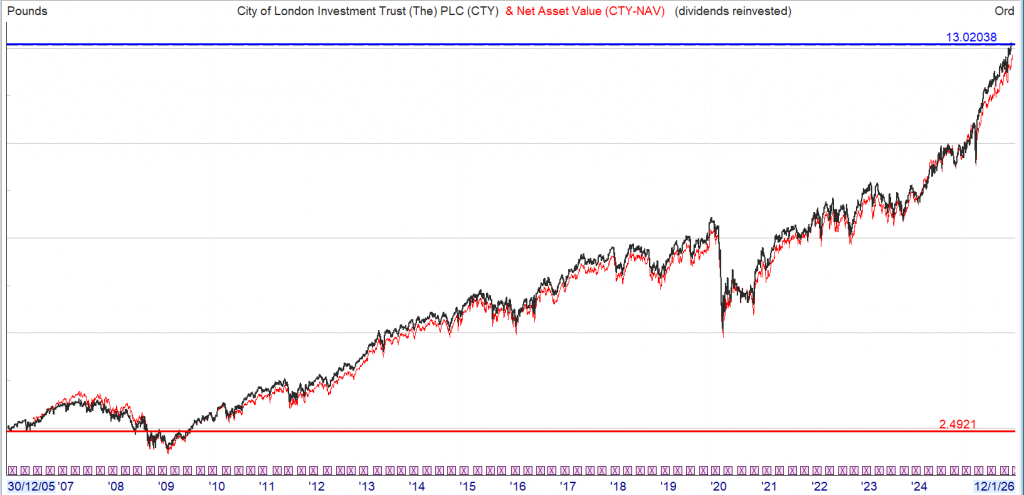

Investment Trust Dividends

Compound Interest.

The interesting thing about compound interest is that you stand to make more in compound interest in the later years of your Snowball than in all the early years.

Good news if you only have a modest amount in savings but intend to add to your Snowball when you can.

“The true investor… will do better if he forgets about the stock market and pays attention to his dividend returns.” – Benjamin Graham

How to harness the power of dividends

Dividends went out of style in the pandemic. It’s great to see them back, says Rupert Hargreaves

Dividend income has always been one of the key contributors to equity-market returns, especially in periods of volatility or bear markets. In the 1970s and 2000s, both periods of significant market volatility for the S&P 500, virtually all of the index’s returns came from income, according to data compiled by Bloomberg and Guinness Global Investors. In the 1970s, the index recorded growth of 76.9%, with 17.2 points coming from price appreciation and 59.7 from dividend income. In the 2000s, the index fell by 24.1%, but dividends added 15 points for a total return of -9.1%.

The longer one stays invested, the more critical dividends become. Guinness Global’s data, going back to 1940, reveal that, over rolling one-year periods, the total contribution from dividend income to total return was just 27%, but that number grew to 57% over a rolling 20-year period. They also reveal that $100 invested at the end of 1940, with dividends reinvested, would have been worth approximately $525,000 at the end of 2019, versus $30,000 with dividends paid out. In this period, dividends and dividend reinvestments accounted for 94% of the index’s total return.

If you want to be a Warren Buffett mini me.

Warren Buffett just collected another $204 million from Coca-Cola — a reminder that some of the most powerful returns on Wall Street come from patience, dividends, and owning the right business for decades.

Here’s how that payout breaks down, why Coca-Cola keeps funding Berkshire’s war chest, and what this kind of compounding looks like in real dollars.

Coca-Cola has been one of Warren Buffett’s signature bets since the late 1980s, and it’s still paying like clockwork.

Berkshire Hathaway owns 400 million shares, and Coca-Cola’s $0.51 quarterly dividend just delivered a $204 million payout. Sometimes the biggest wins aren’t dramatic. They’re automatic.

Coca-Cola dividends now bring Berkshire over $800 million a year, far beyond the original $1.3 billion cost. Coca-Cola may have its “secret” headlines, but Buffett only cares about one secret: the dividend arriving every quarter.

Why Coca-Cola Still Matters

Coca-Cola isn’t just a dividend machine, it’s still a modern profit engine.

With a market cap around $289 billion and gross margins above 61%, the company keeps doing what it does best: defend pricing power, stay everywhere, and find small ways to sell more. Mini cans. Convenience-store pushes. Product tweaks that look boring up close, but scale fast when you’re global.

That durability is why some Wall Street analysts still see upside, with price targets reaching $80. This implies that Coca-Cola is still being priced as a cash machine with staying power. And for Berkshire, that’s the whole point. No hype. No chasing trends. Just owning a durable cash machine, year after year, and letting dividends and compounding do the heavy lifting.

This is where most investors get caught. They chase the hot stock, the pop, the quick win, and end up trading emotions instead of building wealth.

Buffett plays a different game. He doesn’t need to react to every headline. He owns businesses that pay him, then lets time and dividends do the work.

The difference isn’t access to information. It’s behavior, and the traders who last tend to rely on rules, not emotion, like stop-loss and take-profit orders

Why This Dividend Story Matters

That $204 million payout is more than a headline number. It’s what long-term investing looks like when the business is durable and the cash flow is real.

While plenty of investors chase the next spike, Buffett’s Coca-Cola stake shows the quieter path: own a high-quality company, let the dividend stack up, and give compounding time to do its job. You don’t need to love soda to take the point, you just need to respect what consistent payouts can build over decades.

You do not need to take high risks with your hard earned, above the dividends have been re-invested, where because of the lower yield you might have re-invested elsewhere in your Snowball.

If you had bought at £2.50 the yield was around 4% and the current yield on buying price is 8.5%

An option for your Snowball might be to squirrel away some of your dividends, especially if you have a long time before you want to spend your dividends, in a quasi tracker as markets will always go higher because of inflation although near the end of a bull run, maybe is not the best time to start a position.

Finally the rules for the Snowball for any new readers. There are only 3.

Rule one. Buy shares that pay a ‘secure’ dividend and use those dividends to buy more shares that pay a ‘secure’ dividend.

Rule two. Any share that drastically changes its dividend policy mist be sold, even at a loss.

Rule three. Remember the Rules.

The Snowball starts the 2026 journey with a balance of zero, zilch, nothing but with a dividend of £259.00 added to today.

Cash for re-investment £523.00

May the world find some peace.

2023

The Snowball earned income of £9,422.00

2024

The Snowball earned income of £10,786.00

2025

The Snowball earned income of £11,914.00

The target for 2026 remains at 10k.

For comparison, the current value of VWRP is £151,722.

Using the 4% rule that would provide a pension of £5,350.00, after withdrawing 3 years of a cash buffer. That is after one of the best years for a TR strategy in recent memory.

