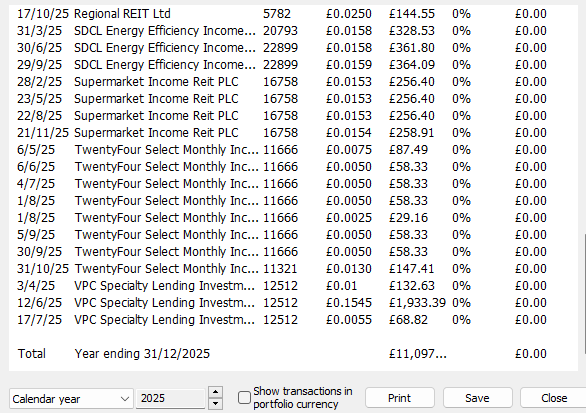

The Snowball has beaten the 2025 fcast and target, so it’s now history.

The Snowball, on all the known unknowns should at least better the year one 2026 target of 10k, especially as there is already a buffer built in for January.

Remember the Snowball doesn’t add any capital, so if you can add to your Snowball, even modestly you should be able to improve the yield in the table above, especially thanks to Mr. Market you can currently re-invest all dividends at above 7%, or pair trade with a blended yield of 7%.

Pair trading is best if you are not near to you retirement date as you have time to correct any unfavourable trading choices.

Also if you can only add a modest amount, compound interest takes several years before the big money is made, which should encourage you to start saving. Can you cut one coffee a day and save the cash ?

Your Snowball should be different from the blog Snowball as it should reflect on your risk profile, which depends mainly on how many years it is before you want to spend your hard earned. Join us on the journey, where there are bound to be many twists and turns as we journey thru the year.

Dividends can be more reliable than share prices as they’re driven by the companies performance itself and not by the whim of investors.

As part of a total return / reinvestment strategy, this income could be reinvested into income assets or back into the equity market depending on the relative valuations.

The emotional benefits of dividend re-investment. In fact, with this investment strategy you can actually welcome falling share prices.

But experts claim there are still reasons to back real estate, especially with the prospect of interest rate cuts in the coming weeks.

Big themes for investors include the return-to-the-office and the rise of online shopping.

Daniel Austin, chief executive and co-founder at specialist property lender ASK Partners, said: “The 2025 Autumn Budget offered limited stimulus for the housing market and, persistent headwinds such as sticky inflation, higher for longer interest rates, elevated construction costs, and slow planning processes continue to impact development viability.

“But there are still reasons for cautious optimism. The UK economy is forecast to grow by 1.4% this year. This is expected to outperform the eurozone and should support investor confidence.

“The UK also remains an attractive destination for global capital, with ongoing interest from the Gulf, Southeast Asia and deepening UK United States investment links, particularly through the technology sector.”

Here are the emerging trends in real estate for 2026 and how to invest in them.

Prime offices

Many companies are reducing remote working and getting staff to be in the office more frequently.

Austin suggests businesses are competing for modern, energy efficient and amenity rich workplaces that support hybrid working.

He said: “Best-in-class offices in central London continue to achieve strong rents and stable yields.”

The rise of build-to-rent

The UK housing market continues to be hit by a lack of supply.

The government is pushing planning reforms through parliament to boost development but there are also fears that landlords could exit the market due to new rental regulations and higher taxes.

Build-to-rent – developments typically run by large institutional landlords – may fill that gap, providing an opportunity for investors. You may already have some exposure to this through your pension.

Austin said: “With so many smaller landlords exiting the sector due to increased costs and regulatory complexity, professionally managed rental formats are becoming more important. Build-to-rent and co-living are particularly well positioned to serve younger, mobile workers who seek affordability, connectivity and community. Mid-market suburban and commuter belt schemes may outperform prime central locations, especially in areas benefiting from new infrastructure such as the Lower Thames Crossing.”

Storage and logistics

Demand for storage and logistics is being driven by the growth of online retail as well as the growing adoption of artificial intelligence, cloud services and high-performance computing.

This means there is more demand for industrial sites to store goods for online deliveries and also hard drives to power cloud software.

Austin said: “Growing adoption of artificial intelligence, cloud services and high-performance computing is placing unprecedented pressure on power capacity and suitable land, making data centres an increasingly strategic real estate category.

“The combination of long-term contracted income, critical infrastructure status and limited supply of appropriate sites means this segment is likely to remain strong. Mixed-use industrial schemes that accommodate logistics, data infrastructure and urban services will offer particularly attractive, income-led opportunities in 2026.”

