If you buy a 10k position with a share yielding 7% and re-invest those dividends at 7%, in ten years time you will be receiving a yield of around 14% on your position, not dependant on Mr. Market. If the price of the share rises and the yield falls, you may have to take your profit and switch horses.

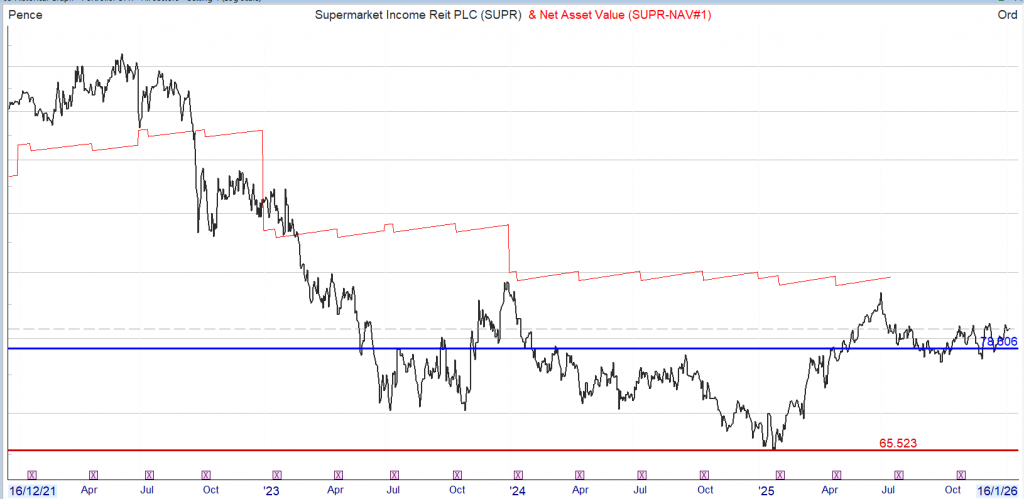

SUPR

Your starting position – 13,000 shares cost 10k – Purchase date: 20 July 2023 Initial yield 7.5% The price fell after the starting position which meant you bought more shares for your money and therefore more dividends.

🟩 FINAL RESULT — Your total SUPR shares today

🎯 Summary

– Starting shares: 13,000 – Dividends received: £1,779.3 – Reinvested at actual prices on xd date – New shares added: ≈2,327 – Total today: ≈15,327 shares

15327 shares x fcast dividend 6.12p = £938.01 a yield on seed capital of 9.38%

All figures subjective to the price you could have dealt at on the xd date.

If you were lucky with you timing, the share including dividends is up 27% over a year, so not so shabby.

Here’s one thing I can say for sure about 2026: This year, we’ll be grateful we’re NOT sitting on “America’s ticker”—my name for the SPDR S&P 500 ETF Trust (SPY).

I call SPY that because pretty well everyone owns it. But its 1% yield makes it more likely that holders will be forced to sell low in the next pullback, if they’re leaning on it to pay the bills.

Not us! We’ll be pocketing the 8%+ cash payouts from the portfolio of my Contrarian Income Report service. So while SPY holders face the next pullback with dread, we’ll be chugging along with our usual “dividends and chill” approach.

When a storm hits, we simply wait for our next big dividend payment to roll in. (And we don’t have to wait long—many of our divvies are paid monthly.)

Today I want to zero in on one attractive 13.4% (!) payer from our portfolio. Then I’ll show you a smart, simple way to forecast that massive dividend (and indeed any payout) with ease.

This 13.4% Payer Loves This “Bearish” Bull Market

We love FS Credit Opportunities (FSCO) for a lot of reasons, but its sky-high—and growing—dividend is right up there. FSCO yields a mammoth 13.4% today (more on that in a second).

Small businesses—the main drivers of US economic growth—love BDCs, too, because they loan money to these firms. BDCs are a godsend for these mom-and-pop shops, who often struggle to get the capital they need from stingy banks.

Most BDC managers sit in their cozy offices, wait for a private-equity sponsor to call, then write a check for a safe but low-paying loan.

Not FSCO. Portfolio manager Andrew Beckman buys distressed loans for dimes—even pennies—on the dollar. His chops in this arena drive the stock’s growing 13.4% payout.

Beckman is the industry’s “credit surgeon.” Forget the safe loan! He wants the patient who’s bleeding out on the table because he can stitch them up—and charge a fortune for doing so.

Before FSCO, he spent the core of his career at Goldman Sachs (GS), in their legendary Special Situations Group. These “credit commandos” thrived buying depressed assets in the 2008/2009 crisis.

FSCO is a BDC in a closed-end fund (CEF) wrapper. As a CEF, it can (and does!) trade at different levels in relation to its value. Today, it trades at a 14.7% discount to NAV because slower jobs numbers are sparking recession worries. That means we’re getting FSCO’s expertly run loan portfolio for just 85 cents on the dollar.

Yes, hiring is slow, but that’s because companies are implementing AI to boost efficiency. And small businesses are the No. 1 users of this tech.

Meantime, the Atlanta Fed’s GDPNow estimate shows that the US economy is still solidly in growth mode: a strong 3.5% rate, to be exact.

The disconnect between investors’ mood and strong growth is our opening to grab FSCO, and its 13.4% payout, at a bargain.

Buy FSCO, Then Do This to Forecast Your Dividends for Years

High, and rising, dividends like this one really are unicorns, and I see a diversified portfolio of them as a far better option than ETFs like SPY.

But the key to getting peace of mind (and dodging the urge to sell when markets fall out of bed) is knowing exactly when your next payout is coming. Truth is, there aren’t many tools out there that do this. And even fewer that do it well.

