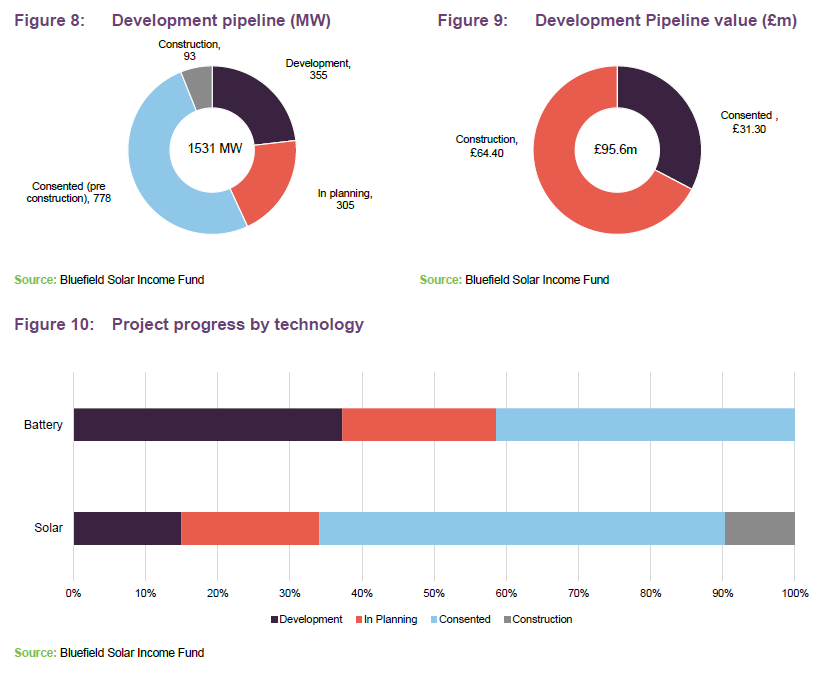

Construction and development pipeline

The manager says that BSIF also maintains a sizeable pipeline of assets. As of 31 December 2023, this stood at a total of 1,531MW, made up of 968MW of solar and 563MW of battery storage. As Figure 8 shows, this is broken down into various stages of development, noting that BSIF has a 5% investment limit in pre-construction development stage activities, of which less than 1% is currently committed.

Figure 9 highlights the current value of the construction projects and consented projects in the BSIF valuation. Currently, no value is attributed to projects without planning consent. The manager says that once developments receive planning consent and move from the development stage to pre-construction, the investment adviser believes it is appropriate to reflect this change in the company valuation. It says that at this point in their lifecycle, the projects will have received all the necessary planning consents, land rights and valid grid connection offers and so, it says, have discernible value beyond the direct costs of development.

Performance

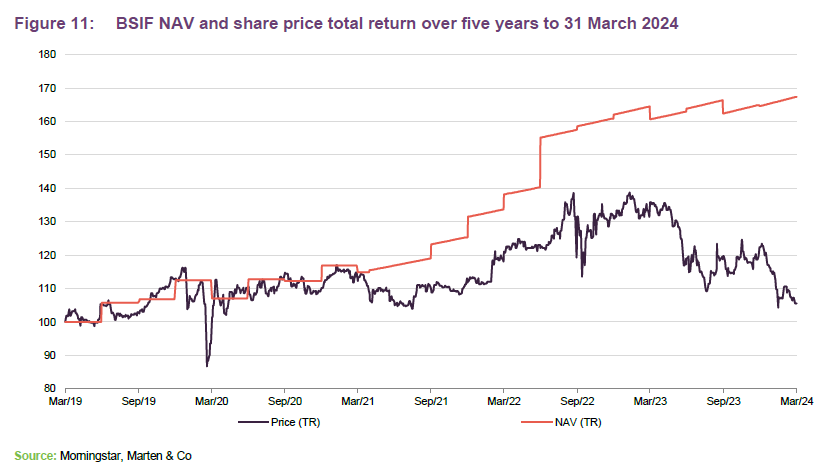

The manager notes that of all the AIC investment trust sectors, renewable energy infrastructure has been one of the hardest-hit by the economic challenges faced by the UK over the last few years. In many cases, it says, a degree of repricing was justified given the extent of the inflation surge and the ensuing tightening of monetary policy which took place over 2022 and 2023. It says that many companies in the sector reliant on debt financing and without sufficient cashflows have seen their share prices fall dramatically, with median sector discounts at one point falling through 30%.