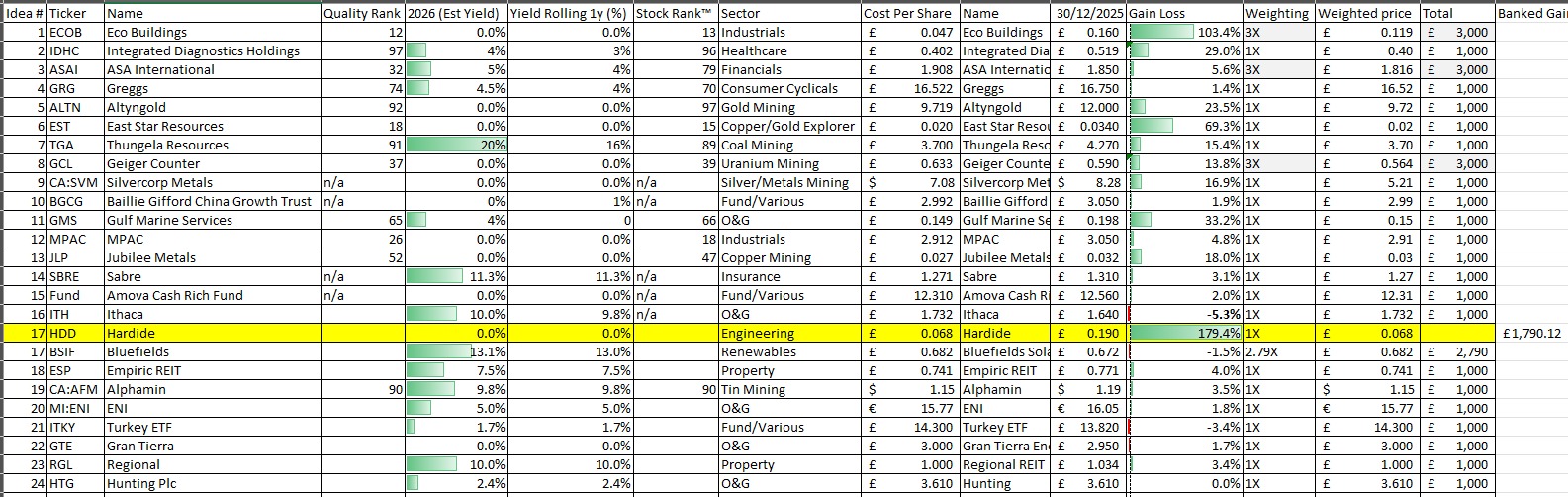

I’ve bought for the Snowball a further1566 shares in FSFL Foresight Solar

Yielding 12.6% and trading at discount to NAV of 38%.

Dec 30, 2025

Dear reader,

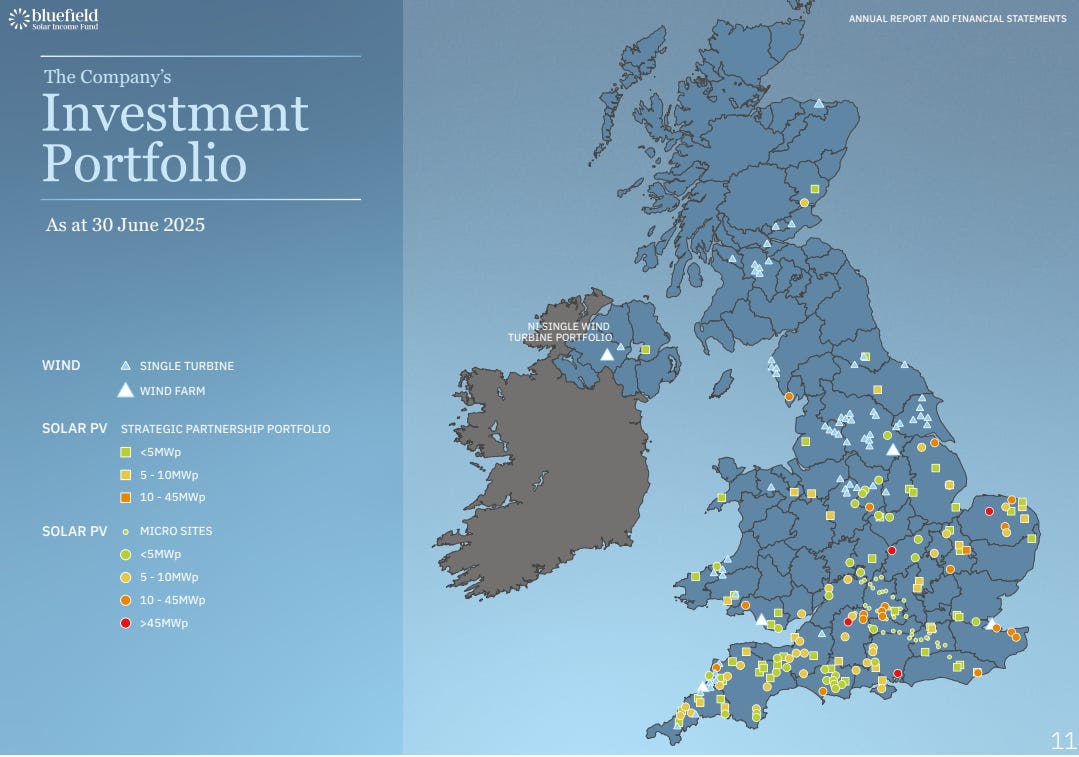

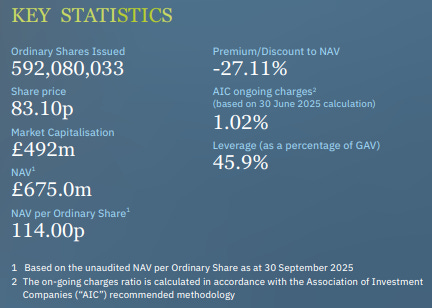

BSIF

Pay £400m to get assets valued at £690.1m (as at 30/06) falling to £675m (as at 30/09) which pays a divi of 13.1% at today’s 68.60p buy. 9p a year. A slippery slope or an opportunity?

These are the assets: All within the UK. Mainly solar with attached BESS, plus some onshore wind assets.

This is the composition of the NAV.

Bluefields (ticker BSIF) investment objective is to provide Shareholders with an attractive return, principally in the form of regular income distributions, by being invested primarily in solar energy assets located in the UK. The Company also invests a minority of its capital into other renewable assets including wind and energy storage.

BSIF is up for sale as a going concern. The sum of its parts exceeds its NAV according to potential buyers. Hmm.

If that’s true then investors soon won’t be Blue.

Today’s potential buyers at 68.6p buy price would be in the green – since that price implies a more than -40% discount, plus a 13.1% dividend yield meanwhile.

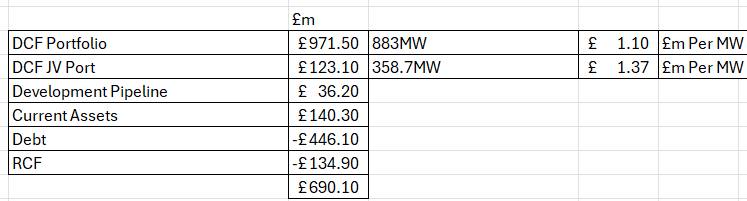

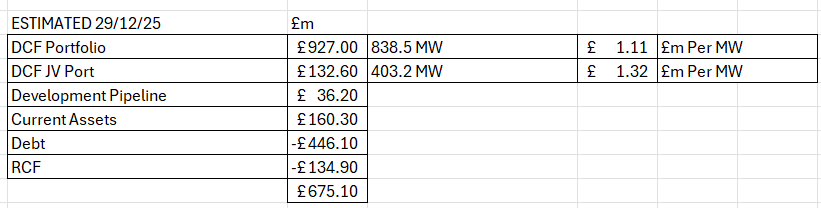

The main portfolio comprised at 30/06 of 883MW of solar and wind assets. These were valued at £1.1m per MW of generating capacity including the attached BESS (there is no separate valuation given to the BESS assets, strangely, only to the generating capacity. This capacity reduced by -44.5MW to 838.5MW in August 2025, as “Phase 3” of its strategic partnership completed, where the assets were sold at NAV to its JV.

Other assets which have no separate valuation value were transferred too. 25MW of BESS and 180MW of development portfolio comprising “four ready to build solar assets” were thrown in too. Three of these have CfD subsidies secured under the AR5 or AR6 schemes.

