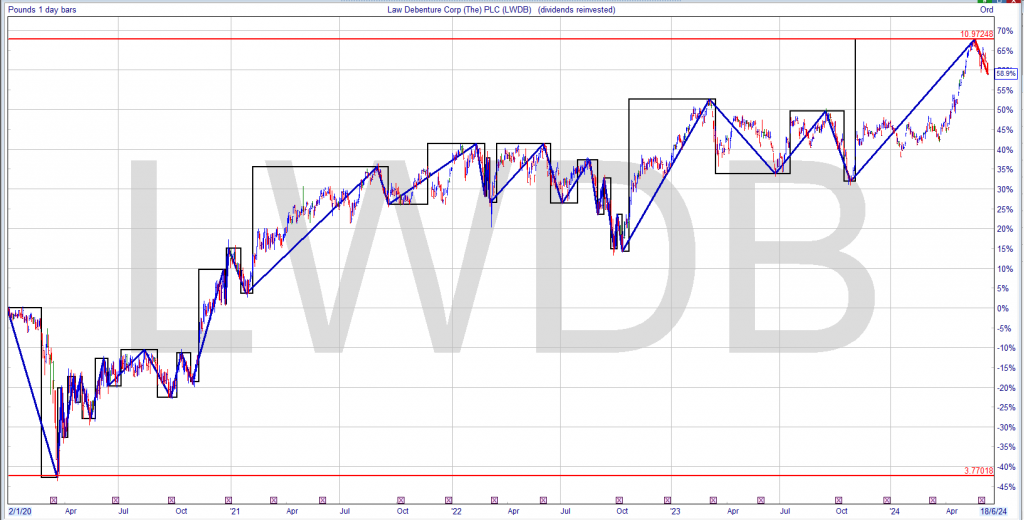

Decide what to buy when Mr. Market gives u the chance, better with a dividend as u wait to be proved correct and u need to re-invest the dividends.

TMPL current yield 3.5%, share price covid low 115p dividend 10.28p yield 8.5%. Of course u might not have bought as u didn’t know if the price was still going to fall but if u bought the yield u wouldn’t be that concerned.

When Mr. Market gives u the chance, watch your list of Dividend Heroes, belt and braces. Now that the price has risen the yield has fallen u could re-invest, by selling part or all the holding and re-invest in a higher yielder to grow your Snowball, which should be different to the Blog’s portfolio.

Remember it’s always easier in the rear view mirror, because as the yield fell to 7% u didn’t know if it was to fall further but if that was as low as it was going to get. Of course there were other Trusts to buy if u missed the one u wanted to buy.

There seems to be some perverse human characteristic that likes to make easy things difficult. Warren Buffett

The Company’s capital performance was disappointing last year, with a net asset value total return of -9.7%. The discount to net asset value also widened, resulting in a share price total return of -10.3%. Since our year end on 31 March 2024, however, the share price has rebounded and the discount narrowed again. Rental income growth was well above inflation last year, and since the year end, 100% of rent has become index-related.

The weakness of the property market is principally the result of the abrupt end of the extended era of exceptionally low interest rates which followed the global financial crisis. Central Banks around the world have been indicating that the next moves in rates are more likely to be down than up. But we should expect a return to historical normality rather than a resumption of the near zero cost bank financing.

As a result, there are some indications that the worst is over for property, although confidence is still fragile and transaction volumes are low. The election in Britain, which will take place on July 4, may result in a degree of political stability which has been missing for most of the current Parliament. It is difficult to maintain similar hopes for the outcome of the US Presidential contest in November. In both countries, fiscal projections bear little relation to reality. The geopolitical uncertainties which contributed to the rise in inflation and consequent increase in interest rates have compounded. The war in Ukraine continues and hostilities have ravaged Palestine. The ambitions of China’s leaders are a growing source of tension and concern.

While no asset classes are immune from these factors, the Company’s portfolio of UK property assets with good locations, strong covenants and rents linked to inflation is well positioned to be robust to external events. During the year, the portfolio was strengthened with the purchase of three long-let leisure investments at yields over 8%, and the sale of seven weaker properties including the last Stonegate pub holdings. That company has since announced it is seeking to refinance its debts. All the remaining tenants appear well financed. All rent due in the last year was collected in full.

