A much better week.

Investment Trust Dividends

A much better week.

We’re fund managers and these are the six big investment lessons we’ve learnt over the years

Story by Rosie Murray-west

As the children across Britain sharpen their pencils and go back to school, there are some financial lessons that their parents can learn too.

We asked Britain’s foremost investment managers to share the most important ones they’ve learnt – and how they’ve put them into practice.

What are the most important investment lessons? We ask the experts by This Is Money

Early mistakes have led to caution for Richard de Lisle, who manages the VT De Lisle America Fund. He began his investment journey at just 16, only to lose his hard-earned pocket money on a risky bet.

‘I read everything on my paper rounds and did well from Patrick Sergeant in the Daily Mail and Jim Slater in The Telegraph. Those were my favourites. Yes, the Mail had a hand in my career.

‘The FT 30 had fallen more than half in two years. Stock prices were so low that I was seduced by the glamorous Court Line [a former shipping company that became a holiday provider]. It was leading the new package holiday boom, opening up the Spanish Costas to people who’d never been abroad before.’

Despite his tender years, De Lisle even looked at the valuation, including the price-earnings ratio, which shows how much profit a company is making per share. As a rule of thumb, the lower the ratio, the cheaper the company.

‘Its P/E ratio was under four; the yield was 17 per cent. What could go wrong?’ De Lisle asks.

Quite a lot, it turns out.

‘Five months later, Court Line went bust because of too much debt and I lost all my hard-earned cash. My friend’s father, who owned the fish and chip shop, did much better. He put everything he had into five blue-chip companies and more than doubled his money in six weeks.

‘Warren Buffett says that debt just speeds things up and so it does. Today we run a value-based fund. While we like cheap, we don’t like debt. Lesson learned.’

For Laurence Hulse, who manages UK smaller companies’ specialist Onward Opportunities, an internship at Barclays Capital when he was 18 brought a lesson he has lived by all his life.

‘You’re almost always wrong before you are right. This was one of the first ‘lessons’ I was ever taught,’ Hulse says. During his time at Barclays under revered equity trader Howard Spooner, Hulse learned that because you do not usually time the market perfectly, your investment is likely to fall at first.

‘Other than in the unlikely event when you buy at the very lowest price or sell at the very highest price to the penny, you have got to be prepared to be wrong initially,’ Hulse says.

As a result of this lesson, he has learned not to make sudden swerves in his trading. ‘We very rarely trade into or out of a company in one transaction, as to do so would be to assume you have timed things perfectly.

John Husselbee, head of multi-asset at LionTrust, learned many of his investment lessons from his family.

‘My father taught me that whenever speculating at the racecourse or a casino, work out beforehand how much money you are prepared to lose betting, then put that amount in a separate pocket to treat as a sunk cost. Whatever is left in that pocket at the end of the day is your good fortune. However, if you have bad luck and your pocket is empty, never add to it – just walk away,’ he says.

From his grandfather, who bet on the horses as well as investing in shares, he learned the difference between investing and gambling.

‘Visiting my grandad on a Saturday morning, we would walk to the newsagent to buy a copy of the FT and the Racing Post. Back home, I would update the prices of Grandad’s shares in his ledger and calculate the profit/loss since purchase.

‘In the meantime, Grandad would study the form to select his bets for afternoon racing live on the telly. We would walk back to the newsagent; Grandad would give me pocket money for sweets and I would wait outside the bookies while he would place his bets.

‘The lesson learnt was the difference between investment and speculation – with the latter you need to be prepared to lose all your money!’

For a lesson he has never forgotten, Ian Lance, fund manager in the UK Value & Income team at Redwheel, casts his mind back to a despondent lunch in City of London oyster bar Sweetings, just as Britain was about to crash out of the European Exchange Rate Mechanism (ERM) in September 1992.

‘I calculated the payments on the mortgage my wife and I had taken out to buy our first home a few months earlier at the new interest rate of 12 per cent which the Government had just announced.

‘On finding that our payments were more than our combined salaries and the UK equity market was crashing, I headed down to Sweetings to drown my sorrows.

‘An hour or so later a colleague turned up and announced the stock market was soaring. The rest is history as Britain crashed out of the ERM, interest rates plummeted, and a new equity bull market began.’

What did he learn from this – apart from to take a long lunch now and then? ‘Markets look forward and will peer through the gloom to the sunlit uplands,’ he says. When all about you are despondent, it might be time for things to recover.

Jamie Ross, portfolio manager of Henderson Eurotrust, says that the facts available at our fingertips leave us more vulnerable than we know. The biggest lesson of his career, he says, has been that he always needs to focus on one important question when deciding whether to invest or not.

That question is: ‘What makes this a good company?’

‘It leads to all sorts of analysis, from understanding the competitive environment, to assessing pricing power to attempting to determine the sustainability of a company’s margins.’

Without this simple question, he says, it is easy to drown in information about a potential investment and to think you know everything about it.

‘Knowledge is not the same thing as understanding. Even experienced investors can sometimes miss the wood for the trees and suffer from familiarity bias – feeling more comfortable investing in something you ‘know’ lots about.