My Top 2026 Market Prediction (and 3 Cheap Dividends to Play It)

Brett Owens, Chief Investment Strategist Updated: January 6, 2026

Ignore the doom-and-gloom “predictions” about 2026. There are plenty of gains—and growing dividends—to be had for us this year.

And if we do see a short-term pullback—possible, as we discussed a few weeks ago—the “smart money” is already setting up for a rebound. We’re going to join them by targeting three “depressed” corners of the market. We’ll get into those (and three tickers) below.

DC Stacks the Deck

Why am I so optimistic? Because, to be frank, the fix is in.

We are entering a year of “administered growth.” The Trump team has made its wishes clear: It wants lower mortgage rates, cheaper borrowing costs and a laissez-faire backdrop for American businesses.

And no matter who takes over at the Fed when Jay Powell leaves in May, they’re certain to push for lower rates out of the gate—in line with the administration’s stated (and stated, and stated) wishes.

Plus, midterm elections! We all know the administration wants a strong economy heading into the midterms. There will be money pumped into the economy this year.

In the meantime, growth remains robust, with the Atlanta Fed’s GDPNow measure giving an initial reading of 3% for Q4. That’s solid—and economists see S&P forecasts popping 15.5% next year. It’s tough to get a recession when bottom lines fatten like that.

… But We Still Need to Be Picky

That said, this is still a stock-picker’s market, and we contrarians will still do what we always do: Go where everyone else is not.

Buy an S&P 500 index fund now and you’ll lock a third of your investment in the Magnificent 7: Apple (AAPL), Amazon.com (AMZN), Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT), NVIDIA (NVDA) and Tesla (TSLA).

I’m an AI bull. But I see the biggest gains flowing to the insurance, pharma, agriculture and other firms using the tech—less so the providers themselves.

I think other investors will see things this way, too, and they’ll rotate into other corners of the market as they do. These three tickers are a great way to “front run” them.

Consumer Spending Is Soaring. Mastercard Is Here for It

Consumers are still spending, though higher income earners are driving most of those gains, while lower-income folks cut back.

No matter how we feel about that, with productivity (and corporate profits) surging thanks to AI, consumers will likely keep tapping their cards in 2026.

That’s great for Mastercard (MA), which, along with Visa (V), essentially holds a duopoly on transaction processing. Every time a card (or phone, or mouse) is used to make a purchase, this duo gets a piece of the action.

Yes, Mastercard’s 0.6% current yield is uninspiring. But dividend growth is where the party’s at. Over the last five years, MA has essentially doubled its payout, and the share price has followed along—the “Dividend Magnet” effect we’ve talked about before. And now we have a gap between the two to take advantage of.

Dividend Doubles—Share Price Primed to Follow

Management knows this stock is strong: They’re hiking the divvie at an accelerating clip, with the last hike coming in at a rich 14%. And they’ve got a free hand to add more payout fuel to the fire, with a mere 17% of free cash flow going to dividends.

At that rate, investors don’t have to worry about a recession. Mastercard can keep the payout popping through any storm!

That payout resilience gets a boost from buybacks: Over the last decade, management has taken 10% of Mastercard’s shares off the market, leaving fewer on which it has to pay out—and setting the stage for even stronger per-share payout growth down the road.

A Low-Risk Play as AI Supercharges Medical Research

Healthcare is one place where we can clearly say there’s no AI bubble. Which is funny, because it’s where the tech can drive the biggest gains, as it slashes the amount of time needed to develop new drugs and medical devices.

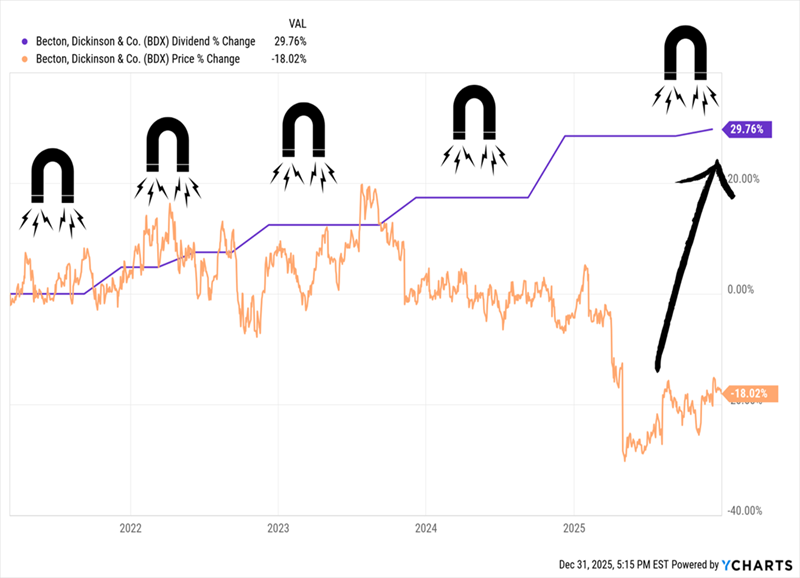

Enter Becton, Dickinson & Co. (BDX), which yields 2.2% and makes hospital mainstays like syringes, catheters and blood-flow monitors.

Our opening? BDX’s Dividend Magnet, which had been working well until a disappointing earnings report in May. That pulled down the stock and gave BDX a “dividend gap” I see as an opportunity.

Another “Dividend Gap” for Us to Play

Meantime, I see dividend growth accelerating, for a couple reasons.

First, demand for BDX’s products will naturally float higher as the population ages. Further growth comes from its Life Sciences division, maker of products every lab needs, like flow cytometers, used to analyze immune cells, cancer cells and biomarkers.

