Two different portfolios, two different ways to make money. Whilst history doesn’t always repeat but it often rhymes, TMPL whilst still high risk is lower risk compared to MNL.

Investment Trust Dividends

Two different portfolios, two different ways to make money. Whilst history doesn’t always repeat but it often rhymes, TMPL whilst still high risk is lower risk compared to MNL.

Pair trading is a trade where you split your capital between a higher risk and a lower risk share, whilst still maintaining a blended yield of 7% which doubles your income every ten years.

You hope that if you time the market correctly the higher risk share increases in value which you can then use to accelerate your Snowball.

Two to consider who have recently changed their dividend policy.

TEMPLE BAR INVESTMENT TRUST Plc TMPL

Dividend

The Trust’s strong revenue performance was again in evidence, with an increase in revenue earnings per share of c.12.3% compared to the first half of the previous financial year. This has enabled your Board to declare an increased second interim dividend of 3.75 pence per share (2024: second interim dividend of 2.75 pence per share). The second interim dividend will be payable on 26 September 2025 to shareholders on the register of members on 22 August 2025. The associated ex-dividend date is 21 August 2025. This follows the payment of a first interim dividend of 3.75 pence per share on 27 June 2025.

As explained in the Company’s most recent Annual Report and supported by shareholders at this year’s Annual General Meeting, the Company’s dividend has recently been altered to see the Company’s progressive revenue-covered dividend enhanced by the payment of an additional 0.75 pence per quarter funded from capital. This has raised the prospective dividend yield on the Company’s shares to c. 4.4%, higher than the average dividend yield of the FTSE All Share which at the time of writing is 3.4%.

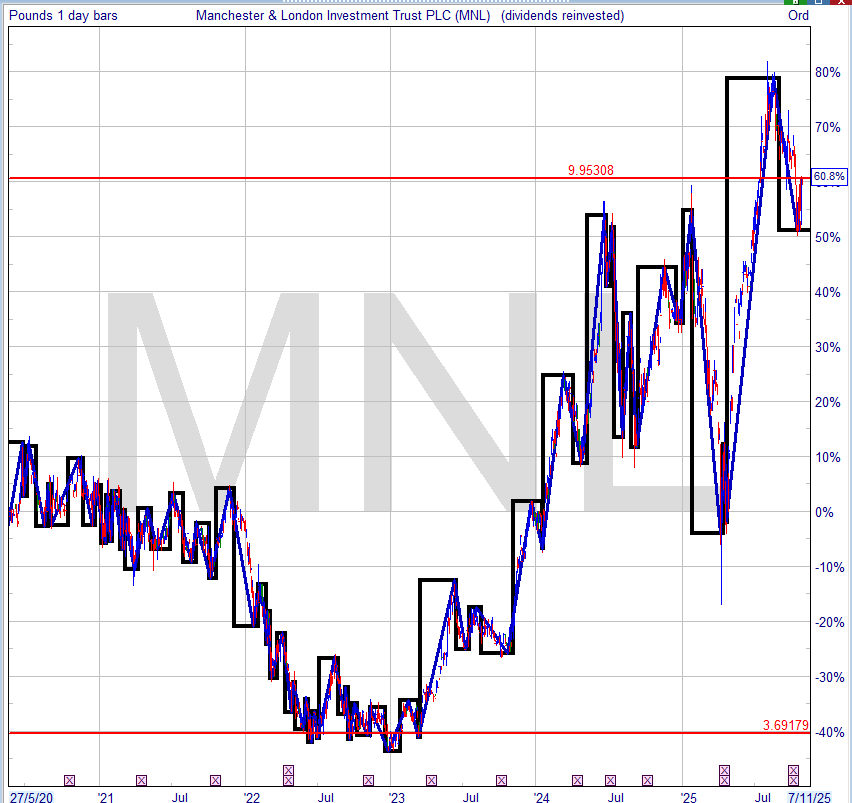

Manchester & London Investment Trust plc

(the “Company”) MNL

Enhanced Dividend Policy

On 24 September 2025 the Company announced it would be pausing on-market share buybacks because the aggregate proportion of the Company’s voting power held by the public (as that term is used in section 446 of the Corporation Tax Act 2010) is now close to the minimum 35 per cent threshold. The Company paid and/or proposed total dividends last financial year of 28p per Share split between special dividends and ordinary dividends.

Some shareholders have expressed their view to the Manager that the pause of share buybacks means that total capital returns via dividends and buybacks to shareholders will hence reduce.

We have listened and the Company would like to announce that it intends to pay at least 40p per share per annum ordinary dividend for the next five years (representing an Annual Yield of 5.01 per cent based on the closing share price of 798p on 22 October 2025) even if a mechanism is found and executed that allowed share buybacks to continue.

Dan Wright, Chairman of the Company, said:

“In essence, this makes Manchester & London a unique fund on the London Market that is both exposed to global growth and the opportunities of the Era of Artificial Intelligence, whilst also paying an attractive dividend income which can be relied upon for, at least, the next five years.”

MNL has a wide spread which you can normally deal within that is until the brown stuff hits the fan.

I’ll update some research on both companies, when I have the time.

GL

Updated 17 Oct 2025

David Brenchley

Kepler

This is a non-independent marketing communication commissioned by Schroder Investment Management. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

From China’s silk to Indonesian islands’ spices, the continent of Asia has always been important to the global economy. Early empires tended to look eastward to Asia first; even Christopher Columbus’s discovery of the Americas happened in search of a westward route to India, China, and the Spice Islands.

Today, we’ve lived through decades of growing US exceptionalism that has led to American companies accounting for 63p of every £1 invested in the FTSE All-World Index, as of 30/09/2025.

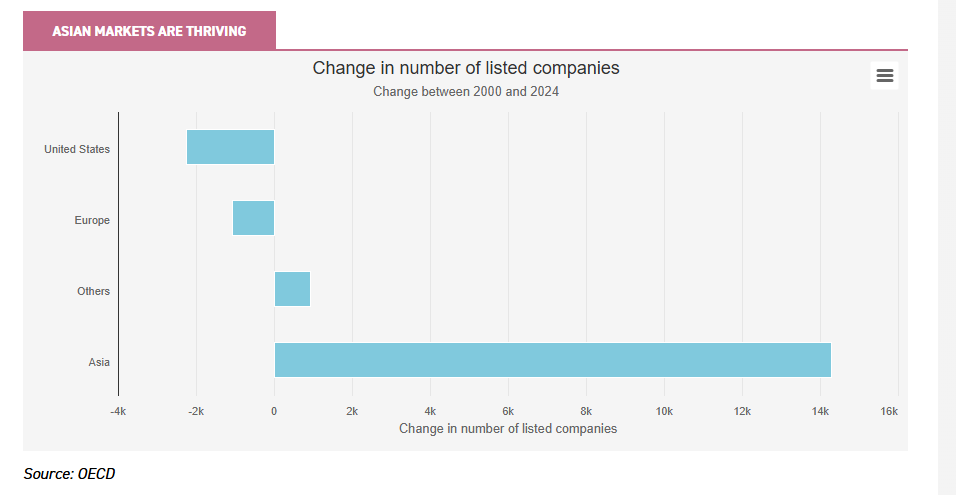

Yet, Asia’s influence on the global economy has remained and is well highlighted today: Asia accounts for 31% of global GDP, according to the OECD. Despite the US’s dominance of major indices, Asia is also now home to 55% of the world’s listed companies by number and accounts for 27% of global market capitalisation.

Its public markets are thriving, too, with the number of listed companies in Asia having almost doubled to c. 29,000 between 2000 and 2024. Indeed, while the stock of publicly listed companies in developed markets continued to shrink considerably in the past 25 years, Asian markets have grown, as you can see from the chart below.

Source: OECD

Despite this, investors are underexposed to Asia, in our view, preferring instead to have either a home bias, by being overweight the UK, or following what worked over the past 15 years, and focusing overly on the US stock market.

Asia is a dynamic and thriving region that remains under-represented, even in world indices. Despite being 27% of total global market capitalisation, Asia accounts for just 12.6% of the FTSE All-World Index, with Japan adding an extra 5.7%.

We believe that there are plenty of compelling reasons, which we will outline below, why Asia deserves a significant allocation in investors’ portfolios.

A growing region

As demonstrated already, Asia has plenty of momentum. By 2040, the consultancy McKinsey believes that Asia could contribute 42% of global GDP, be home to 60% of the Fortune Global 500 companies, and account for 55% of the world’s total workforce.

In addition, populations around the world are ageing rapidly, but the problem is generally much less acute in Asia as a whole than in Western countries. Indeed, McKinsey expects Asia to be home to more than half the population aged 18 to 24 and account for two-thirds of the global middle class by 2030.

McKinsey sees Asia’s new consumer class as “wealthier, more digitally savvy and as having a penchant for luxury goods”. Given this, Asian firms have a large and growing consumer base that is increasingly seeking out domestic brands for some of their luxuries such as coffee chains, cosmetics brands, and apparel sellers.

Asian companies have also become embedded as key players within areas such as digital services, fintech, healthcare, advanced manufacturing, clean energy, and, most recently, artificial intelligence (AI). Indeed, Asia accounted for 75% of AI patents globally in 2022, according to a report by Stanford University.

These are just some of the attractions driving Asian growth, but there are more from an investment perspective, which we’ll touch on below.

Uncorrelated growth and returns

One clear appeal is Asia’s lower correlation with the West, whether that’s relative to GDP growth rates or stock market performance.

Asian economies have and are expected to grow much faster than their developed counterparts. According to the IMF, the Asia and Pacific region, which includes the main economies of Japan, China and India, is expected to see real GDP growth of 3.9% in 2025. By contrast, North America is expected to see real GDP growth of 1.6% and Europe 1.3% in 2025.

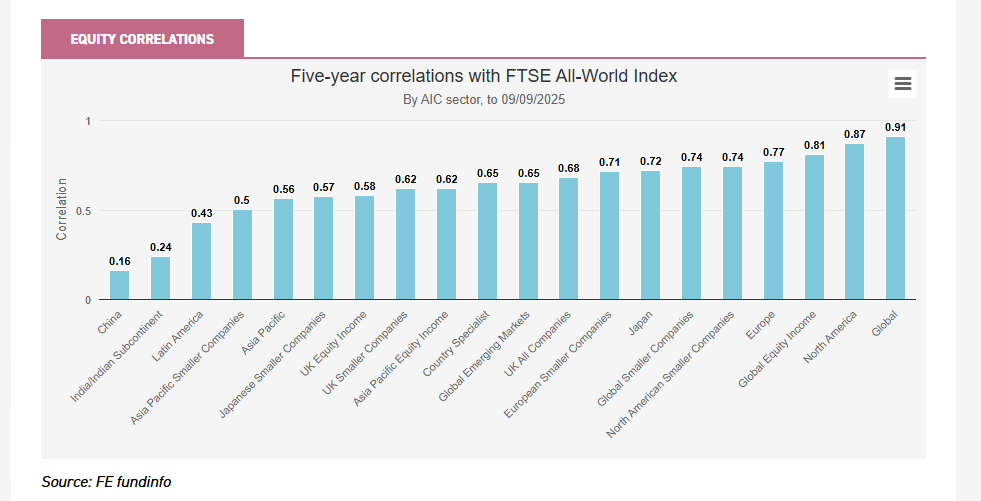

In terms of investments, Asian markets tend to exhibit much lower correlations than developed markets. Indeed, as you can see below, Asia-related investment trust sectors have been less correlated with the FTSE All-World Index in the ten and five years to 09/09/2025, with China/Greater China and India/Indian Subcontinent exhibiting the lowest correlation over both of those timeframes.