The manager says that for the most part, BSIF had managed to steer clear of the carnage, operating throughout this period with one of the narrowest discounts in the entire sector. It says this was a reflection of the resilience of the portfolio and the ability of its advisors to navigate what it says has been one of the most challenging and uncertain periods of the company’s 11-year history.

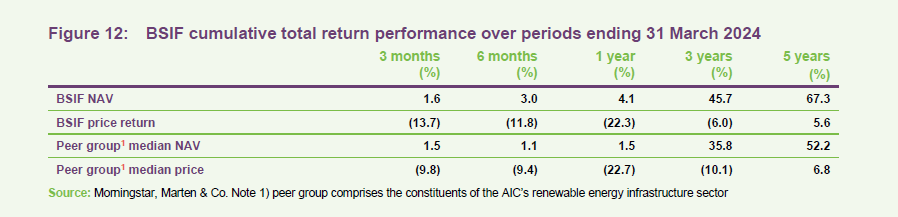

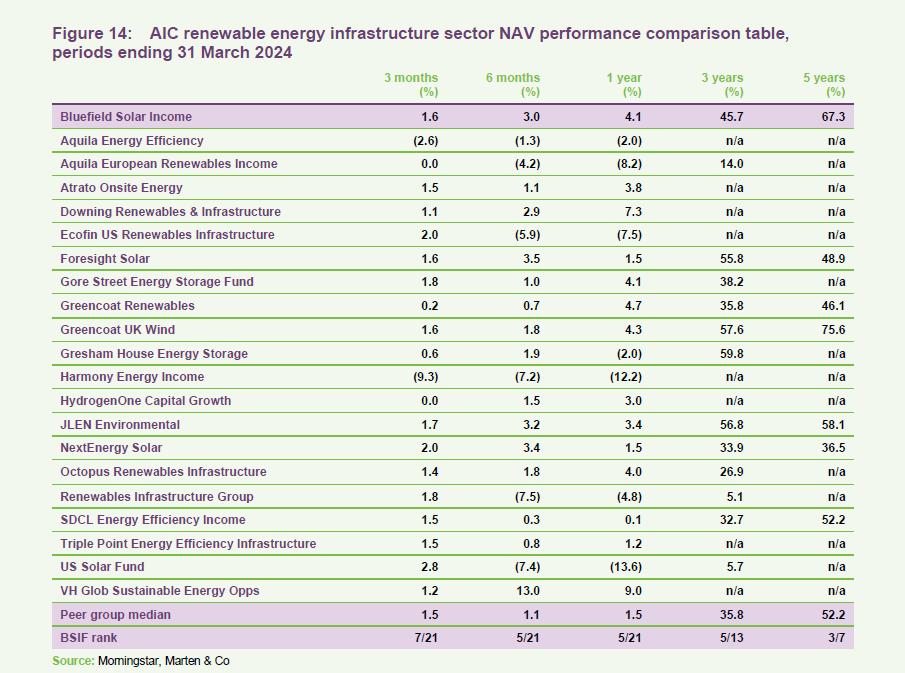

The manager adds that little has changed in that regard and says that the trust’s fundamentals have remained just as good as ever. Despite this, the manager notes that the discount has continued to widen, particularly since the end of 2023. Unfortunately, it says, there does not appear to be a particular catalyst driving the recent selloff. As shown in Figure 12, the company has outperformed its peer group median over the past 12 months, which the manager says suggests that the recent fall is driven more by market sentiment than any fundamental weakness.

Peer group comparison

You can access up-to-date information on BSIF and its peers on the QuotedData website.