Then there’s the upcoming merger of its bioscience and diagnostics businesses with Waters Corp. (WAT). Management sees the deal teeing up 5% to 7% yearly growth for Waters, and here’s the real upside for BDX: Its shareholders will own 39.2% of the combined firm, letting it book a slice of those profits passively. Management can then focus on BDX’s remaining products.

The kicker: BDX also gets $4 billion in cash, half of which will go to buybacks, with the rest paying down debt. As with Mastercard, this opens the door to higher future payout hikes.

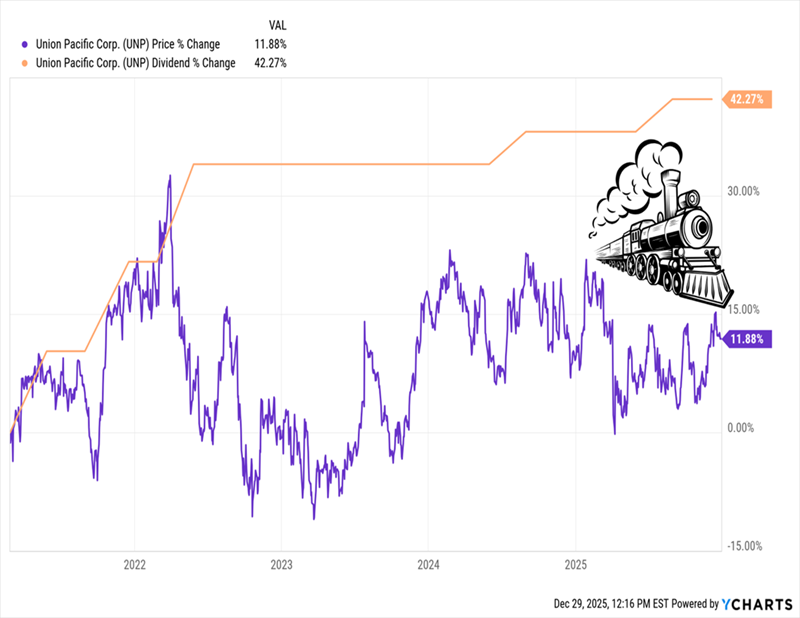

UNP Is About to Leave the Station

Trump’s tariffs hammered shippers in 2025, including railroads. Union Pacific (UNP), whose lines spread across the west and into Mexico, felt the heat. Now the company aims to capture more US business through its merger with eastern-focused Norfolk Southern (NSC).

Regulatory approval is far from certain, but either way, the “trade” winds are about to swing behind railways, and UNP’s soft stock price—which moved sideways in 2025—makes it a contrarian standout.

For one, the administration is being hammered on affordability, and it’s responded by cutting tariffs on over 200 food items. That’s a big “tell” that if inflation doesn’t let up, more tariff cuts are likely.

Then there’s the USMCA, which is up for renegotiation this year. In hearings held so far, US businesses have clearly said they want the deal to stay. And it’s always a safe bet that business—especially American big business—will eventually get what it wants.

Meantime, UNP is performing well, with EPS up 7% year-over-year in Q3. Management has also boosted efficiency, cutting UNP’s operating ratio (operating expense divided by operating revenue, the lower the better) by 1.8 points, to an adjusted 58.5%. That’s a solid result, with most Class I railroads in the 60% to 65% range.

UNP’s dividend growth has slowed recently (though it’s still up nicely in the last five years). The stock, too, has fallen off the pace. But I see that changing as trade worries wane and the NSC merger becomes clearer.

UNP’s Dividend Leaves the Station—Its Share Price Runs Late

That lag makes now a good time for a contrarian pickup—before unloved sectors like railways start to look very appealing to mainstream investors shifting out of tech.

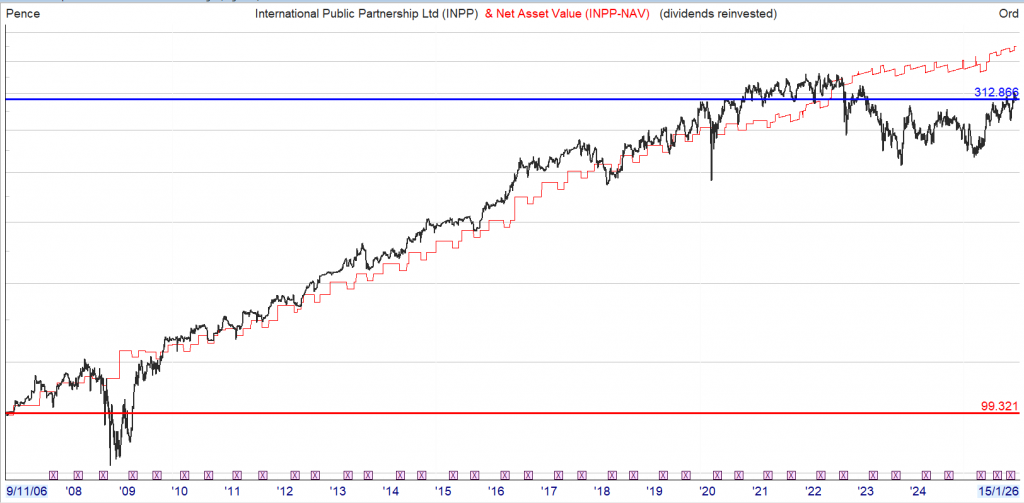

0.32% in 2018 and added significantly to it in 2025. The portfolio of infrastructure projects includes train leasing, offshore power cables and London’s new “super sewer”. INPP yields around 7%. Its discount is -16%.