Hotels and hospitality

The transformation of under-utilised office buildings into hotels are creating new avenues for investors, according to Austin.

He said: “The asset class continues to appeal to private investors and family offices seeking income diversification and long-term value.”

Income producing operational real estate

Operational real estate, including healthcare, specialist care, education and supported living can provide stable and inflation-linked income streams.

Austin said: “Demographic shifts, including an ageing population and rising demand for specialist services, support the long-term resilience of these sectors.”

How to invest in real estate

Unless you are a property developer or landlord who can afford to build or manage one of these assets, one of the most common ways to gain exposure to real estate assets is through real estate investment trusts (REITS) or property funds.

Oli Creasey, head of property research at Quilter Cheviot, said: “The REITs own a portfolio of properties worth a certain value, and shares in the companies are traded on stock exchanges throughout the day.”

Most specialise in a particular sub-sector.

Creasey highlights Derwent London and GPE for development and ownership of London offices, while Big Yellow and Safestore are self-storage specialists.

Investors can get access to health care developments through Primary Health Properties and Target Healthcare, which owns senior living centres.

Meanwhile, Unite Group backs student accommodation, while Grainger does general residential rental.

For buyers not looking to specialise, Creasey says there are several funds that buy REITs but use them to create a more diverse portfolio including Columbia Threadneedle;s Property Growth and Income as well as TIME’s Property Long Income and Growth funds.

There are also funds that create a diverse portfolio around a thematic approach such as Schroder’s Global Cities fund which invests in REITs worldwide that own assets located in the top cities globally, while Gravis’s Digital Infrastructure fund invests in REITs that are aligned with the ongoing technology revolution.

Ben Yearsley, director of Fairview Investing, suggests a broad based fund or trust that then leaves the sector and stock decisions to the fund manager is better than trying to gain direct exposure.

His favoured option is the TR Property investment trust managed by Marcus Phayre-Mudge.

Yearsley said: “It has a mix of UK and European property shares.

“Valuations are cheap and no one is interested on the sector. In addition with no speculative development in the past decade there are shortages of good quality property in many areas.”

For a sustainable option, Daniel Bland, head of sustainable investment management at EQ Investors, suggests the Schroder BSC Social Impact Trust, which backs social housing.

Investors Hate This Market (and They’re Dumping This Great 9% Payer)

by Michael Foster, Investment Strategist

Today we’re going to talk about a subject that might seem a little outside the dividend plays we normally discuss.

But as you’ll see, this topic – a big shift in how Americans feel – is the main reason why some of our favorite high-yielding closed-end funds (CEFs) are woefully underpriced, like one equity-focused 9%-yielder with an incredible track record.

Let’s start with that unlikely topic: Happiness. It matters because, as we’ll see, how happy Americans are ties directly into investing behavior in very predictable ways.

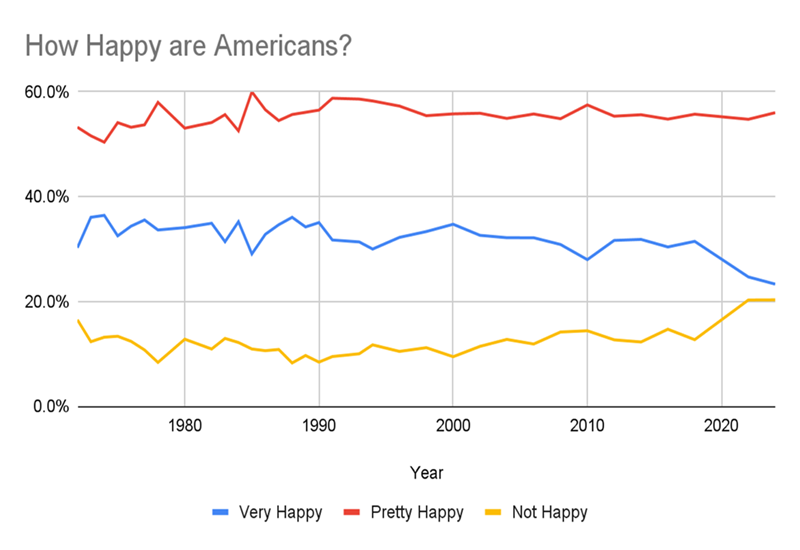

Source: CEF Insider This chart shows the results of the General Social Survey, from the University of Chicago’s National Opinion Research Center. It’s one of the oldest studies of Americans’ views on different social, political and cultural issues.

