Foresight Solar, the fund investing in solar and battery storage assets to generate income and deliver long-term growth, announces its unaudited net asset value (NAV) was £517.9 million at 30 June 2026 (31 March 2026: £543.0 million). This results in a NAV per ordinary share of 94.9 pence (31 March 2026: 99.2 pence).

Summary of key changes to NAV

Item

p/share movement

NAV on 31 March 2026

99.2p

Interim dividends paid

-2.0p

Time value

+1.9p

Discount rate adjustment

-1.4p

Inflation assumptions

+0.9p

Project actuals

-1.3p

Power price forecasts

-1.1p

Carbon Price Support (CPS) removal

-0.5p

Share buyback programme

+0.1p

Other movements

-0.9p

NAV on 30 June 2026

94.9p

Inflation assumptions

UK inflation assumptions also moved higher, with RPI and CPI now expected to be 3.5% and 3.0% in 2027, respectively. From 2028 to 2030, RPI is forecast at 3.0% and CPI at 2.5%, before easing to 2.4%1 and 2.25%, respectively, from 2031. The updated assumptions added 0.9pps to NAV.

Project actuals

Project actuals reduced NAV by 1.3pps, primarily reflecting the timing of cash receipts, payments and power price hedging settlement related to the UK portfolio, as well as lower-than-budgeted generation in Spain and Australia during the second quarter.

Power price forecasts

Updated forecasts from independent market consultants reflected lower near-term power price expectations across Foresight Solar’s markets, following an easing of geopolitical risk during the period, as well as wider UK solar capture price discounts in the long term. Overall, this reduced NAV by 1.1pps.

CPS removal

The UK government announced earlier this year that it will remove the Carbon Price Support mechanism from April 2028. The move is intended to reduce wholesale electricity prices for consumers and industry in the medium term. The change reduced NAV by 0.5pps, in line with the Company’s estimate of between 0.5pps and 1.0pps disclosed at the time of the government’s announcement.

Share buyback programme

Foresight Solar continued to buy back its shares, adding 0.1pps to NAV in the second quarter of 2026. More than £56 million of the £60 million programme has been deployed, delivering a cumulative NAV uplift of 3.4pps since repurchases began.

Other movements

Other movements, including foreign exchange, working capital movements and minor portfolio adjustments, resulted in a net negative impact of 0.9pps.

Independent valuation

Given the persistent share price discount to NAV and the limited number of recent comparable market transactions, the Board commissioned an independent third party to undertake a review of the valuation of the Company’s UK operational solar portfolio. The review considered the valuation methodology, key assumptions and supporting market evidence, and concluded that the valuation is within a reasonable range of fair values.

Trading update

Above-budget production in the UK was partly offset by higher-than-expected curtailment in Spain and below-forecast irradiation in Australia. Overall, global production for the quarter was 3.6% under budget, with solar resource 4.7% above expectations.

In the six months to 30 June 2026, global portfolio generation was 5.6% lower than forecast and irradiation was marginally above budget.

Taking advantage of the macro environment, the investment manager continued to actively manage the Company’s power price hedging strategy. Global contracted revenues are now 84% for 2026, 82% for 2027 and 64% for 2028 of forecast total revenues for each year, with average UK prices at £75.48/MWh, £72.14/MWh and £75.05/MWh for those years, respectively.

Since the end of the second quarter, UK day-ahead electricity prices have risen in reaction to consecutive heatwaves, low wind output and tighter gas markets. Middle East tensions have added pressure to natural gas prices. Solar generators are likely to benefit from these factors, as well as from the sunniest month on record in July, according to the Met Office.

Gearing

The gross asset value (GAV) on 30 June 2026 was £908.0 million (31 March 2026: £931.5 million), with total outstanding debt of £390.1 million, which represented 43.0% of GAV (31 March 2026: £388.5 million and 41.7%) – comfortably within the 50% limit. The modest increase in gearing reflects seasonal working capital requirements.

Interim results date

Foresight Solar expects to publish its interim results for the six months to 30 June 2026 on 15 September 2026. A Notice of Results with more details will be released in due course.

The SNOWBALL bought VPC special lending investments (VSL)

10K on the 28/04/23. VPC paid dividends at a yield of 10%.

They then decided to wind up the trust and the brown stuff hit the fan, currently showing a loss on capital of £4,704.00.

They have returned £4,002 in dividends and return of capital, this has been re-invested back into the portfolio. If the SNOWBALL had re-invested back into VPC the loss would have been greater, one reason to be wary if you CPA.

The cash re-invested has earned around 1k in dividends, and VPC are still paying two dividends a year and trade at a 50% discount to NAV, most of this discount may be eaten up in costs so the final figure may be around another 1k of income. If you deduct the 2k, the loss is now around 2.7k. It will take around another 6 years of dividend income from the re-invested income, after that it will be all profit. When VPC finally winds up, the returned cash will be re-invested back into the SNOWBALL.

If you buy a share and it turns out to a clunker just after you bought, you should sell and try to learn what was wrong with the buy. The more you trade, the more chances, one day, you will buy a clunker.