“These assets are mostly in the UK and have highly predictable, long-term cash flows, typically with an element of inflation linking,” says Laing.

Laing adds: “These private assets are hard to value, so discounts should be taken with a pinch of salt, however INPP has sold £345 million of assets, or 13% of the portfolio, to third parties at or above NAV, giving some hard evidence of pricing.”

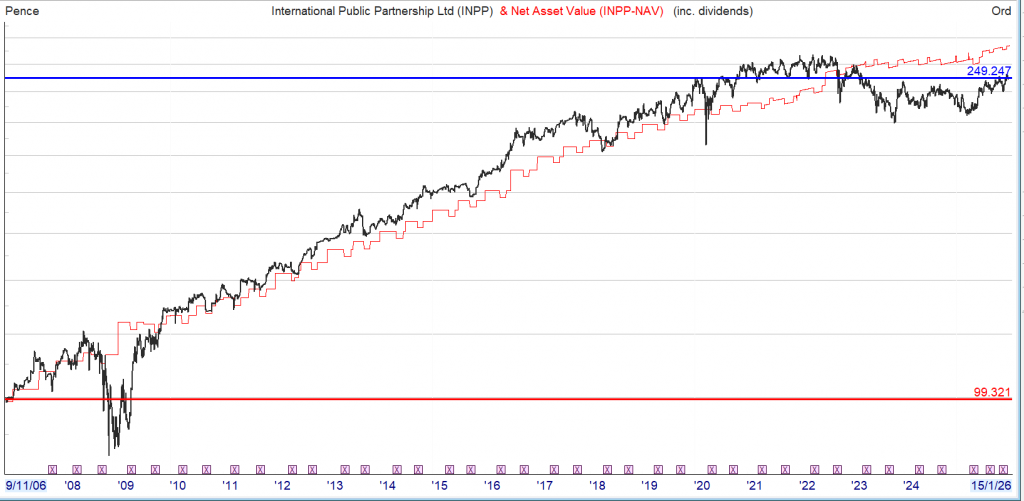

The same chart but with dividends re-invested into your Snowball

Not been a great investment for the last 5 years but has returned reliable dividends for re-investment.

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

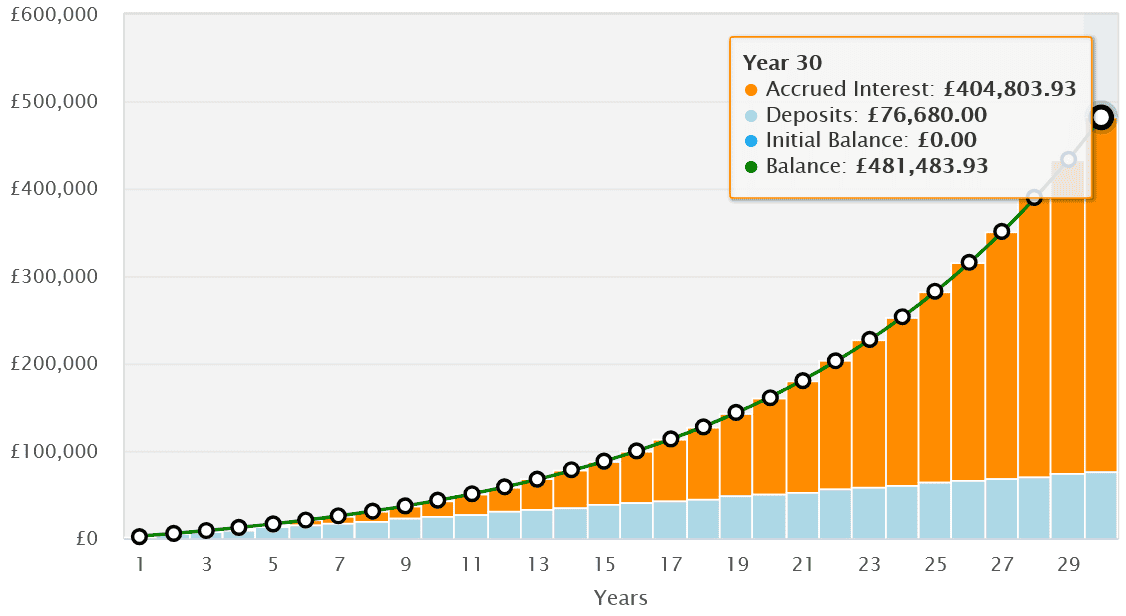

What can you get for £7 nowadays? An overpriced coffee, a short train journey. With the right investment strategy, it could also provide a substantial cash boost in retirement with dividend shares.

Sound far fetched? It really isn’t, as I’ll now demonstrate.

Should you buy iShares III Public – iShares Core Msci World Ucits ETF shares today?

Targeting a £33.7k income

Thanks to the mathematical miracle of compounding — where returns are reinvested to grow over time — and the long-term power of the stock market, even a modest sum like this can create life-changing wealth in later life.

