I was buying more SEIT at 40p last week at a £432m market cap, I’ve been deep diving it further too. Even taking a foray into the chattersphere. Where I find the OB is the topic of conversation.

“The OB is losing it” says one “he’s a ramper” declares another – ah the poisonous crowd in the chattersphere – “He makes broad brush estimates” and “doesn’t really understand the accounting in SEIT…. his analysis is superficial”.

I rarely visit the chattersphere but when I do I’m reminded of why I don’t.

Interesting to see that SEIT’s portfolio gross value has grown over time. There is no collapse to the valuation, compared with the share price. The assets are actually very resilient.

SEIT

The reduction in the RCF with an interest cost of 6.4% saves over £9m interest per year.

How? £133m x 6.4% = £8.5m per annum vs the interest cost in 1H26 of £9m so £18m annualised. Are there some additional costs such as amortisation of arrangement costs in that £9m… perhaps, but £m’s per year? I doubt it.

We know that the “Big 5” are 66% of the Portfolio value in £m terms but delivered 75% of the EBITDA in 1H26 and 2H25 – and an even greater proportion in 1H25 (Oliva was a drag more recently) so losing about a quarter of the “Non Big 5” is an 6% reduction of EBITDA pro rata (25% of 25% is 6% right?), so about a -£4.5m reduction of EBITDA.

So even with costs and the discount taken into account the effect is up to ~£5m net positive for the Fund’s ongoing cash income (excluding one-off costs), implying up to 8% boost to net cash after interest costs from £43m to nearer £48m, even based on a static performance (which appears to be anything but static).

The positive news flow from Primary Energy (Nippon Steel is investing $3bn into US Steel) and Red Rochester (25% growth due to new customers) alongside Driva (Sweden) and Oliva (Spain) being beneficiaries to the current troubles for more expensive European energy there’s reasons to believe Cash Flows from the Big 5 will have grown in FY26 and will have a far brighter outlook for FY27.

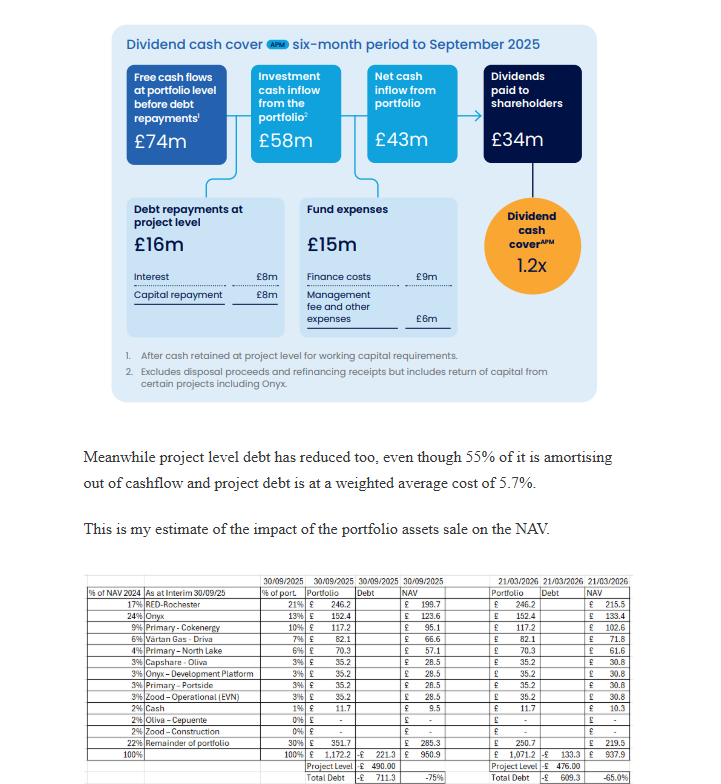

Meanwhile project level debt has reduced too, even though 55% of it is amortising out of cashflow and project debt is at a weighted average cost of 5.7%.