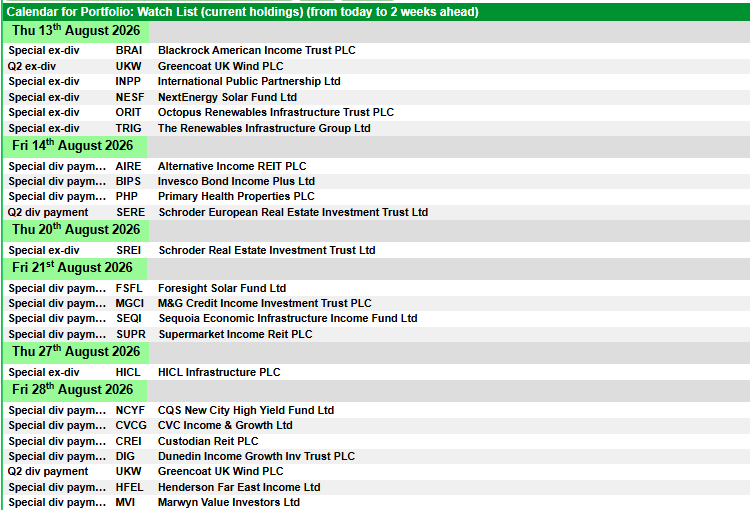

Baillie Gifford UK Growth Trust PLC ex-dividend date BlackRock American Income Trust PLC ex-dividend date Greencoat UK Wind PLC ex-dividend date ICG Enterprise Trust PLC ex-dividend date International Public Partnerships Ltd ex-dividend date Majedie Investments PLC ex-dividend date NextEnergy Solar Fund Ltd ex-dividend date Octopus Renewables Infrastructure Trust PLC ex-dividend date Pershing Square Holdings Ltd ex-dividend date Renewables Infrastructure Group Ltd ex-dividend date Rentokil Initial PLC ex-dividend date Scottish American Investment Co PLC ex-dividend date Target Healthcare REIT PLC ex-dividend date Tritax Big Box REIT PLC ex-dividend date

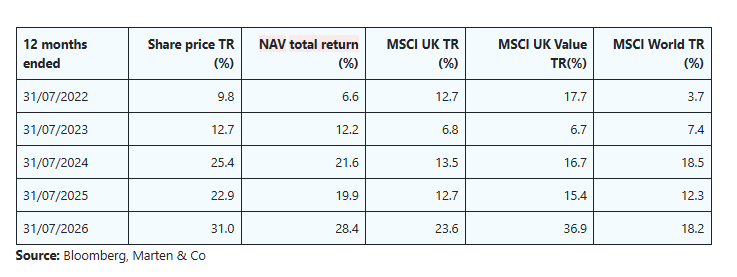

Temple Bar (TMPL) turned 100 earlier this year but shows no signs of slowing down. Its one-, three-, and five-year returns are at or near the top end of its peer group, the dividend continues to climb, and the managers continue to swim against the tide, finding interesting and attractively valued stocks in a UK equity market that is itself cheap relative to peers.

The composition of TMPL’s portfolio is always evolving. The managers are taking profits from financials, adding formerly highly-rated consumer staples stocks, and assessing opportunities in IT services. This cycle of portfolio renewal provides the foundation for future outperformance. Long may it continue.

UK equity income and capital growth

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities, with the majority typically selected from the FTSE 350 Index.

TMPL aims to provide growth in income and capital to achieve a long-term total return greater than its benchmark (the FTSE All-Share Index), through investment primarily in UK securities. The company’s policy is to invest in a broad spread of securities with most holdings typically drawn from the FTSE 350. We have substituted the MSCI UK Index for the FTSE All-Share in this note.

TMPL’s AIFM is Frostrow Capital LLP, and it has delegated responsibility for portfolio management to RWC Asset Management LLC (Redwheel). Redwheel has been managing the trust since 1 November 2020. The lead managers are Nick Purves and Ian Lance (see page 16).

Looking for a disconnect between share prices and underling intrinsic value

Their investment approach is based on the principle that investors tend to overreact to news, becoming overly bullish or overly pessimistic about the prospects for companies and markets. This creates a disconnect between the intrinsic value of a company and its share price, which long-term, value-driven investors can take advantage of as sentiment swings back in their favour.

Avoiding value traps by favouring good quality companies

Care needs to be taken to avoid “value traps” – businesses which look cheap but are in structural decline. Instead, the managers target undervalued but good-quality companies (those with strong cash flows and robust balance sheets). These businesses are better able to withstand cyclical downturns and recover from short-term, company-specific issues. The approach recognises that aspects of ESG can have a profound impact on a company’s long-term success.

TMPL has given the managers the flexibility to invest up to 30% of the portfolio in overseas stocks. The chair noted in his most recent statement that the board and manager monitor the size of the investment universe, particularly as the UK market shrinks through takeovers and a lack of issuance. The board is monitoring the situation with a view, if necessary, to asking shareholders to increase that 30% limit.

Recent data published by Peel Hunt and E&Y highlighted that there were 28 proposed takeovers of UK companies with a total value of £59.7bn over H1 2026, which compares to seven listings raising £577m. However, for the moment, the managers believe that they have a large enough opportunity set within the UK to meet the objective.

Value works – just look at the past 100 years

100 years old on 24 June 2026

On 24 June 2026, TMPL was 100 years old. That means it has survived the Wall Street Crash, the second World War (and many others since), 70s inflation, 80s recession, the tech boom and bust, the 2008 financial crisis, and COVID and its aftermath. The trust has not always had a value focus – at launch it was “The Cable, Telephone and General Trust” – but whilst it did not adopt its current name until 1977, it already had a UK equity income focus by then. TMPL’s focus on dividend yield makes it a value investor.

At this year’s AGM and in a separate video on the subject, Redwheel took the opportunity to look at the long-term case for value investing.

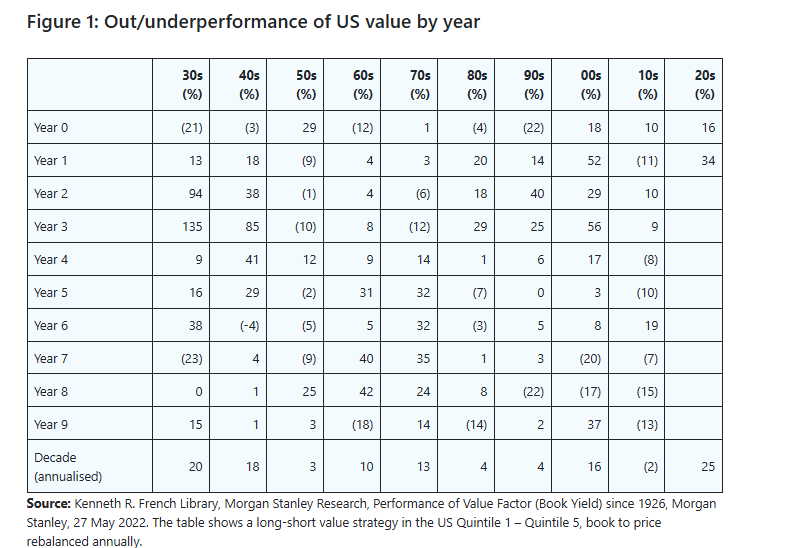

Over almost a century, value outperformed in every decade bar one

Figure 1 is taken from the video and shows the annual returns of US equities, based on holding stocks that look cheaper than market averages on a book to price basis (the inverse of price to book, which is perhaps the more normal way of looking at this) and shorting the more expensive ones, over the 92 calendar years to the end of 2022. This value approach does not outperform every year, but it is a winning strategy over every decade bar the 2010s, when governments and central banks manipulated interest rates to unsustainably low levels.

