3i Infrastructure PLC ex-dividend payment date BlackRock Energy & Resources Income Trust PLC ex-dividend payment date BlackRock Frontiers Investment Trust PLC ex-dividend payment date Brunner Investment Trust PLC ex-dividend payment date CT UK Capital & Income Investment Trust PLC ex-dividend payment date Develop North PLC ex-dividend payment date Empiric Student Property PLC ex-dividend payment date Henderson High Income Trust PLC ex-dividend payment date Land Securities Group PLC ex-dividend payment date LondonMetric Property PLC ex-dividend payment date Pacific Assets Trust PLC ex-dividend payment date Schroder Real Estate Investment Trust Ltd ex-dividend payment date Scottish Mortgage Investment Trust PLC ex-dividend payment date SDCL Energy Efficiency Income Trust PLC ex-dividend payment date Spectra Systems Corp ex-dividend payment date US Solar Fund PLC ex-dividend payment date Worldwide Healthcare Trust PLC ex-dividend payment date

The dividend hero investment trusts yielding more than 5%

Writer, Laith Khalaf Thursday, March 14, 2024

AJ Bell

It’s not just cash savers and bond investors who are enjoying income yields above the rate of inflation, so are those buying investment trusts with exceptionally long records of increasing dividends.

Five UK Equity Income trusts are currently yielding above 5%, together providing an average yield of 5.8%. That compares to the best variable Cash ISA yielding 5.11% and the best fixed term cash ISA yielding 5.25%, according to Moneyfacts.

Of course, unlike cash, capital and income is not guaranteed when holding shares. However these trusts have increased their dividend each year for at least 23 years, through the dotcom crash, the global financial crisis, and the Covid pandemic. City of London investment trust has an unbroken dividend record stretching back to 1966, the year in which England won the football World Cup and number one records in the UK included songs from the Beatles, the Kinks and Elvis Presley.

There’s no guarantee of a rising income going forward, but the resilience shown by these dividend heroes over such a long time should provide investors with some comfort. Investment trusts can hold back income in the bad years to pay out dividends in the good years, a mechanism which has allowed some to continually raise their dividends for decades. This doesn’t increase the overall dividend yield produced by the underlying portfolio of shares, but it does offer investors a smoother ride, something which is especially prized by those relying on their investment portfolio to deliver a retirement income.

It’s not just cash savers and bond investors who are enjoying income yields above the rate of inflation, so are those buying investment trusts with exceptionally long records of increasing dividends.

Five UK Equity Income trusts are currently yielding above 5%, together providing an average yield of 5.8%. That compares to the best variable Cash ISA yielding 5.11% and the best fixed term cash ISA yielding 5.25%, according to Moneyfacts.

Of course, unlike cash, capital and income is not guaranteed when holding shares. However these trusts have increased their dividend each year for at least 23 years, through the dotcom crash, the global financial crisis, and the Covid pandemic. City of London investment trust has an unbroken dividend record stretching back to 1966, the year in which England won the football World Cup and number one records in the UK included songs from the Beatles, the Kinks and Elvis Presley.

There’s no guarantee of a rising income going forward, but the resilience shown by these dividend heroes over such a long time should provide investors with some comfort. Investment trusts can hold back income in the bad years to pay out dividends in the good years, a mechanism which has allowed some to continually raise their dividends for decades. This doesn’t increase the overall dividend yield produced by the underlying portfolio of shares, but it does offer investors a smoother ride, something which is especially prized by those relying on their investment portfolio to deliver a retirement income.

Yield 5-year annual dividend growth Discount Years of dividend increase

City of London 5.1% 2.6% (2.1%) 57 JP Morgan Claverhouse 5.2% 4.6% (5.4%) 51 Merchants Trust 5.2% 2.2% (1.2%) 41 Schroder Income Growth 5.2% 3.2% (10.8%) 28 Abrdn Equity Income 8.4% 3.5% (8.3%) 23

Average 5.8% 3.2% (5.5%) 40 Source: Association of Investment Companies, data as at 8 March 2024

An 8% yield tomorrow from investing today

Based on the historic dividend growth achieved by these trusts, after 10 years they could be yielding 8% a year on an investment made today (based on a 5.8% current yield rising by 3.2% per annum). This also makes them an attractive segue for investors approaching retirement and looking to beef up their future income. Until the income taps are turned on investors can reinvest dividends, further bolstering their eventual income when they come to draw on it.

These are of course not the only investment trusts available to investors, and others may offer a more appealing combination of income and growth prospects to some investors. However, these trusts do showcase the high income stream that can be generated by investing in UK stocks, alongside the prospects for a growing income stream too.

The prospect for both dividend and capital growth are key attractions provided by the stock market to income investors. This is in marked contrast to cash where over time the interest generated is dictated by interest rate changes in both directions, and where there is no long run upward trend that can be relied on.

In the near term it looks like cash rates are likely to fall, with the market pricing in three interest rate cuts from the Bank of England this year. Further falls are then anticipated until the base rate reaches a stable level of around 3.25% in two years’ time (source: OBR). So while headline cash rates look appealing right now, those who are saving money for the longer term face a declining return picture in coming years.

The ISA protection for income stocks

As the tax burden rises as a result of frozen income tax thresholds, so does the value of holding income-producing assets in an ISA. The dividend allowance is being cut to £500 from 6 April, and 2.7 million people are forecast by the OBR to be brought into paying higher rate tax over the next five years, with a further 600,000 more taxpayers tipped into the additional rate tax bracket.

The chancellor’s recent National Insurance cuts don’t alter this picture, and nor do they reduce the tax payable on dividends. A higher rate taxpayer investing £20,000 in a portfolio paying 5.8% with dividend growth of 3.2% per annum would save £2,842 over 10 years by using an ISA.

A higher rate taxpaying couple using their ISA allowance at the end of this tax year and the beginning of next, so £80,000 in total, would save £14,744.

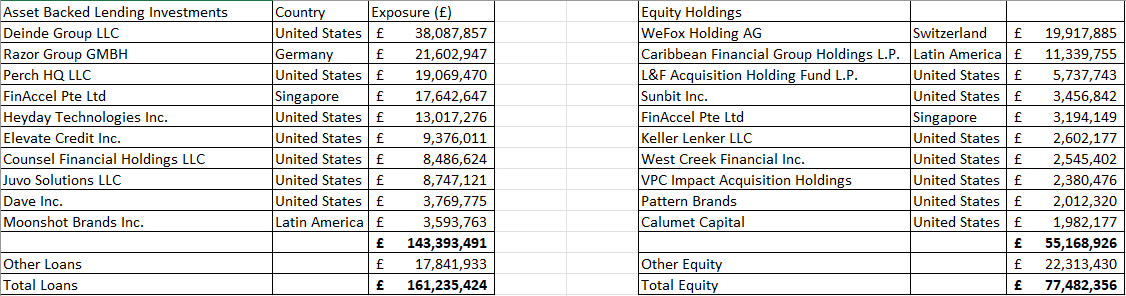

VSL posted a positive +0.64% return in March (positive both for loan revenue and for equity) but the share price has fallen yet further. VSL holds high interest secured loans and equity positions in mainly US Fintech/eCommerce companies. It’s fallen to the point where the entire Fintech/Ecommerce equity holdings could be wiped out and worth zero and there’s still 25% upside from the loans. Loans where VSL is Senior and Equity where VSL has preference.

A 44% discount where dividends and capital returns over the next 12 months alone should be a further 8p+16p = 24p.

On a simple returns basis that leaves you owed 16.5p a share, while the remaining NAV could be around 60p a share net assets…. a 72.5% discount to NAV.

With further capital, dividend returns, and equity holdings which might surprise to the upside, I reckon you could get to a <100% discount to NAV in due course.

The Oak Bloke

Disclaimer:

This is not advice

££££££££££

It’s your hard earned, so only u can u can decide where to invest it, other people’s views can only inform so always best to DYOR before u come to any conclusion.

SMT is a Dividend Hero Trust but only pays a small dividend 0.47% so not a candidate for the Snowball.

It’s been a great trading stock but only for those with a suitable stop gain/loss strategy. There is lots of online information about SMT as someone, somewhere often gives it a buy recommendation but as always best to DYOR.

MoneyWeek share tips 2024 guide pulls together some of the best UK stocks from some of the top share tipsters around.

As well as the UK financial pages, we look at publications across the pond for investors who want to diversify their holdings internationally.

From investing in UK equities, European stocks, to finding the best performing stocks in the S&P 500 – here are our top share tips of the week.

This list is updated weekly on a Friday.

Share tips 2024: top picks of the week FOUR TO BUY

IAG (LON: IAG) The Telegraph British Airways’ parent company IAG’s strong financial performance, decreasing debt, and “dirt-cheap” valuation make it a compelling long-term investment. The positive first-quarter results, notably increased operating profits and passenger numbers, reflect improving conditions in the overall industry. With global demand from passengers on the rise and interest-rate cuts looming, IAG’s solid fundamentals and growth potential suggest significant progress. “Irrespective of any positive or negative personal feelings towards British Airways, IAG remains a worthwhile long-term investment.” 174p

Impax Environmental Markets (LON: IEM) The Mail on Sunday Impax invests in environmentally focused small and medium-sized firms, from hazardous waste treatment in the US to reusable pallets in Australia. It “combines green credentials with hard-nosed commercial nous”. It should benefit from increasing support for green initiatives from governments, investors, and consumers. Notable investments include DSM-Firmenich, which has created a digestion aid for cattle that reduces methane emissions. The shares are a “bargain”. 396p

Moneysupermarket (LON: MONY) The Sunday Times Moneysupermarket, which receives a fixed fee when a product is sold, has seen a decline in sales as car insurance premiums have stabilised. But slowing revenue streams are not new; the firm has been battered by volatile household energy bills, and the “gloom” seems priced in. The stock is on a low earnings multiple with a 6% dividend yield. The group has seen growth in its SuperSaveClub loyalty scheme and is broadening its market share through acquisitions and offering price-comparison services to third-party brands. It’s “good value.” 222p

CVS Group (LON: CVSG) Shares Veterinary services company CVS Group is being investigated by the Competition and Markets Authority for potential unfair practices in the pet care market. The regulator is concerned about high medicine prices and thinks large companies are hampering competition. Despite this, CVS’s shares rose following the announcement, suggesting that the market has priced in “most, if not all, the bad news”. With shares trading far below their 2021 peak and a low price/earnings (p/e) ratio, CVS presents an attractive opportunity for long-term investors. It aims to double earnings over the next five years through organic growth and acquisitions, particularly in Australia and the UK. CVS has a “strong record of growth” and is “conservatively financed.” 1,154p

It’s important to remember that dividends are a method of returning excess capital to shareholders. But should a business land itself in some hot water, excess capital can be hard to find. That’s why most companies tend to cut dividends when economic conditions turn sour, as we’ve recently seen.

Given this risk, it’s no surprise that Dividend Aristocrats are so popular.

These are companies that have not only maintained shareholder payouts for decades but also consistently increased them. As such, many consider them to be some of the safest income stocks money can buy. But are they actually a good investment?

The problem with Dividend Aristocrats

The London Stock Exchange is home to a wide collection of income-generating businesses with a multi-decade track record of rewarding shareholders. But looking a the FTSE 100, five companies with some of the longest streaks include British American Tobacco (LSE:BATS), Bunzl, Croda International, DCC, and Scottish Mortgage Investment Trust.

Now we’re pretty much back at record highs in terms

Each firm has been hiking dividends for more than 25 years. DCC is even celebrating its 30th year of dividend hikes in 2024. Needless to say, consistently delivering a higher payout isn’t exactly easy. And that’s where the problem with Aristocrats starts to emerge.

To keep their status, all these firms have to do is increase their payouts. The amount that dividends increase is irrelevant. And looking at the average growth rate of these firms, dividends have only increased by around 4-5% a year. After factoring in inflation, these firms aren’t delivering much in terms of wealth creation.

A question of safety

Payouts may be on the rise. But since 2017, the share price has more than halved. The company’s facing an increasingly tough regulatory environment surrounding tobacco-based products worldwide. As such, it’s already begun to pivot into alternative products. But the jury’s still out on whether they’ll be able to fully replace current tobacco sales at the same profit margin.

While the early results are encouraging, if the firm cannot adapt fast enough, its multi-decade streak could soon be coming to an end.

The bottom line

Just because Dividend Aristocrats have a reputation of being safe, that doesn’t guarantee them to be sensible investments. Like every stock, investors need to spend time carefully analysing a firm’s current financial position as well as future prospects. Otherwise, it’s easy to fall into an income trap.

The Board of Downing Renewables & Infrastructure Trust plc (the “Company” or “DORE“) is pleased to announce the Company’s unaudited Net Asset Value (“NAV“) as at 31 March 2024.

Net Asset Value as at 31 March 2024

The Company’s unaudited NAV was £212.3 million or 119.2 pence per share (“pps“) as at 31 March 2024. This is an increase of 1.3% from the Company’s NAV per share as at 31 December 2023 (£212.1 million or 117.7pps) following payment of the £2.4m (1.3pps) quarterly dividend.

The movement in NAV during the quarter was attributable to several factors:

– Portfolio performance (+£3.2m, +1.8pps);

– Update to the long-term power price forecasts (-£5.0m, -2.8pps);

– FX movement (+£4.0m, +2.2pps);

– Life extension project (+£3.2m, +1.8pps)

– Share buybacks (-£1.9m, +0.4pps)

– Dividend (-£2.4m, -1.3pps); and

– Other movements (-£0.9m, -0.5pps).

As at 31 March 2024 the Company’s GAV was £351.0 million (31 December 2023: £352.2 million).

As announced on 22 May 2024, the dividend in respect of the period from 1 January 2024 to 31 March 2024 of 1.45pps has been declared and will be paid to shareholders on the register on 31 May 2024 on or around 28 June 2024. The target annual dividend for 2024 of 5.8pps represents a 7.85% increase from the 2023 dividend.

Further to the “Portfolio Sale and Lease Transfer” announcement made on 3 May 2024, the Board of Triple Point Social Housing REIT plc and Triple Point Investment Management LLP (“Triple Point” or the “InvestmentManager“) today provide an update on rent collection, a potential portfolio sale and progress made with tenants, My Space and Parasol.

Increasing rent collection and strong rental growth continues

The Company’s portfolio delivered resilient performance in the first three months of the year to 31 March 2024. Rent collection increased to 93.3% (Dec 23: 90.2%), and 25 out of the Company’s 27 lessees continued to demonstrate no material rental arrears.

Increased rent collection has been complemented by continued rental growth. As at 30 April, 61.6% of the Group’s leases had put through their 2024 annual rent increase at a weighted average uplift of 6.1%.

Update on portfolio sale

The Company has agreed heads of terms in relation to a portfolio sale with an aggregate value in excess of £20 million. The portfolio sale is representative of the Company’s wider portfolio and contains a range of both new build and adapted properties as well as self-contained and shared homes. EPC ratings of the properties range from B to D. We expect the portfolio sale to complete prior to the publication of the Company’s interim results for the sixth month period to 30 June 2024, which will be published in September.

Update on Parasol and My Space

Parasol

The Investment Manager has commenced a process of transferring all of the Group’s properties currently leased to Parasol to Westmoreland, representing 9.6% of rent roll. The transfer process remains on track to complete before the reporting of the Company’s interim results in September.

Following completion of the lease transfer process, an update on forward looking rent collection will be provided and, in the interim, Parasol continues to pay rent in accordance with the existing creditor’s agreement.

My Space

The Investment Manager continues to engage with My Space’s senior management team on their turn-around plan. The Company notes that four new independent Board members have been put in place with housing, audit, compliance and procurement expertise and that rent collection is expected to increase over the course of the year. If an acceptable long-term position cannot be reached with My Space, which represents 8.1% of rent roll, then, as with Parasol, the Investment Manager will move leases to one or more alternative Registered Providers.

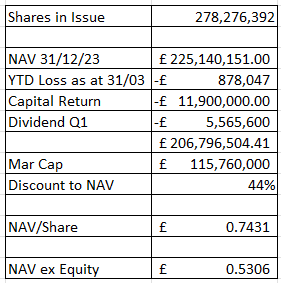

VPC is in a period of wind down. Its dividend on a “headline” basis is one of the strongest on offer at 16.84% per annum but is that good value for money? Is it “real” and sustainable? And should existing shareholders hold on, average down, or exit?

These have a repayment schedule which is shown below.

In the next 12 months over 40% of the loans will settle. The chart below is net of debt (£24m) plus about £45m of paydowns up to Q2 25. Obviously the 16.84% dividend will reduce but it’s likely to continue for another 4 periods at 2p a quarter – so an 8p a share return. After that (Q3 2025) it probably drops to 1p a quarter for another year and after Q3 2026 perhaps drops to 0.5p a quarter until the end of 2028.

If that’s the case then that’s 16p of dividends over 4 years. In 12 months time alone deducting 8p from today’s 48p buy price is equivalent to buying at a discount to NAV of 45.8%

Remember too the 73.82p estimated NAV is net of a 2p per share dividend in Q1 as well as a 4.26p capital return of B shares in April 2024. In other words we are on an 80.08p NAV as at 31/12/23 less distributions in 2024. Less a 1% YTD loss.