BSIF then owns 25% of that same JV valued at £123.1m which comprised of 358.7MW of capacity – equating to a valuation of £1.37m per MW. So 403.2MW post period.

So the estimated portfolio looks like this now:

Yes, well, you see the way that BSIF “should” work is capital pours in and develops further assets generating further returns. But guess what?

The capital has dried up.

There is an inability to raise further funds at a discount to NAV, and debt grew expensive (albeit is falling in cost and is starting to look attractive again).

Certainly an outside buyer would be weighing up the numbers and rubbing their chin. Like I am.

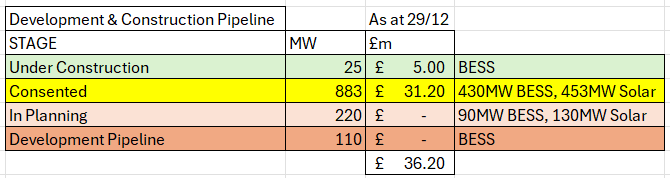

Meanwhile a large pipeline is sat there largely unaddressed. The valuation of this is not in the price. 25MW of pre-construction BESS at £0.2m per MW is 60% below what GSF value theirs for (£0.5m per MW). Or 60% below what Harmony ticker HEIT (a BESS asset IT) sold for in mid 2025.

That alone is £7.5m of potential hidden value.

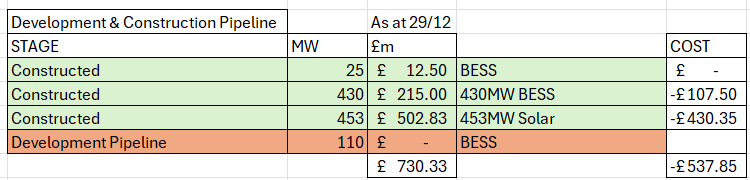

Solar Park construction costs per MW in 2025 range from £0.6m to £0.95m per MW while BESS is around £0.25m per MW (even though the batteries themselves are now £0.1m per MW again as indicated by GSF).

So taking into account the 180MW of consented we have this much remaining.

So if the Consented element were constructed (i.e. assigning zero value to In Planning and Development Pipeline and just considering the “Consented” yellow stuff) what would that mean?

A gain of around £150m. So not worth nothing…. if given away in a 25% JV then the upside is still around £40m…. or double today’s valuation in the NAV (of £36m).

Worth double even if it’s given away to a JV. Think about that.

Of course it’s not this simple, and the connection date matters too. These vary. So this isn’t a slam dunk to riches, but there is value to unlock. However HAVING a scheduled connection is worth a lot. There is a long queue for a newcomer to connect energy assets to the grid. That’s part of the hidden value here.

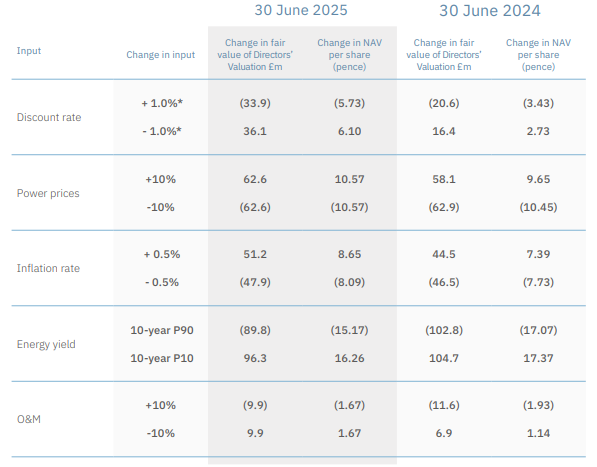

Obviously, the question turns to well, are these assets really worth £1.1m per MW? Or more? They were worth 12% more last year ….. £1.24m per MW at 30/06/24 and a lower revaluation due to power prices were the main reason for the NAV to drop and for BSIF to record a loss in FY25.

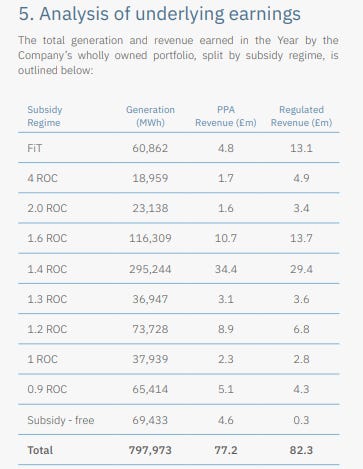

Income Analysis:

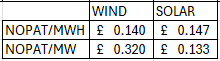

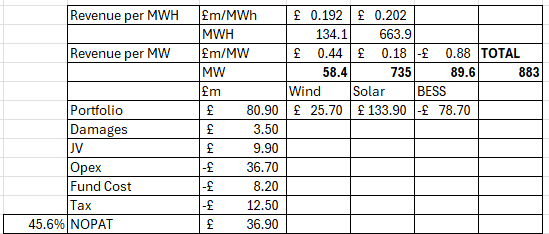

Those assets delivered £161.8m of revenue in FY25, varying between £0.44m per MW for Wind and £0.18m per MW for Solar.

If you consider net operating profit after tax was 72.8% then the assets delivered £0.14m – £0.147m per MWH which is a price divided by pre-interest earnings of 7.5X – 8X.

Now, you’ll notice I’ve gone with NOPAT – net operating profit after tax – but avoided interest costs. That’s deliberate because I wanted to see the earnings relative to the enterprise value and EV/EBITDA is too crude.

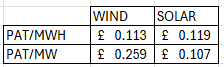

£140,000 per MW is far higher than what the Discounted Cash Flow approach to calculating NAV would imply a 55% upside:

In case you’re curious, the NAV is about 25% higher once you use PAT discounted at 8%.

Of course my calculations assume a flat income based on the prior year numbers. Power Curves and Inflation are increasing and reducing forces.

On one hand, RPI assumed at 3% boosts revenues until 2032. That’s how the subsidy reaches 64% that year. BSIF is a beneficiary to inflation. (Although refer to undermined confidence later)

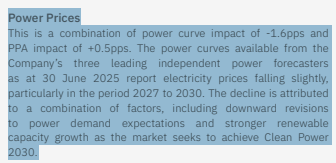

Along with most other electricity generators BSIF is dogged by the 3 leading power forecasters who believe that electricity prices will fall in the period 2025-2030.

Their 2025 forecasts – as usual – have failed, and prices have been rising since early 2025 and stand at £85/MWh as I write vs the £65/MWh they “forecast”.

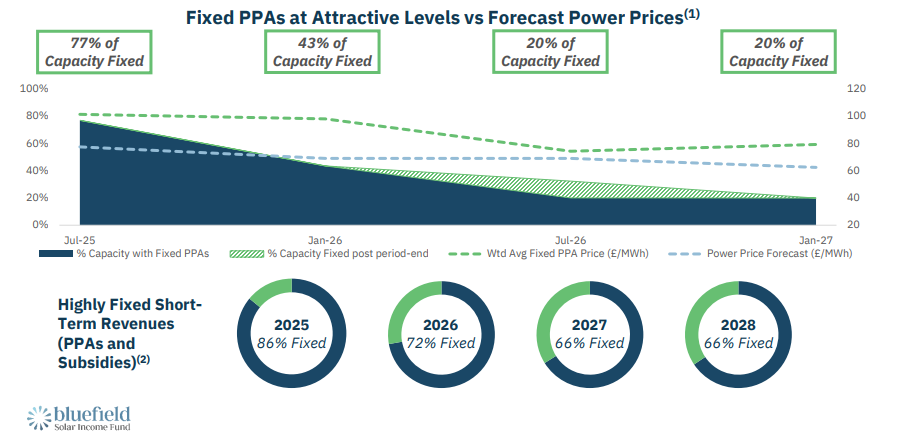

In any case, BSIF lock in 1 year to 3 year PPAs to insulate themselves just in case one day their forecasts end up being in any way accurate.

