost money for the third year in four on both sides of the Atlantic, while commodity prices rose, on average, for the fourth time in five. Oil did poorly, gold did well, and Bitcoin went wild (again).

These trends leave 2021/22 looking like a post-COVID-19 aberration and suggest the long-term trend of cheap energy, food, goods, labour and (above all) money that began in the early 1980s is reasserting itself.

It is therefore worth thinking about what happened in 2024 and why, and whether five trends in particular can continue in 2025 and beyond.

The rate of increase in the cost of living slowed right on cue, to give central banks the chance to cut interest rates. That said, much of the improvement in inflation came from oil and energy, as well as goods, where unblocked supply chains helped supply and the lagged effect of higher interest rates took some of the edge off demand. Services inflation remained sticky and that could yet prompt workers to demand more by way of pay increases, so perhaps central banks cannot be too gung-ho with further interest rate cuts just yet.

Source: Office for National Statistics, US Bureau of Labor Statistics, European Central Bank. US and UK based on consumer price index, EU on Harmonised Index of Consumer Prices

A global slowdown did not materialise in 2024, despite disappointing growth from China, Japan, Germany and France (four of the globe’s seven largest economies). India took up some of the slack, the UK emerged from 2023’s shallow downturn and the US once more led the charge.

The Biden administration’s CHIPS and Inflation Reduction Acts buoyed output and American consumers kept spending, helped by rising house and stock prices. America’s latest debt ceiling breach gave no-one pause for any particular thought, even as the deficit soared, and President-elect Trump’s plan to raise revenues through tariffs has provoked as much concern as it has positive comment. If Elon Musk succeeds in cutting US government spending, and Trump rolls back the Inflation Reduction Act, there could yet be some (unpleasant) unintended consequences.

Source: FRED – St. Louis Federal Reserve database

A tally of 175 interest rate cuts worldwide in 2024, compared to just 28 rate hikes, tells a clear story. The UK, Japan and China all added fiscal stimulus to fresh monetary impetus, and you could argue the USA did as well, given how the Federal deficit grew by another $1.8 trillion to an all-time high of $36 trillion. The question for 2025 is whether a combination of sticky inflation, steady growth and ballooning government debts (and rising sovereign bond yields) crimp central banks’ room for manoeuvre and force the pace of rate cuts to slow or, in a worst case, come to a halt.

Source: CentralBankRates

Given how bullish and confident equity markets feel, this is a bit of an outlier.

Silver hit a twelve-year high and gold and (most spectacularly) bitcoin set new all-time highs. Such demand for havens does not sit comfortably besides equities’ core scenario of cooling inflation, steady growth and lower interest rates.

It may be the result of fears that central banks are playing fast and loose with inflation, or that ever-growing sovereign debts are persuading them to cut rates (and ease governments’ interest bills) whether they feel it is appropriate or not. President-elect Trump’s enthusiasm for all things crypto, his planned deregulation drive and the departure of Gary Gensler from the Securities and Exchange Commission mean bitcoin is up 40% in barely two months, helped by what can be seen as increasingly reflexive ETF flows (the higher bitcoin goes, the more buyers appear), in a clear win for momentum over value investors.

Source: LSEG Refinitiv data

The fifth and final trend is another slightly discordant note, as sovereign bond yields tick higher and prices go lower.

This matters because the ten-year bond represents the local risk-free rate and thus the benchmark minimum return from any investment that is acceptable. Yields on ten-year paper rose (and prices fell) despite interest rate cuts, to suggest that bond vigilantes are becoming nervous about governments’ debt piles in the US, UK and EU and whether there is political or public appetite for the tax increases and spending cuts needed to fix them, in the absence of growth or inflation reducing those growing debt-to-GDP and interest bill-to-total spending ratios.

Anyone who bought ten-year bonds in 2020, when central banks were indiscriminate buyers thanks to COVID-fighting QE schemes, has suffered, to perhaps offer a reminder that valuation always matters – in the end.

