Greencoat UK Wind UKW

UKW shares hit by ROC consultation, but fundamentals remain undimmed.

William Heathcoat Amory

Updated 07 Nov 2025

Disclaimer

Disclosure – Non-Independent Marketing Communication

This is a non-independent marketing communication commissioned by Greencoat UK Wind (UKW). The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

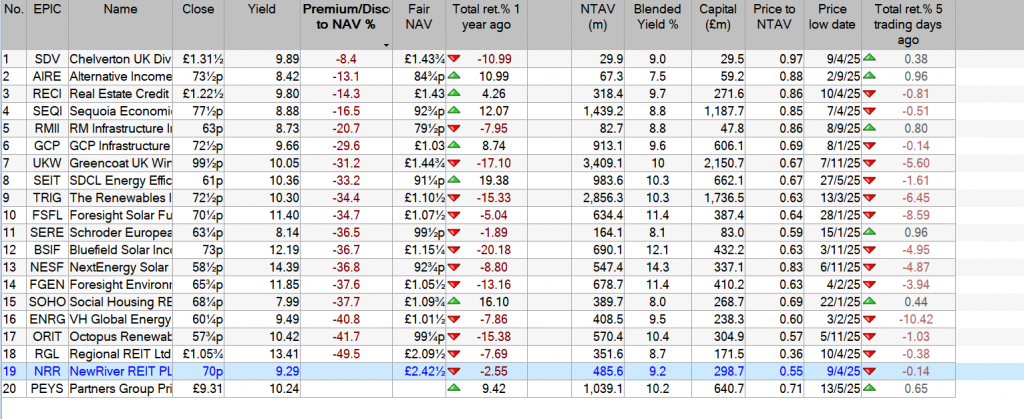

The Department for Energy Security and Net Zero has launched a consultation on proposed changes to the inflation indexation used in the Renewable Obligation (RO) and Feed-in Tariff (FiT) schemes. Some trusts have provided guidance on the potential impact on NAVs, but this has hit share prices across the renewables sector. Discounts to NAV have widened.

In summary the consultation suggests two options:

- Option 1: from March 2026, move ROC indexation from RPI to CPI (this is in effect an immediate move since the next indexation date is March 2026), or

- Option 2: freeze the current ROC level and create a “shadow” ROC price assuming ROCs had always been inflated by CPI since 2002. No further inflation-linked increase would take place until this “shadow” CPI price catches up with today’s level (assumed to happen around 2034/35, so effectively the current price is frozen until then). Thereafter, CPI would apply.

It is important to realise that this is only a consultation, and not necessarily an inevitable change. This is not the first time that a consultation on this has been initiated, with a previous consultation in 2023 focusing on a potential migration of ROCs to a fixed price certificate, which included consultation on ROC indexation. The net result of this previous consultation was that no amendments were made to indexation (or anything else).

It is fair to say that the UKW and the wider industry will be engaging in the consultation, and the UK government will be very aware of the potential impact of any changes on future investment in renewable energy development. With the results of the AR7 auction round due to be announced over the next months, we imagine the government will not want to dent the enthusiasm of developers, given this is a key step towards the UK’s net zero transition.

Kepler View

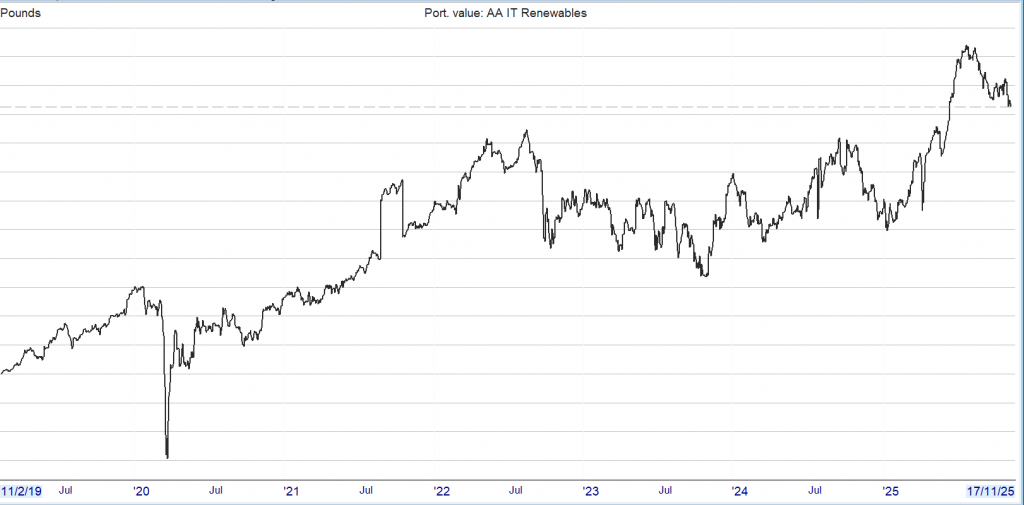

Whilst this recent news has added to the already challenging backdrop for Greencoat UK Wind (UKW), the share price move seems extreme, such that the worst outcomes would appear to be more than accounted for by the current share price discount to NAV. In fact, UKW’s shares now trade below the original IPO price more than twelve years ago, despite the experienced management proving the quality of the asset class and demonstrating how their conservative approach has delivered strong NAV total returns since inception. Backing up this conservative approach is the robust dividend cover, which has allowed UKW to continue to increase the level of the dividend in-line with, or ahead of, UK RPI every year since IPO.

If either proposal in the consultation were implemented, it would clearly reduce the NAV total returns that Greencoat UK Wind (UKW) would earn in the future, and would likely translate into a one-off hit to NAV. However, whilst UKW is clearly 100% exposed to the UK government subsidy regime (rather than other geographies), it has a mix of revenues streams across ROCs, other subsidy schemes (such as CfDs) and market power prices. It is only the indexation mechanism on the RO and not the value of the certificate itself that is up for debate within the consultation. The potential negative effects will also be mitigated by the relatively short remaining life of the ROCs in the portfolio (average remaining duration c. 7yrs). UKW also derives a significantly lower proportion of its revenues from the Renewables Obligation than solar peers, and so we would expect UKW to be significantly less affected than many in the listed peer group.

Fundamentally, UKW appears resilient. Certainly, if either of these proposed options is implemented, this does not help the headwinds the UKW currently faces. UKW’s gearing is slightly above the company’s preferred range. A lower NAV will mechanically increase gearing, and the uncertainty of these proposed changes will likely make further asset sales at NAV (the proceeds of which could be used to repay borrowings) harder to achieve in the short term.

However, UKW’s structurally high dividend cover means that it still has options to deploy surplus cashflows towards new investments, buybacks or reducing debt. We note that UKW continues to buy shares back, illustrating the confidence the board has in strength of the balance sheet. Currently, UKW offers an attractive dividend yield of 10%, given the shares trade on a discount to NAV of c. 30%. In our view, the sell-off on the announcement of the proposed changes to ROC tariffs are arguably overdone. This is not the first time ROCs have been consulted on, and the pullback is pricing in an overly negative scenario for a decision that is far from certain, and still subject to input from key stakeholders. Even then, UKW’s conservative approach means there are considerable levers to pull in order to mitigate a sizeable amount of their potential impact.