Now it’s also true that while electricity have NOT dropped, renewable electricty producers’ share prices HAVE fallen including at BSIF. Why? That is due to everyone’s favourite politician, Ed Milli.

The government recently threatened to do the dirty on the renewables sector, altering their contracted income and moving their increases from RPI to CPI. Good old Milli, moving the goalposts just like a tinpot republic would – never too far away from courting disaster.

Since the remaining average life of assets at BSIF is 25.5 years the impact if the simple switch approach is taken would be 2% of NAV while the harsher freeze approach would impact NAV by around 8%.

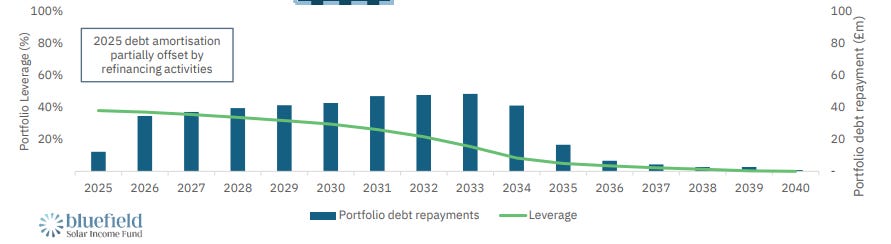

There’s no particular cliff edge to deal with, and the RCF of £135m has a three year life, and costs 1.85%+SOFR (so ~5.1%). The other debt is mainly fixed at 3.95%. Very competitive – and attractive.

The fund can earn leveraged profits on this debt – and does.

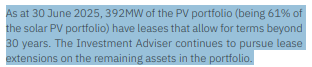

Of course there’s no reason why 30 years is the limit for these assets, and life extensions and upgrades remain possible.

Debt is largely amortising and depreciation is 30 years so as subsidies naturally end at the end of their 15-25 years (the terms differ for each AR/CfD/FiT/RoC scheme) then so do corresponding costs reduce too.

It is also worth contemplating what life under a David Turver inspired government might look like. What if the government completely pulled the plug on subsidies? If Reform came to power that could be a vote winning policy – we’ll slash your bills etc etc – let’s reopen the mines and burn some coal instead.

If that happened, based on the current year accounts, revenue would approximately halve. Obviously the impact fades with each year and the earliest one might think this could happen would be 2029, unless the Labour government collapses.

The fund in FY25 would have earned £37m in FY25 (a 45.6% NOPAT margin) and £15m PAT, and paying over -£54m of dividends would be out of the question. Of course one wonders whether the ensuing chaos of such a policy change would lead to much higher electricity prices, and those prices would insulate a power generator to some extent.

You’d not be able to reopen coal mines and coal power stations quickly and what would energy generators do if the government did this? Stop generating? Or accept new terms.

Of course the other effect would be longer term picture of enjoying inflation-protected subsidy rises would be gone. That’s 50% today but grows to 64% of revenue which is subsidised by 2032 based on the effect of RPI increases (assumed at 3%)

If inflation were higher than 3% in the coming years that would be worth 8.65p per share to BSIF in extra subsidies, and if the 3 leading power forecasters continue to be wrong then the current 15% higher power prices are worth 16p a share more to BSIF.

It remains quite unfashionable to be invested into these companies. There is a chance that the government will follow through on doing its dirty, so there’s a chance this share could fall lower – as harrumphers offload it once the consultation concludes. Although losing 1%-2% NAV when the discount is 40% seems an ok risk.

Equally though, there’s a chance the government would cave in – just like they have with many others. Will a £5 change to people’s energy bill change at a cost of torpedoing a cornerstone policy, be a vote winner? The farmers were celebrating a recent win against inheritance tax I believe, joining all sorts of public sector workers celebrating large pay rises.

You can offer reasons for and against the NAV being a bit more or a bit less than today’s current NAV. You can be like me and be pretty sceptical about the accuracy of power curves, or can be sceptical about government’s willingness to curtail inflation. BSIF would be a beneficiary to either. But if I’m wrong on either or both then it’s already priced in. It’s a one-way bet with no stake.

What I cannot see however is how BSIF would sell for below 40% less than its NAV i.e. to actually lose money in the event of a sale. Much like HEIT was like this.

Is the sale guaranteed? No. But if it didn’t happen even for a few years just relax and earn a covered 13% yield – well that’s a hardship isn’t it?

Regards

The Oak Bloke

Disclaimers:

This is not advice – you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

JD Henning

Investing Group Leader

“Timing, perseverance, and 10 years of trying will eventually make you look like an overnight success.” ― Biz Stone, co-founder of Twitter.