Source: LSEG Refinitiv data

By David Jagielski

Key Points

Investing in the S&P 500 GSPC has historically been a great way for someone to grow their wealth. As a benchmark for the broad market, the index tracks 500 of the largest and most successful U.S. companies.

While you cannot invest directly in the S&P 500, a number of exchange-traded funds (ETFs) track the index at a low cost. And since these ETFs distribute your money across hundreds of stocks, a bet on the S&P 500 can be a lower-risk way to invest in the stock market than picking and choosing individual stocks.

It may not always be possible to put a big lump sum into the stock market. However, if you come into an inheritance or profit from the sale of a home, you may be able to make a sizable investment, even if you haven’t accumulated a significant amount of savings.

Below, I’ll look at whether investing $50,000 into an S&P 500 index fund can set you up on a path to have $1 million by retirement, a goal many people have in order to live comfortably in their golden years.

Going back nearly a century, the compounded annual return for the S&P 500, including dividends, is 10.1%. in the past 10 years, the index’s return has been an even more impressive 13.7%. While that’s great news for investors who have been invested during that time, the outlook for the next decade may not be so rosy.

Goldman Sachs analysts, for example, project the S&P 500 may only generate an average annual return of 3% over the next 10 years due to high valuations and the resulting concentration of value in the index’s biggest holdings. JPMorgan analysts believe the index will deliver an annual return of just 6% over the next decade.

Put simply, investing in the index today could mean significantly lower returns than what investors have grown used to in recent history.

Data by YCharts.

But for someone starting their career or in the middle of it, investing their retirement savings means thinking beyond the next decade. So, even if the next five or 10 years of returns for the index are relatively weak, the S&P 500 could still make up for those slow years with better returns down the road. There are just too many factors that could weigh on the markets, making it next to impossible to predict exactly what the market will do that many years in the future.

Instead of trying to guess exactly what the annual returns for the S&P 500 will be over the next decade and beyond, the table below illustrates what a $50,000 investment could be worth under different scenarios.

| Projected Value of a $50,000 Investment Today | ||||

|---|---|---|---|---|

| Annualized Rate of Return for the S&P 500 | ||||

| Year | 3% | 6% | 8% | 10% |

| 10 | $67,200 | $89,500 | $107,900 | $129,700 |

| 20 | $90,300 | $160,400 | $233,000 | $336,400 |

| 25 | $104,700 | $214,600 | $342,400 | $541,700 |

| 30 | $121,400 | $287,200 | $503,100 | $872,500 |

| 35 | $140,700 | $384,300 | $739,300 | $1,405,100 |

| 40 | $163,100 | $514,300 | $1,086,200 | $2,263,000 |

Table and calculations by author. Amounts rounded to the nearest hundred.

The reality is that while a $50,000 lump investment may be a significant amount of money, it will still take many years and a solid rate of return to grow to $1 million.

One way to help boost these numbers is by contributing to your holdings over time. Even if you’re able to put a large lump sum into the stock market today, periodically adding to your portfolio can be an effective way to help accelerate your gains.

You may look at the table above and think it’s not worth investing in the S&P 500 if its returns may diminish in the years ahead. Or you may believe you’re better off prioritizing other investments like growth stocks. Just remember that the potential for higher returns also means taking on more risk, and not everyone is comfortable with the extra volatility that comes with such an approach.

Meanwhile, a bet on the S&P 500 offers immediate diversification, and its focus on large, high-quality businesses still makes it one of the most reliable ways to invest in the stock market. But even if you have $50,000 to begin your journey, patience is necessary to give your investment the time it needs to grow into a proper nest egg.