Source: FE fundinfo

Looking for assets that are less correlated with global equities is a good way of achieving diversification within one’s portfolio. That’s especially important at a time when the largest eight American companies account for c. 22% of the (4,220-company-strong) FTSE All-World Index (as at 29/08/2025).

In addition, given that a weaker US dollar is a key aim of the current US administration, getting exposure to other currencies, particularly those in Asia, which should benefit from US interest rate cuts and a weak US dollar, is also important.

Cheap valuations

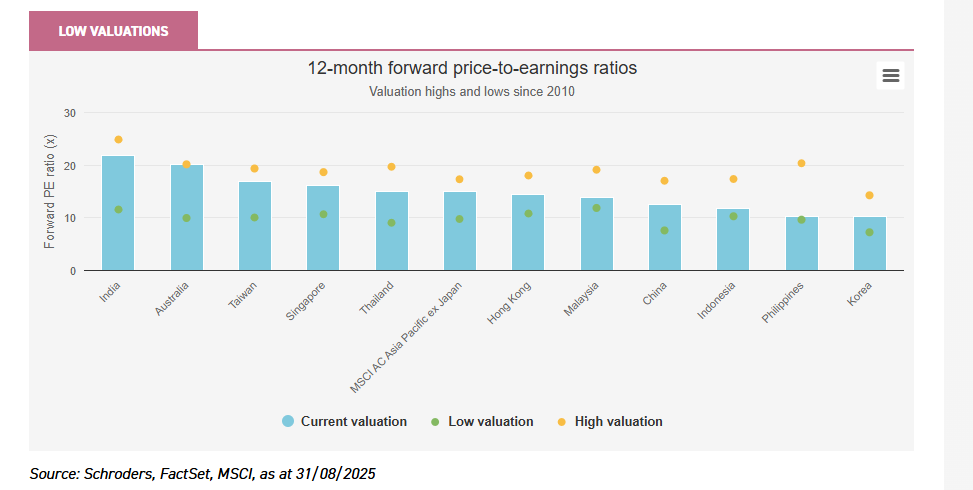

We briefly touched on the US exceptionalism that has driven global stock markets over the past 15 years, largely leaving most other regions in the dust. Asia is no different.

Source: Schroders, FactSet, MSCI, as at 31/08/2025

This extreme divergence has left Asian markets sitting on attractive valuations, both in absolute terms as well as relative to other markets.

Whereas the MSCI USA Index was trading on a forward price-to-earnings (PE) ratio of 23x on 29/08/2025, and a price-to-book (PB) ratio of 5.6x, the MSCI AC Asia Pacific ex Japan Index was on a forward PE of 16x and a PB of 2.1x.

These valuations are in a similar ballpark to the MSCI Europe Index, where the forward PE was 15x and the PB was 2.3x. Japan, by contrast, was slightly more expensive, at 16x on a forward PE ratio, but cheaper, at 1.7x, on a PB ratio.

Long-term outperformance

Despite this recent underperformance and low valuations, over longer timeframes, Asia has performed slightly better than even the US. Between the start of 2001 to 01/09/2025, for instance, the MSCI AC Asia Pacific ex Japan Index has returned over 700%, versus the MSCI USA’s 650% return, in sterling terms.

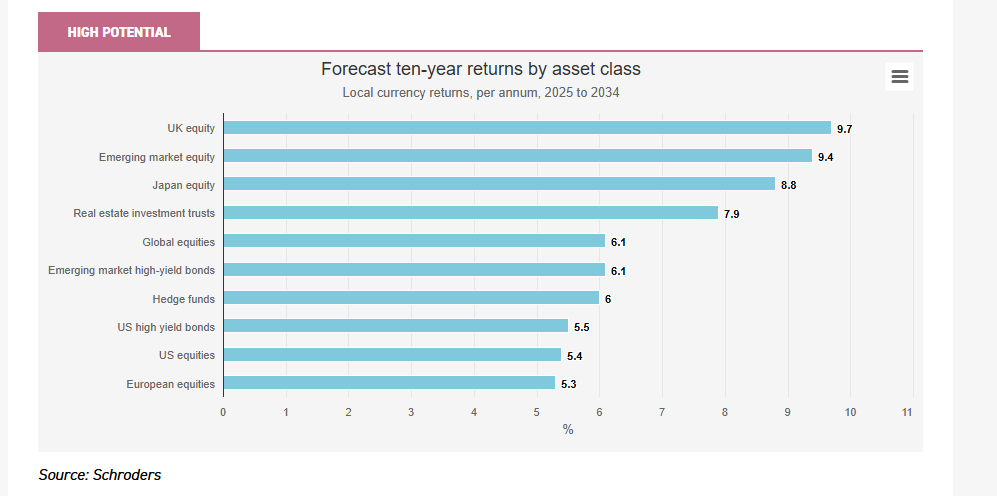

Many experts now believe that the current valuations mean that Asia could re-establish its superior performance versus the US – and other regions – over the next decade or so, as seen below.

Schroders forecasts US equities to return 5.4% per year in local currency terms over the next ten years, whereas emerging markets are expected to return 9.4% and Japan is expected to return 8.8% per year in local currency terms.

Source: Schroders

Unlocking value in Japan

Corporate reform is emerging as one of the most powerful drivers of Asian equity markets. Governments and regulators are pushing companies to improve transparency, raise governance standards, and put shareholder value at the heart of corporate strategy first. This is unlocking value in markets long held back by opaque structures, low returns on equity, and poor capital allocation.

Japan has led the way, with the Tokyo Stock Exchange and regulators forcing companies to unwind cross-holdings, increase return on equity and improve the independence of the board. The results speak for themselves, with a record ¥20 trillion of share repurchases in 2024 and ¥60 trillion returned to shareholders in dividends.

However, almost half of Japanese companies remain in a net cash position, according to SMBC Nikko, compared to less than 20% in North America and Europe. This has already prompted corporations to go beyond regulatory requirements and proactively deploy capital more efficiently, through US acquisitions, investment in AI capabilities, and returning cash to shareholders.

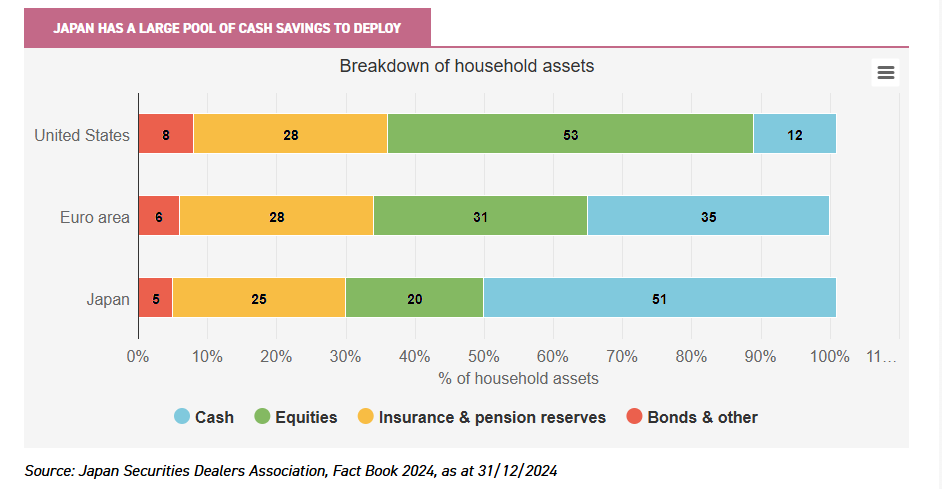

Japan’s economic revival is also being fuelled by shifting household dynamics, with households holding a staggering $14 trillion in financial assets, according to the JSDA (Japan Securities Dealers Association). As the chart below shows, more than half of household assets remain in cash-based holdings, a legacy of the caution towards investing that took root during Japan’s “lost decade”.

Source: Japan Securities Dealers Association, Fact Book 2024, as at 31/12/2024

The expanded NISA (Nippon Individual Savings Account) tax-free investment scheme has already boosted investment inflows by nearly 20% in its first three months, highlighting growing public engagement with asset management.

In addition, the strongest spring wage negotiations (Shuntō) in three decades are increasing disposable income and consumer confidence alike. The redeployment of cash into both consumption and financial assets marks a key step in Japan’s long-awaited transition from a deflationary mindset to sustainable growth and investment.

Corporate governance reform is one of the primary growth drivers identified by Masaki Taketsume, manager of Schroder Japan (SJG). There has been a steady improvement in return on equity, alongside record highs in dividends and share buybacks, but Masaki sees further scope for improvement.

Masaki focuses on company-specific catalysts, such as restructuring, M&A and capital allocation changes to drive returns. This has led to an overweight in small and mid caps, where valuations are more attractive than in larger peers, and in domestically focused companies that are less exposed to global trade and currency swings, and are well-placed to tap into rising consumer spending.

The trust’s returns are testament to the value of an active approach in Japan, delivering an annualised share price total return of 15% over the last five years, beating the 9% return from the TOPIX (as at 31/08/2025). SJG also offers a useful income stream, with a current dividend yield of just under 4%.

Strong income credentials

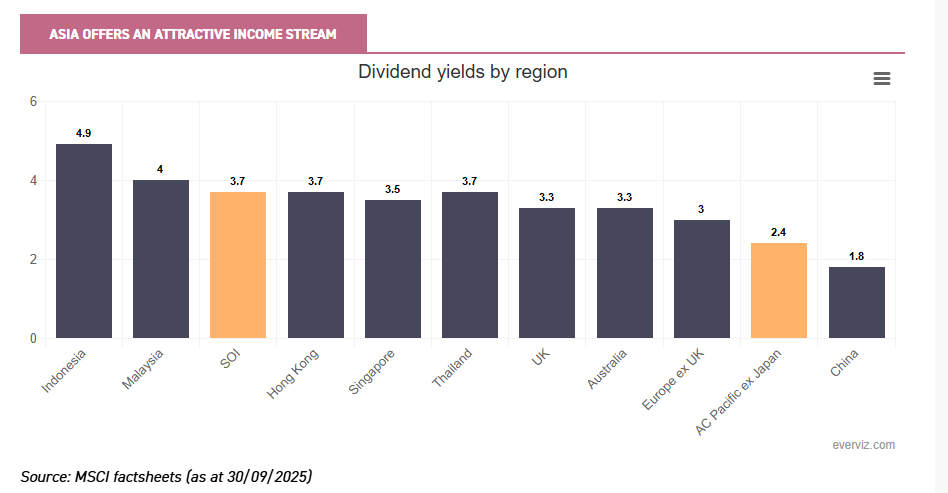

Asia may have flown under the radar for income-seekers, but a thriving dividend culture has put the region on a par with traditional equity markets. As the chart below shows, the yield for the MSCI AC Asia Pacific ex Japan Index isn’t far behind the UK and Europe ex UK, while countries such as Indonesia, Malaysia, and Hong Kong offer even higher payouts.