‘I think about this every time I start to work on a potential new investment.’

Edward Allen, investment director at Tyndall Private Clients, says that for all investment experts’ perceived wisdom they are ‘rarely cynical enough’, so you should never believe what you read from those who don’t have anything to lose from their predictions.

‘Economists and market forecasters have the luxury of being wrong. Investors do not,’ he points out.

‘Understand the biases of an author if you are going to follow their advice and remember that for every balanced, well-reasoned argument for doing something there will be many others for doing the opposite.

‘The investment world is perverse and often seemingly irrational.’

I’ve sold the portfolio shares in FSFL for a profit of £253.00 including the dividend earned but not received. The funds are earmarked for JLEN although trading at a slightly smaller yield, I feel more comfortable holding for the long haul.

A portfolio of shares to DYOR on. If u are growing your pot and time is on your side, u may be willing to take more of a risk and invest for growth and income. Better to have a dividend to re-invest when markets are weak.

If your pot of money has grown by compounding, u may be more interested in preserving your wealth by taking less risks with your money.

Above is a portfolio IT’s at the lower end of the risk spectrum, no share is entirely risk free but if u want a dividend to pay your bills or to re-invest, CTY have paid a gently increasing dividend for 52 years, so are unlikely to change their criteria, especially as they have reserves built up to pay their dividends when markets crash. LWDB could be a buy if/when the next market crash happens.

But as it’s your hard earned it’s always best to DYOR.

Dividends received at the end of April £3,861.00.

Do not scale by 3 to arrive at a figure for the year as the fcast is still 8k and the target 9k.

For any new readers, the portfolio rules there are only 2.

One. Buy Investment Trusts that pay a ‘secure’ dividend to buy more Investment Trusts that pay a secure dividend.

Two. Any Trust that drastically changes it dividend policy must be sold even at a loss.

The target for the portfolio is to pay a ‘pension’ of 14% within ten years, better if u have longer.

The target is not in doubt, although depending on the market the time scale may slip.

Dividend investing, the only strategy where u can welcome falling prices because as the price falls the yield rises.

I forgot to mention, u keep all your capital against buying an annuity at around 7% and gifting all your capital to a pension provider.

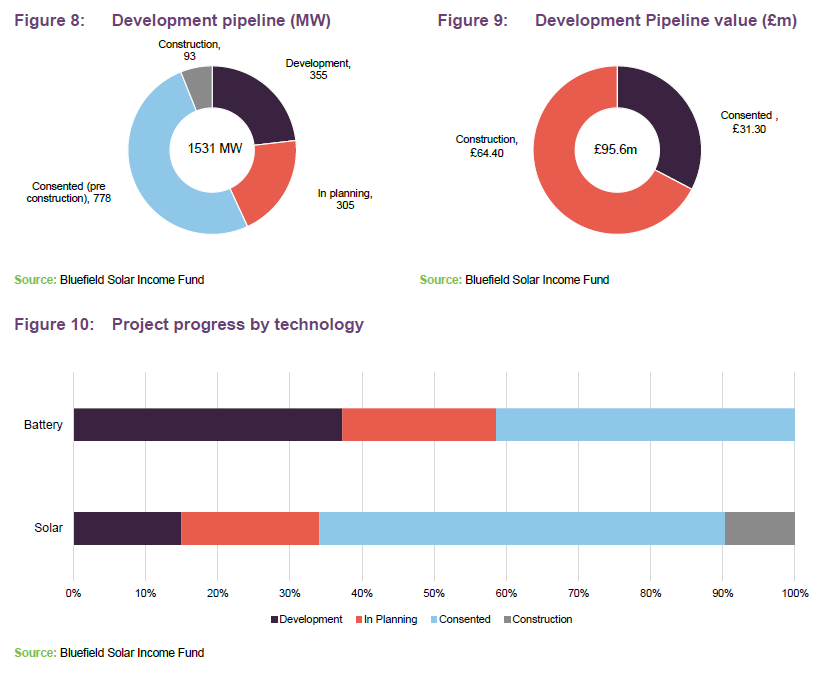

The manager says that BSIF also maintains a sizeable pipeline of assets. As of 31 December 2023, this stood at a total of 1,531MW, made up of 968MW of solar and 563MW of battery storage. As Figure 8 shows, this is broken down into various stages of development, noting that BSIF has a 5% investment limit in pre-construction development stage activities, of which less than 1% is currently committed.

Figure 9 highlights the current value of the construction projects and consented projects in the BSIF valuation. Currently, no value is attributed to projects without planning consent. The manager says that once developments receive planning consent and move from the development stage to pre-construction, the investment adviser believes it is appropriate to reflect this change in the company valuation. It says that at this point in their lifecycle, the projects will have received all the necessary planning consents, land rights and valid grid connection offers and so, it says, have discernible value beyond the direct costs of development.

