Investing Group Leader Rida Morwa

Summary

- Everywhere in life, you pay for flexibility; In the financial markets, you get paid to seek flexibility.

- Regular income from your portfolio creates cash flow flexibility and gives you options to navigate volatile markets.

- We discuss our top picks that enable consumers and businesses to grow, innovate, and expand.

- Looking for more investing ideas like this one? Get them exclusively at High Dividend Opportunities.

Co-authored with Hidden Opportunities

Flexibility always comes at a price. If you cancel your appointment with a doctor or dentist without providing 24–48 hours’ notice, you will be charged a fee. Life happens, but the policies are firm. Yet, when the doctor or dentist cancels on you with little notice, you are not compensated for your time.

The same dynamic exists in travel. In the post-pandemic era, airlines have monetized flexibility by turning it into a product. If you want to cancel or rebook your flight, you must pay extra for that privilege. If you want to choose your seat, or board early, that costs extra too. The aircraft or travel durations haven’t changed, but pricing has. As a traveler, you pay a premium for flexibility and convenience.

From subscriptions, services, and travel, and everywhere in life, you pay for the privilege of keeping your options open. The financial markets are one of the rare exceptions. Here, the market pays you for providing flexibility to others – through capital, timing, and liquidity.

Every time a consumer makes a purchase that they couldn’t upfront in cash, or delays a payment, and every time a business borrows to expand or manage working capital, they are using flexibility. The two investments discussed in this article let you collect generous dividends from companies that enable that flexibility.

Let’s dive in!

Pick #1: BIZD – Yield 11.5%

That local restaurant you love visiting is opening a new location at the other end of town. How do you think they secure the capital to pursue this business expansion? Unlike large public companies, they can’t issue more shares or debt, nor are they flashy enough for a VC (Venture Capital) to step in. Yet, they provide a service that hundreds, if not thousands, relish.

Born from the Small Business Investment Incentive Act of 1980, BDCs (Business Development Companies) are designed to support small and developing U.S. companies. According to The National Center For The Middle Market, there are over 200,000 middle-market businesses in the U.S., employing over 48 million people, representing one-third of the private sector GDP. This category represents the pulse of the American Dream.

BDCs themselves have different focus areas, with larger ones primarily pursuing first-line senior secured loans, while smaller players concentrating on niches like asset-based lending, equipment financing, life sciences loans, or venture growth financing. They provide capital in different forms to their borrowers, and collect interest payments at rates often in the +10% ranges, regardless of the interest rate landscape.

You can invest in time-tested BDCs like Ares Capital Corporation (ARCC) or Main Street Capital Corp (MAIN), focus on custom-lending solutions pursued by Capital Southwest Corporation (CSWC), or lean towards growth sectors through Runway Growth Finance Corp (RWAY) and Trinity Capital (TRIN). Or you could buy the entire basket of BDCs, in a market-cap weighted approach.

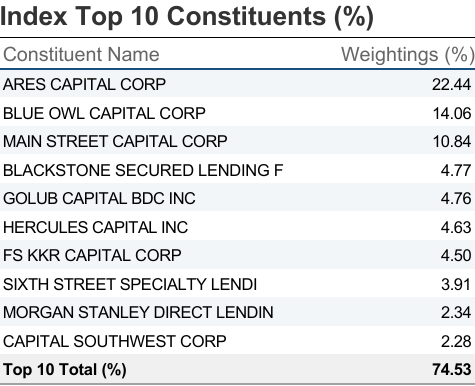

VanEck BDC Income ETF (BIZD) invests in 30 public BDCs with market-cap weighted allocation levels. This means ARCC, the largest public BDC, is its top holding, representing 22.4% of invested assets, followed by Blue Owl Capital Corporation (OBDC) at 14%. Source

Public BDCs provide exposure to over 4,800 middle-market companies. This makes BIZD a large, diversified fund that benefits from the power of the American Economy, almost as the equivalent of the S&P 500 (S&P 5000, anyone?) for middle-market companies.