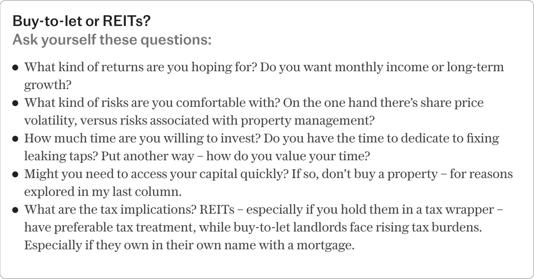

Row of family homes

Often, investors tell me they think buying a property is safer than buying shares. It feel that way, but in reality it’s possible to buy well, or badly, in both cases.

This is no accident. Successive governments have sought a more regulated, professional housing market, discouraging non-professional investors. It’s no surprise that many landlords are selling up.

The thing is, residential property as an asset class continues to thrive. It offers stability, income and long-term growth underpinned by limited housing supply, with demand driven by demographics. Unlike offices or retail investments, we all need a roof over our heads.

So, if you’ve lost faith in buy-to-let, but still want to get a cut of these profits, could property shares, such asTrusts) or shares in housebuilders, offer a practical alternative?

The decision between direct property investment and property shares boils down to control versus convenience.

You benefit from the rental income and growth. It’s not without risks, but if like most road users you think you’re a better than average driver, then you’ll feel safer. If only because owning a physical property can be reassuring.

There are some downsides, of course. There’s the costs I’ve already mentioned which means it’s expensive to get started. You are liable, and compliant tenant management is increasingly costly, time consuming and complex. Plus market risks – for example, changing tax rules and policies – can erode profitability overnight.

At the other end of the control spectrum are property shares, which offer exposure to the housing market without the headaches of direct ownership. REITs, for example, allow you to invest in professionally managed property portfolios, including through your Isa or Sipp.

Liquidity means that shares can be bought or sold quickly and there’s no management hassle or liability for you. Plus, professional managers handle tenants, maintenance and strategy.

However, there are trade-offs. Share prices are volatile and are influenced by market sentiment, not just property values.

You are not in control of anything except when and whether you buy or sell. Instead, you’re betting on fund managers. Incidentally, those fund managers are not cheap, and management fees can erode returns.

REITs also face a “liquidity mismatch”. Shares are easily traded, but underlying property assets take time to sell, which can cause trouble if lots of shareholders decide to sell at once.

The choice often boils down to this: do you want to drive the car or be chauffeured?

Want to make money from buy-to-let? Don’t own property

Buy-to-let allows you to take the wheel. You can potentially earn higher returns through active management, but it also demands time and effort.

Property shares are the muted version. A hands-off option offering lower potential returns, without the headaches or responsibility.

Your decision should align with your financial goals and circumstances. You don’t need to choose one or the other, but you might prioritise differently for your next investment.

A wealth planner I know advises all of her clients to use their Sipp and Isa allowances first, perhaps including property shares, and only then to consider other options like direct property.

In simple terms, risk is the likelihood of losing your money. It can be measured by how much property values and returns vary over time.

In the world of real estate, risk is often explained badly, so many investors overlook the difference between return on investment and return of investment.

For example, as buy-to-let returns have been squeezed, many investors have been seduced into buying “off-plan” or new builds from glossy brochures.

Maintenance costs can be lower for new-build properties (though not necessarily – it really depends on the build quality). However, if you’re buying brand new then, much like a new car, you’re paying the developer’s premium.

If you’re not convinced, find a development that was new 10 years ago on your preferred property platform. Look at the prices paid then, and what has been paid since. Once you factor in stamp duty, legals and agent fees – the original buyer has frequently lost money.

So where does this leave us? Buy-to-let increasingly feels like a strategy that once worked, but doesn’t any more – and property shares could be the modern alternative you’re seeking. But you’ll need to proceed with caution.

As with any investment, do your research, seek professional advice, and, above all, make sure your choices suit your circumstances.

Anna Clare Harper is a property investor, founder, writer and host of a leading property podcast – find out more at annaclareharper.com.

