Fancy a 10%+ dividend yield ? 3 passive income heroes to consider

Each of these UK stocks, funds, and trusts has a double-digit dividend yield and excellent long-term growth potential.

Posted by Royston Wild

Published 18 October

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

UK investors are spoilt for choice when hunting for shares with large dividend yields. Broadly speaking, the London stock market’s strong payout culture makes means it’s packed with top passive income shares.

With this in mind, here are three stocks with a yield above 10% to consider.

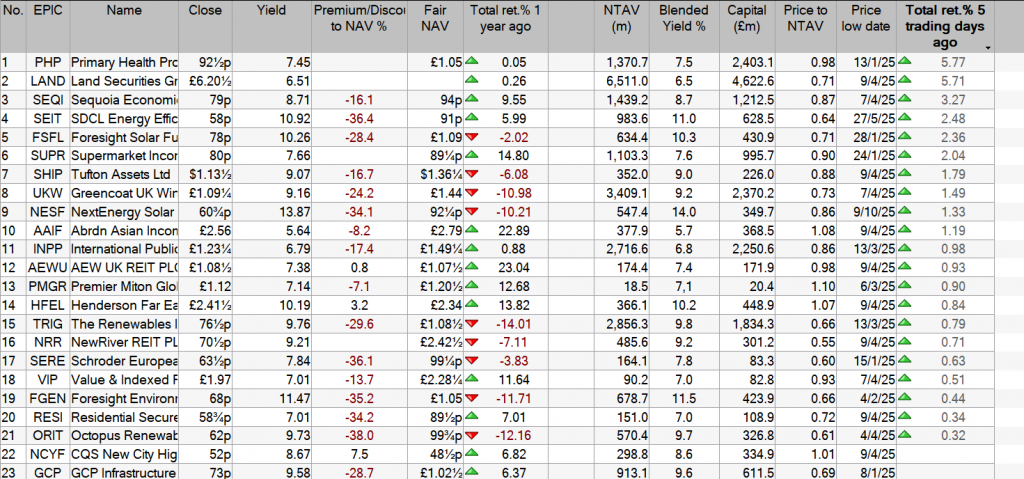

Henderson Far East Income: 10.2% dividend yield

Investing in emerging markets can sometimes be a bumpy experience. Political and economic conditions in regions like Asia can be volatile, impacting returns.

This hasn’t stopped Henderson Far East Income (LSE:HFEL) delivering large and growing dividends over time, though. Cash rewards have grown each year since the mid-2000s.

This reflects the investment trust‘s decision to prioritise passive income over growth. It’s also due to its wide range of holdings spanning different sectors and parts of the Asian continent. This diversified approach provides a smooth return over the economic cycle, and protects investors from weakness in specific industries and regions.

In total, Henderson Far East Income has holdings in 71 highly cash generative businesses. These include companies with enormous dividend yields like China CITIC Bank, Telkom Indonesia, and Evergreen Marine Corp Taiwan.

Roughly 58% of the trust’s assets are currently located in China, Hong Kong, and Taiwan. This leaves it vulnerable to current tough conditions in the region’s largest economy. But it could also help it outperform when the Chinese economy rebounds.

Global X SuperDividend ETF: 10% dividend yield

The Global X SuperDividend ETF (LSE:SDIP) offers similar diversification benefits that reduce risk and can enhance long-term returns.

This exchange-traded fund (ETF) also focuses on high dividend yield businesses across sectors, but does so with a more global flavour. US shares make up its largest single weighting, at 26% of the portfolio. Other well-represented countries include Brazil, Hong Kong, and the UK, providing investors with the stability of developed markets and the growth potential of emerging regions.

In total, Global X SuperDividend has 106 different holdings, including popular FTSE 100 stocks M&G and Phoenix.

Be mindful, though, that a high weighting of financial services stocks may impact performance during economic downturns.

NextEnergy Solar Fund: 13.8% dividend yield

Renewable energy producers like NextEnergy Solar Fund (LSE:NESF) can be among the most stable dividend shares out there.

Electricity demand remains pretty inelastic across the economic cycle, giving predictable cash flows across the economic cycle. Profits can dip during periods of unfavourable weather, but largely speaking these companies are pretty reliable for passive income.

NextEnergy holds particular appeal for me given weather-related uncertainties. It has 101 solar assets spread across nine countries, a diversified footprint that helps compensate for poor conditions in certain places.

This has supported consistent growth in annual dividends since NextEnergy listed in 2014. Encouragingly, the investment trust is increasingly focusing on battery storage to diversify revenue streams and further reduce the weather factor, too.