Source: MSCI factsheets (as at 30/09/2025)

Asia’s income story is also one of resilience. Payout ratios remain lower than in the UK and Europe, leaving headroom if earnings fall, while net gearing is also lower. Sector exposure is also broad, with financials and information technology accounting for much of the dividend base.

Schroder Oriental Income (SOI) aims to capture the combination of income and growth in Asian equity markets. The trust currently offers a yield of almost 4% and is the highest-yielding Asian fund on the AIC Next Generation of Dividend Heroes list, just one year away from achieving full status with 20 consecutive annual dividend increases.

Manager Richard Sennitt focuses on quality rather than chasing the highest-yielding companies, selecting companies with strong governance and the potential for both income and capital appreciation. This approach generates a high, natural income and avoids reliance on enhanced distribution policies used by some peers.

On the growth side, SOI offers exposure to powerful structural themes, from Taiwan’s world-leading semiconductor industry to the growing role of Singapore and Hong Kong as financial hubs. Its notable underweight to China also offers a differentiated option for investors seeking to limit exposure to the country’s ongoing macroeconomic challenges.

This balanced approach has delivered a ten-year share price return of 170%, reinforcing the trust’s ability to combine a dependable income stream with exposure to Asia’s long-term growth story.

A measured approach

While the income story within Asia is an important and understated point, Asia’s real engine is growth: Asia accounts for 82% of the world’s growth companies by global market capitalisation.

That said, this growth does come with big moves both on the upside and the downside.

While Asia is a predominantly growth market, it can also be volatile. To combat this, Schroder Asian Total Return (ATR) provides investors with a vehicle able to take advantage of the exciting growth opportunities of the Asian market while seeking to protect capital.

Managers Robin Parbrook and King Fuei Lee employ a sophisticated strategy that combines bottom-up stock selection, aimed at identifying high-quality companies able to capture the region’s growth potential, along with a top-down overlay to help mitigate downside risk.

The portfolio is made up of 40 to 70 companies with sound balance sheets, professional management teams, and capital allocation policies that are aligned with the interests of minority shareholders.

As ATR has no formal benchmark, Robin and King Fuei are agnostic to the trust’s reference index, the MSCI AC Asia Pacific ex Japan, particularly when it comes to positioning. Instead, they focus on finding the best-quality franchises in the region that they believe can outperform throughout the cycle, and judging them on their own credentials.

ATR’s hedging strategies, built using an in-house quantitative model, are used to identify risks on a country or regional basis. If any risks are detected, the managers will use derivatives such as index futures and options to provide some downside protection to the overall portfolio.

This tried and tested approach has been proven over the 17 years Robin and King Fuei have been working together on the strategy, which includes 12 years on ATR. Indeed, ATR has outperformed the MSCI AC Asia Pacific ex Japan in seven of the past nine full calendar years, with an average outperformance of 6.6 percentage points. The trust was awarded a Kepler Growth Rating for 2025.

Going for growth

Asia’s diversity presents a wealth of opportunities for active stock pickers able to uncover the most compelling opportunities across the region. Schroder AsiaPacific (SDP) stands out as a core holding for investors looking for pure Asian equity growth, aiming to capture the region’s long-term growth potential with a benchmark-plus mindset.

Given the level of heterogeneity across the region, success requires extensive on-the-ground resources to assess not only the macroeconomic and political backdrop in each country, but also the broader corporate ecosystem, from supply chains to competitive positioning.

The trust benefits from three decades of experience navigating Asian markets across a range of market cycles. Managers Abbas Barkhordar and Richard Sennitt are bottom-up stock pickers but remain mindful of broader macroeconomic and geopolitical dynamics.

SDP provides exposure to a diversified range of local and global drivers, providing resilience across different economic and political backdrops. A core focus is the world-class technology leaders in Taiwan and Korea, with SDP being an early investor in semiconductor giant TSMC and consumer electronics firm Samsung. Another export-focused driver is the China +1 re-shoring of global supply chains into ASEAN countries such as Vietnam and the Philippines.

This is balanced with exposure to domestic trends, including the fast-growing financial services sectors in India and the Philippines, as well as exposure to the companies benefitting from the growth of Singapore and Hong Kong as regional wealth management hubs.

One of the benefits of active management is the ability to tilt the portfolio to the most compelling opportunities. Earlier this year, the managers added exposure during the tariff-driven dips, while trimming positions where AI enthusiasm had pushed valuations above fundamentals. The trust is underweight to China, reflecting structural concerns, as well as being selective in India, given valuations.

Retail investors often face barriers when trying to access Asian equities directly. Many mainstream UK investment platforms offer limited access beyond developed markets such as Australia, Japan or Korea, while minimum purchase order sizes are high, as are trading costs due to foreign exchange and transaction fees.

Aside from that, doing your own due diligence can be very challenging, as financial reporting requirements tend to be considerably less onerous than in the UK and US, and documents are often not available in English.

Investment trusts democratise access to Asia by providing one-stop shops for diversified exposure to the region. Managers are rarely tied to their benchmark indices, and there are no liquidity issues, so they can provide access to smaller companies within the region, too.

Columbus may have set out to find an alternative route to Asia, which was then the centre of world trade, but he ended up stumbling across the Americas, part of which, as it would turn out, went on to become the economic powerhouse of the future.

With political risks now dominating the agenda in US discourse and the potential for AI hype to create a monumental bubble in asset prices across the Atlantic, attention may start to turn eastward in search of alternative growth opportunities.

Asia has a thriving and dynamic tech sector, complete with chipmaking capabilities, trading at a much less exorbitant price tag than Silicon Valley, providing a buffer against the excesses of the booming US market and geographic diversification to portfolios.

Schroders’ long-standing presence in Asia underpins its edge in navigating these diverse markets. With over 50 years’ experience in the region and a deeply embedded network of on-the-ground investment teams, the firm combines local insight with global perspective, enabling managers to identify the most compelling opportunities.

These resources underpin a wide range of investment options for investors seeking Asian exposure, from growth-focused SDP to income-oriented SOI. In addition, SJG offers single-country exposure, while ATR provides a risk-managed option for investors. Collectively, they showcase Schroders’ long-standing commitment to helping investors tap into Asia’s evolving opportunities.

William Heathcoat Amory

View profile

Updated 17 Sep 2025

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Discipline and order are important attributes for an effective fighting force. Of course, a guerrilla force may get the edge over a highly regimented army. But one would always back the Romans against the Gauls on the battlefield.

The same might be said about portfolios. Ideally built to withstand the slings and arrows of misfortune, most professionals arrange their clients’ portfolios with military style order. But it is probably most professionals’ guilty secret that their own personal portfolios often do not have the same look. Too many times, random selections of trusts or funds that pique interest mean that portfolios can look more Dad’s Army rather than the Navy SEALs. Captain Mainwaring and Pike usually surmount the many challenges thrown at them, but more through luck than judgement.

Putting portfolios together

There are many different approaches to designing a portfolio. When putting together funds or trusts to assemble a portfolio, the IA or AIC sector groups provide a helpful basis. However, in reality, most of these are rather two-dimensional representations of what the funds or managers set out to achieve. As many of our sector reviews will highlight (such as here), within most sectors, there are a range of different strategies that can be found within a bald descriptor like ‘Emerging Markets’.

In reality, many investors likely assemble portfolios in a less precise manner, and whilst geographic designations are clearly not to be ignored, a different taxonomy must include the role a trust provides in a portfolio. This set us thinking — what would an output-led categorisation of trusts and these more practical ‘sectors’ look like? Given no two trusts offer precisely the same solution (even in the same geographic sector), by definition, there are nearly 400 different solutions. However, there are some trusts that have grown to dominate their own peer groups, which can be viewed as the ‘kings’ of their realm or category.

Kings (in this case) rarely inherit their title, but typically carve out a strong lead over their peers in the long term, creating a loyal following and effectively owning their category. We review how five of these output-led categories might look. As we all know, dynasties can come to an end — sometimes quickly and violently — and so we also highlight the pretenders to the crown, those trusts which are justifiably jostling for attention and could potentially be called up and anointed when their day comes.

Long live the King

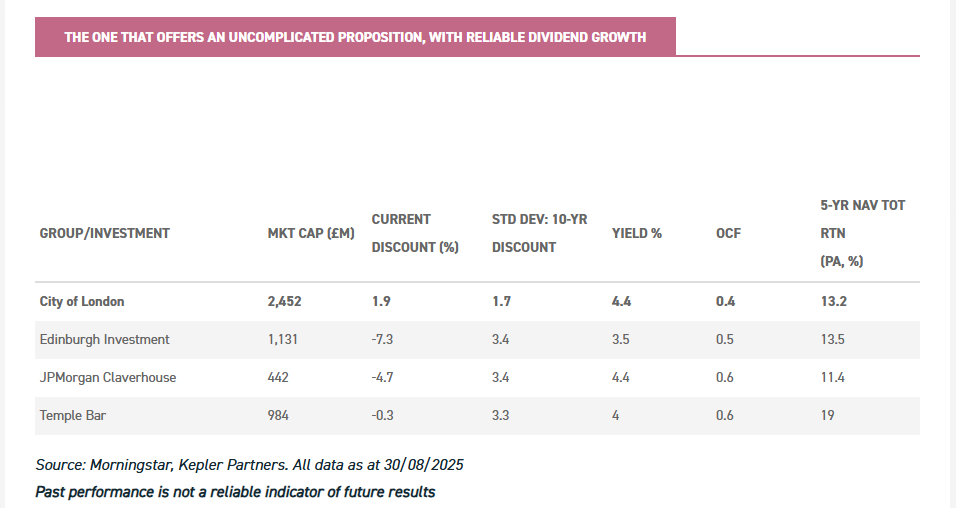

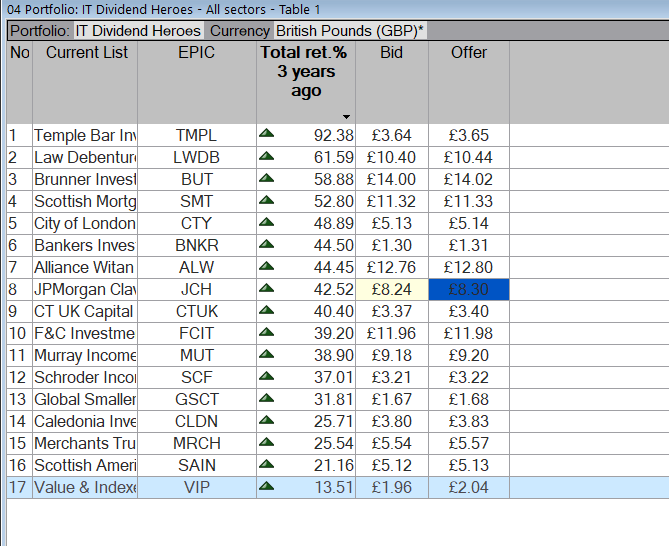

In identifying these ‘kings’, we believe each will fit a clear and readily identifiable role in a portfolio. It will also have grown to such a scale that it dominates peers in terms of scale, bringing a virtuous circle of liquidity, low costs, and likely has traded at or close to NAV for a meaningful period. One example might be City of London (CTY), which has grown to dominate the UK Equity Income sector in terms of size and low cost, but perhaps most importantly in its unrivalled track record of dividend growth. Looked at another way, CTY might be seen to reign over the fund/trust universe in “the one that offers an uncomplicated proposition, with reliable dividend growth”.