Figure 1: Out/underperformance of US value by year

Source: Kenneth R. French Library, Morgan Stanley Research, Performance of Value Factor (Book Yield) since 1926, Morgan Stanley, 27 May 2022. The table shows a long-short value strategy in the US Quintile 1 – Quintile 5, book to price rebalanced annually.

Figure 2: Long-run cumulative performance from low- and high-yielding stocks in the UK, 1900-2025

Figure 2 – which is based on the performance of UK value stocks, this time selected on the basis of their dividend yield – reinforces this message. The scale on the y-axis is logarithmic; consistently investing in high-yielding stocks and reinvesting your dividends meant that would have made 21x the return of a portfolio focused on low-yielding stocks over that 125-year period.

Compelling UK valuation opportunity

As Figure 3 shows, UK equities had a good run over 2025, but progress has stalled since the outbreak of war between the US, Israel, and Iran. Fears about the impact of higher energy costs on inflation compounded concerns about the fiscal profligacy of the Labour government, putting upward pressure on UK borrowing costs – as illustrated by UK 10-year gilt yields in Figure 4.

Figure 3: MSCI UK

Source: Bloomberg

Figure 4: UK 10-year gilt yields

Source: Bloomberg

The revolving door at 10 Downing Street may have had some impact on sentiment towards the UK market. However, economically things have been better than some expected. UK GDP growth was 0.6% in Q1 2026 and roughly flat over April and May. UK base rates are unchanged this year. UK inflation, as measured by CPI, came in at 2.6% for the 12 months to the end of June 2026, lower than some had forecasted.

Oil prices surged in March before easing over the next few months as both sides adopted a more conciliatory tone. That weighed on TMPL’s energy stocks, but the managers had taken some profits when share prices spiked following the outbreak of the Iran war.

More recently, renewed hostilities have pushed on oil and gas prices higher again, with stockpiles dwindling, the situation may now be more serious. EU gas prices are hitting new three-year highs, for example.

UK equities remain cheap on a range of valuation multiples

Nevertheless, UK equities remain cheap on a range of valuation multiples when compared to peers, as Figure 5 shows.

Figure 5: Valuation multiples across various markets

P/E (current)(x)

P/E (FY26)(x)

P/E (FY 27) (x)

Price/book (FY26) (x)

EV/EBITDA (FY26) (%)

Dividend yield (FY26) (%)

MSCI UK

15.11

13.45

12.84

2.30

8.41

3.93

MSCI Europe ex UK

18.37

16.96

15.42

2.41

11.59

2.94

MSCI AC Asia ex Japan

19.04

12.13

9.62

2.17

9.30

2.16

MSCI Japan

19.79

17.56

15.60

1.87

9.10

2.12

MSCI USA

25.87

21.59

18.87

5.13

15.37

1.14

Source: Bloomberg as at 31 July 2026

It is often claimed that the reason that UK equities look cheap is the relative absence of stocks in highly-rated sectors such as information technology. However, as Figure 6 shows, UK stocks are cheaper than global averages in almost every sector.

Figure 6: P/E (FY 26) ratios for UK versus global stocks

Source: Bloomberg as at 31 July 2026

A wave of bids for UK companies underscores this sense that UK equities are undervalued. In 2026 we have seen takeover offers for Schroders, easyJet, Rotork, Tate & Lyle, UK Power Networks, Beazley, Intertek, Senior, Mitie, and SEGRO.

Portfolio

At the end of June 2026, there were 40 holdings in TMPL’s portfolio. The average yield on the portfolio at the end of June was 4.1%, which compares to 3.1% for its benchmark. The average current year P/E ratio on the portfolio was 9.7x, which compares to 12.7x for the index and the figures for price/book were 1.2x and 2.0x, respectively.

TMPL’s geographic and sector exposures are driven by the managers’ stock selection decisions and market movements.

Figure 7: TMPL geographic distribution as at 30 June 2026

Source: Temple Bar Investment Trust

Figure 8: TMPL change in geographic distribution since 30 November 2025

Source: Temple Bar Investment Trust

Since we last published, using data as at 30 November 2025, the portfolio has had more exposure to the US and consumer staples, and less exposure to cash and materials.

Figure 9: TMPL sector distribution as at 30 June 2026

Source: Temple Bar Investment Trust

Figure 10: TMPL change in sector distribution since 30 November 2025

Source: Temple Bar Investment Trust

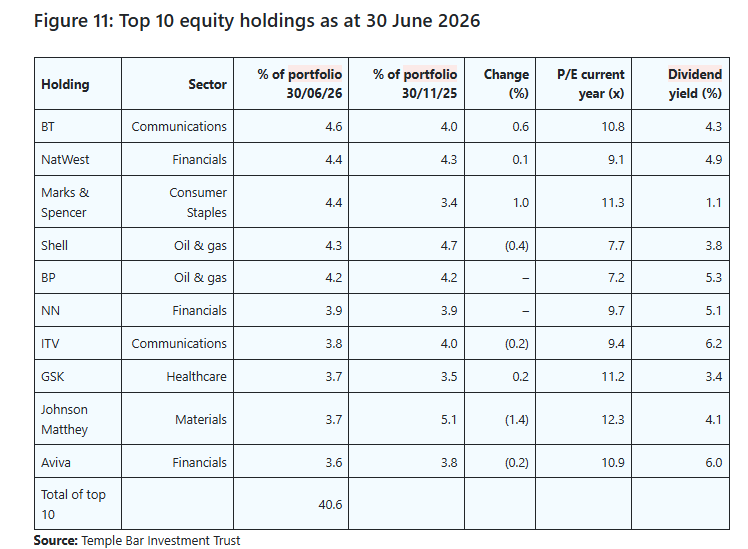

Top 10 holdings

Since we last published using data as at 30 November 2025, Barclays and Smith & Nephew have both dropped out of the list of the 10 largest holdings, to be replaced by Marks & Spencer and GSK.