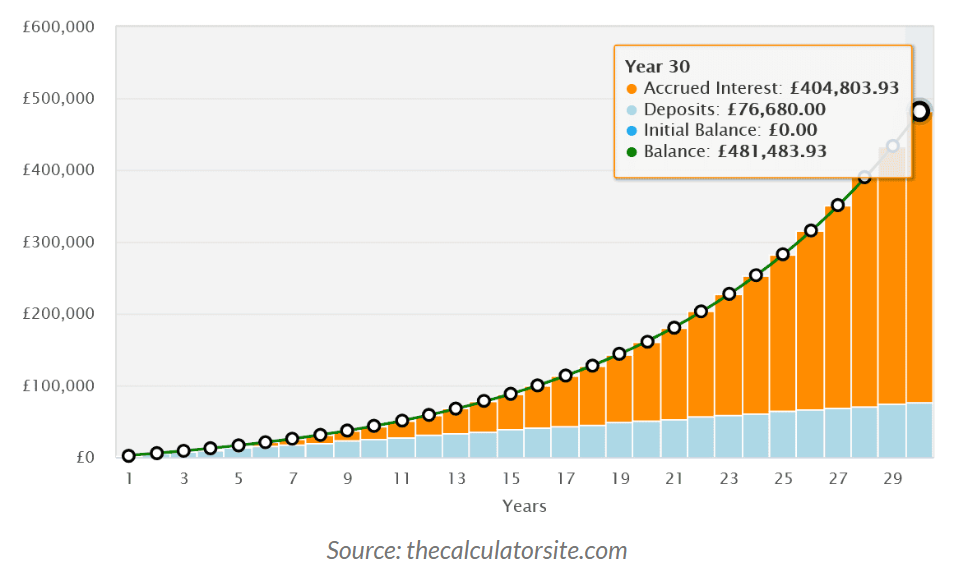

£7 a day works out to £2,555 over a year, or roughly £213 a month. If put in the stock market and delivering a 10% average annual return, an investor could turn that into a whopping £481,484 over 30 years.

Source: thecalculatorsite.com

But how could that be turned into a large retirement income? One method could be by buying dividend shares. It’s a strategy that can provide scope for further portfolio growth alongside a beautiful passive income.

Let’s say our investor puts their £481,484 into dividend-paying stocks with an average 7% yield. At this rate, they would receive a tasty £33,700 second income to supplement the State Pension.

Tips to build wealth

That’s a pretty impressive passive income, I’m sure you’d agree. And it’s one that investors would likely need to pull several smart tricks to achieve.

For example, they’d likely need to eliminate capital gains and dividend taxes to boost compounding — as well as income tax on withdrawals — by investing in a Stocks and Shares ISA.

They’d also need to come up with a sound investing strategy, like thinking long-term and ignoring temporary market volatility; taking time to find durable, quality stocks; and building a diversified portfolio of shares.

The final point is critical, as it provides a smooth return andeliminates concentration risk by spreading out an investor’s cash. This can help an investor enjoy a handsome return even if one or two companies underperform.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Balancing risk and reward

Want to know how this can be achieved quickly and cheaply? Investment trusts and exchange-traded funds (ETFs) are the answer. These investment vehicles can hold hundreds of stocks along with other asset classes like cash, bonds, and precious metals.

Take the iShares Core MSCI World Index (LSE:IWDG). This ETF holds shares in 1,317 different companies, spanning various parts of the globe and taking in around a dozen different industries.

To give you a flavour, some of its notable holdings include chipmaker Nvidia, retailer Amazon, drinks maker Coca-Cola, and bank HSBC.

Like any shares-based fund, it can fall when broader stock markets decline. However, it’s still (in my opinion) a great way to balance risk and reward. Investors here have enjoyed an average annual return of 11.7% since the fund’s creation in 2017.

Purchasing individual shares is higher risk but can yield greater returns. But the gains on many ETFs are far from shoddy, as this iShares product’s performance shows.

The 11.7% return it’s provided beats the broader stock market’s 8% to 10% long-term average. And if that continues, someone investing £7 a day here could realise an even-better dividend income than the £33,700 described here. It’s just one great option to consider to build wealth with shares.

Baillie Gifford European Growth Trust PLC ex-dividend date CT UK High Income Trust PLC ex-dividend date Schroder European Real Estate Investment Trust PLC ex-dividend date Scottish Oriental Smaller Companies Trust PLC ex-dividend date Workspace Group PLC ex-dividend date

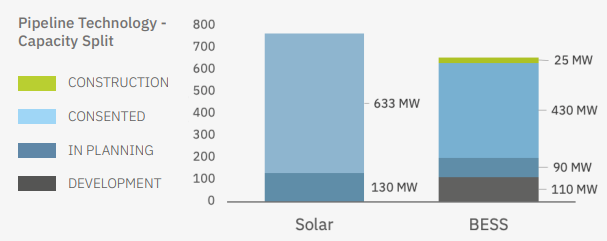

Belatedly picking BSIF for the picks for 26 a reader asked but why not NESF?

Oh ho. That old chestnut. Again. I compared NESF vs SEIT in 2025 and came out strongly in favour of SEIT. Would BSIF beat NESF? And while we are at it, what about BSIF vs SEIT?

Since I covered NESF in “is it crackin’” back in June it’s dropped -30% from 70p to 50p. Is that an opportunity too? Cheap enough to change one’s mind?

Let’s find out which ones are tidy.