Investing largely in the UK, CTY has arguably inbuilt protections against currencies impacting portfolio income. Perhaps this is why 11 out of the 20 AIC Dividend Heroes are focussed on investing in the UK. CTY has delivered progressive dividend growth for 59 years, the longest track record of any. At the same time, (as at 31/07/2025) CTY has delivered NAV outperformance over its benchmark over 6 months, one, three five and ten years. Importantly, it has a low variability of the discount (in the table below we have used the standard deviation of month-end discounts for the last ten years, with a low number indicating that the discount has remained in a very tight range). In our view, this confers significant benefits to long-term investors, who can be relatively sure that share price returns will more closely resemble NAV returns.

The one that offers an uncomplicated proposition, with reliable dividend growth

Past performance is not a reliable indicator of future results

This year marks five years since Liontrust assumed management of Edinburgh Investment Trust (EDIN), a period marked by exceptionally strong NAV and share price performance relative to the FTSE All-Share Index. EDIN’s balanced, total-return-driven approach offers a compelling way to access high-quality UK companies. Imran Sattar’s style-agnostic strategy blends exposure across market caps with a focus on durable economic moats, robust balance sheets and strong capital allocation, helping the trust navigate volatile market conditions more effectively than some more style-constrained peers. This style agnosticism makes EDIN less susceptible to sharp swings between growth and value, providing greater portfolio stability, in our view. For income-focussed investors seeking higher near-term yields, the trust’s lower yield may appear less compelling. However, Imran’s primary focus remains on delivering sustainable, long-term total returns rather than chasing an unsustainably high yield.

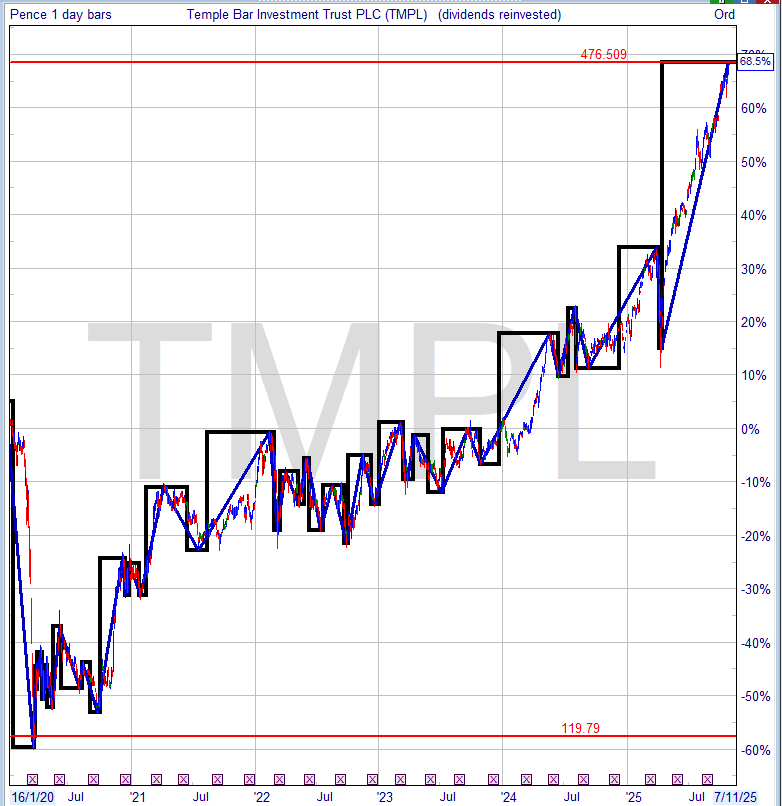

Another team approaching the five-year mark is Ian Lance and Nick Purves, who formally took the helm of Temple Bar (TMPL) in November 2020 when the management contract was won by Redwheel, bringing extensive experience in UK investing and a strong track record in value-oriented strategies. Over their tenure managing TMPL, they’ve aimed to establish the trust as a go-to for value investing, centring their strategy on identifying companies they believe are undervalued by the market, trading significantly below their fair or intrinsic values. By investing in such companies for the long run, they argue it helps build in a margin of safety, which can protect against unforeseen events and offer excess investment returns when the market eventually corrects these undervaluations. The managers have delivered sector-leading performance under their tenure. Providing investors with access to a differentiated portfolio, TMPL is a potentially good counterbalance to growth-heavy portfolios.

JPMorgan Claverhouse (JCH) offers an attractive blend of resilient, yet rising income with long-term capital growth potential, particularly at a time when UK equities remain undervalued and under-owned. The trust has a strong long-term performance profile, with a 52-year record of dividend increases. The new management team has seen Anthony Lynch and Katen Patel join incumbent Callum Abbott, following the retirement of William Meadon in July 2024. The trust has been repositioned in response to a more challenging income environment, shaped by shifting capital allocations where companies increasingly favour buybacks over dividends. A central part of this shift is to look for opportunities more broadly across the market-cap spectrum. This has included a material reallocation to UK mid-cap stocks, where the managers cite a rare blend of higher yields, lower valuations, and superior growth potential relative to large caps. Whilst the new team bring strong credentials, it’s reasonable to expect some investors may take time to build confidence around the trio’s long-term delivery of JCH’s objectives. Nonetheless, the early signs are promising with positioning more dynamic and the managers appear committed to enhancing the portfolio’s underlying income and rebuilding reserves — whilst continuing to deliver long-term capital growth.

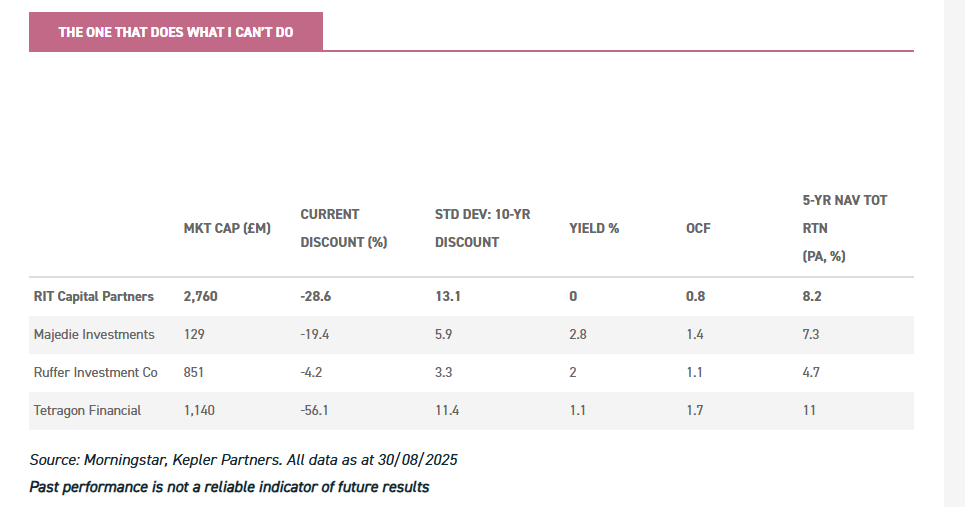

The one that does what I can’t do

Simplicity is always reassuring, but with equity markets on a global basis so dominated by mega-cap technology stocks, investors might seek out differentiated opportunities, purposely well off the beaten track. Historically, there has been only one trust that investors, professional and retail alike, have bought as ‘the one that does what I can’t do’. RIT Capital Partners (RCP) has built a strong reputation over the years, meaning that it traded on a narrow discount or even a premium to NAV as recently as 2022. Over more recent years, investor sentiment has waned, perhaps precisely because it isn’t invested in the same mega-cap stocks that have led the market. Another contributor perhaps is that the management team have undergone a number of significant changes. Fundamentally, RCP continues to deliver what it has always delivered, and on a c. 30% discount, patient investors may see a change in the fortunes to the positive for the trust when market dynamics change.

Whilst the king of this category is (perhaps temporarily) weighted down by investor sentiment, it hasn’t stopped challengers for the crown jostling for position. The fact that the likes of Aberdeen Diversified Income & Growth (ADIG) and JPMorgan Global Core Real Assets (JARA) have attempted a challenge, but are both now in managed wind-down, is, in our view, a symptom of a market-wide shift in sentiment rather than any comment on the quality of their respective offerings. At a different moment in time, both trusts might have gone on to grow to a significant size. Still, remaining in the frame are Tetragon Financial Group (TFG) (although investors may shy away from the voting and non-voting share structure, as well as the generous performance fees), Majedie Investments (MAJE), and Ruffer Investment Company (RICA).

MAJE is managed by Marylebone Partners, which has recently confirmed that it is to be bought by Brown Advisory, with the key individuals remaining in place and no change to the investment process. The trust is the shop window for the manager’s ‘liquid endowment-style’ strategy, which aims to deliver an annualised return of at least 4% above the UK Consumer Price Index (CPI) over five-year rolling periods. This long-term, fundamentally driven strategy mirrors the approach of elite US university endowments in that the team take a long-term view on investing (avoiding market timing). The approach harnesses idiosyncratic performance from an actively managed equities strategy, held alongside high-conviction investments in other asset classes such as specialist external managers (equity and absolute-return specialists), and what the team call “Special Investments”, which offer exposure to differentiated opportunities not likely to be held by investors in their portfolios. Whilst more complex than a simple direct equity strategy, MAJE is managed by a team with extensive experience, resources, and an established industry network — an intangible asset that’s difficult to replicate and likely bolstered by the tie-up with Brown Advisory. In our view, MAJE offers exposure to sources of return that investors are unlikely to capture through more ‘conventional’ strategies. It has the potential to deliver attractive risk-adjusted returns and enhance portfolio diversification. With the discount at ‘only’ 18% (when compared to RCP’s 28% discount), it would appear that the market also sees this potential.