We have discussed Marks & Spencer in our previous notes (see page 19 for a list of these). Its share price has been volatile, but recent performance has moved it back into the list of the 10 largest holdings.

Last year’s damaging cyber-attack has been put behind it, the store refreshment programme is bearing fruit, and the food division is taking share from rivals. TMPL’s managers highlight 4.6% margins on food for the financial year to the end of March 2026 as particularly pleasing.

TMPL’s managers still see more upside in the share price, which they feel is not yet fully reflecting the evident turnaround in the company.

GSK

GSK has also moved into the top 10 following a recovery in its share price. This is not a fast-growing business, but it is delivering revenue growth of about 3% per annum, which is feeding through into double digit organic earnings growth. TMPL’s managers had felt that positive story was not reflected in its rating.

Figure 13: Barclays price/book (x)

Source: Bloomberg

TMPL’s financials exposure has been a big driver of its recent returns, and the managers have been taking profits from this area. The managers observe that almost everything has gone right for TMPL’s bank holdings, for example. Even a couple of years ago, these stocks were very lowly rated. However, rising interest rates opened up net interest margins, costs have been taken out – latterly with the help of AI (there is more to go for on this front), and loan losses have been kept under control.

However, another significant factor in the re-rating of financials stocks has been the considerable share buybacks that these companies have undertaken, which is feeding through into their EPS growth.

Diageo and other consumer staples

Figure 14: Diageo (GBp)

Source: Bloomberg

One sector that Redwheel has been adding to is consumer staples. The managers observe that this is an area that was once the highly-rated preserve of growth-style managers, but a severe de-rating has brought many of these companies into TMPL’s orbit. Stocks in the portfolio include Kraft Heinz, Carrefour, J.M. Smucker, and Diageo.

Diageo’s derating has been savage, with the shares more than 60% below their peak. New CEO, Sir Dave Lewis (ex-Tesco) joined at the start of 2026. One part of his turnaround plan for the company was to halve the dividend, conserving cash to invest in leading brands. He is also focused on cutting costs, decentralising the business to make it more dynamic, refreshing the leadership team, and selling off non-core assets.

Guinness (and Guiness Zero) is delivering sales growth, as is its emerging markets business. However, TMPL’s managers are unsure whether falling spirits sales in North America reflect a structural trend for the drinks industry rather than a stock specific or cyclical issue. That uncertainty is reflected in the position size.

BP

Figure 15: BP (GBp)

Source: Bloomberg

BP is another self-help story in the portfolio. Aside from the impetus given to the stock by the recent oil price increases, the main catalyst has been the shake-up led by its new CEO, Meg O’Neill, who took over on 1 April 2026. Meg was previously CEO of Woodside Petroleum and prior to that spent over 20 years at ExxonMobil. The TMPL managers have met her and were impressed.

TMPL’s managers believe that a key priority will be to unwind the low-return energy transition investments the company made under Bernard Looney (who was the CEO between 2020 and 2023). That process is already underway, and disposals will be used to reduce debt. There is also a need to stabilise the ship after a run of changes at the top of the company, including the recent dismissal of its chair.

ITV

In September 2020, when we wrote about ITV in our first note on TMPL, we commented that TMPL’s managers felt that all of the company’s market capitalisation could be accounted for by its studios business, and in their view, the broadcast business was “in for free”. On 6 July 2026, Sky announced that it would pay up to £1.6bn for ITV’s media and entertainment business. Surprisingly, ITV’s share price fell on the day and is currently lower than it was back in September 2020. It is hard to fathom why this might be, but TMPL’s managers suggest that investors might be unwilling to price in a deal that looks unlikely to complete before H2 2027. In the meantime, it may be that a soon-to-be standalone studios business attracts attention from another bidder; Netflix, for example.

Software and IT services

TMPL has very little exposure to the IT sector currently, but recent falls in the share prices of software and IT stocks have encouraged the managers to have a closer look at some of these companies.

For the moment, the software-as-a-service stocks that have seen sharp share price falls are still too highly-rated to be attractive to TMPL. However, amongst the IT services stocks, many are now on low double-digit or even single-digit earnings multiples. The analyst team is delving into some of these names in more detail.

Performance

Figure 16: Total return performance over periods ending 31 July 2026

3 months (%)

6 months (%)

1 year (%)

3 years (%)

5 years (%)

TMPL share price

8.8

11.6

31.0

101.9

149.8

TMPL NAV

8.5

10.8

28.4

87.2

124.0

MSCI UK

5.2

8.5

23.6

58.1

90.3

MSCI UK Value

8.8

13.1

36.9

84.4

131.6

MSCI World

5.2

9.8

18.2

57.4

75.4

Peer group1 NAV median

7.5

8.6

19.6

49.7

61.4

Peer group1 share price median

8.4

8.3

21.2

44.9

64.1

Source: Bloomberg, Marten & Co. Note: 1) The constituents of the peer group are listed below

TMPL’s three-year and five-year returns remain comfortably ahead of its benchmark and, as we discuss below, peer group averages.

TMPL’s returns relative to the MSCI UK Value Index are skewed by the high levels of concentration within that index. At 30 June 20216, HSBC was 19.1% of the index, Shell 12.8%, Unilever 7.7%, and BAT 7.3%, which limits its usefulness as a comparator. HSBC’s share price is up about 70% over the past 12 months.

