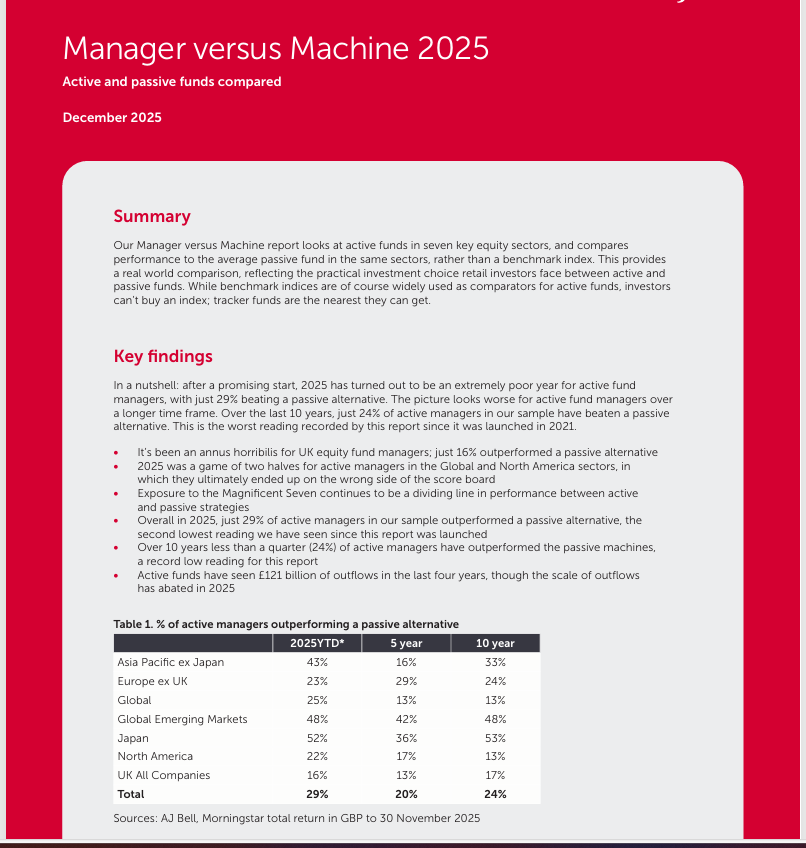

Market snapshot: time is running out as AI stocks struggle

With little more than a week to go before the big day, Wall Street is showing little sign of festive cheer. It’s not much better here. ii’s head of markets explains why.

16th December 2025 08:21

by Richard Hunter from interactive investor

Time is running out for any hopes of a Santa rally, as investors continue to fret about the AI trade, which for the moment has fallen sharply out of fashion.

The rotation into what are seen as relatively stable sectors compared to the previous AI euphoria rumbles on, to the benefit of the likes of industrials, consumer discretionary and healthcare.

Meanwhile, Oracle Corp ORCL

and Broadcom Inc AVGO

continue to be at the eye of the AI storm, falling further with losses of 2% and 5% respectively and, while poster-child NVIDIA Corp NVDA0 managed a small gain, Microsoft Corp MSFT also drifted.

It remains to be seen whether the imminent slew of economic data will be too stale to be meaningful. A combined October/November non-farm payrolls is expected to show an increase of 50,000 jobs, which would compare to 119,000 in September, although the quality of the data could be called into question given the effects of the government shutdown.

Retail sales are also expected, again possibly too historic to be of use given that they will relate to October, although overall the numbers could at least provide some further clues as to the Federal Reserve’s thinking for next year. There is currently a disconnect between market expectations of two cuts and the Fed’s current dot plot, which suggests a solitary reduction.

In the meantime, with no obvious positive catalysts on the immediate horizon, the main indices are in consolidation mode. In the year to date, gains of 13.8%, 15.9% and 19.4% for the Dow Jones, S&P500 and Nasdaq respectively reflect what has become a positive year despite the ever-present headwinds which have variously threatened to upset the investment applecart.

Asian markets also failed to enter into any kind of festive cheer, with technology stocks under pressure given the Wall Street read across. Domestic issues also remained in focus, with the Nikkei 225 declining as preliminary factory data pointed to a slight slowdown, while private sector growth cooled as services declined in Japan. The data comes ahead of a widely expected rate hike from the Bank of Japan at the end of the week, which could further dampen sentiment.

China echoed a subdued economic theme, with retail sales growing by just 1.3% year on year in what was the weakest reading since during the pandemic, while investment and lending numbers were also tepid, inevitably leading for calls of further stimulus from the authorities to revive growth meaningfully.

Domestic issues were also in focus in the UK, where a rise in unemployment to 5.1% in the three months to October should be the final piece of the jigsaw in ensuring that the Bank of England cuts interest rates on Thursday. The reluctance of businesses to invest, hire and plan for the immediate future was already evident leading up to the Budget, let alone in the aftermath, with a moribund economy now patently in need of some immediate stimulus.

The FTSE250 drifted lower at the open, but has still managed a gain of 6.7% so far this year. The FTSE100 was also bereft of any sustainable positive momentum after a stronger showing in the previous session.

The ongoing US tech weakness weighed on the likes of Polar Capital Technology Ord PCT

while a dip in the gold price led to rare losses for the likes of Endeavour Mining EDV2 and Fresnillo FRES. The premier index is also consolidating its strong gain of 19.2% so far this year, with a large exposure to the likes of the banks, miners and defence sectors having been major tailwinds.