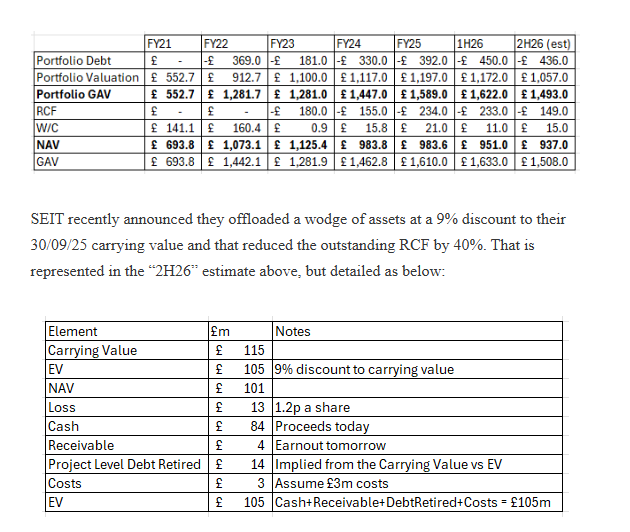

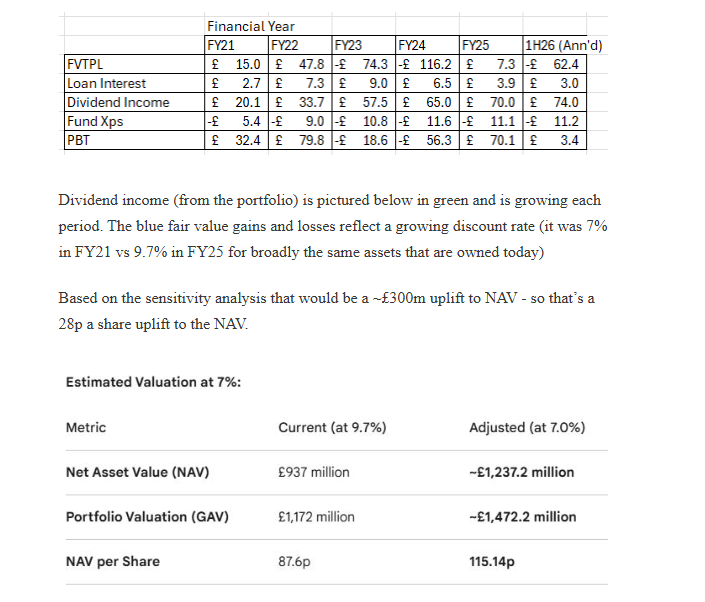

This is my estimate of the impact of the portfolio assets sale on the NAV.

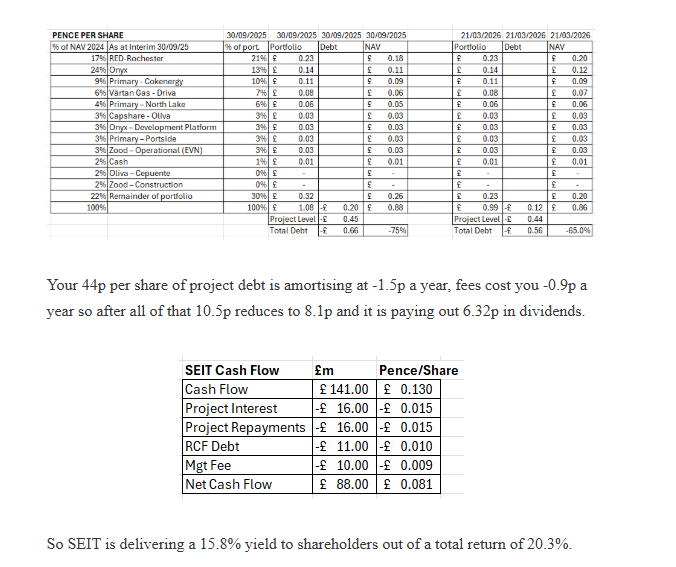

On a pence per share you’re paying 40p a share to own about 132p of real assets less the equivalent of -56p of debt so 40p gets you 86p of net assets.

132p of real assets generate 13p of cash (historically) of which -2.5p gets paid going forwards on interest leaving 10.5p cash earnings.

Your 44p per share of project debt is amortising at -1.5p a year, fees cost you -0.9p a year so after all of that 10.5p reduces to 8.1p and it is paying out 6.32p in dividends.

So SEIT is delivering a 15.8% yield to shareholders out of a total return of 20.3%.

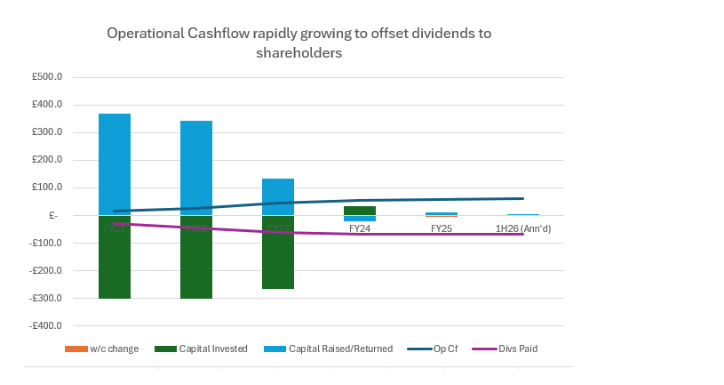

If you look at the Fund’s income and expense the growing income from holdings is apparent too. The green line shows growing dividend income. It’s true that the blue bars are reductions through fair value losses – through rising discount rates (an eyewatering 9.7%) and falling power curves.

Power Curves in 2026 are definitely rising again since the Iran conflict erupted and 65% of income is index-linked. All of that is positive for the NAV – and the attractiveness of its assets.

If you consider the growing income from the portfolio (dividend income and loan interest income) below, and then contrast that with the fair value gains and losses you can see a clear disconnect between the trajectory of each. Why do assets with a lower fair value deliver growing income? Does that actually make sense?

Dividend income (from the portfolio) is pictured below in green and is growing each period. The blue fair value gains and losses reflect a growing discount rate

Regards

The Oak Bloke

Disclaimers:

This is not advice – you make your own investment decisions.

Micro cap and Nano cap holdings including REITs might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”.

Thanks for reading! Subscribe for free to receive new posts and support my work.

Pledge your support

The Oak Bloke’s Substack is free today. But if you enjoyed this post, you can tell The Oak Bloke’s Substack that their writing is valuable by pledging a future subscription. You won’t be charged, unless they enable payments, and you decide to continue with a subscription.

Leave a Reply