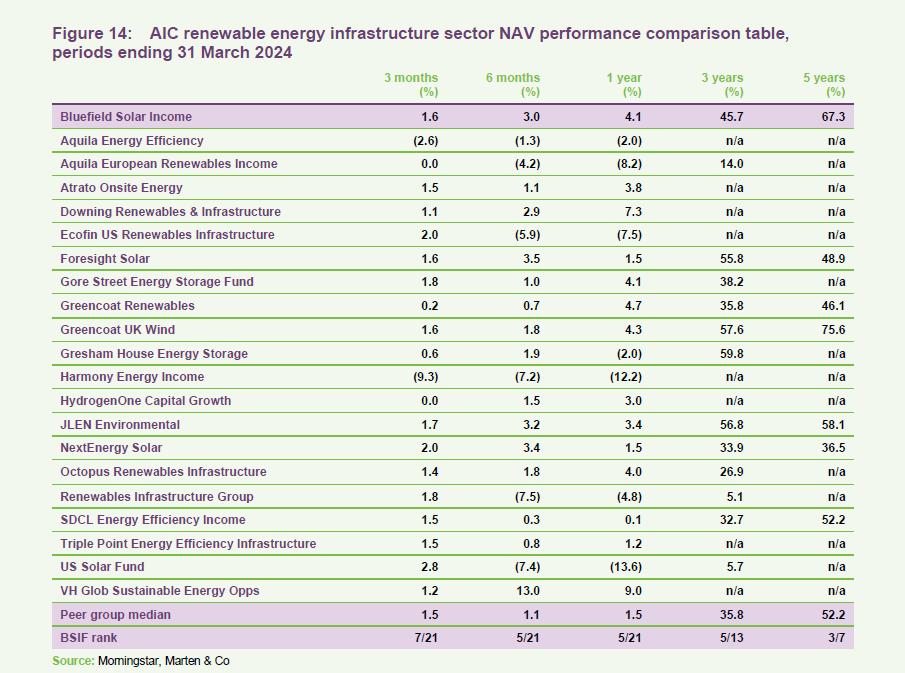

The manager notes that of all the AIC investment trust sectors, renewable energy infrastructure has been one of the hardest-hit by the economic challenges faced by the UK over the last few years. In many cases, it says, a degree of repricing was justified given the extent of the inflation surge and the ensuing tightening of monetary policy which took place over 2022 and 2023. It says that many companies in the sector reliant on debt financing and without sufficient cashflows have seen their share prices fall dramatically, with median sector discounts at one point falling through 30%.

The manager says that for the most part, BSIF had managed to steer clear of the carnage, operating throughout this period with one of the narrowest discounts in the entire sector. It says this was a reflection of the resilience of the portfolio and the ability of its advisors to navigate what it says has been one of the most challenging and uncertain periods of the company’s 11-year history.

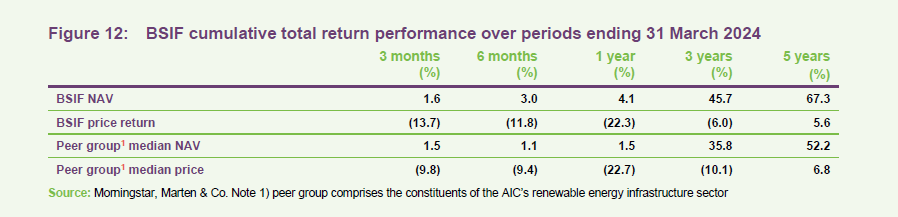

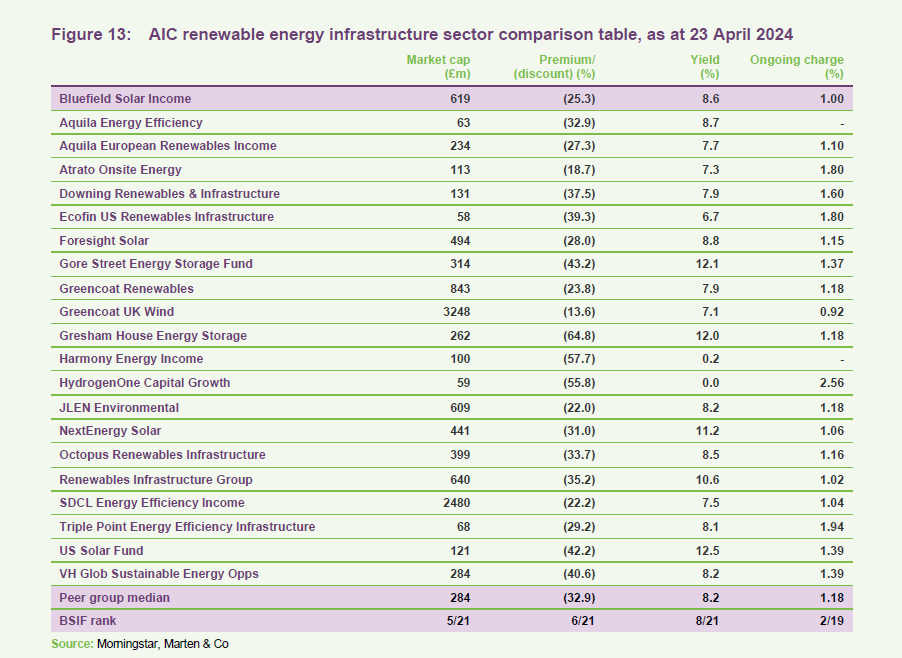

The manager adds that little has changed in that regard and says that the trust’s fundamentals have remained just as good as ever. Despite this, the manager notes that the discount has continued to widen, particularly since the end of 2023. Unfortunately, it says, there does not appear to be a particular catalyst driving the recent selloff. As shown in Figure 12, the company has outperformed its peer group median over the past 12 months, which the manager says suggests that the recent fall is driven more by market sentiment than any fundamental weakness.