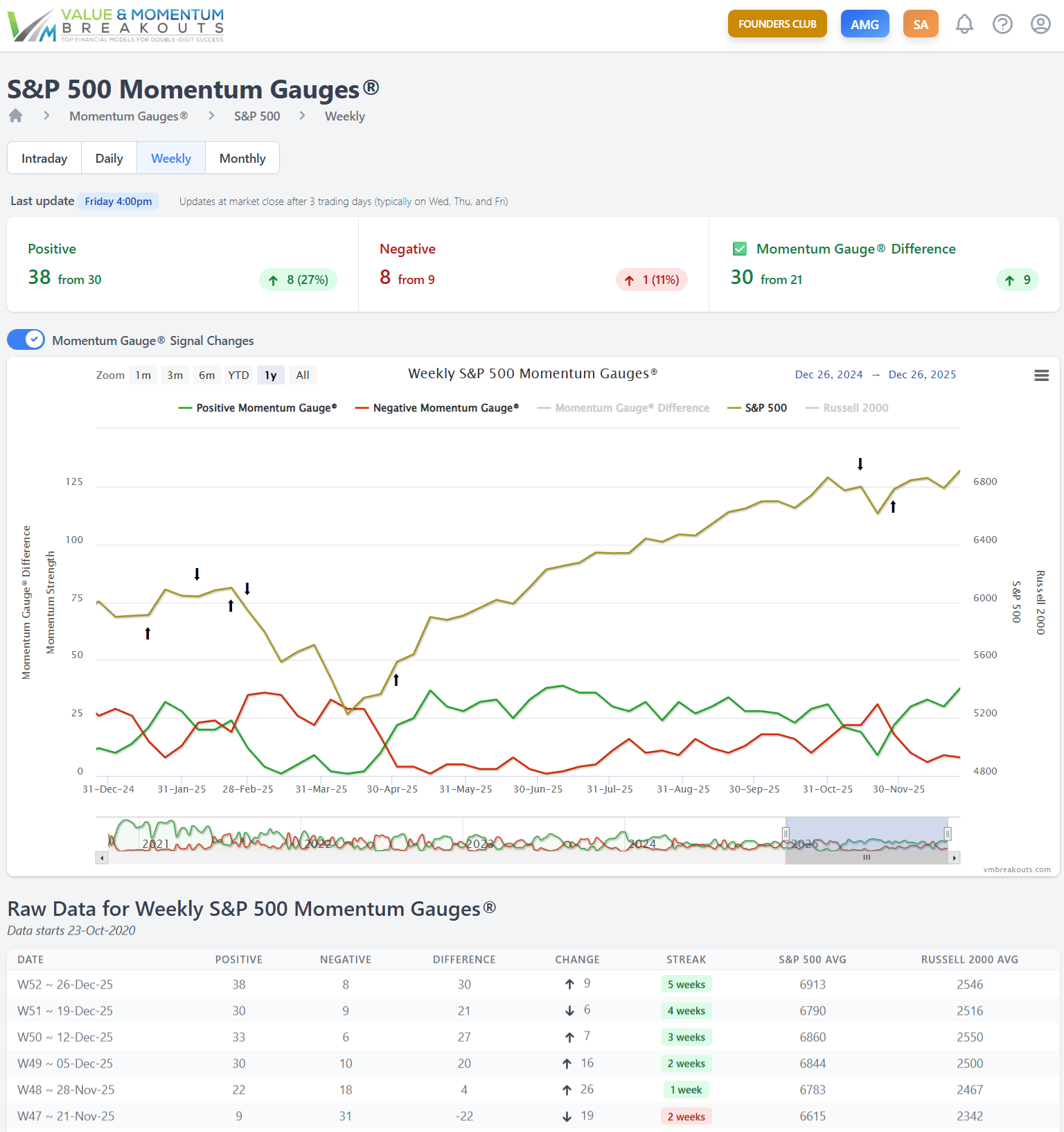

Timing matters, and it matters greatly. I have spent the last 35 years trading, researching, and constructing algorithms to identify and leverage the value across fundamental, technical, and behavioral finance models. Of the ten portfolio models designed for optimal portfolio mixes for members to beat the market at Value & Momentum Breakouts, eight come from enhancing well-tested anomaly research in published financial journals. All of the models continue to outperform the S&P 500 in live forward testing here on Seeking Alpha, and again this year.

This article builds on my prior 2026 outlook articles with a more focused look at one of our top models from published financial literature that I have found to consistently outperform in good and bad seasons.

I am a strong advocate for leveraging the strengths of different fields of financial analysis, from fundamental to technical to a wide variety of behavioral variables. These approaches each can deliver successful model portfolios, as documented through our live trading on Seeking Alpha the last 9 years.

The thing to consider is that we rarely ever see market leaders from the prior year be market leaders for the coming year. ~ JD Henning, January Podcast

Somewhere over the past decades of trading and researching the markets, I discarded the notion of being a pure buy-and-hold investor. People may do well in buy-and-hold approaches, but they invariably have to ride through some major downturns to arrive with good results in the end. Back in the days when I relied on well-known investment firms for advice, I often received more coaching about my patience than any valuable insight about market behavior. Like many of you, my cynicism and curiosity about the financial markets led me to test, experiment, and run studies across thousands of different trading approaches, algorithms, and models. The long-term development of my momentum gauge algorithms for market and sector trading signals is one of the key reasons I am no longer a “buy/hold and hope for the best” investor.

Here’s a 10-minute view of some key factors to consider for next year. Focus is on leveraging our value portfolio from a wide variety of top-performing models available in our Seeking Alpha Investment Group.

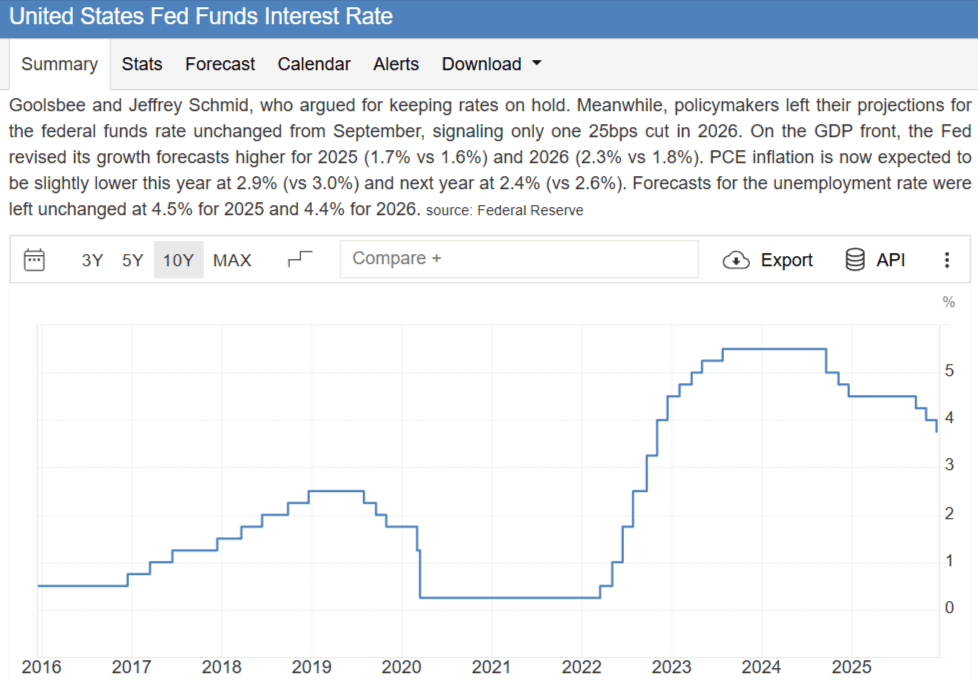

One of the most important factors for market direction is the monetary policy of the Federal Reserve. No forecast of a coming year is complete without consideration of both the fiscal and monetary goals of the key policy drivers. We already know that the Trump administration intends to significantly lower taxes across the board in a loosening of fiscal tax policies. Historically, lower taxes increase the savings rate and are stimulative for markets. We know that major deregulation across U.S. industries has already begun even as tariffs increase to the highest levels in many years.

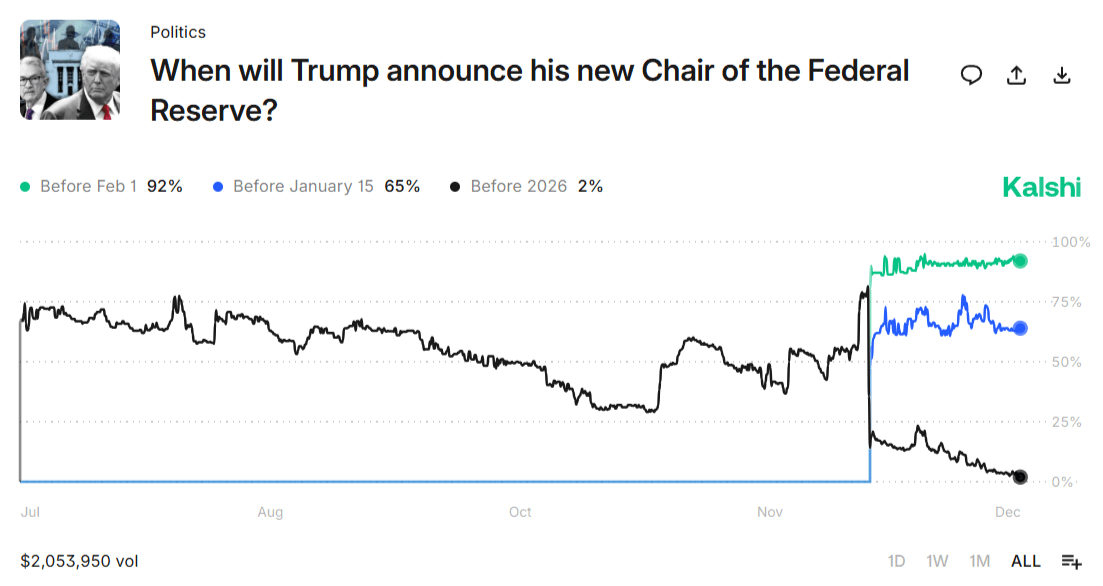

What is new for 2026 is a heightened emphasis on changing the monetary policies of the Federal Reserve and even replacing Fed Chairman Jerome Powell. The betting markets see a 92% probability that Trump will announce his new Fed chairman before February 1st.