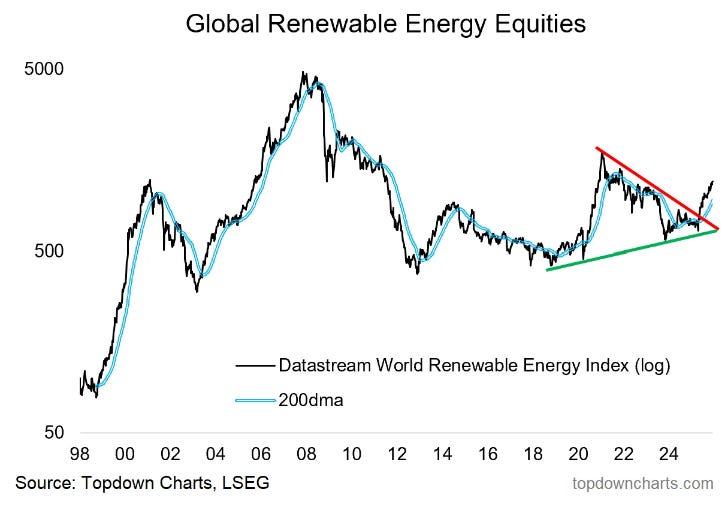

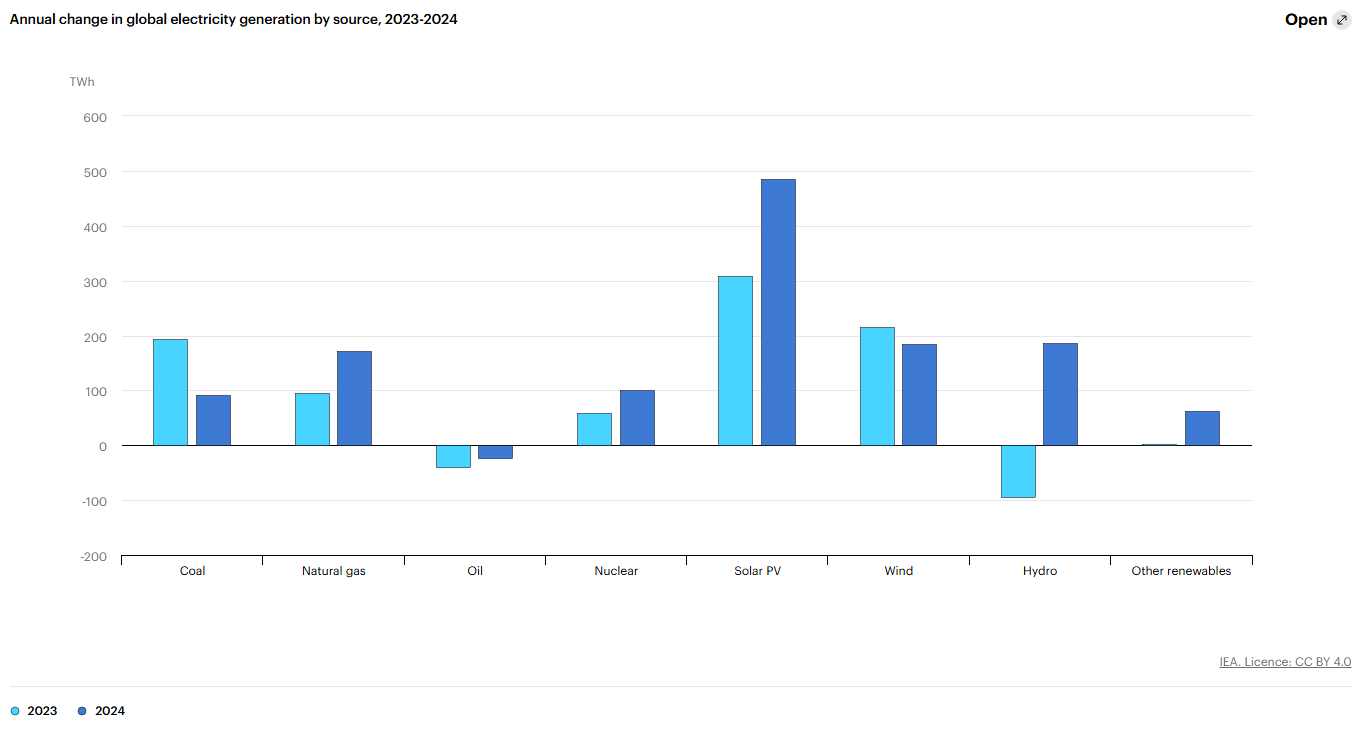

Generally I do feel the sector is over sold. This is an interesting chart I stumbled upon over at Topdowncharts.com that validates that view. How can that be happening if Power Curves are leading Renewables towards perpetual prices of doom? Of course Global Equities aren’t UK equities and we do have Ed Milli to contend with.

Worldwide electricity generation is growing by 100s of TWhs and Solar is leading the, ah, charge. Why is so much investment going into an asset whose income is in decline? Something doesn’t add up, and it’s my contention that it’s the power curves.