You can access up-to-date information on BSIF and its peers on the QuotedData website.

There are now 22 companies that make up the AIC’s renewable energy sector, although we have removed the Asia Energy Impact Trust (formerly Thomas Lloyd Energy Impact) from our analysis, given that its shares were suspended for much of the past year.

The manager notes that of these companies, most are focused on solar or wind or some combination of the two; however, it says, there are several more-targeted funds which provide a different risk profile to BSIF. Three focus exclusively on battery storage assets. Three funds are focused on energy efficiency projects. Two funds invest exclusively in US projects, which it says tend to have long-term PPAs. One invests in hydrogen-related assets and has more of a capital growth focus.

The manager highlights that BSIF is a large, liquid fund, offering an attractive yield, adding that it has one of the most competitive ongoing charges ratios within the peer group.

The manager notes that BSIF has remained one of the most consistent performers in terms of NAV growth across the entire sector, both long-term and more recently. Notably, it says, the NAV performance has been steady despite the selloff in the company’s shares over the last 12 months, with the discount compounded by the 4.1% NAV return.

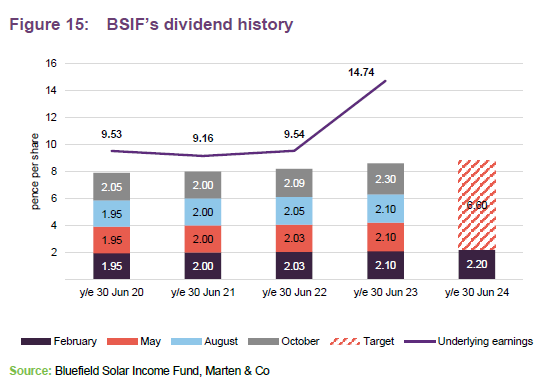

BSIF pays quarterly dividends. For a given financial year, the first interim dividend is paid in February, with the second, third and fourth interims paid in May, August and October/November respectively (dividends are usually declared the month before payment).

In the 2023 financial year, BSIF paid a total of 8.6p, 0.2p ahead of the target dividend following a jump in its underlying earnings. The manager says that within its peer group, BSIF has consistently delivered the highest dividend on a pence per share basis (or euro equivalent).

The target dividend for FY24 has been set at not less than 8.8p, an increase of 2.3% on the total dividend for FY23. The manager notes that whilst this may look like a small uplift in the context of recent adjustments, the existing dividend remains one of the highest in the sector. In addition, it says, given current challenges present in funding markets, there are obvious long-term benefit to shareholders if BSIF balances underlying and carried earnings between dividend payouts and other uses of capital such as the development of its pipeline. The manager adds that the nature of the current discount presents an opportunity to buyback shares.

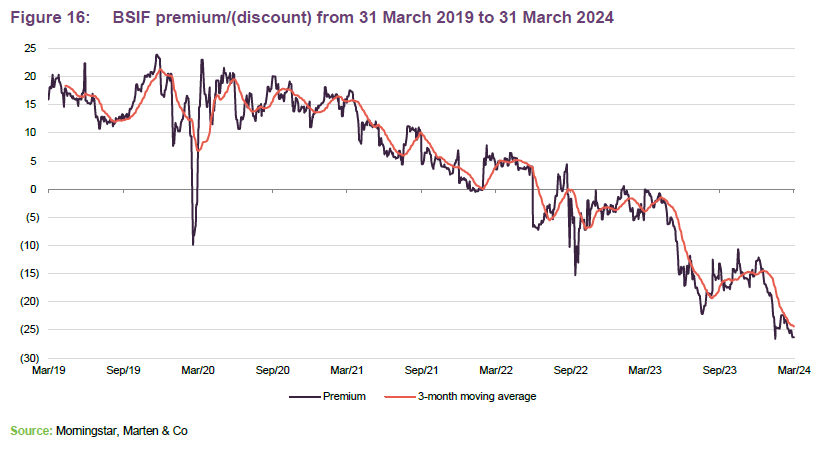

The manager notes that this is the first period in the company’s history where it has traded at a sustained discount. Early in 2023, it says, a period of positive performance saw shares trade close to par before a sharp decline over the next 12 months resulted in the discount widening to 27% at the time of publishing. The manager says that the sell-off became particularly steep at the beginning of 2024. It says there is no clear fundamental justification for this move, which has gone well past the mechanical impact of rising rates.

The manager says that whilst this remains unfortunate for both the advisors and investors, it is not uncommon for markets to overshoot in either direction. It believes that given the ongoing execution of the trust, and the efforts of the advisory team to ensure the long-term health of its portfolio through strategies including the new GLIL partnership, investors should remain confident. that BSIF’s fortunes will improve.