RICA is a sophisticated multi-asset fund which has a strong focus on capital preservation. The aim is to deliver positive returns in all market environments, which means being acutely focussed on the key risks to equity and bond markets. The trust has delivered strong returns during the major market crises of the last two decades, and has also done a good job of protecting during the short-term volatility experienced this year surrounding US tariff announcements. In particular, options on the VIX index of equity market volatility delivered positive returns when markets fell, as did precious metals exposure. RICA then delivered positive returns in the market recovery, the managers buying call options on the S&P Index during the sell-off when they were cheap and monetising them over the following weeks and months. RICA also delivered positive returns in the equity market rotation at the start of the year, meaning that it performed in three distinctive market environments, illustrating exactly how the valuation-sensitive, macro-heavy process is supposed to work.

RICA’s unconventional strategies and sophisticated use of fixed-income instruments and derivatives look appealing in this new environment. Changes to the management team in recent years shouldn’t lead to any significant change in performance, in our view. The collegiate approach taken at Ruffer means that research is shared and views filtered through key members of the investment team. In fact, the size and structure of the team are intended to limit the impact of any manager leaving, in keeping with the focus on risk within the investment philosophy. RICA’s modest discount has remained stable this year, with the board implementing significant buybacks, and we note it has traded on a premium in the past when crises have hit and investors are more keen on protection.

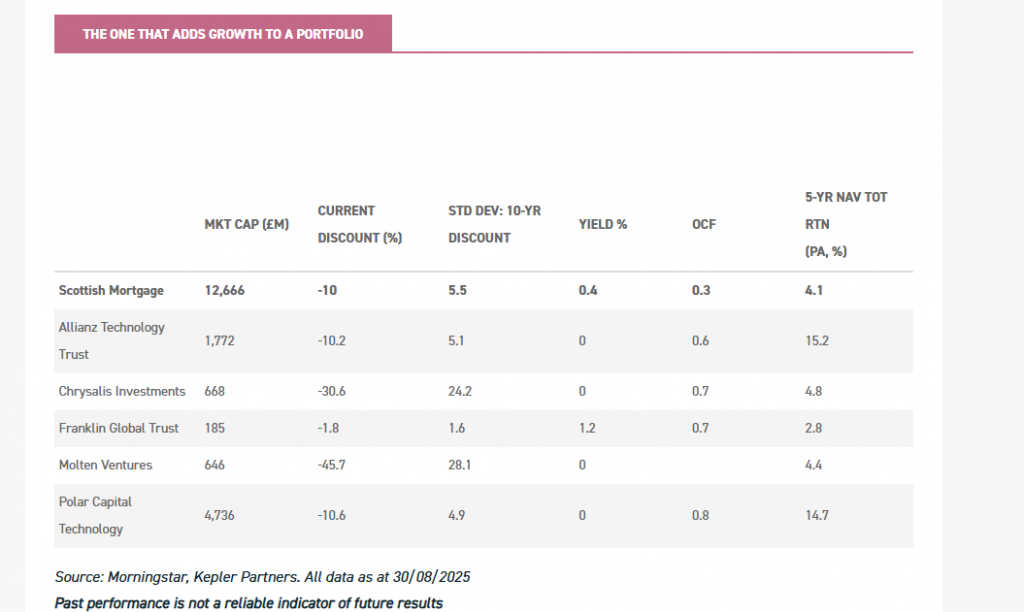

The one that adds growth to a portfolio.

Scottish Mortgage (SMT) has a special place in a lot of investors’ portfolios, not least because of the strong long-term track record it has built (as highlighted here), and the unique exposure it provides to the highest growth opportunities globally. Despite performance challenges more recently, it still appears in the top ten trusts in terms of NAV total returns over 25 years. The managers aim to invest in “exceptional growth companies”, whether they are public or private, and they have been very successful at this. On the latter, we think it is an impressive fact that of the top ten most valuable unicorns currently (growth-focussed, private tech companies), SMT owns five of them (end July 2025). The team aim to harness the startling upside potential from equity investing, but accept that they will lose money on some investments, with the big wins more than offsetting any losses. In terms of its broad reach across private and public growth companies — low charges and market liquidity — SMT’s incumbency is hard to beat.

The one that adds growth to a portfolio

Challengers for SMT’s crown tend either to focus on private or public growth companies. HG Capital Trust (HGT), Schiehallion (MNTN), Schroder British Opportunities (SBO), Chrysalis (CHRY), and Molten Ventures (GROW) all offer exposure to higher growth private companies at different stages of their development. This area of the market has fallen out of favour of late, meaning wide discounts are common. Sentiment is cyclical, and so whilst it is currently hard to see a catalyst for discounts to narrow or premia to establish, it would be foolish to rule this out at some point in the future. Of the early-stage investment vehicles, GROW has the longest pedigree (previously known as Draper Esprit), and historically traded at a premium as the ‘go-to’ exposure for British venture capital. It is a FTSE 250 member and owns and manages a portfolio of early-to-growth stage investments, as well as managing third-party capital. Venture capital (VC) is a high-risk, high-potential return strategy, and the Molten investment team aim to deliver returns of more than 3x on a third of their investments, with 1–2x on a third and the remainder likely to see a loss. We think the current discount likely reflects lower appetite for high-risk investments, and buybacks provide some support. The portfolio offers diversified exposure to the start-up scene in the UK and Europe, in particular, the clusters of innovative thinking in Cambridge, Oxford, and London, which have spun out so many good and profitable ideas already. We think VC and GROW itself have slipped under the radar of investors in recent years, focussed as they have been on large-cap US tech. Both could be a natural home for capital diversifying from the NVIDIAs and Microsofts of the world.

Private companies may not be for everyone though, and so those looking for ways to add high growth to their portfolio may consider Polar Capital Technology (PCT) or Allianz Technology Trust (ATT). The latter has outperformed the former over the longer term, likely thanks to its more active stock-picking approach, and the fact that the portfolio is typically tilted towards the mid-caps and away from the largest stocks in the index. Despite the index’s performance last year being heavily concentrated in a handful of mega caps, ATT kept pace. The mid-cap exposure is currently around double that of the index, and this contributes to a diversified thematic and industry exposure, which arguably makes the trust stand out versus ETFs and peers. The team’s long experience in the sector means they have seen multiple cycles and multiple new industries emerge, giving them insights into how new trends develop over time and which are likely to be winners. The value of their direct access to key founders, executives, and decision-makers in Silicon Valley also shouldn’t be underestimated, and we think it should be an advantage when it comes to stock picking.

Franklin Global Trust (FRGT) offers exposure to high growth, but with a different emphasis. FRGT was previously known as Martin Currie Global Portfolio. Zehrid Osmani remains the manager, investing in an unconstrained manner in attractively valued, high-quality companies with strong fundamentals and a sustainable growth trajectory. High conviction is a cornerstone of the strategy, with only the team’s best ideas getting a place in the portfolio, which consists of 31 stocks as of 30/04/2025. With trade tensions escalating since the beginning of the year, we believe investors may want to focus on companies with strong fundamentals — such as those targeted by Zehrid and his team. The uncertainty stemming from these trade tensions is weighing on earnings growth expectations, as both corporates and consumers are likely to reduce spending. However, we believe FRGT’s high-quality growth investee companies are the types of businesses that could still deliver growth in a subdued macroeconomic environment. FRGT has consistently traded close to par over the past five years, which we believe is an attractive feature and underscores the effectiveness of the board’s policy on discount management, giving rise to the very low volatility in the discount highlighted in the table above.

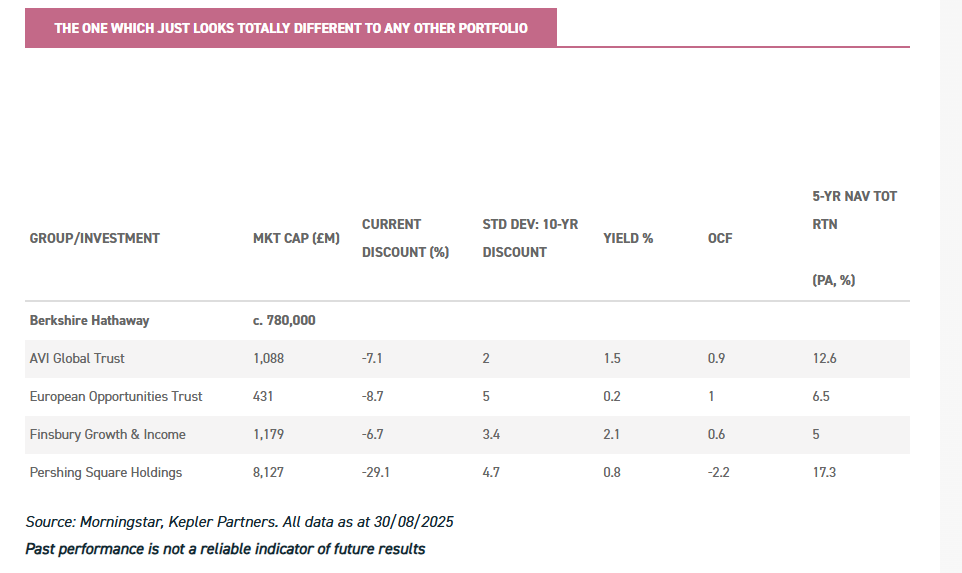

The one which just looks totally different to any other portfolio

In the good old days, before benchmarking and ‘treating customers fairly’ was invented, every equity portfolio looked different. Or maybe it just seemed that way, and the rise of passives and the massive stock market concentration that has occurred over the past decade has just made every portfolio manager wary of the effect of momentum, and being underweight stocks in favour. Either way, Warren Buffett has shown the benefits of ignoring the herd and having a singular manager or process with the (vanishingly rare) skill of picking stocks and adding value over the long term. The undisputed global king is, and remains, Berkshire Hathaway.

The one which just looks totally different to any other portfolio

Within the London-listed universe, the self-proclaimed heir to the Buffett throne is Bill Ackman of Pershing Square Holdings (PSH). In terms of fitting our description of what it is to be a ‘king of a category’, it might be hard to justify, given the persistently wide discount to NAV that PSH shares have traded over a prolonged time, and PSH can hardly be considered low cost. Perhaps a more fitting contender for the crown might be Nick Train, who manages Finsbury Growth & Income (FGT) in a highly concentrated and high-conviction manner with nearly 90% of the portfolio in the top-ten stocks. Prior to 2022, the trust had historically traded at a small premium to NAV. However, Nick’s confidence and resolve in his portfolio companies have been tested over the last five years, with FGT underperforming the UK and Global equity markets significantly. That said, a raging bull market driven by relatively narrow themes such as tech and AI, underperformance might be expected. Proponents will say this is precisely the moment to double down and avoid the temptation to follow the herd.