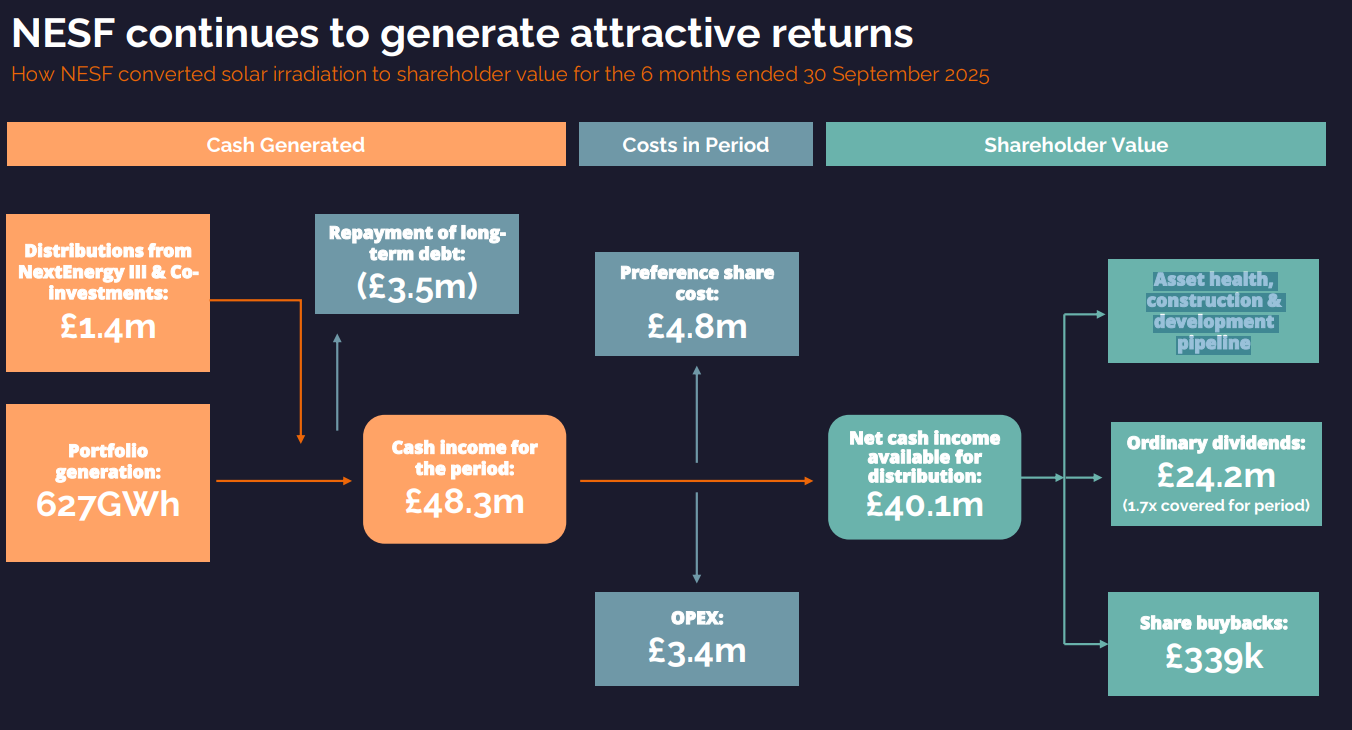

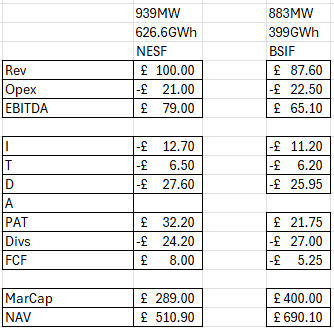

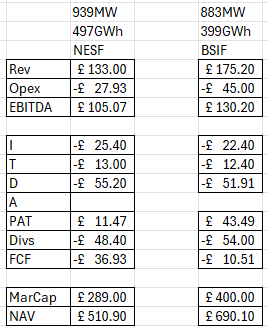

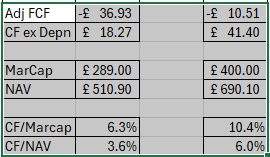

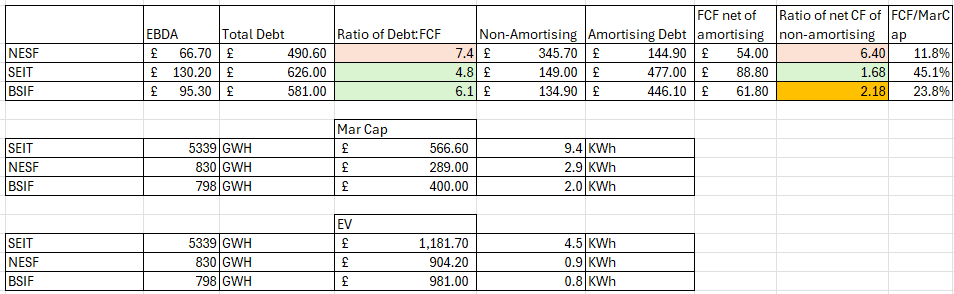

NESF: I’m going to compare the 1H26 at NESF vs 50% of the FY25 results at BSIF to take a view. I’m a bit shocked. BSIF comes back with a -£5.25m deficit post dividends and after imputing an adjusted net profit, while NESF shows +£8m adjusted FCF.

This is where I am ignoring the power curve nonsense of FV gains/losses and instead assigning a Depreciation number in relation to the MW Capacity of generation. It’s crude but we do know these panels depreciate over 30 years and valuing a business this way seems much more sensible than the FV judgments obscured and obsfuscated. Depreciation as a guide which approximately tallies with 1/30th of the estimated capex cost. Remember it is also considering repairs and upgrades. NESF considers this a form of “distribution” and in a way it is – the NAV increases through investment but if the investment is just to stand still – well that’s a P&L cost – whether you call it depreciation, repairs or maintenance. This was one of the other forms of obfuscation that irritated me with how NESF portray their accounts.

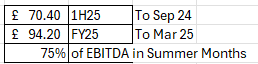

On the face of it NESF is the better investment. But then I start to ponder. NESF’s interim period is March to September. BSIF is 50% from Jan to Dec. Hmm. The sunshine breaks through and I realise I need to think about the seasons.

Comparing 1H26 NESF vs 50% of BSIF FY25

Of course the longer days of summer months are going to deliver a stronger result for Solar during April to September. On a frosty day like today that truth seems truer than ever. Duhhh.

I find the EBITDA split is 75%/25% at NESF.

So if I increase the NESF EBITDA by 33%, and double the BSIF (remember I halved it before), and of course double the ITDA amounts (these are not seasonal), then we see quite a different result.

At current levels of dividends both trusts are “eating themselves” after you factor in depreciation, although on a cash basis NESF delivers £18.20m vs £42.4m at BSIF – post dividends.