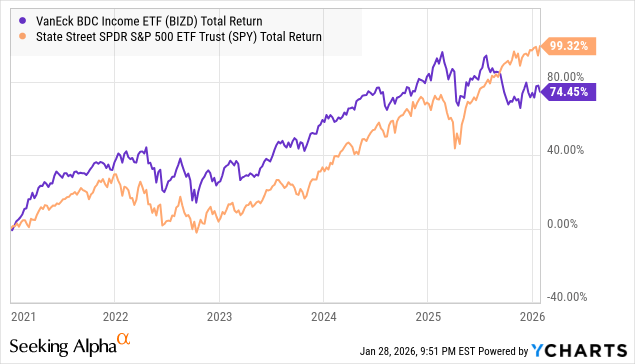

Now, just because of the focus on middle-market companies, BIZD’s 5-year performance against the popular index is not to be underestimated. The ETF has beaten the S&P 500 in the post-COVID recovery, as well as the AI-infused market recovery since 2021, with one notable divergence in mid-2025.

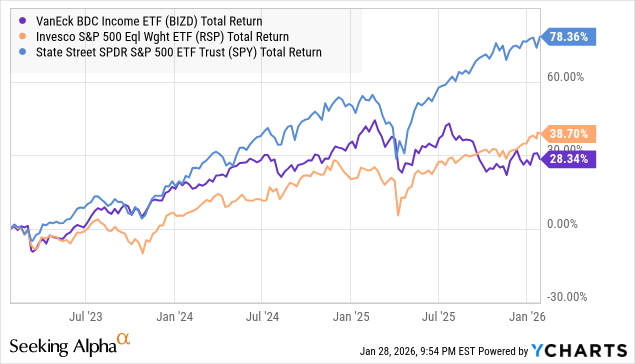

Looking at the 3-year period, the S&P 500 has largely been propelled by the mag-7, and this disconnect from the rest of the index is seen from the equal-weighted S&P 500 significantly underperforming the popular benchmark index. BIZD’s struggles are clearly seen in mid 2025, following the anxiety related to private credit.

Market jitters around private debt quality, caused by the bankruptcy of First Brands and Tricolor, resulted in a steep sell-off in BDCs. None of the larger BDCs invested in either, and despite what the market fears or believes, debt will continue to be a driver for corporate and middle-market America for the foreseeable future.

With over $500 billion in aggregate assets, BDCs represent a major pillar in middle-market debt. A belief in widespread defaults across this segment is not just a bearish view on BDCs; it is a bearish view on the broader economy and capital markets.

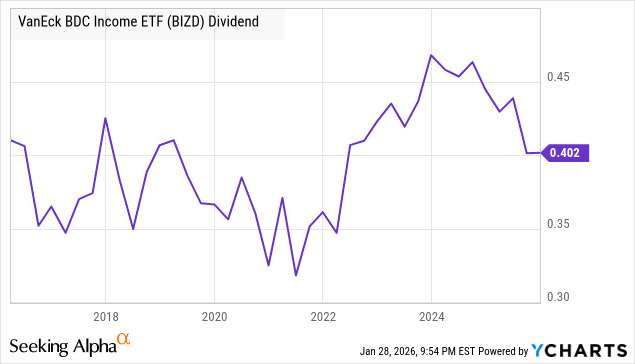

BIZD maintains a variable distribution policy, and its current yield can be estimated at 11.5%. The ETF has delivered reliable distributions over the past ten years, with levels only modestly lower amidst the post-COVID-19 near-zero interest rate conditions.

BDCs benefit from higher rates, but they also benefit from more loan origination at slightly lower rates. We will note that BDCs continue to operate below the midpoint of their target leverage levels, indicating room for expansion. With declining interest rates and massive investment in data centers, and industrial & manufacturing operations, we expect tailwinds for BDC loan origination activity, and BIZD lets you regularly put a portion of all that action in your pocket.