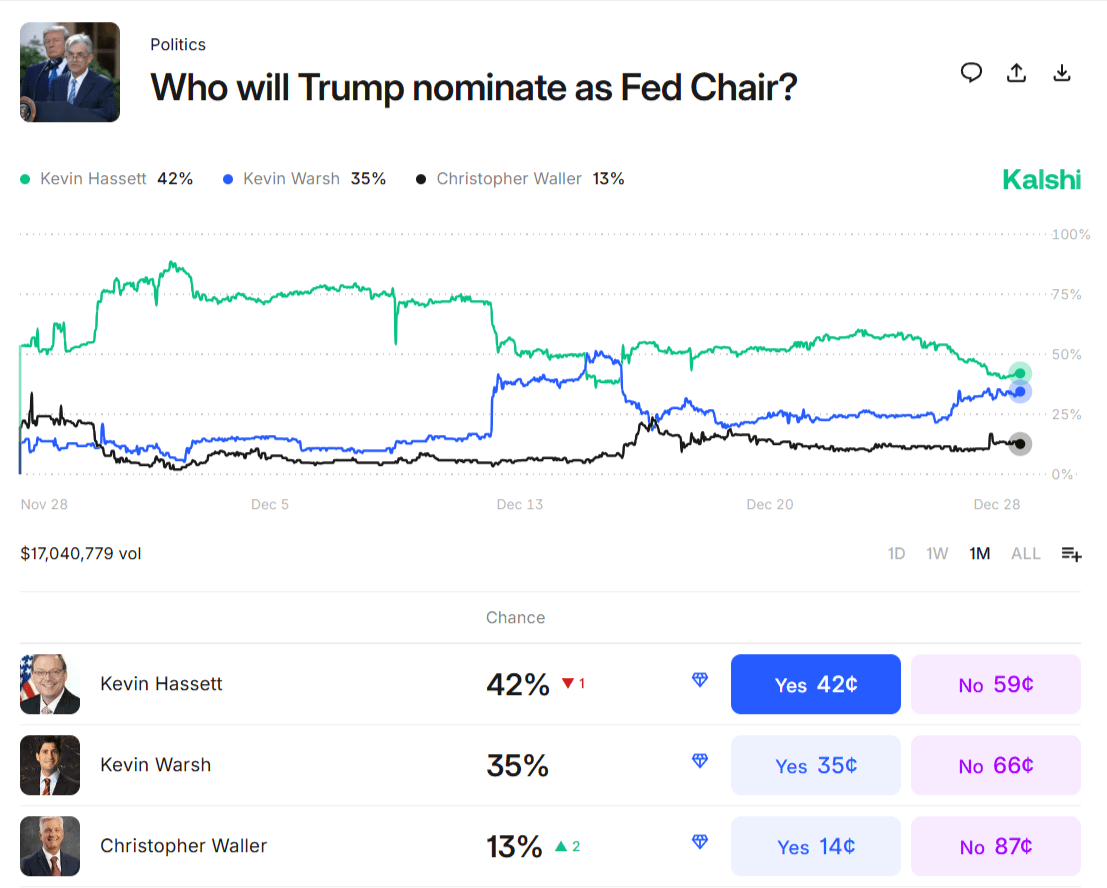

Chairman Powell’s term ends in May, and speculators currently see the most likely replacement is one of two Kevins. Odds place it at 77% that the new Fed Chair will be either Kevin Hassett or Kevin Warsh, with a 92% probability that we will know before February 1st.

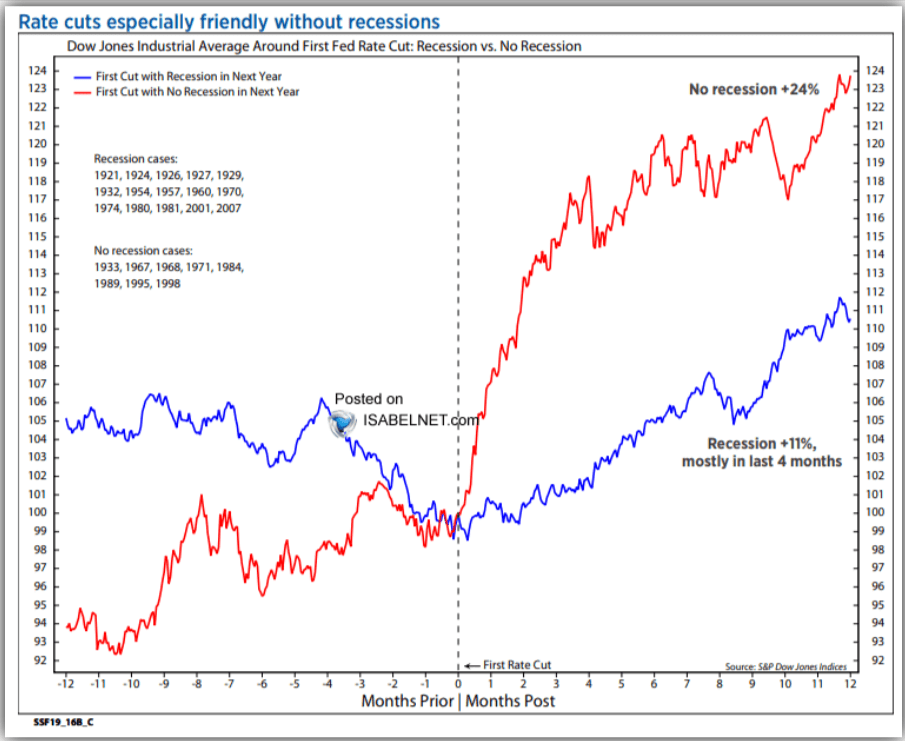

Regardless of which Kevin may be appointed Chairman, we know from Trump’s August appointment of Federal Reserve board member Stephen Miran that the new leadership will be enthusiastically for lower rates. Stephen Miran was the only board member voting for the largest -50 bps rate cut in the latest committee decision. Measurements from 1921 show that lower Fed fund rates are extremely bullish for markets, and the DJIA in particular, when there is no impending recession. The most recent GDP numbers of +4.3% in Q3 2025 certainly support a robust current economic condition far from a recession.

So the Fed fund rate chart above suggests we could experience a very positive DJIA average growth rate for the 12 months from the first rate cut. It may also be that the relatively slow rate of cuts from the highest Fed funds rates in 22 years has not had a meaningful impact yet on the DJIA pattern and a broad market boost beyond the biggest growth stocks.

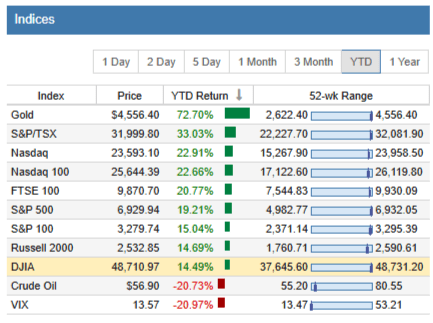

We can see for the past year that the Dow Industrials lagged all the other major indices during the first few rate cuts of 2025. Growth stocks have done very well in the past year, while value stocks and small caps have lagged the strong growth moves. This suggests that the impact of the rate cut pattern may still be well within the average 12-month growth window, with more gains to come.