TMPL’s impressive recent track record owes much to its financials exposure, which we discussed on page 9. Redwheel says that notable contributions to TMPL’s returns have come from stocks such as Standard Chartered, Barclays, NatWest, and Aberdeen Group.

Figure 17: Temple Bar NAV relative to MSCI UK (sterling total return) to 31 July 2026

Source: Bloomberg, Marten & Co

WPP

Figure 18: WPP (GBp)

Source: Bloomberg

The only meaningful detractor from returns has been WPP; however, this is a stock that the managers feel has a lot of potential. Under Martin Sorrell, WPP was built – through a series of acquisitions – into one of the world’s largest advertising agencies and the leading media buyer. A market cap that peaked at around $30bn is now around $4bn. While other big global advertising agencies have been seeing modest top line growth, WPP has seen like-for-like revenue falls over the past couple of years and that is feeding through into declining EPS. TMPL’s managers see this as a sign that WPP’s problems are specific to it rather than a structural issue with the industry.

A new CEO – Cindy Rose, ex Microsoft – took on the job in September 2025. TMPL’s managers have met her and believe that she can turn WPP around. They think it may help that she has a background in technology. One obvious issue is that the individual businesses within WPP were not integrated and often ended up competing with each other for the same business. There is scope to take out complexity and cost from the business, which should help improve cost control.

It might be enough to simply stabilise the business. The managers say that the market is valuing WPP on about 5x earnings, whereas a rating of 10x might be ascribed to a stable business. If the new CEO can grow earnings on top of this – TMPL’s managers think organic revenue growth of 3% p.a. over the medium term, with an operating profit margin of 16~17% is achievable – then the potential for a rerating is considerable.

Redwheel is a significant shareholder in WPP, with about 10% of the company held across its range of funds and mandates, and is content to give the new CEO room to deliver on her planned transformation of the company.

Peer group

You can find up-to-date information on TMPL and its peers on our website

TMPL is one of the larger of the 16 funds in the AIC’s UK equity income sector, and its running costs are below the sector median. The shift to an enhanced dividend helped move TMPL’s yield closer to the sector median. TMPL’s strong long-term track record – which is evident in Figure 19 – is reflected in its rating and regular share issuance.

Figure 19: Snapshot of UK equity income sector as at 31 July 2026

Premium/ (discount) (%)

Yield (%)

Ongoing charges (%)

Market cap (£m)

Temple Bar Investment Trust

1.3

3.7

0.59

1,283

Aberdeen Equity Income Trust

1.5

5.0

0.84

367

BlackRock Income and Growth

(13.0)

3.4

1.15

42

Chelverton UK Dividend Trust

(6.6)

7.0

2.25

32

CT UK Capital and Income

(4.2)

3.6

0.66

334

CT UK High Income

(3.2)

5.1

1.03

105

Dunedin Income Growth

(7.8)

6.1

0.57

368

Edinburgh Investment Trust

(7.6)

3.8

0.52

1,057

Finsbury Growth & Income

(6.5)

2.5

0.62

805

JPMorgan Claverhouse

(1.4)

3.7

0.62

530

Law Debenture Corporation

1.9

2.9

0.56

1,668

Lowland Investment Company

(9.0)

3.6

0.71

400

Murray Income Trust

(6.2)

4.0

0.48

952

Schroder Income Growth Fund

(5.7)

4.0

0.78

242

The City of London Investment Trust

2.0

3.7

0.36

3,057

The Merchants Trust

(5.1)

4.5

0.54

983

Peer group median

(5.4)

3.8

0.62

465

TMPL rank

4/16

10/16

7/16

3/16

Source: QuotedData website

TMPL’s long-term track record is good, ranking at the top end of the table over most time periods. That reflects the success of its value-driven approach. Many trusts drifted away from value investing over the period when the style was underperforming. Many of those that focused on “quality” instead were exposed to software stocks caught in the agentic AI sell off earlier this year (most notably Finsbury Growth & Income).

Those that have a bias to small-cap stocks have also been laggards in recent years.

Figure 20: Total return NAV performance over periods ending 31 July 2026

3 months (%)

6 months (%)

1 year (%)

3 years (%)

5 years (%)

Temple Bar Investment Trust

8.5

10.8

28.4

87.2

124.0

Aberdeen Equity Income Trust

8.9

12.4

32.9

74.2

63.9

BlackRock Income and Growth

5.6

4.0

15.3

38.6

55.0

Chelverton UK Dividend Trust

7.9

7.8

10.5

25.4

(7.5)

CT UK Capital and Income

6.2

4.9

10.2

39.1

36.8

CT UK High Income

7.1

7.2

20.6

61.1

54.5

Dunedin Income Growth

7.5

7.8

12.3

27.5

33.3

Edinburgh Investment Trust

7.6

7.8

10.4

41.6

68.1

Finsbury Growth & Income

6.2

7.1

(9.9)

(1.0)

2.4

JPMorgan Claverhouse

8.1

9.4

22.2

61.6

68.6

Law Debenture Corporation

6.5

10.2

24.6

70.9

93.6

Lowland Investment Company

9.4

10.7

29.4

73.7

77.5

Murray Income Trust

10.3

11.4

18.5

33.4

38.6

Schroder Income Growth Fund

6.8

7.0

18.7

50.3

58.9

The City of London Investment Trust

7.5

10.3

24.9

70.0

92.6

The Merchants Trust

11.6

10.2

24.9

49.0

79.3

Peer group median

7.5

8.6

19.6

49.7

61.4

TMPL rank

5/16

3/16

3/16

1/16

1/16

Source: Bloomberg, Marten & Co

Enhanced dividend

TMPL pays dividends quarterly. Since the AGM in 2025, it has used reserves to top up the dividend that it would have paid from net revenue earnings by an additional 3p per annum (0.75p per quarter). This represents a contribution to payouts in lieu of the money that companies have been spending on buying back shares rather than maximising their dividend payout ratio. In the last annual report, the chair observed that according to Computershare’s UK Dividend Monitor, share buybacks represented 42.1% of the total distributions by UK listed companies in 2025.