The manager notes that the recent sell-off has prompted the BSIF board to announce a share buyback programme, to which an initial £20m has been allocated. This commenced following the publication of the company’s interim report on 28 February 2024. Going forward, the manager says that BSIF’s capital allocation policy is under regular review, with the marginal benefit of buybacks evaluated against the merits of further investment in its existing assets, pipeline, and debt repayment. For the moment, it says that buybacks remain an effective use of capital given current discounts.

The manager notes that since its 2013 IPO, BSIF has focused on a simple and deliberate strategy of ensuring, outside of its revolving credit facility, that all debt within the structure is secured at portfolio level with fixed interest rates on fully amortising terms. As of 31 December 2023, the current average cost of debt is c.3.5% on £410m of long-term borrowings, which the manager says highlights that the company continues to be well insulated from today’s higher-interest-rate environment. Notably, it says, whilst BSIF has a modest amount of index-linked debt, it also has significant levels of RPI-linked revenues, leaving the company a net beneficiary of inflation.

At the group balance sheet level, BSIF has access to a £210m revolving credit facility and an uncommitted accordion feature that allows for a further £30m of borrowing. This facility matures in May 2025 and is provided by Lloyds Bank, RBS International, and Santander UK. The cost of this is 190bps over SONIA. As at 31 December 2023, the company had drawn £167m from its RCF. This is a reduction of £10m from our last note, which was published in October 2023 following a repayment stemming from the GLIL partnership.

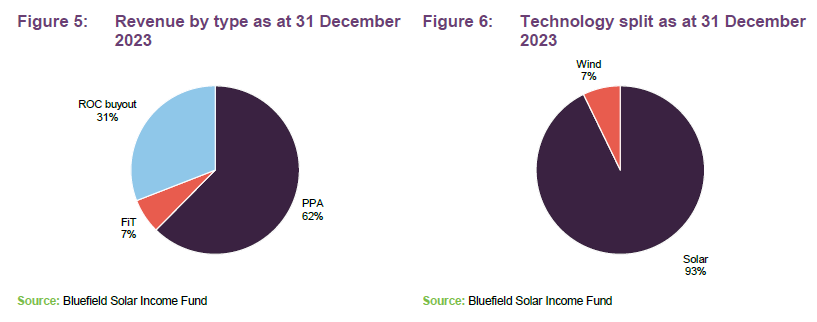

BSIF is a Guernsey-domiciled sterling fund, with a premium main market listing on the London Stock Exchange (LSE). At launch on 12 July 2013, it focused primarily on acquiring and managing a diversified portfolio of large-scale (utility-scale) UK-based solar energy assets, to generate renewable energy for periods of typically 25 years or longer. BSIF owns and operates one of the UK’s largest diversified portfolios of solar assets, with a combined installed power capacity of 813MWp.

In July 2020, shareholders approved proposals to expand the remit and BSIF began making investments in onshore wind and energy storage projects soon after.

BSIF is designed for investors looking for a high level of income with regular distributions.

Further information regarding BSIF can be found at: www.bluefieldsif.com

BSIF’s primary objective is to deliver to its shareholders stable, long-term sterling income via quarterly dividends. The majority of the group’s revenue streams are regulated and non-correlated to the UK energy market.

The underlying investments are held in SPVs which, in turn, are held through BSIF’s wholly-owned and UK-domiciled portfolio holding company, Bluefield Renewables 1 Ltd (BR1).

Investment companies | Update | 24 April 2024

The manger comments that, in common with the other trusts in the renewable energy sector, the last six months have continued what has been a challenging period for the Bluefield Solar Income Fund (BSIF). It adds that the trust’s ongoing fundamental performance has failed to reverse a steady slide in its share price which began back in May 2023. Despite this, it says the company has continued to deliver solid NAV growth and market-leading shareholder distributions thanks to a range of contractual arrangements that underpin its assets.

Positively, the manager notes, the falling share price does not appear to be a reflection on the trust itself, but rather broader macro-economic conditions and negative sentiment surrounding UK companies and renewable energy infrastructure in particular. It says that the board has signalled its dissatisfaction with the situation by authorising a £20m share buyback, which is currently underway. The manager adds that with growth accelerating and a recently announced strategic partnership providing an avenue for the ongoing development of its pipeline, the outlook for the trust remains attractive, as does a well-covered dividend yield approaching 9%.

BSIF aims to pay shareholders an attractive return, principally in the form of regular sector-leading income distributions, by being invested primarily in solar energy assets located in the UK.

BSIF’s share price may be reflecting broader macro-economic conditions and negative sentiment surrounding UK companies and renewable energy infrastructure in particular

The manager says that the renewable energy sector has been a victim of the rapid rise in global interest rates that began back in 2022. At its peak, risk-free returns from government debt climbed above 5%, which it says impacted on the appeal of renewable energy assets. The manager added that compounding the issue was the rise in discount rates and financing costs, which weighed on the ability to drive capital returns. It says that these dynamics have added to the pain caused by the general underperformance of the entire UK equity market, which it says has suffered from slowing growth, stubborn inflation, and a lame duck government. This led to suggestions that the economy may be staring down the barrel of stagflation, it adds.