Pick #2: COF Preferreds – Up To 6.4% Yield

Following the acquisition of Discover, Capital One Financial (COF) became the largest credit card issuer and the sixth-largest bank in the U.S., with total assets of around $660 billion.

The acquisition is expected to result in significant cost savings while positioning the bank for expanded market share and profit synergies.

The Trump Administration seems to want to impose a 1-year, 10% cap on credit card interest rates and also slash interchange fees. This would be problematic for card issuers, but we want to emphasize that such a significant change requires legislation, and it will still face legal challenges by the biggest banks in America. The Federal Government does not dictate rates that lenders can charge, because there are complex underwriting functions to determine that based on borrower profile and financial stature.

Looking at it from a business angle, attempts to dictate credit pricing tend to produce the opposite of the intended outcome of improving affordability. Banks will tighten underwriting, reduce approvals, and shift activity toward higher fees, and other products like line of credit, personal loans, and BNPL. Cuts to interchange fees will lead to sharp reductions in perks and rewards. Overall, lower access to credit is bad for consumers and bad for the economy in general.

Every industry, from time to time, receives the threat of regulation. This doesn’t push the industry out of business, but pushes them to evolve, and those who innovate through the challenges thrive. Capital One has specialized in technology-driven lending for over three decades, successfully navigating numerous regulatory changes and economic cycles. We seek to take advantage of the market panic, but invest with a higher degree of safety with COF preferreds.

COF maintains investment-grade BBB ratings from S&P, and the bank repurchased 4.6 million shares for $1 billion during Q3 2025, and maintains an authorization to repurchase $16 billion in shares. Additionally, the company declared a massive 33% raise to its quarterly dividend to $0.80/share.

COF’s card business continues to deliver growing purchase volume, boosted by the synergies from Discover, up 39% YoY. The provision for credit losses rose by $280 million YoY, and the Net charge-off rate was 4.61% at the end of Q3, comparable to pre-pandemic levels. The acquisition reflected strong consumer banking as well, with Q3 ending deposits of $107.2 billion (up 35% YoY), and auto loan originations up 17% YoY to $1.6 billion. COF finished Q3 with excellent regulatory capital ratios, with the Discover merger positioning the bank as a leader in consumer banking, lending, and credit, providing financial flexibility to millions of consumers in America (and U.K. and Canada)

During the first nine months of 2025, COF spent $1 billion on common stock and $195 million on preferred stock dividends, compared to $3.2 billion in net income during Q3. The preferreds enjoy excellent coverage and safety, and pay qualified dividends to eligible shareholders.

- 5.00% Non-Cumulative Perpetual Preferred Series I (COF.PR.I) – Yield 6.3%

- 4.80% Non-Cumulative Perpetual Preferred Series J (COF.PR.J) – Yield 6.4%

- 4.625% Non-Cumulative Perpetual Preferred Series K (COF.PR.K) – Yield 6.4%

- 4.375% Non-Cumulative Perpetual Preferred Series L (COF.PR.L) – Yield 6.4%

- 4.25% Non-Cumulative Perpetual Preferred Series N (COF.PR.N) – Yield 6.3%

Currently, COF-L and COF-N offer ~6.4% yields, with ~45% upside to par, which makes it a safer choice for strong total returns in the rate cut cycle.

Conclusion

Flexibility is rarely free. In most areas of modern lifestyle, you pay extra to keep your options open, and those who provide flexibility are the ones who get paid.

BDCs supply capital to the businesses that drive employment, growth, and innovation, filling a giant void left behind by traditional financing options. Banking institutions extend credit and liquidity to millions of consumers to help them enhance their affordability and better manage their cash flows. In both cases, investors are compensated not for speculation but for enabling the system to function. With picks like this in your portfolio, the income you generate isn’t just return; it is the fee you get paid for flexibility. This is the beauty of our Income Method.