That change in policy is reflected in the step change in the dividend for 2025 over 2024. The chair has cautioned that the pace of TMPL’s dividend growth going forward is unlikely to match the significant increases seen in the past few years.

The dividend target for the current financial year is 15.6p, payable in four instalments of 3.9p. This represents a 4% increase on the dividend for 2025.

Figure 21: TMPL’s recent dividend record

Source: Temple Bar Investment Trust

Premium/(discount)

Figure 22: TMPL discount over five years ended 31 July 2026

Source: Bloomberg, Marten & Co

As investors became more convinced of TMPL’s ability to outperform over the long term and memories of the extended period of underperformance from value strategies faded, the shares re-rated over the course of 2025. Over the 12-month period that ended on 31 July 2026, TMPL’s shares have traded between a discount of 10.7% and a premium of 1.8%, averaging a discount of 4.6%. As of publishing, the company was trading on a premium of 1.3%.

The board is committed to an active policy to manage TMPL’s share price relative to its NAV

The board is committed to an active policy to manage TMPL’s share price relative to its NAV. That includes both issuing shares at a premium as well as buying back shares at a discount. Both have the effect of enhancing the NAV for ongoing shareholders. At the AGM on 5 May 2026, shareholders authorised the directors to issue up to 20% and buy back up to 14.99% of the then shares in issue.

Over the past 12 months, thanks to strong demand, particularly from retail investors, no shares have been repurchased, and 21.13m shares have been reissued from treasury.

Figure 23: Shares issued and repurchased

Source: Temple Bar

Gearing and hedging

TMPL has a £50m 4.05% private placement loan which is repayable on 3 September 2028, and a £25m 2.99% private placement loan which is repayable on 24 October 2047. The two loans are secured by a floating charge over the assets of the company. TMPL’s net gearing was 3.7% as of 31 May 2026.

TMPL does not currently hedge its currency exposure.

Financial calendar

The trust’s year-end is 31 December. The annual results are usually released in March (interims in September), and its AGMs are usually held in May of each year. TMPL pays quarterly dividends in April, June, September, December each year.

SWOT and Bull versus bear analysis

Figure 25: SWOT analysis for TMPL

Strengths

Weakness

Good performance track record in both NAV and share price terms, over the medium-to-long term.

As a fund with a clear focus on value investing in the UK market, TMPL is exposed to a shift in investor sentiment, which could depress returns even with good stock picking.

Rebuilding its track record of progressive dividend payments, helped by a change in policy of enhancing the payout through its distributable reserves, reflecting the importance of share buybacks by its portfolio companies.

Opportunities

Threats

Despite a strong 2025, the UK market remains undervalued when compared to peers. TMPL’s stocks are even cheaper than the UK market average.

A more pronounced deterioration in the UK economy or renewed concerns about UK government finances could unnerve investors.

The current environment of higher for longer inflation and interest rates is better suited to value rather than growth stocks.

The market is becoming less convinced of the AI capex trade.

Source: Marten & Co

Figure 26: Bull versus bear analysis for TMPL

Bull

Bear

Performance

TMPL can boast strong performance – at or close to the top of peer group tables over one, three and five years.

The period since the outbreak of war in the Gulf has been less favourable to TMPL.

Dividends

Payouts to shareholders have risen every year for five years and we see no reason why this trend should not continue. This is supported by TMPL’s policy of enhancing these through distributable reserves.

There is no guarantee of these increases being maintained, if payouts and buybacks from the underlying companies come under pressure.

Outlook

UK stocks remain undervalued relative to peers and the economic environment ought to be favourable, provided that the new UK government does not jeopardise this.

Both value investing and the UK market could move out of favour with investors, potentially quickly.

Discount

TMPL moved to a premium during 2025 and has been reissuing stock at a small premium (which is beneficial for existing investors).

Sentiment might turn against value investing once again (although we see nothing on the horizon currently to trigger that).

A big price drop can create opportunity only if the company’s future cash flows haven’t deteriorated as much.

Cameco has multiple growth engines through uranium production, fuel services, and its Westinghouse stake.

Even after the selloff it’s not cheap, so expect volatility and consider buying in gradually.

A stock can lose one-third of its value without losing one-third of its business. That uncomfortable gap has opened at one of Canada’s most important energy companies, turning a market darling into a far more interesting long-term candidate. So, let’s look into that one stock and what to consider.

Considerations

A falling price doesn’t automatically create value. Sometimes the market is removing a premium that never belonged there. Investors buying during a stock market correction should therefore ask whether the company’s future cash flows weakened as quickly as its shares.

That question becomes especially useful in nuclear energy. Reactors take years to approve and build, uranium mines can take even longer, and neither supply chain responds quickly when demand rises. The International Energy Agency says support for expanding nuclear power now exists in more than 40 countries as electricity demand from data centres, artificial intelligence, and electrification climbs.

A decades-long investment therefore needs more than exposure to today’s uranium price. It should own scarce deposits, long customer contracts, fuel-processing capabilities, and technology that earns money from the reactors themselves. Very few public companies bring that entire nuclear toolbox to the job.

A nuclear company with several engines

Cameco (TSX:CCO) mines uranium from major Canadian and international operations, converts and manufactures nuclear fuel, and owns 49% of Westinghouse. Westinghouse supplies reactor technology, parts, engineering, and maintenance to utilities, placing Cameco stock on both sides of the nuclear renaissance.

Westinghouse technology is used by 57% of the global operating reactor fleet, while the company is pursuing as many as 91 AP1000 reactor opportunities. Each new reactor could create equipment and service revenue for Westinghouse, followed by decades of uranium and fuel demand. Nuclear plants are not known for impulse purchases.