When asked “How happy are you?” the majority feel pretty happy. That’s been true since the survey started asking this question in 1972.

But look at the yellow line, showing how many Americans are not happy. It reached a new high in 2022 and is stuck there. Similarly, the percentage who are “very happy” has fallen to a new low and is trending further down.

If these trends continue, the percentage who say they’re unhappy will climb above those who are very happy for the first time in history. That’s a big psychological shift, and markets haven’t caught on to it yet.

Consumers Get the Blues

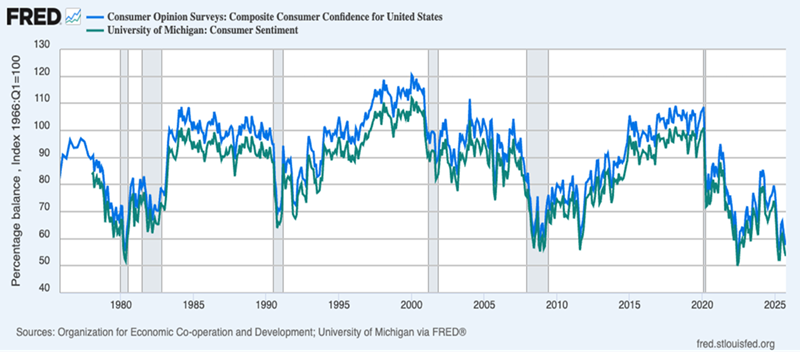

Now let’s get into why this trend is a financial risk. This chart is our first stop.

Here we have two measures of consumer confidence, one from the University of Michigan (in green) and one from the OECD (in blue). As you can see, these tend to drop during recessions (the gray sections above) and rise after, which makes sense.

There are exceptions, like in 1992 and in 2011, when consumer confidence cratered following the recessions that preceded them. Back then, consumers clearly worried that recent bad times would return.

But we’re now five years out from the last recession, and consumer confidence is stuck below where it was even during the pandemic! In other words, people feel worse about the economy now than they did when they were literally in quarantine.

That’s strange, and it demands a closer look because, at least economically, it makes no sense. Unemployment is much lower than it was during the pandemic and remains historically low. Incomes and wealth are rising, breaking trends that lasted two generations, as we’ve recently discussed.

So we’re left with one conclusion: People are just more miserable than they used to be, and it’s causing them to respond more negatively to surveys than they used to.

This makes sense, since the pandemic’s aftermath sent inflation soaring and AI has boosted worries about many things, including job loss.

The Data Has Changed. Wall Street Hasn’t

This all matters because people who make major economic decisions rely on data like this. I know because I spent over a decade consulting with hedge funds and investment banks on how to create just these sorts of studies.

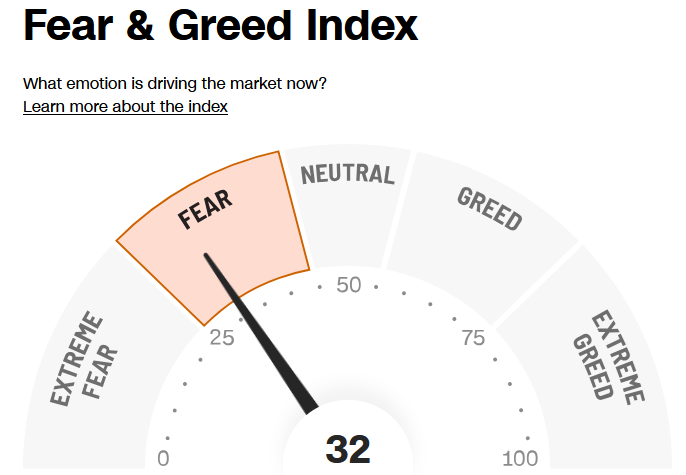

This ties into our income (and portfolio value) in two ways. First, a lot of survey-driven research is less reliable than it used to be – including the oft-cited CNN Fear & Greed Index.

Source: CNN.com For a while now, it’s been saying that investors are fearful. But if so, why have stocks climbed to near all-time highs? This index clearly needs adjusting, because what counts as “fear” is now a lower number than it used to be.

As a result of this shift, negative attitudes are no longer useful indicators of when a selloff will start.

Of course, this also means that when the market sells off because everyone’s worried that attitudes are souring, we contrarians get a chance to profit. Consider how the market tanked in 2022 because most investors expected a recession, but then no recession came. Or how tariff worries sent markets into freefall in April, but nothing major has happened since.