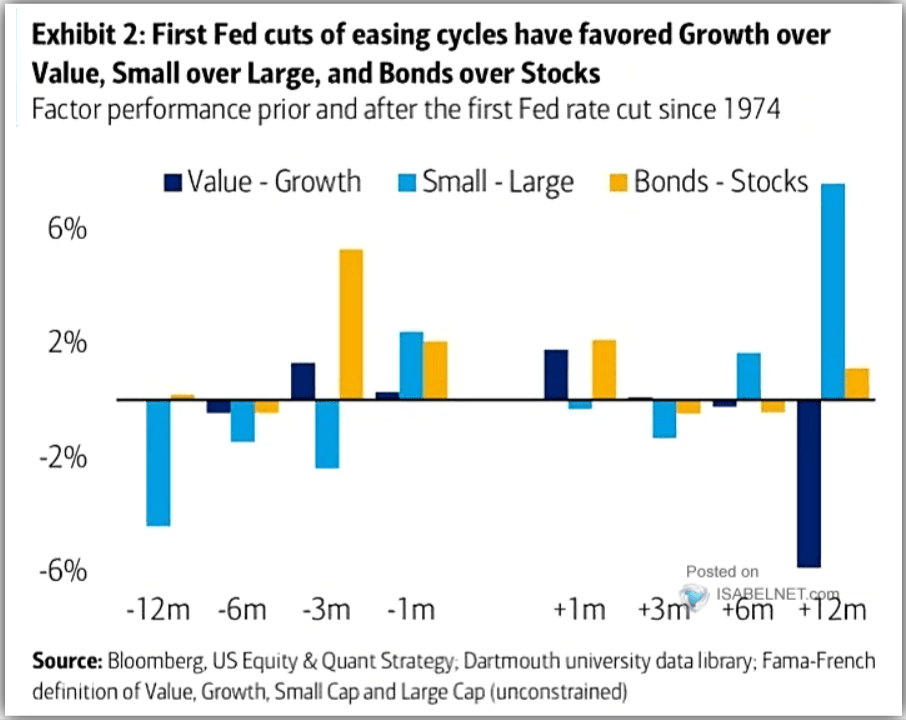

The reaction we have seen to the first few cuts of the Fed easing cycle is fully consistent with historical patterns documented from 1974. Growth typically beats value through the first few rate cuts — that we have seen. Small caps typically beat large caps, which we have not yet seen. Bonds lead stocks, which we have definitely not witnessed yet.

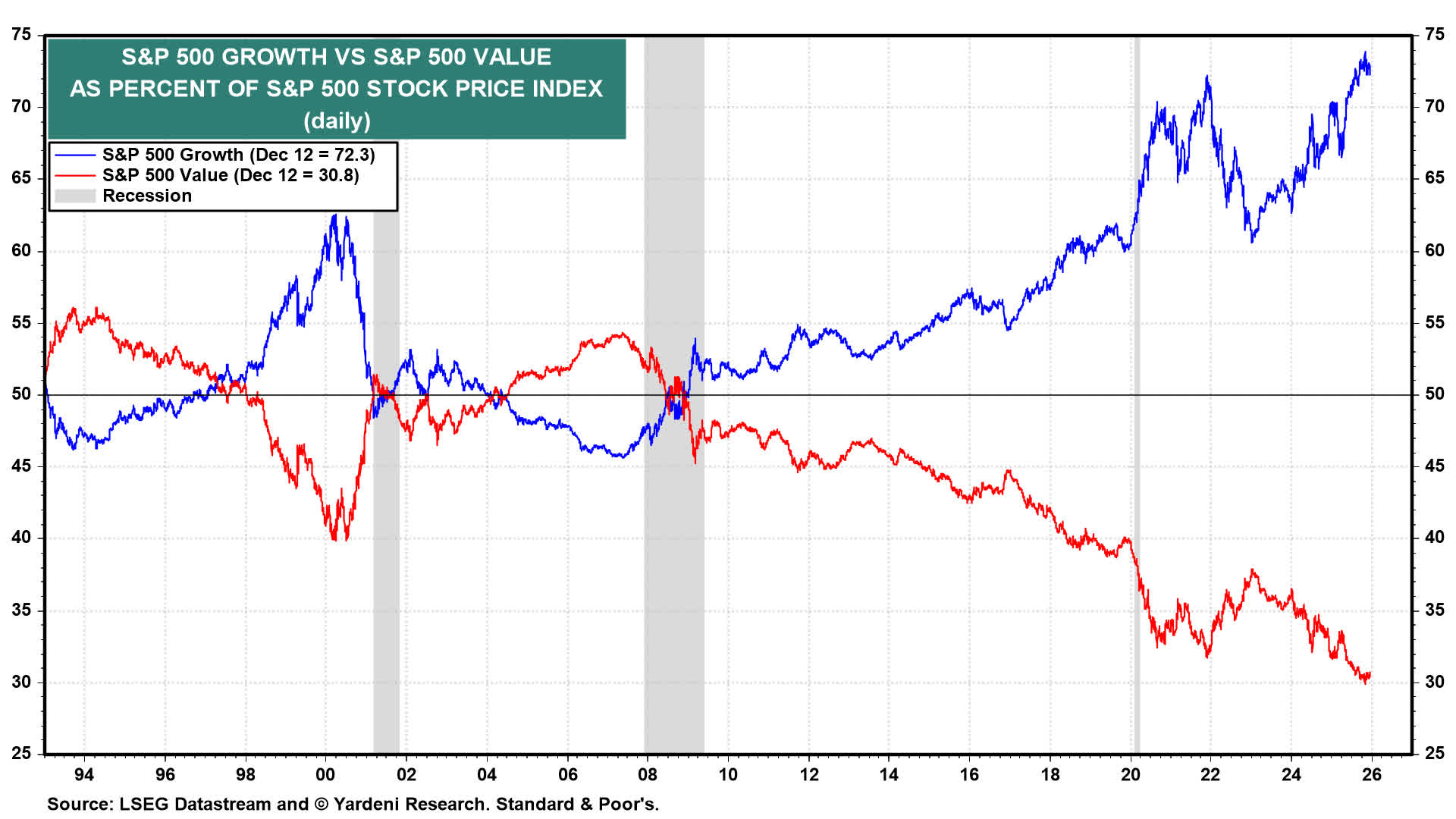

Based on these easing cycles and the current market indices, it seems probable that more value stocks are due for a recovery soon. Certainly more declines in rates may create the expected effects more clearly. I discuss this further in my recent article about market bubbles linked above. Further, the Fed has just shifted from a quantitative tightening program in the fight against inflation to an “unofficial” easing program that started December 1st.

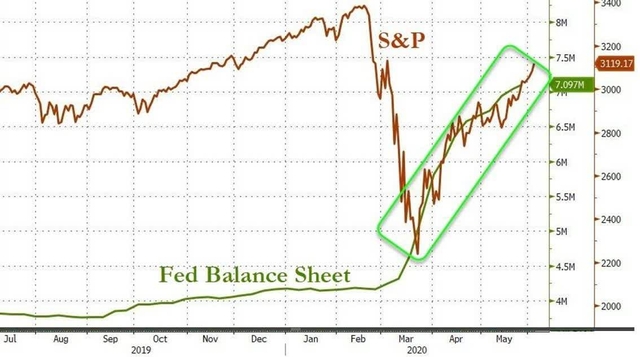

What is the significance of tightening and easing the Fed balance sheet? Since the Global Financial Crisis, we have seen the Fed use quantitative easing to flood the market with liquidity and improve market conditions. The largest and most recent use of quantitative easing was back during the major Covid correction. The S&P 500 lost over -35% from its highs in February, and the Fed stepped in with a major easing program in March of 2020, shown on the chart below.

Fed Balance Sheet vs. S&P 500 during 2020 Covid correction

The context of that incredible QE intervention that rescued markets is also shown in 2020 on the Federal Reserve balance sheet chart below. The correlation between market performance and the Fed balance sheet is remarkably strong, but not the only factor of fund flows that benefit equities.

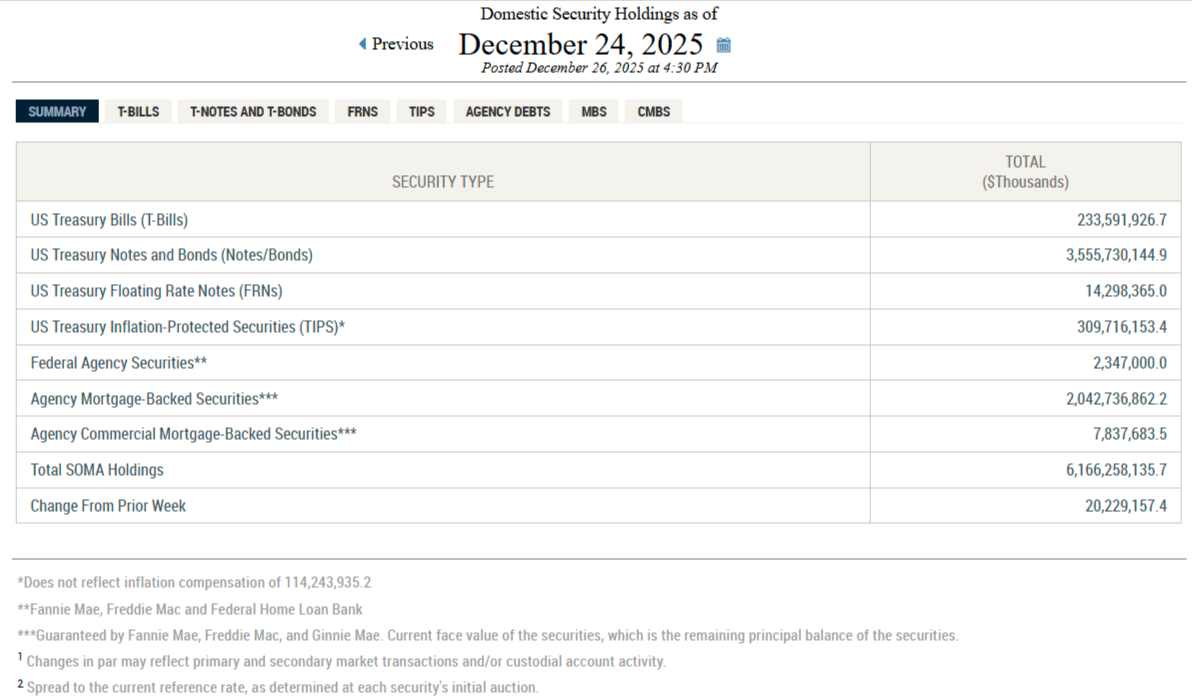

The most important takeaways, without getting into more details about the composition and impact of the Fed’s domestic security holdings, are two-fold:

1. A change in the direction of the Fed balance sheet to more easing is more bullish for markets. The recent Fed promises of up to $40 billion per month added to the balance sheet into 2026 have already begun, as the December SOMA reports show. Last week saw an increase in the Fed’s domestic holdings of $20.2 billion and $14.7 billion in the prior week.

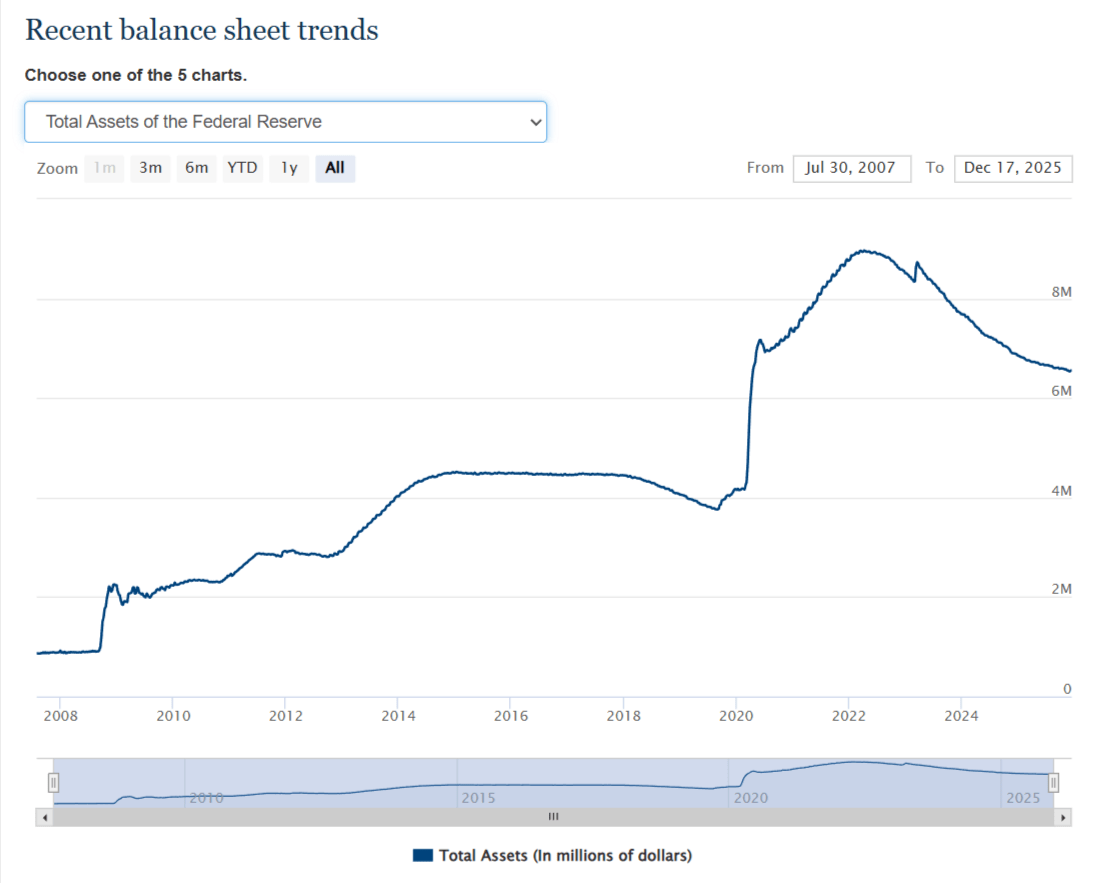

2. The magnitude of the Fed assets on their balance sheet is also of critical importance for overall liquidity. Fed assets peaked at $8.965 trillion in 2022 and have been rolling off steadily to the recent lows of $6.131 trillion this past November, when the tightening ended on December 1st. We can see from the Fed balance sheet chart that these levels rising back up to total SOMA holdings of $6.166 trillion near the end of December are still far above the pre-Covid levels used to stabilize markets through 2018 after the Global Financial Crisis. Many of my prior QE/QT articles suggest that there may be a threshold at which market liquidity gets low enough to shock markets like we saw in 2018.

Both the 2018 QT shock and the 2020 Covid correction were significant negative signals on the Momentum Gauges. I believe that as long as the Fed balance sheet does not dip to 2018 levels, we are less likely to see a severe market liquidity reaction.

So in closing this economic-chartfest section of my article, I am led to believe some notable market shifts are coming that will benefit the broader market and value stocks in particular. These charts illustrate to me the potential for much looser monetary policy, not to mention more fiscal “stimulus” programs and deregulation embedded in the “Big Beautiful Bill” set for action starting in January.

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