Into earnings

Cameco stock’s second quarter looked considerably less magnificent. Net earnings fell to $25 million, while adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) dropped to $391 million. Lower deliveries, operational disruptions, and the absence of a large Westinghouse project contribution from the prior year hurt the comparison.

The wider picture held up better. First-half uranium adjusted EBITDA increased to $676 million from $641 million, supported by improving realized prices. Management maintained its 2026 uranium-production outlook and has contracts covering average annual deliveries of more than 28 million pounds through 2030. Cameco stock also increased its ownership of the tier-one Cigar Lake mine.

Why the 28% drop deserves attention

Cameco stock reached an all-time high of $182.72 on January 29. Its July 31st close of $132 represents a decline of about 28%. Also worth considering? Shares are up about 5% in the last week at writing. Yet while the retreat offers a better entry point into one of the strongest Canadian materials stocks, “better” shouldn’t be mistaken for “cheap.”

The shares still trade near 60 times forward earnings. That valuation assumes years of nuclear growth, stronger uranium pricing, and successful Westinghouse execution. Mine disruptions, reactor delays, weaker commodity prices, cost overruns, or changing government policy could send the stock lower again.

Foolish takeaway

I’d build a Cameco stock position gradually rather than attempt to identify the precise bottom. Its balance sheet ended June with $1.1 billion in cash against $1 billion of debt, providing room to manage the next operational surprise without passing around a financial collection plate.

The next quarter may remain lumpy, and the next year could be volatile. The more useful horizon is measured in reactor lives. If global nuclear capacity keeps expanding, Cameco stock’s mines, contracts, fuel services, and Westinghouse stake could make today’s 28% selloff look like an early chapter in a much longer growth story.

NET ASSET VALUE AND PORTFOLIO VALUATION UPDATE TO 30 JUNE 2026

Unaudited NAV total return for the quarter of 0.4%

Resilient portfolio well-placed to continue to provide secure, index-linked income with the potential for capital growth

The Board of Directors of Alternative Income REIT PLC (ticker: AIRE), the owner of a diversified portfolio of UK commercial property assets, predominantly let on long leases with index-linked rent reviews, provides a trading and business update for the quarter ended 30 June 2026.

Simon Bennett, Non-Executive Chair of Alternative Income REIT plc, comments:

“At 30 June 2026, the Group’s unaudited Net Asset Value (NAV) was £67.0 million, equivalent to 83.3 pence per share (“pps”), representing a decrease of 1.3% from the previous quarter. Including the dividend of 1.40pps paid during the period, the Group delivered an unaudited NAV total return of +0.4% for the quarter.

The Group’s portfolio was valued at £103.1 million at 30 June 2026, reflecting a small decrease in value of £340,000 or 0.33% during the quarter. The portfolio continues to demonstrate resilience, remaining 100% let, with 100% rent collection and 81.9% of leases subject to index-linked rent reviews.

The quarter was characterised by significant corporate activity. On 21 April 2026, the Board determined not to extend the deadline for its discussions with AEW UK REIT plc (“AEWU“) in relation to its indicative all-share proposal. Subsequently, Glenstone REIT plc announced a possible cash offer on 15 May 2026 and made a firm offer (the “Glenstone Offer“) in the following month.

Following the period end, on 16 July 2026 AEWU announced a revised possible all-share offer valuing AIRE at approximately 77.5 pps based on AEWU’s closing share price on Friday 7 August (based on AIRE shareholders receiving 0.725 new AEW UK REIT shares for each AIRE share held). The Board welcomed the proposal and stated that it had the potential to provide a more attractive outcome for shareholders than the Glenstone Offer, whilst noting that there could be no certainty that a firm offer will be made. On 20 July 2026, the Board formally recommended that shareholders reject the Glenstone Offer, believing that it materially undervalued the Company.

This period of corporate activity has resulted in the Board devoting significant time and resources to evaluating the various proposals. The Board recognises that these matters may have raised some uncertainty for shareholders, but the Board is committed to consider the best interests of all shareholders and will continue to issue updates as and when required. Notwithstanding these approaches, the Board remains confident in AIRE’s prospects as a standalone company. Following the successful refinancing of the Company’s debt facilities with HSBC UK Bank plc, the Board believes the Company is well positioned to continue generating secure and predictable income returns while preserving capital values, through investment in UK alternative and specialist sector real estate.”

Overview of Key Financials

At 30 June 2026(unaudited)

At 31 March 2026(unaudited)

Change

Net Asset Value (“NAV“)

£67.0 million

£67.9 million

-1.3%

NAV per share

83.3p

84.4p

-1.3%

Share price per share

69.2p

70.3p

-1.6%

Share price discount to NAV

16.9%

16.7%

0.2%

Investment property fair value (based on external valuation)

£103.1 million

£103.45 million

-0.3%

Loan to gross asset value (“GAV“) A,B

34.5%

34.3%

0.2%

Loan facility B

£36.6 million

£36.6 million

Quarter ended 30 June 2026(unaudited)

Quarter ended 31 March 2026(unaudited)

Change

EPRA earnings per share A,E

1.7p

1.4p

21.4%

Adjusted earnings per share A,F

0.9p

1.4p

-35.5%

Dividend cover A,D

65.0%

100.7%

-35.7%

Total dividends per share

1.4p

1.4p

–

Dividend yield (annualised) A,C

8.1%

8.0%

0.1%

Earnings per share

0.3p

1.3p

-76.9%

Share price total return A

0.4%

-2.6%

NAV total return A

0.4%

1.5%

Annualised passing rent

£8.0 million

£7.9 million

0.8%

Ongoing charges A (annualised)

1.5%

1.5%

–

A Considered to be an Alternative Performance Measure.

B The loan facility with HSBC UK Bank Plc at 30 June 2026 comprised a fully drawn term loan of £31 million and a revolving credit facility of £10 million of which £5.6 million was drawn down. At 30 June 2026, the weighted average interest cost was 5.45% (31 March 2026: 5.44%).

C Dividend yield is based on the target dividend of 5.6 pence per share, divided by the share price at the end of the quarter.