Selling because the market is getting fearful doesn’t work anymore, but buying when the market has whipped itself into a frenzy does.

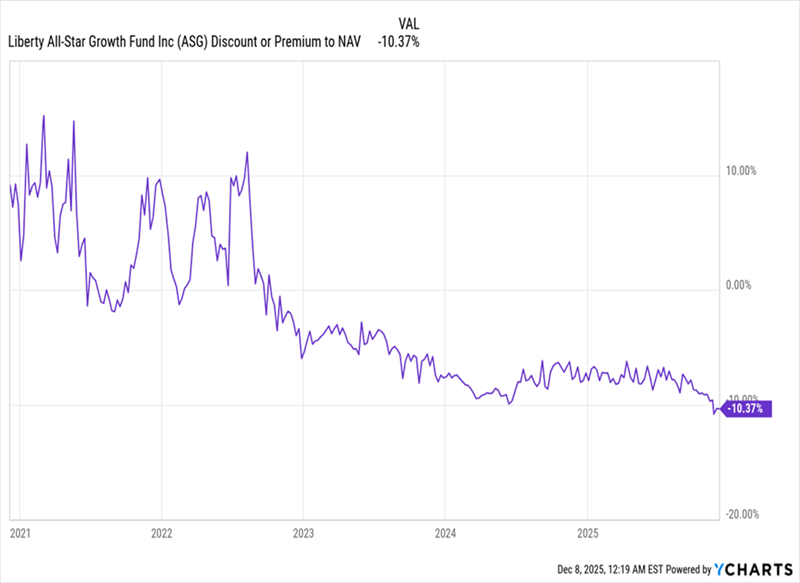

ASG: The Poster Child for Our New Pessimistic Era We see this playing out with CEFs, where discounts to net asset value (NAV) are deeper because risk-averse investors, who tend to be most interested in CEFs, pull back when sentiment sours. A broad drop in happiness, then, can make them more cautious, sending CEF discounts to deeper levels than the fundamentals justify.

As a result, the Liberty All-Star Growth Fund (ASG) has seen its discount drop below 10% in 2025, far below the last decade’s average of a 2.2% discount. That’s despite the fact that ASG has earned a 10.2% annualized return in that time and yields 9% today.

It’s a CEF Insider holding I talk about a lot because, despite the “growth” in its name, it pays us that 9% dividend (which does move around a bit, as it’s tied to the fund’s NAV). ASG also holds a nice mix of large- and mid-cap stocks. Top holdings range from Apple (AAPL) to New York State retailer Ollie’s Bargain Outlet Holdings (OLLI).

Eventually, history suggests that CEF investors will realize we live in a new era where sentiment is lower than it used to be, simply because these are more pessimistic times.

At that point, they’ll likely see that these discounts have gotten too wide and bid them up. If we buy ASG today, we’d be nicely positioned to beat them to the punch – and collect that rich dividend while we wait for this to happen.

GCP says ‘now attractive time to invest’ as net asset value picks up

Thursday, December 11, 2025

GCP Infrastructure Investments Ltd on Thursday announced an unchanged annual dividend as it posted a higher net asset value total return, with material policy support for infrastructure meaning that ‘now is an attractive time to invest.’

The firm is advised by Gravis Capital Management Ltd, the closed-ended investment company aiming to pay dividends and preserve capital from exposure to UK infrastructure debt and similar assets.

GCP said net asset value per share as at September 30 fell 3.6% to 101.40 pence from 105.22p a year prior.

NAV total return for the financial year ended September 30 was 3.1%, higher than 2.2% in financial 2024.

The company said: ‘The main factors driving asset valuations during the year included project specific factors, renewables generation and changes to discount rates applied by the company’s independent valuation agent.’

The dividend for financial 2025 was 7.0p, unchanged from a year ago.

Looking ahead, GCP said: ‘The recent UK autumn budget is unlikely to have a material impact on the company. Investors remain concerned by the UK’s long-term prospects and have generally been reducing allocations to long-duration UK exposure, which has impacted demand for the company’s shares.

‘The combination of interest rates and material policy support for infrastructure means now is an attractive time to invest, whilst maintaining an awareness of the political risks. The opportunity to lock-in attractive risk adjusted returns given the interest rate backdrop and invest early in some of the new sectors the UK government is supporting is something the company has done successfully during its 15 year life.’

GCP shares were 0.6% higher at 71.09 pence each on Thursday morning in London.

Copyright 2025 Alliance News Ltd. All Rights Reserved.

Source:

Source:

Source:

Source: