How much do you need to invest in the FTSE 250 to aim for a £5,000 passive income?

Zaven Boyrazian crunches the numbers to show how much money investors need to start earning £5,000 passively using the FTSE 250 index.

Posted by Zaven Boyrazian, CFA

Published 15 September

When investing, your capital is at risk. The value of your investments can go down as well as up and you may get back less than you put in.Read More

The content of this article is provided for information purposes only and is not intended to be, nor does it constitute, any form of personal advice. Investments in a currency other than sterling are exposed to currency exchange risk. Currency exchange rates are constantly changing, which may affect the value of the investment in sterling terms. You could lose money in sterling even if the stock price rises in the currency of origin. Stocks listed on overseas exchanges may be subject to additional dealing and exchange rate charges, and may have other tax implications, and may not provide the same, or any, regulatory protection as in the UK.

The FTSE 250‘s predominantly known as the UK’s leading growth index. Yet, it’s also home to a wide range of generous dividend-paying stocks as well. In fact, right now, there are more than 60 stocks with a yield of 5% or more.

Obviously, not all of these passive income opportunities will turn out to be winning investments. But every once in a while, it’s possible to discover a hidden gem that other investors have overlooked.

Should you buy NextEnergy Solar Fund Limited shares today?

Before you decide, please take a moment to review this report first. Despite ongoing uncertainties from Trump’s tariffs to global conflicts, Mark and his team believe many UK shares still trade at substantial discounts, offering savvy investors plenty of potential opportunities to learn about.

So for investors considering snapping up some FTSE 250 dividend stocks today, how much money do they need to invest to start earning a £5,000 passive income?

Crunching the numbers

Right now, the FTSE 250 index as a whole offers a total average yield of 3.4% – slightly higher than the FTSE 100. That means any investor relying on index funds will need to have a total of £147,059. But for stock pickers, the capital requirements might be significantly less.

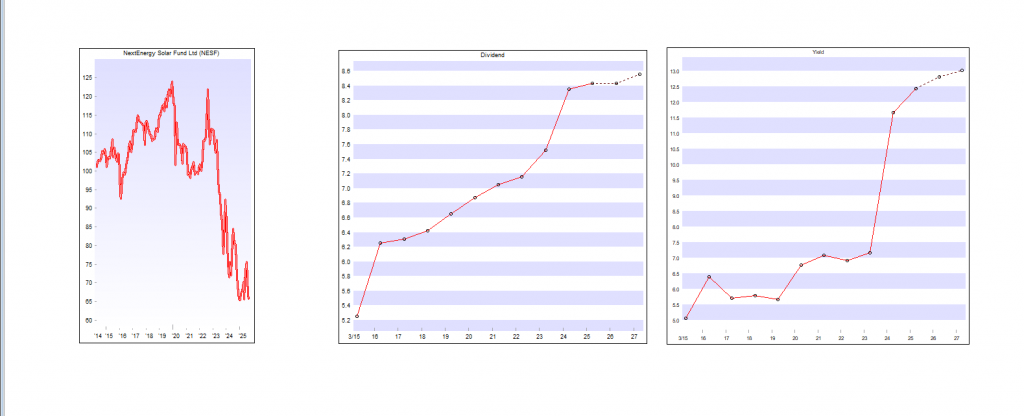

Take NextEnergy Solar (LSE:NESF) as a prime example to consider. The renewable energy enterprise currently has the largest yield in the index at 12.7%! At this rate of payout, the amount of capital needed to earn £5,000 passively drops to just £39,370. That’s still a pretty chunky lump sum, but it’s far quicker to build up with compounding compared to almost £150,000.

Yet, sadly, high yields aren’t guaranteed. And if NextEnergy can’t maintain this generous dividend scheme, buying shares today could lure investors into a trap that destroys wealth rather than creates it. With that in mind, let’s take a deeper dive into the FTSE 250 business.

Investigating the yield

When it comes to dividend sustainability, NextEnergy Solar has quite a favourable business model. The group owns and operates a diverse portfolio of solar farms based mainly in the UK. These assets generate clean electricity, which is sold to the energy grid, generating a recurring inflation-linked revenue stream.

Having said that, solar farms only generate electricity when the sun’s shining. So far in 2025, the weather’s been quite favourable, resulting in above-budget energy generation. But that’s not always the case, and it remains a perpetual risk that investors must consider.

Nevertheless, even with this constant fluctuation, management’s prudent approach to capital allocation has translated into 10 years of continuous dividend hikes. And looking at the latest operating update, the company’s aiming to maintain the current shareholder payout at 8.43p per share.

In other words, so long as there aren’t any unexpected surprises, today’s double-digit yield looks like it’s here to stay. But if that’s the case, why aren’t more investors capitalising on this passive income opportunity?

What could go wrong?

Investor sentiment surrounding renewable energy stocks in 2025 is pretty weak. Like many of its peers, NextEnergy Solar has a chunky 48.5% gearing ratio driven by a high debt burden and preference shares. And in a higher interest rate environment, that can be problematic.

So far, that’s still manageable. But with long-term forecasts pointing towards a downturn in energy prices, dividends may have to be sacrificed to keep its financial obligations under control. Therefore, this isn’t a FTSE 250 stock I’m rushing to buy right now. Instead, my focus is on other investing opportunities.