The manager says that for the moment, the fortunes of the renewable energy sector appear tied to those of the broader economy and that given the challenges faced over the last 12 months, it was difficult to see where a positive catalyst might emerge from. However, in recent months it says we have seen some signs of improvement.

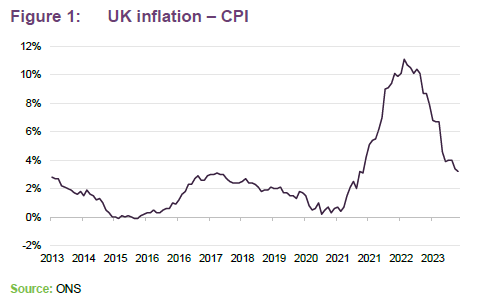

The positive news is headlined by February’s inflation data, which was down sharply, falling to 3.4% from 4.2% the month prior

The manager notes that the positive news was headlined by continued progress on inflation which, after a steep decline in February, fell to 3.2% in March. The reading marking the slowest annual rate since September 2021. Promisingly, it says, the data shows many of the underlying components of the CPI index are also falling including the service sector figure which it says typically reflects domestic rather than imported pricing pressures.

Promisingly, the manager highlights that steady wage growth suggests that we are beginning to see some stability in the labour market, and it says that sustained real earnings should provide a much-needed boost for GDP.

Even so, the manager believes economic growth remains a concern, and with the ECB still at the terminal, it says there appears to be considerable headroom to lower interest rates.

The manager says that with the renewable energy sector one of the worst-affected by the previous rise in rates, it was hoped that any easing of financial conditions would result in a sustained uplift. However, despite gilt yields falling by almost 50 basis points from their peak, the share prices of both BSIF and the broader sector have continued to deteriorate. Because of this, the manager suggests that there may remain other factors at play.

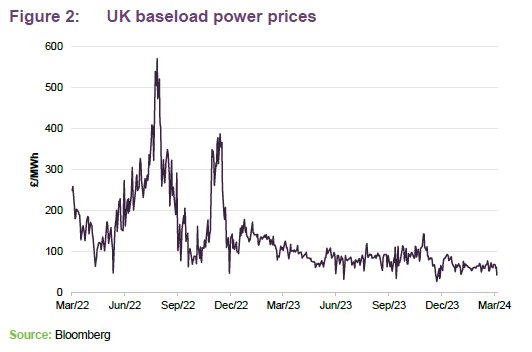

One possible explanation, it says, is falling power prices. According to the manager, despite appearing to undergo a structural resight higher post-COVID, these have retreated from their highs, which has impacted on NAVs as medium to longer-term forecasts are reduced as shown in Figure 2.

However, the manager says that BSIF has maintained strategies that greatly limit the impact of any power price volatility.

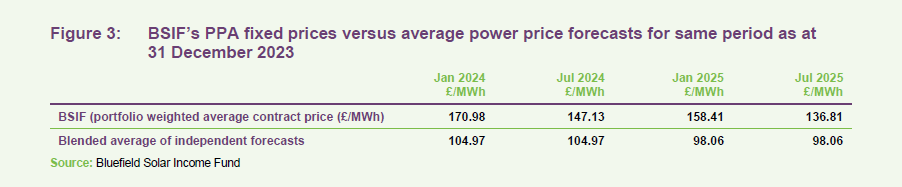

The manager highlights that BSIF’s strategy is to lock in power sale contracts for individual assets not covered by long-term contracts for periods between 12 and 36 months. It says that this helps to mitigate much of the volatility inherent in energy markets, which it comments has become particularly elevated in recent years due to escalating geopolitical tensions and ongoing supply disruptions. Entering into 2024, the company had more than 78% of its merchant revenue sold forward to March 2025, with the strategy securing power price fixes at levels that are materially higher than the latest industry forecaster expectations, as highlighted in Figure 3 below:

The manager says that in addition to its power price management, BSIF also benefits from a range of inflation-linked contracts, which account for almost two-thirds of the company’s revenues. It says that this means that increases in RPI have the effect of boosting both earnings and the valuation of BSIF’s assets. In combination with the company’s price-fixing strategy, the manager comments that the structure provides both the advisors and investors with excellent visibility over BSIF’s medium-term revenues. It says this also provides a hedge against an increasingly uncertain interest rate environment.

The manager says the success of these strategies is highlighted in the company’s recent interim results with strong revenue growth and dividend cover well in excess of 2x. This, it adds, consolidates BSIF’s position as arguably one of the more reliable income options for investors in the UK.

The manager observes that another potential overhang is the ongoing issues surrounding investment trust cost disclosures. The manager says there is currently a campaign to reform these regulations, which, it is hoped, will help improve sentiment towards the entire investment trust sector.

The manager thinks that with the UK’s economic outlook steadily improving, and BSIF continuing to execute on its fundamental performance, current discounts could provide a very attractive entry point for a trust.