That said, another highly idiosyncratic trust — with an underlying portfolio which looks nothing like any benchmark — has performed very well despite its lack of exposure to the magnificent seven. AVI Global (AGT) provides exposure to undervalued special situations, and return drivers for its holdings tend to be driven by company-specific events, meaning performance should not be overly reliant on broader global equity market movements. At times in markets, it pays to consider opportunities that have been overlooked, especially if they are trading at attractive valuations. If market returns broaden, AGT could be well-positioned to benefit. AGT also has significant exposure to markets outside of the US, including in Europe and Japan, meaning that it could gain from a continued shift in market focus outside of the US.

European Opportunities Trust (EOT) has been managed by Alexander Darwall for two and a half decades. It has a concentrated portfolio of just under 30 stocks, representing ‘special’ pan-European companies with enduring qualities and high barriers to entry. Historically a highflier with a loyal following, the last few years have been challenging for the trust, and the board have been buying shares back. The recent acquisition of the manager, Devon Equity Management, by River Global should be a positive for the team managing EOT, as it will give them access to more resources and a broader perspective from River Global’s existing equity teams. EOT has lagged the benchmark recently due to several factors, including a low weight in banks, which have performed strongly, and underperformance by long-standing holdings such as pharmaceutical giant Novo Nordisk, which EOT has invested in for over two decades. Highly concentrated portfolios can (and do) diverge from the index from time to time, and in fairness to EOT, the same investment manager and process have delivered positive divergence from the index over many years. The current positive outlook for European equities could be the last piece in the puzzle for EOT to return to form, and perhaps stake a claim to re-take its crown.

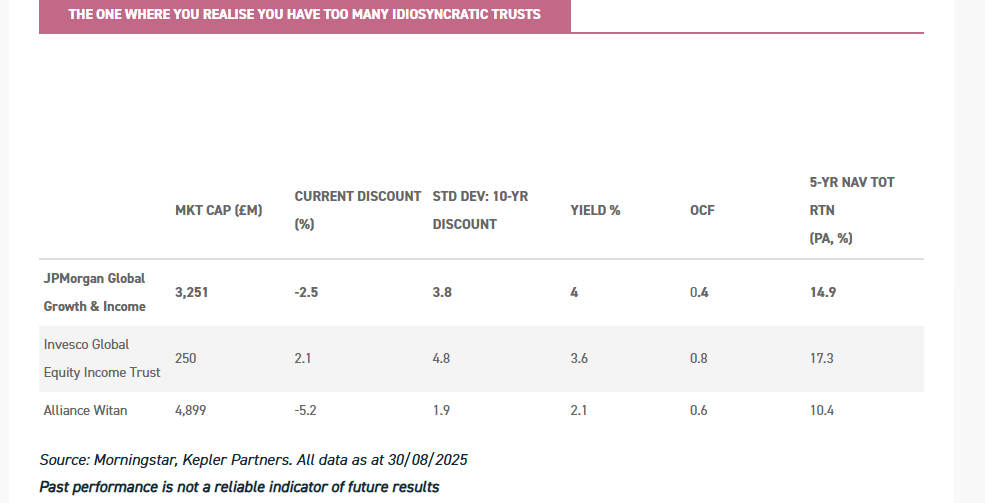

The one where you realise you have too many idiosyncratic trusts

Let’s face it, we’ve all been there. Or maybe it is just that your patience with this article is being tested. Your portfolio has just too many ‘interesting’ exposures, and you realise that the pendulum has swung too far. Back to safety… but the mainstream passives just have too much exposure to the magnificent seven. What is needed is a core exposure that is highly active. In our view, JPMorgan Global Growth & Income (JGGI) has unequivocally taken this crown. JGGI’s approach — which emphasises superior earnings quality, higher earnings growth, and valuation discipline — has delivered strong returns over the past five years, comfortably outperforming its benchmark. Notably, the trust has outperformed its benchmark in every completed calendar year since 2019, reflecting the consistency of the approach. The team have been rewarded through organic growth, as well as consolidation, having absorbed the assets of four other trusts since 2022. As the table shows, the trust has scale, low fees, and a stable rating. It also has the potentially useful feature of paying an enhanced dividend, supplemented by capital. The board aim to pay an annual dividend of at least 4% of the NAV as at the end of the trust’s previous financial year. As well as being resilient, the advantage of this approach is that the managers are free to invest in whatever stocks they like, without any income generation concerns.

The one where you realise you have too many idiosyncratic trusts

Amongst the pretenders to JGGI’s crown, Invesco Global Equity Income (IGET) is a perhaps lesser-known claimant. IGET has been the best-performing investment trust across both the AIC Global Equity Income and AIC Global sectors over the past five years, successfully navigating rapidly changing market environments with a portfolio designed to be ‘all-weather’, that is without bias towards any investment factor. For that purpose, managers Stephen Anness and Joe Dowling follow a bottom-up process, focussing on companies with strong balance sheets that they believe are cheap relative to their fair value. This approach can lead them to take contrarian positions, meaning investing in businesses that they think are temporarily out of favour. For example, in the first quarter of this year, when markets went risk-off, they rotated out of defensive names and into cyclical stocks like private equity firm KKR. They also took advantage of the post–Liberation Day (02/04/2025) sell-off to add stocks they believed had been oversold, such as lithography machine manufacturer ASML. Conversely, they have exited holdings that they assessed had reached fair value, as well as those where their conviction had weakened. The managers observed that their trading activity had not been this intense since 2022, underscoring their willingness to act with urgency to seize opportunities as they arise.

As IGET has seen increased demand for its shares, its discount has closed since the beginning of the year, and the trust is currently commanding a 2% premium. IGET, too, has a similar dividend policy to JGGI. The board has been proactive in issuing shares to meet the increasing demand for the trust’s shares, which over time could start to see the trust scale, creating the virtuous circle of better liquidity and a falling OCF, given the tiered fee structure.

Alliance Witan (ALW) is one of the largest investment trusts, with a market capitalisation of c. £4.8bn and a member of the FTSE 100 Index. ALW offers a one-stop shop for global equities through a multi-manager approach. The investment committee at Willis Towers Watson (WTW) oversees the allocation to a team of complementary stock pickers, aiming to keep the Portfolio as neutral as possible in terms of geographic, sectoral, and market factor exposure, but allowing stock selection to drive relative returns. ALW’s style-balanced approach makes it a strong candidate for investors seeking a core global equity strategy. The trust has a track record of delivering good performance relative to both its sector peers and benchmark across different market environments, such as the 2022 bear market and the AI rally of 2023. ALW delivered double-digit returns in 2024, but similarly to many active global equity strategies, it struggled against its benchmark due to the concentration of market returns in a handful of US tech mega-cap stocks. However, we would argue that 2024 was an exceptional year, and we expect the strategy to deliver better relative performance in a more normal market environment.

Conclusion

Loyalty towards ‘king of a category’ trusts can be sticky and long lived. The prize for achieving prime position in a segment of the market is big, reflected in the ability to issue shares and grow an investment trust franchise. Competition for these prime spots is vigorous and will likely continue to be so. In the current environment where mergers and corporate activity are at the forefront of the board’s minds, this is a Darwinian battle for survival.

‘What doesn’t kill you only makes you stronger’ might apply here. Wind-ups and mergers create an opportunity for the winners. Discounts have narrowed across the sector, particularly on equity trusts, and as and when interest rates come down, it is likely more money will come back into the investment trust market, now with fewer options for investors. This will be the opportunity for the winners to surf this wave of resurgent interest and extend their dominance over peers.

Are the US and Europe drifting apart?

Alan Ray

Kepler

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

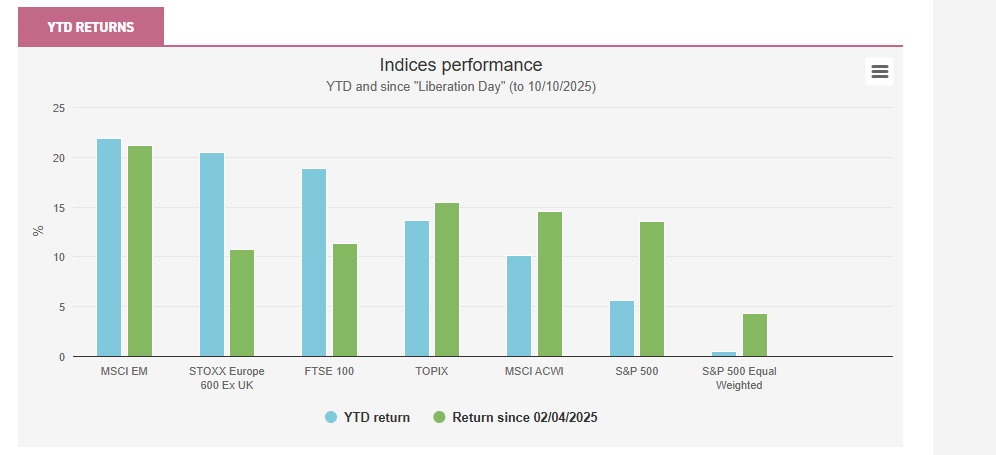

There have been some fascinating twists and turns in the last 12 months’ journey through the investment landscape, the rising price of gold, China’s equity market surge, and the bond market’s rebuke to the US administration being three that have attracted plenty of headlines. It would be an exaggeration to say that the interplay between the US and Europe has been less well covered, with the game of golf taking on an internationally significant role, but perhaps less so in terms of the interplay between US and European equities, which has quietly been one of the big themes of 2025. At the time of writing, the S&P 500 is up year-to-date by about 7% for a GBP investor compared to about 14% for European markets. Given the huge resurgence of the US market since April, one could be forgiven for not knowing these figures, and they certainly surprised us.

This difference is exacerbated by the polarisation in the S&P 500, where active managers are either long of the Magnificent Seven or are underperforming. In Europe, conversely, owning the GRANOLAS, a set of large-cap growth companies analogous to the Magnificent Seven, has been the wrong strategy, with a resurgence in more domestically orientated stocks, which some active managers have been quick to pick up on. Europe’s equity market resurgence does seem to be partly powered by positive fund flows coming from global investors lightening up on the US, and thus it feels right to ask whether the two continents have drifted apart, or is this just a cyclical phase? Let’s start by taking a short journey back in time and remind ourselves of how, perhaps only two years ago, we would have defined the US and Europe from a big picture investment perspective.

The US is a continental-sized economy united by a single language and with an abundance of natural resources. Its culture favours hard work and innovation. Further, it has an as-yet-unparalleled industrial military complex. Many individuals are directly connected to the equity markets through their savings and are acutely aware of the direction of the S&P 500. The country has an outstanding track record of growing world-leading companies that dominate or even monopolise their niche, as well as some outstanding domestic businesses that, although defined as ‘small cap’, would in any other country be a mid or large cap. Considering the US is a highly developed economy, it maintains a GDP growth rate that other developed economies just can’t seem to match. All of this combines to make the US ‘exceptional’.