Editor Insights

The average discount in the investment trust sector has expanded to -15.5%. With all sub-sectors, except Debt trading at discounts, funds like MIGO Opportunities and others that exploit pricing inefficiencies may offer attractive returns. Here’s a breakdown of the top holdings among key investment trust investors to help you navigate the sector.

By Frank Buhagiar

As at end of November 2024, the average share price discount to net assets in the investment trust sector stood at -15.5%. According to broker Winterflood, this compares with -12.7% at the end of 2023, -10.7% at the end of 2022 and -2.0% at the end of 2021. Over the last 12 months, the sector average discount has ranged between -11.6% and -16.3% and averaged -14.7%. Over the last ten years, the sector average discount has ranged between -0.3% and -20.9%, while averaging -6.5%. It would seem, based on history at least, that value is on offer in London’s investment trust space. But with all investment trust sub-sectors (aside from Debt – Loans & Bonds) trading at discounts, where does one start when trying to identify those funds that offer the most value?

A good starting point can be the top ten holdings of funds that invest in other trusts. Funds, such as MIGO Opportunities (MIGO), after all, aim to take advantage of price inefficiencies in the investment trust space to generate value for shareholders. Looking at which funds investors, such as MIGO, CT Global Managed Growth (CMPG), CT Global Managed Income (CMPI) and AVI Global Trust (AGT) hold can therefore be a useful exercise. So, we’ve looked at each of these four funds’ top investment company holdings, ranked each one based on the position occupied (10 points for being the top holding, one point for being the tenth holding), totted these up and come up with a combined top ten list of funds held by the above four investment trust investors.

MIGO’s recent half-year report opens with a summary of the fund’s objective:

The objective of MIGO is to outperform SONIA plus 2% over the longer term, principally through exploiting inefficiencies in the pricing of closed-end funds (SONIA being the Sterling Overnight Index Average, the Sterling Risk-Free Reference Rate preferred by the Bank of England for use in Sterling derivatives and relevant financial contracts). This objective is intended to reflect the Company’s aim of providing a better return to shareholders over the longer term than they would get by placing money on deposit.

During the latest half year, MIGO’s NAV and share price moved in opposite directions: NAV per share total return came in at -0.5% while the share price generated a +2.8% total return. Both, slightly below SONIA +2%, which delivered a total return of +3.6%.

The reports penned by MIGO’s investment managers are often an informative read, particularly on the state of the sector. In their latest report, the managers note “Over the past year we have seen several articles about the ‘death’ of the investment trust sector. While it is true that a boom of alternative, income-producing trusts launched to cater to income-starved investors over a prolonged period of easy money has created an over-supply, we think these fears are overdone.” Rather they believe, “Trusts are going through a clean-up period where we see the creative destruction of the excesses of a bull market born of low interest rates and easy money. This has been exacerbated by the availability to obtain a decent income from conventional sources now that interest rates have risen. We fully intend to exploit this process in order to produce attractive returns for our shareholders.” The sector going through a blip but all in all alive and well.

And if that’s the case then, as broker Numis notes, “MIGO Opportunities has a unique mandate, through its focus on exploiting pricing inefficiencies among closed-end funds, with low correlation to mainstream indices. We believe it remains well-placed to deliver attractive returns to investors in real terms, and that now is an attractive time to invest given that the average discount of underlying holdings remains wide at c.35% for the top 10 holdings.”

The table below lists MIGO’s top ten holdings as at 31 August 2024:

| Investment company | % of total assets | Points scored |

| VinaCapital Vietnam Opp Fund | 5.4 | 10 |

| Oakley Capital Investments | 4.7 | 9 |

| Baker Steel Resources | 4.4 | 8 |

| JPMorgan Indian | 4.1 | 7 |

| Georgia Capital | 4.1 | 7 |

| Tufton Oceanic Assets | 3.9 | 5 |

| Aquila European Renewables | 3.8 | 4 |

| Phoenix Spree Deutschland | 3.2 | 3 |

| Real Estate Investors | 2.9 | 2 |

| River UK Micro Cap | 2.8 | 1 |

CMPG’s objective is to provide capital growth for shareholders by investing principally in a diversified portfolio of investment companies. As at 31 October 2024, the fund’s top ten holdings were as below:

| Investment company | % of total assets | Points scored |

| HgCapital Trust | 4.5 | 10 |

| Fidelity Special Values | 4.1 | 9 |

| Polar Capital Technology | 4.0 | 8 |

| Law Debenture | 3.7 | 7 |

| Allianz Technology | 3.6 | 6 |

| JPMorgan American | 3.4 | 5 |

| Monks | 3.3 | 4 |

| Worldwide Healthcare | 3.2 | 3 |

| Oakley Capital Investments | 3.0 | 2 |

| Aurora | 2.9 | 1 |

As with stablemate CMPG, CMPI aims to deliver its objective principally through a diversified portfolio of investment companies. This time, the objective is to provide investors with an attractive level of income with the potential for income and capital growth. As at 31 October 2024, CMPI’s top ten holdings were as below:

| Investment company | % of total assets | Points scored |

| Law Debenture | 5.0 | 10 |

| JPMorgan Global Growth & Income | 4.3 | 9 |

| NB Private Equity Partners Class A | 4.2 | 8 |

| Murray International | 3.9 | 7 |

| Mercantile | 3.8 | 6 |

| Merchants Trust | 3.5 | 5 |

| City of London | 3.3 | 4 |

| 3i Infrastructure | 3.2 | 3 |

| Greencoat UK Wind | 3.0 | 2 |

| Temple Bar | 3.0 | 2 |

AGT, a little different from the other three investment trust investors as it does not exclusively invest in investment companies. Instead, the fund looks to achieve capital growth through a focused portfolio of investments, particularly in listed companies whose shares stand at a discount to estimated underlying NAV. Because of this, AGT’s top ten holdings only included four investment companies as at 31 August 2024. The four funds are listed in the table below:

| Investment company | % of total assets | Points scored |

| Oakley Capital Investments | 6.8 | 4 |

| Partners Group Private Equity | 5.9 | 3 |

| Chrysalis Investments | 4.5 | 2 |

| Cordiant Digital Infrastructure | 4.5 | 2 |

Actually, the table below details the top eleven most popular funds among the above four investment trust investors as the final two have the same score:

| Investment company | Combined score | Current discount (-) / premium (+) | 12-mth discount (-) / premium (+) range |

| Law Debenture | 17 | +1.73% | -6.81% to +2.97% |

| Oakley Capital Invs | 15 | -27.43% | -36.09% to -25.61% |

| VinaCapital Vietnam Opp Fund | 10 | -25.25% | -26.73% to -15.73% |

| HgCapital Trust | 10 | -1.29% | -18.22% to +5.12% |

| Fidelity Special Values | 9 | -8.46% | -10.64% to -4.76% |

| JPMorgan Global Growth & Income | 9 | +1.54% | -3.41% to +3.17% |

| Baker Steel Resources | 8 | -28.92% | -48.83% to -27.60% |

| Polar Capital Technology | 8 | -12.83% | -14.78% to -5.63% |

| NB Private Equity Partners Class A | 8 | -23.31% | -28.84% to -19.99% |

| JPMorgan Indian | 7 | -17.73% | -21.24% to -15.31% |

| Murray International | 7 | -9.41% | -11.99% to -4.87% |

A mixture of subsectors represented from global to private equity, natural resources and technology. Law Debenture (LWDB), the clear winner, although Oakley Capital (OCI) not too far behind. The pair, the only funds to feature in the top ten of more than one of the investment trust investors – OCI featured in three lists, LWDB, two. Interestingly, not all funds in the above table are trading at discounts to net assets – LWDB and JPMorgan Global Growth & Income (JGGI) both trading at premia, while private equity giant HgCapital (HGT) trades at a slight discount

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