The manager highlights that BSIF has continued to generate solid returns despite its falling share price, saying the fundamentals of the portfolio are as good as they have ever been in the 10-plus years that the fund has been operating. The manager adds that the company’s recent interim results, released on February 28 for the six-month period ending 31 December 2023, show no signs of this momentum slowing, with a number of record returns and a full-year outlook, which it says has continued to improve.

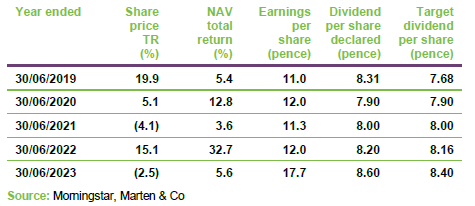

BSIF’s headline revenue return was 91.6m, a 17% year on year increase and more than double that of the equivalent period in 2021.

The manager continues that despite irradiation levels some 13% below those experienced in the second half of calendar 2022, the company’s headline revenue return was £91.6m, a 17% year on year increase and more than double that of the equivalent period in 2021. Total funds available for distribution reached a record high of 70.2m and, as noted, dividend cover is now well in excess of 2x with a total dividend of almost 9%, one of the highest in the sector.

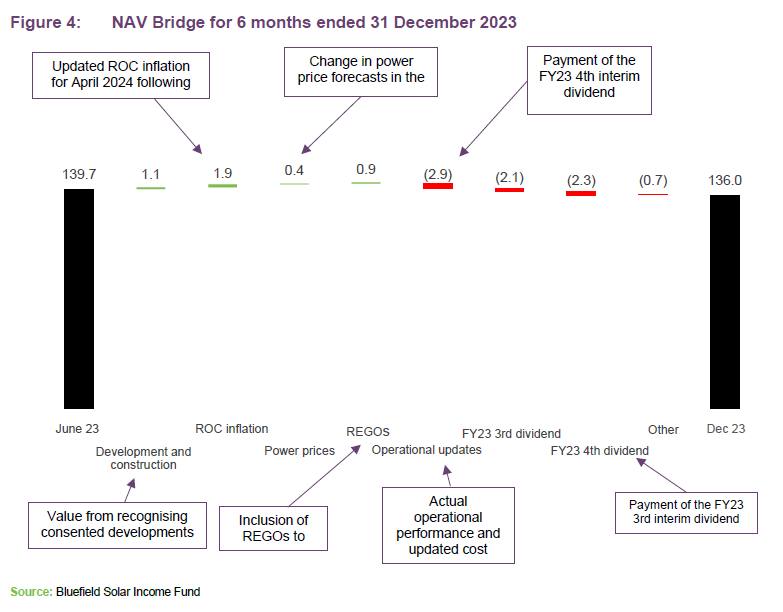

BSIF’s NAV over the six-month period fell slightly from 139.7p at 30 June 2023 to 136.0p at 31 December 2023 with the positive impact of inflation and power price forecasting offset by dividend payments, highlighted in Figure 4.

The manager says that the company has also maintained its focus on the build out of its development pipeline, the extent and value of which it says is significantly underappreciated by the market. During the second half of 2023, the company secured planning consents on 137MW of solar projects and 90MW of battery projects, while post period end one project of 50MW solar received consent. The wider pipeline grew to approximately 968MW of solar and 563MW of battery storage (with a full breakdown available on page 9 of this report). Of these developments, over 600MW are consented solar sites, with a significant share of this capacity holding valuable 15-year CPI indexed linked contracts.

The manager notes that these investments not only establish a significant growth ramp for BSIF, but also provide the portfolio with what it says is considerable financial flexibility. It adds that in the event that funding markets remain closed in the near term due to the company’s stubborn discount and broader economic challenges, BSIF has the option to sell some of this pipeline to third parties. The manager says that with these assets predominantly held at consented value, such a strategy could provide an immediate boost to NAV while generating additional liquidity for the portfolio to either refocus on other developments or pay down debt.

The manager outlines that given the challenges present in the current market, the board has been evaluating how best to continue this development programme while maximising value for its shareholders over the long term. It says that having explored various options, BSIF has announced a Strategic Partnership with GLIL Infrastructure in December 2023. GLIL is a partnership of UK pension funds that invests into core UK infrastructure and has a £3bn portfolio of infrastructure assets.

It says that the partnership is a significant development and allows BSIF to deliver on a number of key areas. Primarily, it allows the company to maintain its investment momentum in what continues to be a difficult time for public infrastructure funds, it adds. The manager continues that the deal also increases the diversification of the company’s revenue base, provides external validation of its assets, reduces debt, and creates additional liquidity for the fund.

It says the partnership can be broken down into three main phases, the first of which occurred post-period-end in January 2024, with BSIF investing £20m alongside £200m from GLIL to acquire a 247MW portfolio of UK solar assets from Lightsource bp. BSIF’s ownership stake in the portfolio is 9%.