D Dividend cover is the ratio to measure the Group’s ability to pay its dividend and is calculated as adjusted earnings per share divided by dividend per share.

E EPRA earnings per share excludes non-recurring expenses which in this quarter includes approximately £750,000 of exceptional costs in respect of corporate activity.

F Adjusted earnings per share includes non-recurring expenses, but excludes change in fair value of investment properties, profit or losses on disposal of investment properties and other non-cash items.

Earnings per share and Dividend Cover

The fourth quarter interim dividend of 1.4pps (31 March 2026: 1.4pps) was announced on 23 July 2026 and is in line with the Company’s dividend target of 5.6pps. All rents due in the period were collected in full and the dividend would have been fully covered by earnings in the quarter, on a normalised basis, were it not for the exceptional costs relating to the corporate activity , which amounted to approximately £750,000. EPRA earnings per share was 1.7 pence.

Property Portfolio

At 30 June 2026, the Group held 19 properties (31 March 2026: 19 properties) valued at £103.1 million (31 March 2026: £103.45 million). In the quarter ended 30 June 2026, the portfolio valuation decreased marginally by 0.33% (£340,000), attributable to a slight weakening in the industrial market. The Group’s portfolio continues to demonstrate resilience in a difficult marketplace and the quarter ended 30 June 2026 benefitted from remaining 100% let, with 100% rent collection and 81.9% of leases being subject to index-linked rent reviews.

At 30 June 2026, the Net Initial Yield on the Group’s portfolio was 7.3% (31 March 2026: 7.2%). The weighted average unexpired lease term at 30 June 2026 was 15.0 years to the earlier of break and expiry (31 March 2026: 15.1 years) and 16.7 years to expiry (31 March 2026: 16.8 years).

During the quarter, the Group’s contracted annualised rent increased by 0.8% (31 March 2026: 0.2%), driven by the five-yearly review at Travelodge, Duke House, Swindon and a further four annual reviews. These uplifts were partly offset by a reduced rent at the Group’s gym facility in Chiswick, following the surrender of one lease and the new letting to Pure Gym.

Further to the announcement made on 9 July 2026, the Company is providing an update on Meridian Steel Limited, which currently lets three industrial units located in Dudley and Sheffield (the “Properties”). Since then, the Company has been in active discussions with the tenant, which are ongoing. The Board would like to reiterate that as a result of the parent company guarantee in the Properties, which AIRE has benefit of, the Company expects minimal impact on its rental income for the financial year ending 30 June 2027. Further information will be provided as new information becomes available.

At 30 June 2026, 81.9% of leases within the portfolio are index-linked, with 27.9% of the contracted rental income reviewed annually. Active portfolio management continues to focus on re-gearing leases, removing tenant breaks and extending lease lengths. For the current quarter ending 30 September 2026, 10.5% of the Group’s income is subject to rent review, reflecting the annual review of AIRE’s largest tenant by contracted income at Bramall Court, Salford.

Net Asset Value, Share Price and Share Price Discount to NAV

At 30 June 2026, the Group’s unaudited NAV was £67.0 million, 83.3pps (31 March 2026: £67.9 million, 84.4pps), representing a 1.3% decrease over the previous quarter. The decrease in NAV for the quarter was driven by the small reduction in the Group’s property portfolio and the exceptional costs associated with the corporate activity highlighted above. Given the on-going corporate activity, the Board expects that the exceptional costs will continue in the new financial year to 30 June 2027.

When combined with the 1.40pps dividend paid in the quarter, this produces an unaudited NAV total return for the quarter of +0.4% (31 March 2026; +1.5%). Over the quarter, the Company’s share price decreased by 1.6% to 69.2pps, reflecting a small increase in the discount from 16.7% to 16.9%.

The table below sets out the movement in NAV during the quarter.

Pence per share

£ million

NAV at 31 March 2026

84.4

67.9

Valuation movement in property portfolio

-0.5

-0.4

Income earned for the period

+2.9

+2.3

Expenses for the period

-0.5

-0.4

Exceptional corporate activity costs expensed for the period

-0.9

-0.7

Net finance costs for the period

-0.7

-0.6

Interim dividend paid during the quarter

-1.4

-1.1

NAV at 30 June 2026

83.3

67.0

The NAV attributable to the ordinary shares has been calculated under International Financial Reporting Standards as adopted by the United Kingdom and incorporates both the Group’s property portfolio individually valued on a ‘Red Book’ basis at 30 June 2026 and net income for the quarter but does not include a provision for the interim dividend declared on 23 July 2026.

The income earned for the period includes an accrual for the minimum contractual uplifts contained in the index-linked leases. In the event that inflation is greater than these minimum contractual uplifts, the actual income will be greater than the income currently accrued.

For the purposes of Rule 29.5 of the Takeover Code, the Board confirms that it has received confirmation from Knight Frank that an updated valuation of the Company’s property portfolio as at the date of this announcement would not be materially different from the valuation as 30 June 2026, which forms the basis of the Company’s unaudited net asset value announced today.

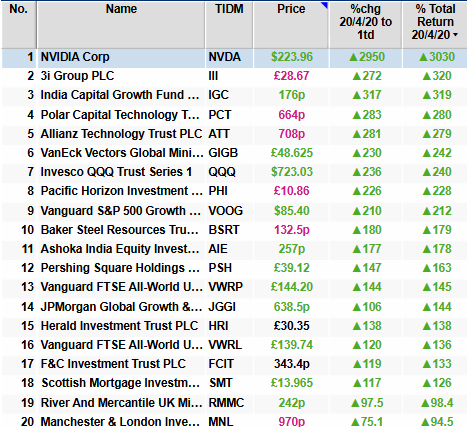

If you want to trade TR for part of your portfolio, you may want to have two pots of money, one for dividends and one to release cash for your tax free amount, subject of course if there will be a tax free amount, when you want to spend your hard earned.

The above is my TR watch list based on a 5 year returns history, other shares are available DYOR.