In relation to the marcap you are in the long run much better off buying BSIF unless NESF falls to below 30p a share. That’s because NESF doesn’t appear to be keeping enough money to maintain its portfolio. Bear in mind these numbers are post dividend and NESF pays a higher dividend (as a percentage)

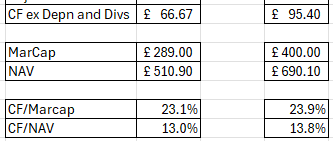

If we add back the dividend the difference between NESF and BSIF reduces to a much smaller difference, although compared to the NAV or the current share price BSIF does look the better pick generating 23.9p per £1 invested vs 23.1p.

But there are further reasons to choose BSIF.

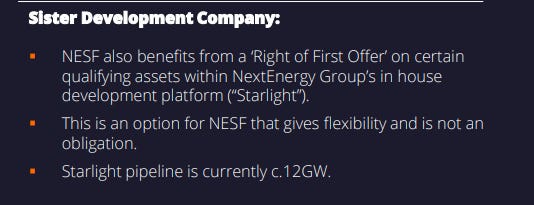

NESF has a “sister co”. It has a first refusal but owns no development pipeline of its own. It has carried out no further disposals in 1H26.

BSIF actually owns the pipeline and can sell these to its sister co the JV which it owns 25% of.

Some other metrics that catch my eye include BSIF has much better debt metrics cost in terms of average cost plus in terms of gearing. As debt gets run down the difference between NESF and BSIF would get more acute because BSIF cost of capital is 1% lower and it has less absolute debt and with no cliff edge (middle of Norfolk remember).

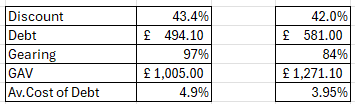

NESF it is fair to say has a slightly higher discount to its NAV: 43.4% vs 42%

From an income generation point of view SEIT exceeds BSIF on earnings as a proportion to its market cap and the cash flow relative to debt.

SEIT also exceeds BSIF from an energy generation/conservation per £ of market cap and enterprise value too. But BSIF exceeds NESF, by quite some way.

Conclusion

BSIF stands up well to NESF – if you compare it season for season.

BSIF also has the advantage of being sold – potentially – in 2026 as a going concern. That’s not the case for either NESF or SEIT (although some selected disposals are planned for SEIT and Saba have been buying SEIT and a continuation vote is planned)

BSIF as part of the picks for 26 stands up to the scrutiny of comparison with its peers. Yes the headline yield number is slightly lower but that’s because NESF continues to eat its own tail in my opinion. A high yield can be too high.

Regards

The Oak Bloke

Disclaimers:

This is not advice – you make your own investment decisions.

Discover three top UK and US dividend stocks with yields of up to 7.1% — and why Royston Wild believes they might be too cheap for investors to ignore.

Posted by Royston Wild

Published 4 January

Image source: Getty Images

You’re reading a free article with opinions that may differ from The Motley Fool’s Premium Investing Services.

2025 proved to be a spectacular year for global stock markets. Unfortunately, this made things more challenging for investors seeking a large passive income from dividend-paying stocks.

The MSCI All Country World Index — which tracks large- and mid-cap shares in developed and emerging markets — has delivered its best year since before the Covid-19 pandemic. As a consequence, dividend yields have toppled across the globe.

Yields fall when share prices rise, meaning share pickers receive lower income on their investment. But this doesn’t make it impossible to find quality high-yield shares. Indeed, stock markets remain packed with brilliant bargains, and not just in terms of future dividends.

Realty Income, Aberdeen Asian Income Fund and Verizon Communications (NYSE:VZ.) are just three top stocks deserving consideration right now. Want to know what I think makes them so great?

Realty check

Realty Income’s a US-listed real estate investment trust (REIT). As such, it offers dividend visibility that few other shares can. Under sector rules, these trusts must pay at least 90% of annual rental earnings out to shareholders.

This doesn’t necessarily mean companies like this are watertight income stocks. Dividends remain linked to profits, which can dive when occupancy levels drop and/or rent collection issues spring up.

But Realty Income’s huge portfolio of 15,000-plus properties helps spread this risk. Its diversified approach has delivered regular annual dividend growth since the mid-1990s.

Today, the REIT’s forward dividend yield’s a huge 5.9%. And its forward price-to-earnings growth (PEG) ratio’s 0.9, illustrating excellent value.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Looking to Asia

The Aberdeen Asian Income Fund is a cheap and easy way to harness the dividend potential of emerging market shares. An investment here provides one with instant exposure to 57 different dividend-paying stocks.

Okay, Asian shares can be more volatile than those in the UK and US. But it can also lead to enormous long-term returns as rapid economic growth drives company profits.

Aberdeen Asian Income’s proved an excellent dividend share down the years. Annual payouts have risen for 22 years on the spin. For 2026, its dividend yield is a tasty 7.1%. Right now, the trust also trades at a 7% discount to its net asset value (NAV) per share.

A top US stock

Verizon is in many ways one of the best US dividend shares. It’s not perfect, as high infrastructure spending and competitive pressures can impact earnings and by shareholder payouts. But there’s also a lot to like here.

Telecoms remains one of the most defensive industries out there, and especially in our increasingly digital age. This gives the company recurring subscription revenues and stable cash flows it can use to fund large and reliable dividends.

Verizon’s also raised annual dividends every year for almost two decades. Predictions of a further rise in 2026 means its shares yield an enormous 6.9%.

With the company undergoing significant restructuring under new CEO Dan Schulman, it could deliver increasingly tantalising dividends and strong capital gains looking ahead. Today, its shares trade on a low forward price-to-earnings (P/E) ratio of 8.4 times.