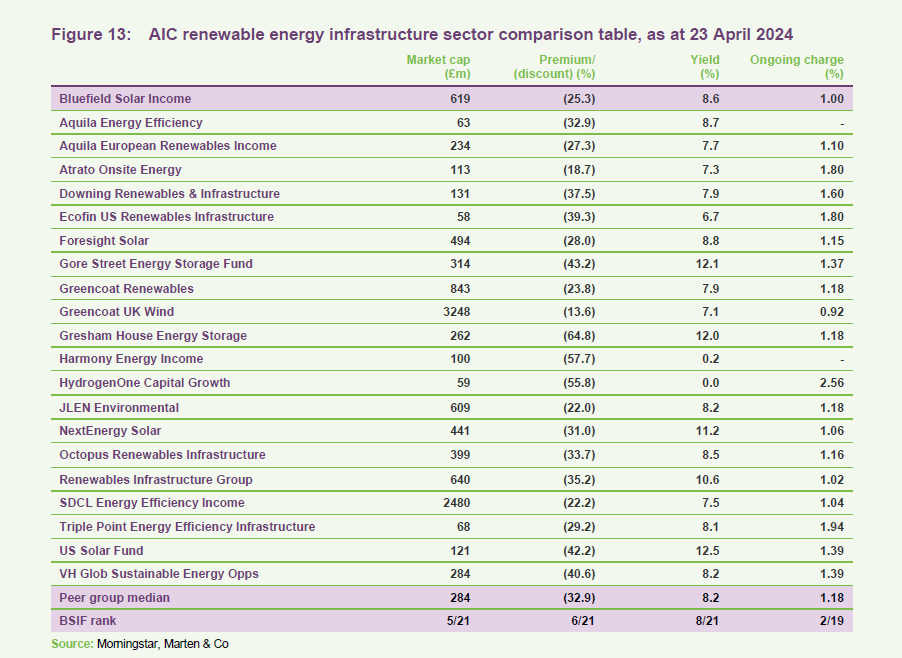

There are now 22 companies that make up the AIC’s renewable energy sector, although we have removed the Asia Energy Impact Trust (formerly Thomas Lloyd Energy Impact) from our analysis, given that its shares were suspended for much of the past year.

The manager notes that of these companies, most are focused on solar or wind or some combination of the two; however, it says, there are several more-targeted funds which provide a different risk profile to BSIF. Three focus exclusively on battery storage assets. Three funds are focused on energy efficiency projects. Two funds invest exclusively in US projects, which it says tend to have long-term PPAs. One invests in hydrogen-related assets and has more of a capital growth focus.

The manager highlights that BSIF is a large, liquid fund, offering an attractive yield, adding that it has one of the most competitive ongoing charges ratios within the peer group.

The manager notes that BSIF has remained one of the most consistent performers in terms of NAV growth across the entire sector, both long-term and more recently. Notably, it says, the NAV performance has been steady despite the selloff in the company’s shares over the last 12 months, with the discount compounded by the 4.1% NAV return.

Dividend

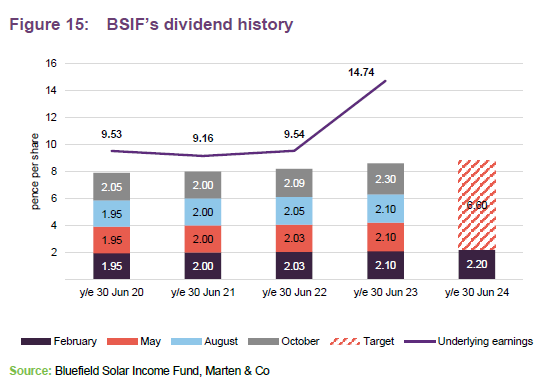

BSIF pays quarterly dividends. For a given financial year, the first interim dividend is paid in February, with the second, third and fourth interims paid in May, August and October/November respectively (dividends are usually declared the month before payment).

In the 2023 financial year, BSIF paid a total of 8.6p, 0.2p ahead of the target dividend following a jump in its underlying earnings. The manager says that within its peer group, BSIF has consistently delivered the highest dividend on a pence per share basis (or euro equivalent).

The target dividend for FY24 has been set at not less than 8.8p, an increase of 2.3% on the total dividend for FY23. The manager notes that whilst this may look like a small uplift in the context of recent adjustments, the existing dividend remains one of the highest in the sector. In addition, it says, given current challenges present in funding markets, there are obvious long-term benefit to shareholders if BSIF balances underlying and carried earnings between dividend payouts and other uses of capital such as the development of its pipeline. The manager adds that the nature of the current discount presents an opportunity to buyback shares.

Premium/(discount)

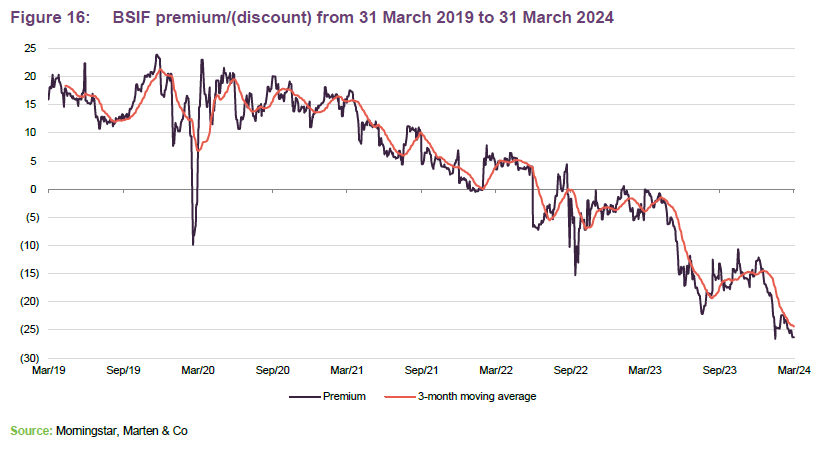

The manager notes that this is the first period in the company’s history where it has traded at a sustained discount. Early in 2023, it says, a period of positive performance saw shares trade close to par before a sharp decline over the next 12 months resulted in the discount widening to 27% at the time of publishing. The manager says that the sell-off became particularly steep at the beginning of 2024. It says there is no clear fundamental justification for this move, which has gone well past the mechanical impact of rising rates.

The manager says that whilst this remains unfortunate for both the advisors and investors, it is not uncommon for markets to overshoot in either direction. It believes that given the ongoing execution of the trust, and the efforts of the advisory team to ensure the long-term health of its portfolio through strategies including the new GLIL partnership, investors should remain confident. that BSIF’s fortunes will improve.

Buybacks

The manager notes that the recent sell-off has prompted the BSIF board to announce a share buyback programme, to which an initial £20m has been allocated. This commenced following the publication of the company’s interim report on 28 February 2024. Going forward, the manager says that BSIF’s capital allocation policy is under regular review, with the marginal benefit of buybacks evaluated against the merits of further investment in its existing assets, pipeline, and debt repayment. For the moment, it says that buybacks remain an effective use of capital given current discounts.

Balance sheet

The manager notes that since its 2013 IPO, BSIF has focused on a simple and deliberate strategy of ensuring, outside of its revolving credit facility, that all debt within the structure is secured at portfolio level with fixed interest rates on fully amortising terms. As of 31 December 2023, the current average cost of debt is c.3.5% on £410m of long-term borrowings, which the manager says highlights that the company continues to be well insulated from today’s higher-interest-rate environment. Notably, it says, whilst BSIF has a modest amount of index-linked debt, it also has significant levels of RPI-linked revenues, leaving the company a net beneficiary of inflation.

At the group balance sheet level, BSIF has access to a £210m revolving credit facility and an uncommitted accordion feature that allows for a further £30m of borrowing. This facility matures in May 2025 and is provided by Lloyds Bank, RBS International, and Santander UK. The cost of this is 190bps over SONIA. As at 31 December 2023, the company had drawn £167m from its RCF. This is a reduction of £10m from our last note, which was published in October 2023 following a repayment stemming from the GLIL partnership.

Fund profile

BSIF is a Guernsey-domiciled sterling fund, with a premium main market listing on the London Stock Exchange (LSE). At launch on 12 July 2013, it focused primarily on acquiring and managing a diversified portfolio of large-scale (utility-scale) UK-based solar energy assets, to generate renewable energy for periods of typically 25 years or longer. BSIF owns and operates one of the UK’s largest diversified portfolios of solar assets, with a combined installed power capacity of 813MWp.

In July 2020, shareholders approved proposals to expand the remit and BSIF began making investments in onshore wind and energy storage projects soon after.

BSIF is designed for investors looking for a high level of income with regular distributions.

Further information regarding BSIF can be found at: www.bluefieldsif.com

BSIF’s primary objective is to deliver to its shareholders stable, long-term sterling income via quarterly dividends. The majority of the group’s revenue streams are regulated and non-correlated to the UK energy market.

The underlying investments are held in SPVs which, in turn, are held through BSIF’s wholly-owned and UK-domiciled portfolio holding company, Bluefield Renewables 1 Ltd (BR1).

Leave a Reply