BSIF announced a Strategic Partnership with GLIL Infrastructure in December 2023

The Lightsource bp portfolio is predominantly diversified across southern and central England and comprises 58 operating sites: 184MW backed by feed in tariff subsidies, 15MW by renewable obligation certificates and two subsidy-free projects totalling 48MW. It says that through the period 2023 to 2035, the proportion of fixed and regulated revenues from the portfolio is projected to be approximately 80%. The acquisition raises the level of regulated revenues in the BSIF portfolio whilst also increasing the proportion of FiT income. The deal also facilitated a £10m repayment of BSIF’s revolving credit facility, which is discussed on page 15.

The manager continues that phase 2 comprises a provisional agreement for GLIL to acquire a 50% stake in a portfolio of more than 100MW of BSIF’s existing solar assets, at a price which is in line with the company’s existing valuation. It says the proceeds of this partial sale will be used in part to fund BSIF’s participation in the rollout of its development pipeline and, as appropriate, to reduce debt. This phase is expected to be completed in the first half of 2024.

The manager says that in phase 3, Bluefield Solar and GLIL intend via the strategic partnership to commit capital jointly to a selection of the company’s development pipeline, assuming market conditions are supportive. It says the identified development assets are expected to be grid-connected over the next two to three years.

Altogether, the manager believes the relationship shapes as an important development at a crucial juncture for BSIF. It says that in an ideal world, the company would have the financial flexibility to develop some of these assets under its own steam. However, the manager notes that this is unrealistic given current conditions and the agreement appears to be the next best alternative, given the time pressures attached to some of the existing consents in BSIF’s pipeline. It says the deal also removes some of the development risk associated with the pipeline at a time when the industry has been faced with dramatic cost blowouts. The manager also adds that the added financial flexibility should allow the company to achieve keen pricing on any future projects given discounts across the rest of the sector.

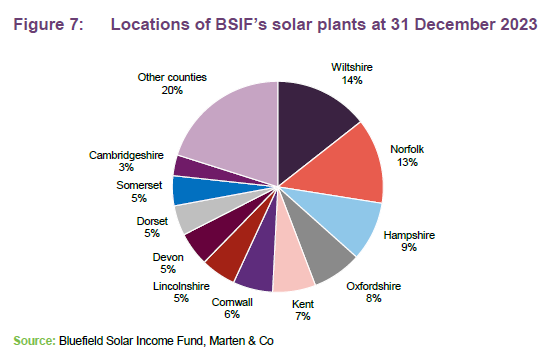

BSIF operational portfolio as of 31 December 2023, consisted of 812.6MW, which was made up of 754.2MW solar and 58.4MW onshore wind. This encompasses 129 solar PV projects (87 large-scale sites, 39 micro-sites and three rooftop sites), six wind farms and 109 single-stick wind turbines, spread across England, Wales, Scotland and Northern Ireland.

During the period to 31 December 2023, the combined solar and wind portfolio generated an aggregated total of 376.05GWh (31 December 2022: 391.8GWh), representing a generation yield of 462.8 MWh/MW (31 December 2022: 511.4MWh/MW)

Here’s how I’d aim for a ton of passive income from £20k in an ISA

© Provided by The Motley Fool

It’s spring, and investors’ thoughts are turning to passive income. And what better way than with our new ISA contribution limit of £20,000 ?

We could go for a Cash ISA, and some of those pay around 5% these days. And it’s guaranteed, at least for the duration of the deal.

As with so many things in life, we have to balance risk and reward.

Over the long term, the UK stock market has beaten other forms of investment. But it’s had bad spells, like the past decade.

There are ways we can reduce risk though.

One way is what I think of as playing the percentage shots. Using a term from sport, if we play the shots that are more likely to be modestly successful rather than going for the riskier glory chances, we can stand a better chance of coming out ahead in the long term.

Let’s compare a couple of UK stocks.

Vodafone (LSE: VOD) has been paying some of the FTSE 100‘s biggest dividends. We’re talking serious money here, with yields above 10%. And if that’s not a great route to passive income, what is?

What’s the point of big dividends if we lose the bulk of our initial stake?

Oh, and Vodafone will slash its dividend in 2025, though shareholders should get one final 10% for 2024.

Still, it’s part of Vodafone’s refocus, and I do think the stock could have a good future now. But back to my point…

Let’s compare that with a stock I rate as possibly the most reliable dividend payer in the FTSE 100. I’m talking of National Grid (LSE: NG.),with a forecast 5.4% dividend for 2024.

That’s not big growth. But it’s a few points ahead of the Footsie, which I think is fine in the decade we’ve had.

National Grid faces a reduction in gas distribution. And it’s in a regulated industry where minimum investment is often mandated. So it’s not without risk, and the dividend is far from guaranteed.

But I rate it as the percentage shot, while Vodafone was the glory shot.

Still, I reckon we can do better than a 5.4% return. But we do need to lift the risk a bit. By spreading my ISA cash across a diversified range of dividend stocks, I expect I could snag 7% per year.

A whole ISA allowance invested at that rate could compound to more than£75,000 in 20 years. And then that could pay £6,800 a year in passive income.

Or someone who can stash away the full £20k each year could build more than £850k, for a £60k annual passive income.

Do you like the idea of dividend income?

The prospect of investing in a company just once, then sitting back and watching as it potentially pays a dividend out over and over?

© 2026 Passive Income Live

Theme by Anders Noren — Up ↑