Europe, by contrast, has a similar-sized population divided by several languages, borders, and varying political systems. Europeans are hard-working too, but take more holidays. Many Europeans are not very aware of stock markets, and they typically save through products where the links to stock and bond markets are opaque. Europe is innovative too, but often lacks the corporate ambition of the US, with companies often sold at an earlier stage. Far from being exceptional, Europe is seen as being a bit old and tired and probably too dependent on the US for its influence in the world.

Putting it more simply, let’s imagine that Jeff Bezos had started his business in a European country. Would Amazon be what it is today, or would Jeff have been happy running a successful online bookstore? Perhaps to be bought out by one of the traditional retailers after a few years.

All of this adds up to an investment mindset for many of us, myself included, that means we invest in US equities partly because, well, it’s the US and you just have to, right? Whereas Europe doesn’t seem all that essential. But, well, we ought to have a bit there just in case. After all, Europe is big and old enough that it’s bound to have grown a few large successful global companies. More recently, as Europe’s largest companies got their own acronym and it seemed like Europe was finally about more than just expensive handbags, investors did start to take more of an interest, and a very similar pattern of very narrow market leadership developed, with Europe’s ‘global champions’ a.k.a. the GRANOLAS, being the essential ingredient in any portfolio.

In 2025, something very interesting happened, though. In Europe, those ‘global champions’ have not performed well, and instead, more domestically orientated stocks have been doing the driving. For example, banks, which many active fund managers shy away from, have been a standout sector. Engineering and construction companies have seen their share prices run up in anticipation of the German government’s infrastructure spending, and Europe seems genuinely determined to build up its domestic defence industry. For the first time in a long time, European equities have risen because of Europe, rather than in spite of Europe, and it is perhaps no surprise that, in the short term, not all active managers have navigated this. It’s hard to be optimistic about Europe after a career when it has paid not to be. Japanese equity fund managers probably feel the same way.

Some active managers have adapted rapidly, though, and one trust which we think has done an outstanding job is JPMorgan European Growth & Income (JEGI). This trust aims to be an all-weather core holding in Europe and also pays a dividend partly funded from capital, which provides a yield on an asset class that income investors might otherwise be prevented from owning. You can read about why capital dividends can be a very good thing indeed here. The team managing JEGI correctly identified the momentum building behind banks, for example, as well as anticipating the momentum going out of some of those global champions and have significantly outperformed the market as a result, extending a very good long-term track record.

Another very successful strategy in Europe is the succinctly named European Smaller Companies (ESCT). As we noted above, the swing factor for investors shifting allocation to Europe has been a slightly better economic outlook for domestic economies. This has been incredibly helpful for ESCT’s portfolio of mid and smaller companies, where again, we see performance coming from domestic areas such as construction and engineering and defence. We also observe that ESCT has been the subject of more corporate activity in the last year than most investment trusts see in a decade. First, for baffling reasons given its performance track record, ESCT was strong-armed into a tender offer by an activist investor, but then, in recognition of that same track record, became the merger host for one of its peers, European Assets (EAT). In so doing, ESCT has also adopted a capital dividend policy and thus income investors have been given yet another extremely useful tool.

This surge in more domestically orientated stocks has led to others in the peer group underperforming slightly. The largest trust in the group, Fidelity European (FEV), has an outstanding long-term track record, but over the last year has just missed the benchmark. Others, such as Baillie Gifford European Growth (BGEU), BlackRock Greater European (BRGE), and European Opportunities (EOT) have been caught on the same side of the trade. This is, though, a short period of time, and as we’ll look at further on, has Europe really changed all that much? It seems likely that first, active managers will adapt, but second, perhaps it’s also good to reflect that some of those global businesses that have performed less well this year are successful for a reason.

In the US, the polarisation between the Magnificent Seven and ‘the other 493’ (constituents of the S&P500) is well known, and the investment stalwart JPMorgan American (JAM) has done an exceptionally good job of outperforming the index over the last five years, without relying on full Magnificent Seven exposure. We think this is what an investor in a core product should be looking for, and while JAM has trailed the index in the nine months elapsed in 2025, in our opinion it’s a relatively small price to pay for the lower volatility and outperformance it has delivered over five years. A less commented upon divergence in the US market is the underperformance of small caps as an asset class, and while this has persisted for several years, this year’s strong bounce back by the S&P 500 after April’s sharp falls was not matched by small caps, which broadly speaking fell at the same time but failed to bounce.

Again, while corporate activity in investment trusts isn’t always timed as an exact contrarian signal, it’s interesting that, for example, Brown Advisory US Smaller Companies (BASC) very recently introduced a conditional tender offer linking performance to an opportunity for investors to get up to 100% of their money back. BASC’s closest peer, JPMorgan US Smaller Companies (JUSC), did hold a tender offer in 2024, and while this was likely driven by activist investor Saba, it’s still a signal that other investors have lost interest in US smaller companies. Contrarian signals like this are, if nothing else, good prompts to re-examine an asset class. Both these trusts’ managers have really good long-term track records investing in the quality growth domestic businesses that are at the core of the US small-cap universe, and which have not been rewarded by investors at all for quietly compounding, while a few mega-cap stocks undergo explosive growth phases that may, or may not, prove to be rooted in long-term reality. US small caps have had such a tough time getting attention from stock market investors for a long time now that anyone with an ounce of contrarianism ought to be looking more closely.

In a similar vein, North American Income (NAIT) offers investors a real alternative to the concentrated performance of the index and could be, as the name implies, a very good option for income investors otherwise put off by the US’s relatively low dividend yield. Although not its intention, we can see this trust as a natural diversifier from the Magnificent Seven-led index.

With the polarisation in investment trust performance discussed above seemingly driven by that switch in the fortunes of Europe and the US in investors’ minds, it’s fair to ask whether this really is a case of continents drifting apart, or something more cyclical? Uncomfortable scenes at golf clubs on both sides of the Atlantic this year are representative of a strained relationship between the US and Europe, but perhaps also serve as a reminder of the incredible importance of the relationship between the two. One conclusion we might reach from the last year as investors is that there has been an irreversible shift in the balance. Before, we invested in US equities because of the US, and in European equities, in spite of Europe. Every day that the gold price goes up and the dollar goes down helps confirm this year’s narrative that the rest of the world is seeking to diversify its investment exposure. And now, we are investing in Europe as an ‘improver’ and being more selective about our investments in the US, focussing on its ‘global champions’ that are less reliant on its domestic economy. If true, that’s quite the reversal.

If, on the other hand, we had a slightly contrary streak, we could look at it differently. The shift is real enough. Given the polarising nature of the current US administration, it’s incredibly difficult to compose short sentences that don’t imply some bias, so we’re going to trust our readers to see the next statement as a non-partisan comment. As a dispassionate investor, it is important to acknowledge that it is very likely true that, on average, a negative perception among global investors is an important part of the shift. But perhaps the sheer volume of noise generated means that it’s easy to miss, for example, that the US has made some extremely positive pro-business revisions to the tax system that will encourage more investment.

In contrast, what is driving optimism in Europe? German infrastructure spending is often cited as one of the swing factors, and it’s true that Germany’s very conservative balance sheet does allow it to borrow more to fund this. But infrastructure in democratic countries is notoriously difficult to do at scale, and we don’t think it’s too cynical to point out that politicians’ plans often include previously announced spending to make up the total. Europe’s new determination to spend more on defence is also cited as a positive factor for markets, and while it does seem likely there will be an increase, one can easily imagine there will be wavering once it becomes clear that this comes at the cost of what? Spending on health care? Social care? These are highly prized parts of European society. In short, it’s not hard to see how backtracking from today’s very positive outlook could occur.

Make no mistake, though. A lot of capital has flowed into Europe, and it’s hard to dismiss it all as ‘hot money’ seeking a quick, safe haven from an, ahem, non-conformist US administration. We think European equities deserve to be pushed up the rankings in terms of the attention they receive. But are we really so confident that those two opening descriptions of the US and Europe have changed all that much? It’s a strange world indeed when US equities might be the biggest contrarian bet in global markets, but that’s the world we find ourselves in.

We look at the performance of global equity trusts year-to-date.

Jean-Baptiste Andrieux

Updated 22 Oct 2025

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should be considered as general market commentary.

Some figures seem untouchable, no matter how dire the circumstances. Take Tintin, for example, who always emerges unscathed from the most desperate moments — whether escaping assassination attempts by Chicago mobsters, dodging the imperial Japanese army, or returning from space in a rocket running low on oxygen.

Arguably, a similar resilience can be observed in the US mega cap stocks linked to artificial intelligence (AI), that appear to withstand almost anything thrown their way. These stocks have faced numerous headwinds this year, particularly from escalating trade tensions between the US and the rest of the world. The situation reached a climax on Liberation Day (02/04/2025), when Donald Trump announced higher tariffs against most countries. This triggered a broad market sell-off as investors feared the economic fallout of these tariffs. Yet, much like Tintin’s knack for landing on his feet, AI-related stocks bounced back once tariffs were paused and reduced, further supported by robust second-quarter earnings from US companies. That said, it is worth noting that the US dollar has weakened over the period, negatively impacting returns for GBP investors.

As a result, while the S&P 500 index has lagged European and UK equities (in GBP terms) since the start of the year (to 10/10/2025), some US AI-related companies, such as NVIDIA and Broadcom, have delivered superior returns. In fact, it is worth noting that the equal-weighted version of the S&P 500 has largely underperformed the market-cap weighted version, suggesting that gains in the US equity market have been driven primarily by its largest constituents, many of which are linked to the AI theme.