We continue to improve the sustainability credentials of our properties, post year end 100% of all Energy Performance Certificates are now A – C. All rent due in the last year was collected in full.

A major restructuring of the Company’s debt was completed last year with the repayment of the costly debenture and the Company now has a comfortable loan to value position locked in at affordable interest rates.

Underlying income growth was strong with 11 rent reviews adding 4.9% to total rental income. As the revised name of the Company, adopted in 2021 emphasises, our focus is on achieving value from secure indexed property income.

At the year end, the yield on the Company’s shares (at the proposed dividend) was 7.7% as against 0.1% on the UK Government’s 2031 indexed gilt, which is linked to the Retail Prices Index (RPI).

Some of the rents on VIP’s properties are linked to the RPI, others to the slightly slower rising Consumer Prices Index (CPI), which is the basis for the 2% target prescribed for the Bank of England. The Company’s index-related rent reviews should make it well placed to at least match inflation now it is nearer to the official target.

As anticipated, dividend cover has now been restored and the Board aims to maintain the Company’s thirty-seven year history of progressive dividend increases. The Board is recommending a final dividend of 3.6p per share, making total dividends of 13.2p per share for the year to 31 March 2024, compared to 12.9p in the previous year, an increase of 2.3%. Subject to Shareholder approval at the 2024 Annual General Meeting (AGM), the final dividend will be paid on 26 July 2024 to Shareholders on the register on 28 June 2024. The ex-dividend date is 27 June 2024.

The Tip Sheet The Mail on Sunday thinks Impax Environmental Markets shares are a bargain, while The Investors Chronicle believes Caledonia can solve a quandary faced by some investors. Quandary? The Tip Sheet reveals all.

By Frank Buhagiar 11 Jun, 2024

MIDAS SHARE TIPS: The unheralded eco firms being turned into green giants According to the Mail on Sunday tipster, there’s one fund which gives investors exposure to ‘the unheralded eco firms being turned into green giants’ – Impax Environmental Markets (IEM), a fund that focuses on ‘small and mid-sized businesses with an environmental twist, from hazardous waste treatment in America to reusable pallets in Australia.’ The small to mid-cap focus sets IEM apart from its peers which typically invest in either unlisted cash-hungry businesses and projects, or large-scale companies that face stiff competition. It also has the potential to drive ‘faster growth over time’.

The share price is down around a third since 2021, as economic and market uncertainty have weighed on the valuations of IEM’s underlying holdings. But this works both ways – the portfolio managers are looking to take advantage of the current market environment to pick up stocks at attractive prices. Could be perfect timing as climate change continues to rise up the agenda which ought to benefit ‘companies with robust green credentials’.

Midas concludes, ‘Impax Environmental Markets has been through a rough few years but, at £3.96, the shares are a bargain. The group combines green credentials with hard-nosed commercial nous. Buy and hold.’

Investors Chronicle: A clever and cheap way to invest in private equity Hot on the heels of last week’s tip in The Telegraph, Caledonia Investments (CLDN) finds itself the subject of another positive piece, this time from The Investors Chronicle. The article kicks off by highlighting a quandary faced by investors considering allocating a portion of their portfolios to private equity. On the one hand, there are the stellar returns generated by private equity investment trusts over the past decade, several of which have returned over 200% in this time. On the other hand, some investors will be put off by the sector’s high debt levels, particularly with interest rates high and economic conditions challenging.

What to do? Enter CLDN ‘For those who are intrigued by private assets but are unsure about whether to back a private equity fund, Caledonia Investments (CLDN) is an attractive proposition.’ Why? Because it is a multi-asset investment trust with a long-term buy and hold approach – currently 59% of assets are in private markets with the remaining 41% largely invested in listed companies. And the fund’s strategy has a track record of delivery. The IC highlights how the fund has outperformed broker Investec’s composite index (35% the FTSE All-Share; 65% the MSCI ACWI excluding the UK) – over the last five years, Caledonia has generated a +10.9% NAV return a year, compared to the benchmark’s +10.2%.

And then there’s the income. CLDN has grown its dividends for 57 consecutive years – the shares currently yield just under 2%. All of which leads the IC to write ‘Investors in search of a trust with a long-term approach, a unique strategy and growing dividends will find a lot to like in Caledonia’s portfolio’. That is ‘as long as they are happy not to shy away from private markets.’ And for those worried about investing in the private sector, the 35% discount to net assets at which CLDN’s shares currently trade at provides a useful margin of safety.

REITs have historically been fertile ground for active managers.

By Jason Yablon

Cohen & Steers

Index investing reached a milestone in early 2024, with assets in passive investment vehicles surpassing those in actively managed strategies for the first time. On the surface, the appeal of index investing is compelling: passive exchange-traded funds (ETFs) offer lower costs.

And, in the case of broad-based equity and bond categories, active managers frequently fail to consistently outperform their benchmarks. But cheaper is not always better, and not all markets are alike.

Real estate is one area of the equity market that lends itself to active management. REIT managers who commit time and resources to understanding current property fundamentals, shifting market trends and factors that may affect listed equity performance can potentially spot pricing inefficiencies and rapidly implement plans to generate excess returns.

We believe this advantage is reflected in the performance of the largest active REIT mutual funds relative to passive investment vehicles, despite active funds typically having greater expense ratios.

The modern REIT market offers a diverse opportunity set

When investors think of commercial real estate, they may envision office buildings, malls, shopping centres and apartments.

REIT ownership of these kinds of assets exists, of course. However, REITs have become increasingly specialized in new property types since 2000, shifting the REIT market’s composition away from traditional sectors.

For well-resourced managers, these new sectors provide a broad selection of REIT-owned assets for constructing portfolios, many of which have secular growth drivers.

These include data centres, where companies rent by the kilowatt to connect cloud servers; cell towers that lease space to wireless carriers for 5G networks; high-tech distribution hubs that facilitate next-day shipping on e-commerce orders; climate-controlled food storage facilities; biotech research labs; and senior living centres, just to name a few.

Capitalising on distinct sector characteristics

REIT sectors and companies tend to respond to market conditions very differently depending on factors such as lease durations, types of tenants, economic drivers and supply cycles. These differences have historically resulted in wide dispersion of sector returns in any given period.

More economically sensitive sectors with short lease terms, such as hotels and self-storage, can adjust rents relatively quickly to capture accelerating demand in a cyclical upswing.

By contrast, longer-lease sectors such as net lease and health care have more defensive cash flows that may be more resilient during economic downturns. In 2023, returns between the best and worst sectors were separated by 38 percentage points. In other years, the dispersion has been considerably greater.

We have observed that the difference in returns at the security level within each sector is often similar to the variance at the sector level. We believe this dispersion highlights the opportunities active managers have to enhance returns through both sector and stock selection.

Navigating secular growth opportunities and challenges

As economic cycles progress, property types are likely to have different fundamentals. For instance, the pandemic upended retail, hotels and offices, but benefited technology-related REITs amid acceleration in e-commerce and working from home.

And many sectors and cities continue to feel the lasting effects of the pandemic as flexible work-from-home policies have changed how and where people want to work and live, creating an uncertain outlook for offices.

Consequently, high-quality offices may continue to see healthy demand, while lower-quality assets may experience soft demand for years to come – a distinction not likely to be reflected in passive portfolios.

Active managers can also add value by capitalising on regional differences and trends. Many US residents are moving from dense, high-cost northern and coastal cities to lower-cost markets in the sunbelt.

In global portfolios, REIT managers may assess geographic regions to understand local property supply and demand fundamentals, economic trends, monetary policy and other factors that may affect the operating performance of different real estate companies, as well as the markets valuation relative to other regions.

Anticipating secular trends such as these is a key component of active management since they can present opportunities for active managers to capitalize on diverging fundamentals. For example, the divergence in industrial and office properties.

By contrast, passive portfolios are, by design, not able to allocate assets to capitalise on potential secular growth opportunities, nor can they sidestep sectors that may be facing long-term headwinds. Of course, there is no guarantee that active management can successfully navigate these trends.

REIT managers may also invest based on relative value, seeking to allocate portfolio assets based on merit rather than market capitalization, as is often the approach for many passive index funds.

Investing outside the benchmark – participating in special opportunities such as recapitalizations, private placements, initial public offerings (IPOs) or pre-IPO investments – is another way for active managers to add value.

These activities are not within the scope of passive index-tracking strategies – a notable disadvantage in recent years due to the inability of passive vehicles to get out of the way of the secular declines in retail and offices.

Jason Yablon is head of listed real estate at Cohen & Steers. The views expressed above should not be taken as investment advice.

If the portfolio achieves it’s target of 9k of dividend income this year, it’s more likely to than not but it’s still a target, the following could be achieved if compounding the earned dividends at 7%.

10 years £18k

20 years £33k

30 years £78k

It’s more than likely that Labour will raid your pension savings as Tony Blair and Gordon Brown did, although they kept it secret before they were elected, so u may have to add some years to the projection. One thing that u can learn from the projection is lifestyling is detrimental to your wealth. Of course u will have to allow for inflation. Using the 4% rule u would need to turn 100k into 2 million so good luck with that if that’s your plan.

The clear message is that Reits are cyclical and if u buy them at the wrong time u are likely to lose money. Where if u buy at the right time, u are likely to make money and u receive the dividends as u wait to be proved right or wrong.

If it sounds too good to be true, it’s definitely not true!

Anyone promising returns over 15% per year should be asked why they’re not counted among the greatest investors like Warren Buffett, Peter Lynch, or Ray Dalio.

To gain more, you often have to risk more, but sometimes your risk tolerance is zero (and you might not realize it).

Only invest in what you can explain to a 5-year-old or even a German Shepherd. In investing, complex thinking isn’t necessary.

Minimize costs – if you’re overpaying, someone else is cashing in.

When everyone agrees, everyone’s likely mistaken.

Investing is like snagging a pair of top-notch shoes – it’s a real deal when they’re on sale.

Those who can, do it – those who can’t just talk.

A great book is worth more than an expensive course.

Doing the right thing might make you feel foolish at times, but it eventually pays off.

Time is on your side: Use it as much as you can.

You’re not your neighbor or coworker; everyone charts their own path and outcomes.

Diversify – remember, you’re not Warren Buffett!

All extremes tend to balance out in the end.

Invest because you comprehend the business, not because you like the name or have a connection.

Evaluate results across years, not days.

Every invested dollar should have a purpose; never invest without understanding why.

Develop a clear strategy before committing your money.

Compounding is a marvel, but you have to leverage it for it to matter.

Speculation isn’t an investment – it’s the price paid by those who rush in without thinking.

I’m an income-hunter and this dividend stock with a 9% yield looks juicy Story by Jon Smith The Motley Fool

I’m sure there are many like me always on the prowl to find new ways to make income. Inflation might be moving lower, but that doesn’t mean the cost-of-living crisis has disappeared. In finding good dividend stocks with above-average yields, I can create a handy source of additional money.

A specialist manager One idea that caught my eye was CVC Income & Growth (LSE:CVCG). It’s an investment trust listed on the stock market. What this means is that CVC (a private equity and debt manager) runs the trust and invests the money. The value of the portfolio at any point is referred to as the net asset value (NAV) of the company. As a result, the share price should closely mirror the movements in the NAV, over time. As a dividend investor, these trusts can be a great source of income. The reason is that unlike a more traditional company, the focus of CVC is to purely generate income for shareholders while aiming to grow the value of the trust over time.

The firm has a good track record, with the current dividend yield returning 9%. It generates the funds by providing loans and other forms of credit to private companies. Given that some of these firms might struggle to get traditional lending from major banks, the interest rate charged can be quite high.

It focuses on Europe, so doesn’t try and get too fancy in targeting obscure investment opportunities in other far flung parts of the world.

Growth from here The 12% move higher in the stock over the past year impresses me. It currently matches the NAV, so I don’t see it as being overvalued. Looking forward, I’m optimistic about how the trust can continue to profit.

Unlike some trusts that focus just on stocks and have a heavy weighting to tech, this trust has a really diversified sector exposure. The largest sectors are healthcare and beverage & food, both with a 17% allocation. In fact, tech has just a 3% weighting at the moment. Based on my view on which sectors could outperform over the next year, this is a positive.

One risk that people could flag up is that trading in debt is a dangerous business. If CVC is involved with a firm that defaults on the debt, it’s seriously bad news. I accept this as a risk, but do counter it with the fact that it mostly deals in senior secured loans. This means there’s some form of collateral attached to the loans (eg a business asset). So in the case of a default, it’s not like there’s nothing left to claim against.

Putting things all together, I think this is a positive option for investors to consider, including for income. I’m looking at buying it when I have some free cash.

The post I’m an income-hunter and this dividend stock with a 9% yield looks juicy appeared first on The Motley Fool UK.