Source: Morningstar

Past performance is not a reliable indicator of future results

The large-cap tech stocks are outperforming because of their superior earnings outlook, largely due to the impact of AI. The table below shows that over the next two years, the Magnificent Seven are expected to deliver earnings growth way ahead of non-US developed markets, with only the emerging markets expected to deliver a similar result. In fact, the gap between these stocks and the rest of the US market is even wider than it is to the ex-US developed world. There is a strange dichotomy between the optimism around AI and the otherwise sluggish US economy. While US indices are being dragged up by the Magnificent Seven and AI, investors who want to stick with this trade might want to consider a technology-focussed portfolio rather than a US fund or ETF. It is notable how the valuation multiple for the tech stocks rapidly falls when you look out two years, much more rapidly than the multiples for the other indices in our table. The bull case for AI is that it will transform most industries, in which case this superior earnings growth would be expected to continue for many years to come, and the valuation multiple would rapidly decline when considering these further forward earnings.

| Index | Price-to-earnings (1-year forward) | EPS growth (1-year forward) (%) | Price-to-earnings (2-year forward) | EPS growth (2-year forward) (%) |

| MSCI World ex USA | 14.6x | 12.1 | 12.9x | 13.5 |

| S&P 500 | 20.7x | 12.7 | 18.8x | 10.1 |

| Bloomberg Magnificent 7 | 29.7x | 13.8 | 25.7x | 15.4 |

| MSCI Emerging Markets | 12.7x | 17.1 | 11x | 15.8 |

Source: Bloomberg Estimates, as of 17/10/2025

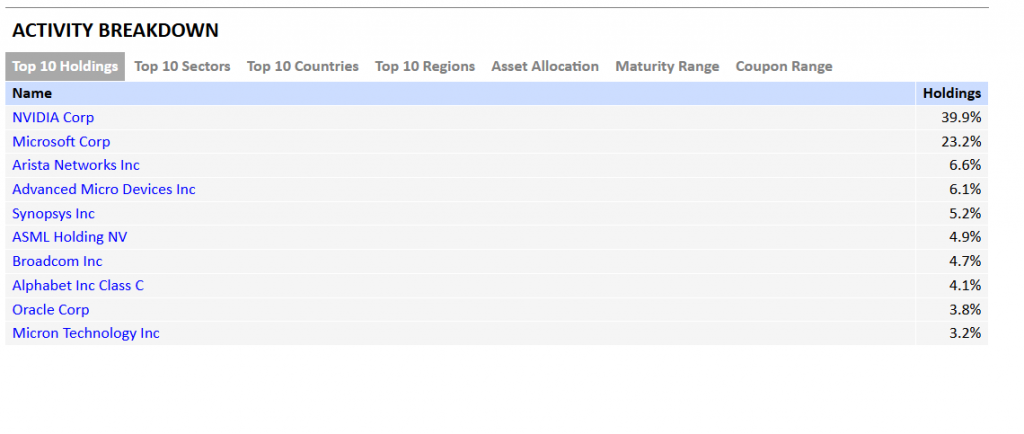

Given the strong performance of AI-related stocks, it is perhaps unsurprising that the best-performing investment company across both the AIC Global and AIC Global Equity Income sectors year-to-date is Manchester & London (MNL). Its portfolio is highly concentrated in AI-related names, with NVIDIA, Microsoft, and Broadcom together accounting for c. 72% of its holdings (as of the end of August). Over that period, MNL generated a NAV total return (TR) of 27.8%, outperforming global equity indices such as the MSCI ACWI Index, which returned 10.1%, and the 8.8% simple average return of global equity-focussed investment companies. MNL, however, can be seen as an outlier within the peer group given its very concentrated portfolio and near-exclusive focus on the information technology sector. The runner-up, Scottish Mortgage (SMT), also has significant exposure to AI-linked companies and has benefited from positions such as Cloudflare, a cloud services provider whose shares have risen 86.9% year-to-date.

Exposure to AI-related stocks, notably Broadcom, also supported the performance of Invesco Global Equity Income (IGET), which outpaced global equity indices with a NAV TR of 12% year-to-date. Yet, IGET’s performance was also aided by overweight allocations to continental Europe and the UK, regions that saw a recovery in the first half of the year, notably with defence companies and banks rallying. Key contributors also included UK-listed bank Standard Chartered, which reported improved earnings and net interest margins, as well as aerospace & defence company Rolls-Royce, which has experienced revenue and profit growth under CEO Tufan Erginbilgiç (appointed in January 2023). Similarly, Murray International (MYI) benefited from its holding in Broadcom as well as from its overweight position in emerging markets, which have performed strongly since the beginning of the year, notably thanks to a weaker US dollar.

The table below lists all investment companies in the AIC Global and AIC Global Equity Income sectors that have outperformed the MSCI ACWI Index since the beginning of the year (to 10/10/2025).

| Investment company | Sector | Return to 10/10/2025 (%) |

| Manchester & London (MNL) | AIC Global | 27.8 |

| Scottish Mortgage (SMT) | AIC Global | 18.4 |

| Murray International (MYI) | AIC Global Equity Income | 14.2 |

| Monks (MNKS) | AIC Global | 13.2 |

| Invesco Global Equity Income (IGET) | AIC Global Equity Income | 12 |

| MSCI ACWI | N/A | 10.10% |

Source: Morningstar

Past performance is not a reliable indicator of future results

Among his numerous adventures, Tintin sometimes faces painful dilemmas. For example, in Tintin in Tibet, he must choose between risking his life to climb the Himalayas in the hope of rescuing his friend Chang, whose plane crashed in the mountains, or accepting the high probability that his friend did not survive and calling off the perilous expedition. Similarly, global equity investors may face difficult dilemmas in the current market environment. The recent outperformance of non-US equities could be seen as the premise of a sustained broadening of returns beyond the technology-dominated US equity market. Yet, the strong rebound of AI-related stocks since Liberation Day may suggest that the outperformance of international equities was only a short-term blip and that US tech stocks will continue to dominate. Managers of trusts in the AIC Global and AIC Global Equity Income sectors take different views on this matter, with some remaining enthusiastic about AI-related names, while others see better opportunities elsewhere.

Franklin Global Trust (FRGT) is one strategy with significant conviction in the AI theme, expecting it to drive growth for many years, potentially decades. Managers Zehrid Osmani and Jonathan Curtis gain exposure to AI primarily through semiconductor companies — including NVIDIA, ASML, Cadence Design Systems, and BE Semiconductors — which they view as key beneficiaries of increased spending on AI infrastructure. They also anticipate that the next phase of AI development will reward companies capable of monetising the technology. Accordingly, they hold Meta Platforms, which they believe can leverage AI to boost advertising revenue and enhance user experience across its platforms. In the first half of the trust’s 2025 financial year (ended 31/07/2025), the managers also built exposure to AI in China, noting the country’s progress in this area, and initiated a new position in Tencent, China’s leading social media company and a significant player in the global gaming industry. They see multiple ways the company could leverage AI, such as improving advertising allocation, expanding its addressable market, and supporting more efficient game production.

Source: Franklin Templeton, MSCI

Similarly, SMT is exposed to AI through companies involved in the build-out of the AI infrastructure, such as NVIDIA and TSMC — the world’s largest semiconductor foundry — as well as through businesses that leverage AI by embedding it into their products. For example, the trust holds AppLovin, an ad tech company that uses AI to optimise mobile game monetisation and is expanding into e-commerce advertising, as well as Meta.

On the contrary, Alliance Witan (ALW) exhibits more pronounced underweight positions in the information technology sector and North American equities than usual. ALW is managed by an investment committee at Willis Towers Watson, who aim to keep the portfolio as closely aligned as possible with the benchmark in terms of country, sector, and factor exposure, while allocating capital to high conviction stock pickers. The underweights are therefore due to those stock pickers not investing much in US technology mega-caps. For instance, GQG Partners — a stock picker following a quality growth-at-a-reasonable-price approach — has rotated out of technology names and into defensive stocks. The team is concerned about the valuations commanded by US tech mega-caps, drawing parallels with late 2021 and early 2022, just before interest rates rose and technology stocks subsequently sold off. Other stock pickers also reduced their exposure to technology following the launch of DeepSeek’s cost-efficient AI chatbot in January 2025, which raised questions about the substantial capital expenditure by US tech firms on AI infrastructure.

Source: Willis Towers Watson

IGET has an even larger underweight in North America and the information technology sector, and more sizeable overweight positions in Europe and the UK, deviating further from global equity indices. This positioning is not the result of top-down views but stems from the managers’ approach to stock selection, as they favour attractively valued companies with robust fundamentals. This valuation-sensitive approach naturally steers them away from US tech mega-caps, which trade on high multiples, and toward Europe and the UK, where mispriced opportunities are arguably more abundant. Managers Stephen Anness and Joe Dowling have also identified opportunities in the US outside of the tech mega-caps. This includes cruise operator Viking, which benefits from a strong position in the cruise market. The managers also believe that the company could be less sensitive to inflation and recession risks, as Viking targets wealthy US retirees. Nonetheless, Stephen and Joe are also willing to hold stocks exposed to the AI theme if the price is attractive. For example, they have been holding Broadcom rather than NVIDIA, seeing the former as more attractive from a valuation standpoint and offering greater diversification in revenues while providing similar exposure.

Brunner (BUT) is also underweight North America relative to standard global equity indices; however, this is structural, as the trust uses a composite benchmark consisting of 70% FTSE World ex-UK and 30% FTSE All-Share. Conversely, BUT has a structural overweight to the UK, which the managers view as a differentiated market, rich in mature, cash-generative businesses trading at attractive valuations. This does not mean BUT has no AI exposure. For instance, the managers took advantage of the market sell-off in April to build a position in Amazon — whose cloud business, Amazon Web Services, provides exposure to the AI theme — while the portfolio also holds two other Magnificent Seven stocks: Microsoft and Alphabet. That said, the managers view US equities as richly valued in aggregate and have added new positions in non-US stocks since the start of the year, focussing particularly on value-oriented names. Examples include South Korean car manufacturer KIA, noting that it is one of the most profitable automakers with a strong balance sheet and exceptional operating margins, which are uncommon features in the automotive industry.

In The Secret of the Unicorn, Tintin purchases an old model ship at Brussels’ flea market to gift it to his friend Captain Haddock. Unknown to him, a scroll containing a clue leading to a 17th-century pirate’s treasure is hidden under the mainmast. This treasure is later found by Tintin and his companions, Captain Haddock and Professor Calculus, in Red Rackham’s Treasure, enabling Haddock to acquire Marlinspike Hall. In short, the modest price Tintin paid for an old model ship technically led to Captain Haddock acquiring a country house — undoubtedly a great bargain. Stretching the analogy somewhat, acquiring shares of investment trusts trading at a discount can prove to be excellent bargains for patient investors, as they may benefit not only from the performance of the underlying NAV but also from a potential narrowing of the discount.

In the AIC Global sector, we think SMT’s discount of 11.5% could be particularly attractive. The trust’s discount has been narrowing from its low point of 22.7% in the first half of 2023 and may continue to narrow if AI-related stocks remain dominant in market returns. That said, given SMT’s high-growth mandate, its discount has historically been, and is likely to remain, prone to sharp swings, reflecting the strategy’s volatility. We would also highlight F&C Investment Trust (FCIT), which offers core exposure to global equities and currently trades at a 7.7% discount. The trust traded close to par or at small premiums in Q4 2022 and Q1 2023, possibly reflecting its resilience during the bear market of 2022 compared with sector peers. In addition, the board operates a share buyback policy aimed at keeping the share price close to NAV and reducing discount volatility. For example, over the course of the year to 10/10/2025, c. 2% of the shares outstanding were repurchased.

Source: Morningstar

Most constituents of the AIC Global Equity Income are trading at discounts close to par, with some even commanding a small premium. The outlier is Scottish American (SAIN), which is trading at a 10.2% discount at the time of writing, more than one standard deviation below its five-year average of 3.5%. The trust commanded a premium prior to 2022 but fell to a discount when central banks began hiking interest rates. This may reflect the fact that the trust had a relatively high-growth portfolio for its sector, and has therefore been affected by the higher-rate environment, with the strategy prioritising dividend growth rather than generating the highest possible yield. That said, central banks have been lowering interest rates since 2024, which could make SAIN more attractive. Moreover, we think it is worth remembering that fixed-income instruments do not offer income growth potential.

Source: Morningstar